Corporate Business Accounting Report

VerifiedAdded on 2022/09/01

|13

|3948

|19

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author note:

Corporate Accounting

Name of the Student:

Name of the University:

Author note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

CORPORATE ACCOUNTING

Executive Summary:

The main purpose of the analysis is conduct a review on the reporting process which

is followed by the business of Rio Tinto Ltd and BHP Billiton Ltd. The reporting

process highlights the capital structure which is used by both the companies for

financing the operations of the business. The assessment also shows the changes

which has taken place in the capital structure of the business and how the same is

related to the risks of the business. The analysis also shows assets and liabilities of

the business considering the reported items which are presented in the financial

statements of the business. The analysis also shows whether the business utilizes

AASB 137 in the reporting of contingent assets and liabilities of the business.

CORPORATE ACCOUNTING

Executive Summary:

The main purpose of the analysis is conduct a review on the reporting process which

is followed by the business of Rio Tinto Ltd and BHP Billiton Ltd. The reporting

process highlights the capital structure which is used by both the companies for

financing the operations of the business. The assessment also shows the changes

which has taken place in the capital structure of the business and how the same is

related to the risks of the business. The analysis also shows assets and liabilities of

the business considering the reported items which are presented in the financial

statements of the business. The analysis also shows whether the business utilizes

AASB 137 in the reporting of contingent assets and liabilities of the business.

2

CORPORATE ACCOUNTING

Table of Contents

Introduction:..................................................................................................................4

DISCUSSION:..............................................................................................................4

Rio Tinto:.......................................................................................................................4

Portfolio:....................................................................................................................4

Financial Performance:.............................................................................................4

(i) Different sources of fund:.......................................................................................4

(ii) Evolution of Sources of Fund:............................................................................5

Share Capital:...........................................................................................................5

Merits:........................................................................................................................5

Shortcomings:...........................................................................................................5

Reserves:..................................................................................................................5

Merits:........................................................................................................................5

Shortcomings:...........................................................................................................5

Retained Earnings:....................................................................................................5

Merits:........................................................................................................................5

Demerits:...................................................................................................................5

(iii) Brief About Different Types of Liabilities:...........................................................6

Current Liabilities:.....................................................................................................6

Non-Current Liabilities:.............................................................................................6

Borrowings and other financial liabilities:..................................................................6

Trade and other payables:........................................................................................6

Tax payable:..............................................................................................................6

Deferred tax liabilities:...............................................................................................6

Provisions including post-retirement benefit:............................................................6

(iv) Key Provisions Under AASB 137 ‘Provisions, Contingent Liabilities and

Contingent Assets’........................................................................................................7

(v) Different Types of Assets shown in the Balance Sheet:....................................7

(vi) Basis of measurement to evaluate each asset:..................................................7

BHP Billiton...................................................................................................................8

Portfolio:....................................................................................................................8

Performance:.............................................................................................................8

(i) Different sources of fund:.......................................................................................8

(ii) Evolution of Sources of Fund:............................................................................8

Share capital Buyback programmes:........................................................................8

Reserves:..................................................................................................................9

CORPORATE ACCOUNTING

Table of Contents

Introduction:..................................................................................................................4

DISCUSSION:..............................................................................................................4

Rio Tinto:.......................................................................................................................4

Portfolio:....................................................................................................................4

Financial Performance:.............................................................................................4

(i) Different sources of fund:.......................................................................................4

(ii) Evolution of Sources of Fund:............................................................................5

Share Capital:...........................................................................................................5

Merits:........................................................................................................................5

Shortcomings:...........................................................................................................5

Reserves:..................................................................................................................5

Merits:........................................................................................................................5

Shortcomings:...........................................................................................................5

Retained Earnings:....................................................................................................5

Merits:........................................................................................................................5

Demerits:...................................................................................................................5

(iii) Brief About Different Types of Liabilities:...........................................................6

Current Liabilities:.....................................................................................................6

Non-Current Liabilities:.............................................................................................6

Borrowings and other financial liabilities:..................................................................6

Trade and other payables:........................................................................................6

Tax payable:..............................................................................................................6

Deferred tax liabilities:...............................................................................................6

Provisions including post-retirement benefit:............................................................6

(iv) Key Provisions Under AASB 137 ‘Provisions, Contingent Liabilities and

Contingent Assets’........................................................................................................7

(v) Different Types of Assets shown in the Balance Sheet:....................................7

(vi) Basis of measurement to evaluate each asset:..................................................7

BHP Billiton...................................................................................................................8

Portfolio:....................................................................................................................8

Performance:.............................................................................................................8

(i) Different sources of fund:.......................................................................................8

(ii) Evolution of Sources of Fund:............................................................................8

Share capital Buyback programmes:........................................................................8

Reserves:..................................................................................................................9

3

CORPORATE ACCOUNTING

Impact on Financial Reporting:.................................................................................9

Retained Earnings:....................................................................................................9

(iii) Merits and Demerits of the selected funds:.....................................................9

(iv) Different types of liabilities:..............................................................................9

(vi) Different types of assets:...............................................................................11

(vii) Basis of measurement of each asset:...........................................................11

Conclusion..................................................................................................................11

Reference...................................................................................................................12

CORPORATE ACCOUNTING

Impact on Financial Reporting:.................................................................................9

Retained Earnings:....................................................................................................9

(iii) Merits and Demerits of the selected funds:.....................................................9

(iv) Different types of liabilities:..............................................................................9

(vi) Different types of assets:...............................................................................11

(vii) Basis of measurement of each asset:...........................................................11

Conclusion..................................................................................................................11

Reference...................................................................................................................12

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

CORPORATE ACCOUNTING

Introduction:

Corporate accounting deals with some process such as the preparation of

cash flow statements, financial records, balance sheets and more about financials of

the company. The company can use such an accounting technique called as

corporate accounting to control the business process very uniquely like absorption,

amalgamation and creation of consolidated documents. Corporate accounting is also

performed to confirm the activities which are of financial nature rely on the laws and

legislations which are stipulated. It also refers that the activities of a entity follow with

the tune of organizational policies (Barker and Schulte 2017). It usually performs

much of their work internally. They generate reports which help to take strategic

decision by the management.

This study takes two companies, namely Rio Tinto Limited and BHP Billiton

Limited to compare their annual report to examine and identify the different sources

of funds, liabilities and different categories of assets.

