Corporate Finance Report: Evaluation of Ford's Value Enhancement Plan

VerifiedAdded on 2020/10/22

|11

|3719

|151

Report

AI Summary

This report provides a comprehensive analysis of Ford Motor Company's Value Enhancement Plan (VEP), examining various financial strategies and their implications. The report begins with an introduction to corporate finance and the context of Ford's VEP, which aimed to distribute cash reserves to shareholders. It evaluates different options, including the VEP, cash dividends, and share repurchases, concluding that share repurchase is the most suitable plan due to its simplicity and potential to enhance stock value. The report also analyzes the preferences of individual investors, including Ford family members, institutional investors, and regular shareholders, concerning the VEP. Furthermore, it calculates the Weighted Average Cost of Capital (WACC) for Ford, Daimler Chrysler, and General Motors, providing justifications for the WACC calculation and its importance in financial decision-making. The analysis highlights the complexities of the VEP and suggests more conventional and beneficial methods for distributing cash reserves to maximize shareholder value.

Corporate finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK ..............................................................................................................................................1

1. Suitable plan for Ford..............................................................................................................1

2. Individual investor preferences for VEP plan.........................................................................3

3. Calculation of WACC along with its justifications.................................................................4

4. Dividend policy followed by Ford Motor Company...............................................................6

CONCLUSION................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK ..............................................................................................................................................1

1. Suitable plan for Ford..............................................................................................................1

2. Individual investor preferences for VEP plan.........................................................................3

3. Calculation of WACC along with its justifications.................................................................4

4. Dividend policy followed by Ford Motor Company...............................................................6

CONCLUSION................................................................................................................................8

INTRODUCTION

Corporate finance is the branch of an organisation which deals with finance and

investment decisions. This concept is focused to prepare strategies which can be used in short

term and long term financial planning. In this project report a case study on Ford is studied

concerning Value enhancement plan. Ford Company is an American multinational auto maker

which operates in several countries including France, USA and many more and has headquarters

in Dearborn, Michigan. The primary aim of this project report is to develop an understanding

towards the implementation of VEP by Ford. Various alternative plans such as cash dividend and

share repurchase are discussed in this report in order to suggest suitable plan for Ford. Responses

of individual investors are analysed in this report along with justification of WACC. Importance

of dividend policy is described in order to identify rationale behind the policy which is used by

Ford (Brealey, 2012).

TASK

1. Suitable plan for Ford

Ford Motor Company deals in manufacturing cars and trucks and operates in multiple

countries. This organisation had adopted a Value Enhancement Plan in the year of 2000 which

has a main aim of distributing company's accumulated cash reserves to their existing

shareholders. Due to the option provided to shareholders of either receiving cash or cash

equivalent common shares, has raised various issues regarding pro rata basis. In order to resolve

their issues, Ford company is reconsidering their plan and evaluating different options which can

be selected by them. These three options are analysed below in order to suggest Ford the most

suitable plan:

VEP – The Value enhancement plan introduced by Ford was extremely complicated not

only for their shareholders but also for the company itself. According to VEP, Ford has proposed

that every shareholder will either receive 20 dollars against their per common share or will

receive equivalent valued stock but the problem arises when every shareholder preferred cash

and not stocks then the company decided to adopt pro rata basis but that proposal was not

favourable for ample of members. The Complications in this plan begins with offering different

type of tax liability to different members along with complex capital gains and future payout

models. This confusion can be described by an example, if a shareholder has 10 shares of ford

1

Corporate finance is the branch of an organisation which deals with finance and

investment decisions. This concept is focused to prepare strategies which can be used in short

term and long term financial planning. In this project report a case study on Ford is studied

concerning Value enhancement plan. Ford Company is an American multinational auto maker

which operates in several countries including France, USA and many more and has headquarters

in Dearborn, Michigan. The primary aim of this project report is to develop an understanding

towards the implementation of VEP by Ford. Various alternative plans such as cash dividend and

share repurchase are discussed in this report in order to suggest suitable plan for Ford. Responses

of individual investors are analysed in this report along with justification of WACC. Importance

of dividend policy is described in order to identify rationale behind the policy which is used by

Ford (Brealey, 2012).

