Corporate and Finance Accounting - Importance of Financial Reporting Frameworks and Equity Analysis of Retail Companies

VerifiedAdded on 2023/06/07

|14

|3653

|255

AI Summary

This article discusses the importance of financial reporting frameworks and equity analysis of four retail companies. It covers corporate regulation, accounting standard setting, and owners equity. The article is relevant for students studying corporate and finance accounting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Corporate and Finance Accounting

Corporate and Finance Accounting

1 | P a g e

Corporate and Finance Accounting

1 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate and Finance Accounting

Contents

EXECUTIVE SUMMARY:..........................................................................................................................3

BRIEF......................................................................................................................................................4

CORPORATE REGULATION.....................................................................................................................5

ACCOUNTING STANDARD SETTING:......................................................................................................6

OWNERS EQUITY...................................................................................................................................7

CONCLUSION:......................................................................................................................................11

REFERENCES:.......................................................................................................................................12

2 | P a g e

Contents

EXECUTIVE SUMMARY:..........................................................................................................................3

BRIEF......................................................................................................................................................4

CORPORATE REGULATION.....................................................................................................................5

ACCOUNTING STANDARD SETTING:......................................................................................................6

OWNERS EQUITY...................................................................................................................................7

CONCLUSION:......................................................................................................................................11

REFERENCES:.......................................................................................................................................12

2 | P a g e

Corporate and Finance Accounting

EXECUTIVE SUMMARY:

Nowadays, users take the decision on the basis of the financial statement of an entity. If the

entities financial data are not as per standard or underlying rules, their decision may be wrong

which would ultimately affect the goodwill of the company. As such, the financial reporting

framework plays a critical role in the presentation of the financial statement of each

organization. So that users can rely on the presented data and take decision accordingly.

In addition to that, there are global accounting standards like IFRS, IASB, GAAP etc. These

are to be followed in the presentation and preparation of the financial statement. Every

country adopts such standards subject to some changes due to its countries condition.

3 | P a g e

EXECUTIVE SUMMARY:

Nowadays, users take the decision on the basis of the financial statement of an entity. If the

entities financial data are not as per standard or underlying rules, their decision may be wrong

which would ultimately affect the goodwill of the company. As such, the financial reporting

framework plays a critical role in the presentation of the financial statement of each

organization. So that users can rely on the presented data and take decision accordingly.

In addition to that, there are global accounting standards like IFRS, IASB, GAAP etc. These

are to be followed in the presentation and preparation of the financial statement. Every

country adopts such standards subject to some changes due to its countries condition.

3 | P a g e

Corporate and Finance Accounting

BRIEF:

Financial reporting frameworks are the most important tools to the preparation and

presentation of the financial statements. In this assignment, we will be discussing the needs of

the standards or guidelines for the accounting and reporting of financial records of an

organization. We have also covered in the assignment the reason to why should preparation

and presentation not be voluntary to the organizations.

International Accounting Standard Board (IASB) issued the International Financial Reporting

Standards (IFRS). We will be discussing the adoption of IFRS by the Australian Accounting

Standard Board (AASB). We will also discuss the reason for not adopting the IFRS by the

countries which are the member of IASB.

We will also discuss the equity analysis of the four companies from the retail sector and

which are listed in ASX. We will be analyzing the debt and equity relationship of these

companies.

4 | P a g e

BRIEF:

Financial reporting frameworks are the most important tools to the preparation and

presentation of the financial statements. In this assignment, we will be discussing the needs of

the standards or guidelines for the accounting and reporting of financial records of an

organization. We have also covered in the assignment the reason to why should preparation

and presentation not be voluntary to the organizations.

International Accounting Standard Board (IASB) issued the International Financial Reporting

Standards (IFRS). We will be discussing the adoption of IFRS by the Australian Accounting

Standard Board (AASB). We will also discuss the reason for not adopting the IFRS by the

countries which are the member of IASB.

We will also discuss the equity analysis of the four companies from the retail sector and

which are listed in ASX. We will be analyzing the debt and equity relationship of these

companies.

4 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate and Finance Accounting

CORPORATE REGULATION:

There are various financial reporting frameworks which are to be complied with in the

preparation and presentation of the financial statement of an organization. Now the basic

question comes that why these frameworks have been developed and why these should be

complied with? Before answering this question, we have discussed one thing that what would

be the situation if the entities have freedom of financial accounting and reporting as per their

own wish. It would be interesting where the company will maintain their own reporting

standard. Financial reporting is the base of decision making by the users or stakeholders

(Gordon, 2015).

If the financial accounting is done by the company as per its own standards then it is very

clear that financial accounts of the same or similar company in the same industry will not be

comparable to each other. The reason thereof may be as they were adopting their own

standards, accounting policies, reporting framework etc. for the financial accounting and

reporting purposes (Deloitte, no date).

