Analysis of Myer Holdings Limited

VerifiedAdded on 2023/01/18

|17

|3014

|68

AI Summary

This paper provides a critical analysis of the annual report of Myer Holdings Limited based on its annual report in 2016. It covers business risks, results of analytical procedures, inherent risks, key accounts at risk, and planning materiality.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE AUDITING

Corporate Auditing

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Auditing

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE AUDITING

Table of Contents

Part 2: Memorandum to the audit partner........................................................................................3

a. Business risks of Myer Holdings Limited:..............................................................................3

b. Results of analytical procedures:.............................................................................................5

c. Inherent risks identified from business risks and analytical procedures:................................8

d. Key account and key related assertion at risk:.......................................................................10

e. Analysis of inherent risk:.......................................................................................................10

f. Planning materiality:..............................................................................................................10

References:....................................................................................................................................12

Appendices:...................................................................................................................................14

Table of Contents

Part 2: Memorandum to the audit partner........................................................................................3

a. Business risks of Myer Holdings Limited:..............................................................................3

b. Results of analytical procedures:.............................................................................................5

c. Inherent risks identified from business risks and analytical procedures:................................8

d. Key account and key related assertion at risk:.......................................................................10

e. Analysis of inherent risk:.......................................................................................................10

f. Planning materiality:..............................................................................................................10

References:....................................................................................................................................12

Appendices:...................................................................................................................................14

2CORPORATE AUDITING

Part 2: Memorandum to the audit partner

Memorandum

To: The Audit Partner

From: The Auditor

Date: 15/04/2019

Subject: Analysis of Myer Holdings Limited

The following paper includes a critical analysis of the annual report of Myer Holdings

Limited based on its annual report in 2016. The aspects covered in this memorandum include the

following:

a. Business risks of Myer Holdings Limited:

According to the 2016 annual report of Myer, the four major business risks of the

organisation include the following:

External risk or economic risk:

The macro-economic factors like fluctuations in AUD, lower customer confidence,

variations in government policies and natural or unforeseen events such as natural strike or act of

terrorism and weakness in international economy could have unfavourable impact on the ability

of the organisation in accomplishing sales growth. Myer is involved in regular analysis and using

available and economic data for mitigating the future effect on sales. The techniques

implemented by the organisation include capital management, conservative hedging,

Part 2: Memorandum to the audit partner

Memorandum

To: The Audit Partner

From: The Auditor

Date: 15/04/2019

Subject: Analysis of Myer Holdings Limited

The following paper includes a critical analysis of the annual report of Myer Holdings

Limited based on its annual report in 2016. The aspects covered in this memorandum include the

following:

a. Business risks of Myer Holdings Limited:

According to the 2016 annual report of Myer, the four major business risks of the

organisation include the following:

External risk or economic risk:

The macro-economic factors like fluctuations in AUD, lower customer confidence,

variations in government policies and natural or unforeseen events such as natural strike or act of

terrorism and weakness in international economy could have unfavourable impact on the ability

of the organisation in accomplishing sales growth. Myer is involved in regular analysis and using

available and economic data for mitigating the future effect on sales. The techniques

implemented by the organisation include capital management, conservative hedging,

3CORPORATE AUDITING

merchandise initiatives and marketing for combating the cyclical nature of business

(Investor.myer.com.au 2019).

Competitive landscape risk:

Myer operates in the Australian retail industry, which is extremely competitive. The

competitive position of the organisation might be affected adversely by the new market entrants,

present competition and increased competition in online platforms (Junior, Best and Cotter

2014). For minimising these risks, Myer has adopted new strategy, which is guided by detailed

customer overview and concentration on providing customer-led offer, Omni-channel shopping

and excellent experiences.

Brand reputation risks:

The positive brand reputation of Myer is critical to develop positive relationships with the

customers, which would result in generation of sales and goodwill towards the organisation. Any

considerable issue or event could draw criticism on the brand and the result would be

unfavourable effect on its share price (Knechel and Salterio 2016). For dealing with the same,

Myer has formulated a group of initiatives and policies for eliminating brand risk that constitutes

of code of conduct, ethical sourcing policy, whistleblower policy, sustainability and

environmental initiatives and marketing campaigns.

Technology risk:

Myer has been increasing on its dependence on technology due to the changing

environment. This might increase the possibility of risk in the malfunctioning of IT systems,

outdated infrastructure in IT or cyber security breach and the effect would be detrimental on

sales, brand reputation and business efficiencies (Knechel 2016). For dealing with these risks,

merchandise initiatives and marketing for combating the cyclical nature of business

(Investor.myer.com.au 2019).

Competitive landscape risk:

Myer operates in the Australian retail industry, which is extremely competitive. The

competitive position of the organisation might be affected adversely by the new market entrants,

present competition and increased competition in online platforms (Junior, Best and Cotter

2014). For minimising these risks, Myer has adopted new strategy, which is guided by detailed

customer overview and concentration on providing customer-led offer, Omni-channel shopping

and excellent experiences.

Brand reputation risks:

The positive brand reputation of Myer is critical to develop positive relationships with the

customers, which would result in generation of sales and goodwill towards the organisation. Any

considerable issue or event could draw criticism on the brand and the result would be

unfavourable effect on its share price (Knechel and Salterio 2016). For dealing with the same,

Myer has formulated a group of initiatives and policies for eliminating brand risk that constitutes

of code of conduct, ethical sourcing policy, whistleblower policy, sustainability and

environmental initiatives and marketing campaigns.

