Corporate and Financial Accounting Module Report: Consolidation

VerifiedAdded on 2023/01/16

|14

|3511

|92

Report

AI Summary

This report provides a comprehensive overview of corporate and financial accounting, focusing on the key differences between consolidation and equity accounting methods. It analyzes the application of AASB standards, including AASB 3, AASB 10, AASB 127, and AASB 128, to business combinations. The report delves into the treatment of intra-group transactions and their impact on consolidated financial statements, including the calculation of non-controlling interests (NCI). Furthermore, it examines the necessary adjustments to ensure the accurate presentation of consolidated financial statements and discusses the related disclosure requirements in annual reports. Through detailed examples, the report illustrates the practical implications of these accounting principles, offering valuable insights into financial reporting practices.

Corporate and financial accounting

Module Number-

Module Number-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

A reporting entity’s accounting for the interest held in other legal entity depends upon

the ownership share held by it. Ownership of 50% or more results in control, while ownership

given between 20% to 50% results in exercise of significant influence. The accounting when

the reporting entity holds control is done according to the acquisition or purchase method as

specified by the AASB 3, Business Combinations. In this case consolidated financial

statements as required by AASB 10, and AASB 127 have to be followed. When, there is

only a significant influence, the provisions of AASB 128, Investments in Associates and Joint

Ventures are followed. Every disclosure as provided for stand-alone financial statements are

to be provided for consolidated financial statements in the annual report by the reporting

entity, including separate disclosure for Non-controlling interests.

A reporting entity’s accounting for the interest held in other legal entity depends upon

the ownership share held by it. Ownership of 50% or more results in control, while ownership

given between 20% to 50% results in exercise of significant influence. The accounting when

the reporting entity holds control is done according to the acquisition or purchase method as

specified by the AASB 3, Business Combinations. In this case consolidated financial

statements as required by AASB 10, and AASB 127 have to be followed. When, there is

only a significant influence, the provisions of AASB 128, Investments in Associates and Joint

Ventures are followed. Every disclosure as provided for stand-alone financial statements are

to be provided for consolidated financial statements in the annual report by the reporting

entity, including separate disclosure for Non-controlling interests.

Table of Contents

Executive summary...............................................................................................................................1

Introduction...........................................................................................................................................2

Part A Response....................................................................................................................................2

Part B Response.....................................................................................................................................5

Treatment of intra group transactions................................................................................................5

Effect upon the non-controlling Interest (NCI) calculation in the subsidiary’s annual profit.............5

Part C response......................................................................................................................................6

Changes required to ensure that the consolidated financial statements are correctly stated...............7

Effect on the disclosure requirements in the annual report................................................................7

Conclusion.............................................................................................................................................8

References.............................................................................................................................................9

Executive summary...............................................................................................................................1

Introduction...........................................................................................................................................2

Part A Response....................................................................................................................................2

Part B Response.....................................................................................................................................5

Treatment of intra group transactions................................................................................................5

Effect upon the non-controlling Interest (NCI) calculation in the subsidiary’s annual profit.............5

Part C response......................................................................................................................................6

Changes required to ensure that the consolidated financial statements are correctly stated...............7

Effect on the disclosure requirements in the annual report................................................................7

Conclusion.............................................................................................................................................8

References.............................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The current report emphasises the importance attached with the business

combinations attached to an entity. The difference existent between the different methods of

business combinations being equity accounting and Consolidation accounting is being

discussed with analysis of key demarcating areas between the both. Analysis of AASB 3:

Business Combinations, AASB 128 Investments in Associates and Joint Ventures and AASB

10 Consolidated Financial Statements, AASB 127 Consolidated and Separate Financial

Statements and AASB 101 Presentation of Financial Statements is undertaken. The treatment

of intra group transactions is explained considering the examples from the case study

presented. Finally the effects of disclosure of Non-Comprehensive Income in the

consolidated financial statements are considered. There are several accounting standards

which helps organization to strengthen the reporting frameworks and make the proper

transparency in the recorded items given in the books of account. Nonetheless, IAS 136 helps

in finding out the impairment loss which company would have in its assets by using the

impairment testing methods. This will help in keeping the true and fair view of the recorded

assets in the books of accounts (Auditing and Assurance Standards Board, 2015b)

