Corporate Accounting and Financial Reporting: Goodwill Impairment

VerifiedAdded on 2019/10/30

|9

|1594

|415

Report

AI Summary

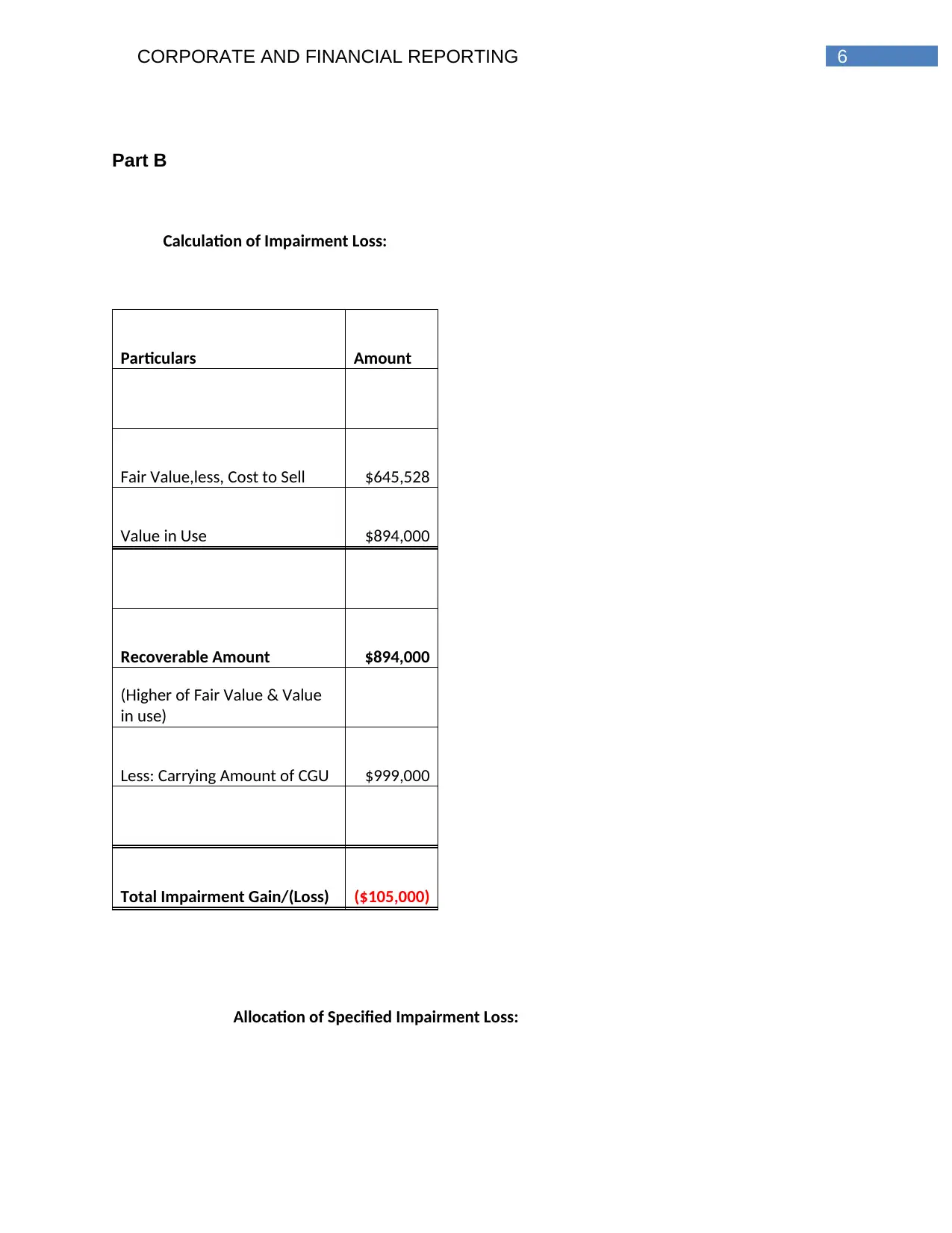

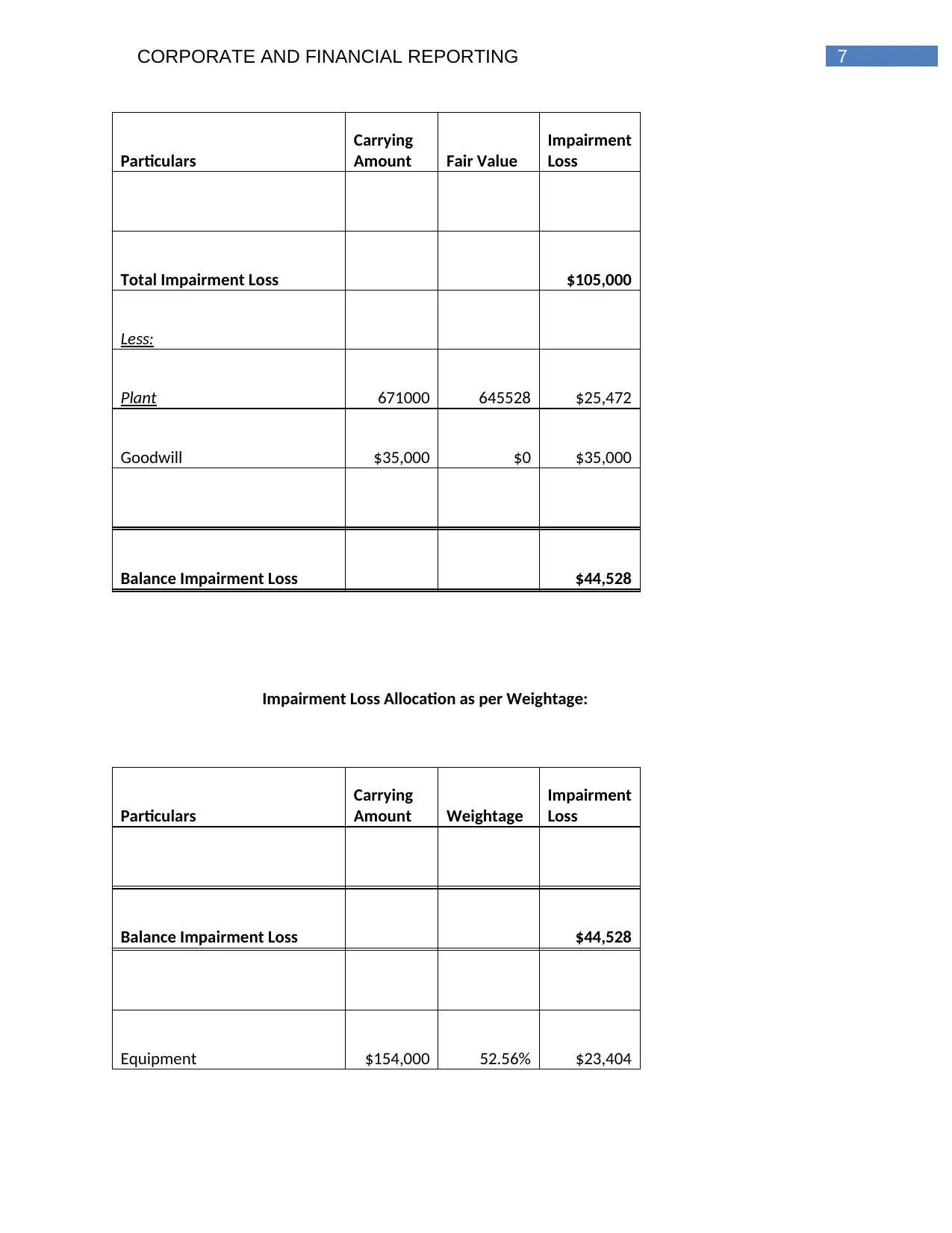

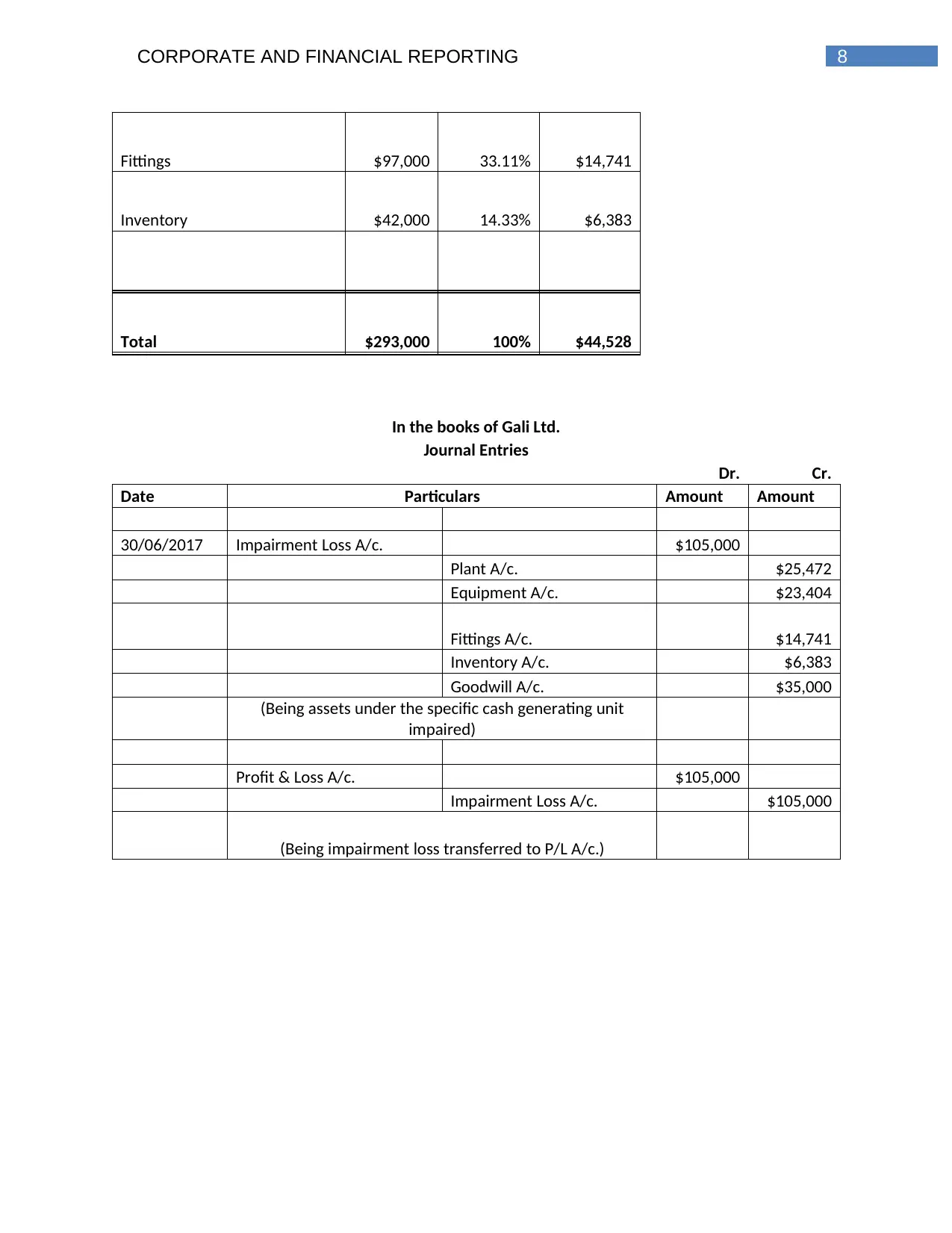

This report delves into the intricacies of corporate accounting and financial reporting, specifically focusing on the treatment of impairment losses and goodwill. It begins by outlining the principles of impairment testing, particularly for goodwill acquired through business combinations, and references AASB 136. The report explains the concepts of recoverable amount, value in use, and fair value, which are crucial in determining asset impairment. It further discusses the prohibition of goodwill amortization and the limitations on reversing impairment losses for goodwill. The report then provides a practical calculation of an impairment loss, including journal entries for Gali Ltd., demonstrating how to allocate the loss across various assets such as plant, equipment, fittings, and inventory. The report concludes with a list of relevant references.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.