DISCUSSION:

The study depicts the examination and evaluation of financial statements of

both companies like Rio Tinto and BHP Billiton as follows:

Rio Tinto:

Rio Tinto is regarded as one of the legal mineral extraction companies which

has its operations settled in Australia and is well recognized in the mining industry.

The foundation of the company was set in 1873 and it was listed the same with the

ASX.

Portfolio:

The company has an objective to make investments in the growth and

development of a project which can add further values. They have finished the

Amrun project which was initiated in Queensland, Australia in a very low cash outlay.

In November they have approved the expansion of the $6.2 billion project which

focused on extraction of iron ores in Pilbara for achieving more revenues. Continuing

to reshape their portfolio the company has enhance their development projects for

the combine sale value of $4.15 billion and acquired more mines so that the

company is able to generate more revenues (Riotinto.com. 2020).

Financial Performance:

During 2018, the company generated earnings of $8.8 billion which is bit more

that 2017 was $8.6 billion. Although some volatility commodity price remained helpful

but the development was delayed and have shown inflationary pressure in some of

their products. The EBIDTA margin of 42% as compared to 44% in 2017.

(i) Different sources of fund:

The company has used different types of funds to operate its business activities.

In the matter of equity, the company has utilised the share capital of $211, which

was reduced from $220. More precisely, the company issued ordinary shares at 1st

January of 1351.609 numbers valued of $220 million during the time the company

has repurchased the shares 63.984 million numbers valued of $9 million which

comes down to $211 million. The company also raised capital through the issue of

shares from treasury and the public as well so the total share capital was 1287.660.

Reserve was $8661 million (Schaltegger, Etxeberria and Ortas 2017). The company

CORPORATE ACCOUNTING

Introduction:

Corporate accounting deals with some process such as the preparation of

cash flow statements, financial records, balance sheets and more about financials of

the company. The company can use such an accounting technique called as

corporate accounting to control the business process very uniquely like absorption,

amalgamation and creation of consolidated documents. Corporate accounting is also

performed to confirm the activities which are of financial nature rely on the laws and

legislations which are stipulated. It also refers that the activities of a entity follow with

the tune of organizational policies (Barker and Schulte 2017). It usually performs

much of their work internally. They generate reports which help to take strategic

decision by the management.

This study takes two companies, namely Rio Tinto Limited and BHP Billiton

Limited to compare their annual report to examine and identify the different sources

of funds, liabilities and different categories of assets.

DISCUSSION:

The study depicts the examination and evaluation of financial statements of

both companies like Rio Tinto and BHP Billiton as follows:

Rio Tinto:

Rio Tinto is regarded as one of the legal mineral extraction companies which

has its operations settled in Australia and is well recognized in the mining industry.

The foundation of the company was set in 1873 and it was listed the same with the

ASX.

Portfolio:

The company has an objective to make investments in the growth and

development of a project which can add further values. They have finished the

Amrun project which was initiated in Queensland, Australia in a very low cash outlay.

In November they have approved the expansion of the $6.2 billion project which

focused on extraction of iron ores in Pilbara for achieving more revenues. Continuing

to reshape their portfolio the company has enhance their development projects for

the combine sale value of $4.15 billion and acquired more mines so that the

company is able to generate more revenues (Riotinto.com. 2020).

Financial Performance:

During 2018, the company generated earnings of $8.8 billion which is bit more

that 2017 was $8.6 billion. Although some volatility commodity price remained helpful

but the development was delayed and have shown inflationary pressure in some of

their products. The EBIDTA margin of 42% as compared to 44% in 2017.

(i) Different sources of fund:

The company has used different types of funds to operate its business activities.

In the matter of equity, the company has utilised the share capital of $211, which

was reduced from $220. More precisely, the company issued ordinary shares at 1st

January of 1351.609 numbers valued of $220 million during the time the company

has repurchased the shares 63.984 million numbers valued of $9 million which

comes down to $211 million. The company also raised capital through the issue of

shares from treasury and the public as well so the total share capital was 1287.660.

Reserve was $8661 million (Schaltegger, Etxeberria and Ortas 2017). The company

5

CORPORATE ACCOUNTING

also took long term borrowings and other financial liabilities of $12847 million. So,

after sum up, all the financial data the financial statements depicts that total equity is

$49823 million in 2018 which was $51115 million in 2017 and borrowings they have

taken less in comparison to 2017 which was $15148 million.

(ii) Evolution of Sources of Fund:

In 2016 share capital was $224 million, in 2017 $220 million and in 2018 is $211

million so it can be said the company is trying to reduce the share capital gradually

through buyback of shares. Retained earnings in 2016 was $21613 million, in 2017 it

was $23761 million and in 2018 the retained earnings were $27025 million, so the

company is more focusing on the retained earnings over the years. Share premium

account also increased over the years of $4304 million, $4306 million and $4312

million in 2016, 2017 and 2018 respectively. Reserves decreased from $9216 million

to $8661 million over the years. Looking upon the long term borrowings in 2016,

which was $17470 million, in 2017 $15148 million and in 2018 is $12847 million.

Company is paying off the borrowings gradually.

Share Capital:

Merits:

Dividend: It is entitled to receive to investors. One of the primary sources from

the investment

Capital Gain: Other sources of return on investment arising from the market.

Liquidity: Company shares which is listed on the stock exchange have liquidity

benefit.

Exercise Control: By investing in the company’s shares, the shareholders get

ownership; thus, they can get exercise control.

Shortcomings:

Risk: The investment in share capital is riskier than any other investment.

Market Volatility: Often fluctuate the market price because of volatility in the

market.

Reserves:

Merits:

To Improve the Financial Position

To Expand Business

To Overcome Future Loss

To Distribute Dividend

Shortcomings:

True Condition Not Disclosed

Problem of Loan In Crises

Insurance Claim Problem

Retained Earnings:

Merits:

Cheaper Source of Financing

Financial Stability

Stable Dividend

Demerits:

Improper Utilization of Funds

CORPORATE ACCOUNTING

also took long term borrowings and other financial liabilities of $12847 million. So,

after sum up, all the financial data the financial statements depicts that total equity is

$49823 million in 2018 which was $51115 million in 2017 and borrowings they have

taken less in comparison to 2017 which was $15148 million.

