Corporate Finance Report: Investment Analysis and Project Evaluation

VerifiedAdded on 2020/06/05

|7

|1087

|46

Report

AI Summary

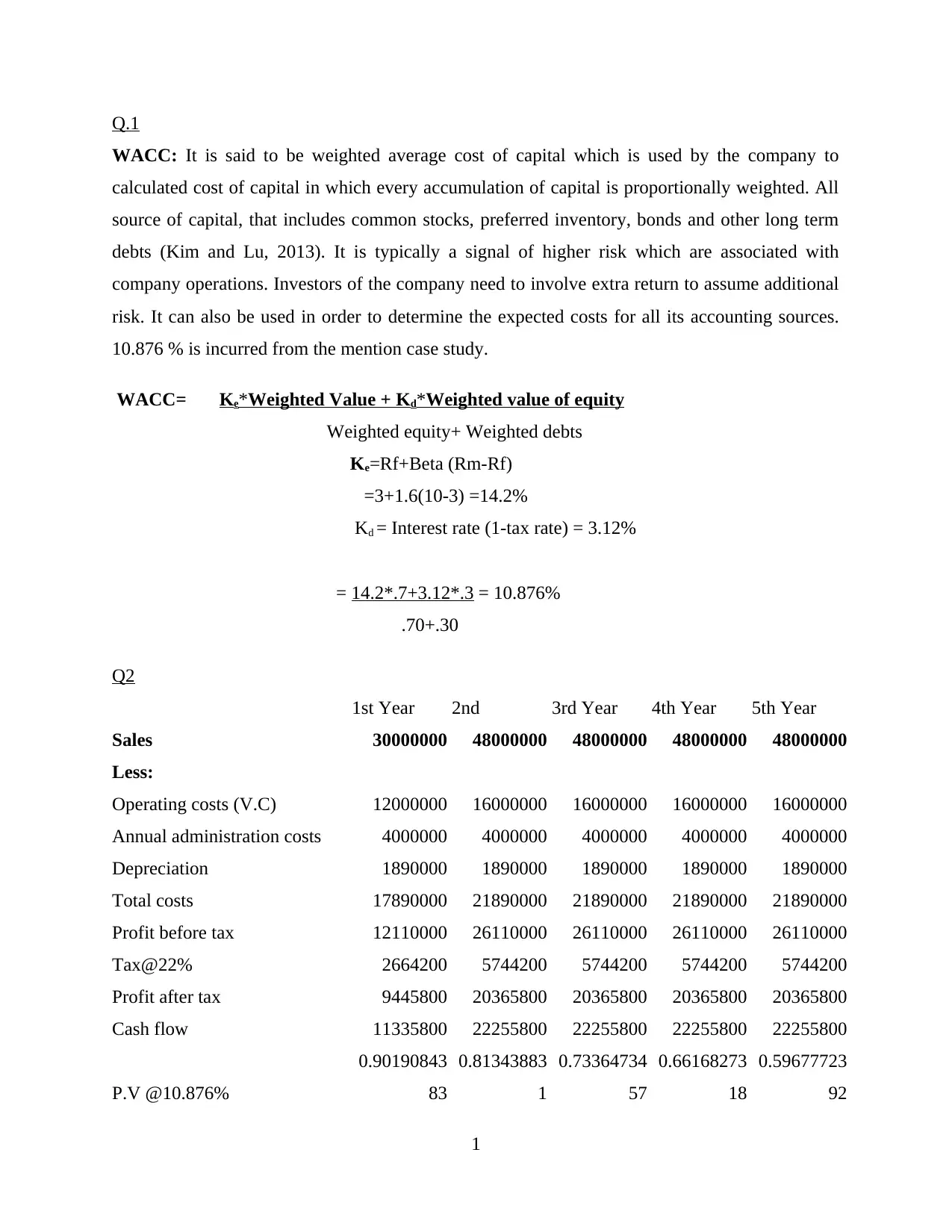

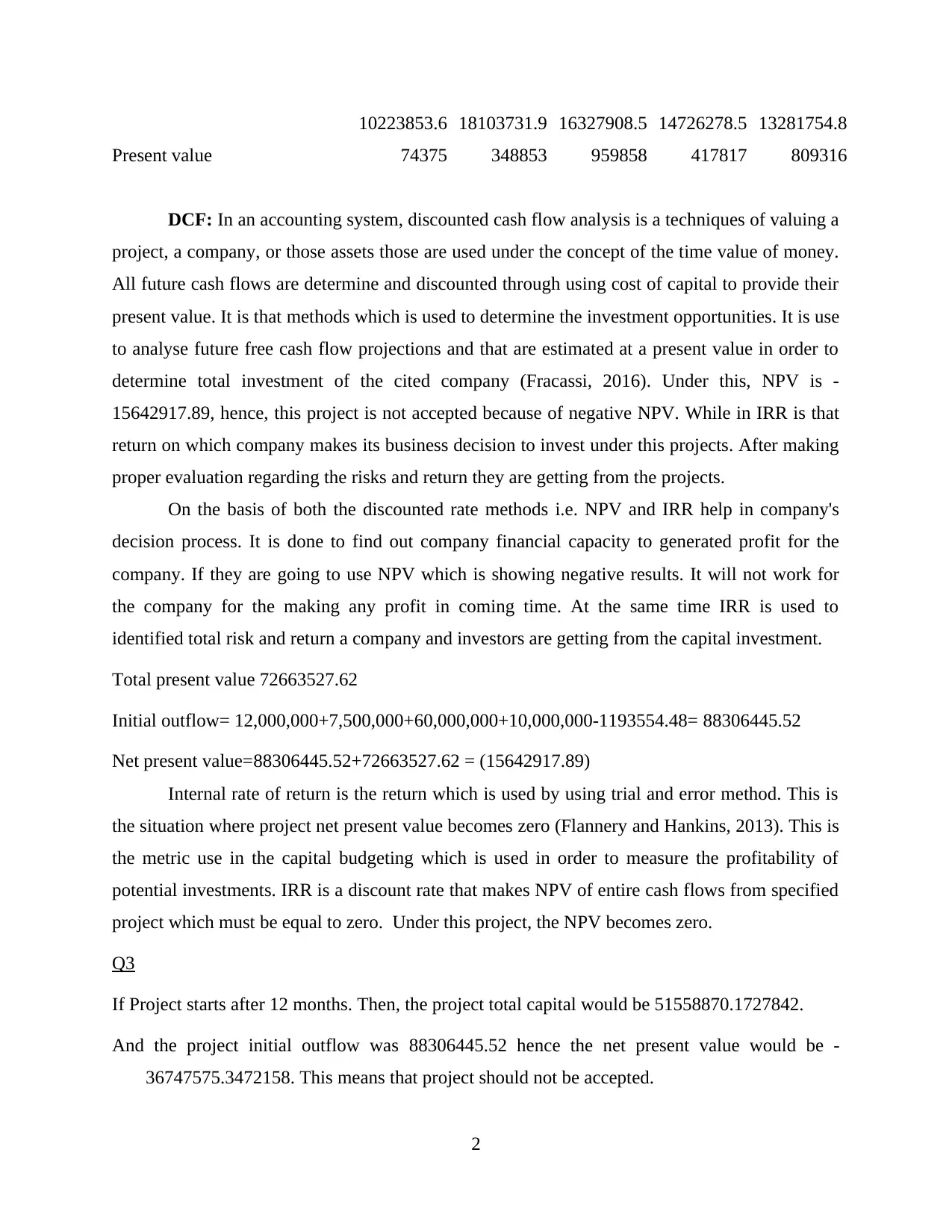

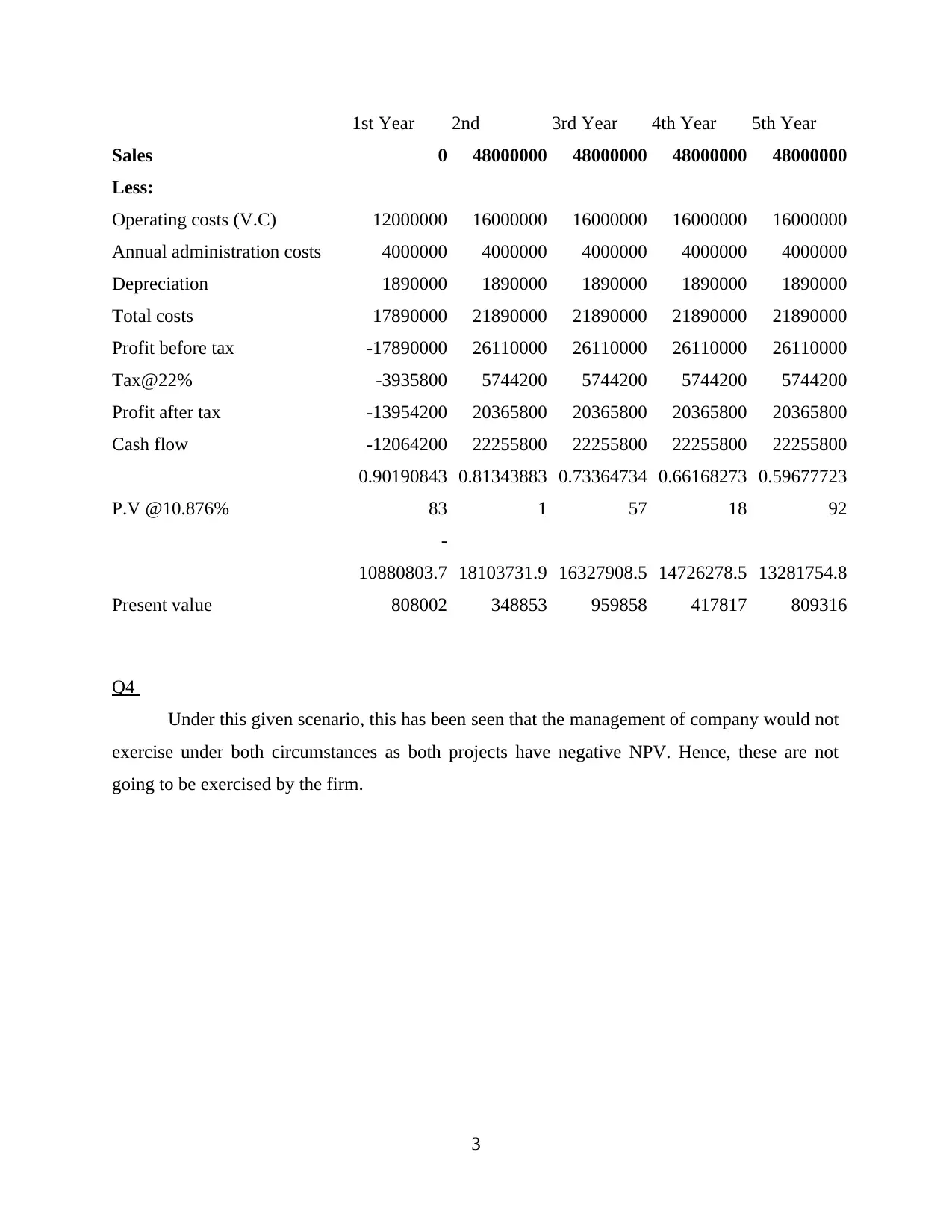

This report provides an executive summary and detailed analysis of corporate finance concepts. It begins by explaining the Weighted Average Cost of Capital (WACC), demonstrating its calculation and significance in determining a company's overall cost of capital. The report then delves into Discounted Cash Flow (DCF) analysis, including Net Present Value (NPV) and Internal Rate of Return (IRR), to evaluate potential investment projects. The report presents financial data, including sales, operating costs, and tax calculations, to determine cash flows and present values. The analysis includes calculations for two scenarios, evaluating the financial viability of projects under different timelines. The report concludes with recommendations based on the NPV and IRR results, indicating whether the projects should be undertaken. The report also includes references to academic sources supporting the financial analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.