TASK

1. Suitable plan for Ford

Ford Motor Company deals in manufacturing cars and trucks and operates in multiple

countries. This organisation had adopted a Value Enhancement Plan in the year of 2000 which

has a main aim of distributing company's accumulated cash reserves to their existing

shareholders. Due to the option provided to shareholders of either receiving cash or cash

equivalent common shares, has raised various issues regarding pro rata basis. In order to resolve

their issues, Ford company is reconsidering their plan and evaluating different options which can

be selected by them. These three options are analysed below in order to suggest Ford the most

suitable plan:

VEP – The Value enhancement plan introduced by Ford was extremely complicated not

only for their shareholders but also for the company itself. According to VEP, Ford has proposed

that every shareholder will either receive 20 dollars against their per common share or will

receive equivalent valued stock but the problem arises when every shareholder preferred cash

and not stocks then the company decided to adopt pro rata basis but that proposal was not

favourable for ample of members. The Complications in this plan begins with offering different

type of tax liability to different members along with complex capital gains and future payout

models. This confusion can be described by an example, if a shareholder has 10 shares of ford

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and decides to opt for extra shares and not cash then they will have shares equivalent of 20

dollars each share and according to the their share cost in 2000 that shareholder will have extra

of 7 shares (Clark, Feiner and Viehs, 2015).

This proposal has modified stock dividend due to which simple stock split have been

increased by about 1.6. This plan is considered as to raise disparity among investors as according

to VEP an investor can choose shares over cash which will help them by exempting them from

tax. Another problem in this proposal was that it leads to excessive voting rights. According to

companies act, every share has one vote which can be used to cast the vote at the time of general

meeting. This excess in the voting rights resultant in degrading managerial performance.

Issue a cash dividend – This is a traditional method of distributing cash reserves to the

shareholders. According to this method, cash dividend is the money which is paid to the

shareholders as a part of profit against their investment in company' s stocks. This dividend is a

compulsion over an organisation, they can distribute dividend whenever there is a excessive cash

in their company reserves. These dividends can be paid monthly, quarterly or even yearly basis.

The money is paid to shareholders is done on per share basis in order to ignore the partiality. In

this case scenario, Ford auto mobile company could adapt this method in order to distribute their

cash reserves. Benefits of this method is that there is simplicity in the operations unlike VEP and

there will be higher satisfaction amongst the shareholders. Ford could also gain huge brand

equity by providing 20 dollars per share which is relatively higher than any other organisation.

This method was not selected by this company because of the tax liability which would

be imposed on their shareholders. Cash dividend is a effective method but for Ford, this method

is not that beneficial as they contributing a lot against a share which would raise the problem of

excessive tax liability (Coles, Lemmon and Meschke, 2012).

Share repurchase – According to this method, an organisation buys back their own

share from the market. This process is considered as ideal for the conditions where management

thinks that their shares are undervalued so reducing the number of shares can increase the value

of their shares. Company buys their stocks directly from from the market price at a fixed rate. In

the case scenario of Ford company, the main intention of introducing value enhancement plan

was to increase the value of their share and for that this method is considered as most significant.

After analysing all the methods, this has been observed that Value enhancement plan had

various complexities due to which, company faced various issues. Share repurchase is a more

2

dollars each share and according to the their share cost in 2000 that shareholder will have extra

of 7 shares (Clark, Feiner and Viehs, 2015).

This proposal has modified stock dividend due to which simple stock split have been

increased by about 1.6. This plan is considered as to raise disparity among investors as according

to VEP an investor can choose shares over cash which will help them by exempting them from

tax. Another problem in this proposal was that it leads to excessive voting rights. According to

companies act, every share has one vote which can be used to cast the vote at the time of general

meeting. This excess in the voting rights resultant in degrading managerial performance.

Issue a cash dividend – This is a traditional method of distributing cash reserves to the

shareholders. According to this method, cash dividend is the money which is paid to the

shareholders as a part of profit against their investment in company' s stocks. This dividend is a

compulsion over an organisation, they can distribute dividend whenever there is a excessive cash

in their company reserves. These dividends can be paid monthly, quarterly or even yearly basis.

The money is paid to shareholders is done on per share basis in order to ignore the partiality. In

this case scenario, Ford auto mobile company could adapt this method in order to distribute their

cash reserves. Benefits of this method is that there is simplicity in the operations unlike VEP and

there will be higher satisfaction amongst the shareholders. Ford could also gain huge brand

equity by providing 20 dollars per share which is relatively higher than any other organisation.

This method was not selected by this company because of the tax liability which would

be imposed on their shareholders. Cash dividend is a effective method but for Ford, this method

is not that beneficial as they contributing a lot against a share which would raise the problem of

excessive tax liability (Coles, Lemmon and Meschke, 2012).

Share repurchase – According to this method, an organisation buys back their own

share from the market. This process is considered as ideal for the conditions where management

thinks that their shares are undervalued so reducing the number of shares can increase the value

of their shares. Company buys their stocks directly from from the market price at a fixed rate. In

the case scenario of Ford company, the main intention of introducing value enhancement plan

was to increase the value of their share and for that this method is considered as most significant.

