ECF2222 Corporate Finance: Investment Analysis and Capital Budgeting

VerifiedAdded on 2023/06/14

|15

|4909

|192

Report

AI Summary

This report provides a comprehensive analysis of capital budgeting techniques, focusing on Net Present Value (NPV) and Internal Rate of Return (IRR) for evaluating investment opportunities. It examines two alternative investment options for a company's trawler operations, detailing the preparation of schedules, incremental cash flow analysis, and determination of NPV and IRR for each alternative. The report applies the NPV infinity approach, conducts a break-even analysis at minimum market price and maximum operating cost, and presents a scenario analysis to assess the potential outcomes. Furthermore, it evaluates the option to lease versus buy, providing recommendations to the board of directors based on the long-term value of the firm. The analysis considers factors such as inflation rates, annual catch sizes, market prices, operating costs, and salvage values to determine the most viable investment strategy. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

Running head: FINANCE

Finance

Name of the Student

Name of the University

Authors Note

Course ID

Finance

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE

Table of Contents

Introduction:...............................................................................................................................2

Preparation of schedules:...........................................................................................................2

Incremental Cash flow:..............................................................................................................3

Determination of NPV and IRR for each Alternative:...............................................................4

Application of NPV infinity Approach:.....................................................................................6

Break even analysis at minimum market price and maximum operating cost:..........................7

Scenario Analysis:....................................................................................................................10

Recommendations of the scenarios:.........................................................................................11

Evaluation of option to lease:...................................................................................................11

Conclusion:..............................................................................................................................12

Reference List:.........................................................................................................................13

Table of Contents

Introduction:...............................................................................................................................2

Preparation of schedules:...........................................................................................................2

Incremental Cash flow:..............................................................................................................3

Determination of NPV and IRR for each Alternative:...............................................................4

Application of NPV infinity Approach:.....................................................................................6

Break even analysis at minimum market price and maximum operating cost:..........................7

Scenario Analysis:....................................................................................................................10

Recommendations of the scenarios:.........................................................................................11

Evaluation of option to lease:...................................................................................................11

Conclusion:..............................................................................................................................12

Reference List:.........................................................................................................................13

2FINANCE

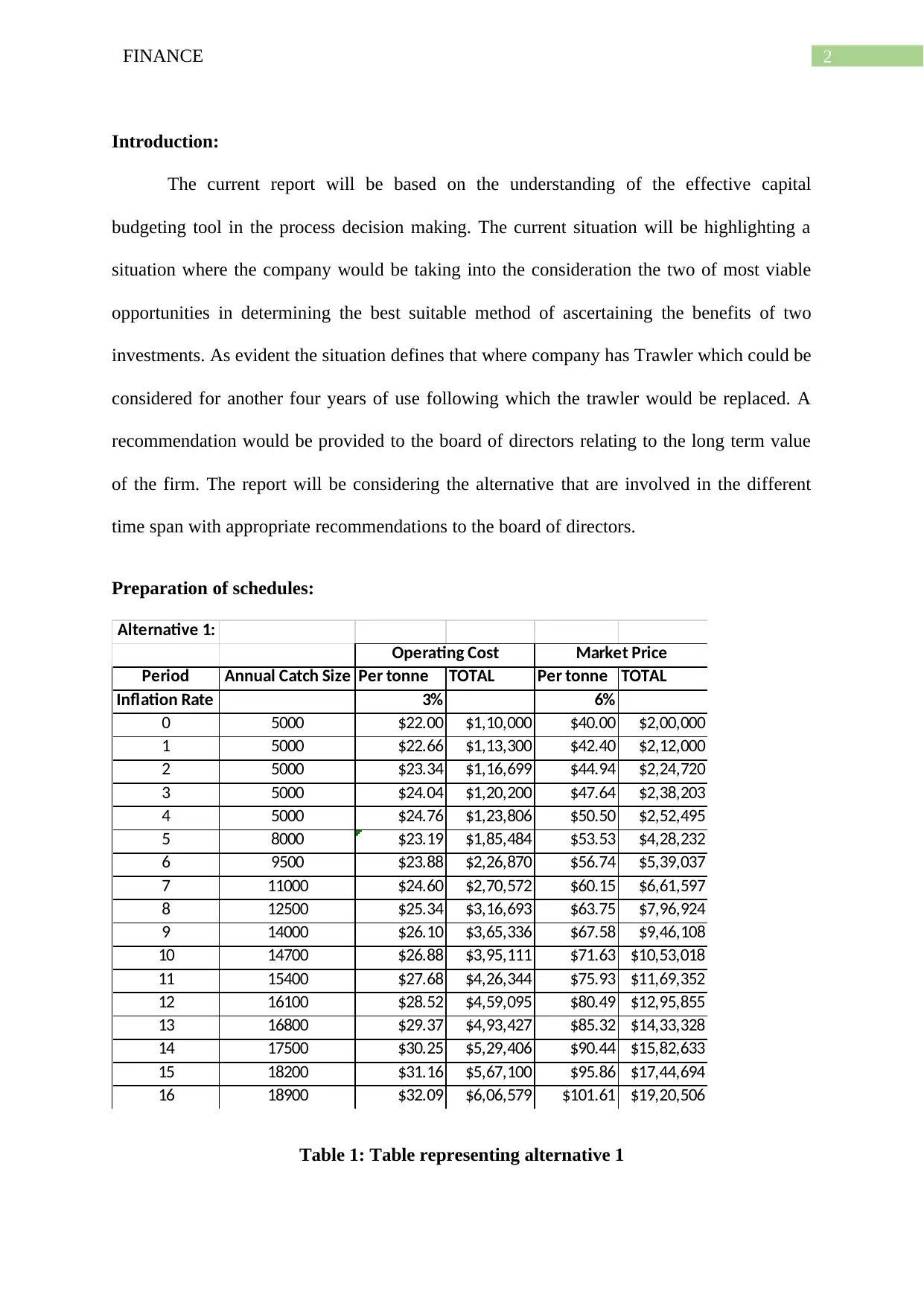

Introduction:

The current report will be based on the understanding of the effective capital

budgeting tool in the process decision making. The current situation will be highlighting a

situation where the company would be taking into the consideration the two of most viable

opportunities in determining the best suitable method of ascertaining the benefits of two

investments. As evident the situation defines that where company has Trawler which could be

considered for another four years of use following which the trawler would be replaced. A

recommendation would be provided to the board of directors relating to the long term value

of the firm. The report will be considering the alternative that are involved in the different

time span with appropriate recommendations to the board of directors.

Preparation of schedules:

Alternative 1:

Period Annual Catch Size Per tonne TOTAL Per tonne TOTAL

Inflation Rate 3% 6%

0 5000 $22.00 $1,10,000 $40.00 $2,00,000

1 5000 $22.66 $1,13,300 $42.40 $2,12,000

2 5000 $23.34 $1,16,699 $44.94 $2,24,720

3 5000 $24.04 $1,20,200 $47.64 $2,38,203

4 5000 $24.76 $1,23,806 $50.50 $2,52,495

5 8000 $23.19 $1,85,484 $53.53 $4,28,232

6 9500 $23.88 $2,26,870 $56.74 $5,39,037

7 11000 $24.60 $2,70,572 $60.15 $6,61,597

8 12500 $25.34 $3,16,693 $63.75 $7,96,924

9 14000 $26.10 $3,65,336 $67.58 $9,46,108

10 14700 $26.88 $3,95,111 $71.63 $10,53,018

11 15400 $27.68 $4,26,344 $75.93 $11,69,352

12 16100 $28.52 $4,59,095 $80.49 $12,95,855

13 16800 $29.37 $4,93,427 $85.32 $14,33,328

14 17500 $30.25 $5,29,406 $90.44 $15,82,633

15 18200 $31.16 $5,67,100 $95.86 $17,44,694

16 18900 $32.09 $6,06,579 $101.61 $19,20,506

Operating Cost Market Price

Table 1: Table representing alternative 1

Introduction:

The current report will be based on the understanding of the effective capital

budgeting tool in the process decision making. The current situation will be highlighting a

situation where the company would be taking into the consideration the two of most viable

opportunities in determining the best suitable method of ascertaining the benefits of two

investments. As evident the situation defines that where company has Trawler which could be

considered for another four years of use following which the trawler would be replaced. A

recommendation would be provided to the board of directors relating to the long term value

of the firm. The report will be considering the alternative that are involved in the different

time span with appropriate recommendations to the board of directors.