Technology risk:

Myer has been increasing on its dependence on technology due to the changing

environment. This might increase the possibility of risk in the malfunctioning of IT systems,

outdated infrastructure in IT or cyber security breach and the effect would be detrimental on

sales, brand reputation and business efficiencies (Knechel 2016). For dealing with these risks,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE AUDITING

Myer has invested in enhancing its in-house technological capabilities along with involving in

reputable third-party IT service providers for assuring the presence of issue management

procedures and reliable IT systems.

b. Results of analytical procedures:

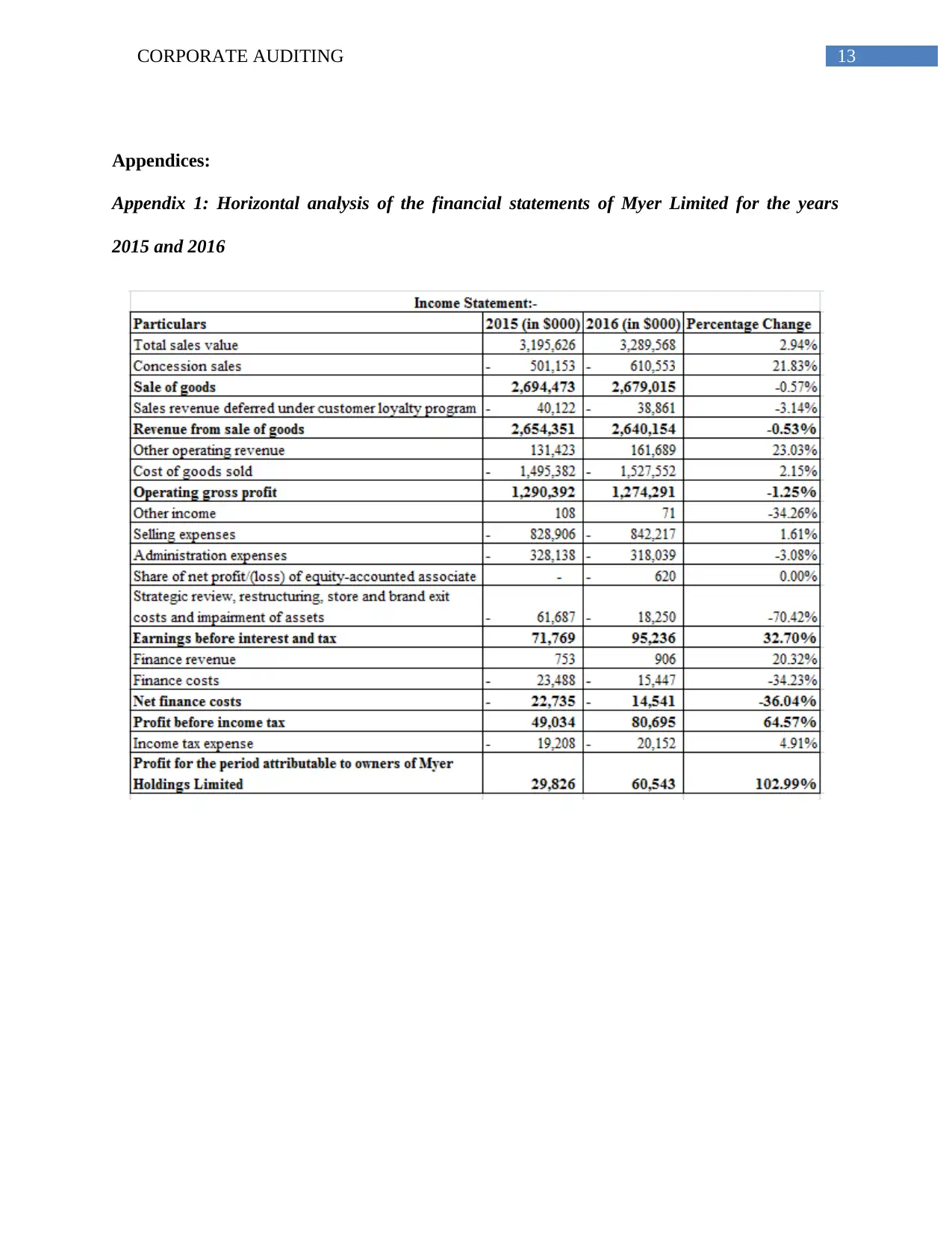

For determining the outcomes of the analytical procedures, the techniques used include

horizontal analysis and ratio analysis (Refer to Appendices, Appendix 1 and Appendix 2). The

detailed analysis of these techniques is represented as follows:

Horizontal analysis:

Income statement:

It has been identified that revenue from sale of goods for Myer has fallen by 0.53% in

2016 owing to the increase in discounts offered to the customers and loyal revenue generated

under customer loyalty program. On the other hand, due to the increase in cost of goods sold by

2.15% in 2016, there has been decline in operating gross profit by 1.25%. However, the

organisation has managed to minimise its operating expenses largely in 2016, which has

increased its operating profit by 32.70%. This is evident from decline in costs related to strategic

review, store, restructuring and asset impairment by 70.42% in 2016. In addition, Myer has

managed to reduce its finance costs owing to which it experienced increase of 102.99% in 2016

(Investor.myer.com.au 2019).