After analysing all the methods, this has been observed that Value enhancement plan had

various complexities due to which, company faced various issues. Share repurchase is a more

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

conventional and beneficial method as it is easy to be interpreted. Using this method of

distributing cash reserves can be more effective as they can enhance the value of their stocks

without giving up any cash. Under this method, Ford can buy back their shares from the market

and lower the number of shares which will automatically results in increased value of their

stocks. VEP or cash dividend should not be selected by Ford as according to these methods,

company has to give up their cash reserves but in the case of stock repurchase organisation can

use those cash reserves to purchase their own shares from market and enhance their reputation

and credibility (Grenadier and Malenko, 2011).

2. Individual investor preferences for VEP plan

If the Value enhancement plan is implemented by Ford, the responses and reactions of

various individual investors of Ford are discussed below:

Ford family member holding Class B shares:

The member of Ford family would prefer to increase their stake in the firm for which

they would chose a mix of cash and shares as by the way of that they can maintain their

superiority in the voting rights and can also earn profit by the dividend which is 20 dollars per

shares. For example, A member of Ford family has chosen a combination of stocks and cash than

they will be eligible to maintain their voting rights along with no tax liability and can also earn a

decent amount of cash. This combination can benefit them by providing them an substantial

amount of cash as well as Ford common stocks which can serve their purpose of value

enhancement. For a Ford family member this option is better than previous option (Cronqvist,

Makhija and Yonker, 2012).

An institutional investor:

Institutional investors are the organisations which are interested in investing in the stocks

of other listed company. TIAA-CREF is a national services organisation which has huge

combined assets and is a leading provider of retirement and academic services. Another

institutional investor mentioned in this case scenario is Calpers. Calpers is a government

regulated agency stands for California Public Employees Retirement System which manages

pension and health benefits. These two mentioned institutions are the investors of Ford and they

would prefer mic of shares and cash. The selection of this combination is based on the

philosophy that funds and trusts considers the dividend amount as incomes which can last only

for short interval. The another reason of selecting this combination is that these institutions are

3

distributing cash reserves can be more effective as they can enhance the value of their stocks

without giving up any cash. Under this method, Ford can buy back their shares from the market

and lower the number of shares which will automatically results in increased value of their

stocks. VEP or cash dividend should not be selected by Ford as according to these methods,

company has to give up their cash reserves but in the case of stock repurchase organisation can

use those cash reserves to purchase their own shares from market and enhance their reputation

and credibility (Grenadier and Malenko, 2011).

2. Individual investor preferences for VEP plan

If the Value enhancement plan is implemented by Ford, the responses and reactions of

various individual investors of Ford are discussed below:

Ford family member holding Class B shares:

The member of Ford family would prefer to increase their stake in the firm for which

they would chose a mix of cash and shares as by the way of that they can maintain their

superiority in the voting rights and can also earn profit by the dividend which is 20 dollars per

shares. For example, A member of Ford family has chosen a combination of stocks and cash than

they will be eligible to maintain their voting rights along with no tax liability and can also earn a

decent amount of cash. This combination can benefit them by providing them an substantial

amount of cash as well as Ford common stocks which can serve their purpose of value

enhancement. For a Ford family member this option is better than previous option (Cronqvist,

Makhija and Yonker, 2012).

An institutional investor:

Institutional investors are the organisations which are interested in investing in the stocks

of other listed company. TIAA-CREF is a national services organisation which has huge

combined assets and is a leading provider of retirement and academic services. Another

institutional investor mentioned in this case scenario is Calpers. Calpers is a government

regulated agency stands for California Public Employees Retirement System which manages

pension and health benefits. These two mentioned institutions are the investors of Ford and they

would prefer mic of shares and cash. The selection of this combination is based on the

philosophy that funds and trusts considers the dividend amount as incomes which can last only

for short interval. The another reason of selecting this combination is that these institutions are

3

exempted from tax liability and they can store as much cash they want to, but under proper

governance. But in order to maintain their cash payout system they have also selected a part of

shares in their combination so that they can avoid reduction of holdings. For example, Investor

such as TIAA-CREF holds shares of Ford worth 6 million dollars then they can select the option

of having cash for most of their shares which will not impose any tax liability on them and in

addition few shares will also be redeemed which will help them in maintaining their pay out

ratio. The main reason behind selecting this combination is, all stock will leave them with no

cash to pay to their investors and all cash will dis-balance their cash payout system. Thus a mix

of cash and stock is perfect for them as it will optimise their holding value by minimising yielded

cash (Damodaran, 2016).