Preparation of schedules:

Alternative 1:

Period Annual Catch Size Per tonne TOTAL Per tonne TOTAL

Inflation Rate 3% 6%

0 5000 $22.00 $1,10,000 $40.00 $2,00,000

1 5000 $22.66 $1,13,300 $42.40 $2,12,000

2 5000 $23.34 $1,16,699 $44.94 $2,24,720

3 5000 $24.04 $1,20,200 $47.64 $2,38,203

4 5000 $24.76 $1,23,806 $50.50 $2,52,495

5 8000 $23.19 $1,85,484 $53.53 $4,28,232

6 9500 $23.88 $2,26,870 $56.74 $5,39,037

7 11000 $24.60 $2,70,572 $60.15 $6,61,597

8 12500 $25.34 $3,16,693 $63.75 $7,96,924

9 14000 $26.10 $3,65,336 $67.58 $9,46,108

10 14700 $26.88 $3,95,111 $71.63 $10,53,018

11 15400 $27.68 $4,26,344 $75.93 $11,69,352

12 16100 $28.52 $4,59,095 $80.49 $12,95,855

13 16800 $29.37 $4,93,427 $85.32 $14,33,328

14 17500 $30.25 $5,29,406 $90.44 $15,82,633

15 18200 $31.16 $5,67,100 $95.86 $17,44,694

16 18900 $32.09 $6,06,579 $101.61 $19,20,506

Operating Cost Market Price

Table 1: Table representing alternative 1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE

(Source: As Created by Author)

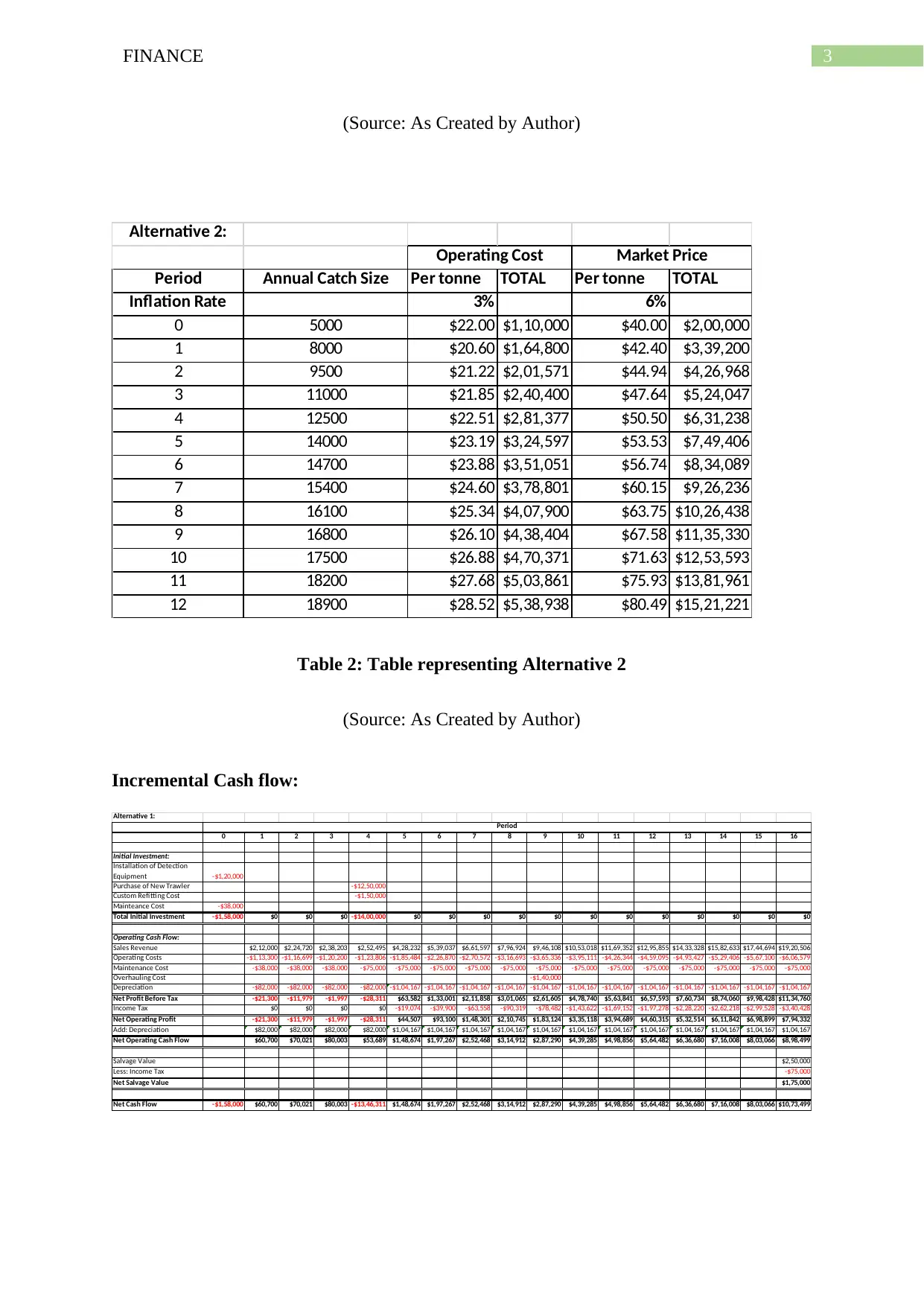

Alternative 2:

Period Annual Catch Size Per tonne TOTAL Per tonne TOTAL

Inflation Rate 3% 6%

0 5000 $22.00 $1,10,000 $40.00 $2,00,000

1 8000 $20.60 $1,64,800 $42.40 $3,39,200

2 9500 $21.22 $2,01,571 $44.94 $4,26,968

3 11000 $21.85 $2,40,400 $47.64 $5,24,047

4 12500 $22.51 $2,81,377 $50.50 $6,31,238

5 14000 $23.19 $3,24,597 $53.53 $7,49,406

6 14700 $23.88 $3,51,051 $56.74 $8,34,089

7 15400 $24.60 $3,78,801 $60.15 $9,26,236

8 16100 $25.34 $4,07,900 $63.75 $10,26,438

9 16800 $26.10 $4,38,404 $67.58 $11,35,330

10 17500 $26.88 $4,70,371 $71.63 $12,53,593

11 18200 $27.68 $5,03,861 $75.93 $13,81,961

12 18900 $28.52 $5,38,938 $80.49 $15,21,221

Operating Cost Market Price

Table 2: Table representing Alternative 2

(Source: As Created by Author)

Incremental Cash flow:

Alternative 1:

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Initial Investment:

Installation of Detection

Equipment -$1,20,000

Purchase of New Trawler -$12,50,000

Custom Refitting Cost -$1,50,000

Mainteance Cost -$38,000

Total Initial Investment -$1,58,000 $0 $0 $0 -$14,00,000 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Operating Cash Flow:

Sales Revenue $2,12,000 $2,24,720 $2,38,203 $2,52,495 $4,28,232 $5,39,037 $6,61,597 $7,96,924 $9,46,108 $10,53,018 $11,69,352 $12,95,855 $14,33,328 $15,82,633 $17,44,694 $19,20,506

Operating Costs -$1,13,300 -$1,16,699 -$1,20,200 -$1,23,806 -$1,85,484 -$2,26,870 -$2,70,572 -$3,16,693 -$3,65,336 -$3,95,111 -$4,26,344 -$4,59,095 -$4,93,427 -$5,29,406 -$5,67,100 -$6,06,579