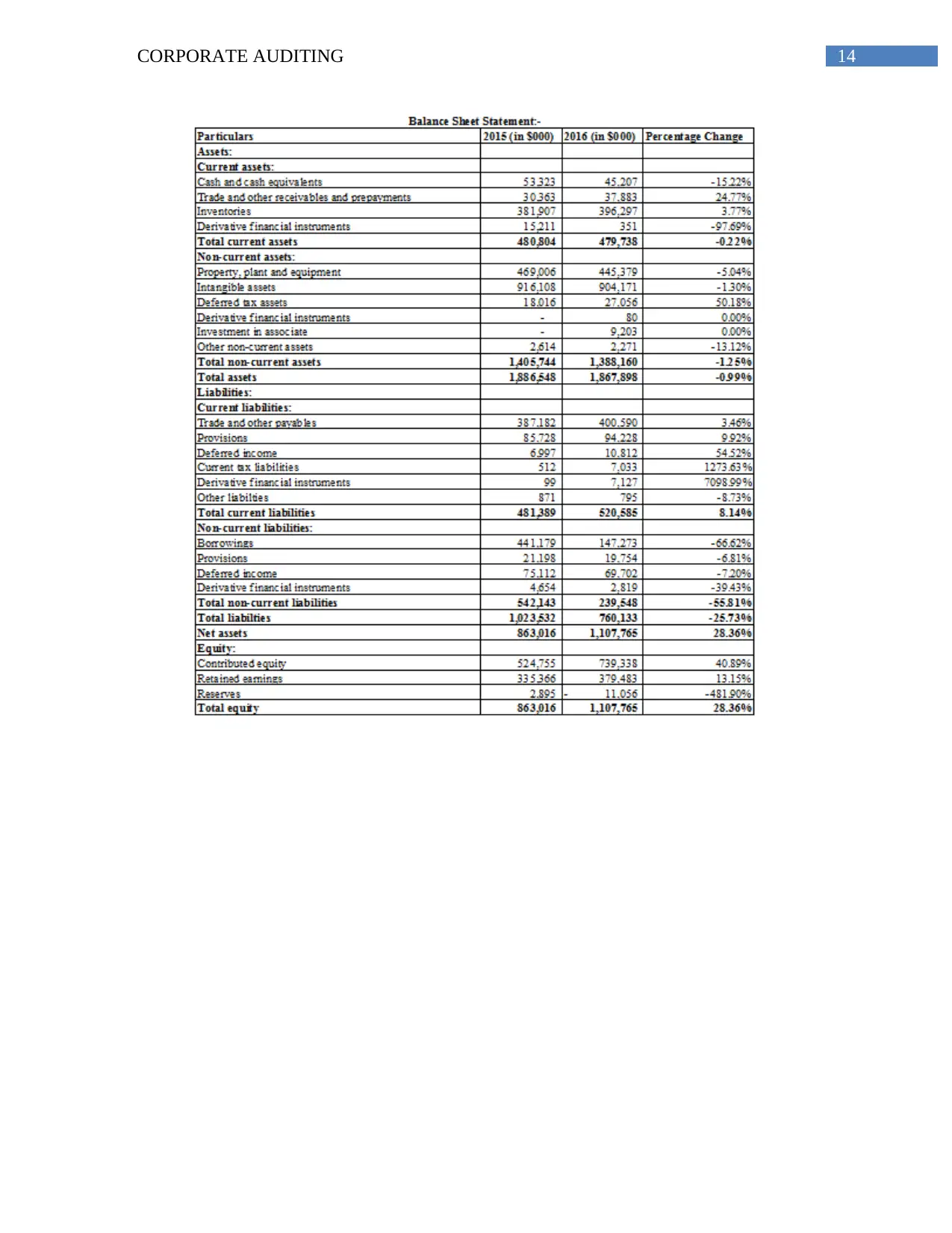

Balance sheet statement:

It could be seen that Myer has experienced a decline in its current assets by 0.22% owing

to decline in cash and cash equivalents and derivative financial instruments. The similar trend is

followed in case of non-current assets that have declined by 0.99% in 2016 owing to fall in the

Myer has invested in enhancing its in-house technological capabilities along with involving in

reputable third-party IT service providers for assuring the presence of issue management

procedures and reliable IT systems.

b. Results of analytical procedures:

For determining the outcomes of the analytical procedures, the techniques used include

horizontal analysis and ratio analysis (Refer to Appendices, Appendix 1 and Appendix 2). The

detailed analysis of these techniques is represented as follows:

Horizontal analysis:

Income statement:

It has been identified that revenue from sale of goods for Myer has fallen by 0.53% in

2016 owing to the increase in discounts offered to the customers and loyal revenue generated

under customer loyalty program. On the other hand, due to the increase in cost of goods sold by

2.15% in 2016, there has been decline in operating gross profit by 1.25%. However, the

organisation has managed to minimise its operating expenses largely in 2016, which has

increased its operating profit by 32.70%. This is evident from decline in costs related to strategic

review, store, restructuring and asset impairment by 70.42% in 2016. In addition, Myer has

managed to reduce its finance costs owing to which it experienced increase of 102.99% in 2016

(Investor.myer.com.au 2019).

Balance sheet statement:

It could be seen that Myer has experienced a decline in its current assets by 0.22% owing

to decline in cash and cash equivalents and derivative financial instruments. The similar trend is

followed in case of non-current assets that have declined by 0.99% in 2016 owing to fall in the

5CORPORATE AUDITING

values of property, plant and equipment, intangible assets and other non-current assets. On the

other hand, the current liabilities of Myer have been observed to increase by 8.14% in 2016

because of increase in trade and other payables, provisions, deferred income, current tax

liabilities and derivative financial instruments. However, there has been significant downfall in

non-current liabilities by -55.81% in 2016 owing to decline in long-term borrowings As a result,

this has resulted in increase in total equity by 28.36% for Myer in 2016 (Investor.myer.com.au

2019).

