Corporate Finance and Accountancy: Analyzing Key Financial Metrics

VerifiedAdded on 2023/06/17

|14

|3306

|98

Report

AI Summary

This report provides a comprehensive analysis of corporate finance and accountancy, examining the major factors that influence company results, differentiating between micro and macro economics, and analyzing the socioeconomic elements that affect an institution's competitiveness. It describes the function of accountancy in a company, highlighting its significance in monitoring and decision-making, and differentiates among the main fiscal reports, describing their structure and terminology. The report also calculates and interprets the accountancy metrics of a hypothetical business, XYZ Ltd., and describes managerial accountancy, explaining its crucial role in organizational strategy, accountability, and judgment calls. This document aims to provide a detailed understanding of the key components of corporate economics and accountancy and is available on Desklib, a platform offering study tools and resources for students.

Business finance and

economics

economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

1. Describe the major factors that influence company results and identify whether they are

micro or macro economics. Analyze the socioeconomic elements which influence an

institution's competitiveness climate...........................................................................................1

2. Describe the function of accountancy in a company and the significance of it in terms of

monitoring and judgement call....................................................................................................2

3. Differentiate amongst the main fiscal reports and describe the structure and terminology

employed......................................................................................................................................4

4. The accountancy metrics of the business XYZ Ltd. were calculated and interpreted.............7

5. Describe managerial accountancy and explain why it is crucial for organisational strategy,

accountability, and judgement call..............................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

1. Describe the major factors that influence company results and identify whether they are

micro or macro economics. Analyze the socioeconomic elements which influence an

institution's competitiveness climate...........................................................................................1

2. Describe the function of accountancy in a company and the significance of it in terms of

monitoring and judgement call....................................................................................................2

3. Differentiate amongst the main fiscal reports and describe the structure and terminology

employed......................................................................................................................................4

4. The accountancy metrics of the business XYZ Ltd. were calculated and interpreted.............7

5. Describe managerial accountancy and explain why it is crucial for organisational strategy,

accountability, and judgement call..............................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Corporate economics and accountancy are seen as critical components of a company's

operation (Becker, Lee and Nobre, 2018). It essentially aids an institution's competing

atmosphere management as well as effective decision-making abilities. Economics aids a

company in analysing statistics and numbers, which in turn aids in the management of all

commercial lending processes in order to improve the company's efficiency. Sectors of the

economy, accountancy, and corporate finance are described with applicable explanation in the

sections of this document, in compliance with the components of organization, management, and

strategic preparing.

MAIN BODY

1. Describe the major factors that influence company results and identify whether they are micro

or macro economics. Analyze the socioeconomic elements which influence an institution's

competitiveness climate

An efficient economic management is critical for all businesses, as it strives to run company

processes and activity in a way that aligns groups, supports staff engagement, and improves the

general efficiency of the system. The following are the primary drivers of corporate strategy

which aid in the achievement of an organization's goal:

Leverage: It is a term employed to describe an investing method which includes using

various finance products and loan funds to increase the possible yield on holdings. It's

also known as a sum of money utilised by a company to fund equipment. Since all

choices linked to growing or reducing the firm's leverage are made solely by the

institution's administration, it is called a microeconomic term (Cavicchioli, 2018).

Liquidity: The pace about which economic instruments could be purchased and traded

in the industry is known as volatility. It relates to the company's ability to transform

inventory into money at its ease. Furthermore, since this variable is involved with the

firm's domestic affairs, it could be regarded a microeconomic element.

Inflation: It is defined as a rise in the cost of products or activities over time. It's

essentially a factor which can affect whether a major currencies buying value increases or

decreases with time. The rationale for this element's macroeconomic character is that

Corporate economics and accountancy are seen as critical components of a company's

operation (Becker, Lee and Nobre, 2018). It essentially aids an institution's competing

atmosphere management as well as effective decision-making abilities. Economics aids a

company in analysing statistics and numbers, which in turn aids in the management of all

commercial lending processes in order to improve the company's efficiency. Sectors of the

economy, accountancy, and corporate finance are described with applicable explanation in the

sections of this document, in compliance with the components of organization, management, and

strategic preparing.