(ii) Evolution of Sources of Fund:

In 2016 share capital was $224 million, in 2017 $220 million and in 2018 is $211

million so it can be said the company is trying to reduce the share capital gradually

through buyback of shares. Retained earnings in 2016 was $21613 million, in 2017 it

was $23761 million and in 2018 the retained earnings were $27025 million, so the

company is more focusing on the retained earnings over the years. Share premium

account also increased over the years of $4304 million, $4306 million and $4312

million in 2016, 2017 and 2018 respectively. Reserves decreased from $9216 million

to $8661 million over the years. Looking upon the long term borrowings in 2016,

which was $17470 million, in 2017 $15148 million and in 2018 is $12847 million.

Company is paying off the borrowings gradually.

Share Capital:

Merits:

Dividend: It is entitled to receive to investors. One of the primary sources from

the investment

Capital Gain: Other sources of return on investment arising from the market.

Liquidity: Company shares which is listed on the stock exchange have liquidity

benefit.

Exercise Control: By investing in the company’s shares, the shareholders get

ownership; thus, they can get exercise control.

Shortcomings:

Risk: The investment in share capital is riskier than any other investment.

Market Volatility: Often fluctuate the market price because of volatility in the

market.

Reserves:

Merits:

To Improve the Financial Position

To Expand Business

To Overcome Future Loss

To Distribute Dividend

Shortcomings:

True Condition Not Disclosed

Problem of Loan In Crises

Insurance Claim Problem

Retained Earnings:

Merits:

Cheaper Source of Financing

Financial Stability

Stable Dividend

Demerits:

Improper Utilization of Funds

6

CORPORATE ACCOUNTING

Over-capitalization

Lower Rate of Dividend

(iii) Brief About Different Types of Liabilities:

This study critically examines the financial statement from which the balance

sheet shows some current liabilities and non-current liabilities. Under current

liabilities, there are Borrowings and other financial liabilities, Trade and other

payables, Tax payable, Provisions including post-retirement benefits (Raiborn and

Sivitanides 2015). Under non-current liabilities, there are also Borrowings and other

financial liabilities and several other liabilities which includes trade payables

prominently.

Current Liabilities:

It is an obligation that will due within one year of the date of the company’s

balance sheet. The amount of money that would pay off within a year.

Non-Current Liabilities:

Non-current liabilities are those obligations which are not due for settlement

within one year. It is posted separately in the balance sheet.

Current liability and non-current liability further illustrate their category, which

is discussed as follows:

Borrowings and other financial liabilities:

Borrowings in a simple term is a loan taken by the entity for its business activities.

It is for short term and long term purpose also. Financial liabilities for business are

like credit cards of an individual. It includes debt payable and interest payable.

Rio Tinto has borrowings and other financial liabilities of $12847 million during

2018 which is less as compared to 2017 of $15148 million under non-current

liabilities. So it indicates that the company took a loan for long term purpose

also for short term purpose they have taken loan of $1073 million which came

under current liabilities. That needs to be paid off within one financial year.

Rio Tinto has a European Debt Insurance Programme of $10 billion.

The group’s borrowings of $12.8 billion which was due to borrowings which

was made by subsidiary entities of Rio Tinto

Trade and other payables:

This liability is an obligation to pay which have been accumulated from

suppliers in the operations of the business. Trade payables are classified as current

liabilities and also non-current liabilities.

Looking into the balance sheet, it can easily depict that the company reduced

the figure than the previous in the short term and long term purpose as well. Under

current liability, it is $6600 million and under non-current liability, it is $841

Tax payable:

Tax payable is a term that shows the liability of a business organization where

it is owed to the local government based on the profitability during a given period.

Deferred tax liabilities:

It is an amount of tax that is assessed or is due for the recent period has not

yet been paid. It arises from the timing difference when the tax is due and when the

tax is being paid.

Provisions including post-retirement benefit:

The amount keeps aside from the emtity’s earnings to cover an expected

liability or in the fall in the value of an asset regardless that exact amount is

CORPORATE ACCOUNTING

Over-capitalization

Lower Rate of Dividend

(iii) Brief About Different Types of Liabilities:

This study critically examines the financial statement from which the balance

sheet shows some current liabilities and non-current liabilities. Under current

liabilities, there are Borrowings and other financial liabilities, Trade and other

payables, Tax payable, Provisions including post-retirement benefits (Raiborn and

Sivitanides 2015). Under non-current liabilities, there are also Borrowings and other

financial liabilities and several other liabilities which includes trade payables

prominently.

Current Liabilities:

It is an obligation that will due within one year of the date of the company’s

balance sheet. The amount of money that would pay off within a year.

Non-Current Liabilities:

Non-current liabilities are those obligations which are not due for settlement

within one year. It is posted separately in the balance sheet.

Current liability and non-current liability further illustrate their category, which

is discussed as follows:

Borrowings and other financial liabilities:

Borrowings in a simple term is a loan taken by the entity for its business activities.

It is for short term and long term purpose also. Financial liabilities for business are

like credit cards of an individual. It includes debt payable and interest payable.

Rio Tinto has borrowings and other financial liabilities of $12847 million during

2018 which is less as compared to 2017 of $15148 million under non-current

liabilities. So it indicates that the company took a loan for long term purpose

also for short term purpose they have taken loan of $1073 million which came

under current liabilities. That needs to be paid off within one financial year.

Rio Tinto has a European Debt Insurance Programme of $10 billion.

The group’s borrowings of $12.8 billion which was due to borrowings which

was made by subsidiary entities of Rio Tinto

Trade and other payables:

This liability is an obligation to pay which have been accumulated from

suppliers in the operations of the business. Trade payables are classified as current

liabilities and also non-current liabilities.

Looking into the balance sheet, it can easily depict that the company reduced

the figure than the previous in the short term and long term purpose as well. Under

current liability, it is $6600 million and under non-current liability, it is $841

Tax payable:

Tax payable is a term that shows the liability of a business organization where

it is owed to the local government based on the profitability during a given period.

Deferred tax liabilities:

It is an amount of tax that is assessed or is due for the recent period has not

yet been paid. It arises from the timing difference when the tax is due and when the

tax is being paid.

Provisions including post-retirement benefit:

The amount keeps aside from the emtity’s earnings to cover an expected

liability or in the fall in the value of an asset regardless that exact amount is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

unknown. The post-retirement benefit is those who have served to achieve a lifetime

benefit for themselves. This amount is accumulated for the years and the amount will

be given to the employee at the time of retirement.

Under current liabilities, it is $1056 million for the year 2018 and the as non-

current liabilities it is $12 552 million. Both the figure has reduced than previous.