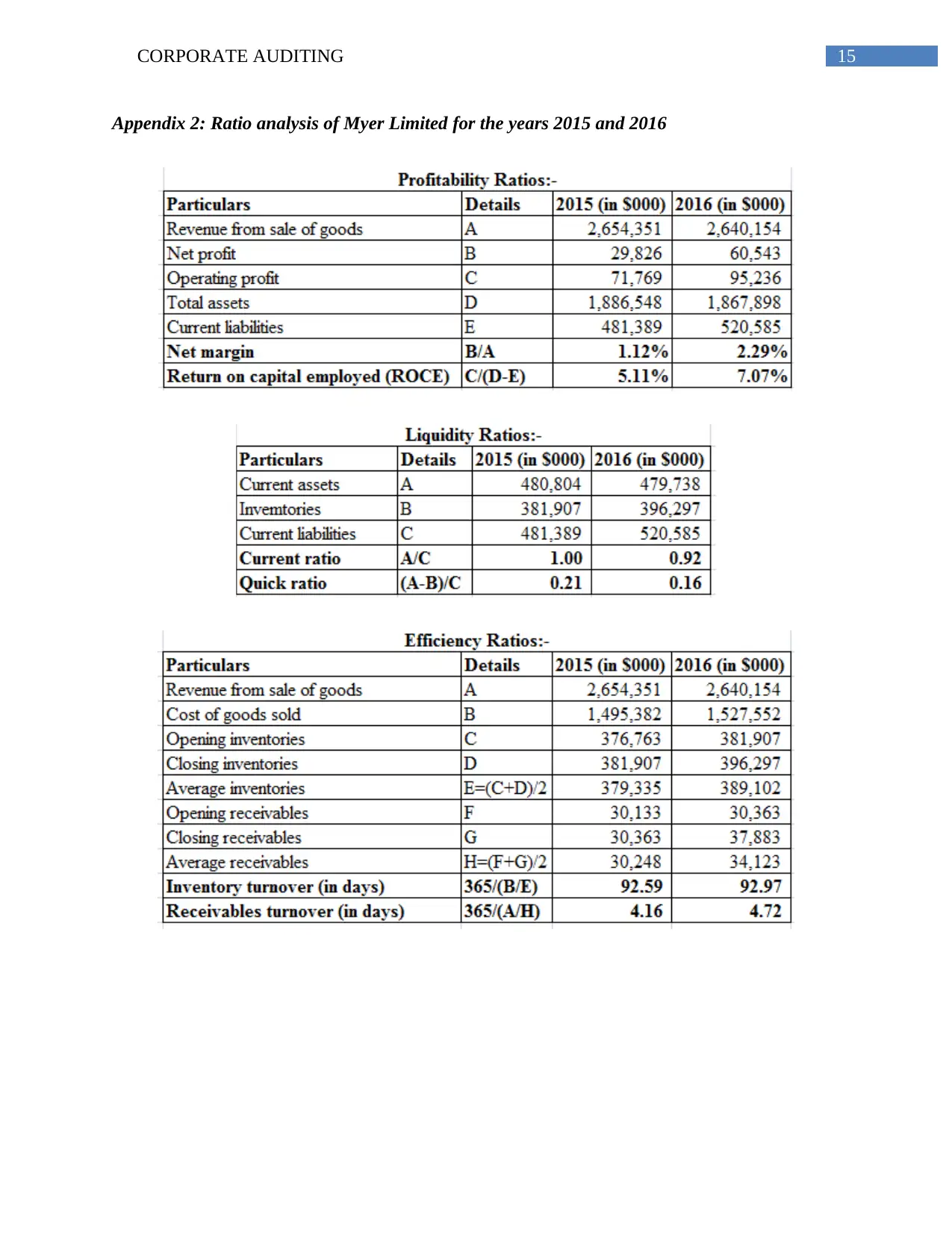

Ratio analysis:

For analysing the financial condition of Myer in 2016, the following ratios are used:

Profitability ratios:

The two profitability ratios used for evaluating the financial performance of Myer include

net margin and return on capital employed (ROCE). Net margin is observed to increase from

1.12% in 2015 to 2.29% in 2016, which implies that it has managed to earn more profit in the

year to be distributed to the shareholders (Lenz and Hahn 2015). For Myer, it has managed to

reduce its administrative expense compared to sales revenue largely that has resulted in better

profitability position for the organisation. The trend is similar in case of ROCE as well, which

has increased from 5.11% in 2015 to 7.07% in 2016. This implies that for every $1 employed by

Myer, it generates $0.0707 in 2016 compared to $0.0511, which is definitely a favourable

indication for the organisation.

Liquidity ratios:

The liquidity ratios that are considered for analysing the financial position of Myer

include current ratio and quick ratio. Both these ratios assist in identifying the ability of an

values of property, plant and equipment, intangible assets and other non-current assets. On the

other hand, the current liabilities of Myer have been observed to increase by 8.14% in 2016

because of increase in trade and other payables, provisions, deferred income, current tax

liabilities and derivative financial instruments. However, there has been significant downfall in

non-current liabilities by -55.81% in 2016 owing to decline in long-term borrowings As a result,

this has resulted in increase in total equity by 28.36% for Myer in 2016 (Investor.myer.com.au

2019).

Ratio analysis:

For analysing the financial condition of Myer in 2016, the following ratios are used:

Profitability ratios:

The two profitability ratios used for evaluating the financial performance of Myer include

net margin and return on capital employed (ROCE). Net margin is observed to increase from

1.12% in 2015 to 2.29% in 2016, which implies that it has managed to earn more profit in the

year to be distributed to the shareholders (Lenz and Hahn 2015). For Myer, it has managed to

reduce its administrative expense compared to sales revenue largely that has resulted in better

profitability position for the organisation. The trend is similar in case of ROCE as well, which

has increased from 5.11% in 2015 to 7.07% in 2016. This implies that for every $1 employed by

Myer, it generates $0.0707 in 2016 compared to $0.0511, which is definitely a favourable

indication for the organisation.

Liquidity ratios:

The liquidity ratios that are considered for analysing the financial position of Myer

include current ratio and quick ratio. Both these ratios assist in identifying the ability of an

6CORPORATE AUDITING

organisation in settling its short-term dues by using its current assets (Lombardi, Bloch and

Vasarhelyi 2014). In case of Myer, current ratio is observed to decline from 1 in 2015 to 0.92 in

2016, as there has been decline in cash and cash equivalents and short-term derivative financial

instruments. On the other hand, quick ratio is deemed to be the superior measure of liquidity,

since it excludes inventories for analysing the liquidity position of an organisation (Ojala et al.

2014). This ratio has fallen as well for Myer from 0.21 in 2015 to 0.16 in 2016, which is well

below the ideal standard of 1. This is due to the fact that the organisation has undertaken

significant investment in inventories due to which it has failed to maintain adequate amount of

working capital.

Efficiency ratios:

In order to assess the efficiency position of Myer Holdings Limited, the two ratios taken

into consideration mainly include inventory turnover and receivables turnover expressed in

number of days. Inventory turnover denotes the time taken by an organisation in releasing its

inventory in a particular period (Messier Jr 2016). In case of Myer, inventory turnover has

increased marginally from 92.59 days in 2015 to 92.97 days in 2016, which implies that the

organisation has experienced a fall in product demand due to which it could not release its

inventory at a faster rate. On the other hand, receivables turnover denotes the time that an

organisation takes in obtaining due amounts from the customers. A lower timeframe is always

favourable, as it denotes quick collection of due amounts and increase in working capital (Pitt

2014). In case of Myer, receivables turnover period has increased from 4.16 days in 2015 to 4.72

days in 2016 owing to the lenient debtor policy it has adopted for accelerating sales revenue.