For Example, Company A and B are dealing in the retail market. During the recording of

sales revenue the company A considers the accrual concept, while company B does not

consider the accrual concept. It means that Company A will record its revenue on cash as

well as credit basis. But, company B will book the revenue on the cash basis. In that case,

financial statements of both the companies are not comparable.

Where the power of voluntary preparation and presentation of financial statement goes in the

hand of entities, they will prepare and present their financial statement in such manner which

may be beneficial to the company in all aspect. It may cause the various issues some of them

are as under (Rouse, no date):

a) Misstatement in the financial statement

b) It may influence the investor’s decision

c) It may impact the shareholder’s interest

d) It may disrupt the economy of the country in which it operates.

e) Users of financial statements may not take correct decisions etc.

As such, there are a lot of complexities in the voluntary preparation and presentation of the

financial statement of the companies. To eliminate such types of complexities, the regulatory

framework has been designed for the preparation and reporting of the accounting records of

the companies (Bonner, 2012). By using these frameworks or guidelines, all the companies

come at par. Which become a very useful tool in the decision making either by users of the

statements or management as well.

As such, if the financial accounting and reporting are regulated by any law or any regulatory

body, it would be benefited to everyone, who is most concerned with them. There are some

benefits to follow the rules of accounting and reporting, which are as under (Anon, 2017):

a) It would be beneficial to the organization in term of providing the useful information

for decision making, planning, and analysis.

b) Shareholders can rely on such financial statements of the companies as they would

not be worried about the manipulation in the data that usually followed in the

traditional approach.

5 | P a g e

CORPORATE REGULATION:

There are various financial reporting frameworks which are to be complied with in the

preparation and presentation of the financial statement of an organization. Now the basic

question comes that why these frameworks have been developed and why these should be

complied with? Before answering this question, we have discussed one thing that what would

be the situation if the entities have freedom of financial accounting and reporting as per their

own wish. It would be interesting where the company will maintain their own reporting

standard. Financial reporting is the base of decision making by the users or stakeholders

(Gordon, 2015).

If the financial accounting is done by the company as per its own standards then it is very

clear that financial accounts of the same or similar company in the same industry will not be

comparable to each other. The reason thereof may be as they were adopting their own

standards, accounting policies, reporting framework etc. for the financial accounting and

reporting purposes (Deloitte, no date).

For Example, Company A and B are dealing in the retail market. During the recording of

sales revenue the company A considers the accrual concept, while company B does not

consider the accrual concept. It means that Company A will record its revenue on cash as

well as credit basis. But, company B will book the revenue on the cash basis. In that case,

financial statements of both the companies are not comparable.

Where the power of voluntary preparation and presentation of financial statement goes in the

hand of entities, they will prepare and present their financial statement in such manner which

may be beneficial to the company in all aspect. It may cause the various issues some of them

are as under (Rouse, no date):

a) Misstatement in the financial statement

b) It may influence the investor’s decision

c) It may impact the shareholder’s interest

d) It may disrupt the economy of the country in which it operates.

e) Users of financial statements may not take correct decisions etc.

As such, there are a lot of complexities in the voluntary preparation and presentation of the

financial statement of the companies. To eliminate such types of complexities, the regulatory

framework has been designed for the preparation and reporting of the accounting records of

the companies (Bonner, 2012). By using these frameworks or guidelines, all the companies

come at par. Which become a very useful tool in the decision making either by users of the

statements or management as well.

As such, if the financial accounting and reporting are regulated by any law or any regulatory

body, it would be benefited to everyone, who is most concerned with them. There are some

benefits to follow the rules of accounting and reporting, which are as under (Anon, 2017):

a) It would be beneficial to the organization in term of providing the useful information

for decision making, planning, and analysis.

b) Shareholders can rely on such financial statements of the companies as they would

not be worried about the manipulation in the data that usually followed in the

traditional approach.

5 | P a g e

Corporate and Finance Accounting

c) Investors would take the decision to invest in the company without any hesitation.

d) Actual industry data can be calculated.

e) Actual picture of the contribution of industry in the country’s economy etc.

As such, financial accounting and reporting should be regulated rather than voluntary

preparation and presentation thereof. It would be useful to all the stakeholders as well as the

company itself. In this concept, companies cannot manipulate the data which ultimately

mislead the users of the financial statements.

ACCOUNTING STANDARD SETTING:

International Financial Reporting Framework (IFRS) refers to the accounting standards

issued by the Internal Accounting Standard Board (IASB) to recognize the transactions or

reporting of the financial statements, which come on at par with the international business

reporting (PWC, no date). Nowadays, the number of organizations operates in the different

countries. Accounting record of such companies should be prepared in such a manner that

can be comparable with the internal business or it may be useful for the overseas users of the

financial statements (AICPA, no date).

Australian Accounting Standard Board (AASB) is the Australian government body, which set

out the accounting standards for the organizations of country Australia. It is engaged in the

regular monitoring of the financial reporting standard and proceeds to make an amendment

accordingly.