The liabilities, which leads to interest as follows:

Financial liabilities at amortized cost and associated derivatives

Finance leases

The liabilities, which do not bear the interest as follows:

Tax Payable

Deferred tax liabilities

Provision

(iv) Key Provisions Under AASB 137 ‘Provisions, Contingent

Liabilities and Contingent Assets’

As per AASB 137 Provisions, Contingent Liabilities and Contingent Assets

defines present obligations of the entity arising from past events. A contingent

liability is an liability that arises from events of pasts and it will come to existence by

the occurrence and non-occurrence of one or more uncertain future events.

Contingent assets are also defined only when then future events will happen.

As the company’s report suggests, that the management has decided to rely on

its onerous lease assessment under AASB 137 “Provision, Contingent Liabilities,

Contingent Assets” as on 31st December 2018 permitted by IFRS 16, as a

convenient under the costs which cannot be avoided or expenses of certain

obligations involved in the contract which exceeds benefits of the same. Provisions

are created by management for appropriately preparing for some losses which the

business might attract in future.

(v) Different Types of Assets shown in the Balance Sheet:

The study examines all types of assets that being recorded by the company is as

follows:

Non-Current Assets Current Assets

Goodwill Inventories

Intangible Assets Trade and other receivables

Property, plant and equipment Tax recoverable

Equity investment Other financial assets

Inventories Cash and cash equivalents

Deferred tax assets

Trade and other receivables

Tax Recoverable

Other financial assets

(vi) Basis of measurement to evaluate each asset:

Goodwill = (Consideration paid + Fair value of non-controlling interests + Fair value

of equity interests) – Fair value of net identifiable assets

Cost of inventories must be measured using either,

CORPORATE ACCOUNTING

unknown. The post-retirement benefit is those who have served to achieve a lifetime

benefit for themselves. This amount is accumulated for the years and the amount will

be given to the employee at the time of retirement.

Under current liabilities, it is $1056 million for the year 2018 and the as non-

current liabilities it is $12 552 million. Both the figure has reduced than previous.

The liabilities, which leads to interest as follows:

Financial liabilities at amortized cost and associated derivatives

Finance leases

The liabilities, which do not bear the interest as follows:

Tax Payable

Deferred tax liabilities

Provision

(iv) Key Provisions Under AASB 137 ‘Provisions, Contingent

Liabilities and Contingent Assets’

As per AASB 137 Provisions, Contingent Liabilities and Contingent Assets

defines present obligations of the entity arising from past events. A contingent

liability is an liability that arises from events of pasts and it will come to existence by

the occurrence and non-occurrence of one or more uncertain future events.

Contingent assets are also defined only when then future events will happen.

As the company’s report suggests, that the management has decided to rely on

its onerous lease assessment under AASB 137 “Provision, Contingent Liabilities,

Contingent Assets” as on 31st December 2018 permitted by IFRS 16, as a

convenient under the costs which cannot be avoided or expenses of certain

obligations involved in the contract which exceeds benefits of the same. Provisions

are created by management for appropriately preparing for some losses which the

business might attract in future.

(v) Different Types of Assets shown in the Balance Sheet:

The study examines all types of assets that being recorded by the company is as

follows:

Non-Current Assets Current Assets

Goodwill Inventories

Intangible Assets Trade and other receivables

Property, plant and equipment Tax recoverable

Equity investment Other financial assets

Inventories Cash and cash equivalents

Deferred tax assets

Trade and other receivables

Tax Recoverable

Other financial assets

(vi) Basis of measurement to evaluate each asset:

Goodwill = (Consideration paid + Fair value of non-controlling interests + Fair value

of equity interests) – Fair value of net identifiable assets

Cost of inventories must be measured using either,

8

CORPORATE ACCOUNTING

FIFO method (First-in, First-out method)

Weighted-average cost (WAC) method

The calculation of Inventory purchase is:

(Closing balance – Opening balance)+ Cost of goods sold= Inventory purchase

Deferred Tax assets= Temporary difference x Tax rate

BHP Billiton

BHP, previously called as BHP Billiton, is a treading enterprise of BHP Group

Limited, an Anglo- Australian multinational mining, metals and petroleum. Listed on

Australian Securities Exchange (ASX). Headquartered in Melbourne, Victoria,

Australia. It was founded in 1885. By 2017 BHP ranked world’s largest mining

company based on market capitalization (Bhp.com. 2020).

Portfolio:

It has been around for 133 years with a total economic contribution of $33.9

billion. It operates,

Evaluation and exploration

Development

Extraction and processing

Rehabilitation and closure

Performance:

The company’s KPIs enable to measure developmental practices of the

business and also the financial performance of the same. While valuing the key

performance, there should be two categories of financial key performance and non-

financial key performance.

The financial key performance suggests that underlying attributable profit,

underlying EBIDTA, Net operating cash flows. Whereas the measurement of non-

financial key performance indicates total shareholder return, Long-term credit rating,

total recovery injury frequency.

(i) Different sources of fund:

After analysing the financial statement, the company used various sources like

share capital, reserves, retained earnings. The company has $1186 million of share

capital, reserves $2290 million, retained earnings $51064 million during 2018. The

company keeps the equity share remain the same over the two years in 2018 and

2017, respectively. But the company slightly reduce the level of its reserves and

retained earnings. In 2017 reserve was $2400 million but in 2018 the reserve is

$2290 million. Looking into the retained earnings of the company in 2017 it was

$52618 million and in 2018 retained earnings is $51064 million.

(ii) Evolution of Sources of Fund:

BHP Billiton kept the share capital figure the same as the previous year that is

$1186 million in 2018 and 2017 respectively. So, it can be easily depicted that there

was no buyback happen.

The share buy-back reserve represents the reserve which is created from the

shares which have been cancelled by the company during the period.

Share capital Buyback programmes:

At the AGM held in 2016 and 2017, BHP Billiton’s shares have been

authorised to the shareholders to make the market cap up to 211,207,180 of its

CORPORATE ACCOUNTING

FIFO method (First-in, First-out method)

Weighted-average cost (WAC) method

The calculation of Inventory purchase is:

(Closing balance – Opening balance)+ Cost of goods sold= Inventory purchase

Deferred Tax assets= Temporary difference x Tax rate

BHP Billiton

BHP, previously called as BHP Billiton, is a treading enterprise of BHP Group

Limited, an Anglo- Australian multinational mining, metals and petroleum. Listed on

Australian Securities Exchange (ASX). Headquartered in Melbourne, Victoria,

Australia. It was founded in 1885. By 2017 BHP ranked world’s largest mining

company based on market capitalization (Bhp.com. 2020).