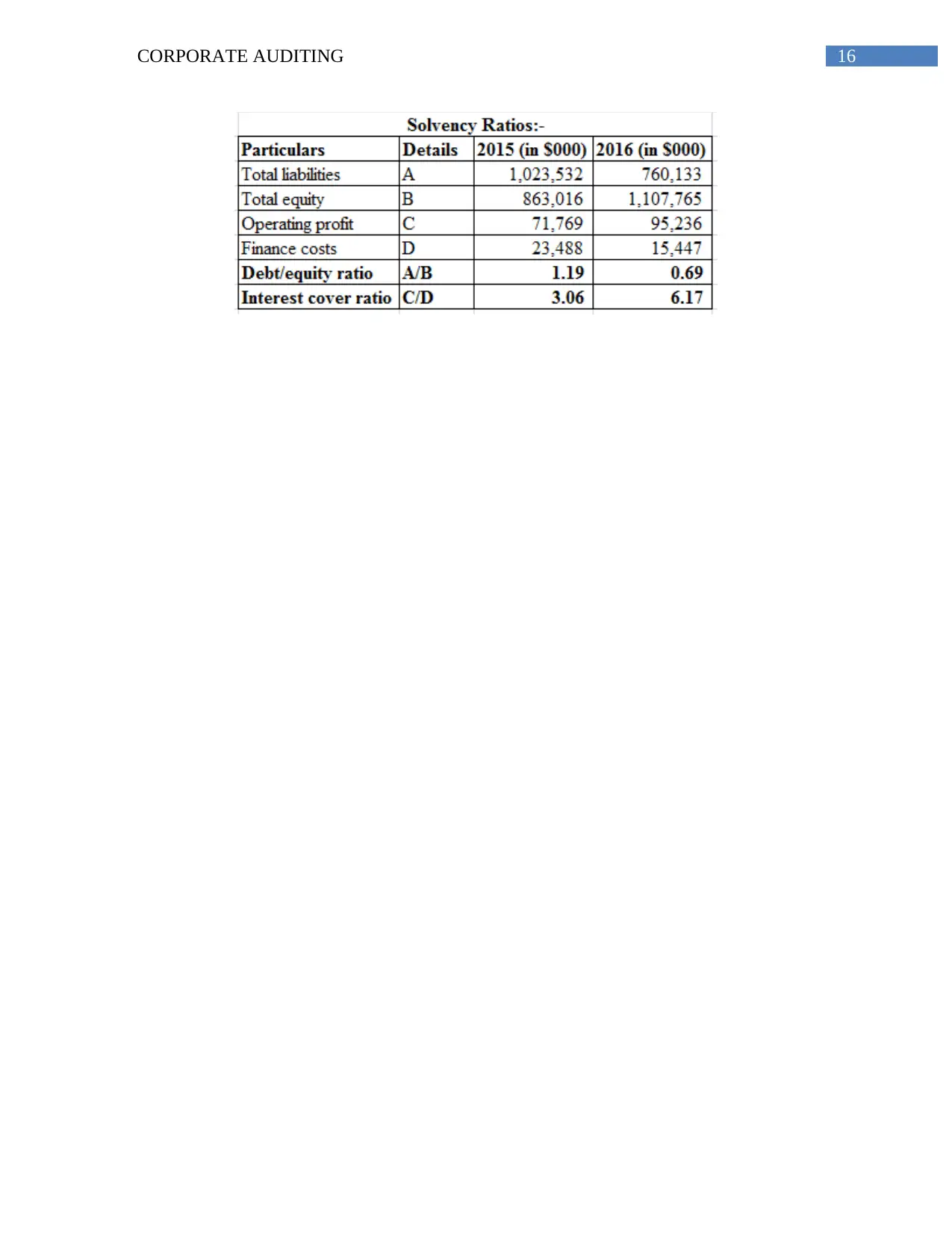

Solvency ratios:

organisation in settling its short-term dues by using its current assets (Lombardi, Bloch and

Vasarhelyi 2014). In case of Myer, current ratio is observed to decline from 1 in 2015 to 0.92 in

2016, as there has been decline in cash and cash equivalents and short-term derivative financial

instruments. On the other hand, quick ratio is deemed to be the superior measure of liquidity,

since it excludes inventories for analysing the liquidity position of an organisation (Ojala et al.

2014). This ratio has fallen as well for Myer from 0.21 in 2015 to 0.16 in 2016, which is well

below the ideal standard of 1. This is due to the fact that the organisation has undertaken

significant investment in inventories due to which it has failed to maintain adequate amount of

working capital.

Efficiency ratios:

In order to assess the efficiency position of Myer Holdings Limited, the two ratios taken

into consideration mainly include inventory turnover and receivables turnover expressed in

number of days. Inventory turnover denotes the time taken by an organisation in releasing its

inventory in a particular period (Messier Jr 2016). In case of Myer, inventory turnover has

increased marginally from 92.59 days in 2015 to 92.97 days in 2016, which implies that the

organisation has experienced a fall in product demand due to which it could not release its

inventory at a faster rate. On the other hand, receivables turnover denotes the time that an

organisation takes in obtaining due amounts from the customers. A lower timeframe is always

favourable, as it denotes quick collection of due amounts and increase in working capital (Pitt

2014). In case of Myer, receivables turnover period has increased from 4.16 days in 2015 to 4.72

days in 2016 owing to the lenient debtor policy it has adopted for accelerating sales revenue.

