Collinsville Plant Acquisition Analysis

VerifiedAdded on 2020/02/12

|7

|1025

|211

AI Summary

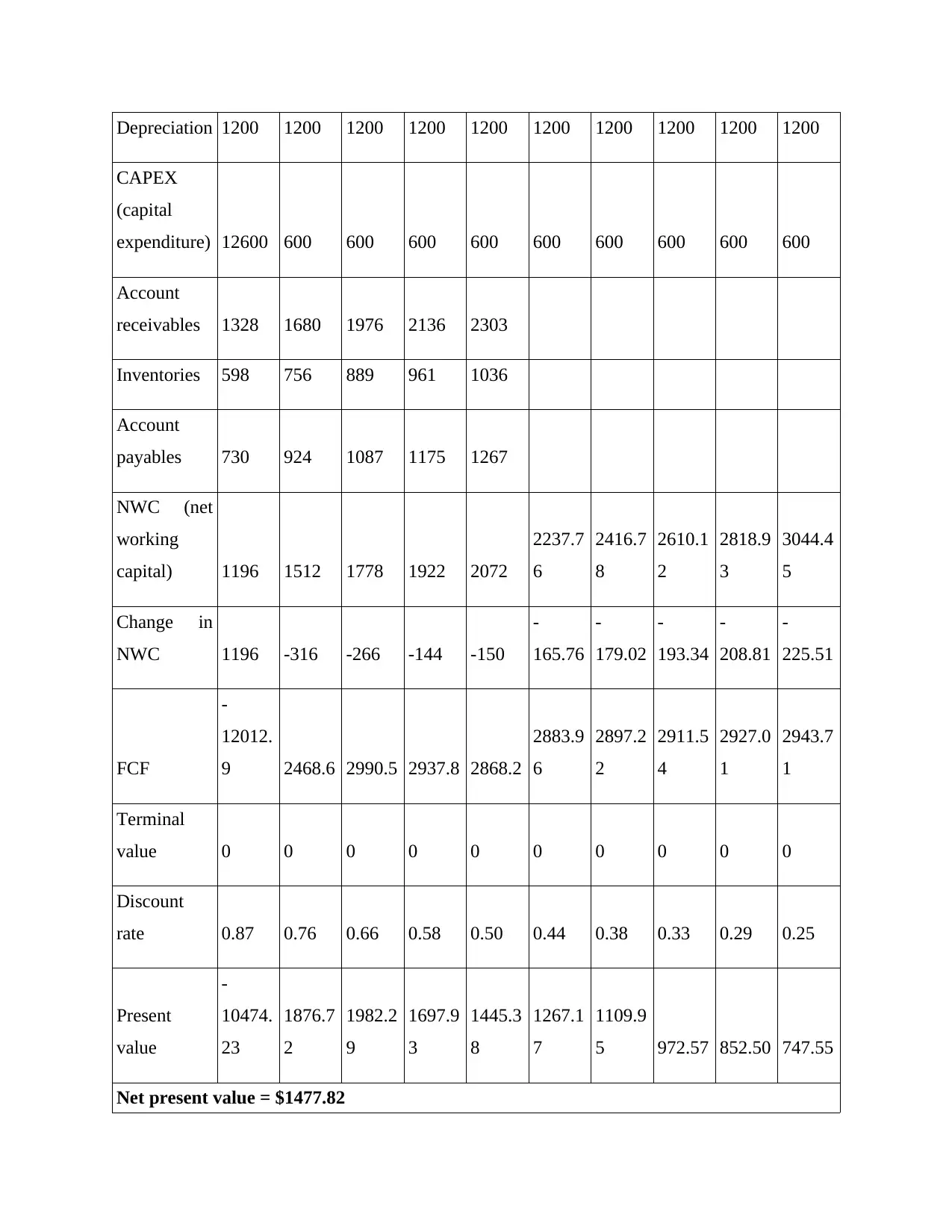

This assignment presents a detailed analysis of the potential acquisition of the Collinsville Plant by Dixon Enterprises. It includes calculations of key financial metrics such as net working capital, depreciation, projected FCF, terminal value, and discounted cash flow. The report culminates in a Net Present Value (NPV) calculation and a conclusion recommending whether or not Dixon should acquire the plant based on its financial projections.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.