MAIN BODY

1. Describe the major factors that influence company results and identify whether they are micro

or macro economics. Analyze the socioeconomic elements which influence an institution's

competitiveness climate

An efficient economic management is critical for all businesses, as it strives to run company

processes and activity in a way that aligns groups, supports staff engagement, and improves the

general efficiency of the system. The following are the primary drivers of corporate strategy

which aid in the achievement of an organization's goal:

Leverage: It is a term employed to describe an investing method which includes using

various finance products and loan funds to increase the possible yield on holdings. It's

also known as a sum of money utilised by a company to fund equipment. Since all

choices linked to growing or reducing the firm's leverage are made solely by the

institution's administration, it is called a microeconomic term (Cavicchioli, 2018).

Liquidity: The pace about which economic instruments could be purchased and traded

in the industry is known as volatility. It relates to the company's ability to transform

inventory into money at its ease. Furthermore, since this variable is involved with the

firm's domestic affairs, it could be regarded a microeconomic element.

Inflation: It is defined as a rise in the cost of products or activities over time. It's

essentially a factor which can affect whether a major currencies buying value increases or

decreases with time. The rationale for this element's macroeconomic character is that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

every alteration in the pricing range would eventually impact the market's disposable

income as in general.

Economical variables that impact the market economy include: Such elements are seen

as extremely essential in the corporate world, and they aid a firm's understanding of how they

influence the challenging market. It is critical for individual businesses to have an eye on such

aspects and evaluate them on a regular basis in order to avoid any eventualities that could

develop in the near future. The following are the several socioeconomic variables:

Consumption: Among the most essential factors in determining whether or not an item

or services is needed by clients in the marketplace is requirement. Businesses could

leverage a range of tactics in the industry to assist them adopt diverse methods in a

competition climate.

Industry Volume: It is critical for businesses to have a large marketing magnitude since

it would enable them to attract a large variety of clients, allowing them to raise their

profitability in intense competition. A larger marketplace volume would enable the firm

in capturing larger earnings and ensuring long-term prosperity amid rivals.

Vendors: In addition to remain successful in the industry, it is critical that supply chain

operations maintain a higher level of service, allowing businesses to deliver completed

items to clients sans delay. This would enable the organisation to remain competing in

the industry by ensuring consistent supplies with no delays (Chang and Hanson, 2016).

2. Describe the function of accountancy in a company and the significance of it in terms of

monitoring and judgement call

Accountancy is the practise of keeping track of the fiscal dealings which happen as a

consequence of corporate bookkeeping activities. Accountancy is used to document all of the

fiscal transactions of a particular investment quarter. This has a significant impact on reports and

decision-making for the firm's most crucial issues.

Accountancy Functions-

Collection and management of finance information: Accountancy serves a crucial

function in accumulating finance statistics, which would eventually aid in retrieving

finance sets of information and creating documentation in such a direction in which it

assists the firm's management in creating specific finance choices.

income as in general.

Economical variables that impact the market economy include: Such elements are seen

as extremely essential in the corporate world, and they aid a firm's understanding of how they

influence the challenging market. It is critical for individual businesses to have an eye on such

aspects and evaluate them on a regular basis in order to avoid any eventualities that could

develop in the near future. The following are the several socioeconomic variables:

Consumption: Among the most essential factors in determining whether or not an item

or services is needed by clients in the marketplace is requirement. Businesses could

leverage a range of tactics in the industry to assist them adopt diverse methods in a

competition climate.

Industry Volume: It is critical for businesses to have a large marketing magnitude since

it would enable them to attract a large variety of clients, allowing them to raise their

profitability in intense competition. A larger marketplace volume would enable the firm

in capturing larger earnings and ensuring long-term prosperity amid rivals.

Vendors: In addition to remain successful in the industry, it is critical that supply chain

operations maintain a higher level of service, allowing businesses to deliver completed

items to clients sans delay. This would enable the organisation to remain competing in

the industry by ensuring consistent supplies with no delays (Chang and Hanson, 2016).

2. Describe the function of accountancy in a company and the significance of it in terms of

monitoring and judgement call

Accountancy is the practise of keeping track of the fiscal dealings which happen as a

consequence of corporate bookkeeping activities. Accountancy is used to document all of the

fiscal transactions of a particular investment quarter. This has a significant impact on reports and

decision-making for the firm's most crucial issues.