Part A Response

It is analysed that Consolidation Accounting and Equity Accounting both are different than

each other and used by company to strengthen the recording frameworks and helps in setting

up harmonization in accounting and reporting frameworks. The key differences in

methodology between Consolidation Accounting and Equity Accounting are depicted as

follows (Auditing and Assurance Standards Board, 2015b)

Consolidation Accounting Equity Accounting

This method is also known as Acquisition or

purchase method. As per AASB 3 Business

Combinations the consolidation method can

be applied when the reporting organisation

have a controlling financial interest over the

operations of the legal entity (i.e. in which

As per AASB 128 Investments in Associates

and Joint Ventures this method is applied

when the reporting organisation is entitled to

exercise a significant influence over the

business of legal entity, but there is no

entitlement to exercise full control (Dagwell,

The current report emphasises the importance attached with the business

combinations attached to an entity. The difference existent between the different methods of

business combinations being equity accounting and Consolidation accounting is being

discussed with analysis of key demarcating areas between the both. Analysis of AASB 3:

Business Combinations, AASB 128 Investments in Associates and Joint Ventures and AASB

10 Consolidated Financial Statements, AASB 127 Consolidated and Separate Financial

Statements and AASB 101 Presentation of Financial Statements is undertaken. The treatment

of intra group transactions is explained considering the examples from the case study

presented. Finally the effects of disclosure of Non-Comprehensive Income in the

consolidated financial statements are considered. There are several accounting standards

which helps organization to strengthen the reporting frameworks and make the proper

transparency in the recorded items given in the books of account. Nonetheless, IAS 136 helps

in finding out the impairment loss which company would have in its assets by using the

impairment testing methods. This will help in keeping the true and fair view of the recorded

assets in the books of accounts (Auditing and Assurance Standards Board, 2015b)

Part A Response

It is analysed that Consolidation Accounting and Equity Accounting both are different than

each other and used by company to strengthen the recording frameworks and helps in setting

up harmonization in accounting and reporting frameworks. The key differences in

methodology between Consolidation Accounting and Equity Accounting are depicted as

follows (Auditing and Assurance Standards Board, 2015b)

Consolidation Accounting Equity Accounting

This method is also known as Acquisition or

purchase method. As per AASB 3 Business

Combinations the consolidation method can

be applied when the reporting organisation

have a controlling financial interest over the

operations of the legal entity (i.e. in which

As per AASB 128 Investments in Associates

and Joint Ventures this method is applied

when the reporting organisation is entitled to

exercise a significant influence over the

business of legal entity, but there is no

entitlement to exercise full control (Dagwell,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

investments are made). Wines, and Lambert, 2015).

Control is exercised when the ownership in

the legal entity by the reporting entity

exceeds 50% or is equal to 50% (Su, and

Wells, 2018).

Significant influence is exercised by the

reporting entity when ownership in the legal

entity falls in between 20 to 50%.

In consolidation accounting method a

combination has to be done of the financial

statements i.e. the statement of financial

position and statement of financial

performance of both the reporting and legal

entity. a set of consolidated financial

statements is presented to the users (Bugeja,

and Loyeung, 2017).

In equity method, no consolidation of the

financials of the reporting entity and legal

entity takes place. The reporting entity

prepares stand-alone financial statements as

always prepared and presented. Only the

accounting for the investment made is

represented on the asset side of the statement

of financial performance and the income

received upon the investment is accounted as

other incomes are accounted in the income

statement.

Due to the applicability of AASB 10,

Business Combinations, the intra group

transactions effected between the reporting

entity and the legal entity, i.e. between the

parent and the subsidiary shall be completely

eliminated while preparation of the

consolidated set of financial statements.

e.g.: profit arising to subsidiary on inventory

sale to parent, shall be eliminated while

consolidating the income statement and

Until and unless the legal entity is a

subsidiary as per AASB 3, no intra group

transactions are required to be eliminated.

This is because the provisions of AASB 10 in

relation to consolidation of the financial

statements of reporting and legal entity do

not apply when equity method prevails, i.e.

where only significant influence is exercised.

