Business Risks of Woodside Petroleum

VerifiedAdded on 2022/09/17

|18

|4115

|22

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE AUDITING

Corporate Auditing

Name of the Student:

Name of the University:

Author’s Note

Corporate Auditing

Name of the Student:

Name of the University:

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

CORPORATE AUDITING

Table of Contents

Part 1................................................................................................................................................2

Difference in role of Auditor, Those Charged with Governance and Management....................2

Misconception Regarding the Role of an Auditor.......................................................................3

Reasons for Suspecting Errors in Revenue recognition principles..............................................4

Fraud Cases..................................................................................................................................5

Part 2................................................................................................................................................6

Business Risks of Woodside Petroleum Ltd................................................................................6

Analytical Procedures..................................................................................................................8

Inherent Risks of the Business.....................................................................................................8

Key Accounts and Assertions......................................................................................................9

Inherent risks Evaluation...........................................................................................................11

Planning Materiality..................................................................................................................11

Reference.......................................................................................................................................13

Appendix........................................................................................................................................15

CORPORATE AUDITING

Table of Contents

Part 1................................................................................................................................................2

Difference in role of Auditor, Those Charged with Governance and Management....................2

Misconception Regarding the Role of an Auditor.......................................................................3

Reasons for Suspecting Errors in Revenue recognition principles..............................................4

Fraud Cases..................................................................................................................................5

Part 2................................................................................................................................................6

Business Risks of Woodside Petroleum Ltd................................................................................6

Analytical Procedures..................................................................................................................8

Inherent Risks of the Business.....................................................................................................8

Key Accounts and Assertions......................................................................................................9

Inherent risks Evaluation...........................................................................................................11

Planning Materiality..................................................................................................................11

Reference.......................................................................................................................................13

Appendix........................................................................................................................................15

2

CORPORATE AUDITING

Part 1

To, Mrs. Williams

Audit Manager

Subject: Update Regarding the Risks of Audit and Role of Auditor

Respected Madam

I would like to update you with the risks which we are facing while conducting the

audit of the business and also regarding the facts which indicate that there might be fraudulent

activities in the operations of the business. Th provisions which are stated in ASA 240 makes it

clear that there is a difference in the responsibilities of the auditor and those charged with

governance and the management of the entity itself. All such parties have different role to play

which can ultimately lead to prevention and detection of frauds in a business.

Difference in role of Auditor, Those Charged with Governance and Management

The primary role of an auditor as stated by ASA 240 is to ensure that the financial

statements which is prepared by the management of the company is showing true and fair view

of the financial position of the business. The auditor provides reliance to the stakeholders by

assuring them whether the financial statements are appropriately presented or not and thus

guiding them to take appropriate decisions relating to the business (Auasb.gov.au. 2019).

However, if the auditor notices that there is a material misstatement resulting from fraud in a

business, then the same cannot be ignored even though it is not the primary responsibility of the

auditor. The provisions of ASA 200 make it clear that the auditor needs to consider the

implications of risks which are resulting from frauds especially management frauds (Griffiths

2016). The provisions of ASA 315 states that the auditor shall identify and assess the risks of

CORPORATE AUDITING

Part 1

To, Mrs. Williams

Audit Manager

Subject: Update Regarding the Risks of Audit and Role of Auditor

Respected Madam

I would like to update you with the risks which we are facing while conducting the

audit of the business and also regarding the facts which indicate that there might be fraudulent

activities in the operations of the business. Th provisions which are stated in ASA 240 makes it

clear that there is a difference in the responsibilities of the auditor and those charged with

governance and the management of the entity itself. All such parties have different role to play

which can ultimately lead to prevention and detection of frauds in a business.

Difference in role of Auditor, Those Charged with Governance and Management

The primary role of an auditor as stated by ASA 240 is to ensure that the financial

statements which is prepared by the management of the company is showing true and fair view

of the financial position of the business. The auditor provides reliance to the stakeholders by

assuring them whether the financial statements are appropriately presented or not and thus

guiding them to take appropriate decisions relating to the business (Auasb.gov.au. 2019).

However, if the auditor notices that there is a material misstatement resulting from fraud in a

business, then the same cannot be ignored even though it is not the primary responsibility of the

auditor. The provisions of ASA 200 make it clear that the auditor needs to consider the

implications of risks which are resulting from frauds especially management frauds (Griffiths

2016). The provisions of ASA 315 states that the auditor shall identify and assess the risks of

3

CORPORATE AUDITING

material misstatement due to fraud at the financial report level. Hence. risk of not detecting the

material misstatement resulting from fraud is higher than the risk of not detecting due to error.

Furthermore, the auditor also needs to maintain an independent approach while conducting the

audit for the business and ensure that the judgement of the auditor is not clouded by anything.

The role of the management and those charge with governance is to ensure that the

financial statements are free from errors or is free from any fraudulent activities. The

management and those charged with governance also needs to realize that it is not the role of the

auditor to prepare or maintain the financial statements and rather it is their role (Chou 2015). In

addition to this, the management and those charged with governance also needs to understand

that the auditor is not an employee of the business and therefore independence of the auditor

while conducting audit for the business is crucial.

Misconception Regarding the Role of an Auditor

The auditor is an individual who conducts independent examination of the financial

statements in order to ensure whether the financial statements are free from material

misstatement or not. In a business or society, there is a misconception that the auditor is

appointed for the purpose of detecting frauds which might be taking place in the operations of

the business. However, this is not the case. The auditor is not responsible for detection of frauds

in the business and would only be concerned regarding the presence of any misstatement or

errors in the financial statement of the business. However, ASA 315 provides that if while

conducting audit procedures, the auditor suspects presence of fraud than he needs to apply more

audit procedures and assertions so that the presence of fraud can either be confirmed or denied.

The auditing standards which are implemented in the business environment needs to be followed

by the auditor while performing auditing procedures for a business. Another major

CORPORATE AUDITING

material misstatement due to fraud at the financial report level. Hence. risk of not detecting the

material misstatement resulting from fraud is higher than the risk of not detecting due to error.

Furthermore, the auditor also needs to maintain an independent approach while conducting the

audit for the business and ensure that the judgement of the auditor is not clouded by anything.

The role of the management and those charge with governance is to ensure that the

financial statements are free from errors or is free from any fraudulent activities. The

management and those charged with governance also needs to realize that it is not the role of the

auditor to prepare or maintain the financial statements and rather it is their role (Chou 2015). In

addition to this, the management and those charged with governance also needs to understand

that the auditor is not an employee of the business and therefore independence of the auditor

while conducting audit for the business is crucial.

Misconception Regarding the Role of an Auditor

The auditor is an individual who conducts independent examination of the financial

statements in order to ensure whether the financial statements are free from material

misstatement or not. In a business or society, there is a misconception that the auditor is

appointed for the purpose of detecting frauds which might be taking place in the operations of

the business. However, this is not the case. The auditor is not responsible for detection of frauds

in the business and would only be concerned regarding the presence of any misstatement or

errors in the financial statement of the business. However, ASA 315 provides that if while

conducting audit procedures, the auditor suspects presence of fraud than he needs to apply more

audit procedures and assertions so that the presence of fraud can either be confirmed or denied.