A regular outsider shareholder:

A regular shareholder which does not has any direct relationship with the company would

prefer all cash option. For example, a shareholder which has shareholding of 500 shares is

eligible to receive 20 dollars per share, which gives that shareholder cash of 10000 dollars. Even

after paying their tax liability, this shareholder would have a total of 8500 dollars cash. This

option is considered as most suitable for regular individual shareholders as this cash will be

considered as capital gains by them. Despite of the fact that the payout will decrease by the time,

an outside investor will still be able to earn profit. Problems related with this option is that they

can not increase the superiority of their voting rights and they have to comply all their tax

liabilities but for an regular outside investor, voting rights is not an important concern and tax

liabilities does not concerns them much because they are earning 20 dollars per share (Fracassi,

2016).

After analysing the responses and their justification, it has been observed that individual

outside investors is more concerned with short term profit whereas institutional investors and

Ford family investors are more focused on acquirement of maximum shares as they will result in

long term profitability. This section criteria has various justifications which are mentioned above

can also turn the preferences of investors according to the diverse conditions (Fan, 2011).

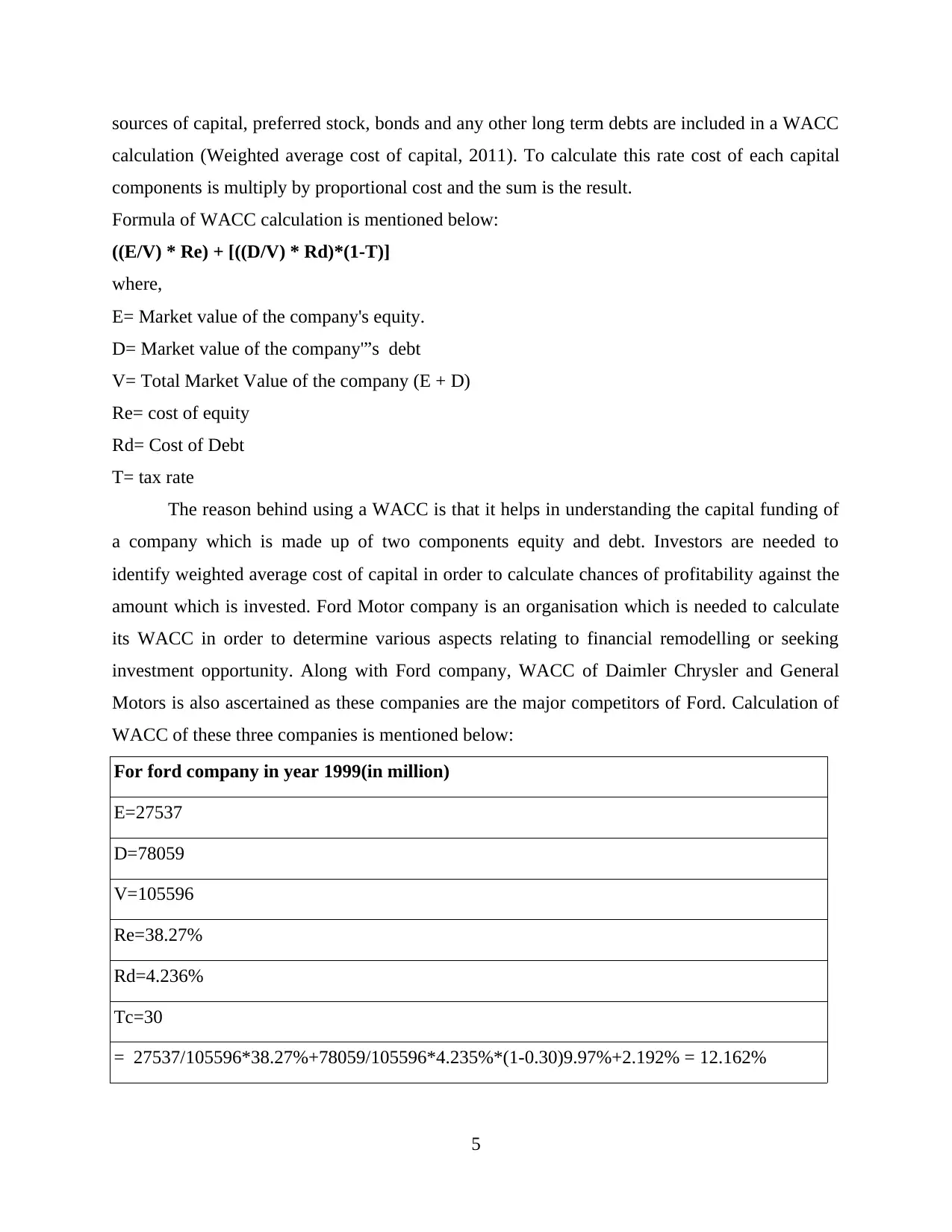

3. Calculation of WACC along with its justifications

WACC is a method of calculating firm's average cost of capital through which each

capital and assets is weighted by total percentage of total capital. It is a rate that a company is

going to pay on a weighted average to all its equity holder in order to finance their assets. All