Portfolio:

It has been around for 133 years with a total economic contribution of $33.9

billion. It operates,

Evaluation and exploration

Development

Extraction and processing

Rehabilitation and closure

Performance:

The company’s KPIs enable to measure developmental practices of the

business and also the financial performance of the same. While valuing the key

performance, there should be two categories of financial key performance and non-

financial key performance.

The financial key performance suggests that underlying attributable profit,

underlying EBIDTA, Net operating cash flows. Whereas the measurement of non-

financial key performance indicates total shareholder return, Long-term credit rating,

total recovery injury frequency.

(i) Different sources of fund:

After analysing the financial statement, the company used various sources like

share capital, reserves, retained earnings. The company has $1186 million of share

capital, reserves $2290 million, retained earnings $51064 million during 2018. The

company keeps the equity share remain the same over the two years in 2018 and

2017, respectively. But the company slightly reduce the level of its reserves and

retained earnings. In 2017 reserve was $2400 million but in 2018 the reserve is

$2290 million. Looking into the retained earnings of the company in 2017 it was

$52618 million and in 2018 retained earnings is $51064 million.

(ii) Evolution of Sources of Fund:

BHP Billiton kept the share capital figure the same as the previous year that is

$1186 million in 2018 and 2017 respectively. So, it can be easily depicted that there

was no buyback happen.

The share buy-back reserve represents the reserve which is created from the

shares which have been cancelled by the company during the period.

Share capital Buyback programmes:

At the AGM held in 2016 and 2017, BHP Billiton’s shares have been

authorised to the shareholders to make the market cap up to 211,207,180 of its

9

CORPORATE ACCOUNTING

ordinary shares, which represents 10 per cent of BHP Billiton Plc’s. During the

financial year 2018, the company did not purchase any shares which is related to

BHP Billiton Limited or BHP Billiton Plc through the share buyback programme.

However, BHP expects some returns to the shareholders from their sale proceeds.

Reserves:

Reserves are measured the amount of product that is extracted by

economically and legally from the Group’s properties (Killian and O'Regan 2016).

The company used Foreign currency translation reserve, and different types of

reserves as represented in the financial statements of the business..

Impact on Financial Reporting:

Reserves calculation may vary from time-to-time as the economic factor used

to improve, and additional geological data is gathered during operations (Cheng,

Ioannou and Serafeim 2014). Factor changes in reserves may affect the Group’s

financial results and financial position in several ways:

Retained Earnings:

The study suggests that any difference between the carrying amount and the

consideration if reissued is recognised in retained earnings. As of 30th July 2018, the

company’s retained earning’s stood at $51064 million.

(iii) Merits and Demerits of the selected funds:

Merits Demerits

Share Capital Raising capital via the

sale of shares through

public

No repayment

requirement

It does not require interest

payment but typically has

a greater cost

Takes time to get a loan

Reserves Source of power

Financial Stability build-up

Fair condition do not

expose

Claiming of insurance

would face a problem.

Retained Earnings It has declared a stable

dividend

Strengthen the market

value

Conservative dividend

policy leads to high

accumulated retrained

earnings

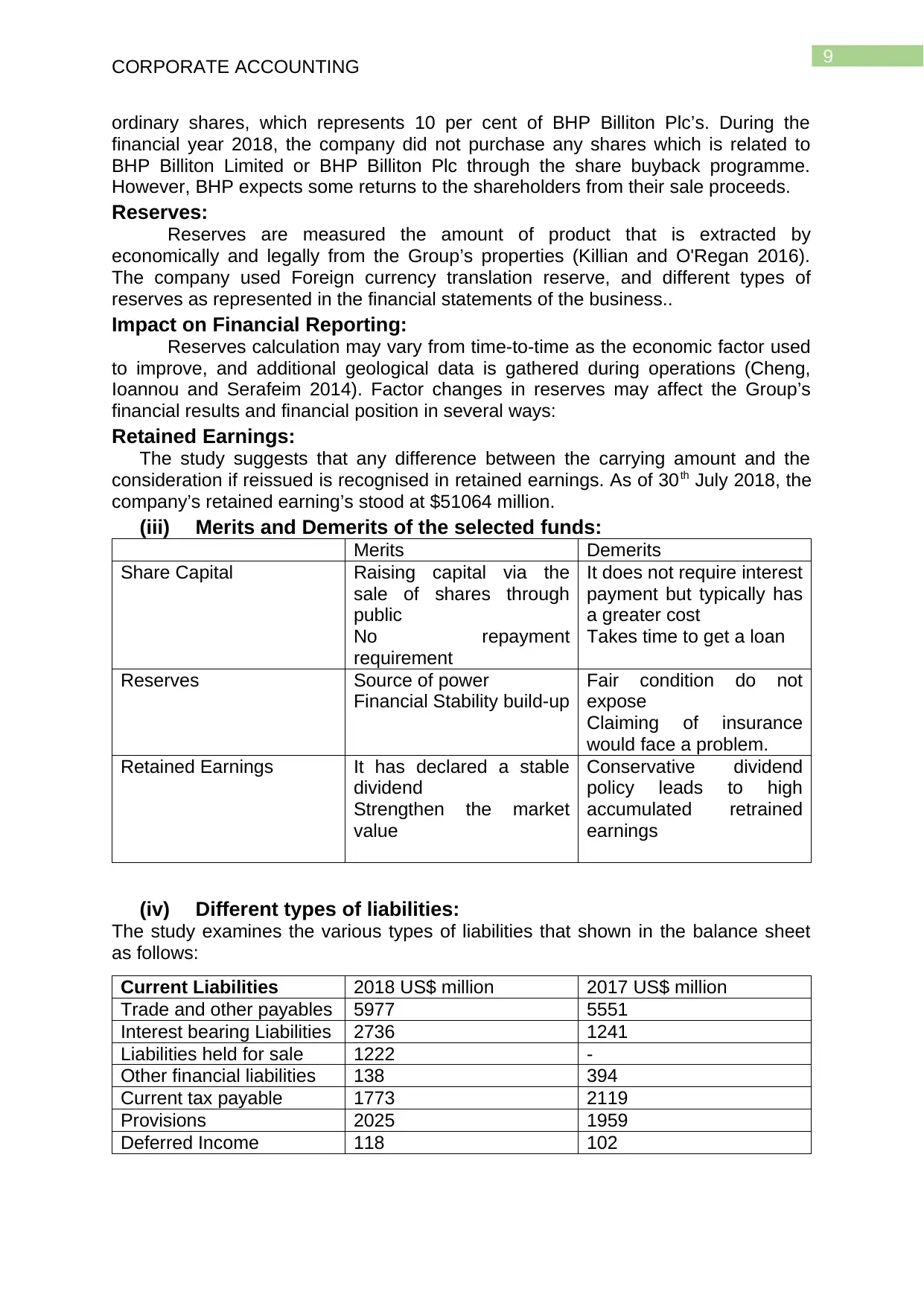

(iv) Different types of liabilities:

The study examines the various types of liabilities that shown in the balance sheet

as follows:

Current Liabilities 2018 US$ million 2017 US$ million

Trade and other payables 5977 5551

Interest bearing Liabilities 2736 1241

Liabilities held for sale 1222 -

Other financial liabilities 138 394

Current tax payable 1773 2119

Provisions 2025 1959

Deferred Income 118 102

CORPORATE ACCOUNTING

ordinary shares, which represents 10 per cent of BHP Billiton Plc’s. During the

financial year 2018, the company did not purchase any shares which is related to

BHP Billiton Limited or BHP Billiton Plc through the share buyback programme.

However, BHP expects some returns to the shareholders from their sale proceeds.

Reserves:

Reserves are measured the amount of product that is extracted by

economically and legally from the Group’s properties (Killian and O'Regan 2016).

The company used Foreign currency translation reserve, and different types of

reserves as represented in the financial statements of the business..

Impact on Financial Reporting:

Reserves calculation may vary from time-to-time as the economic factor used

to improve, and additional geological data is gathered during operations (Cheng,

Ioannou and Serafeim 2014). Factor changes in reserves may affect the Group’s

financial results and financial position in several ways:

Retained Earnings:

The study suggests that any difference between the carrying amount and the

consideration if reissued is recognised in retained earnings. As of 30th July 2018, the

company’s retained earning’s stood at $51064 million.

(iii) Merits and Demerits of the selected funds:

Merits Demerits

Share Capital Raising capital via the

sale of shares through

public

No repayment

requirement

It does not require interest

payment but typically has

a greater cost

Takes time to get a loan

Reserves Source of power

Financial Stability build-up

Fair condition do not

expose

Claiming of insurance

would face a problem.

Retained Earnings It has declared a stable

dividend

Strengthen the market

value

Conservative dividend

policy leads to high

accumulated retrained

earnings

(iv) Different types of liabilities:

The study examines the various types of liabilities that shown in the balance sheet

as follows:

Current Liabilities 2018 US$ million 2017 US$ million

Trade and other payables 5977 5551

Interest bearing Liabilities 2736 1241

Liabilities held for sale 1222 -

Other financial liabilities 138 394

Current tax payable 1773 2119

Provisions 2025 1959

Deferred Income 118 102

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

CORPORATE ACCOUNTING

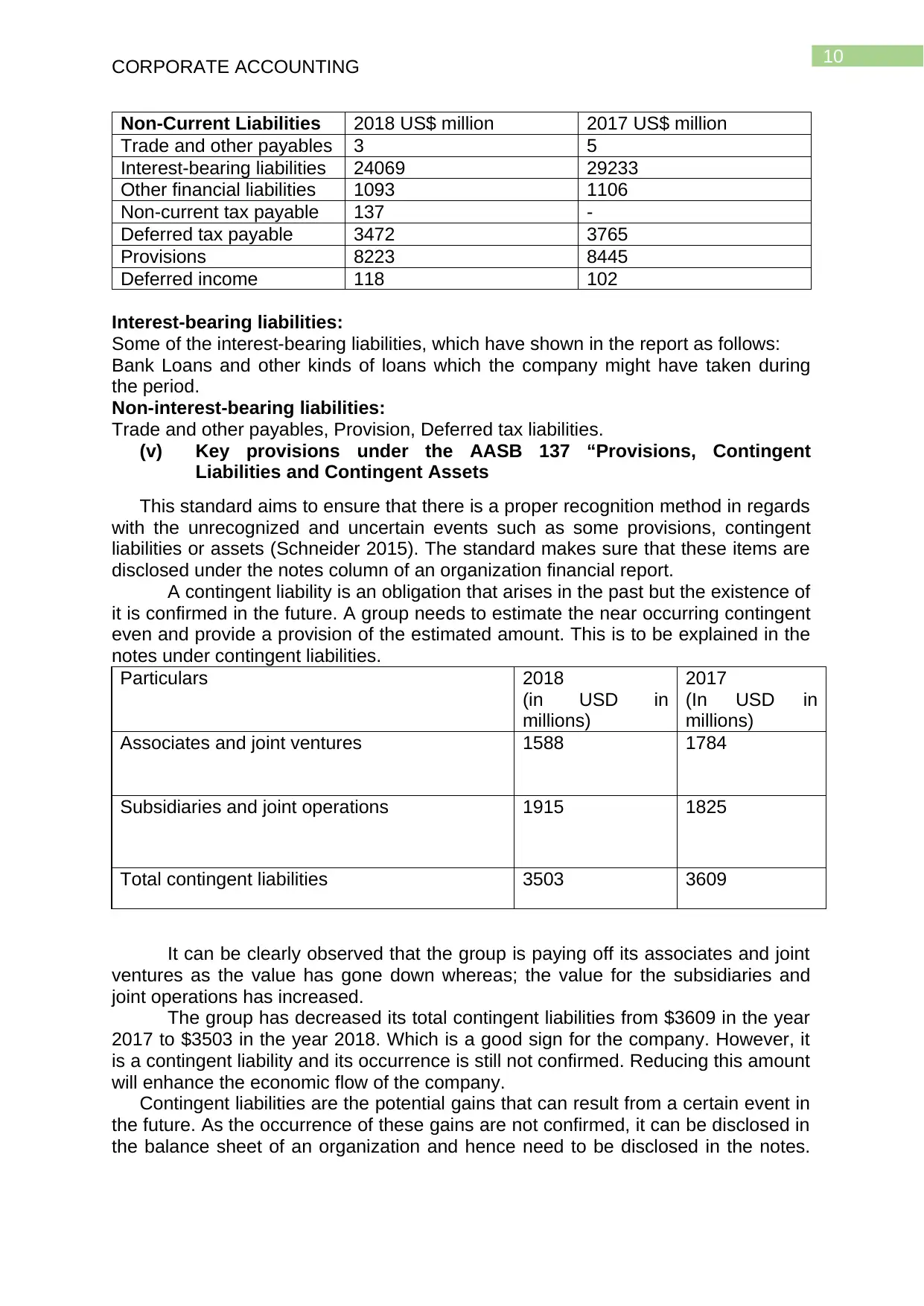

Non-Current Liabilities 2018 US$ million 2017 US$ million

Trade and other payables 3 5

Interest-bearing liabilities 24069 29233

Other financial liabilities 1093 1106

Non-current tax payable 137 -

Deferred tax payable 3472 3765

Provisions 8223 8445

Deferred income 118 102

Interest-bearing liabilities:

Some of the interest-bearing liabilities, which have shown in the report as follows:

Bank Loans and other kinds of loans which the company might have taken during

the period.