The auditing standards which are implemented in the business environment needs to be followed

by the auditor while performing auditing procedures for a business. Another major

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

CORPORATE AUDITING

misconception regarding the role of the auditor, is that the auditor is an employee of the business

(Drogalas et al. 2017). This is not the case as one of the fundamental principles which needs to

be followed by the auditor is the principle of independence while performing audit procedures in

a business. If independence principles are not maintained in auditing procedures than the quality

of the audit would be affected significantly.

The management of the company is responsible for ensuring that there is no frauds in the

business and also for setting up the internal control structure of the business. The auditor would

be just checking the financial statements and ensure that the annual reports are fairly presented

and all relevant disclosures are provided in the report.

Reasons for Suspecting Errors in Revenue recognition principles

The auditor of a business needs to follow appropriate audit procedures while conducting

the audit and the same needs to be done so that material audit evidences can be collected. The

auditor also needs to follow the principle of professional skepticism in a business so that

appropriate and sufficient audit evidences can be collected by the management of the company

while conducting the operations of the business (Czerney, Schmidt and Thompson 2014). The

reasons due to which an auditor suspects the presence of errors or frauds in the concept o

revenue recognition are listed below in details:

The auditor might suspect that a revenue has been overstated in the financial statement

which can have an impact on the operations of the business. In certain cases, the auditor

of the business might also might suspect that the assets which are shown in the financial

statements are fictitious in nature and therefore, there is a high probability of fraud in the

operations of the business.

CORPORATE AUDITING

misconception regarding the role of the auditor, is that the auditor is an employee of the business

(Drogalas et al. 2017). This is not the case as one of the fundamental principles which needs to

be followed by the auditor is the principle of independence while performing audit procedures in

a business. If independence principles are not maintained in auditing procedures than the quality

of the audit would be affected significantly.

The management of the company is responsible for ensuring that there is no frauds in the

business and also for setting up the internal control structure of the business. The auditor would

be just checking the financial statements and ensure that the annual reports are fairly presented

and all relevant disclosures are provided in the report.

Reasons for Suspecting Errors in Revenue recognition principles

The auditor of a business needs to follow appropriate audit procedures while conducting

the audit and the same needs to be done so that material audit evidences can be collected. The

auditor also needs to follow the principle of professional skepticism in a business so that

appropriate and sufficient audit evidences can be collected by the management of the company

while conducting the operations of the business (Czerney, Schmidt and Thompson 2014). The

reasons due to which an auditor suspects the presence of errors or frauds in the concept o

revenue recognition are listed below in details:

The auditor might suspect that a revenue has been overstated in the financial statement

which can have an impact on the operations of the business. In certain cases, the auditor

of the business might also might suspect that the assets which are shown in the financial

statements are fictitious in nature and therefore, there is a high probability of fraud in the

operations of the business.

5

CORPORATE AUDITING

Another reason due to which the auditor might consider presence of fraud in the revenue

recognition criteria of a business is when the auditor notices that there is a weakness in

the internal control system or there is an opportunity for the management of the company

to engage in unethical practices in business. There are many cases where the management

have the opportunity to engage in fraud and this causes maximum cases of such scandals.

It is therefore for this reason that the auditor needs to appropriate be skeptic of the

situation.

In case, the revenue related transactions of a business are complex in nature then the

auditor needs to provide special attention to the same as there might be a appropriate

opportunity for the management of the company to engage in fraudulent activities.

Fraud Cases

There have been various scandals which have affected the field of accounting and shaken

the business environment drastically and most of these cases are related to misappropriation of

revenue or cooking of profits in the financial statements of the business. Some of the cases are

discussed below in details:

Enron Case

One of the most significant scandal which affected the USA and shook its financial

markets was the Enron Scandal which not only questioned the accounting practices which was

followed in a business but also affected the integrity of the profession of Audit. It was discovered

in 2001 that the senior executives of the company had been making use of the accounting

loopholes to show favorable financial position of the business (Eckhaus and Sheaffer 2018). The

company had systematically covered up billions of dollars’ worth of losses in order to depict a

positive financial performance of the business. The auditing partners of the company Anderson

CORPORATE AUDITING

Another reason due to which the auditor might consider presence of fraud in the revenue

recognition criteria of a business is when the auditor notices that there is a weakness in

the internal control system or there is an opportunity for the management of the company

to engage in unethical practices in business. There are many cases where the management

have the opportunity to engage in fraud and this causes maximum cases of such scandals.

It is therefore for this reason that the auditor needs to appropriate be skeptic of the

situation.

In case, the revenue related transactions of a business are complex in nature then the

auditor needs to provide special attention to the same as there might be a appropriate

opportunity for the management of the company to engage in fraudulent activities.

Fraud Cases

There have been various scandals which have affected the field of accounting and shaken

the business environment drastically and most of these cases are related to misappropriation of

revenue or cooking of profits in the financial statements of the business. Some of the cases are

discussed below in details:

Enron Case

One of the most significant scandal which affected the USA and shook its financial

markets was the Enron Scandal which not only questioned the accounting practices which was

followed in a business but also affected the integrity of the profession of Audit. It was discovered

in 2001 that the senior executives of the company had been making use of the accounting

loopholes to show favorable financial position of the business (Eckhaus and Sheaffer 2018). The

company had systematically covered up billions of dollars’ worth of losses in order to depict a

positive financial performance of the business. The auditing partners of the company Anderson

6

CORPORATE AUDITING

was also pressurized to show that the policies of the company were appropriate and all things

were perfect. When the scandal was exposed, the share price of the company fell rapidly and it

ultimately resulted in bankruptcy of the company (Dibra 2016). Legal action was taken against

the CEO of the company and also the auditing firm for their hand in the scandal.

Bernie Madoff scandal (2002)

The Bernie Madoff scandal is also known far and wide which was considered to be one

of the biggest Ponzi scandal in the history. Bernie Madoff was a stock broker and operated in the

region of United states. The stockbroker had tricked the investors several times over the years

and it was discovered after the financial crisis that Bernie Madoff had accumulated around $ 64.8

billion from tricking the investors. In this case as well, it can be seen that the revenue of the

business has been affected by the unethical practices which resulted in fraud which was

discovered after the financial crisis of 2008.

Part 2

Business Risks of Woodside Petroleum Ltd

The company which is selected for this part Woodside petroleum ltd which is considered

to be one of largest oil and gas company operating in Australia with a global portfolio

(Annualreports.com. 2019). The annual report for the business is considered for estimating the

performance of the business during the period. Some of the business risks which have been

identified are listed below in details:

Fluctuation in Oil Prices: The prices of oil have fluctuated significantly at the start of

the years which can affect the operations of the business. The main source of revenue for

Woodside petroleum ltd is oil and therefore, it is obvious that if the prices of oil

CORPORATE AUDITING

was also pressurized to show that the policies of the company were appropriate and all things

were perfect. When the scandal was exposed, the share price of the company fell rapidly and it

ultimately resulted in bankruptcy of the company (Dibra 2016). Legal action was taken against

the CEO of the company and also the auditing firm for their hand in the scandal.

Bernie Madoff scandal (2002)

The Bernie Madoff scandal is also known far and wide which was considered to be one

of the biggest Ponzi scandal in the history. Bernie Madoff was a stock broker and operated in the

region of United states. The stockbroker had tricked the investors several times over the years

and it was discovered after the financial crisis that Bernie Madoff had accumulated around $ 64.8

billion from tricking the investors. In this case as well, it can be seen that the revenue of the

business has been affected by the unethical practices which resulted in fraud which was

discovered after the financial crisis of 2008.

