Corporate Finance: Dividend Hypothesis, Repurchase Analysis, Returns

VerifiedAdded on 2020/03/16

|7

|1228

|33

Homework Assignment

AI Summary

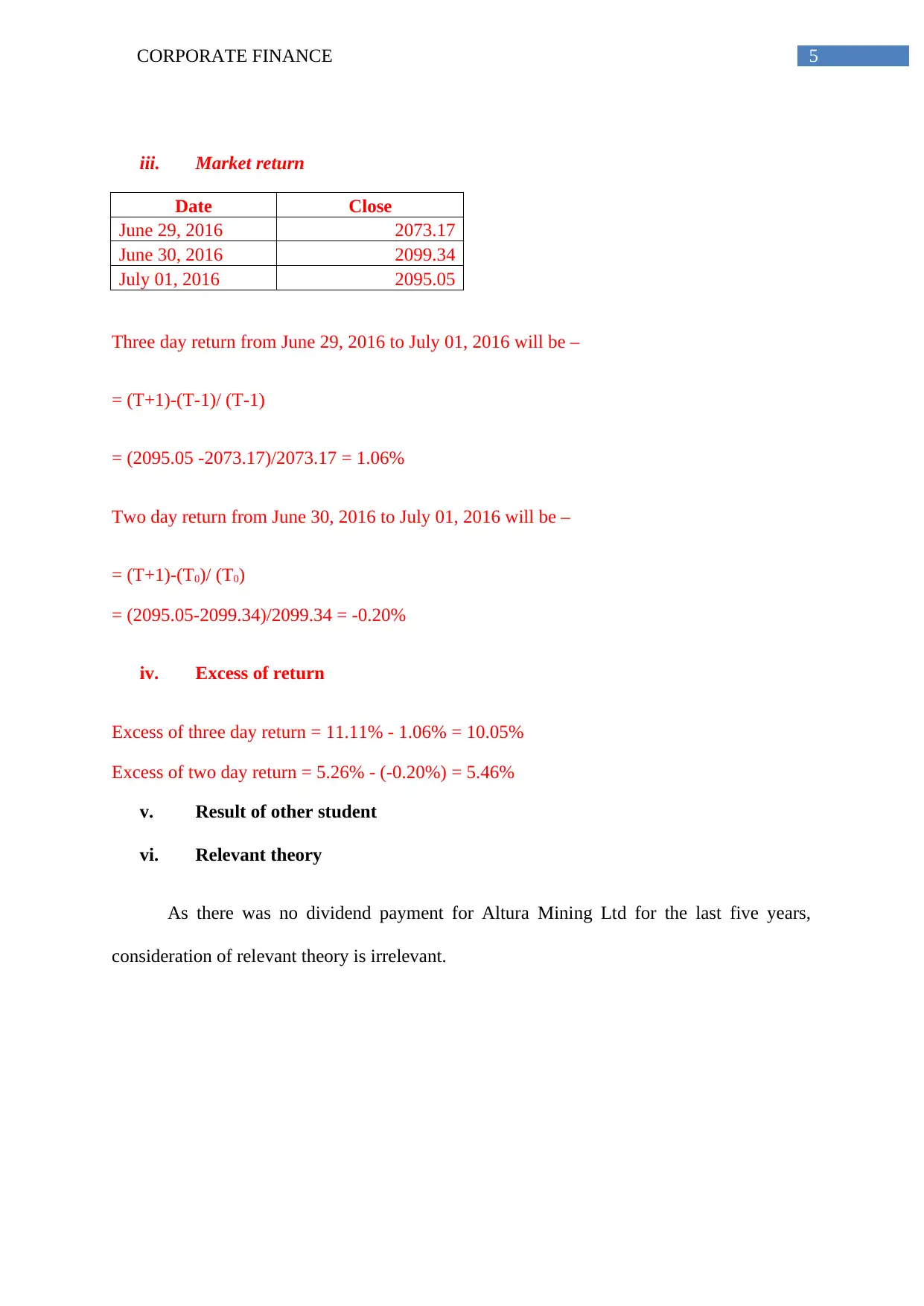

This corporate finance assignment explores the dividend hypothesis, reasons for stock repurchases over dividends under a classical tax system, and return calculations. The assignment delves into the information content or signaling hypothesis, free cash flow hypothesis, and clientele effect related to dividends. It analyzes the advantages of stock repurchases, particularly their tax efficiency and flexibility compared to dividends. The document includes a calculation of returns for a given stock, demonstrating the practical application of financial concepts. The analysis also highlights the irrelevance of dividend-related theories due to the company's dividend history. The student has provided a complete analysis of the subject, making it a good resource for students to understand the concepts.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.