Control is exercised when the ownership in

the legal entity by the reporting entity

exceeds 50% or is equal to 50% (Su, and

Wells, 2018).

Significant influence is exercised by the

reporting entity when ownership in the legal

entity falls in between 20 to 50%.

In consolidation accounting method a

combination has to be done of the financial

statements i.e. the statement of financial

position and statement of financial

performance of both the reporting and legal

entity. a set of consolidated financial

statements is presented to the users (Bugeja,

and Loyeung, 2017).

In equity method, no consolidation of the

financials of the reporting entity and legal

entity takes place. The reporting entity

prepares stand-alone financial statements as

always prepared and presented. Only the

accounting for the investment made is

represented on the asset side of the statement

of financial performance and the income

received upon the investment is accounted as

other incomes are accounted in the income

statement.

Due to the applicability of AASB 10,

Business Combinations, the intra group

transactions effected between the reporting

entity and the legal entity, i.e. between the

parent and the subsidiary shall be completely

eliminated while preparation of the

consolidated set of financial statements.

e.g.: profit arising to subsidiary on inventory

sale to parent, shall be eliminated while

consolidating the income statement and

Until and unless the legal entity is a

subsidiary as per AASB 3, no intra group

transactions are required to be eliminated.

This is because the provisions of AASB 10 in

relation to consolidation of the financial

statements of reporting and legal entity do

not apply when equity method prevails, i.e.

where only significant influence is exercised.