IFRS is the globally recognized accounting standard i.e. it should be adopted by the all the

organization operates in different countries. But, there may be a problem of deferment of

adoption by some countries. The reason may be that every country has its own policies to

govern the rule (AUASB, 2009). As such, every country may not adopt the international

standards as a whole. They are adopted with some modification and amendments.

In the present case, AASB is the convergence of IFRS from the perspective of the country

Australia. As such, Australian companies need to prepare its financial statement in

compliance with the standards issued by the AASB. If the Australian companies are adopting

the AASB in the presentation and reporting of the financial statements, It does not mean that

companies are not adopting the IFRS. We should not forget here that, standards developed by

the AASB are the part of IFRS which have been adopted following some changes due to

country’s specific requirements.

For Example, A company adopting the IFRS can value its inventory by following the normal

procedure. But if in the case of AASB LIFO method is not allowed for the valuation of

inventory.

In addition that in the IFRS, changes in the accounting policies are allowed only where it is

legal requirements. Besides that, AASB does not the changes in the accounting policies even

in case of legal requirements. AASB allows the changes in the accounting policies only when

6 | P a g e

c) Investors would take the decision to invest in the company without any hesitation.

d) Actual industry data can be calculated.

e) Actual picture of the contribution of industry in the country’s economy etc.

As such, financial accounting and reporting should be regulated rather than voluntary

preparation and presentation thereof. It would be useful to all the stakeholders as well as the

company itself. In this concept, companies cannot manipulate the data which ultimately

mislead the users of the financial statements.

ACCOUNTING STANDARD SETTING:

International Financial Reporting Framework (IFRS) refers to the accounting standards

issued by the Internal Accounting Standard Board (IASB) to recognize the transactions or

reporting of the financial statements, which come on at par with the international business

reporting (PWC, no date). Nowadays, the number of organizations operates in the different

countries. Accounting record of such companies should be prepared in such a manner that

can be comparable with the internal business or it may be useful for the overseas users of the

financial statements (AICPA, no date).

Australian Accounting Standard Board (AASB) is the Australian government body, which set

out the accounting standards for the organizations of country Australia. It is engaged in the

regular monitoring of the financial reporting standard and proceeds to make an amendment

accordingly.

IFRS is the globally recognized accounting standard i.e. it should be adopted by the all the

organization operates in different countries. But, there may be a problem of deferment of

adoption by some countries. The reason may be that every country has its own policies to

govern the rule (AUASB, 2009). As such, every country may not adopt the international

standards as a whole. They are adopted with some modification and amendments.

In the present case, AASB is the convergence of IFRS from the perspective of the country

Australia. As such, Australian companies need to prepare its financial statement in

compliance with the standards issued by the AASB. If the Australian companies are adopting

the AASB in the presentation and reporting of the financial statements, It does not mean that

companies are not adopting the IFRS. We should not forget here that, standards developed by

the AASB are the part of IFRS which have been adopted following some changes due to

country’s specific requirements.

For Example, A company adopting the IFRS can value its inventory by following the normal

procedure. But if in the case of AASB LIFO method is not allowed for the valuation of

inventory.

In addition that in the IFRS, changes in the accounting policies are allowed only where it is

legal requirements. Besides that, AASB does not the changes in the accounting policies even

in case of legal requirements. AASB allows the changes in the accounting policies only when

6 | P a g e

Corporate and Finance Accounting

it is necessary to tally the adopted accounting policies with the other accounting policies

(Wikipedia, no date).

IFRS not compulsory for the member countries of IASB?

Mostly the member country of the IASB, are adopting the Generally Accepted Accounting

Principles (GAAP). IFRS are slightly different from the GAAP. The countries adopted

GAAP were criticizing that it would be costlier for them to migrate to IFRS in term of staff

training, change in the systems etc (Anon, no date). They had also criticized that IFRS is not

quality standards in comparison to the GAAP. By these reasons, IFRS is not compulsory for

the countries adopted GAAP (Kumaran, 2015).

OWNERS EQUITY

For the purpose of this analysis, we have taken the following four companies from the retail

industry. These are as follows:

a) Accent Group Limited

b) Adairs Retail Group Limited

c) Baby Bunting Group Limited

d) Bapcor Limited

Let us discuss one by one:

i) Accent Group Limited: The Company is engaged in the business of distribution of

footwear through the retail outlets. Former name of the company is RCG

Corporation Limited. Equity analysis of the company is as under:

Particular 2017 ($ ‘000) 2016 ($ ‘000) 2015 ($ ‘000) 2014 ($ ‘000)

Equity 3,85,310 3,19,319 2,57,741 70,860

Year 2014:

In this year equity portion includes the option exercised during the year 2014. In

the year 2014 the group has acquired the business of Saucony and Podium Sports

and in consideration thereof, it has issued the shares of $ 5953000. In addition to

that in this year, it has capitalized the option fees.