Maintenance Cost -$38,000 -$38,000 -$38,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000

Overhauling Cost -$1,40,000

Depreciation -$82,000 -$82,000 -$82,000 -$82,000 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167

Net Profit Before Tax -$21,300 -$11,979 -$1,997 -$28,311 $63,582 $1,33,001 $2,11,858 $3,01,065 $2,61,605 $4,78,740 $5,63,841 $6,57,593 $7,60,734 $8,74,060 $9,98,428 $11,34,760

Income Tax $0 $0 $0 $0 -$19,074 -$39,900 -$63,558 -$90,319 -$78,482 -$1,43,622 -$1,69,152 -$1,97,278 -$2,28,220 -$2,62,218 -$2,99,528 -$3,40,428

Net Operating Profit -$21,300 -$11,979 -$1,997 -$28,311 $44,507 $93,100 $1,48,301 $2,10,745 $1,83,124 $3,35,118 $3,94,689 $4,60,315 $5,32,514 $6,11,842 $6,98,899 $7,94,332

Add: Depreciation $82,000 $82,000 $82,000 $82,000 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167

Net Operating Cash Flow $60,700 $70,021 $80,003 $53,689 $1,48,674 $1,97,267 $2,52,468 $3,14,912 $2,87,290 $4,39,285 $4,98,856 $5,64,482 $6,36,680 $7,16,008 $8,03,066 $8,98,499

Salvage Value $2,50,000

Less: Income Tax -$75,000

Net Salvage Value $1,75,000

Net Cash Flow -$1,58,000 $60,700 $70,021 $80,003 -$13,46,311 $1,48,674 $1,97,267 $2,52,468 $3,14,912 $2,87,290 $4,39,285 $4,98,856 $5,64,482 $6,36,680 $7,16,008 $8,03,066 $10,73,499

Period

(Source: As Created by Author)

Alternative 2:

Period Annual Catch Size Per tonne TOTAL Per tonne TOTAL

Inflation Rate 3% 6%

0 5000 $22.00 $1,10,000 $40.00 $2,00,000

1 8000 $20.60 $1,64,800 $42.40 $3,39,200

2 9500 $21.22 $2,01,571 $44.94 $4,26,968

3 11000 $21.85 $2,40,400 $47.64 $5,24,047

4 12500 $22.51 $2,81,377 $50.50 $6,31,238

5 14000 $23.19 $3,24,597 $53.53 $7,49,406

6 14700 $23.88 $3,51,051 $56.74 $8,34,089

7 15400 $24.60 $3,78,801 $60.15 $9,26,236

8 16100 $25.34 $4,07,900 $63.75 $10,26,438

9 16800 $26.10 $4,38,404 $67.58 $11,35,330

10 17500 $26.88 $4,70,371 $71.63 $12,53,593

11 18200 $27.68 $5,03,861 $75.93 $13,81,961

12 18900 $28.52 $5,38,938 $80.49 $15,21,221

Operating Cost Market Price

Table 2: Table representing Alternative 2

(Source: As Created by Author)

Incremental Cash flow:

Alternative 1:

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Initial Investment:

Installation of Detection

Equipment -$1,20,000

Purchase of New Trawler -$12,50,000

Custom Refitting Cost -$1,50,000

Mainteance Cost -$38,000

Total Initial Investment -$1,58,000 $0 $0 $0 -$14,00,000 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Operating Cash Flow:

Sales Revenue $2,12,000 $2,24,720 $2,38,203 $2,52,495 $4,28,232 $5,39,037 $6,61,597 $7,96,924 $9,46,108 $10,53,018 $11,69,352 $12,95,855 $14,33,328 $15,82,633 $17,44,694 $19,20,506

Operating Costs -$1,13,300 -$1,16,699 -$1,20,200 -$1,23,806 -$1,85,484 -$2,26,870 -$2,70,572 -$3,16,693 -$3,65,336 -$3,95,111 -$4,26,344 -$4,59,095 -$4,93,427 -$5,29,406 -$5,67,100 -$6,06,579

Maintenance Cost -$38,000 -$38,000 -$38,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000

Overhauling Cost -$1,40,000

Depreciation -$82,000 -$82,000 -$82,000 -$82,000 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167

Net Profit Before Tax -$21,300 -$11,979 -$1,997 -$28,311 $63,582 $1,33,001 $2,11,858 $3,01,065 $2,61,605 $4,78,740 $5,63,841 $6,57,593 $7,60,734 $8,74,060 $9,98,428 $11,34,760

Income Tax $0 $0 $0 $0 -$19,074 -$39,900 -$63,558 -$90,319 -$78,482 -$1,43,622 -$1,69,152 -$1,97,278 -$2,28,220 -$2,62,218 -$2,99,528 -$3,40,428

Net Operating Profit -$21,300 -$11,979 -$1,997 -$28,311 $44,507 $93,100 $1,48,301 $2,10,745 $1,83,124 $3,35,118 $3,94,689 $4,60,315 $5,32,514 $6,11,842 $6,98,899 $7,94,332

Add: Depreciation $82,000 $82,000 $82,000 $82,000 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167

Net Operating Cash Flow $60,700 $70,021 $80,003 $53,689 $1,48,674 $1,97,267 $2,52,468 $3,14,912 $2,87,290 $4,39,285 $4,98,856 $5,64,482 $6,36,680 $7,16,008 $8,03,066 $8,98,499

Salvage Value $2,50,000

Less: Income Tax -$75,000

Net Salvage Value $1,75,000

Net Cash Flow -$1,58,000 $60,700 $70,021 $80,003 -$13,46,311 $1,48,674 $1,97,267 $2,52,468 $3,14,912 $2,87,290 $4,39,285 $4,98,856 $5,64,482 $6,36,680 $7,16,008 $8,03,066 $10,73,499