4

governance. But in order to maintain their cash payout system they have also selected a part of

shares in their combination so that they can avoid reduction of holdings. For example, Investor

such as TIAA-CREF holds shares of Ford worth 6 million dollars then they can select the option

of having cash for most of their shares which will not impose any tax liability on them and in

addition few shares will also be redeemed which will help them in maintaining their pay out

ratio. The main reason behind selecting this combination is, all stock will leave them with no

cash to pay to their investors and all cash will dis-balance their cash payout system. Thus a mix

of cash and stock is perfect for them as it will optimise their holding value by minimising yielded

cash (Damodaran, 2016).

A regular outsider shareholder:

A regular shareholder which does not has any direct relationship with the company would

prefer all cash option. For example, a shareholder which has shareholding of 500 shares is

eligible to receive 20 dollars per share, which gives that shareholder cash of 10000 dollars. Even

after paying their tax liability, this shareholder would have a total of 8500 dollars cash. This

option is considered as most suitable for regular individual shareholders as this cash will be

considered as capital gains by them. Despite of the fact that the payout will decrease by the time,

an outside investor will still be able to earn profit. Problems related with this option is that they

can not increase the superiority of their voting rights and they have to comply all their tax

liabilities but for an regular outside investor, voting rights is not an important concern and tax

liabilities does not concerns them much because they are earning 20 dollars per share (Fracassi,

2016).

After analysing the responses and their justification, it has been observed that individual

outside investors is more concerned with short term profit whereas institutional investors and

Ford family investors are more focused on acquirement of maximum shares as they will result in

long term profitability. This section criteria has various justifications which are mentioned above

can also turn the preferences of investors according to the diverse conditions (Fan, 2011).

3. Calculation of WACC along with its justifications

WACC is a method of calculating firm's average cost of capital through which each

capital and assets is weighted by total percentage of total capital. It is a rate that a company is

going to pay on a weighted average to all its equity holder in order to finance their assets. All

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sources of capital, preferred stock, bonds and any other long term debts are included in a WACC

calculation (Weighted average cost of capital, 2011). To calculate this rate cost of each capital

components is multiply by proportional cost and the sum is the result.

Formula of WACC calculation is mentioned below:

((E/V) * Re) + [((D/V) * Rd)*(1-T)]

where,

E= Market value of the company's equity.

D= Market value of the company'”s debt

V= Total Market Value of the company (E + D)

Re= cost of equity

Rd= Cost of Debt

T= tax rate

The reason behind using a WACC is that it helps in understanding the capital funding of

a company which is made up of two components equity and debt. Investors are needed to

identify weighted average cost of capital in order to calculate chances of profitability against the

amount which is invested. Ford Motor company is an organisation which is needed to calculate

its WACC in order to determine various aspects relating to financial remodelling or seeking

investment opportunity. Along with Ford company, WACC of Daimler Chrysler and General

Motors is also ascertained as these companies are the major competitors of Ford. Calculation of

WACC of these three companies is mentioned below:

For ford company in year 1999(in million)

E=27537

D=78059

V=105596

Re=38.27%

Rd=4.236%

Tc=30

= 27537/105596*38.27%+78059/105596*4.235%*(1-0.30)9.97%+2.192% = 12.162%

5

calculation (Weighted average cost of capital, 2011). To calculate this rate cost of each capital

components is multiply by proportional cost and the sum is the result.

Formula of WACC calculation is mentioned below:

((E/V) * Re) + [((D/V) * Rd)*(1-T)]

where,

E= Market value of the company's equity.

D= Market value of the company'”s debt

V= Total Market Value of the company (E + D)

Re= cost of equity

Rd= Cost of Debt

T= tax rate

The reason behind using a WACC is that it helps in understanding the capital funding of

a company which is made up of two components equity and debt. Investors are needed to

identify weighted average cost of capital in order to calculate chances of profitability against the

amount which is invested. Ford Motor company is an organisation which is needed to calculate

its WACC in order to determine various aspects relating to financial remodelling or seeking

investment opportunity. Along with Ford company, WACC of Daimler Chrysler and General

Motors is also ascertained as these companies are the major competitors of Ford. Calculation of

WACC of these three companies is mentioned below:

For ford company in year 1999(in million)