Non-interest-bearing liabilities:

Trade and other payables, Provision, Deferred tax liabilities.

(v) Key provisions under the AASB 137 “Provisions, Contingent

Liabilities and Contingent Assets

This standard aims to ensure that there is a proper recognition method in regards

with the unrecognized and uncertain events such as some provisions, contingent

liabilities or assets (Schneider 2015). The standard makes sure that these items are

disclosed under the notes column of an organization financial report.

A contingent liability is an obligation that arises in the past but the existence of

it is confirmed in the future. A group needs to estimate the near occurring contingent

even and provide a provision of the estimated amount. This is to be explained in the

notes under contingent liabilities.

Particulars 2018

(in USD in

millions)

2017

(In USD in

millions)

Associates and joint ventures 1588 1784

Subsidiaries and joint operations 1915 1825

Total contingent liabilities 3503 3609

It can be clearly observed that the group is paying off its associates and joint

ventures as the value has gone down whereas; the value for the subsidiaries and

joint operations has increased.

The group has decreased its total contingent liabilities from $3609 in the year

2017 to $3503 in the year 2018. Which is a good sign for the company. However, it

is a contingent liability and its occurrence is still not confirmed. Reducing this amount

will enhance the economic flow of the company.

Contingent liabilities are the potential gains that can result from a certain event in

the future. As the occurrence of these gains are not confirmed, it can be disclosed in

the balance sheet of an organization and hence need to be disclosed in the notes.

CORPORATE ACCOUNTING

Non-Current Liabilities 2018 US$ million 2017 US$ million

Trade and other payables 3 5

Interest-bearing liabilities 24069 29233

Other financial liabilities 1093 1106

Non-current tax payable 137 -

Deferred tax payable 3472 3765

Provisions 8223 8445

Deferred income 118 102

Interest-bearing liabilities:

Some of the interest-bearing liabilities, which have shown in the report as follows:

Bank Loans and other kinds of loans which the company might have taken during

the period.

Non-interest-bearing liabilities:

Trade and other payables, Provision, Deferred tax liabilities.

(v) Key provisions under the AASB 137 “Provisions, Contingent

Liabilities and Contingent Assets

This standard aims to ensure that there is a proper recognition method in regards

with the unrecognized and uncertain events such as some provisions, contingent

liabilities or assets (Schneider 2015). The standard makes sure that these items are

disclosed under the notes column of an organization financial report.

A contingent liability is an obligation that arises in the past but the existence of

it is confirmed in the future. A group needs to estimate the near occurring contingent

even and provide a provision of the estimated amount. This is to be explained in the

notes under contingent liabilities.

Particulars 2018

(in USD in

millions)

2017

(In USD in

millions)

Associates and joint ventures 1588 1784

Subsidiaries and joint operations 1915 1825

Total contingent liabilities 3503 3609

It can be clearly observed that the group is paying off its associates and joint

ventures as the value has gone down whereas; the value for the subsidiaries and

joint operations has increased.

The group has decreased its total contingent liabilities from $3609 in the year

2017 to $3503 in the year 2018. Which is a good sign for the company. However, it

is a contingent liability and its occurrence is still not confirmed. Reducing this amount

will enhance the economic flow of the company.

Contingent liabilities are the potential gains that can result from a certain event in

the future. As the occurrence of these gains are not confirmed, it can be disclosed in

the balance sheet of an organization and hence need to be disclosed in the notes.

11

CORPORATE ACCOUNTING

BHP Billiton does not record any such contingent asset in its financial statements

(Caskey and Laux 2016).