Period

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE

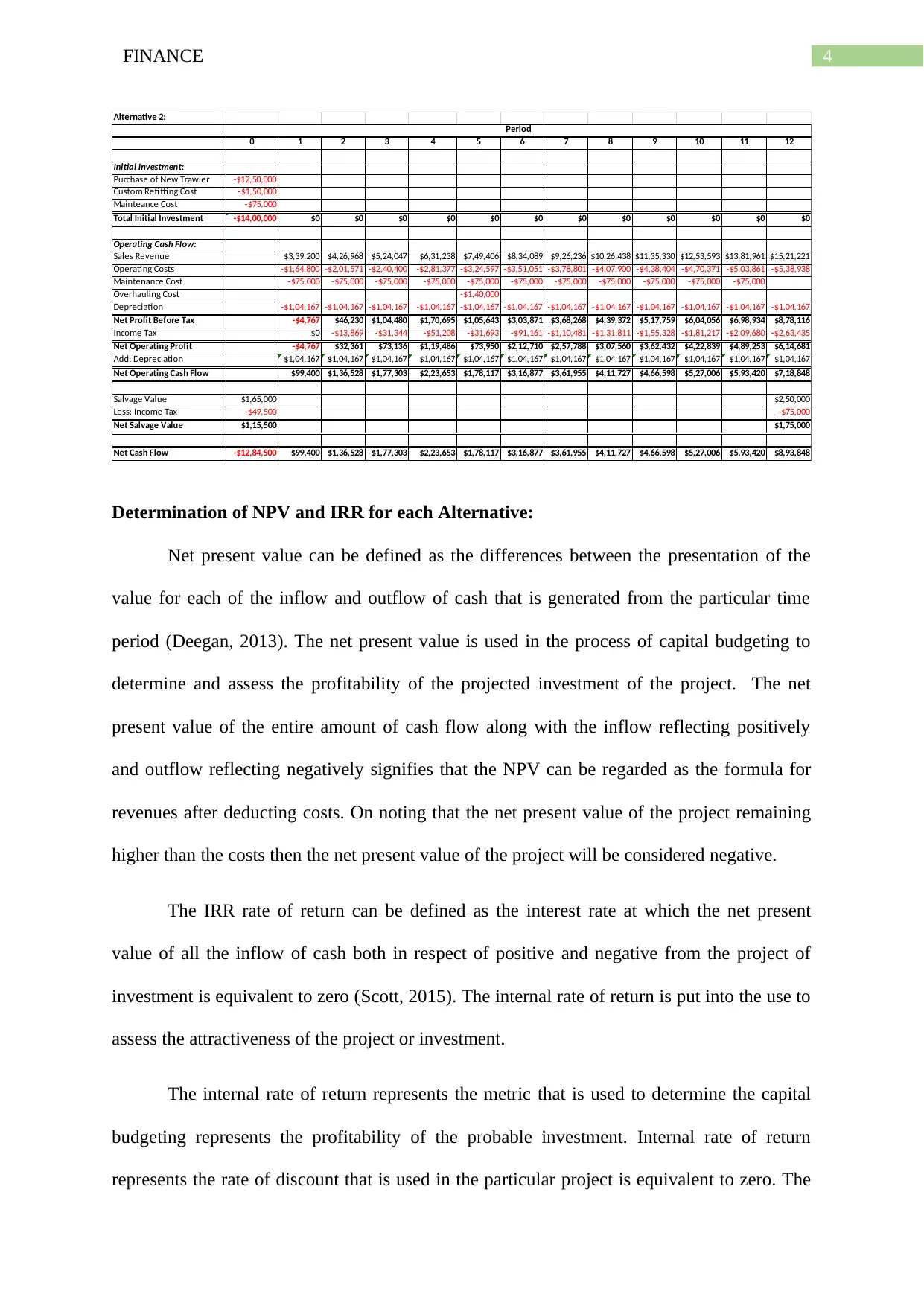

Alternative 2:

0 1 2 3 4 5 6 7 8 9 10 11 12

Initial Investment:

Purchase of New Trawler -$12,50,000

Custom Refitting Cost -$1,50,000

Mainteance Cost -$75,000

Total Initial Investment -$14,00,000 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Operating Cash Flow:

Sales Revenue $3,39,200 $4,26,968 $5,24,047 $6,31,238 $7,49,406 $8,34,089 $9,26,236 $10,26,438 $11,35,330 $12,53,593 $13,81,961 $15,21,221

Operating Costs -$1,64,800 -$2,01,571 -$2,40,400 -$2,81,377 -$3,24,597 -$3,51,051 -$3,78,801 -$4,07,900 -$4,38,404 -$4,70,371 -$5,03,861 -$5,38,938

Maintenance Cost -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000

Overhauling Cost -$1,40,000

Depreciation -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167

Net Profit Before Tax -$4,767 $46,230 $1,04,480 $1,70,695 $1,05,643 $3,03,871 $3,68,268 $4,39,372 $5,17,759 $6,04,056 $6,98,934 $8,78,116

Income Tax $0 -$13,869 -$31,344 -$51,208 -$31,693 -$91,161 -$1,10,481 -$1,31,811 -$1,55,328 -$1,81,217 -$2,09,680 -$2,63,435

Net Operating Profit -$4,767 $32,361 $73,136 $1,19,486 $73,950 $2,12,710 $2,57,788 $3,07,560 $3,62,432 $4,22,839 $4,89,253 $6,14,681

Add: Depreciation $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167

Net Operating Cash Flow $99,400 $1,36,528 $1,77,303 $2,23,653 $1,78,117 $3,16,877 $3,61,955 $4,11,727 $4,66,598 $5,27,006 $5,93,420 $7,18,848

Salvage Value $1,65,000 $2,50,000

Less: Income Tax -$49,500 -$75,000

Net Salvage Value $1,15,500 $1,75,000

Net Cash Flow -$12,84,500 $99,400 $1,36,528 $1,77,303 $2,23,653 $1,78,117 $3,16,877 $3,61,955 $4,11,727 $4,66,598 $5,27,006 $5,93,420 $8,93,848

Period

Determination of NPV and IRR for each Alternative:

Net present value can be defined as the differences between the presentation of the

value for each of the inflow and outflow of cash that is generated from the particular time

period (Deegan, 2013). The net present value is used in the process of capital budgeting to

determine and assess the profitability of the projected investment of the project. The net

present value of the entire amount of cash flow along with the inflow reflecting positively

and outflow reflecting negatively signifies that the NPV can be regarded as the formula for

revenues after deducting costs. On noting that the net present value of the project remaining

higher than the costs then the net present value of the project will be considered negative.

The IRR rate of return can be defined as the interest rate at which the net present

value of all the inflow of cash both in respect of positive and negative from the project of

investment is equivalent to zero (Scott, 2015). The internal rate of return is put into the use to

assess the attractiveness of the project or investment.

The internal rate of return represents the metric that is used to determine the capital

budgeting represents the profitability of the probable investment. Internal rate of return

represents the rate of discount that is used in the particular project is equivalent to zero. The

Alternative 2:

0 1 2 3 4 5 6 7 8 9 10 11 12

Initial Investment:

Purchase of New Trawler -$12,50,000

Custom Refitting Cost -$1,50,000

Mainteance Cost -$75,000

Total Initial Investment -$14,00,000 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Operating Cash Flow:

Sales Revenue $3,39,200 $4,26,968 $5,24,047 $6,31,238 $7,49,406 $8,34,089 $9,26,236 $10,26,438 $11,35,330 $12,53,593 $13,81,961 $15,21,221

Operating Costs -$1,64,800 -$2,01,571 -$2,40,400 -$2,81,377 -$3,24,597 -$3,51,051 -$3,78,801 -$4,07,900 -$4,38,404 -$4,70,371 -$5,03,861 -$5,38,938

Maintenance Cost -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000 -$75,000

Overhauling Cost -$1,40,000

Depreciation -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167 -$1,04,167

Net Profit Before Tax -$4,767 $46,230 $1,04,480 $1,70,695 $1,05,643 $3,03,871 $3,68,268 $4,39,372 $5,17,759 $6,04,056 $6,98,934 $8,78,116

Income Tax $0 -$13,869 -$31,344 -$51,208 -$31,693 -$91,161 -$1,10,481 -$1,31,811 -$1,55,328 -$1,81,217 -$2,09,680 -$2,63,435

Net Operating Profit -$4,767 $32,361 $73,136 $1,19,486 $73,950 $2,12,710 $2,57,788 $3,07,560 $3,62,432 $4,22,839 $4,89,253 $6,14,681

Add: Depreciation $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167 $1,04,167

Net Operating Cash Flow $99,400 $1,36,528 $1,77,303 $2,23,653 $1,78,117 $3,16,877 $3,61,955 $4,11,727 $4,66,598 $5,27,006 $5,93,420 $7,18,848

Salvage Value $1,65,000 $2,50,000

Less: Income Tax -$49,500 -$75,000

Net Salvage Value $1,15,500 $1,75,000

Net Cash Flow -$12,84,500 $99,400 $1,36,528 $1,77,303 $2,23,653 $1,78,117 $3,16,877 $3,61,955 $4,11,727 $4,66,598 $5,27,006 $5,93,420 $8,93,848

Period

Determination of NPV and IRR for each Alternative:

Net present value can be defined as the differences between the presentation of the

value for each of the inflow and outflow of cash that is generated from the particular time

period (Deegan, 2013). The net present value is used in the process of capital budgeting to

determine and assess the profitability of the projected investment of the project. The net

present value of the entire amount of cash flow along with the inflow reflecting positively

and outflow reflecting negatively signifies that the NPV can be regarded as the formula for

revenues after deducting costs. On noting that the net present value of the project remaining

higher than the costs then the net present value of the project will be considered negative.

The IRR rate of return can be defined as the interest rate at which the net present

value of all the inflow of cash both in respect of positive and negative from the project of

investment is equivalent to zero (Scott, 2015). The internal rate of return is put into the use to

assess the attractiveness of the project or investment.