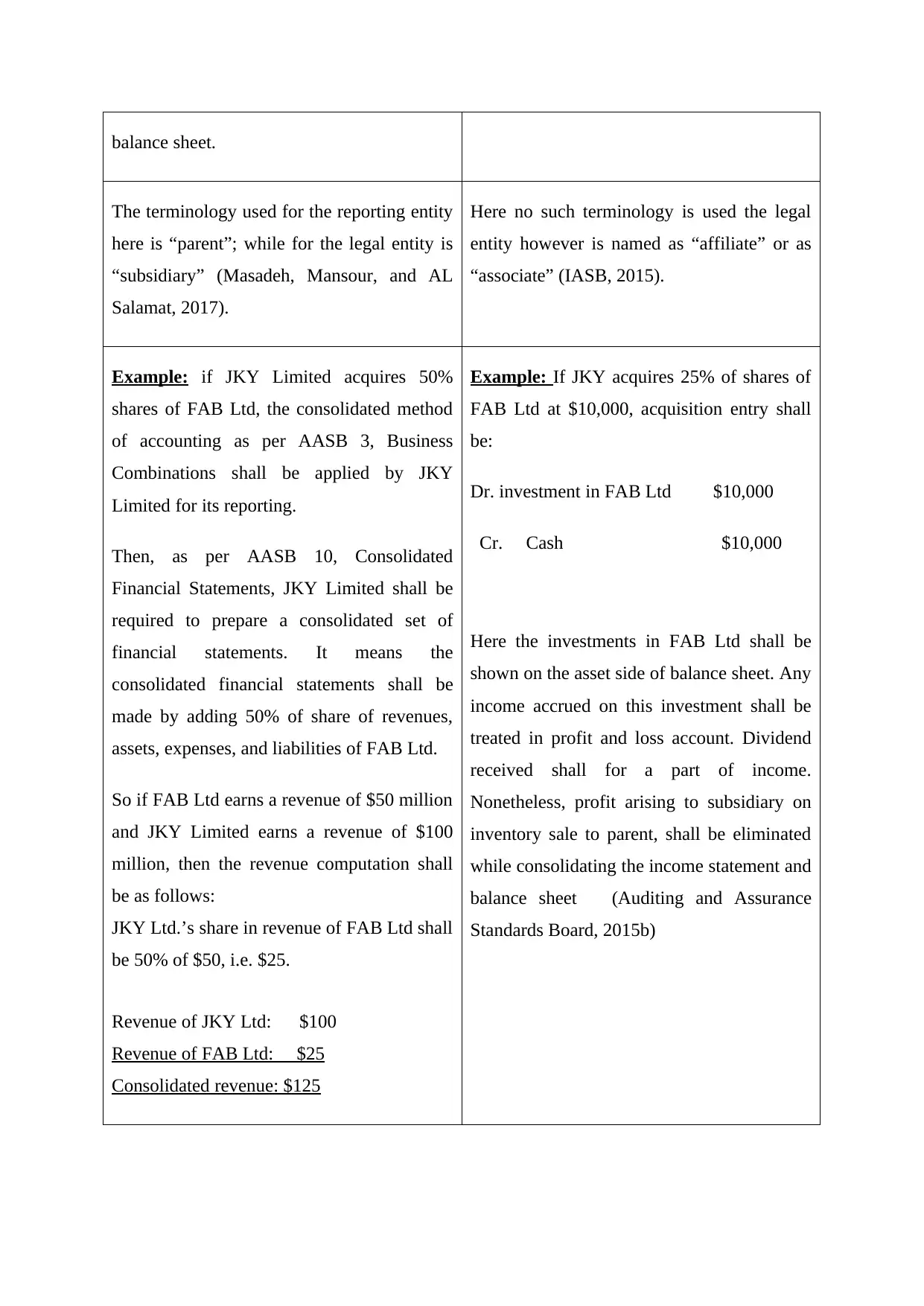

balance sheet.

The terminology used for the reporting entity

here is “parent”; while for the legal entity is

“subsidiary” (Masadeh, Mansour, and AL

Salamat, 2017).

Here no such terminology is used the legal

entity however is named as “affiliate” or as

“associate” (IASB, 2015).

Example: if JKY Limited acquires 50%

shares of FAB Ltd, the consolidated method

of accounting as per AASB 3, Business

Combinations shall be applied by JKY

Limited for its reporting.

Then, as per AASB 10, Consolidated

Financial Statements, JKY Limited shall be

required to prepare a consolidated set of

financial statements. It means the

consolidated financial statements shall be

made by adding 50% of share of revenues,

assets, expenses, and liabilities of FAB Ltd.

So if FAB Ltd earns a revenue of $50 million

and JKY Limited earns a revenue of $100

million, then the revenue computation shall

be as follows:

JKY Ltd.’s share in revenue of FAB Ltd shall

be 50% of $50, i.e. $25.

Revenue of JKY Ltd: $100

Revenue of FAB Ltd: $25

Consolidated revenue: $125

Example: If JKY acquires 25% of shares of

FAB Ltd at $10,000, acquisition entry shall

be:

Dr. investment in FAB Ltd $10,000

Cr. Cash $10,000

Here the investments in FAB Ltd shall be

shown on the asset side of balance sheet. Any

income accrued on this investment shall be

treated in profit and loss account. Dividend

received shall for a part of income.

Nonetheless, profit arising to subsidiary on

inventory sale to parent, shall be eliminated

while consolidating the income statement and

balance sheet (Auditing and Assurance

Standards Board, 2015b)

The terminology used for the reporting entity

here is “parent”; while for the legal entity is

“subsidiary” (Masadeh, Mansour, and AL

Salamat, 2017).

Here no such terminology is used the legal

entity however is named as “affiliate” or as

“associate” (IASB, 2015).

Example: if JKY Limited acquires 50%

shares of FAB Ltd, the consolidated method

of accounting as per AASB 3, Business

Combinations shall be applied by JKY

Limited for its reporting.

Then, as per AASB 10, Consolidated

Financial Statements, JKY Limited shall be

required to prepare a consolidated set of

financial statements. It means the

consolidated financial statements shall be

made by adding 50% of share of revenues,

assets, expenses, and liabilities of FAB Ltd.

So if FAB Ltd earns a revenue of $50 million

and JKY Limited earns a revenue of $100

million, then the revenue computation shall

be as follows:

JKY Ltd.’s share in revenue of FAB Ltd shall

be 50% of $50, i.e. $25.

Revenue of JKY Ltd: $100

Revenue of FAB Ltd: $25

Consolidated revenue: $125

Example: If JKY acquires 25% of shares of

FAB Ltd at $10,000, acquisition entry shall

be:

Dr. investment in FAB Ltd $10,000

Cr. Cash $10,000

Here the investments in FAB Ltd shall be

shown on the asset side of balance sheet. Any

income accrued on this investment shall be

treated in profit and loss account. Dividend

received shall for a part of income.

