Corporate Accounting Report: Finance and Investment Decisions

VerifiedAdded on 2023/01/11

|11

|2483

|59

Report

AI Summary

This report, prepared for a Board of Directors, analyzes financial decisions for a recently quoted company, focusing on raising capital and evaluating a new investment opportunity. The report assesses the current capital structure, calculates the Weighted Average Cost of Capital (WACC) under different financing scenarios (equity only, debt only, and the existing structure), and recommends the most cost-efficient method for raising additional capital. The investment proposal analyzes a new product launch, calculating cash flows, and evaluating profitability using Net Present Value (NPV) and payback period methods. The analysis concludes that raising capital through equity is the most beneficial option and the proposed investment is not profitable.

CORPORATE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

REPORT..........................................................................................................................................1

Financial Proposal.......................................................................................................................1

Investment Proposal.....................................................................................................................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

REPORT..........................................................................................................................................1

Financial Proposal.......................................................................................................................1

Investment Proposal.....................................................................................................................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Corporate accounting refers to the branch of accounting that deals with recording of

accounting transaction of the companies for the preparation of financial statements such as

income statement, cash flow statement, balance sheet, analysis and also for the interpretation of

financial results of the companies. Corporate accounting also helps the enterprise in ensuring a

optimum capital structure analysing the cost of every option. With use of corporate accounting

managers also take various investments decisions about the profitability of the proposed

investments. Present report i based over application of concepts and techniques of corporate

accounting for deciding the ways of raising capital that is optimum. It will also provide the

company about the viability of investments in new proposed products by measuring the cash

flows that will be generated by the company. This will enhance the understanding about the

concepts of various accounting tools for effective decision making. Concepts will be explained

through the numerical examples in the report.

REPORT

Financial Proposal

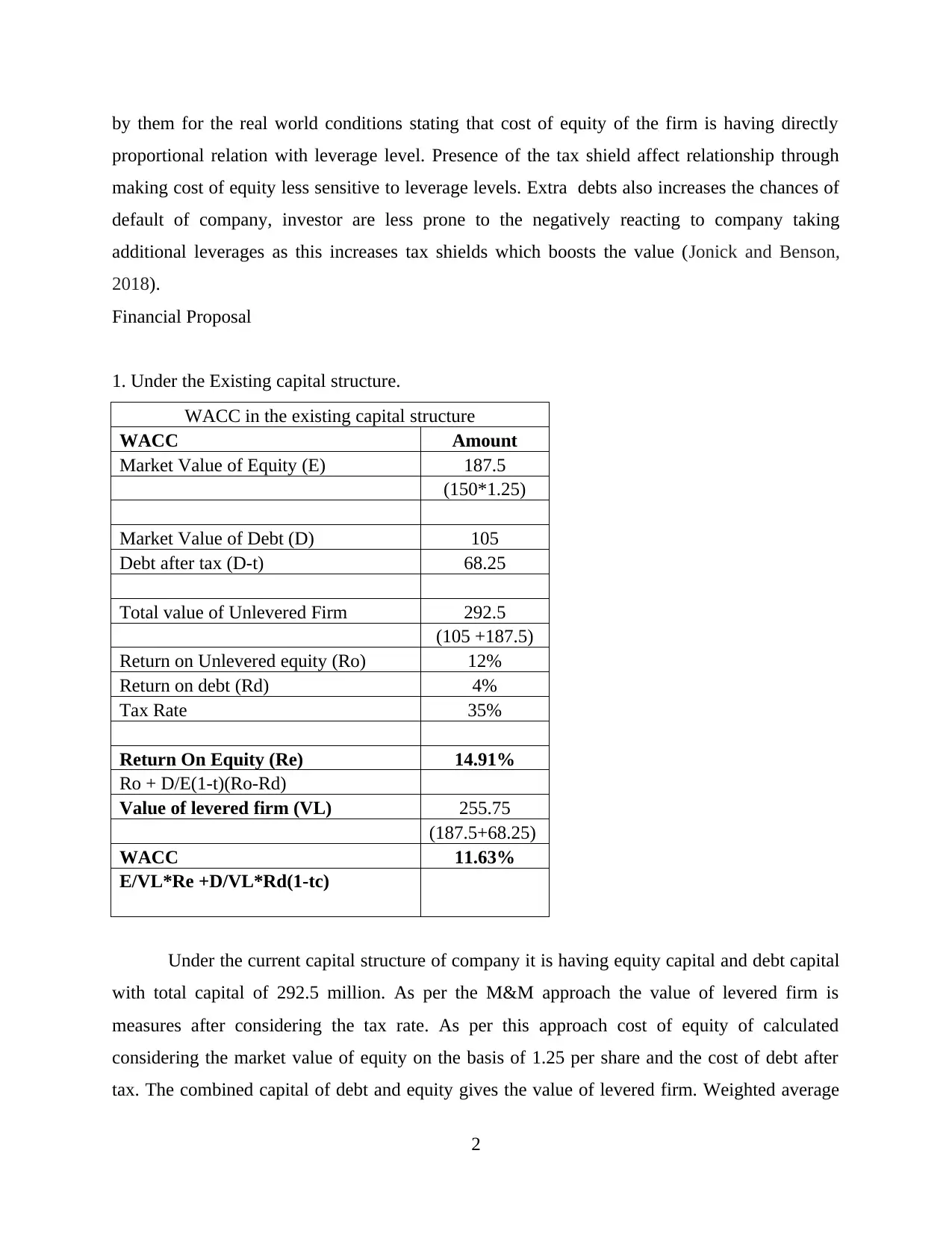

Current Scenario of the company

Current Capital Structure €m

Issued Share Capital: 150,000,000 Ordinary Shares of 50c

each 75

Long-term debt 105

Company is currently having a capital structure of issued share capital valued at 50c that

equals to 75 million and with the debt capital of 105 million. Company is having higher of the

debt capital in comparison with the equity capital. Cost of equity of the unlevered firm is 12%

and the cost of long term debt is 4%. Company is having optimum capital structures as the

market value of shares is €1.25 each (Mulatinho and et.al., 2019).