Solvency ratios:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AUDITING

In order to analyse the solvency position of Myer Holdings Limited, the ratios used for

conducting the same include debt/equity ratio and interest cover ratio. Debt/equity ratio denotes

the portion of debt and equity an organisation is using for funding its assets and the degree to

which it could meet creditor obligation, if there is an eventual business decline (Pizzini, Lin and

Ziegenfuss 2014). For Myer, a considerable decline in the ratio could be observed from 1.19 in

2015 to 0.69 in 2016, which has been due to significant decline in long-term borrowings and

considerable rise in contributed equity. The intention of the organisation has been to minimise its

solvency risk for balancing its poor liquidity position in the Australian market. On the other

hand, a higher interest cover ratio is always desirable, as it denotes better ability of the

organisation to settle its finance cost through increased operating income (Ratzinger-Sakel and

Schönberger 2015). The ratio has increased for Myer from 3.06 in 2015 to 6.17 in 2016, which

implies that the organisation is capable to settle its interest expense effectively because of

increased operating profit.

From the above analysis, the accounts that need further audit investigation include

inventory, supplier rebates (profitability), technology risk and refinancing and debt covenants

(solvency).

c. Inherent risks identified from business risks and analytical procedures:

The four inherent risks identified from the business risks and analytical procedures of

Myer include the following:

Inventory:

Myer held inventory amounting to $396,297,000 in 2016, which was $381,907,000 in

2015. It has been identified from its annual report that the organisation realises a provision, in

In order to analyse the solvency position of Myer Holdings Limited, the ratios used for

conducting the same include debt/equity ratio and interest cover ratio. Debt/equity ratio denotes

the portion of debt and equity an organisation is using for funding its assets and the degree to

which it could meet creditor obligation, if there is an eventual business decline (Pizzini, Lin and

Ziegenfuss 2014). For Myer, a considerable decline in the ratio could be observed from 1.19 in

2015 to 0.69 in 2016, which has been due to significant decline in long-term borrowings and

considerable rise in contributed equity. The intention of the organisation has been to minimise its

solvency risk for balancing its poor liquidity position in the Australian market. On the other

hand, a higher interest cover ratio is always desirable, as it denotes better ability of the

organisation to settle its finance cost through increased operating income (Ratzinger-Sakel and

Schönberger 2015). The ratio has increased for Myer from 3.06 in 2015 to 6.17 in 2016, which

implies that the organisation is capable to settle its interest expense effectively because of

increased operating profit.

From the above analysis, the accounts that need further audit investigation include

inventory, supplier rebates (profitability), technology risk and refinancing and debt covenants

(solvency).

c. Inherent risks identified from business risks and analytical procedures:

The four inherent risks identified from the business risks and analytical procedures of

Myer include the following:

Inventory:

Myer held inventory amounting to $396,297,000 in 2016, which was $381,907,000 in

2015. It has been identified from its annual report that the organisation realises a provision, in

8CORPORATE AUDITING

which it meets the net realisable inventory value to decline below its cost price. This policy of

Myer is subject to inherent risk, as it has to make assumptions in estimating sales through

inventory rates on hand at the end of the year to project inventory value probable to be sold

below cost in future (Simnett, Carson and Vanstraelen 2016).

Supplier rebates:

Myer realises amounts receivable from its suppliers as a minimisation in inventory

purchased and fall in cost of goods sold. This is subject to inherent risk, as the organisation

requires judgements for ascertaining supplier rebates to be realised in the income statement and

the amounts to be deferred to inventory (Ruhnke and Schmidt 2014). Thus, it needs detailed

insight of the contractual agreements with the suppliers and correct sale and purchase through

information.

Refinancing and debt structure:

There has been sudden decline in long-term borrowings to $147,273,000 in 2016

compared from $441,179,000 in 2015. Thus, it contains inherent risk with respect to cyclical

financing demands, accounting for borrowings and significance of capital in supporting the

strategy of the organisation (Soh and Martinov-Bennie 2015).

Technology risk:

Myer has implemented IT systems in place for dealing with cyber threats. However, it

needs appropriate checks to assure that it is performed in line with best practice (Vanstraelen and

Schelleman 2017).

which it meets the net realisable inventory value to decline below its cost price. This policy of

Myer is subject to inherent risk, as it has to make assumptions in estimating sales through

inventory rates on hand at the end of the year to project inventory value probable to be sold

below cost in future (Simnett, Carson and Vanstraelen 2016).

Supplier rebates:

Myer realises amounts receivable from its suppliers as a minimisation in inventory

purchased and fall in cost of goods sold. This is subject to inherent risk, as the organisation

requires judgements for ascertaining supplier rebates to be realised in the income statement and

the amounts to be deferred to inventory (Ruhnke and Schmidt 2014). Thus, it needs detailed

insight of the contractual agreements with the suppliers and correct sale and purchase through

information.

Refinancing and debt structure:

There has been sudden decline in long-term borrowings to $147,273,000 in 2016

compared from $441,179,000 in 2015. Thus, it contains inherent risk with respect to cyclical

financing demands, accounting for borrowings and significance of capital in supporting the

strategy of the organisation (Soh and Martinov-Bennie 2015).

Technology risk:

Myer has implemented IT systems in place for dealing with cyber threats. However, it

needs appropriate checks to assure that it is performed in line with best practice (Vanstraelen and

Schelleman 2017).

9CORPORATE AUDITING

d. Key account and key related assertion at risk:

From the above-identified inherent risks, the key account at risk is inventory. Since Myer

operates in the consumer products retail sector, there is changing inventory level. The

organisation has undertaken considerable amount in inventory and such investment in changing

or obsolete inventory posed significant inherent risk. Therefore, the key assertion at risk is

valuation. According to valuation assertion, it is necessary to value the balances of liabilities,

assets and equity accurately (William Jr, Glover and Prawitt 2016). Myer makes assumptions for

projecting inventory value to be sold below cost and thus, it places the valuation assertion at risk.

e. Analysis of inherent risk:

The factors affecting inventory identified as the inherent risk for Myer include the

following:

Nature of the business:

Since Myer operates in the Australian retail sector, it is highly dependent on inventory.

Hence, in the absence of desired inventory, Myer might not be able to increase its sales and as a

result, the desired profit level could not be accomplished.

Related party transactions:

Myer might be involved in related party transactions, which might raise its business

expenses and this might minimise the overall working capital base of Myer.

