Corporate Finance Assignment: Cardno Limited Dividend Analysis Report

VerifiedAdded on 2020/05/16

|9

|1704

|99

Homework Assignment

AI Summary

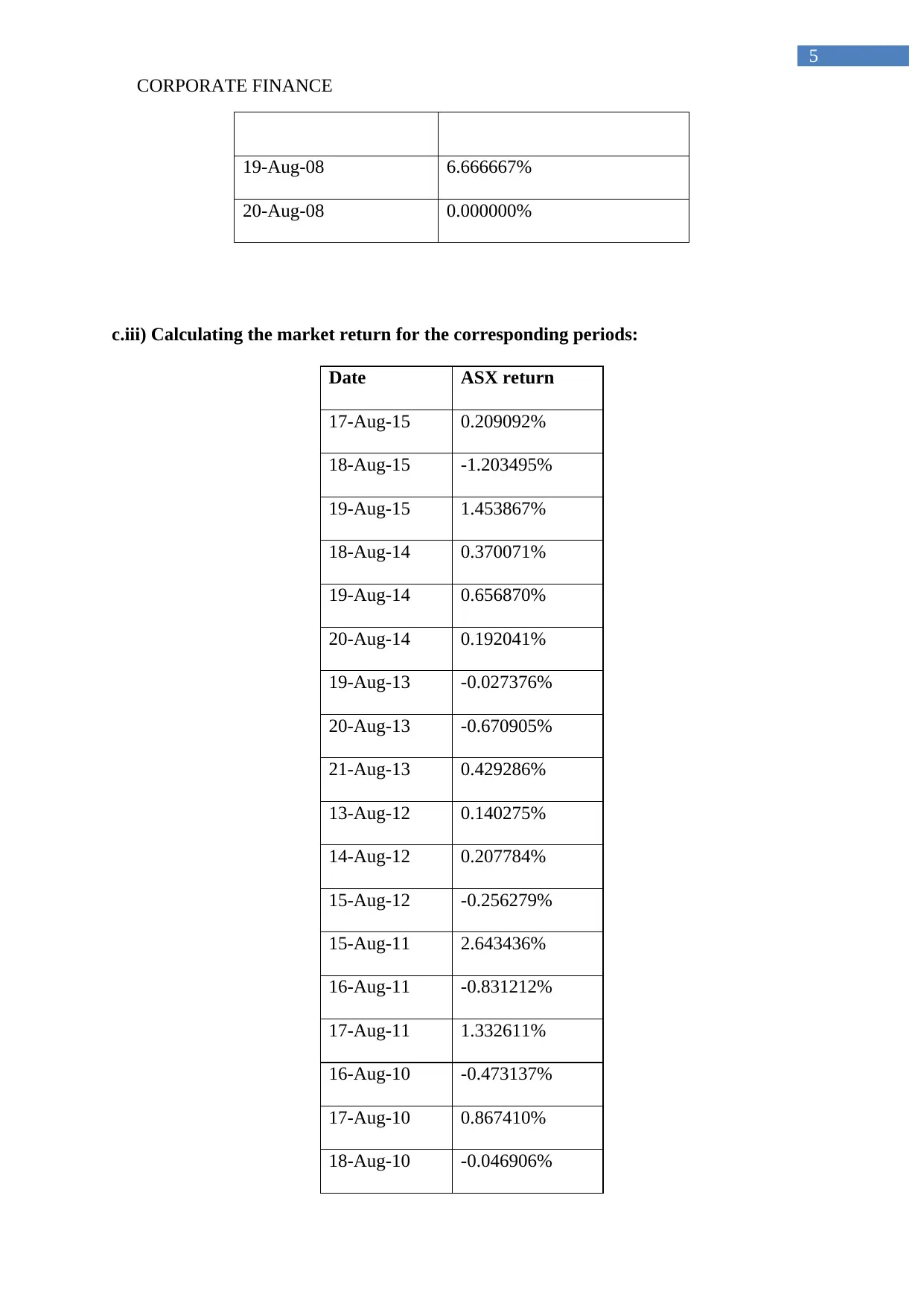

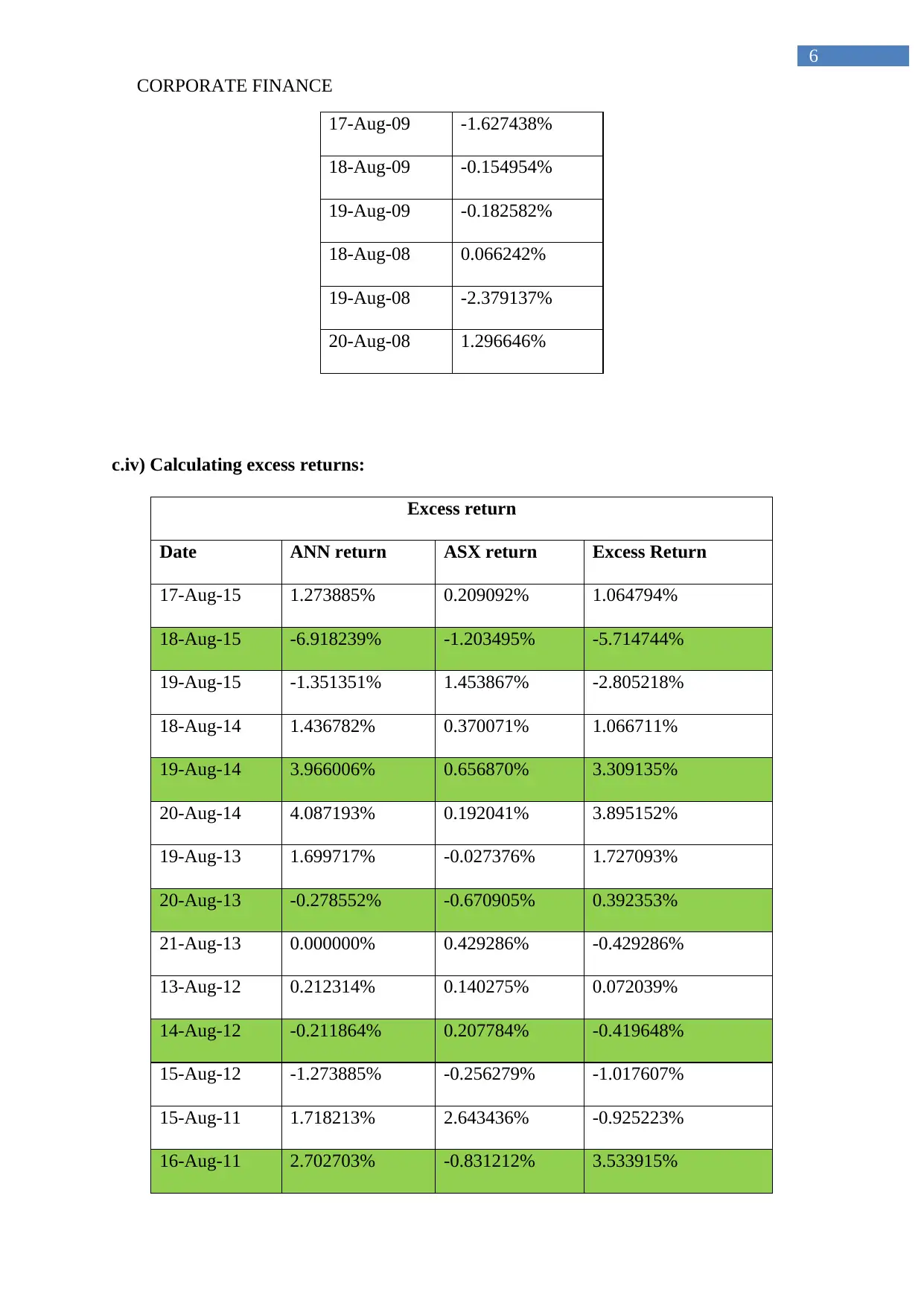

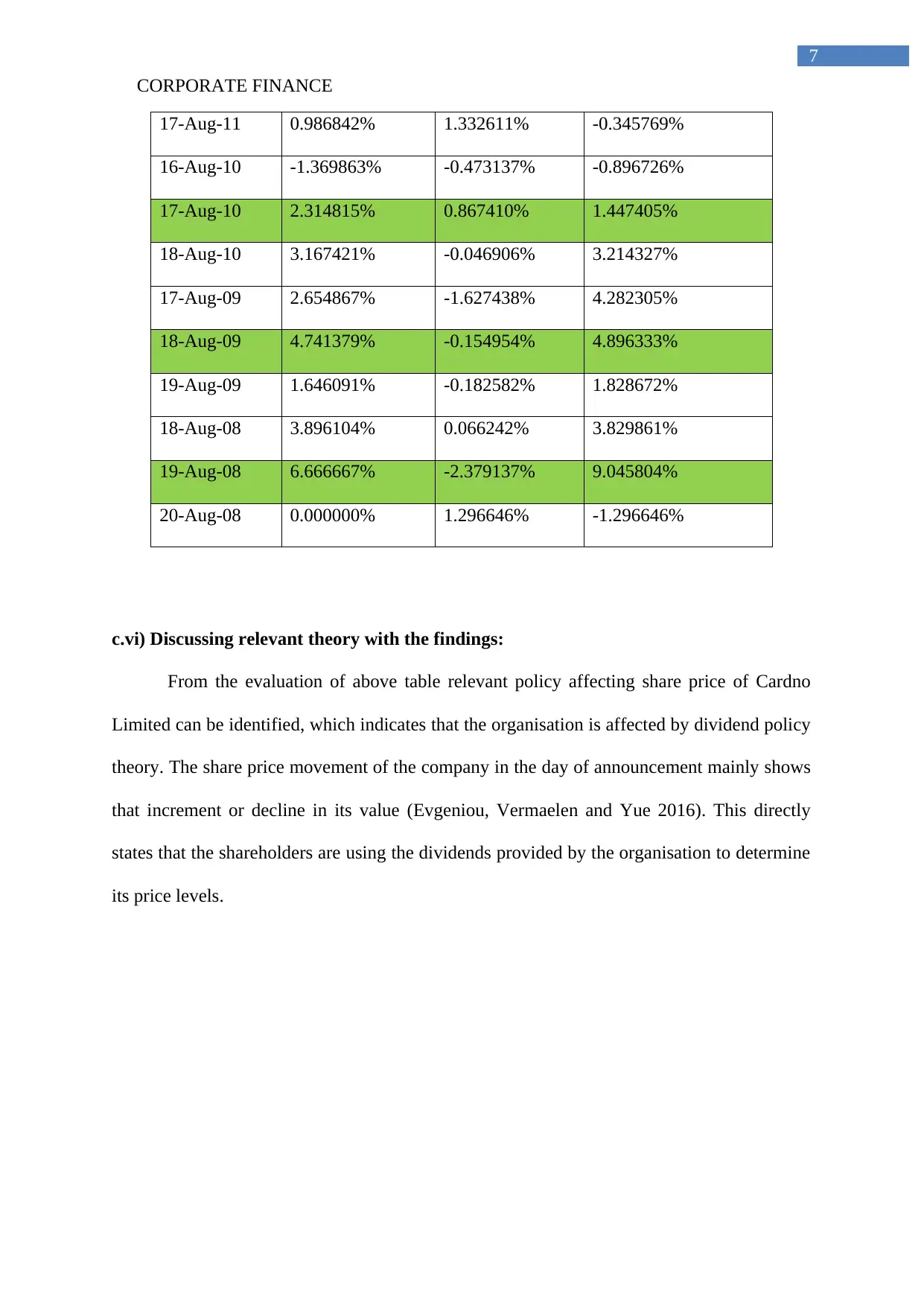

This corporate finance assignment delves into dividend policy, exploring the signaling hypothesis, free cash flow hypothesis, and clientele effect. It examines the reasons companies choose share repurchases over dividends, particularly under a classical tax system. The assignment includes an analysis of Cardno Limited's dividend history, calculating three-day returns and market returns around dividend announcements. Excess returns are calculated to assess the market's reaction. The findings are discussed in relation to relevant financial theories, providing a comprehensive overview of dividend policy's impact on share prices and corporate financial strategy. The assignment uses data from 2008-2015 for analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.