Part 2

Business Risks of Woodside Petroleum Ltd

The company which is selected for this part Woodside petroleum ltd which is considered

to be one of largest oil and gas company operating in Australia with a global portfolio

(Annualreports.com. 2019). The annual report for the business is considered for estimating the

performance of the business during the period. Some of the business risks which have been

identified are listed below in details:

Fluctuation in Oil Prices: The prices of oil have fluctuated significantly at the start of

the years which can affect the operations of the business. The main source of revenue for

Woodside petroleum ltd is oil and therefore, it is obvious that if the prices of oil

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE AUDITING

fluctuates than the profit margin of the company would be affected. The annual report for

2016 shows that the prices of oil had significantly fallen and it was almost 20% below

last years prices. Therefore, this can be considered to a major risk for the business as it

directly impacts the revenue and profits of the business. Increase in debts: Another major factor which can affect the profitability and also

enhance the risks of the business is the increase in debts of the business. The annual

report of the business shows that the management has focused on acquiring more oil

fields and businesses and therefore a lot of capital was required. The business was able

to finance such operations by increasing the debts of the business. Increase in debts also

means an increase in the finance costs of the business which is clearly shown in the

income statement of 2016. Governmental Policies: The governmental policies also play a vital role and can affect

the revenue which is generated by the business. As per the annual report of Woodside

petroleum ltd for the year 2016, the government has introduced regulations and has also

decided to review the oil industry as there has been a serious decline in the revenue of the

business (DeZoort and Harrison 2018). The investments which are made on such

industries have also not been fruitful and returns after obtained after a long wait. Inflation: Another important factor which affects the revenue of the business is the

inflationary pressure in the country. Due to the effects of inflation, the factor costs have

increased significantly such a labour costs, material costs which directly impacts the

revenue of the business. In the case of Woodside petroleum ltd, the economy of Australia

faces a cyclical rise in prices which has affected the revenue made by the business.

CORPORATE AUDITING

fluctuates than the profit margin of the company would be affected. The annual report for

2016 shows that the prices of oil had significantly fallen and it was almost 20% below

last years prices. Therefore, this can be considered to a major risk for the business as it

directly impacts the revenue and profits of the business. Increase in debts: Another major factor which can affect the profitability and also

enhance the risks of the business is the increase in debts of the business. The annual

report of the business shows that the management has focused on acquiring more oil

fields and businesses and therefore a lot of capital was required. The business was able

to finance such operations by increasing the debts of the business. Increase in debts also

means an increase in the finance costs of the business which is clearly shown in the

income statement of 2016. Governmental Policies: The governmental policies also play a vital role and can affect

the revenue which is generated by the business. As per the annual report of Woodside

petroleum ltd for the year 2016, the government has introduced regulations and has also

decided to review the oil industry as there has been a serious decline in the revenue of the

business (DeZoort and Harrison 2018). The investments which are made on such

industries have also not been fruitful and returns after obtained after a long wait. Inflation: Another important factor which affects the revenue of the business is the

inflationary pressure in the country. Due to the effects of inflation, the factor costs have

increased significantly such a labour costs, material costs which directly impacts the

revenue of the business. In the case of Woodside petroleum ltd, the economy of Australia

faces a cyclical rise in prices which has affected the revenue made by the business.