Nonetheless, profit arising to subsidiary on

inventory sale to parent, shall be eliminated

while consolidating the income statement and

balance sheet (Auditing and Assurance

Standards Board, 2015b)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part B Response

The discussion for the treatment of intragroup transactions arise only when an entity

controls 50% or more of another entity and the method followed is consolidation or

acquisition method as per the AASB 3, Business Combinations. In this case, there comes

requirement at the end of reporting period to formulate consolidated financial statements by

following the provisions of AASB 127 Consolidated and Separate Financial Statements and

AASB 10 Consolidated Financial Statements. All the companies having the consolidated

balance sheet are required to file the same to the reporting authority disclosing the balance

sheet of other subsidiary companies. If any of the party found to be in relation to the other

party then it is required to disclose all the details to other party and stakeholders of the

company before entering into the contract or business transactions (Auditing and Assurance

Standards Board, 2015b)

Treatment of intra group transactions

While preparation of consolidated financial statements, the assets, liabilities, expenses and

incomes of both the parent entity and subsidiary entity are not just unambiguously added, but

the formation of the consolidated financial statements happens considering both the entities

as a single economic entity.

Paragraph 20 of AASB 127 mentions elimination of the intragroup income, expenses,

transactions and balances in full. Along with these transactions it is clearly specified by the

Paragraph 21 of AASB 127 to completely eliminate the profits and losses which result from

intragroup transactions and are recognised as a part of assets should also be completely

eliminated. Also the provision lays out the applicability of AASB 12 Income Tax upon the

temporary differences which resulted from the profits and losses that are eliminated. AASB

10 also sets same provision as an accounting requirement for consolidation procedure (Haier,

Molchanov, and Schmutz, 2016).

Effect upon the non-controlling Interest (NCI) calculation in the subsidiary’s annual

profit

The non-controlling interest is represented by all the ownership interest in the subsidiary of

the reporting entity other than that of the reporting entity. The subsidiary’s annual profit is

divided into two parts, one is the share of parent i.e. reporting entity and the other of non-

The discussion for the treatment of intragroup transactions arise only when an entity

controls 50% or more of another entity and the method followed is consolidation or

acquisition method as per the AASB 3, Business Combinations. In this case, there comes

requirement at the end of reporting period to formulate consolidated financial statements by

following the provisions of AASB 127 Consolidated and Separate Financial Statements and

AASB 10 Consolidated Financial Statements. All the companies having the consolidated

balance sheet are required to file the same to the reporting authority disclosing the balance

sheet of other subsidiary companies. If any of the party found to be in relation to the other

party then it is required to disclose all the details to other party and stakeholders of the

company before entering into the contract or business transactions (Auditing and Assurance

Standards Board, 2015b)

Treatment of intra group transactions

While preparation of consolidated financial statements, the assets, liabilities, expenses and

incomes of both the parent entity and subsidiary entity are not just unambiguously added, but

the formation of the consolidated financial statements happens considering both the entities

as a single economic entity.

Paragraph 20 of AASB 127 mentions elimination of the intragroup income, expenses,

transactions and balances in full. Along with these transactions it is clearly specified by the

Paragraph 21 of AASB 127 to completely eliminate the profits and losses which result from

intragroup transactions and are recognised as a part of assets should also be completely

eliminated. Also the provision lays out the applicability of AASB 12 Income Tax upon the

temporary differences which resulted from the profits and losses that are eliminated. AASB

10 also sets same provision as an accounting requirement for consolidation procedure (Haier,

Molchanov, and Schmutz, 2016).