Year 2015:

In this year equity portion also includes the option exercised during the year.

Options are share available to the employees of the company based on their work

performance, experience etc. When such shares are exercised by the employees

they become the shareholder of the company and the respective amount is shown

7 | P a g e

it is necessary to tally the adopted accounting policies with the other accounting policies

(Wikipedia, no date).

IFRS not compulsory for the member countries of IASB?

Mostly the member country of the IASB, are adopting the Generally Accepted Accounting

Principles (GAAP). IFRS are slightly different from the GAAP. The countries adopted

GAAP were criticizing that it would be costlier for them to migrate to IFRS in term of staff

training, change in the systems etc (Anon, no date). They had also criticized that IFRS is not

quality standards in comparison to the GAAP. By these reasons, IFRS is not compulsory for

the countries adopted GAAP (Kumaran, 2015).

OWNERS EQUITY

For the purpose of this analysis, we have taken the following four companies from the retail

industry. These are as follows:

a) Accent Group Limited

b) Adairs Retail Group Limited

c) Baby Bunting Group Limited

d) Bapcor Limited

Let us discuss one by one:

i) Accent Group Limited: The Company is engaged in the business of distribution of

footwear through the retail outlets. Former name of the company is RCG

Corporation Limited. Equity analysis of the company is as under:

Particular 2017 ($ ‘000) 2016 ($ ‘000) 2015 ($ ‘000) 2014 ($ ‘000)

Equity 3,85,310 3,19,319 2,57,741 70,860

Year 2014:

In this year equity portion includes the option exercised during the year 2014. In

the year 2014 the group has acquired the business of Saucony and Podium Sports

and in consideration thereof, it has issued the shares of $ 5953000. In addition to

that in this year, it has capitalized the option fees.

Year 2015:

In this year equity portion also includes the option exercised during the year.

Options are share available to the employees of the company based on their work

performance, experience etc. When such shares are exercised by the employees

they become the shareholder of the company and the respective amount is shown

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Finance Accounting

as equity of the company. The company during this year has acquired the business

of Accent Group and issued the shares of $ 160714000 against consideration.

A major reason for the change in equity from the last is the shares issued as

consideration for acquisition of the business of Accent Group (David, 2017).

Year 2016:

In the year the equity includes the share issued under placements which amount to

$ 50000000 and shares issued under the share purchase plan of $ 10056000. The

equity also includes the share issued for the payment of debt i.e. where debts are

not repaid actually but for settlement thereof share are issued at an agreed price.

Reason for the change in equity in comparison to the last year is the issue of the

placement shares and shares issued under share purchase plan (Calla, 2011).

Year 2017:

In the year 2017 the company has paid a lot of debt through the issue of shares.

Thus, the major portion of the equity of this year covered by the share issued for

the settlement of debts. In addition to that, the company has acquired the business

of Hype DC Pty Limited and issued shares of $ 62926000 as consideration

thereof.

Reason for the change in equity as compared to the previous is same as above i.e.

acquisition of the business of Hype DC Pty Limited and loan paid through shares

issued.

ii) Adairs Retail Group Limited: The Company is engaged in the retail business of

home furnishing. It deals in the products like, bedding, towels etc. Equity analysis

of the company is under:

Particular 2017 ($ ‘000) 2016 ($ ‘000) 2015 ($ ‘000) 2014 ($ ‘000)

Equity 1,00,312 95,590 77,952 41,900

Debt 60,347 59,513 45,796 1,22,663

Year 2014:

In this year the company comes up with Initial Public Offer of $ 35,645 and but

equity get reduced by the reserves adverse balance.

Year 2015:

In the year 2015, the company has restructured the equity and it had split the 1

share by 4.35 shares resulting which 116305000 shares have zero value.

8 | P a g e

as equity of the company. The company during this year has acquired the business

of Accent Group and issued the shares of $ 160714000 against consideration.

A major reason for the change in equity from the last is the shares issued as

consideration for acquisition of the business of Accent Group (David, 2017).

Year 2016:

In the year the equity includes the share issued under placements which amount to

$ 50000000 and shares issued under the share purchase plan of $ 10056000. The

equity also includes the share issued for the payment of debt i.e. where debts are

not repaid actually but for settlement thereof share are issued at an agreed price.

Reason for the change in equity in comparison to the last year is the issue of the

placement shares and shares issued under share purchase plan (Calla, 2011).

Year 2017:

In the year 2017 the company has paid a lot of debt through the issue of shares.

Thus, the major portion of the equity of this year covered by the share issued for

the settlement of debts. In addition to that, the company has acquired the business

of Hype DC Pty Limited and issued shares of $ 62926000 as consideration

thereof.