Accountancy Functions-

Collection and management of finance information: Accountancy serves a crucial

function in accumulating finance statistics, which would eventually aid in retrieving

finance sets of information and creating documentation in such a direction in which it

assists the firm's management in creating specific finance choices.

Legislative and Administrative Standards: Accountancy is among the most critical

functions in ensuring that policy and institutional structures are followed. This covers a

variety of guidelines that establish a series of guidelines for the preparation of fiscal

reports.

Budgetary control: Accountancy is critical in giving an assessment of all fiscal records,

which ultimately assists the responsible person in developing plans. This enables

financial employees to make working capital estimates that are in line with financial

reporting (Emrah Aydinonat, 2018).

Supply material to interested stakeholders: Accountancy aids in the preparation of

fiscal reports, which serves a critical purpose in disseminating fiscal data from the

business to interested parties, both inner and outer.

Effective management: Accountancy aids in having a close eye on the firm's entire

operations and ensuring a greater degree of effectiveness. As a result, a higher

effectiveness and productivity would aid the organisation in making the most use of its

assets.

Accountancy Significance in Reports and Judgement call-

Efficient Preparation: Accountancy is a technique which is primarily focused with the

seamless execution of all of a company's fiscal processes. As a result, accountancy aids a

firm's capacity to prepare effectively so that it could fulfil its goals. This would also assist

in efficient monitoring and making a good selections feasible related to the preparation.

Expertise guidance: Accountancy is a crucial function that assists management and

professionals in providing specialist advice on significant fiscal concerns. As a result,

accountancy statistics aids professionals in providing sound expert guidance.

Explaining Funding levels: Budgetary control is regarded to be quite important for a

business since it entails making decisions depending on revenue and accounting

information. Accountancy is a crucial element in this case since it is used to compile all

financial documents and to make all budgeting decisions.

Minimizing Inconsistencies: Accountancy aids a company in making prospective

projections, which could eventually lead to the management of a contingency scenario. It

is also possible to make significant judgments about how to limit the danger (Filimonau

and Gherbin, 2017).

functions in ensuring that policy and institutional structures are followed. This covers a

variety of guidelines that establish a series of guidelines for the preparation of fiscal

reports.

Budgetary control: Accountancy is critical in giving an assessment of all fiscal records,

which ultimately assists the responsible person in developing plans. This enables

financial employees to make working capital estimates that are in line with financial

reporting (Emrah Aydinonat, 2018).

Supply material to interested stakeholders: Accountancy aids in the preparation of

fiscal reports, which serves a critical purpose in disseminating fiscal data from the

business to interested parties, both inner and outer.

Effective management: Accountancy aids in having a close eye on the firm's entire

operations and ensuring a greater degree of effectiveness. As a result, a higher

effectiveness and productivity would aid the organisation in making the most use of its

assets.

Accountancy Significance in Reports and Judgement call-

Efficient Preparation: Accountancy is a technique which is primarily focused with the

seamless execution of all of a company's fiscal processes. As a result, accountancy aids a

firm's capacity to prepare effectively so that it could fulfil its goals. This would also assist

in efficient monitoring and making a good selections feasible related to the preparation.

Expertise guidance: Accountancy is a crucial function that assists management and

professionals in providing specialist advice on significant fiscal concerns. As a result,

accountancy statistics aids professionals in providing sound expert guidance.

Explaining Funding levels: Budgetary control is regarded to be quite important for a

business since it entails making decisions depending on revenue and accounting

information. Accountancy is a crucial element in this case since it is used to compile all

financial documents and to make all budgeting decisions.

