Corporate Finance Assignment: Australian Stock Performance Analysis

VerifiedAdded on 2023/02/01

|7

|1916

|44

Report

AI Summary

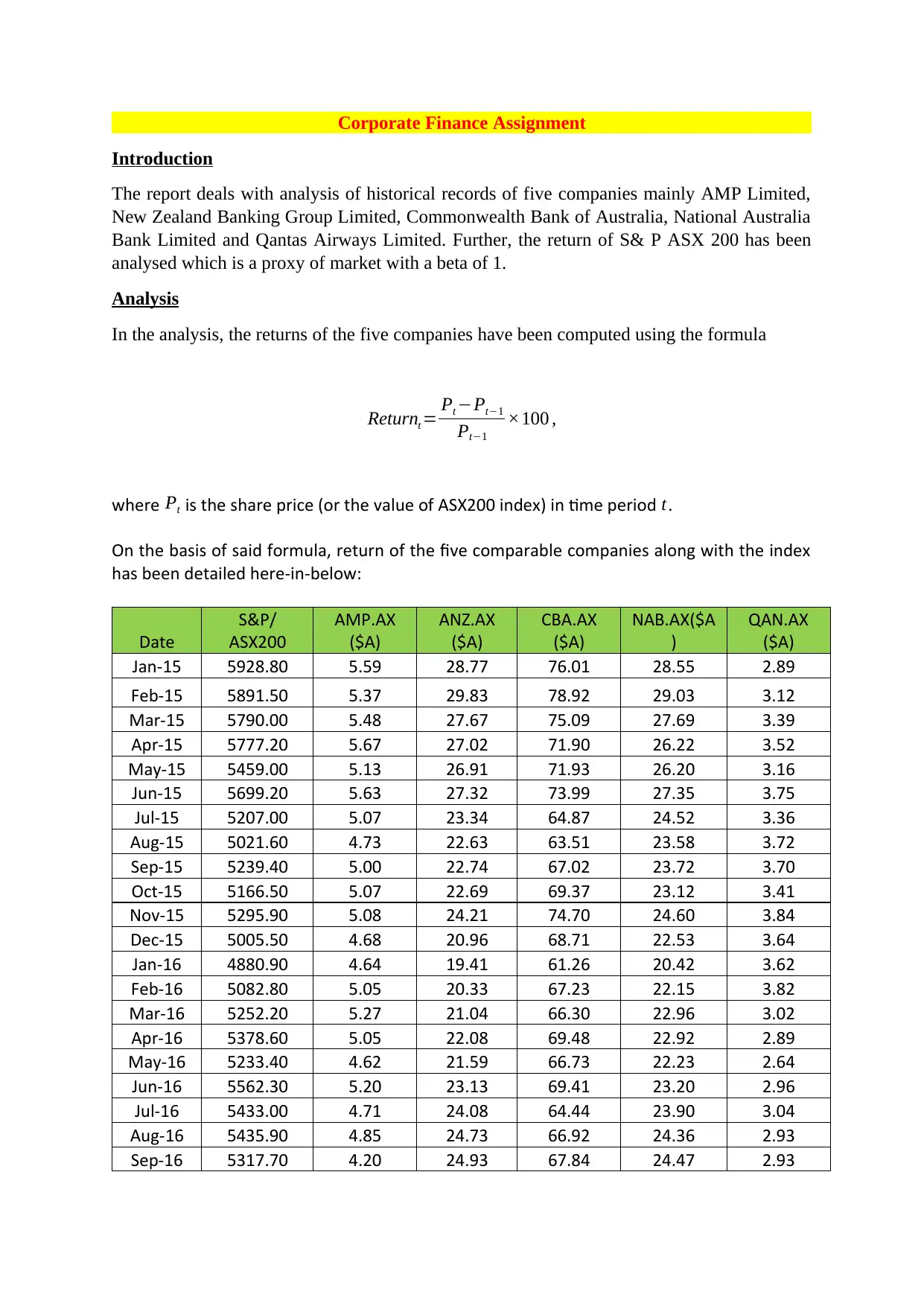

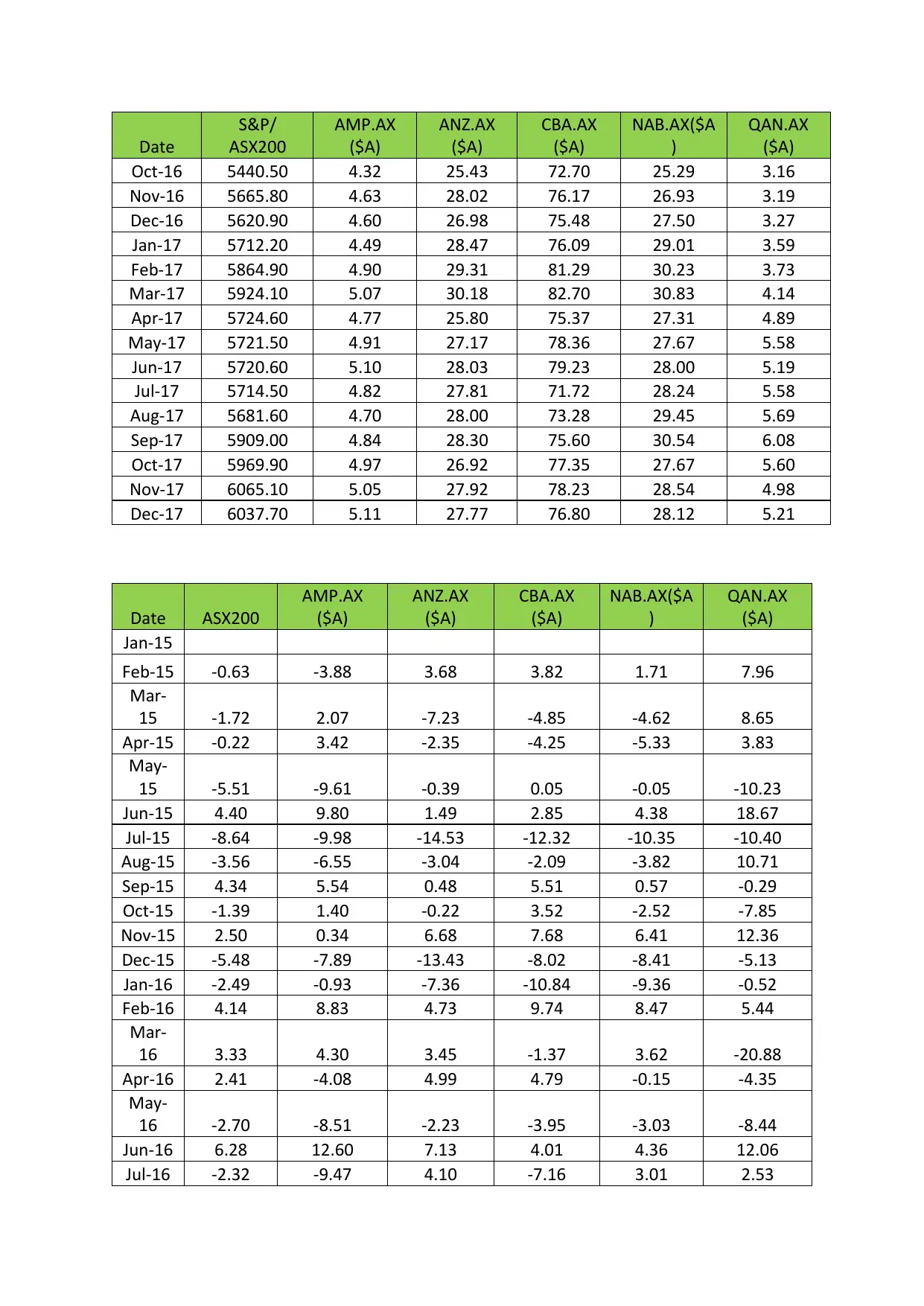