The internal rate of return represents the metric that is used to determine the capital

budgeting represents the profitability of the probable investment. Internal rate of return

represents the rate of discount that is used in the particular project is equivalent to zero. The

5FINANCE

higher the internal rate of return on the project the greater would be the amount of the cash

flow that exceeds the cost of capital resulting in higher amount of cash flow to the investors

(Williams, 2014). An organization would prefer a lower amount of IRR for the project that

are small in size while a project with large amount of outlay would be requiring higher

amount of internal rate of return due to the higher amount of cash flow that is generated from

the larger project.

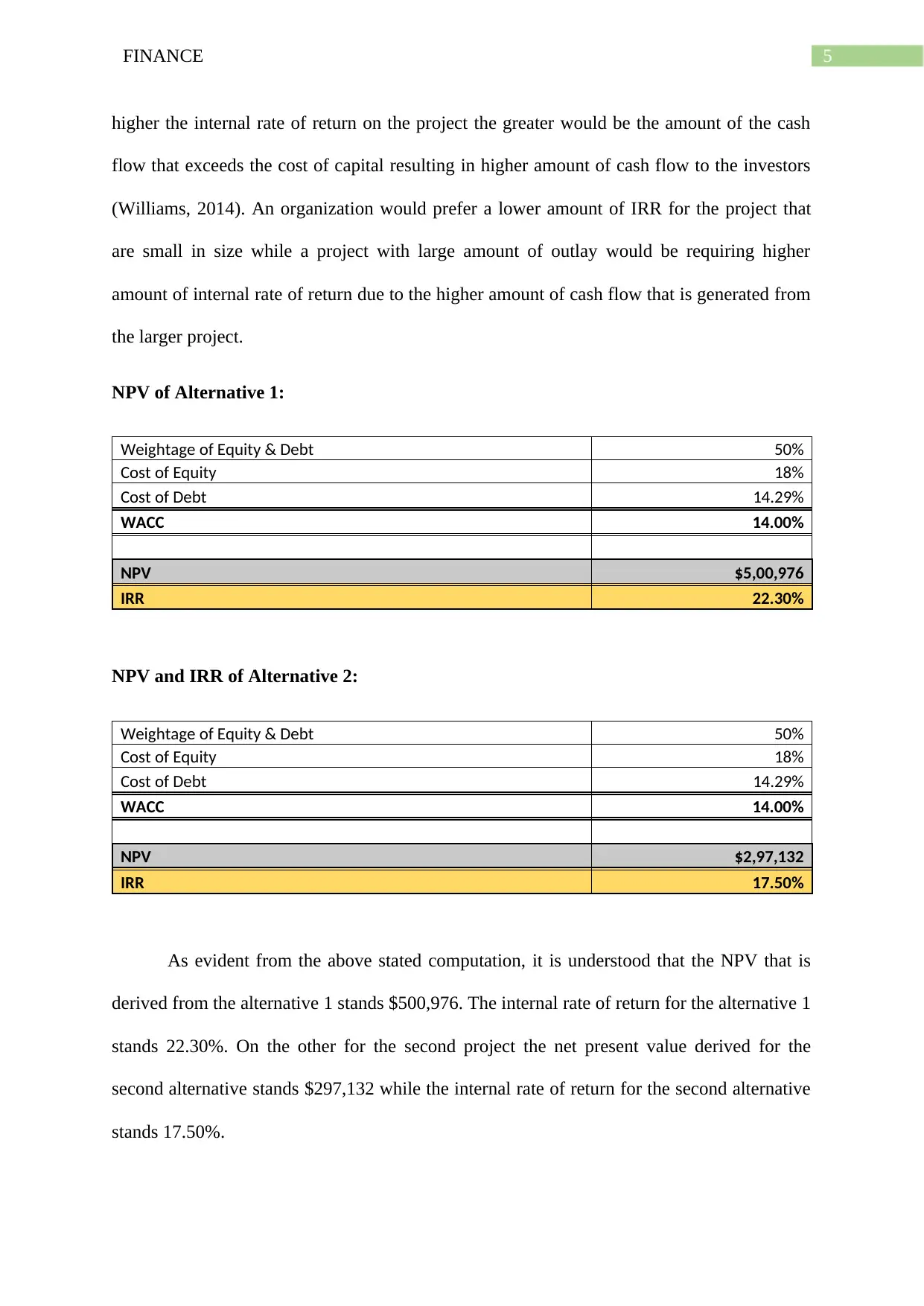

NPV of Alternative 1:

Weightage of Equity & Debt 50%

Cost of Equity 18%

Cost of Debt 14.29%

WACC 14.00%

NPV $5,00,976

IRR 22.30%

NPV and IRR of Alternative 2:

Weightage of Equity & Debt 50%

Cost of Equity 18%

Cost of Debt 14.29%

WACC 14.00%

NPV $2,97,132

IRR 17.50%

As evident from the above stated computation, it is understood that the NPV that is

derived from the alternative 1 stands $500,976. The internal rate of return for the alternative 1

stands 22.30%. On the other for the second project the net present value derived for the

second alternative stands $297,132 while the internal rate of return for the second alternative

stands 17.50%.

higher the internal rate of return on the project the greater would be the amount of the cash

flow that exceeds the cost of capital resulting in higher amount of cash flow to the investors

(Williams, 2014). An organization would prefer a lower amount of IRR for the project that

are small in size while a project with large amount of outlay would be requiring higher

amount of internal rate of return due to the higher amount of cash flow that is generated from

the larger project.

NPV of Alternative 1:

Weightage of Equity & Debt 50%

Cost of Equity 18%

Cost of Debt 14.29%

WACC 14.00%

NPV $5,00,976

IRR 22.30%

NPV and IRR of Alternative 2:

Weightage of Equity & Debt 50%

Cost of Equity 18%

Cost of Debt 14.29%

WACC 14.00%

NPV $2,97,132

IRR 17.50%

As evident from the above stated computation, it is understood that the NPV that is

derived from the alternative 1 stands $500,976. The internal rate of return for the alternative 1

stands 22.30%. On the other for the second project the net present value derived for the

second alternative stands $297,132 while the internal rate of return for the second alternative

stands 17.50%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE

An important assertion can be bought forward by stating that the NPV of the

Alternative 1 is higher than the NPV of the Alternative 2. Additionally, the viability of the

project in contest to generating higher amount of cash flow is higher. The higher amount of

cash flow for Alternative 1 represents the net present value of the entire amount of cash flow

along with the inflow reflecting positively and outflow reflecting negatively signifies that the

NPV can be regarded as the most viable of the two alternatives (Warren & Jones, 2018).

Application of NPV infinity Approach:

The basic principles of the application of the net present value approach is how the

amount of dollars are impacted by the compound interest and current value computation that

can be put into the use to make the better business decision (Henderson et al., 2015). There

are large number of alternatives for assessing the capital budgeting procedure. This comprises

of the net present value, accounting rate of return and the internal rate of return and payback.

The net present value helps in offsetting the present value of the investment cash flow

against the present value of the cash outflows. Present value of the amounts is computed by

making use of the company’s yearly cost of capital (Magni & Martin, 2017). The cost of

capital represents the theoretical cost of capital that is occurred by the organization. The cost

might be determined with the reference of the interest rates based on the debt and the

blending of the debt equity costs.

In the present context of Trawler, the tool of internal rate of return and the net present

value is computed for each investment opportunity. In the present context the tool of capital

budgeting framework is computed to derive the viability of each of the options as the highest

internal rate of return representing the positive amount of cash flow generated from each of

the product (Liu et al., 2017). In contrast to the net present value the general decision rule is

that accepting the project with the positive cash flow or in other words the net present value

An important assertion can be bought forward by stating that the NPV of the

Alternative 1 is higher than the NPV of the Alternative 2. Additionally, the viability of the

project in contest to generating higher amount of cash flow is higher. The higher amount of

cash flow for Alternative 1 represents the net present value of the entire amount of cash flow

along with the inflow reflecting positively and outflow reflecting negatively signifies that the

NPV can be regarded as the most viable of the two alternatives (Warren & Jones, 2018).