Reason for the change in equity as compared to the previous is same as above i.e.

acquisition of the business of Hype DC Pty Limited and loan paid through shares

issued.

ii) Adairs Retail Group Limited: The Company is engaged in the retail business of

home furnishing. It deals in the products like, bedding, towels etc. Equity analysis

of the company is under:

Particular 2017 ($ ‘000) 2016 ($ ‘000) 2015 ($ ‘000) 2014 ($ ‘000)

Equity 1,00,312 95,590 77,952 41,900

Debt 60,347 59,513 45,796 1,22,663

Year 2014:

In this year the company comes up with Initial Public Offer of $ 35,645 and but

equity get reduced by the reserves adverse balance.

Year 2015:

In the year 2015, the company has restructured the equity and it had split the 1

share by 4.35 shares resulting which 116305000 shares have zero value.

8 | P a g e

Corporate and Finance Accounting

Reason for the change in equity was only the increase in the retained earnings and

reserves. Reserve has been increased due to capitalization of forward currency

contracts.

Year 2016:

In the year 2016 contributed equity was same as the previous year. Component of

the total equity includes the retained earnings and cash flow hedge movement.

Cash flow movement is the result of hedge accounting because the company has

purchased of inventory in US Dollar and for the payment thereof in the US Dollar,

the company has most concerned with the foreign currency fluctuations.

The reason for the change in the total equity was the recognition of cash flow

movement due to hedge accounting.

Year 2017:

The year 2017 contributed equity of the company was the same as the previous

year. But the total equity includes the foreign currency translation reserves and

share-based payment reserves.

Reason for increase in equity in comparison to earlier year is an increase in

retained earnings is much higher than the other adjustment in the equity such as

reversal of foreign currency translation reserves etc (Zacks, no date).

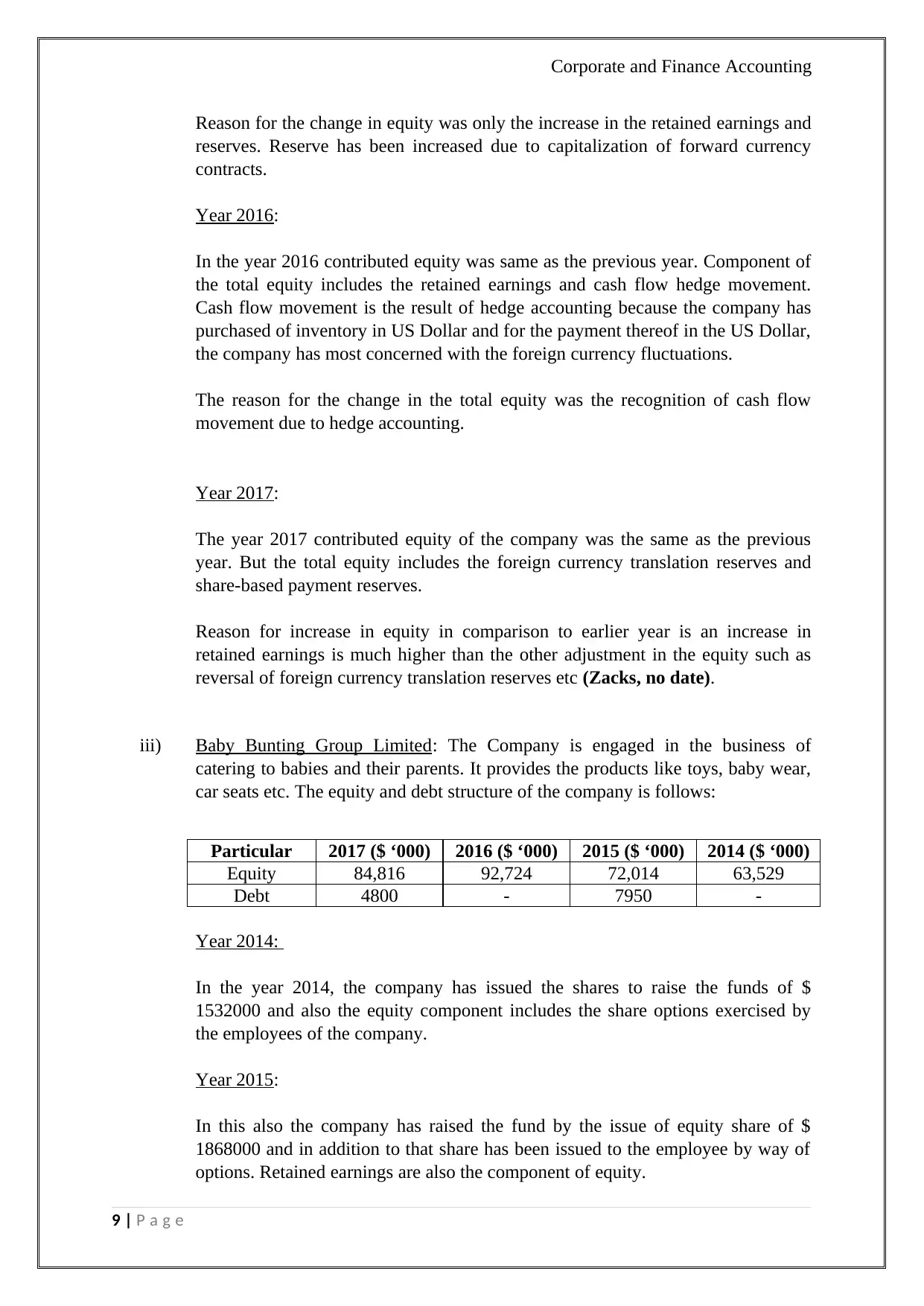

iii) Baby Bunting Group Limited: The Company is engaged in the business of

catering to babies and their parents. It provides the products like toys, baby wear,

car seats etc. The equity and debt structure of the company is follows:

Particular 2017 ($ ‘000) 2016 ($ ‘000) 2015 ($ ‘000) 2014 ($ ‘000)

Equity 84,816 92,724 72,014 63,529

Debt 4800 - 7950 -

Year 2014:

In the year 2014, the company has issued the shares to raise the funds of $

1532000 and also the equity component includes the share options exercised by

the employees of the company.

Year 2015:

In this also the company has raised the fund by the issue of equity share of $

1868000 and in addition to that share has been issued to the employee by way of

options. Retained earnings are also the component of equity.

9 | P a g e

Reason for the change in equity was only the increase in the retained earnings and

reserves. Reserve has been increased due to capitalization of forward currency

contracts.

Year 2016:

In the year 2016 contributed equity was same as the previous year. Component of

the total equity includes the retained earnings and cash flow hedge movement.

Cash flow movement is the result of hedge accounting because the company has

purchased of inventory in US Dollar and for the payment thereof in the US Dollar,

the company has most concerned with the foreign currency fluctuations.

The reason for the change in the total equity was the recognition of cash flow

movement due to hedge accounting.

Year 2017:

The year 2017 contributed equity of the company was the same as the previous

year. But the total equity includes the foreign currency translation reserves and

share-based payment reserves.

Reason for increase in equity in comparison to earlier year is an increase in

retained earnings is much higher than the other adjustment in the equity such as

reversal of foreign currency translation reserves etc (Zacks, no date).

iii) Baby Bunting Group Limited: The Company is engaged in the business of

catering to babies and their parents. It provides the products like toys, baby wear,

car seats etc. The equity and debt structure of the company is follows:

Particular 2017 ($ ‘000) 2016 ($ ‘000) 2015 ($ ‘000) 2014 ($ ‘000)

Equity 84,816 92,724 72,014 63,529

Debt 4800 - 7950 -

Year 2014:

In the year 2014, the company has issued the shares to raise the funds of $

1532000 and also the equity component includes the share options exercised by

the employees of the company.

Year 2015:

In this also the company has raised the fund by the issue of equity share of $

1868000 and in addition to that share has been issued to the employee by way of

options. Retained earnings are also the component of equity.

9 | P a g e

Corporate and Finance Accounting

Reason for the increase in the equity was options exercised by the employee are

greater than in comparison to the earlier year.

Year 2016:

In this company has come up with the initial public offer of $ 25000000 and also

issued the shares to its employees who have exercised the options. Apart from that

company has offered the employee gift in terms of shares.

Reason for the increase in the equity is same as discussed above.

Year 2017:

In this year the company has only issued the share as a gift to its employees. In

this year the company has granted the performance right.

iv) Bapcor Limited: The Company is engaged in the business of providing Auto

Parts. It deals with these products through its wholesale and retail outlets. Equity

and debt position of the company is as under:

Particular 2017 ($ ‘000) 2016 ($ ‘000) 2015 ($ ‘000) 2014 ($ ‘000)

Equity 5,89,967 3,66,220 2,66,925 96,961

Debt 4,29,747 1,48,184 - 73,342

Year 2014:

In this year the company has issued the shares to raise the fund of $ 143615000

and also received the amount of partly paid-up shares of $ 1168000.

Year 2015:

In this year the company come up with an IPO of $ 159821000 and capitalized the

cost related to such issues of shares amounting to $ 3206000.

These are also the main reason of an increase in the equity of the company.

Year 2016:

In this year it has acquired the business of Hellaby Holdings Limited and issue the

shares of $ 161051000 and 16288000 as consideration. Apart from that, it has

recognized the relating that issues of share and capitalized it into the equity of the

company.

Year 2017:

10 | P a g e

Reason for the increase in the equity was options exercised by the employee are

greater than in comparison to the earlier year.

Year 2016:

In this company has come up with the initial public offer of $ 25000000 and also

issued the shares to its employees who have exercised the options. Apart from that

company has offered the employee gift in terms of shares.

Reason for the increase in the equity is same as discussed above.