8

CORPORATE AUDITING

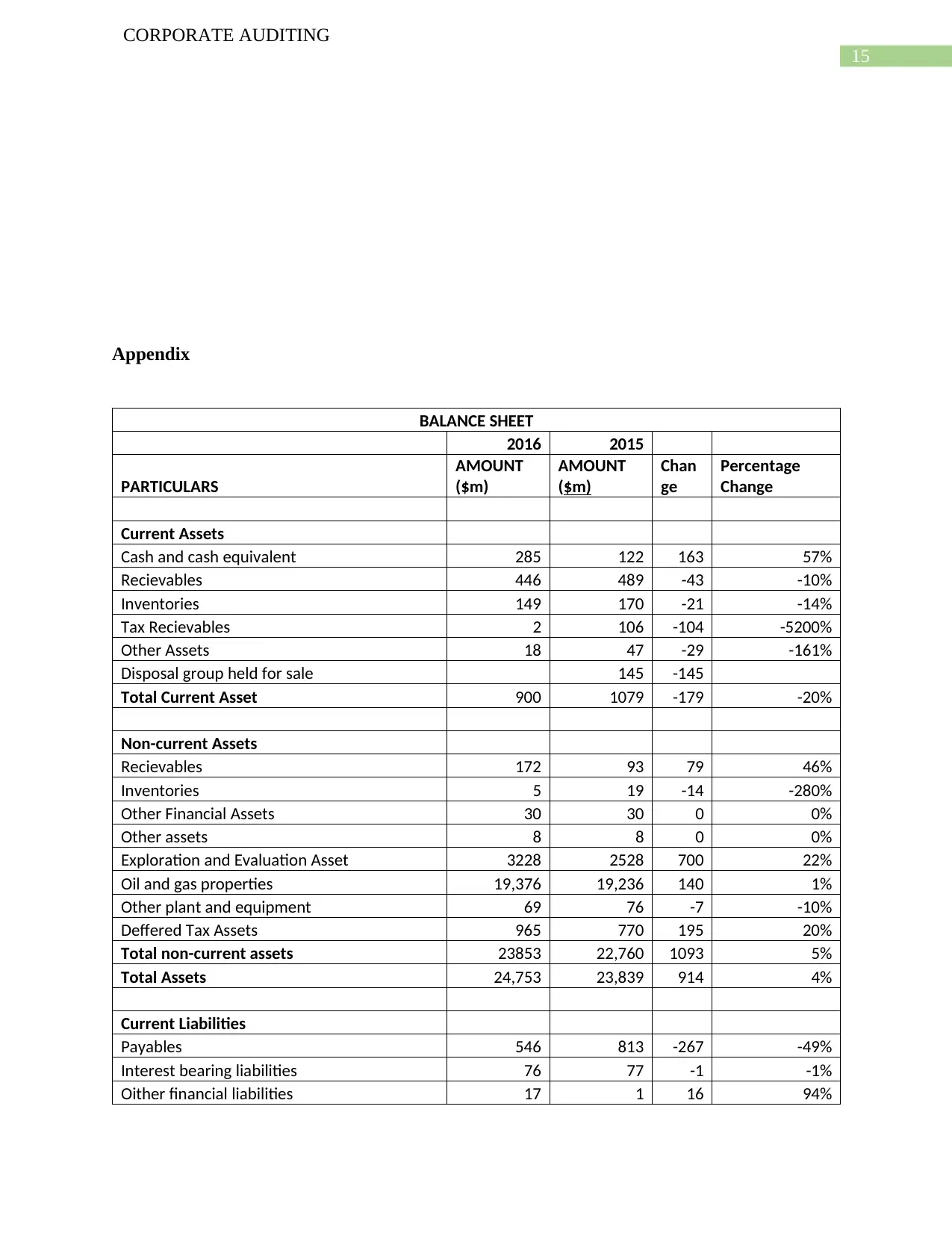

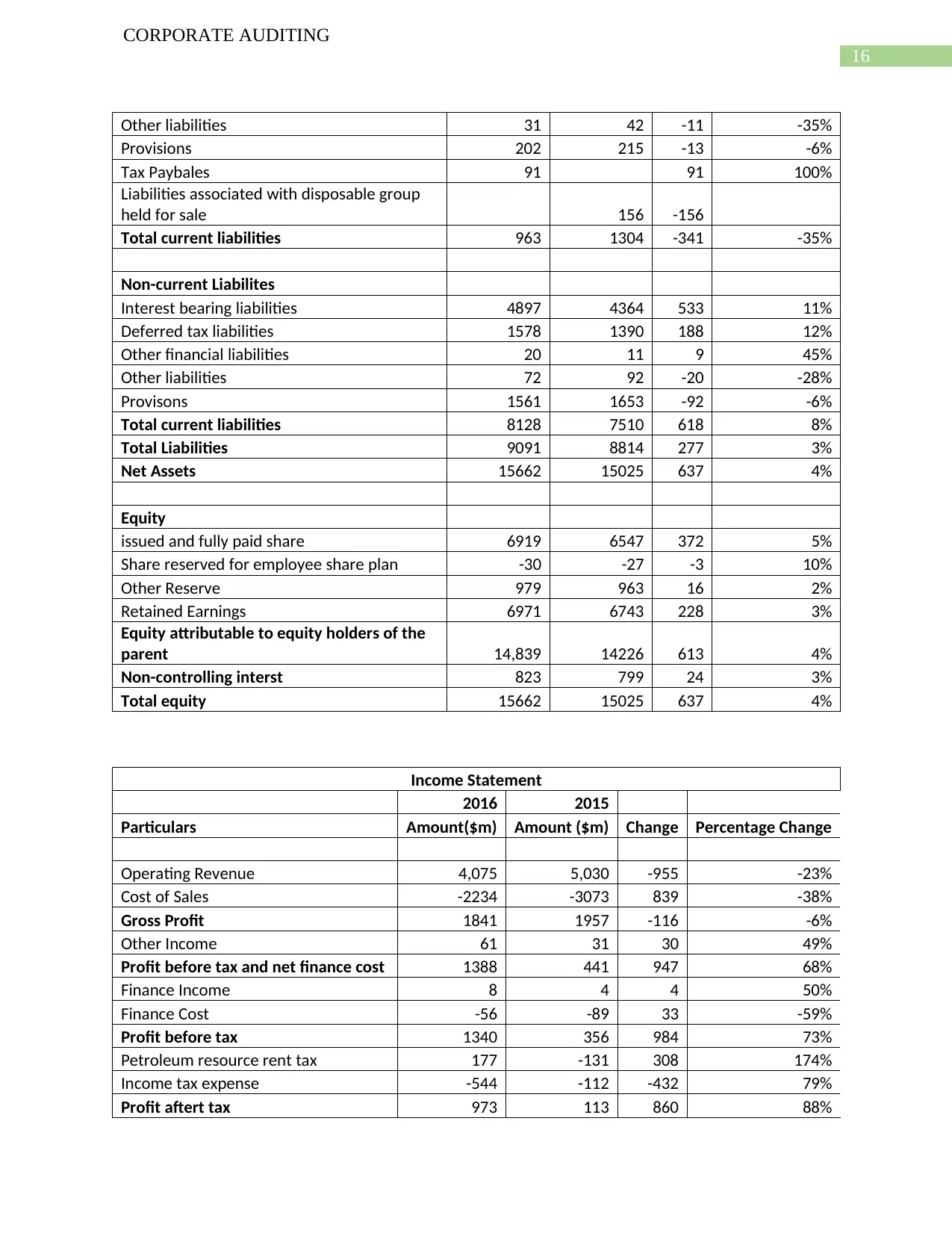

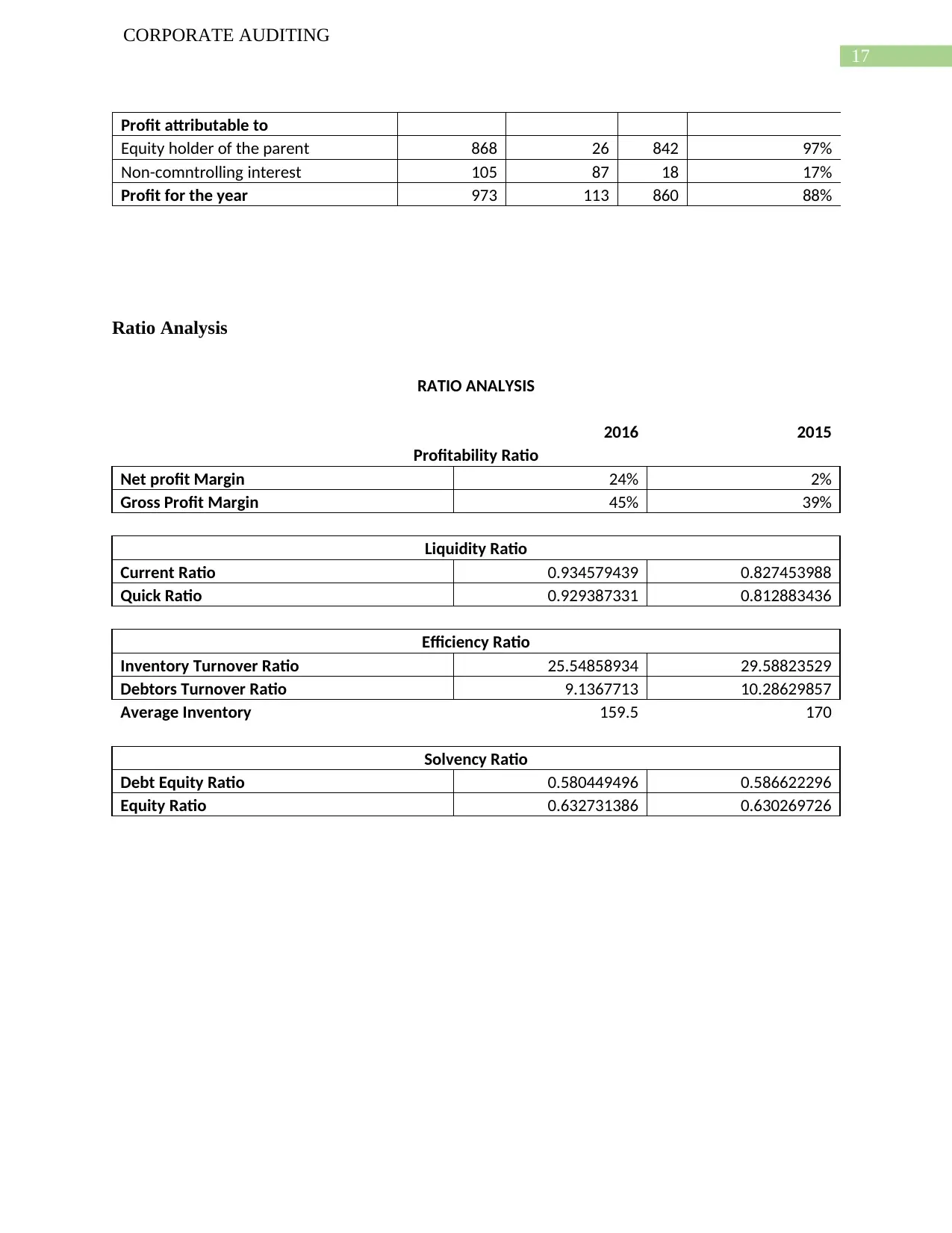

Analytical Procedures

Analytical procedures are one of the techniques which is used by the auditor for checking

the accuracy of the financial statement of the business. The auditor also is able to notice the

changes in items which are presented in the financial statement so that he can apply appropriate

audit procedures for the same. The techniques which are used for the analysis in the case of

Woodside petroleum ltd is ratio analysis where key financial ratios of the company are

ascertained and horizontal analysis which would allow the auditor to review the changes in the

items of the financial statements in comparison to previous year. The cash balance of the

business shows a tremendous increase from 2015 which needs to be invested by the auditor of

the business. In addition to this, the net profit of the business has increased significant which is

clear from the net profit ratio shown in the ratio analysis depicted in the appendix. The auditor

also needs to check the assets of the business as the same shows significant increase in 2016 in

comparison to previous years estimate (Guiral, Guillamon Saorin and Blanco 2014). The analysis

shows that the auditor of the company needs to apply appropriate audit procedures in order to

ensure that the financial statements are showing true and fair view of the financial position of the

business.