Application of NPV infinity Approach:

The basic principles of the application of the net present value approach is how the

amount of dollars are impacted by the compound interest and current value computation that

can be put into the use to make the better business decision (Henderson et al., 2015). There

are large number of alternatives for assessing the capital budgeting procedure. This comprises

of the net present value, accounting rate of return and the internal rate of return and payback.

The net present value helps in offsetting the present value of the investment cash flow

against the present value of the cash outflows. Present value of the amounts is computed by

making use of the company’s yearly cost of capital (Magni & Martin, 2017). The cost of

capital represents the theoretical cost of capital that is occurred by the organization. The cost

might be determined with the reference of the interest rates based on the debt and the

blending of the debt equity costs.

In the present context of Trawler, the tool of internal rate of return and the net present

value is computed for each investment opportunity. In the present context the tool of capital

budgeting framework is computed to derive the viability of each of the options as the highest

internal rate of return representing the positive amount of cash flow generated from each of

the product (Liu et al., 2017). In contrast to the net present value the general decision rule is

that accepting the project with the positive cash flow or in other words the net present value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE

is subjected to the accessibility of the capital. In the current context of the HFC the manual

computation of internal rate of return by making use of the net present value table is

considered to be challenging. However, the positive net present value derived for the project

explains the viability of the capital.

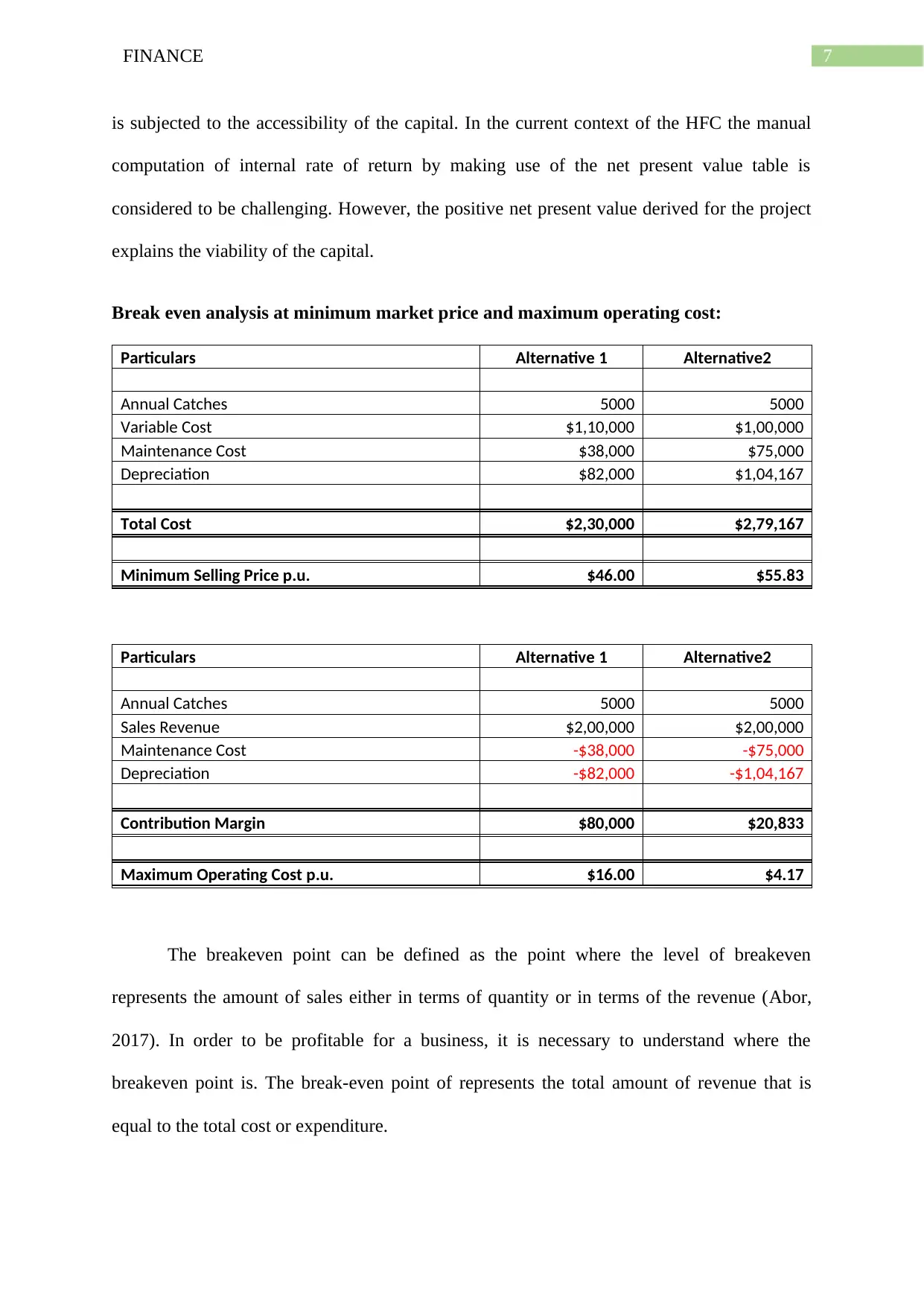

Break even analysis at minimum market price and maximum operating cost:

Particulars Alternative 1 Alternative2

Annual Catches 5000 5000

Variable Cost $1,10,000 $1,00,000

Maintenance Cost $38,000 $75,000

Depreciation $82,000 $1,04,167

Total Cost $2,30,000 $2,79,167

Minimum Selling Price p.u. $46.00 $55.83

Particulars Alternative 1 Alternative2

Annual Catches 5000 5000

Sales Revenue $2,00,000 $2,00,000

Maintenance Cost -$38,000 -$75,000

Depreciation -$82,000 -$1,04,167

Contribution Margin $80,000 $20,833

Maximum Operating Cost p.u. $16.00 $4.17

The breakeven point can be defined as the point where the level of breakeven

represents the amount of sales either in terms of quantity or in terms of the revenue (Abor,

2017). In order to be profitable for a business, it is necessary to understand where the

breakeven point is. The break-even point of represents the total amount of revenue that is

equal to the total cost or expenditure.

is subjected to the accessibility of the capital. In the current context of the HFC the manual

computation of internal rate of return by making use of the net present value table is

considered to be challenging. However, the positive net present value derived for the project

explains the viability of the capital.

Break even analysis at minimum market price and maximum operating cost:

Particulars Alternative 1 Alternative2

Annual Catches 5000 5000

Variable Cost $1,10,000 $1,00,000

Maintenance Cost $38,000 $75,000

Depreciation $82,000 $1,04,167

Total Cost $2,30,000 $2,79,167

Minimum Selling Price p.u. $46.00 $55.83

Particulars Alternative 1 Alternative2

Annual Catches 5000 5000

Sales Revenue $2,00,000 $2,00,000

Maintenance Cost -$38,000 -$75,000

Depreciation -$82,000 -$1,04,167

Contribution Margin $80,000 $20,833

Maximum Operating Cost p.u. $16.00 $4.17

The breakeven point can be defined as the point where the level of breakeven

represents the amount of sales either in terms of quantity or in terms of the revenue (Abor,

2017). In order to be profitable for a business, it is necessary to understand where the

breakeven point is. The break-even point of represents the total amount of revenue that is

equal to the total cost or expenditure.

8FINANCE

Taking into the consideration of the business feasibility and unfeasibility of

investment an important assertion can be bought forward by stating that minimum selling

price per unit stands under alternative 1 at $46.00. However, during the first year of operation

the market price per tonne under the first alternative stands $42.40. Therefore, it can be stated

that the business would not be able to generate profit since the market price per tonne is

below the minimum selling price per unit (Magni & Martin, 2017). However, the business

gains profit from the following years as from the third year on wards the market price per

tonne is higher than the minimum selling price per unit.