Year 2017:

In this year the company has only issued the share as a gift to its employees. In

this year the company has granted the performance right.

iv) Bapcor Limited: The Company is engaged in the business of providing Auto

Parts. It deals with these products through its wholesale and retail outlets. Equity

and debt position of the company is as under:

Particular 2017 ($ ‘000) 2016 ($ ‘000) 2015 ($ ‘000) 2014 ($ ‘000)

Equity 5,89,967 3,66,220 2,66,925 96,961

Debt 4,29,747 1,48,184 - 73,342

Year 2014:

In this year the company has issued the shares to raise the fund of $ 143615000

and also received the amount of partly paid-up shares of $ 1168000.

Year 2015:

In this year the company come up with an IPO of $ 159821000 and capitalized the

cost related to such issues of shares amounting to $ 3206000.

These are also the main reason of an increase in the equity of the company.

Year 2016:

In this year it has acquired the business of Hellaby Holdings Limited and issue the

shares of $ 161051000 and 16288000 as consideration. Apart from that, it has

recognized the relating that issues of share and capitalized it into the equity of the

company.

Year 2017:

10 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate and Finance Accounting

In this year the company has booked the cash flow hedge reserve arising out of the

hedge fund accounting. Also has considered the foreign currency reserves in the

equity.

CONCLUSION:

From the above discussion of the requirements of financial regulatory frameworks, we

conclude that it should be followed in the preparation and presentation of the financial

statement. It should not be left on the part of management. Further, we have discussed the

relationship between the AASB and IFRS. Based on this we can conclude that the AASB is

the convergence of the IFRS. There is no more difference in the AASB and IFRS.

At last, in the equity analysis of the four companies, we can conclude the equity of an

organization is affected by some factors i.e. issues of shares in IPO, shares issued under

options exercised, shares issued as consideration of an acquisition of any business etc. We

also conclude that Accent Group Limited has maintained the debt and equity relationship in

proper manners i.e. it has paid the debt through the issues of shares through which it converts

debt into equity.

11 | P a g e

In this year the company has booked the cash flow hedge reserve arising out of the

hedge fund accounting. Also has considered the foreign currency reserves in the

equity.

CONCLUSION:

From the above discussion of the requirements of financial regulatory frameworks, we

conclude that it should be followed in the preparation and presentation of the financial

statement. It should not be left on the part of management. Further, we have discussed the

relationship between the AASB and IFRS. Based on this we can conclude that the AASB is

the convergence of the IFRS. There is no more difference in the AASB and IFRS.

At last, in the equity analysis of the four companies, we can conclude the equity of an

organization is affected by some factors i.e. issues of shares in IPO, shares issued under

options exercised, shares issued as consideration of an acquisition of any business etc. We

also conclude that Accent Group Limited has maintained the debt and equity relationship in

proper manners i.e. it has paid the debt through the issues of shares through which it converts

debt into equity.

11 | P a g e

Corporate and Finance Accounting

REFERENCES:

Accounting Tools (2017), Applicable financial reporting framework [Online] Available from:

https://www.accountingtools.com/articles/2017/5/7/applicable-financial-reporting-framework

[Assessed 04 September 2018]

AICPA (no date), IFRS FAQs [Online] Available from: https://www.ifrs.com/ifrs_faqs.html

[Assessed 04 September 2018]

Anon (2017), Financial Reporting [Online] Available from:

https://www.edupristine.com/blog/financial-reporting [Assessed 04 September 2018]

Anon (no date), Why is the United Sate not adopting the IFRS and are continuing with the

GAAP whereas most of the countries are moving to IFRS? [Online] Available from:

https://www.quora.com/Why-is-the-United-States-Canada-not-adopting-IFRS-and-are-

continuing-with-GAAP-whereas-most-of-the-other-countries-are-moving-to-IFRS [Assessed

04 September 2018]

AUASB (2009), Applicable Financial Reporting Framework [Online] Available from:

https://definedterm.com/applicable_financial_reporting_framework [Assessed 04 September

2018]

Bonner, J. (2012), Voluntary vs. Mandatory Reporting, [Online] Available from:

https://blogs.accaglobal.com/2012/10/05/voluntary-vs-mandatory-reporting/ [Assessed 04

September 2018]

Calla, H. (2011), What Affects Shareholder’s Equity? [Online] Available from:

https://www.sapling.com/8606124/affects-stockholders-equity [Assessed 04 September

2018]

David, R., 2017, Types of Transactions that Affect the Equity of the Company, [Online]

Available from: https://pocketsense.com/types-transactions-affect-equity-company-

8433302.html [Assessed 04 September 2018]

12 | P a g e

REFERENCES:

Accounting Tools (2017), Applicable financial reporting framework [Online] Available from:

https://www.accountingtools.com/articles/2017/5/7/applicable-financial-reporting-framework

[Assessed 04 September 2018]

AICPA (no date), IFRS FAQs [Online] Available from: https://www.ifrs.com/ifrs_faqs.html

[Assessed 04 September 2018]

Anon (2017), Financial Reporting [Online] Available from:

https://www.edupristine.com/blog/financial-reporting [Assessed 04 September 2018]