Effect upon the non-controlling Interest (NCI) calculation in the subsidiary’s annual

profit

The non-controlling interest is represented by all the ownership interest in the subsidiary of

the reporting entity other than that of the reporting entity. The subsidiary’s annual profit is

divided into two parts, one is the share of parent i.e. reporting entity and the other of non-

controlling interest. Due to elimination of unrealised profits affected as a result of intra group

transactions where in the subsidiary sells to parent, the accounting profit of the subsidiary

falls. Vice-versa happens in elimination of unrealised losses. However, the accounting profit

of subsidiary is affected when the subsidiary is the seller and had made some profit or loss on

sale. This accounting profit if changes due to unrealised profits and losses being eliminated

due to elimination of intra group transactions hence effects the computation of non-

controlling interest (Lee, P.J., Tavallali, R. and Lee, 2017).

The key points discussed in the relation of intragroup transaction elimination and its effect

upon the accounting profit of subsidiary which is attributable to the non-controlling interest

can be studied with the help of the following example (Auditing and Assurance Standards

Board, (2015b)

Suppose the ownership of JKY Ltd in its partially owned subsidiary is of 70%. The

professional service provisioning and inventory sale is made to JKY Ltd at $5000 and

$6000 respectively. The cost to subsidiary for both had been $4000 and $5000

respectively. Inventory is still lying unsold with parent. the accounting profit reported

by subsidiary had been $20000 for the year which has to be divided in the ratio of 70%

and 30% between parent and non-controlling interest. The treatment shall be as

follows:

Firstly, as per AASB 127 and AASB 10, the effect of intragroup transactions has to be

eliminated. Resultant, the preparation of consolidated financial statements shall require the

consolidated inventory amount to be reduced by the unrealised profit amount. Unrealised

profit in case of inventory shall be $1000 ($6000-$5000). Accounting profit of $20,000 shall

also fall by same amount.

Secondly, the unrealised profit of $1,000 ($5000-$4000) on provision of professional service

shall also reduce the accounting profit.

Hence, the accounting profit shall be $18000, being $12,600 attributed to parent and $5400

attributed to non-controlling interest as compared to earlier attributable amount of $6000 to

the non-controlling interest. Due to elimination of intra group upstream transactions, the

accounting profit attributable to non-controlling interest has fallen.

transactions where in the subsidiary sells to parent, the accounting profit of the subsidiary

falls. Vice-versa happens in elimination of unrealised losses. However, the accounting profit

of subsidiary is affected when the subsidiary is the seller and had made some profit or loss on

sale. This accounting profit if changes due to unrealised profits and losses being eliminated

due to elimination of intra group transactions hence effects the computation of non-

controlling interest (Lee, P.J., Tavallali, R. and Lee, 2017).

The key points discussed in the relation of intragroup transaction elimination and its effect

upon the accounting profit of subsidiary which is attributable to the non-controlling interest

can be studied with the help of the following example (Auditing and Assurance Standards

Board, (2015b)

Suppose the ownership of JKY Ltd in its partially owned subsidiary is of 70%. The

professional service provisioning and inventory sale is made to JKY Ltd at $5000 and

$6000 respectively. The cost to subsidiary for both had been $4000 and $5000

respectively. Inventory is still lying unsold with parent. the accounting profit reported

by subsidiary had been $20000 for the year which has to be divided in the ratio of 70%

and 30% between parent and non-controlling interest. The treatment shall be as

follows:

Firstly, as per AASB 127 and AASB 10, the effect of intragroup transactions has to be

eliminated. Resultant, the preparation of consolidated financial statements shall require the

consolidated inventory amount to be reduced by the unrealised profit amount. Unrealised

profit in case of inventory shall be $1000 ($6000-$5000). Accounting profit of $20,000 shall

also fall by same amount.

Secondly, the unrealised profit of $1,000 ($5000-$4000) on provision of professional service

shall also reduce the accounting profit.

Hence, the accounting profit shall be $18000, being $12,600 attributed to parent and $5400

attributed to non-controlling interest as compared to earlier attributable amount of $6000 to

the non-controlling interest. Due to elimination of intra group upstream transactions, the

accounting profit attributable to non-controlling interest has fallen.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part C response

AASB 127 lays the requirement to separately report non-controlling interest in the

consolidated financial statements. This non-controlling interest is also allocated the Other

Comprehensive Profit. The subsidiary of JKY Ltd is reported to be recording assets at

historic cost (Bodle, Brimble, Weaven, Frazer, and Blue, (2018).