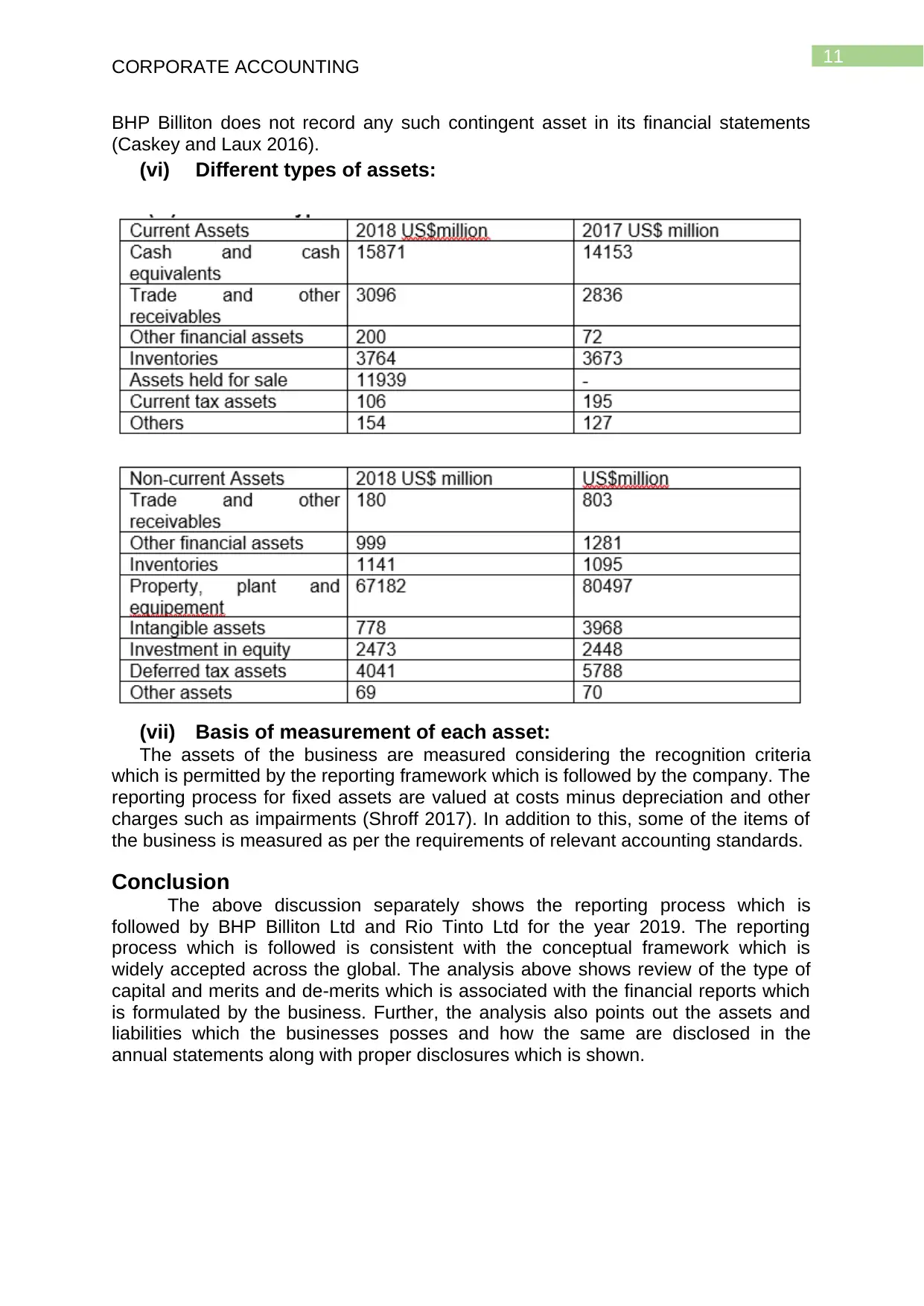

(vi) Different types of assets:

(vii) Basis of measurement of each asset:

The assets of the business are measured considering the recognition criteria

which is permitted by the reporting framework which is followed by the company. The

reporting process for fixed assets are valued at costs minus depreciation and other

charges such as impairments (Shroff 2017). In addition to this, some of the items of

the business is measured as per the requirements of relevant accounting standards.

Conclusion

The above discussion separately shows the reporting process which is

followed by BHP Billiton Ltd and Rio Tinto Ltd for the year 2019. The reporting

process which is followed is consistent with the conceptual framework which is

widely accepted across the global. The analysis above shows review of the type of

capital and merits and de-merits which is associated with the financial reports which

is formulated by the business. Further, the analysis also points out the assets and

liabilities which the businesses posses and how the same are disclosed in the

annual statements along with proper disclosures which is shown.

CORPORATE ACCOUNTING

BHP Billiton does not record any such contingent asset in its financial statements

(Caskey and Laux 2016).

(vi) Different types of assets:

(vii) Basis of measurement of each asset:

The assets of the business are measured considering the recognition criteria

which is permitted by the reporting framework which is followed by the company. The

reporting process for fixed assets are valued at costs minus depreciation and other

charges such as impairments (Shroff 2017). In addition to this, some of the items of

the business is measured as per the requirements of relevant accounting standards.

Conclusion

The above discussion separately shows the reporting process which is

followed by BHP Billiton Ltd and Rio Tinto Ltd for the year 2019. The reporting

process which is followed is consistent with the conceptual framework which is

widely accepted across the global. The analysis above shows review of the type of

capital and merits and de-merits which is associated with the financial reports which

is formulated by the business. Further, the analysis also points out the assets and

liabilities which the businesses posses and how the same are disclosed in the

annual statements along with proper disclosures which is shown.

12

CORPORATE ACCOUNTING

Reference

Barker, R. and Schulte, S., 2017. Representing the market perspective: Fair value

measurement for non-financial assets. Accounting, Organizations and Society, 56,

pp.55-67.

Bhp.com. (2020). [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2019/

bhpannualreport2019.pdf [Accessed 14 Jan. 2020].

Caskey, J. and Laux, V., 2016. Corporate governance, accounting conservatism,

and manipulation. Management Science, 63(2), pp.424-437.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and

access to finance. Strategic management journal, 35(1), pp.1-23.

Killian, S. and O'Regan, P., 2016. Social accounting and the co-creation of corporate

legitimacy. Accounting, Organizations and Society, 50, pp.1-12.

Raiborn, C. and Sivitanides, M., 2015. Accounting issues related to Bitcoins. Journal

of Corporate Accounting & Finance, 26(2), pp.25-34.

Riotinto.com. (2020). Reports. [online] Available at:

https://www.riotinto.com/invest/reports [Accessed 14 Jan. 2020].

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate

accounting and reporting for sustainability–attributes and challenges. Sustainable

Development, 25(2), pp.113-122.

Schneider, A., 2015. Reflexivity in sustainability accounting and management:

Transcending the economic focus of corporate sustainability. Journal of Business

Ethics, 127(3), pp.525-536.

Shroff, N., 2017. Corporate investment and changes in GAAP. Review of Accounting

Studies, 22(1), pp.1-63.

CORPORATE ACCOUNTING

Reference

Barker, R. and Schulte, S., 2017. Representing the market perspective: Fair value

measurement for non-financial assets. Accounting, Organizations and Society, 56,

pp.55-67.

Bhp.com. (2020). [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2019/

bhpannualreport2019.pdf [Accessed 14 Jan. 2020].

Caskey, J. and Laux, V., 2016. Corporate governance, accounting conservatism,

and manipulation. Management Science, 63(2), pp.424-437.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and

access to finance. Strategic management journal, 35(1), pp.1-23.

Killian, S. and O'Regan, P., 2016. Social accounting and the co-creation of corporate

legitimacy. Accounting, Organizations and Society, 50, pp.1-12.

Raiborn, C. and Sivitanides, M., 2015. Accounting issues related to Bitcoins. Journal

of Corporate Accounting & Finance, 26(2), pp.25-34.

Riotinto.com. (2020). Reports. [online] Available at:

https://www.riotinto.com/invest/reports [Accessed 14 Jan. 2020].

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate

accounting and reporting for sustainability–attributes and challenges. Sustainable

Development, 25(2), pp.113-122.

Schneider, A., 2015. Reflexivity in sustainability accounting and management:

Transcending the economic focus of corporate sustainability. Journal of Business

Ethics, 127(3), pp.525-536.

Shroff, N., 2017. Corporate investment and changes in GAAP. Review of Accounting

Studies, 22(1), pp.1-63.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.