Anon (no date), Why is the United Sate not adopting the IFRS and are continuing with the

GAAP whereas most of the countries are moving to IFRS? [Online] Available from:

https://www.quora.com/Why-is-the-United-States-Canada-not-adopting-IFRS-and-are-

continuing-with-GAAP-whereas-most-of-the-other-countries-are-moving-to-IFRS [Assessed

04 September 2018]

AUASB (2009), Applicable Financial Reporting Framework [Online] Available from:

https://definedterm.com/applicable_financial_reporting_framework [Assessed 04 September

2018]

Bonner, J. (2012), Voluntary vs. Mandatory Reporting, [Online] Available from:

https://blogs.accaglobal.com/2012/10/05/voluntary-vs-mandatory-reporting/ [Assessed 04

September 2018]

Calla, H. (2011), What Affects Shareholder’s Equity? [Online] Available from:

https://www.sapling.com/8606124/affects-stockholders-equity [Assessed 04 September

2018]

David, R., 2017, Types of Transactions that Affect the Equity of the Company, [Online]

Available from: https://pocketsense.com/types-transactions-affect-equity-company-

8433302.html [Assessed 04 September 2018]

12 | P a g e

Corporate and Finance Accounting

Deloitte (no date), Conceptual Framework for Financial Reporting 2018 [Online] Available

from: https://www.iasplus.com/en/standards/other/framework [Assessed 04 September 2018]

Deloitte (no date), Adoption of IFRS by country [Online] Available from:

https://www.iasplus.com/en/resources/ifrs-topics/adoption-of-ifrs [Assessed 04 September

2018]

Kumaran, S. (2015), The Ten Generally Accepted Accounting Principles [Online] Available

from: https://www.invensis.net/blog/finance-and-accounting/ten-generally-accepted-

accounting-principles-gaap/ [Assessed 04 September 2018]

Gordon, E. (2015), The IASB’s Discussion Paper on the Conceptual Framework for Financial

Reporting: A Commentary and Research Review. Journal of International Financial

Management & Accounting [Online]. V. 26(1), pp (72-110), Available from:

https://onlinelibrary.wiley.com/doi/abs/10.1111/jifm.12024 [Assessed 04 September 2018]

PWC (no date), Financial Reporting Framework [Online] Available from:

https://www.pwc.com/zm/en/publications/financial-reporting-framework.html [Assessed 04

September 2018]

Rouse, M. (no date), GAAP (Generally Accepted Accounting Principles) [Online] Available

from: https://whatis.techtarget.com/definition/GAAP-generally-accepted-accounting-

principles [Assessed 04 September 2018]

Wikipedia (no date), International Financial Reporting Standards [Online] Available from:

https://en.wikipedia.org/wiki/International_Financial_Reporting_Standards [Assessed 04

September 2018]

Zacks (no date), What Items Impact Stakeholder’s Equity? [Online] Available from:

https://finance.zacks.com/items-impact-stockholders-equity-3448.html [Assessed 04

September 2018]

13 | P a g e

Deloitte (no date), Conceptual Framework for Financial Reporting 2018 [Online] Available

from: https://www.iasplus.com/en/standards/other/framework [Assessed 04 September 2018]

Deloitte (no date), Adoption of IFRS by country [Online] Available from:

https://www.iasplus.com/en/resources/ifrs-topics/adoption-of-ifrs [Assessed 04 September

2018]

Kumaran, S. (2015), The Ten Generally Accepted Accounting Principles [Online] Available

from: https://www.invensis.net/blog/finance-and-accounting/ten-generally-accepted-

accounting-principles-gaap/ [Assessed 04 September 2018]

Gordon, E. (2015), The IASB’s Discussion Paper on the Conceptual Framework for Financial

Reporting: A Commentary and Research Review. Journal of International Financial

Management & Accounting [Online]. V. 26(1), pp (72-110), Available from:

https://onlinelibrary.wiley.com/doi/abs/10.1111/jifm.12024 [Assessed 04 September 2018]

PWC (no date), Financial Reporting Framework [Online] Available from:

https://www.pwc.com/zm/en/publications/financial-reporting-framework.html [Assessed 04

September 2018]

Rouse, M. (no date), GAAP (Generally Accepted Accounting Principles) [Online] Available

from: https://whatis.techtarget.com/definition/GAAP-generally-accepted-accounting-

principles [Assessed 04 September 2018]

Wikipedia (no date), International Financial Reporting Standards [Online] Available from:

https://en.wikipedia.org/wiki/International_Financial_Reporting_Standards [Assessed 04

September 2018]

Zacks (no date), What Items Impact Stakeholder’s Equity? [Online] Available from:

https://finance.zacks.com/items-impact-stockholders-equity-3448.html [Assessed 04

September 2018]

13 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Finance Accounting

14 | P a g e

14 | P a g e

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.