Inherent Risks of the Business

The inherent risks are the risks which arises when there is an error or omission of

appropriate information in the financial statement of the business. The analysis of Woodside

petroleum ltd reveals certain inherent risks which are faced by the business and the same are

discussed below in details:

Cost of operations: The revenue of Woodside petroleum ltd is shown to be have decreased

significantly from previous year but the profits of the business has increased significantly.

CORPORATE AUDITING

Analytical Procedures

Analytical procedures are one of the techniques which is used by the auditor for checking

the accuracy of the financial statement of the business. The auditor also is able to notice the

changes in items which are presented in the financial statement so that he can apply appropriate

audit procedures for the same. The techniques which are used for the analysis in the case of

Woodside petroleum ltd is ratio analysis where key financial ratios of the company are

ascertained and horizontal analysis which would allow the auditor to review the changes in the

items of the financial statements in comparison to previous year. The cash balance of the

business shows a tremendous increase from 2015 which needs to be invested by the auditor of

the business. In addition to this, the net profit of the business has increased significant which is

clear from the net profit ratio shown in the ratio analysis depicted in the appendix. The auditor

also needs to check the assets of the business as the same shows significant increase in 2016 in

comparison to previous years estimate (Guiral, Guillamon Saorin and Blanco 2014). The analysis

shows that the auditor of the company needs to apply appropriate audit procedures in order to

ensure that the financial statements are showing true and fair view of the financial position of the

business.

Inherent Risks of the Business

The inherent risks are the risks which arises when there is an error or omission of

appropriate information in the financial statement of the business. The analysis of Woodside

petroleum ltd reveals certain inherent risks which are faced by the business and the same are

discussed below in details:

Cost of operations: The revenue of Woodside petroleum ltd is shown to be have decreased

significantly from previous year but the profits of the business has increased significantly.

9

CORPORATE AUDITING

This means that the business has reduced the costs of operations (Bennett and Hatfield

2017). The audit needs to check the expenses of the business and ensure whether the same

has been presented in appropriate manner. There is chance that the expenses are portrayed

to be lower in order to show favorable income statement.

Exploration and Evaluation assets: The exploration and evaluation assets show material

value in the financial statements of the business. The auditor needs to check if the same is

genuine or not. The auditor needs to apply audit assertion so that it can be confirmed or

denied that the items are showing true and fair view.

Contingent Liabilities: The annual report of Woodside petroleum ltd shows that the

business has contingent liabilities and the same is shown in the notes to account section of

the financial statements (Hatfield 2014). The auditor needs to check the actual liability in

such a situation and whether the same poses any threats to the operations of the business or

not.

Long term debts: The long-term debts of the business is shown to have changed in

comparison to previous year and the auditor needs to ascertain if the same is the actual case

or not and also needs to conduct audit procedures to confirm or deny the suspicions of the

auditor.

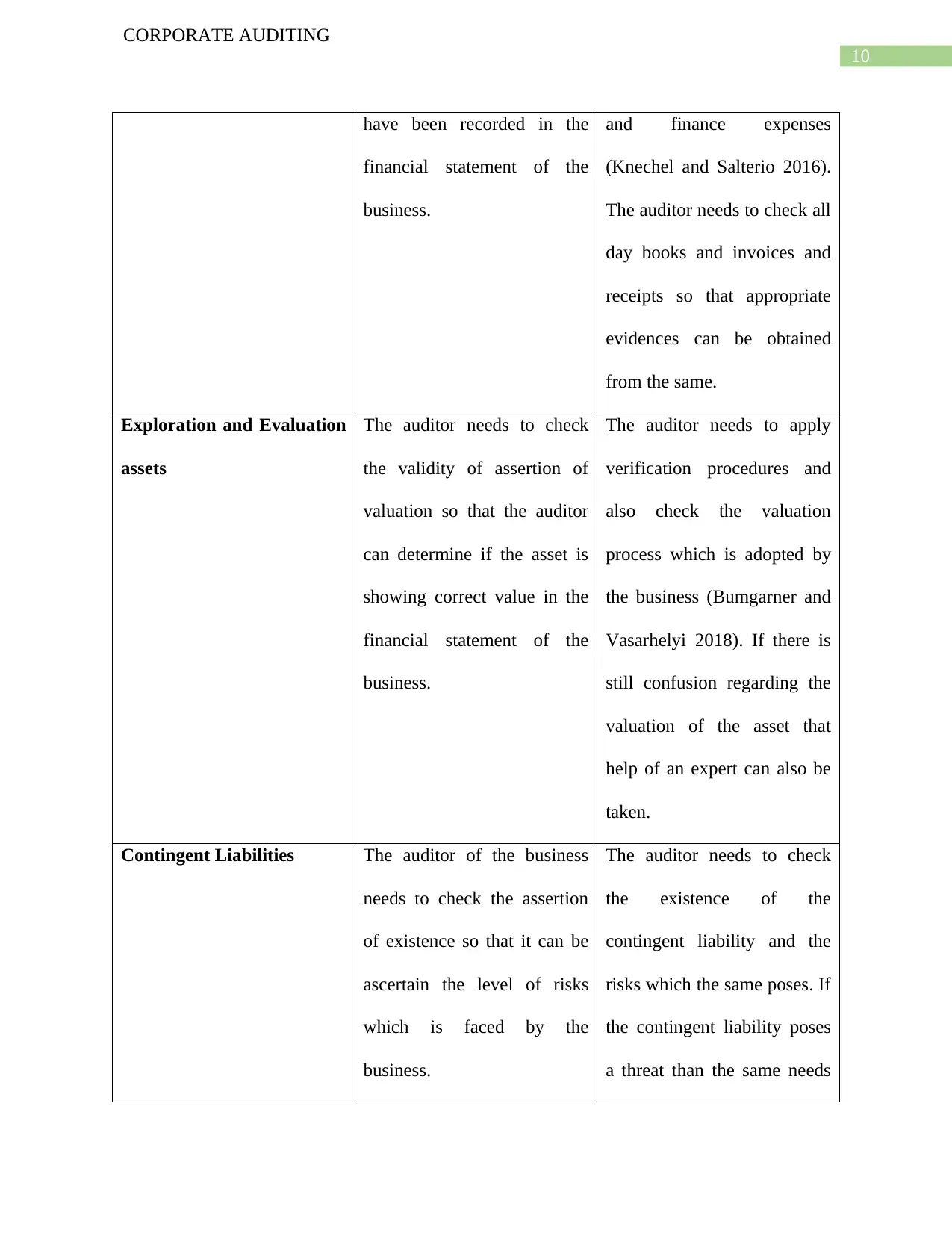

Key Accounts and Assertions

Account Name Assertion Audit procedure

Cost of Operations The auditor needs to check

the assertion of completeness

and ensure that expenses

relate to the current years

The auditor needs to apply

vouching practices to

different expenses such as

wages, cost of sales, taxes

CORPORATE AUDITING

This means that the business has reduced the costs of operations (Bennett and Hatfield

2017). The audit needs to check the expenses of the business and ensure whether the same

has been presented in appropriate manner. There is chance that the expenses are portrayed

to be lower in order to show favorable income statement.