Minimizing Inconsistencies: Accountancy aids a company in making prospective

projections, which could eventually lead to the management of a contingency scenario. It

is also possible to make significant judgments about how to limit the danger (Filimonau

and Gherbin, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Differentiate amongst the main fiscal reports and describe the structure and terminology

employed

Finance reports are a formalized documented record which incorporates all of a

corporation's finance operations in such a manner in which it aids in showing the firm's true and

equitable fiscal situation. Since the fiscal reports of the business reflect all of the firm's income,

profits, expenditures, and liabilities, these aid in conveying such data to shareholders. There

seem to be primarily three fiscal reports which aid in the documenting and analysis of all of the

monetary operations listed beneath, as well as their formats:

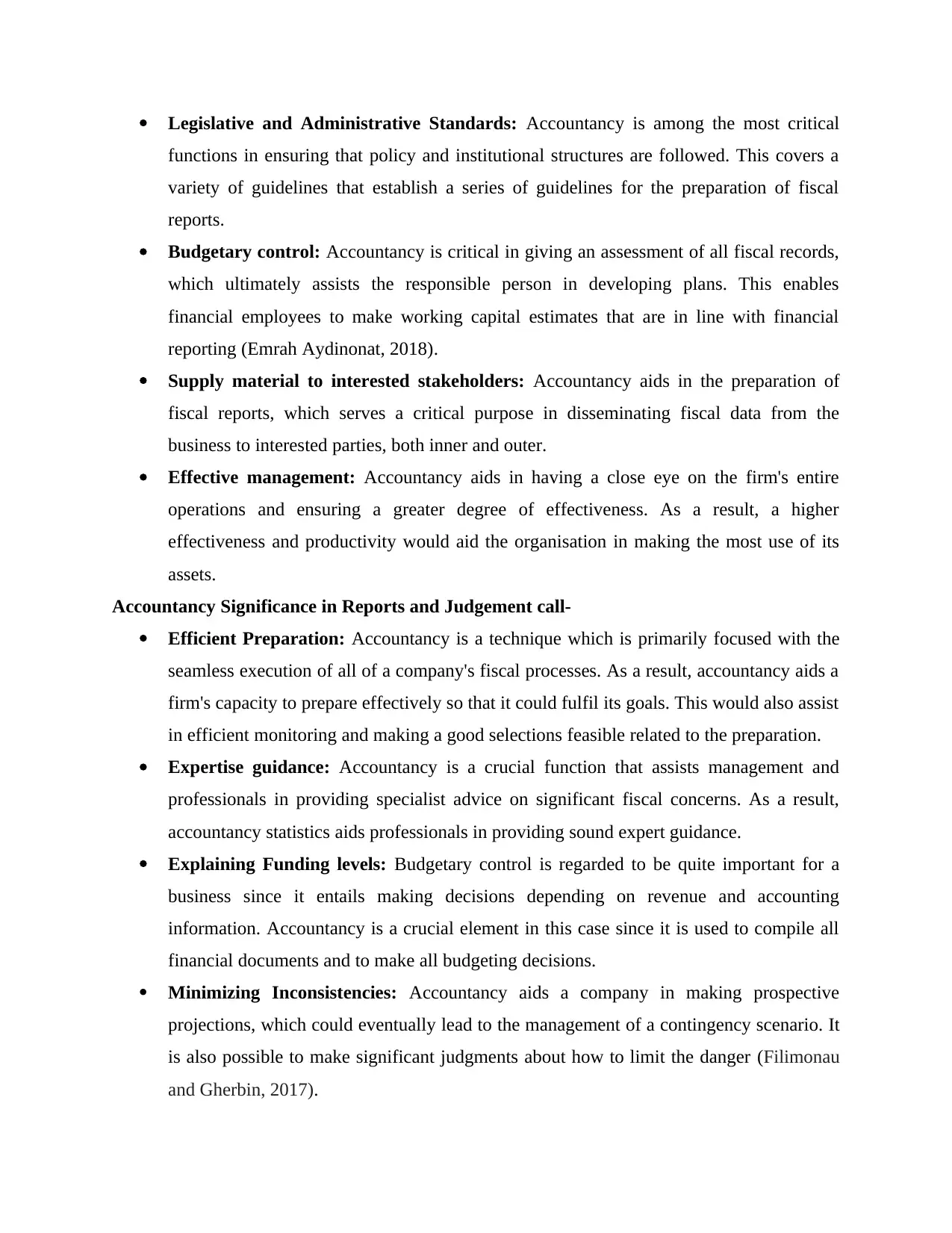

Balance Sheet: It is among the most important fiscal reports since it shows all of the

firm's resources, obligations, and owners' capital in a clear and concise manner. It

accurately lays forth the corporation's fiscal standing as well as its current condition,

complete with all numbers. Economics professionals, researchers, and management

consultants frequently are using the balance sheet as a key instrument for determining the

firm's various metrics and analysing its cash reserves in a range of methods (Gillard,

2019).