E=27537

D=78059

V=105596

Re=38.27%

Rd=4.236%

Tc=30

= 27537/105596*38.27%+78059/105596*4.235%*(1-0.30)9.97%+2.192% = 12.162%

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

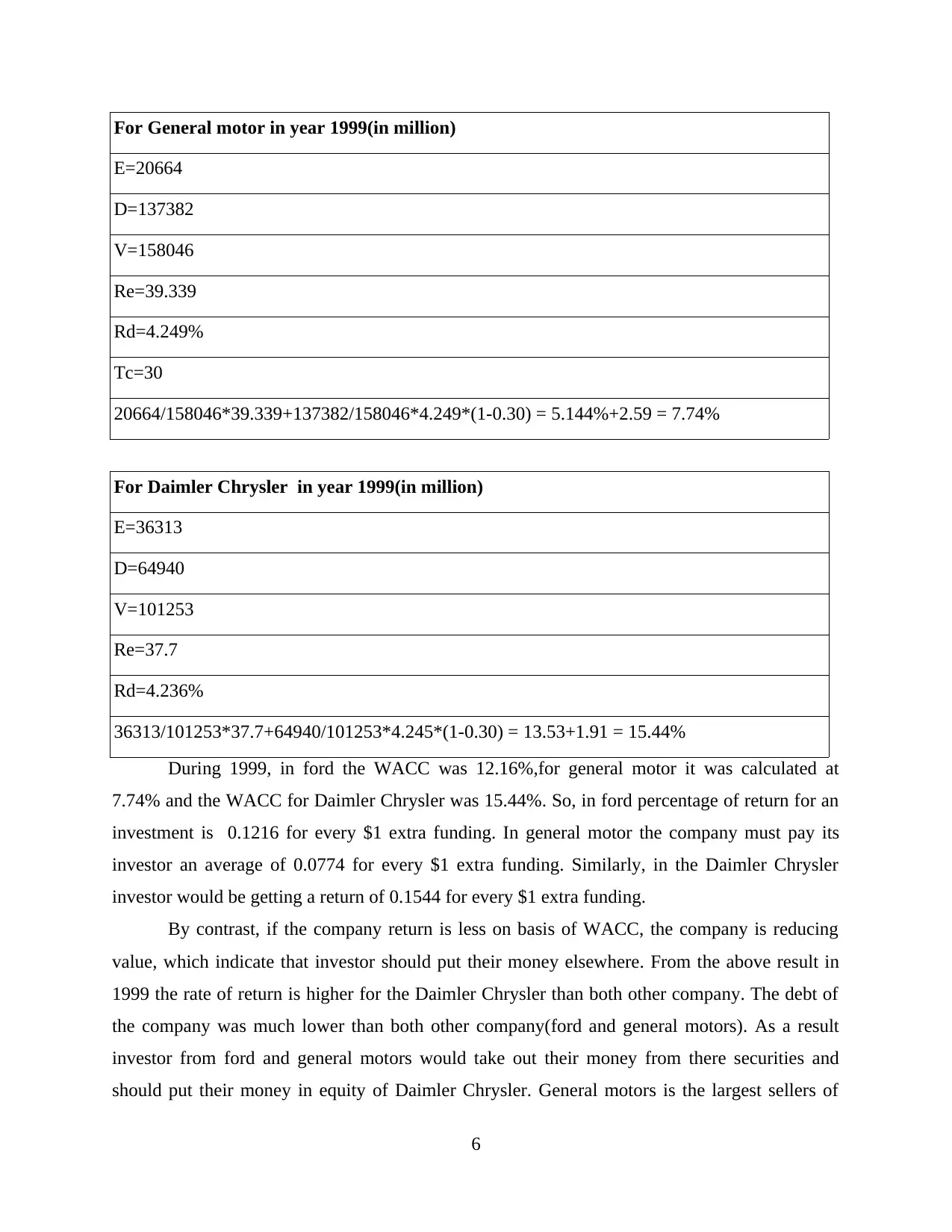

For General motor in year 1999(in million)

E=20664

D=137382

V=158046

Re=39.339

Rd=4.249%

Tc=30

20664/158046*39.339+137382/158046*4.249*(1-0.30) = 5.144%+2.59 = 7.74%

For Daimler Chrysler in year 1999(in million)

E=36313

D=64940

V=101253

Re=37.7

Rd=4.236%

36313/101253*37.7+64940/101253*4.245*(1-0.30) = 13.53+1.91 = 15.44%

During 1999, in ford the WACC was 12.16%,for general motor it was calculated at

7.74% and the WACC for Daimler Chrysler was 15.44%. So, in ford percentage of return for an

investment is 0.1216 for every $1 extra funding. In general motor the company must pay its

investor an average of 0.0774 for every $1 extra funding. Similarly, in the Daimler Chrysler

investor would be getting a return of 0.1544 for every $1 extra funding.