Changes required to ensure that the consolidated financial statements are correctly

stated

AASB 127 requires adoption of uniform accounting policies by all the members whose

financials are consolidated as a group by the parent or reporting entity. The consolidated

financial statements shall be prepared by the group only by incorporating accounting policies

that are uniform. in case the accounting policies followed by any member differ from the

group, an adjustment is required in its policies to bring them in conformity with the

accounting policies of the group. By using the uniform accounting policies, company could

easily set up proper harmonization in its recording frameworks and helps in strengthen the

recording frameworks as per the AASB 127. Nonetheless internal audit program will also be

set up to assess the changes made in the accounting frameworks of the company (Brunelli,

2018).

Here, in this case if JKY Ltd is using the fair value method to value assets and record assets,

then the financials of the subsidiary shall be adjusted accordingly. The assets of subsidiary

which have till now been recorded at cost shall now have to be recorded at fair value. These

are the changes which are required to ensure that the consolidated financial statements are

correctly stated (Yang, and Aquilino, 2017).

Effect on the disclosure requirements in the annual report

AASB 127 requires attribution of other comprehensive income to the non-controlling interest

even if the balance of NCI turns deficit after that. Other comprehensive income shall also be

separately shown attributable to the non-controlling interest in the financial statements of the

parent as per the requirements of AASB 101, Presentation of Financial Statements. The

disclosures required have to be made in stand-alone financial statements for other

comprehensive income and non-controlling interest are also the same for consolidated sets of

financial statements (Schwarzbichler, Steiner, and Turnheim, 2018).

AASB 127 lays the requirement to separately report non-controlling interest in the

consolidated financial statements. This non-controlling interest is also allocated the Other

Comprehensive Profit. The subsidiary of JKY Ltd is reported to be recording assets at

historic cost (Bodle, Brimble, Weaven, Frazer, and Blue, (2018).

Changes required to ensure that the consolidated financial statements are correctly

stated

AASB 127 requires adoption of uniform accounting policies by all the members whose

financials are consolidated as a group by the parent or reporting entity. The consolidated

financial statements shall be prepared by the group only by incorporating accounting policies

that are uniform. in case the accounting policies followed by any member differ from the

group, an adjustment is required in its policies to bring them in conformity with the

accounting policies of the group. By using the uniform accounting policies, company could

easily set up proper harmonization in its recording frameworks and helps in strengthen the

recording frameworks as per the AASB 127. Nonetheless internal audit program will also be

set up to assess the changes made in the accounting frameworks of the company (Brunelli,

2018).

Here, in this case if JKY Ltd is using the fair value method to value assets and record assets,

then the financials of the subsidiary shall be adjusted accordingly. The assets of subsidiary

which have till now been recorded at cost shall now have to be recorded at fair value. These

are the changes which are required to ensure that the consolidated financial statements are

correctly stated (Yang, and Aquilino, 2017).

Effect on the disclosure requirements in the annual report

AASB 127 requires attribution of other comprehensive income to the non-controlling interest

even if the balance of NCI turns deficit after that. Other comprehensive income shall also be

separately shown attributable to the non-controlling interest in the financial statements of the

parent as per the requirements of AASB 101, Presentation of Financial Statements. The

disclosures required have to be made in stand-alone financial statements for other

comprehensive income and non-controlling interest are also the same for consolidated sets of

financial statements (Schwarzbichler, Steiner, and Turnheim, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the given case to accommodate the fair value accounting for the assets of subsidiary, the

effects shall be reflected through the other comprehensive income section of the income

statement. If the asset is re-valued upwards, the effect shall be directly observed in the other

comprehensive income by opening a revaluation surplus on the other end. In the annual

report presented with the consolidated financial statement, the disclosures have to be made

for:

The adjustments made in the financials of the subsidiary entity to adopt the revaluation model

for assets than the historical cost to make the accounting policies consistent with that of JKY

Ltd.

The effect of the revaluation upon the other comprehensive income.

The allocation of the other comprehensive income to the parent and the non-controlling

interest shown separately (Gluzová, 2016).

The overall effect of the additions or deductions on the other comprehensive income and the

resultant effect on the share attributable to the non-controlling interests.