Exploration and Evaluation assets: The exploration and evaluation assets show material

value in the financial statements of the business. The auditor needs to check if the same is

genuine or not. The auditor needs to apply audit assertion so that it can be confirmed or

denied that the items are showing true and fair view.

Contingent Liabilities: The annual report of Woodside petroleum ltd shows that the

business has contingent liabilities and the same is shown in the notes to account section of

the financial statements (Hatfield 2014). The auditor needs to check the actual liability in

such a situation and whether the same poses any threats to the operations of the business or

not.

Long term debts: The long-term debts of the business is shown to have changed in

comparison to previous year and the auditor needs to ascertain if the same is the actual case

or not and also needs to conduct audit procedures to confirm or deny the suspicions of the

auditor.

Key Accounts and Assertions

Account Name Assertion Audit procedure

Cost of Operations The auditor needs to check

the assertion of completeness

and ensure that expenses

relate to the current years

The auditor needs to apply

vouching practices to

different expenses such as

wages, cost of sales, taxes

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

CORPORATE AUDITING

have been recorded in the

financial statement of the

business.

and finance expenses

(Knechel and Salterio 2016).

The auditor needs to check all

day books and invoices and

receipts so that appropriate

evidences can be obtained

from the same.

Exploration and Evaluation

assets

The auditor needs to check

the validity of assertion of

valuation so that the auditor

can determine if the asset is

showing correct value in the

financial statement of the

business.

The auditor needs to apply

verification procedures and

also check the valuation

process which is adopted by

the business (Bumgarner and

Vasarhelyi 2018). If there is

still confusion regarding the

valuation of the asset that

help of an expert can also be

taken.

Contingent Liabilities The auditor of the business

needs to check the assertion

of existence so that it can be

ascertain the level of risks

which is faced by the

business.

The auditor needs to check

the existence of the

contingent liability and the

risks which the same poses. If

the contingent liability poses

a threat than the same needs

CORPORATE AUDITING

have been recorded in the

financial statement of the

business.

and finance expenses

(Knechel and Salterio 2016).

The auditor needs to check all

day books and invoices and

receipts so that appropriate

evidences can be obtained

from the same.

Exploration and Evaluation

assets

The auditor needs to check

the validity of assertion of

valuation so that the auditor

can determine if the asset is

showing correct value in the

financial statement of the

business.

The auditor needs to apply

verification procedures and

also check the valuation

process which is adopted by

the business (Bumgarner and

Vasarhelyi 2018). If there is

still confusion regarding the

valuation of the asset that

help of an expert can also be

taken.

Contingent Liabilities The auditor of the business

needs to check the assertion

of existence so that it can be

ascertain the level of risks

which is faced by the

business.

The auditor needs to check

the existence of the

contingent liability and the

risks which the same poses. If

the contingent liability poses

a threat than the same needs

11

CORPORATE AUDITING

to be recorded in the financial

statement of the business.

Long term debts The auditor in this case needs

to check the assertion of

existence and ensure that the

business has actually taken a

debt or not.

The auditor can opt for

external confirmation from

the creditors or banks so that

existence of debts can be

confirmed (Kharisova and

Kozlova 2014).

Inherent risks Evaluation

The inherent risks posses a serious threat to the process of audit and effective

consideration should be provided to process of audit so that audit procedures can be conducted

for reducing the inherent risks of the business. The auditor needs to pan effectively for the

inherent risks and choose appropriate samples based on planning materiality estimates so that the

overall audit risks of the business can be lowered.

Planning Materiality

The computation of planning materiality depends on the judgement of the auditor and the

percentage which is used for determining the planning materiality also depends on the judgement

of the auditor (Eilifsen and Messier Jr 2014). The business of Woodside petroleum ltd shows that

the most material figure presented in the balance sheet of the company is total assets and the

same is considered to be the base for computing the planning materiality of the business. The

percentage which is considered is 5% of the value of total assets. The computation of planning

materiality is shown below:

CORPORATE AUDITING

to be recorded in the financial

statement of the business.

Long term debts The auditor in this case needs

to check the assertion of

existence and ensure that the

business has actually taken a

debt or not.

The auditor can opt for

external confirmation from

the creditors or banks so that

existence of debts can be

confirmed (Kharisova and

Kozlova 2014).

Inherent risks Evaluation

The inherent risks posses a serious threat to the process of audit and effective

consideration should be provided to process of audit so that audit procedures can be conducted

for reducing the inherent risks of the business. The auditor needs to pan effectively for the

inherent risks and choose appropriate samples based on planning materiality estimates so that the

overall audit risks of the business can be lowered.

Planning Materiality

The computation of planning materiality depends on the judgement of the auditor and the

percentage which is used for determining the planning materiality also depends on the judgement

of the auditor (Eilifsen and Messier Jr 2014). The business of Woodside petroleum ltd shows that

the most material figure presented in the balance sheet of the company is total assets and the

same is considered to be the base for computing the planning materiality of the business. The

percentage which is considered is 5% of the value of total assets. The computation of planning

materiality is shown below:

12

CORPORATE AUDITING

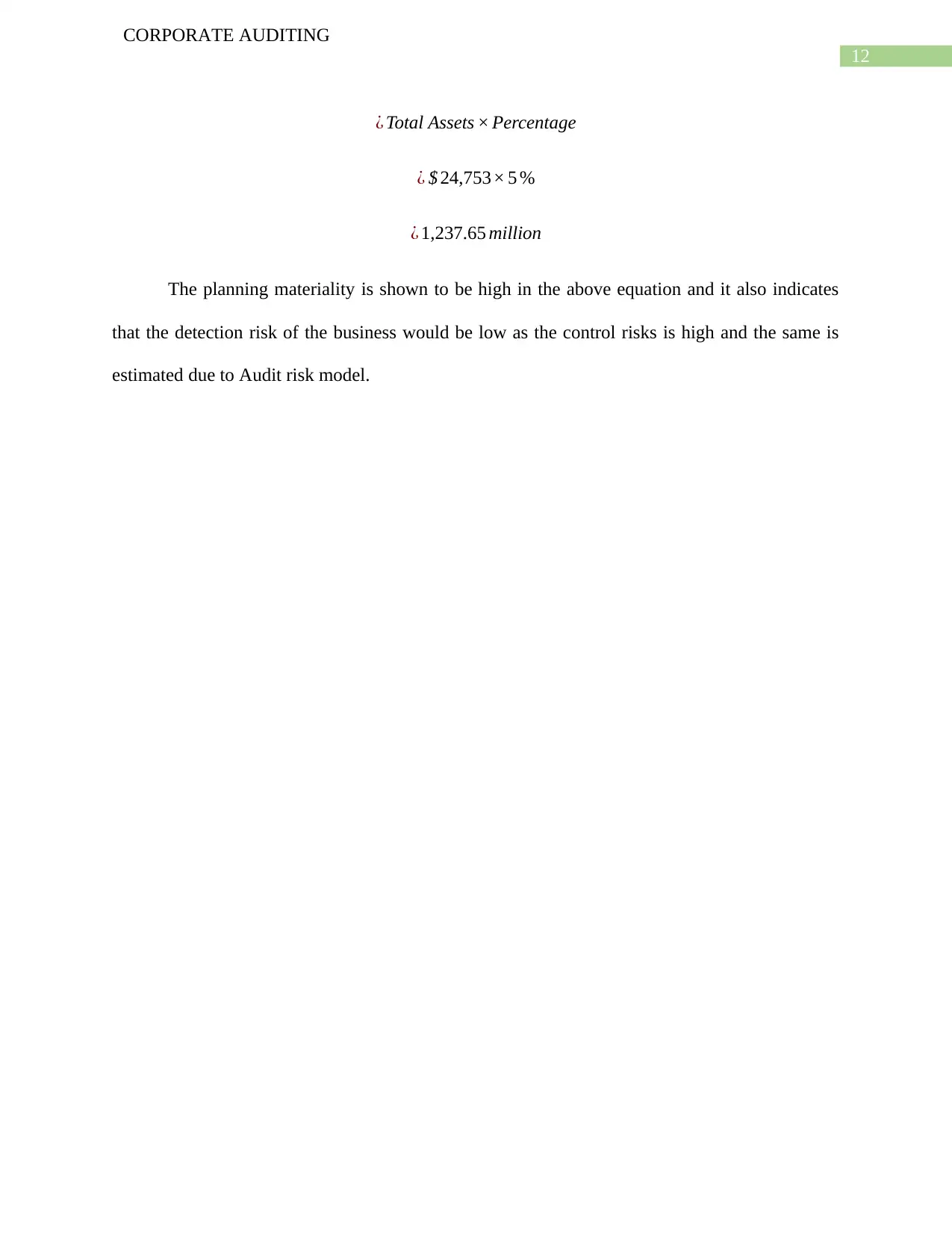

¿ Total Assets × Percentage

¿ $ 24,753× 5 %

¿ 1,237.65 million

The planning materiality is shown to be high in the above equation and it also indicates

that the detection risk of the business would be low as the control risks is high and the same is

estimated due to Audit risk model.

CORPORATE AUDITING

¿ Total Assets × Percentage

¿ $ 24,753× 5 %

¿ 1,237.65 million

The planning materiality is shown to be high in the above equation and it also indicates

that the detection risk of the business would be low as the control risks is high and the same is

estimated due to Audit risk model.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

CORPORATE AUDITING

Reference

Annualreports.com. (2019). Woodside Petroleum Limited - AnnualReports.com. [online]

Available at: http://www.annualreports.com/Company/Woodside-Petroleum-Limited [Accessed

1 Sep. 2019].

Auasb.gov.au. (2019). [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_240_Compiled_2015.pdf [Accessed 1

Sep. 2019].

Bennett, G.B. and Hatfield, R.C., 2017. Do approaching deadlines influence auditors' materiality

assessments?. Auditing: A Journal of Practice & Theory, 36(4), pp.29-48.

Bumgarner, N. and Vasarhelyi, M.A., 2018. Continuous auditing—A new view. In Continuous

Auditing: Theory and Application (pp. 7-51). Emerald Publishing Limited.

Chou, D.C., 2015. Cloud computing risk and audit issues. Computer Standards & Interfaces, 42,

pp.137-142.

Czerney, K., Schmidt, J.J. and Thompson, A.M., 2014. Does auditor explanatory language in

unqualified audit reports indicate increased financial misstatement risk?. The Accounting

Review, 89(6), pp.2115-2149.

CORPORATE AUDITING

Reference

Annualreports.com. (2019). Woodside Petroleum Limited - AnnualReports.com. [online]

Available at: http://www.annualreports.com/Company/Woodside-Petroleum-Limited [Accessed

1 Sep. 2019].

Auasb.gov.au. (2019). [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_240_Compiled_2015.pdf [Accessed 1

Sep. 2019].

Bennett, G.B. and Hatfield, R.C., 2017. Do approaching deadlines influence auditors' materiality

assessments?. Auditing: A Journal of Practice & Theory, 36(4), pp.29-48.

Bumgarner, N. and Vasarhelyi, M.A., 2018. Continuous auditing—A new view. In Continuous

Auditing: Theory and Application (pp. 7-51). Emerald Publishing Limited.

Chou, D.C., 2015. Cloud computing risk and audit issues. Computer Standards & Interfaces, 42,

pp.137-142.

Czerney, K., Schmidt, J.J. and Thompson, A.M., 2014. Does auditor explanatory language in

unqualified audit reports indicate increased financial misstatement risk?. The Accounting

Review, 89(6), pp.2115-2149.

14

CORPORATE AUDITING

DeZoort, F.T. and Harrison, P.D., 2018. Understanding auditors’ sense of responsibility for

detecting fraud within organizations. Journal of Business Ethics, 149(4), pp.857-874.

Dibra, R., 2016. Corporate Governance failure: the case of Enron and Parmalat. European

Scientific Journal, 12(16).

Drogalas, G., Pazarskis, M., Anagnostopoulou, E. and Papachristou, A., 2017. The effect of

internal audit effectiveness, auditor responsibility and training in fraud detection. Accounting

and Management Information Systems, 16(4), pp.434-454.

Eckhaus, E. and Sheaffer, Z., 2018. Managerial hubris detection: the case of Enron. Risk

Management, 20(4), pp.304-325.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Guiral, A., Guillamon Saorin, E. and Blanco, B., 2014. Are Auditor Opinions on Internal Control

Effectiveness Influenced by Corporate Social Responsibility?. Available at SSRN 2485733.

Hatfield, R., 2014. Do approaching deadlines influence auditors’ materiality assessments and

audit sampling decisions. Prieiga per https://www. business. unsw. edu. au/About-Site/Schools-

Site/Accounting-Site/Documents.

Kharisova, F.I. and Kozlova, N.N., 2014. Applying the category of «Assertions (or

preconditions)» In audit of financial statement. Mediterranean journal of social sciences, 5(24),

p.180.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

CORPORATE AUDITING

DeZoort, F.T. and Harrison, P.D., 2018. Understanding auditors’ sense of responsibility for

detecting fraud within organizations. Journal of Business Ethics, 149(4), pp.857-874.

Dibra, R., 2016. Corporate Governance failure: the case of Enron and Parmalat. European

Scientific Journal, 12(16).

Drogalas, G., Pazarskis, M., Anagnostopoulou, E. and Papachristou, A., 2017. The effect of

internal audit effectiveness, auditor responsibility and training in fraud detection. Accounting

and Management Information Systems, 16(4), pp.434-454.

Eckhaus, E. and Sheaffer, Z., 2018. Managerial hubris detection: the case of Enron. Risk

Management, 20(4), pp.304-325.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Guiral, A., Guillamon Saorin, E. and Blanco, B., 2014. Are Auditor Opinions on Internal Control

Effectiveness Influenced by Corporate Social Responsibility?. Available at SSRN 2485733.

Hatfield, R., 2014. Do approaching deadlines influence auditors’ materiality assessments and

audit sampling decisions. Prieiga per https://www. business. unsw. edu. au/About-Site/Schools-

Site/Accounting-Site/Documents.