Resources and Obligations are the two primary elements of a balance sheet, as illustrated

beneath:

Resources: It could be described as a material with financial worth that a person or

organisation owns with the intention of generating greater yields. It could be both

financial and non - financial.

Obligations- It could be described as the quantity owed to another entity by a person, a

business, or a government. All of the things in this group impose a financial obligation

on the business to repay the entities to whom it owed money.

employed

Finance reports are a formalized documented record which incorporates all of a

corporation's finance operations in such a manner in which it aids in showing the firm's true and

equitable fiscal situation. Since the fiscal reports of the business reflect all of the firm's income,

profits, expenditures, and liabilities, these aid in conveying such data to shareholders. There

seem to be primarily three fiscal reports which aid in the documenting and analysis of all of the

monetary operations listed beneath, as well as their formats:

Balance Sheet: It is among the most important fiscal reports since it shows all of the

firm's resources, obligations, and owners' capital in a clear and concise manner. It

accurately lays forth the corporation's fiscal standing as well as its current condition,

complete with all numbers. Economics professionals, researchers, and management

consultants frequently are using the balance sheet as a key instrument for determining the

firm's various metrics and analysing its cash reserves in a range of methods (Gillard,

2019).

Resources and Obligations are the two primary elements of a balance sheet, as illustrated

beneath:

Resources: It could be described as a material with financial worth that a person or

organisation owns with the intention of generating greater yields. It could be both

financial and non - financial.

Obligations- It could be described as the quantity owed to another entity by a person, a

business, or a government. All of the things in this group impose a financial obligation

on the business to repay the entities to whom it owed money.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income Statement: It is a fiscal report which shows a firm's earnings and losses over a

certain timeframe. It is a crucial statement since it comprises all of a group's revenue and

expenditures linked to its economic activities. An income statement's method is

subtracting all expenditures from the total of the company's earnings, both in operational

and non operations. It's employed in both accountancy and business financing. The main

goal of these statements is to assist the firm's directors and investors in making important

judgments on how to generate revenues by growing revenues or reducing prices

(Hommes and LeBaron, 2018). The following is the income statement layout:

Illustration 1: Format of Balance Sheet

certain timeframe. It is a crucial statement since it comprises all of a group's revenue and

expenditures linked to its economic activities. An income statement's method is

subtracting all expenditures from the total of the company's earnings, both in operational

and non operations. It's employed in both accountancy and business financing. The main

goal of these statements is to assist the firm's directors and investors in making important

judgments on how to generate revenues by growing revenues or reducing prices

(Hommes and LeBaron, 2018). The following is the income statement layout:

Illustration 1: Format of Balance Sheet

o Revenue: It refers to the entire quantity of products and activities which an organisation

has delivered to clients in order to make a gain.

o Spending: It is among the most significant components since it contains all of the

expenditures associated with producing and selling items to consumers.

o Earnings: Profitability is among the most crucial elements in this sentence. It comprises

all of the money left over after subtracting the selling from the entire value collected from

clients and subtracting the cost of goods.

o Deficit: This term refers to the surplus of costs paid by the business as a result

wherein the business has been unable to generate a gain.

Cash Flow Statement: It is a financial statement which shows how a company's money

circulation during its commercial activities. It entails all cash receiving and exiting from

the company as a result of its operational processes. The main goal of creating a capital

circulation report for a business is to aid in the management of the firm's cash balance as

Illustration 2: Format of income statement

has delivered to clients in order to make a gain.

o Spending: It is among the most significant components since it contains all of the

expenditures associated with producing and selling items to consumers.

o Earnings: Profitability is among the most crucial elements in this sentence. It comprises

all of the money left over after subtracting the selling from the entire value collected from

clients and subtracting the cost of goods.

o Deficit: This term refers to the surplus of costs paid by the business as a result

wherein the business has been unable to generate a gain.

