Portfolio Standard Deviation and Correlation

VerifiedAdded on 2020/05/11

|6

|1280

|67

AI Summary

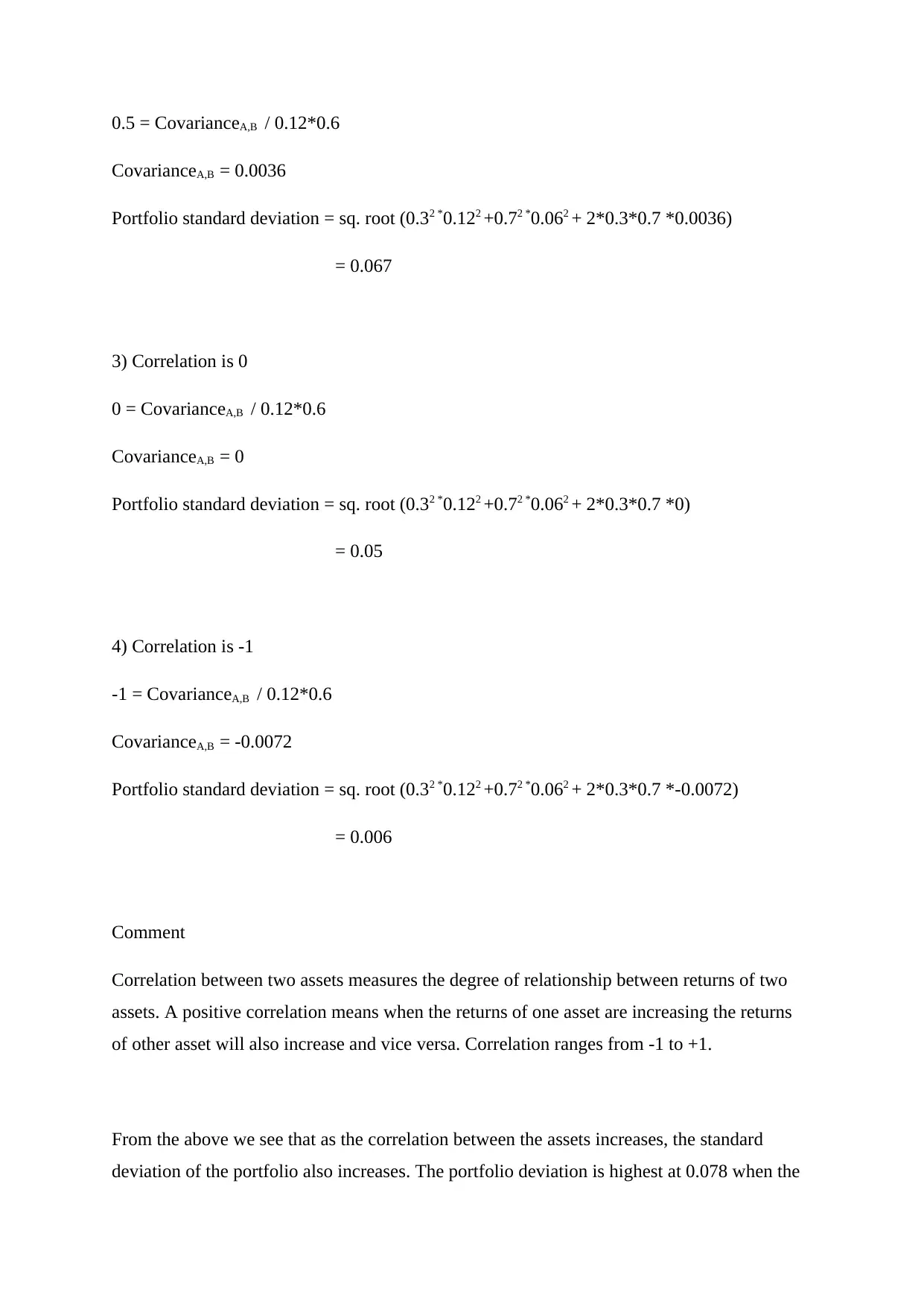

This assignment examines the relationship between asset correlation and portfolio risk (standard deviation). It demonstrates how to calculate portfolio standard deviation using weights and variances of individual assets, along with the impact of covariance due to correlation. Calculations are shown for correlations ranging from +1 (perfect positive) to -1 (perfect negative), illustrating the varying levels of risk associated with different correlation scenarios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.