Kharisova, F.I. and Kozlova, N.N., 2014. Applying the category of «Assertions (or

preconditions)» In audit of financial statement. Mediterranean journal of social sciences, 5(24),

p.180.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

15

CORPORATE AUDITING

Appendix

BALANCE SHEET

2016 2015

PARTICULARS

AMOUNT

($m)

AMOUNT

($m)

Chan

ge

Percentage

Change

Current Assets

Cash and cash equivalent 285 122 163 57%

Recievables 446 489 -43 -10%

Inventories 149 170 -21 -14%

Tax Recievables 2 106 -104 -5200%

Other Assets 18 47 -29 -161%

Disposal group held for sale 145 -145

Total Current Asset 900 1079 -179 -20%

Non-current Assets

Recievables 172 93 79 46%

Inventories 5 19 -14 -280%

Other Financial Assets 30 30 0 0%

Other assets 8 8 0 0%

Exploration and Evaluation Asset 3228 2528 700 22%

Oil and gas properties 19,376 19,236 140 1%

Other plant and equipment 69 76 -7 -10%

Deffered Tax Assets 965 770 195 20%

Total non-current assets 23853 22,760 1093 5%

Total Assets 24,753 23,839 914 4%

Current Liabilities

Payables 546 813 -267 -49%

Interest bearing liabilities 76 77 -1 -1%

Oither financial liabilities 17 1 16 94%

CORPORATE AUDITING

Appendix

BALANCE SHEET

2016 2015

PARTICULARS

AMOUNT

($m)

AMOUNT

($m)

Chan

ge

Percentage

Change

Current Assets

Cash and cash equivalent 285 122 163 57%

Recievables 446 489 -43 -10%

Inventories 149 170 -21 -14%

Tax Recievables 2 106 -104 -5200%

Other Assets 18 47 -29 -161%

Disposal group held for sale 145 -145

Total Current Asset 900 1079 -179 -20%

Non-current Assets

Recievables 172 93 79 46%

Inventories 5 19 -14 -280%

Other Financial Assets 30 30 0 0%

Other assets 8 8 0 0%

Exploration and Evaluation Asset 3228 2528 700 22%

Oil and gas properties 19,376 19,236 140 1%

Other plant and equipment 69 76 -7 -10%

Deffered Tax Assets 965 770 195 20%

Total non-current assets 23853 22,760 1093 5%

Total Assets 24,753 23,839 914 4%

Current Liabilities

Payables 546 813 -267 -49%

Interest bearing liabilities 76 77 -1 -1%

Oither financial liabilities 17 1 16 94%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

CORPORATE AUDITING

Other liabilities 31 42 -11 -35%

Provisions 202 215 -13 -6%

Tax Paybales 91 91 100%

Liabilities associated with disposable group

held for sale 156 -156

Total current liabilities 963 1304 -341 -35%

Non-current Liabilites

Interest bearing liabilities 4897 4364 533 11%

Deferred tax liabilities 1578 1390 188 12%

Other financial liabilities 20 11 9 45%

Other liabilities 72 92 -20 -28%

Provisons 1561 1653 -92 -6%

Total current liabilities 8128 7510 618 8%

Total Liabilities 9091 8814 277 3%

Net Assets 15662 15025 637 4%

Equity

issued and fully paid share 6919 6547 372 5%

Share reserved for employee share plan -30 -27 -3 10%

Other Reserve 979 963 16 2%

Retained Earnings 6971 6743 228 3%

Equity attributable to equity holders of the

parent 14,839 14226 613 4%

Non-controlling interst 823 799 24 3%

Total equity 15662 15025 637 4%

Income Statement

2016 2015

Particulars Amount($m) Amount ($m) Change Percentage Change

Operating Revenue 4,075 5,030 -955 -23%

Cost of Sales -2234 -3073 839 -38%

Gross Profit 1841 1957 -116 -6%

Other Income 61 31 30 49%

Profit before tax and net finance cost 1388 441 947 68%

Finance Income 8 4 4 50%

Finance Cost -56 -89 33 -59%

Profit before tax 1340 356 984 73%

Petroleum resource rent tax 177 -131 308 174%

Income tax expense -544 -112 -432 79%

Profit aftert tax 973 113 860 88%

CORPORATE AUDITING

Other liabilities 31 42 -11 -35%

Provisions 202 215 -13 -6%

Tax Paybales 91 91 100%

Liabilities associated with disposable group

held for sale 156 -156

Total current liabilities 963 1304 -341 -35%

Non-current Liabilites

Interest bearing liabilities 4897 4364 533 11%

Deferred tax liabilities 1578 1390 188 12%

Other financial liabilities 20 11 9 45%

Other liabilities 72 92 -20 -28%

Provisons 1561 1653 -92 -6%

Total current liabilities 8128 7510 618 8%

Total Liabilities 9091 8814 277 3%

Net Assets 15662 15025 637 4%

Equity

issued and fully paid share 6919 6547 372 5%

Share reserved for employee share plan -30 -27 -3 10%

Other Reserve 979 963 16 2%

Retained Earnings 6971 6743 228 3%

Equity attributable to equity holders of the

parent 14,839 14226 613 4%

Non-controlling interst 823 799 24 3%

Total equity 15662 15025 637 4%

Income Statement

2016 2015

Particulars Amount($m) Amount ($m) Change Percentage Change

Operating Revenue 4,075 5,030 -955 -23%

Cost of Sales -2234 -3073 839 -38%

Gross Profit 1841 1957 -116 -6%

Other Income 61 31 30 49%

Profit before tax and net finance cost 1388 441 947 68%

Finance Income 8 4 4 50%

Finance Cost -56 -89 33 -59%

Profit before tax 1340 356 984 73%

Petroleum resource rent tax 177 -131 308 174%

Income tax expense -544 -112 -432 79%

Profit aftert tax 973 113 860 88%

17

CORPORATE AUDITING

Profit attributable to

Equity holder of the parent 868 26 842 97%

Non-comntrolling interest 105 87 18 17%

Profit for the year 973 113 860 88%

Ratio Analysis

RATIO ANALYSIS

2016 2015

Profitability Ratio

Net profit Margin 24% 2%

Gross Profit Margin 45% 39%

Liquidity Ratio

Current Ratio 0.934579439 0.827453988

Quick Ratio 0.929387331 0.812883436

Efficiency Ratio

Inventory Turnover Ratio 25.54858934 29.58823529

Debtors Turnover Ratio 9.1367713 10.28629857

Average Inventory 159.5 170

Solvency Ratio

Debt Equity Ratio 0.580449496 0.586622296

Equity Ratio 0.632731386 0.630269726

CORPORATE AUDITING

Profit attributable to

Equity holder of the parent 868 26 842 97%

Non-comntrolling interest 105 87 18 17%

Profit for the year 973 113 860 88%

Ratio Analysis

RATIO ANALYSIS

2016 2015

Profitability Ratio

Net profit Margin 24% 2%

Gross Profit Margin 45% 39%

Liquidity Ratio

Current Ratio 0.934579439 0.827453988

Quick Ratio 0.929387331 0.812883436

Efficiency Ratio

Inventory Turnover Ratio 25.54858934 29.58823529

Debtors Turnover Ratio 9.1367713 10.28629857

Average Inventory 159.5 170

Solvency Ratio

Debt Equity Ratio 0.580449496 0.586622296

Equity Ratio 0.632731386 0.630269726

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.