Cash Flow Statement: It is a financial statement which shows how a company's money

circulation during its commercial activities. It entails all cash receiving and exiting from

the company as a result of its operational processes. The main goal of creating a capital

circulation report for a business is to aid in the management of the firm's cash balance as

Illustration 2: Format of income statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

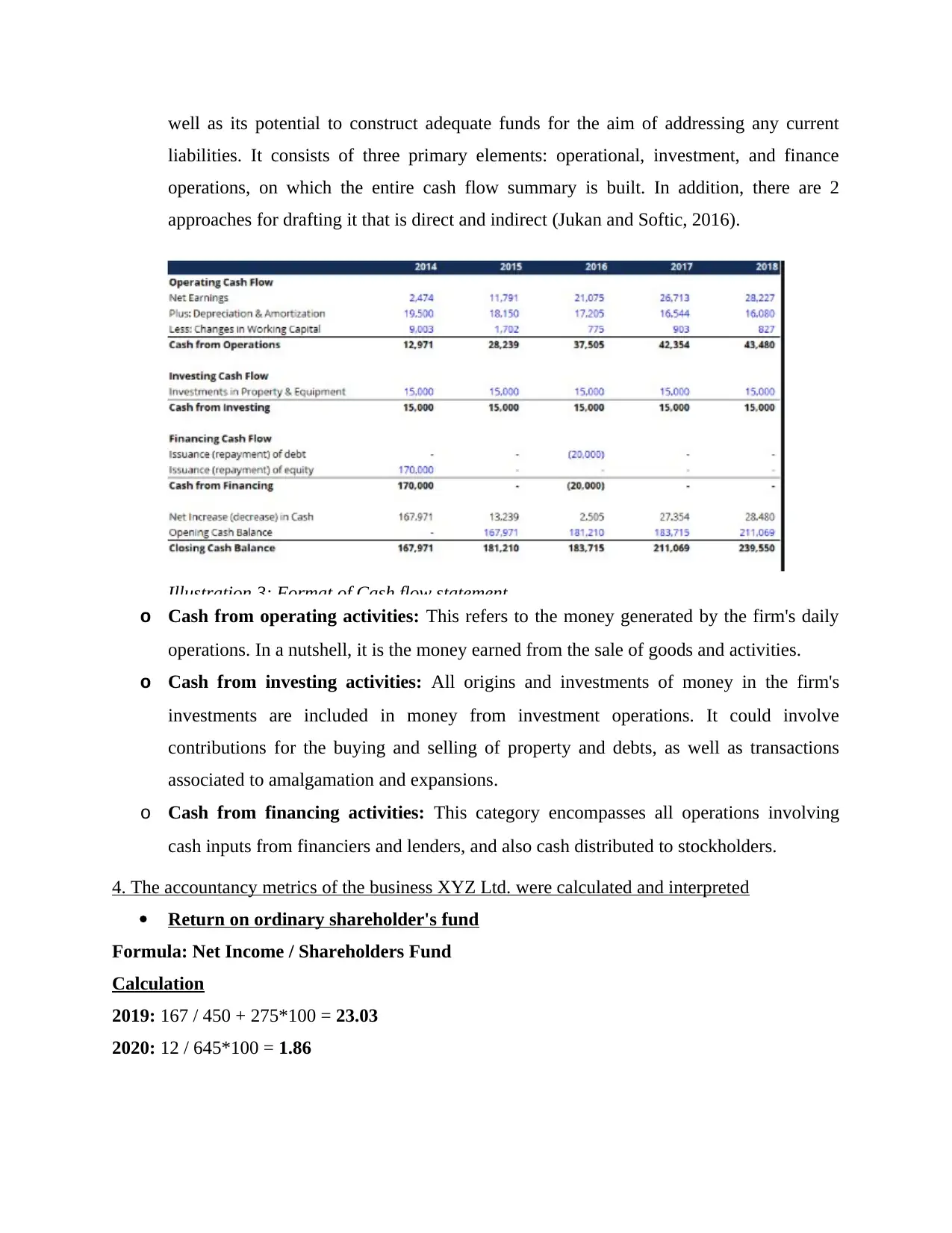

well as its potential to construct adequate funds for the aim of addressing any current

liabilities. It consists of three primary elements: operational, investment, and finance

operations, on which the entire cash flow summary is built. In addition, there are 2

approaches for drafting it that is direct and indirect (Jukan and Softic, 2016).