Every disclosure as provided for stand-alone financial statements needs to be provided for

consolidated financial statements in the annual report by the concerned reporting entity. In

addition to this, notes to accounts and separate disclosure is also required for the same.

Due to the applicability of AASB 10, Business Combinations, the intra group transactions

found to be affected between the reporting entity and the legal entity, i.e. between the parent

and the subsidiary, will be completely eliminated while preparation of the consolidated

financial statements.

Implication of the AASB 127, consider the disclosure of Non-Comprehensive Income in the

consolidated financial statements are considered. It helps in strengthen the transparency of

the Non-Comprehensive Income in the consolidated financial statements recorded in the

books of account (Chaplin, 2016).

Conclusion

All the accounting standards are followed by company to prepare the financial

statements to set up uniformity and establish the harmonization in the international and

domestic reporting frameworks. Nonetheless, AASB 127 requires adoption of uniform

accounting policies by all the members whose financials are consolidated as a group by the

parent or reporting entity. However, AASB standards have been followed with the

implication of the treatment of intra group transactions and proper explanation regarding

effects shall be reflected through the other comprehensive income section of the income

statement. If the asset is re-valued upwards, the effect shall be directly observed in the other

comprehensive income by opening a revaluation surplus on the other end. In the annual

report presented with the consolidated financial statement, the disclosures have to be made

for:

The adjustments made in the financials of the subsidiary entity to adopt the revaluation model

for assets than the historical cost to make the accounting policies consistent with that of JKY

Ltd.

The effect of the revaluation upon the other comprehensive income.

The allocation of the other comprehensive income to the parent and the non-controlling

interest shown separately (Gluzová, 2016).

The overall effect of the additions or deductions on the other comprehensive income and the

resultant effect on the share attributable to the non-controlling interests.

Every disclosure as provided for stand-alone financial statements needs to be provided for

consolidated financial statements in the annual report by the concerned reporting entity. In

addition to this, notes to accounts and separate disclosure is also required for the same.

Due to the applicability of AASB 10, Business Combinations, the intra group transactions

found to be affected between the reporting entity and the legal entity, i.e. between the parent

and the subsidiary, will be completely eliminated while preparation of the consolidated

financial statements.

Implication of the AASB 127, consider the disclosure of Non-Comprehensive Income in the

consolidated financial statements are considered. It helps in strengthen the transparency of

the Non-Comprehensive Income in the consolidated financial statements recorded in the

books of account (Chaplin, 2016).

Conclusion

All the accounting standards are followed by company to prepare the financial

statements to set up uniformity and establish the harmonization in the international and

domestic reporting frameworks. Nonetheless, AASB 127 requires adoption of uniform

accounting policies by all the members whose financials are consolidated as a group by the

parent or reporting entity. However, AASB standards have been followed with the

implication of the treatment of intra group transactions and proper explanation regarding

considering the examples from the case study presented. This helps company to strengthen

the reporting framework and making the changes required for preparing the consolidated

financial statements. Separate accounting standards are formulated for accounting as per

consolidated method or as per equity method. These have to be followed stringently when an

entity accounts such transactions. Non-adoption of such standards can lead an organisation in

legal trouble. It is analysed that the non-controlling interest is represented by all the

ownership interest in the subsidiary of the reporting entity other than that of the reporting

entity and annual profit of subsidiary company is divided into two parts, one is the share of

parent i.e. reporting entity and the other of non-controlling interest. This shows that there

needs to be proper disclosure of the recorded assets in the books of account of company.

the reporting framework and making the changes required for preparing the consolidated

financial statements. Separate accounting standards are formulated for accounting as per

consolidated method or as per equity method. These have to be followed stringently when an

entity accounts such transactions. Non-adoption of such standards can lead an organisation in

legal trouble. It is analysed that the non-controlling interest is represented by all the

ownership interest in the subsidiary of the reporting entity other than that of the reporting

entity and annual profit of subsidiary company is divided into two parts, one is the share of

parent i.e. reporting entity and the other of non-controlling interest. This shows that there

needs to be proper disclosure of the recorded assets in the books of account of company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.