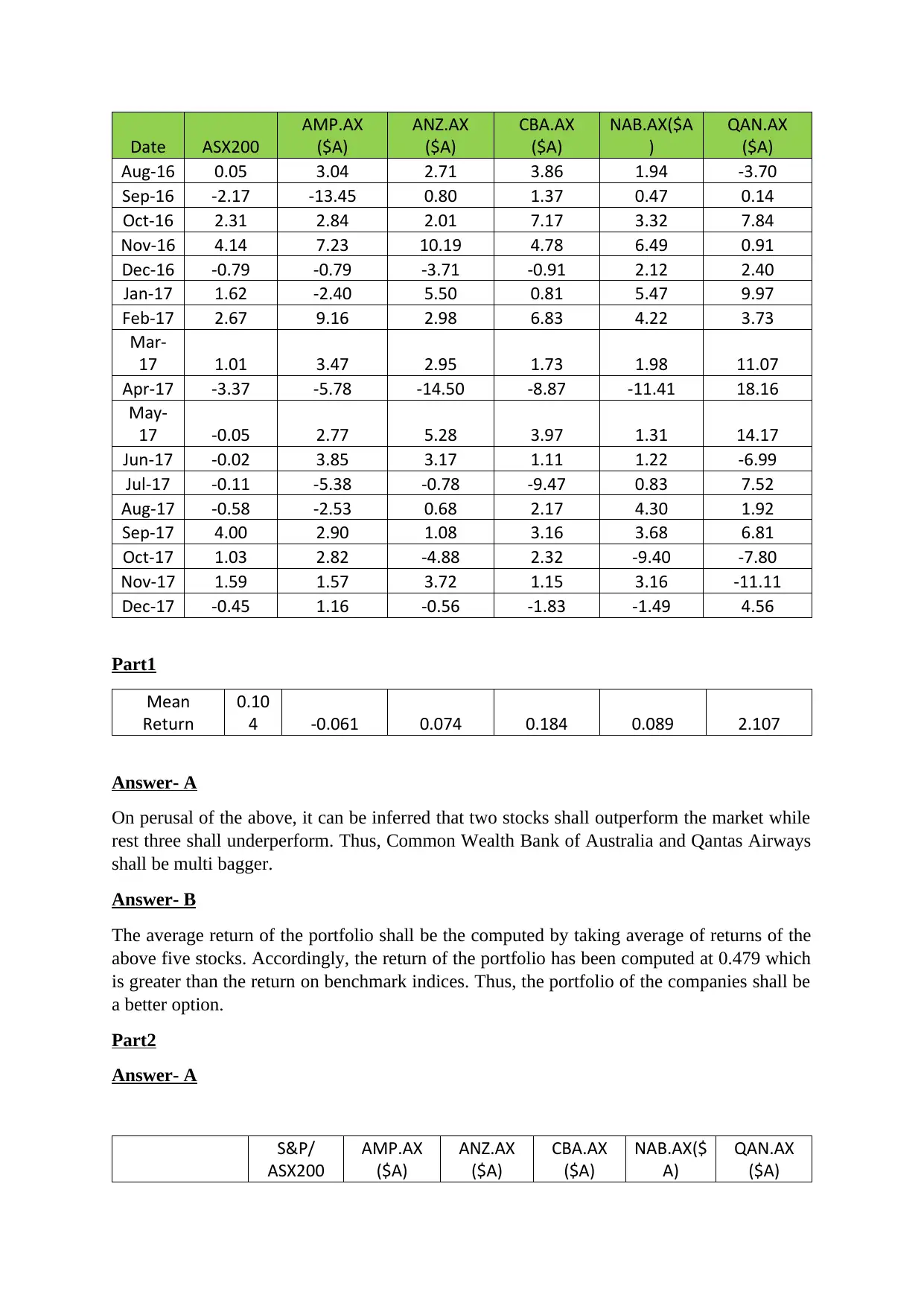

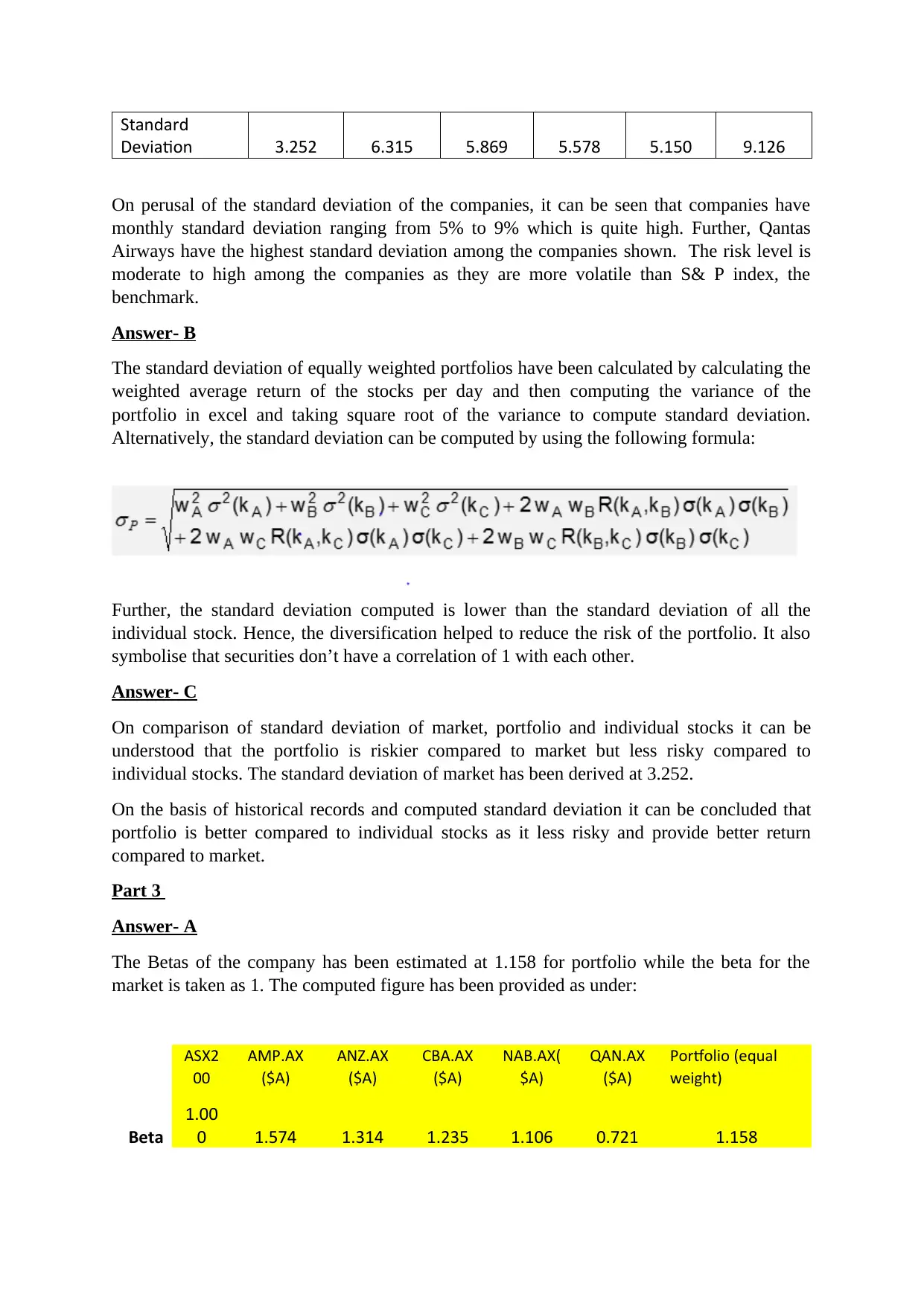

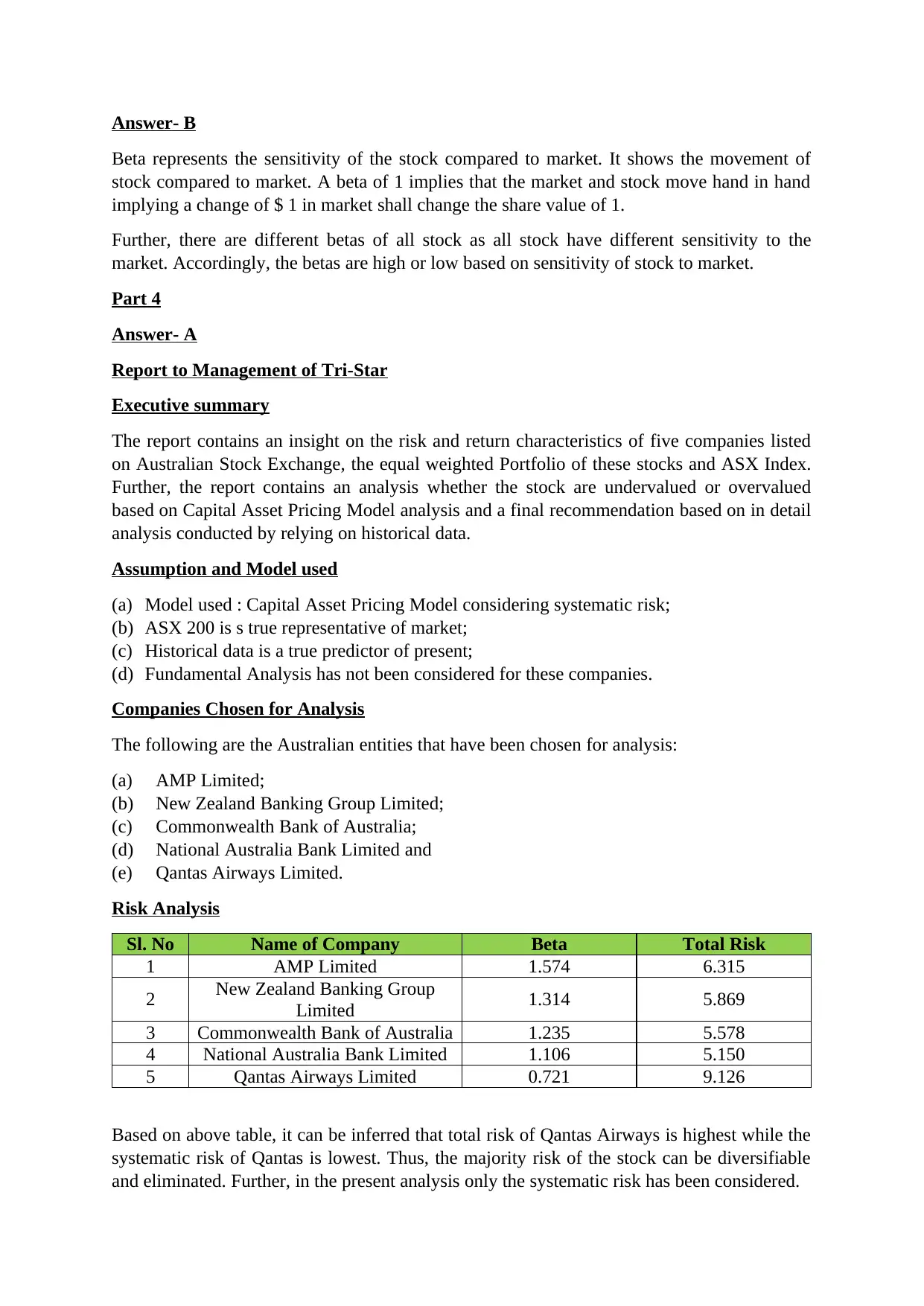

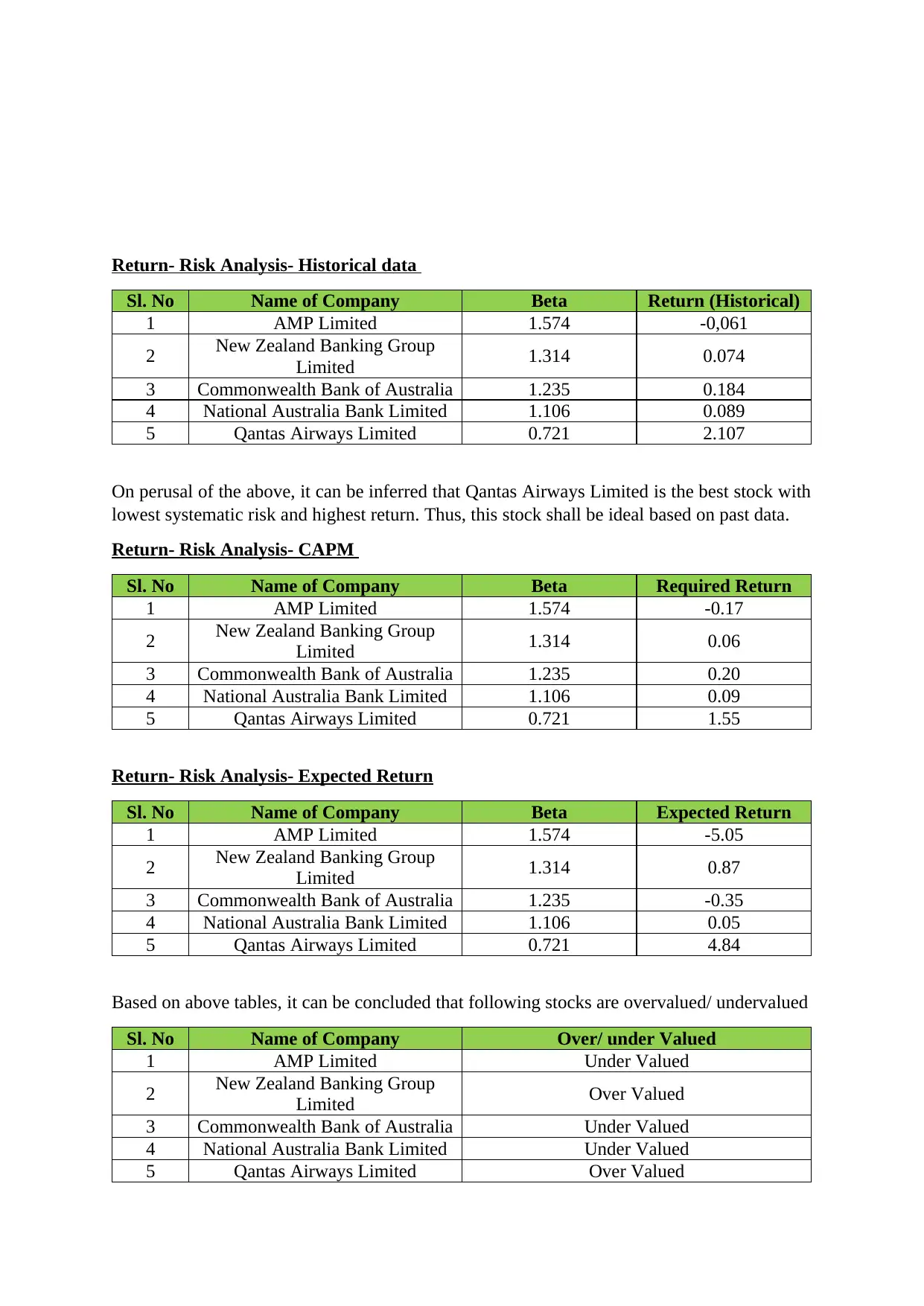

This report presents a comprehensive analysis of the financial performance of five prominent Australian companies: AMP Limited, New Zealand Banking Group Limited, Commonwealth Bank of Australia, National Australia Bank Limited, and Qantas Airways Limited. The analysis spans from January 2015 to December 2017, comparing their returns against the S&P/ASX 200 index, serving as a market proxy. The study computes returns, standard deviations, and betas to assess risk and return profiles. The report includes an examination of the companies' historical data, calculating mean returns and standard deviations. Furthermore, the report utilizes the Capital Asset Pricing Model (CAPM) to evaluate the companies' valuations, classifying them as either undervalued or overvalued. The analysis culminates in investment recommendations, considering both individual stock performance and the potential of an equally weighted portfolio, offering strategic insights for investment decisions.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.