o Cash from operating activities: This refers to the money generated by the firm's daily

operations. In a nutshell, it is the money earned from the sale of goods and activities.

o Cash from investing activities: All origins and investments of money in the firm's

investments are included in money from investment operations. It could involve

contributions for the buying and selling of property and debts, as well as transactions

associated to amalgamation and expansions.

o Cash from financing activities: This category encompasses all operations involving

cash inputs from financiers and lenders, and also cash distributed to stockholders.

4. The accountancy metrics of the business XYZ Ltd. were calculated and interpreted

Return on ordinary shareholder's fund

Formula: Net Income / Shareholders Fund

Calculation

2019: 167 / 450 + 275*100 = 23.03

2020: 12 / 645*100 = 1.86

Illustration 3: Format of Cash flow statement

liabilities. It consists of three primary elements: operational, investment, and finance

operations, on which the entire cash flow summary is built. In addition, there are 2

approaches for drafting it that is direct and indirect (Jukan and Softic, 2016).

o Cash from operating activities: This refers to the money generated by the firm's daily

operations. In a nutshell, it is the money earned from the sale of goods and activities.

o Cash from investing activities: All origins and investments of money in the firm's

investments are included in money from investment operations. It could involve

contributions for the buying and selling of property and debts, as well as transactions

associated to amalgamation and expansions.

o Cash from financing activities: This category encompasses all operations involving

cash inputs from financiers and lenders, and also cash distributed to stockholders.

4. The accountancy metrics of the business XYZ Ltd. were calculated and interpreted

Return on ordinary shareholder's fund

Formula: Net Income / Shareholders Fund

Calculation

2019: 167 / 450 + 275*100 = 23.03

2020: 12 / 645*100 = 1.86

Illustration 3: Format of Cash flow statement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: The yield on the equity owner capital was particularly high in 2019, at 23.03

percent, showing that the firm's productivity was good in comparison to the year 2020, which

had a yield of only 1.86 percent.

Return on Capital Employed

Formula: EBIT / Total Assets – Total Current Liabilities

Calculation

2019: 240 / 1115-190 *100= 25.94

2020: 35 / 1290-295 *100= 3.51

Interpretation: The firm's ROCE was exceptionally significant in the year 2019 and

severely decreased in the year 2020, according to the analysis of this proportion. The 2019

margin indicates that the organisation is producing effectively and in sufficient quantities.

Operating Profit Margin:

Formula: Operating Profit / Net Sales * 100

Calculation

2019: 240 / 2500 * 100 = 9.6%

2020: 35 / 2750 * 100 = 1.27 %

Interpretation: The operational income margins for the year 2019 indicates that the business

has been very well controlled and is at a lower risk than in previous years. The proportion is

substantially lower in 2020, indicating that the firm is vulnerable to fiscal hazards (Kanev and

Terziev, 2017).

Current Ratio

Formula: Current Assets / Current Liabilities

Calculation

2019: 1115 / 190 = 5.86:1

2020: 1290 / 295 = 4.37:1

Interpretation: In the year 2019, the firm is quite responsible for paying off its obligations

efficiently; however in the year 2020, the proportion is less, indicating that the firm's ability has

decreased over the year.

Earnings Per Share:

Formula: Net Income – Dividend Paid / Number of shares outstanding

Calculation

percent, showing that the firm's productivity was good in comparison to the year 2020, which

had a yield of only 1.86 percent.

Return on Capital Employed

Formula: EBIT / Total Assets – Total Current Liabilities

Calculation

2019: 240 / 1115-190 *100= 25.94

2020: 35 / 1290-295 *100= 3.51

Interpretation: The firm's ROCE was exceptionally significant in the year 2019 and

severely decreased in the year 2020, according to the analysis of this proportion. The 2019

margin indicates that the organisation is producing effectively and in sufficient quantities.