By contrast, if the company return is less on basis of WACC, the company is reducing

value, which indicate that investor should put their money elsewhere. From the above result in

1999 the rate of return is higher for the Daimler Chrysler than both other company. The debt of

the company was much lower than both other company(ford and general motors). As a result

investor from ford and general motors would take out their money from there securities and

should put their money in equity of Daimler Chrysler. General motors is the largest sellers of

6

E=20664

D=137382

V=158046

Re=39.339

Rd=4.249%

Tc=30

20664/158046*39.339+137382/158046*4.249*(1-0.30) = 5.144%+2.59 = 7.74%

For Daimler Chrysler in year 1999(in million)

E=36313

D=64940

V=101253

Re=37.7

Rd=4.236%

36313/101253*37.7+64940/101253*4.245*(1-0.30) = 13.53+1.91 = 15.44%

During 1999, in ford the WACC was 12.16%,for general motor it was calculated at

7.74% and the WACC for Daimler Chrysler was 15.44%. So, in ford percentage of return for an

investment is 0.1216 for every $1 extra funding. In general motor the company must pay its

investor an average of 0.0774 for every $1 extra funding. Similarly, in the Daimler Chrysler

investor would be getting a return of 0.1544 for every $1 extra funding.

By contrast, if the company return is less on basis of WACC, the company is reducing

value, which indicate that investor should put their money elsewhere. From the above result in

1999 the rate of return is higher for the Daimler Chrysler than both other company. The debt of

the company was much lower than both other company(ford and general motors). As a result

investor from ford and general motors would take out their money from there securities and

should put their money in equity of Daimler Chrysler. General motors is the largest sellers of

6

cars and has turnover which is greater than Ford but then also when it comes to WACC, Ford has

approximately 12% which is way more than of General motors that is 7%. The above

calculations are presented using financial statements of all the companies. Year 1999 is selected

for this comparison.

4. Dividend policy followed by Ford Motor Company

This is a policy is concerned with the structure of payment to shareholder, owner and

stockholder of the firm. It is a policy of financial policy regarding paying cash dividend in the

present time or payment in future stage for their increased dividend. The term dividend refer to

that portion of profit (after tax) which must be distributed among shareholder on his

shareholding.

In other words, dividend policy means guidelines/plans followed by the management in

declaring of dividend on the other hand making decision about how much to do retaining and

reinvesting earning in the firm. Most companies consider a dividend policy as an integral part of

the corporate strategy. On the basis of these theories there are three type of dividend policy:

Stable Dividend Policy -one of the most easiest and commonly used in which a certain

amount of money is regular paid to their shareholder. Further it is classified on what basis

amount are paid per share-

Constant Dividend Per Share- here a reserve fund is raised to pay fixed amount of

dividend every year even if in the year earning of company it not enough of there are

losses (Hillier, 2013).

Constant pay out ratio- Here fixed percentage of earning are distributed as dividend

every year.

Stable Rupee Dividend+Extra Dividend -here extra dividend are given in the year when

company earns high profit plus constant payment (Hillier, Titman, 2011).

Regular Dividend Policy - under this investor gets dividend at usual rate as the wants to

get regular income for example investor like retired person .

Residual Dividend policy - this policy means dividend should be paid only if there are

fund left after all its capital expenditure happens or all investment have been financed. The

primary focus of the firm is on investment therefore dividend policy a passive decision variable.

Ford Motor Company has a huge brand image due to their effective dividend policies.

Dividend is the part of profit which is given to shareholders. By reducing the debt liabilities and

7

approximately 12% which is way more than of General motors that is 7%. The above

calculations are presented using financial statements of all the companies. Year 1999 is selected

for this comparison.

4. Dividend policy followed by Ford Motor Company

This is a policy is concerned with the structure of payment to shareholder, owner and

stockholder of the firm. It is a policy of financial policy regarding paying cash dividend in the

present time or payment in future stage for their increased dividend. The term dividend refer to

that portion of profit (after tax) which must be distributed among shareholder on his

shareholding.

In other words, dividend policy means guidelines/plans followed by the management in

declaring of dividend on the other hand making decision about how much to do retaining and

reinvesting earning in the firm. Most companies consider a dividend policy as an integral part of

the corporate strategy. On the basis of these theories there are three type of dividend policy:

Stable Dividend Policy -one of the most easiest and commonly used in which a certain

amount of money is regular paid to their shareholder. Further it is classified on what basis

amount are paid per share-

Constant Dividend Per Share- here a reserve fund is raised to pay fixed amount of

dividend every year even if in the year earning of company it not enough of there are

losses (Hillier, 2013).