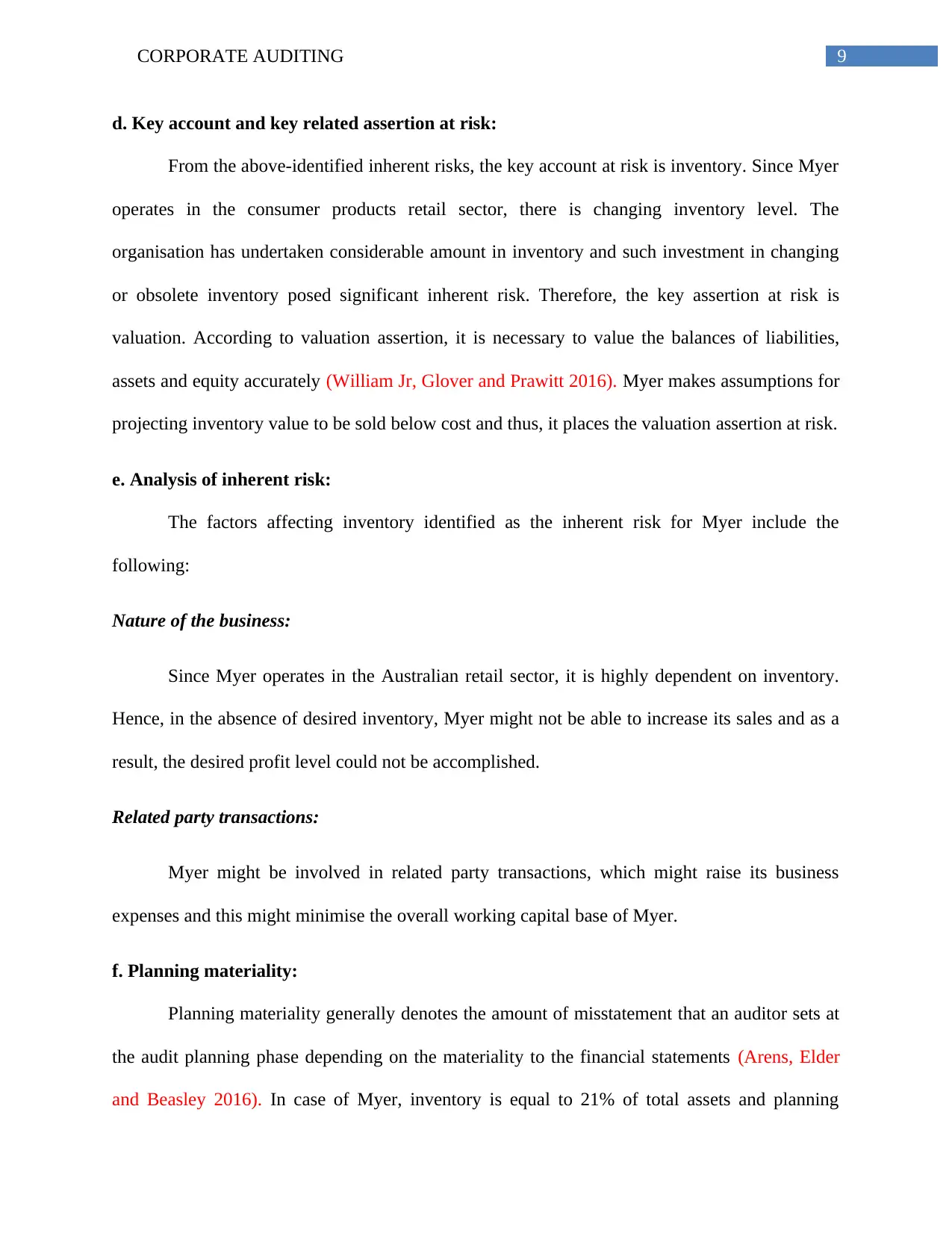

f. Planning materiality:

Planning materiality generally denotes the amount of misstatement that an auditor sets at

the audit planning phase depending on the materiality to the financial statements (Arens, Elder

and Beasley 2016). In case of Myer, inventory is equal to 21% of total assets and planning

d. Key account and key related assertion at risk:

From the above-identified inherent risks, the key account at risk is inventory. Since Myer

operates in the consumer products retail sector, there is changing inventory level. The

organisation has undertaken considerable amount in inventory and such investment in changing

or obsolete inventory posed significant inherent risk. Therefore, the key assertion at risk is

valuation. According to valuation assertion, it is necessary to value the balances of liabilities,

assets and equity accurately (William Jr, Glover and Prawitt 2016). Myer makes assumptions for

projecting inventory value to be sold below cost and thus, it places the valuation assertion at risk.

e. Analysis of inherent risk:

The factors affecting inventory identified as the inherent risk for Myer include the

following:

Nature of the business:

Since Myer operates in the Australian retail sector, it is highly dependent on inventory.

Hence, in the absence of desired inventory, Myer might not be able to increase its sales and as a

result, the desired profit level could not be accomplished.

Related party transactions:

Myer might be involved in related party transactions, which might raise its business

expenses and this might minimise the overall working capital base of Myer.

f. Planning materiality:

Planning materiality generally denotes the amount of misstatement that an auditor sets at

the audit planning phase depending on the materiality to the financial statements (Arens, Elder

and Beasley 2016). In case of Myer, inventory is equal to 21% of total assets and planning

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CORPORATE AUDITING

materiality for any asset account varies between 1% and 2% of total assets. Since inventory

comprises of a significant proportion of total assets of Myer in 2016, planning materiality for

inventory is computed as 2% of total assets. Therefore, as inventory is identified as the account

containing the highest inherent risk, the total assets are taken as base for computing materiality

amount.

materiality for any asset account varies between 1% and 2% of total assets. Since inventory

comprises of a significant proportion of total assets of Myer in 2016, planning materiality for

inventory is computed as 2% of total assets. Therefore, as inventory is identified as the account

containing the highest inherent risk, the total assets are taken as base for computing materiality

amount.