Operating Profit Margin:

Formula: Operating Profit / Net Sales * 100

Calculation

2019: 240 / 2500 * 100 = 9.6%

2020: 35 / 2750 * 100 = 1.27 %

Interpretation: The operational income margins for the year 2019 indicates that the business

has been very well controlled and is at a lower risk than in previous years. The proportion is

substantially lower in 2020, indicating that the firm is vulnerable to fiscal hazards (Kanev and

Terziev, 2017).

Current Ratio

Formula: Current Assets / Current Liabilities

Calculation

2019: 1115 / 190 = 5.86:1

2020: 1290 / 295 = 4.37:1

Interpretation: In the year 2019, the firm is quite responsible for paying off its obligations

efficiently; however in the year 2020, the proportion is less, indicating that the firm's ability has

decreased over the year.

Earnings Per Share:

Formula: Net Income – Dividend Paid / Number of shares outstanding

Calculation

2019: 167-40 / 133.33 = 0.952

2020: 12 – 40 / 200 = 0.14

Interpretation: The earnings per share valuation for the year 2019 indicates how the firm

generated more value than in the year 2020, which is communicated to various clients of finance

data.

5. Describe managerial accountancy and explain why it is crucial for organisational strategy,

accountability, and judgement call

Managerial accountancy is a procedure or approach for preparing fiscal statements based

on corporate activities which primarily assists managerial in creating short- and long-term

choices. It simply aids a company in successfully planning, analysing, interpreting, and sharing

data. It assists firm executives in managing operations processes and ultimately making choice

making. It aids in the most efficient management of a company's operations so that productivity

and profitability may be preserved and even expanded. This would assist the firm's interested

people in making choices concerning different sorts of choices. The following are among the

benefits of managerial financial reporting:

Strategically Managerial: Managerial accountancy may assist a company in making

selling strategies selections for a commodity. The item selling approach would be

determined by whether or not the system is likely to be maintained. Furthermore, since

managerial accountancy is not governed by any laws, managerial has the freedom to

determine certain aspects of the business deserve examination and research before

developing policies.

Preparation instrument: Managerial accountancy is a vital feature which aids in the

preparation of analyses for the objectives at hand. This could assist the organisation in

planning, financing, and in-depth study of various vital sectors. As a result, it assists in

the most proper coordination of company operations.

Organizational peaceful coexistence: Managerial accountancy is in charge of making

choices for the entire organisation, from the lowest grade workers to the highest possible

level executives. As a result, it serves a crucial role in ensuring that all stakeholders

engaged in the industry are on the same page (Souza-Monteiro and Hooker, 2017).

2020: 12 – 40 / 200 = 0.14

Interpretation: The earnings per share valuation for the year 2019 indicates how the firm

generated more value than in the year 2020, which is communicated to various clients of finance

data.

5. Describe managerial accountancy and explain why it is crucial for organisational strategy,

accountability, and judgement call

Managerial accountancy is a procedure or approach for preparing fiscal statements based

on corporate activities which primarily assists managerial in creating short- and long-term

choices. It simply aids a company in successfully planning, analysing, interpreting, and sharing

data. It assists firm executives in managing operations processes and ultimately making choice

making. It aids in the most efficient management of a company's operations so that productivity

and profitability may be preserved and even expanded. This would assist the firm's interested

people in making choices concerning different sorts of choices. The following are among the

benefits of managerial financial reporting:

Strategically Managerial: Managerial accountancy may assist a company in making

selling strategies selections for a commodity. The item selling approach would be

determined by whether or not the system is likely to be maintained. Furthermore, since

managerial accountancy is not governed by any laws, managerial has the freedom to

determine certain aspects of the business deserve examination and research before

developing policies.

Preparation instrument: Managerial accountancy is a vital feature which aids in the

preparation of analyses for the objectives at hand. This could assist the organisation in

planning, financing, and in-depth study of various vital sectors. As a result, it assists in

the most proper coordination of company operations.

Organizational peaceful coexistence: Managerial accountancy is in charge of making

choices for the entire organisation, from the lowest grade workers to the highest possible

level executives. As a result, it serves a crucial role in ensuring that all stakeholders

engaged in the industry are on the same page (Souza-Monteiro and Hooker, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.