Constant pay out ratio- Here fixed percentage of earning are distributed as dividend

every year.

Stable Rupee Dividend+Extra Dividend -here extra dividend are given in the year when

company earns high profit plus constant payment (Hillier, Titman, 2011).

Regular Dividend Policy - under this investor gets dividend at usual rate as the wants to

get regular income for example investor like retired person .

Residual Dividend policy - this policy means dividend should be paid only if there are

fund left after all its capital expenditure happens or all investment have been financed. The

primary focus of the firm is on investment therefore dividend policy a passive decision variable.

Ford Motor Company has a huge brand image due to their effective dividend policies.

Dividend is the part of profit which is given to shareholders. By reducing the debt liabilities and

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

having continuous positive earnings dividends which are contributed are better. According to the

dividend policy of Ford, they use various combinations of dividend such as dividend as cash,

dividend as shares or a combination of both of them. For example, In the year of 2006 this

company has contributed 3.5 million dollars as dividend (Ehrhardt and Brigham, 2016).

Dividend policies of this company are not fixed and keep on changing according to the

situations and necessities of their shareholders. As in the year of 2000, this company decided to

distribute dividend using Value enhancement plan which resultant into failure and then they

adapted the traditional method of dividend and that is stock repurchase in which they purchased

their own shares from the market in order to increase the value of their shares.

The Framework by which this company decides their amount of dividend is mentioned below:

Net income – (Capital expenditures – Depreciation).

By using above formula, this company distributes their excess cash reserve and profit as

dividend. Dividend policy has always considered as most important because they understand that

dividend can help them in gaining trust of shareholders and brand equity. Ford pays out dividend

only when they have suitable cash reserves. In the year 2007-2012 Ford has not distributed any

dividend as they were facing issues of cash deficiency. This company pays dividend when none

of the others organisation can even think of contributing towards their shareholders (Baker and

Wurgler 2013).

CONCLUSION

From the above project report, it has been concluded that finance corporate is that branch

of an organisation which helps in making investment decision. This project report is concerned

with Value enhancement plan of Ford Motor Company. After analysing the case it has been

observed that the above mentioned company should conduct a share repurchase in order to

improve the value of their shares as VEP plan is much more complex. Various responses and

reactions of several parties are evaluated in order to ascertain what group prefer what

combination of choices of dividend provided by Ford company. Weighted average cost of capital

of three companies is calculated in this project, these companies are Ford Motor Company,

General Motors and DaimlerChrysler in order to analyse the return of Ford as the other two

companies are their major competitors. Dividend policy of this company is evaluated in order to

identify the strategies and the rationale behind those plans and policies. From the case study, it

8

dividend policy of Ford, they use various combinations of dividend such as dividend as cash,

dividend as shares or a combination of both of them. For example, In the year of 2006 this

company has contributed 3.5 million dollars as dividend (Ehrhardt and Brigham, 2016).

Dividend policies of this company are not fixed and keep on changing according to the

situations and necessities of their shareholders. As in the year of 2000, this company decided to

distribute dividend using Value enhancement plan which resultant into failure and then they

adapted the traditional method of dividend and that is stock repurchase in which they purchased

their own shares from the market in order to increase the value of their shares.

The Framework by which this company decides their amount of dividend is mentioned below:

Net income – (Capital expenditures – Depreciation).

By using above formula, this company distributes their excess cash reserve and profit as

dividend. Dividend policy has always considered as most important because they understand that

dividend can help them in gaining trust of shareholders and brand equity. Ford pays out dividend

only when they have suitable cash reserves. In the year 2007-2012 Ford has not distributed any

dividend as they were facing issues of cash deficiency. This company pays dividend when none

of the others organisation can even think of contributing towards their shareholders (Baker and

Wurgler 2013).

CONCLUSION

From the above project report, it has been concluded that finance corporate is that branch

of an organisation which helps in making investment decision. This project report is concerned

with Value enhancement plan of Ford Motor Company. After analysing the case it has been

observed that the above mentioned company should conduct a share repurchase in order to

improve the value of their shares as VEP plan is much more complex. Various responses and

reactions of several parties are evaluated in order to ascertain what group prefer what

combination of choices of dividend provided by Ford company. Weighted average cost of capital

of three companies is calculated in this project, these companies are Ford Motor Company,

General Motors and DaimlerChrysler in order to analyse the return of Ford as the other two

companies are their major competitors. Dividend policy of this company is evaluated in order to

identify the strategies and the rationale behind those plans and policies. From the case study, it

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

has been recommended that Ford Motor Company should have adopted stock repurchase and not

VEP plan.

9

VEP plan.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.