11CORPORATE AUDITING

References:

Arens, A.A., Elder, R.J. and Beasley, M.S., 2016. Auditing and Assurance Services, Global

Edition. Pearson Education Limited.

Investor.myer.com.au., 2019. [online] Available at:

http://investor.myer.com.au/FormBuilder/_Resource/_module/dGngnzELxUikQxL5gb1cgA/

file/Myer_Annual_Report_2016.pdf [Accessed 13 Apr. 2019].

Junior, R.M., Best, P.J. and Cotter, J., 2014. Sustainability reporting and assurance: a historical

analysis on a world-wide phenomenon. Journal of Business Ethics, 120(1), pp.1-11.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Knechel, W.R., 2016. Audit quality and regulation. International Journal of Auditing, 20(3),

pp.215-223.

Lenz, R. and Hahn, U., 2015. A synthesis of empirical internal audit effectiveness literature

pointing to new research opportunities. Managerial Auditing Journal, 30(1), pp.5-33.

Lombardi, D., Bloch, R. and Vasarhelyi, M., 2014. The future of audit. JISTEM-Journal of

Information Systems and Technology Management, 11(1), pp.21-32.

Messier Jr, W., 2016. Auditing & assurance services: A systematic approach. McGraw-Hill

Higher Education.

Ojala, H., Niskanen, M., Collis, J. and Pajunen, K., 2014. Audit quality and decision-making in

small companies. Managerial Auditing Journal, 29(9), pp.800-817.

References:

Arens, A.A., Elder, R.J. and Beasley, M.S., 2016. Auditing and Assurance Services, Global

Edition. Pearson Education Limited.

Investor.myer.com.au., 2019. [online] Available at:

http://investor.myer.com.au/FormBuilder/_Resource/_module/dGngnzELxUikQxL5gb1cgA/

file/Myer_Annual_Report_2016.pdf [Accessed 13 Apr. 2019].

Junior, R.M., Best, P.J. and Cotter, J., 2014. Sustainability reporting and assurance: a historical

analysis on a world-wide phenomenon. Journal of Business Ethics, 120(1), pp.1-11.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Knechel, W.R., 2016. Audit quality and regulation. International Journal of Auditing, 20(3),

pp.215-223.

Lenz, R. and Hahn, U., 2015. A synthesis of empirical internal audit effectiveness literature

pointing to new research opportunities. Managerial Auditing Journal, 30(1), pp.5-33.

Lombardi, D., Bloch, R. and Vasarhelyi, M., 2014. The future of audit. JISTEM-Journal of

Information Systems and Technology Management, 11(1), pp.21-32.

Messier Jr, W., 2016. Auditing & assurance services: A systematic approach. McGraw-Hill

Higher Education.

Ojala, H., Niskanen, M., Collis, J. and Pajunen, K., 2014. Audit quality and decision-making in

small companies. Managerial Auditing Journal, 29(9), pp.800-817.

12CORPORATE AUDITING

Pitt, S.A., 2014. Internal audit quality: Developing a quality assurance and improvement

program. John Wiley & Sons.

Pizzini, M., Lin, S. and Ziegenfuss, D.E., 2014. The impact of internal audit function quality and

contribution on audit delay. Auditing: A Journal of Practice & Theory, 34(1), pp.25-58.

Ratzinger-Sakel, N.V. and Schönberger, M.W., 2015. Restricting non-audit services in Europe–

the potential (lack of) impact of a blacklist and a fee cap on auditor independence and audit

quality. Accounting in Europe, 12(1), pp.61-86.

Ruhnke, K. and Schmidt, M., 2014. The audit expectation gap: existence, causes, and the impact

of changes. Accounting and Business research, 44(5), pp.572-601.

Simnett, R., Carson, E. and Vanstraelen, A., 2016. International archival auditing and assurance

research: Trends, methodological issues, and opportunities. Auditing: A Journal of Practice &

Theory, 35(3), pp.1-32.

Soh, D.S. and Martinov-Bennie, N., 2015. Internal auditors’ perceptions of their role in

environmental, social and governance assurance and consulting. Managerial Auditing

Journal, 30(1), pp.80-111.

Vanstraelen, A. and Schelleman, C., 2017. Auditing private companies: what do we

know?. Accounting and Business Research, 47(5), pp.565-584.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Pitt, S.A., 2014. Internal audit quality: Developing a quality assurance and improvement

program. John Wiley & Sons.

Pizzini, M., Lin, S. and Ziegenfuss, D.E., 2014. The impact of internal audit function quality and

contribution on audit delay. Auditing: A Journal of Practice & Theory, 34(1), pp.25-58.

Ratzinger-Sakel, N.V. and Schönberger, M.W., 2015. Restricting non-audit services in Europe–

the potential (lack of) impact of a blacklist and a fee cap on auditor independence and audit

quality. Accounting in Europe, 12(1), pp.61-86.

Ruhnke, K. and Schmidt, M., 2014. The audit expectation gap: existence, causes, and the impact

of changes. Accounting and Business research, 44(5), pp.572-601.

Simnett, R., Carson, E. and Vanstraelen, A., 2016. International archival auditing and assurance

research: Trends, methodological issues, and opportunities. Auditing: A Journal of Practice &

Theory, 35(3), pp.1-32.

Soh, D.S. and Martinov-Bennie, N., 2015. Internal auditors’ perceptions of their role in

environmental, social and governance assurance and consulting. Managerial Auditing

Journal, 30(1), pp.80-111.

Vanstraelen, A. and Schelleman, C., 2017. Auditing private companies: what do we

know?. Accounting and Business Research, 47(5), pp.565-584.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13CORPORATE AUDITING

Appendices:

Appendix 1: Horizontal analysis of the financial statements of Myer Limited for the years

2015 and 2016

Appendices:

Appendix 1: Horizontal analysis of the financial statements of Myer Limited for the years

2015 and 2016

14CORPORATE AUDITING

15CORPORATE AUDITING

Appendix 2: Ratio analysis of Myer Limited for the years 2015 and 2016

Appendix 2: Ratio analysis of Myer Limited for the years 2015 and 2016

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16CORPORATE AUDITING

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.