Similarly, for the second alternative the minimum selling price per unit stands $55.83

while for the market price per tonne is lower (Burns & Walker, 2015). The second alternative

provides that the minimum selling price stands $55.83 while the market price per unit at the

first year stands $42.40. But in the following years the business gains profit from the

following years as from the third year on wards the market price per tonne is higher than the

minimum selling price per unit.

The preparation of the schedule is associated with the determination of the market

price per tonne of fish, operating cost per tonne of fish along with the yearly catch size for

each of the alternative considered (Andor et al., 2015). At the time of preparing the schedules

of market price per tonne of fish, operating costs and yearly catch size for the alternatives, the

schedule would be tracking the impact of the inflation created on the variables considered in

market price and operating cost per tonne. The schedule prepared acts as an important tool in

determining the yearly revenues and operating cost before tax. Moving on the operating

costs, an assertion can be bought forward by stating that operating cost can be defined as the

operating expenses of the ongoing costs that are involved in the running of the project

business or product.

Taking into the consideration of the business feasibility and unfeasibility of

investment an important assertion can be bought forward by stating that minimum selling

price per unit stands under alternative 1 at $46.00. However, during the first year of operation

the market price per tonne under the first alternative stands $42.40. Therefore, it can be stated

that the business would not be able to generate profit since the market price per tonne is

below the minimum selling price per unit (Magni & Martin, 2017). However, the business

gains profit from the following years as from the third year on wards the market price per

tonne is higher than the minimum selling price per unit.

Similarly, for the second alternative the minimum selling price per unit stands $55.83

while for the market price per tonne is lower (Burns & Walker, 2015). The second alternative

provides that the minimum selling price stands $55.83 while the market price per unit at the

first year stands $42.40. But in the following years the business gains profit from the

following years as from the third year on wards the market price per tonne is higher than the

minimum selling price per unit.

The preparation of the schedule is associated with the determination of the market

price per tonne of fish, operating cost per tonne of fish along with the yearly catch size for

each of the alternative considered (Andor et al., 2015). At the time of preparing the schedules

of market price per tonne of fish, operating costs and yearly catch size for the alternatives, the

schedule would be tracking the impact of the inflation created on the variables considered in

market price and operating cost per tonne. The schedule prepared acts as an important tool in

determining the yearly revenues and operating cost before tax. Moving on the operating

costs, an assertion can be bought forward by stating that operating cost can be defined as the

operating expenses of the ongoing costs that are involved in the running of the project

business or product.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE

The operating costs is regarded as the counter part of the capital expenditure that

involves cost occurred in the development of product or offering non-consumable parts of the

products (Ağca & Mozumdar, 2017). In the current context an assertion can be bought

forward by stating that the operating cost that is incurred on the trawler is based on the cost

occurred in respect of per tonne. In the current respect the operating costs takes into the

considerations cost that are incurred on the worker and facility expenditure.

Similarly, the evidences that has been obtained from the computation states that

market price per tonne during the first year of inflation stood $212,000 with total operating

costs standing $113,300 respectively (Derouiche et al., 2017). On arriving at the final year the

rate of inflation stood 3% and the total amount of cost that is incurred at the annual catch size

of 18900 the company obtains the market price of $19,20,506. Under the first alternative the

operating cost per tonne stands $32.09 at the final year of inflation period. On the other hand,

the market price per tonne under the first alternative at the market final year of inflation

period stands $101.61.

Similarly, on the second alternative it is noticed that the annual catch size at 5000 the

operating cost per tonne stands $22 for each unit with total operating cost standing $110000.

Later the market price per tonne at $40 per unit signifies the total of $200,000 per tonne

(Moshirian et al., 2017). On arriving at the 12th period the annual catch size increases to

18900 with operating cost per tonne standing $28.52 and total operating cost per tonne

standing $538,938. On the other hand, the market price per tonne at the 18900 annual catch

size stands $80.49 with total market price standing $15,21,221.

As evident from the above stated situation it can be stated that Alternative 1 is the best

suited from the other alternative (Andrén & Jankensgård, 2015). The alternative derived from

the situation states that Alternative 1 is considered to be viable option.

The operating costs is regarded as the counter part of the capital expenditure that

involves cost occurred in the development of product or offering non-consumable parts of the

products (Ağca & Mozumdar, 2017). In the current context an assertion can be bought

forward by stating that the operating cost that is incurred on the trawler is based on the cost

occurred in respect of per tonne. In the current respect the operating costs takes into the

considerations cost that are incurred on the worker and facility expenditure.

Similarly, the evidences that has been obtained from the computation states that

market price per tonne during the first year of inflation stood $212,000 with total operating

costs standing $113,300 respectively (Derouiche et al., 2017). On arriving at the final year the

rate of inflation stood 3% and the total amount of cost that is incurred at the annual catch size

of 18900 the company obtains the market price of $19,20,506. Under the first alternative the

operating cost per tonne stands $32.09 at the final year of inflation period. On the other hand,

the market price per tonne under the first alternative at the market final year of inflation

period stands $101.61.

Similarly, on the second alternative it is noticed that the annual catch size at 5000 the

operating cost per tonne stands $22 for each unit with total operating cost standing $110000.

Later the market price per tonne at $40 per unit signifies the total of $200,000 per tonne

(Moshirian et al., 2017). On arriving at the 12th period the annual catch size increases to

18900 with operating cost per tonne standing $28.52 and total operating cost per tonne

standing $538,938. On the other hand, the market price per tonne at the 18900 annual catch

size stands $80.49 with total market price standing $15,21,221.

As evident from the above stated situation it can be stated that Alternative 1 is the best

suited from the other alternative (Andrén & Jankensgård, 2015). The alternative derived from

the situation states that Alternative 1 is considered to be viable option.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE

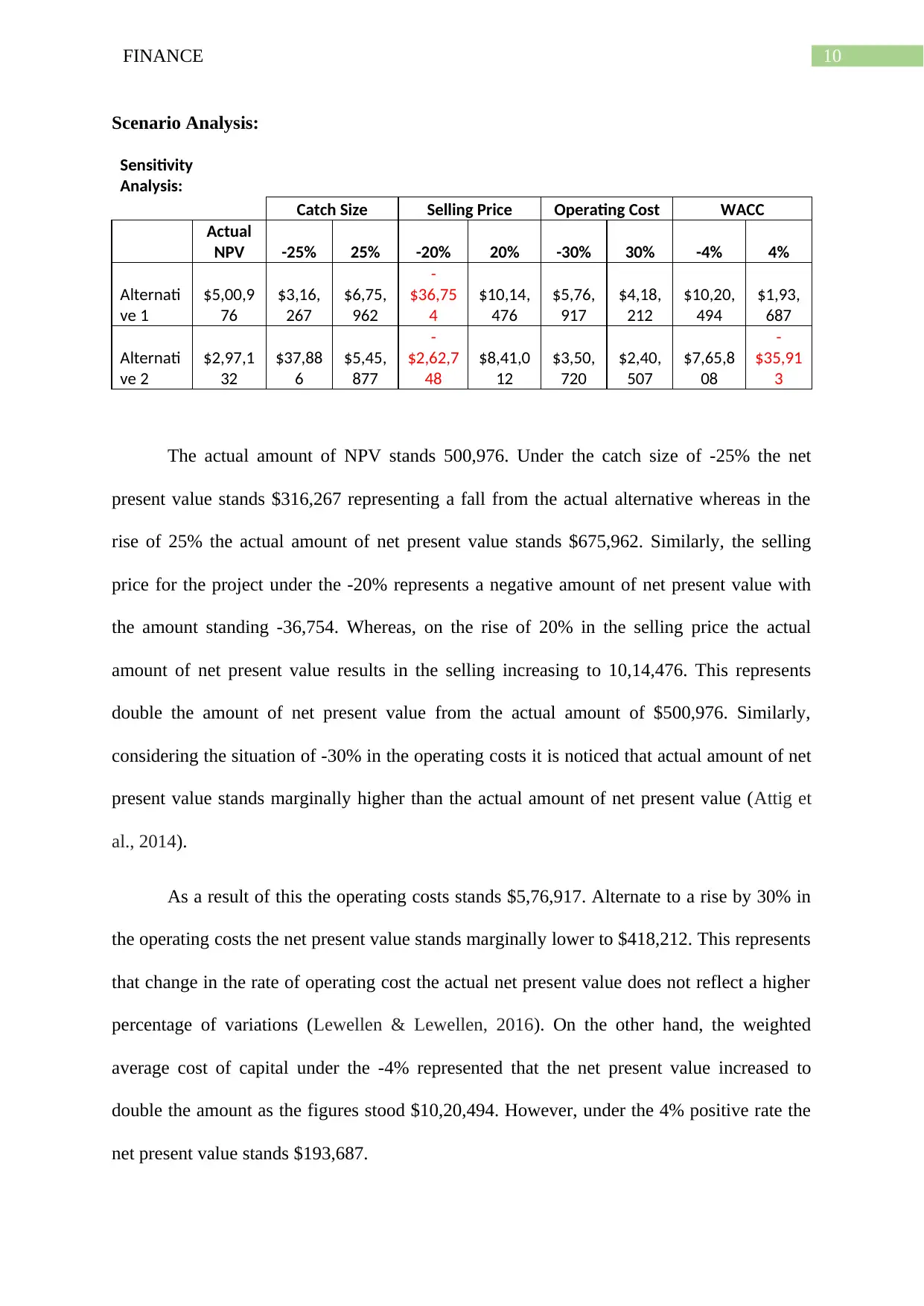

Scenario Analysis:

Sensitivity

Analysis:

Catch Size Selling Price Operating Cost WACC

Actual

NPV -25% 25% -20% 20% -30% 30% -4% 4%

Alternati

ve 1

$5,00,9

76

$3,16,

267

$6,75,

962

-

$36,75

4

$10,14,

476

$5,76,

917

$4,18,

212

$10,20,

494

$1,93,

687

Alternati

ve 2

$2,97,1

32

$37,88

6

$5,45,

877

-

$2,62,7

48

$8,41,0

12

$3,50,

720

$2,40,

507

$7,65,8

08

-

$35,91

3

The actual amount of NPV stands 500,976. Under the catch size of -25% the net

present value stands $316,267 representing a fall from the actual alternative whereas in the

rise of 25% the actual amount of net present value stands $675,962. Similarly, the selling

price for the project under the -20% represents a negative amount of net present value with

the amount standing -36,754. Whereas, on the rise of 20% in the selling price the actual

amount of net present value results in the selling increasing to 10,14,476. This represents

double the amount of net present value from the actual amount of $500,976. Similarly,

considering the situation of -30% in the operating costs it is noticed that actual amount of net

present value stands marginally higher than the actual amount of net present value (Attig et

al., 2014).

As a result of this the operating costs stands $5,76,917. Alternate to a rise by 30% in

the operating costs the net present value stands marginally lower to $418,212. This represents

that change in the rate of operating cost the actual net present value does not reflect a higher

percentage of variations (Lewellen & Lewellen, 2016). On the other hand, the weighted

average cost of capital under the -4% represented that the net present value increased to

double the amount as the figures stood $10,20,494. However, under the 4% positive rate the

net present value stands $193,687.

Scenario Analysis:

Sensitivity

Analysis:

Catch Size Selling Price Operating Cost WACC

Actual

NPV -25% 25% -20% 20% -30% 30% -4% 4%

Alternati

ve 1

$5,00,9

76

$3,16,

267

$6,75,

962

-

$36,75

4

$10,14,

476

$5,76,

917

$4,18,

212

$10,20,

494

$1,93,

687

Alternati

ve 2

$2,97,1

32

$37,88

6

$5,45,

877

-

$2,62,7

48

$8,41,0

12

$3,50,

720

$2,40,

507

$7,65,8

08

-

$35,91

3

The actual amount of NPV stands 500,976. Under the catch size of -25% the net

present value stands $316,267 representing a fall from the actual alternative whereas in the

rise of 25% the actual amount of net present value stands $675,962. Similarly, the selling

price for the project under the -20% represents a negative amount of net present value with

the amount standing -36,754. Whereas, on the rise of 20% in the selling price the actual

amount of net present value results in the selling increasing to 10,14,476. This represents

double the amount of net present value from the actual amount of $500,976. Similarly,

considering the situation of -30% in the operating costs it is noticed that actual amount of net

present value stands marginally higher than the actual amount of net present value (Attig et

al., 2014).

As a result of this the operating costs stands $5,76,917. Alternate to a rise by 30% in

the operating costs the net present value stands marginally lower to $418,212. This represents

that change in the rate of operating cost the actual net present value does not reflect a higher

percentage of variations (Lewellen & Lewellen, 2016). On the other hand, the weighted

average cost of capital under the -4% represented that the net present value increased to

double the amount as the figures stood $10,20,494. However, under the 4% positive rate the

net present value stands $193,687.

11FINANCE

Taking into the consideration the above stated scenario analysis an assertion can be

forward by stating that there is a higher amount of impact is noticed when the selling price

falls by -20% as the net present value fell significantly negatively to -$36,754 while a

positive selling price of 20% reflected a higher amount of net present value (Hall & Sibanda,

2016). On the other hand, the weighted average cost of capital is also the highest impacted as

under the -4% the net present value stood significantly higher than the actual amount.

Whereas at the 4% level the net present value stood significantly lower to $193,687. It can be

assumed that with changes in the scenarios the operating cost hardly reflecting any significant

change but the selling price and the weighted average cost of capital is higher impacted.

Recommendations of the scenarios:

On analysing the above stated scenario a recommendation can be provided to the

board of directors that alternative scenarios of Catch size and operating cost scenario should

be considered (Sabri et al., 2014). This primary reason for the assertion is that there is a lower

variation in the actual amount of net present value under the -+25% change. Similarly, for the

operating cost method irrespective of the change in the scenario the impact created does not

effects the cash flow of the actual net present value.

Evaluation of option to lease:

On evaluating the options, it can be stated that the net present value derived under the

first options is higher since the net present value stands $673,865 while as the internal rate of

return stands 37.40% for the first options. However, the figures derived under the second

options an assertion can be bought forward by stating that the net present value derived for

the second options stands $475,765 while the internal rate of return stands 29.37%. The

business can consider Alternative 1 however bearing in mind the operating lease

Taking into the consideration the above stated scenario analysis an assertion can be

forward by stating that there is a higher amount of impact is noticed when the selling price

falls by -20% as the net present value fell significantly negatively to -$36,754 while a

positive selling price of 20% reflected a higher amount of net present value (Hall & Sibanda,

2016). On the other hand, the weighted average cost of capital is also the highest impacted as

under the -4% the net present value stood significantly higher than the actual amount.

Whereas at the 4% level the net present value stood significantly lower to $193,687. It can be

assumed that with changes in the scenarios the operating cost hardly reflecting any significant

change but the selling price and the weighted average cost of capital is higher impacted.

Recommendations of the scenarios:

On analysing the above stated scenario a recommendation can be provided to the

board of directors that alternative scenarios of Catch size and operating cost scenario should

be considered (Sabri et al., 2014). This primary reason for the assertion is that there is a lower

variation in the actual amount of net present value under the -+25% change. Similarly, for the

operating cost method irrespective of the change in the scenario the impact created does not

effects the cash flow of the actual net present value.

Evaluation of option to lease:

On evaluating the options, it can be stated that the net present value derived under the

first options is higher since the net present value stands $673,865 while as the internal rate of

return stands 37.40% for the first options. However, the figures derived under the second

options an assertion can be bought forward by stating that the net present value derived for

the second options stands $475,765 while the internal rate of return stands 29.37%. The

business can consider Alternative 1 however bearing in mind the operating lease

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.