Cost of capital is measured using Modigliani & Miller Proposition II approach with taxes

under all the three scenarios.

M&M approach is the most commonly used approach in the corporate world. It was

developed by France Modigliani & Merton Miller in the year 1985. The main idea behind the

concept is that it does not affect the overall value of the firm. The second proposition was given

1

Corporate accounting refers to the branch of accounting that deals with recording of

accounting transaction of the companies for the preparation of financial statements such as

income statement, cash flow statement, balance sheet, analysis and also for the interpretation of

financial results of the companies. Corporate accounting also helps the enterprise in ensuring a

optimum capital structure analysing the cost of every option. With use of corporate accounting

managers also take various investments decisions about the profitability of the proposed

investments. Present report i based over application of concepts and techniques of corporate

accounting for deciding the ways of raising capital that is optimum. It will also provide the

company about the viability of investments in new proposed products by measuring the cash

flows that will be generated by the company. This will enhance the understanding about the

concepts of various accounting tools for effective decision making. Concepts will be explained

through the numerical examples in the report.

REPORT

Financial Proposal

Current Scenario of the company

Current Capital Structure €m

Issued Share Capital: 150,000,000 Ordinary Shares of 50c

each 75

Long-term debt 105

Company is currently having a capital structure of issued share capital valued at 50c that

equals to 75 million and with the debt capital of 105 million. Company is having higher of the

debt capital in comparison with the equity capital. Cost of equity of the unlevered firm is 12%

and the cost of long term debt is 4%. Company is having optimum capital structures as the

market value of shares is €1.25 each (Mulatinho and et.al., 2019).

Cost of capital is measured using Modigliani & Miller Proposition II approach with taxes

under all the three scenarios.

M&M approach is the most commonly used approach in the corporate world. It was

developed by France Modigliani & Merton Miller in the year 1985. The main idea behind the

concept is that it does not affect the overall value of the firm. The second proposition was given

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by them for the real world conditions stating that cost of equity of the firm is having directly

proportional relation with leverage level. Presence of the tax shield affect relationship through

making cost of equity less sensitive to leverage levels. Extra debts also increases the chances of

default of company, investor are less prone to the negatively reacting to company taking

additional leverages as this increases tax shields which boosts the value (Jonick and Benson,

2018).

Financial Proposal

1. Under the Existing capital structure.

WACC in the existing capital structure

WACC Amount

Market Value of Equity (E) 187.5

(150*1.25)

Market Value of Debt (D) 105

Debt after tax (D-t) 68.25

Total value of Unlevered Firm 292.5

(105 +187.5)

Return on Unlevered equity (Ro) 12%

Return on debt (Rd) 4%

Tax Rate 35%

Return On Equity (Re) 14.91%

Ro + D/E(1-t)(Ro-Rd)

Value of levered firm (VL) 255.75

(187.5+68.25)

WACC 11.63%

E/VL*Re +D/VL*Rd(1-tc)

Under the current capital structure of company it is having equity capital and debt capital

with total capital of 292.5 million. As per the M&M approach the value of levered firm is

measures after considering the tax rate. As per this approach cost of equity of calculated

considering the market value of equity on the basis of 1.25 per share and the cost of debt after

tax. The combined capital of debt and equity gives the value of levered firm. Weighted average

2

proportional relation with leverage level. Presence of the tax shield affect relationship through

making cost of equity less sensitive to leverage levels. Extra debts also increases the chances of

default of company, investor are less prone to the negatively reacting to company taking

additional leverages as this increases tax shields which boosts the value (Jonick and Benson,

2018).

Financial Proposal

1. Under the Existing capital structure.

WACC in the existing capital structure

WACC Amount

Market Value of Equity (E) 187.5

(150*1.25)

Market Value of Debt (D) 105

Debt after tax (D-t) 68.25

Total value of Unlevered Firm 292.5

(105 +187.5)

Return on Unlevered equity (Ro) 12%

Return on debt (Rd) 4%

Tax Rate 35%

Return On Equity (Re) 14.91%

Ro + D/E(1-t)(Ro-Rd)

Value of levered firm (VL) 255.75

(187.5+68.25)

WACC 11.63%

E/VL*Re +D/VL*Rd(1-tc)

Under the current capital structure of company it is having equity capital and debt capital

with total capital of 292.5 million. As per the M&M approach the value of levered firm is

measures after considering the tax rate. As per this approach cost of equity of calculated

considering the market value of equity on the basis of 1.25 per share and the cost of debt after

tax. The combined capital of debt and equity gives the value of levered firm. Weighted average

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

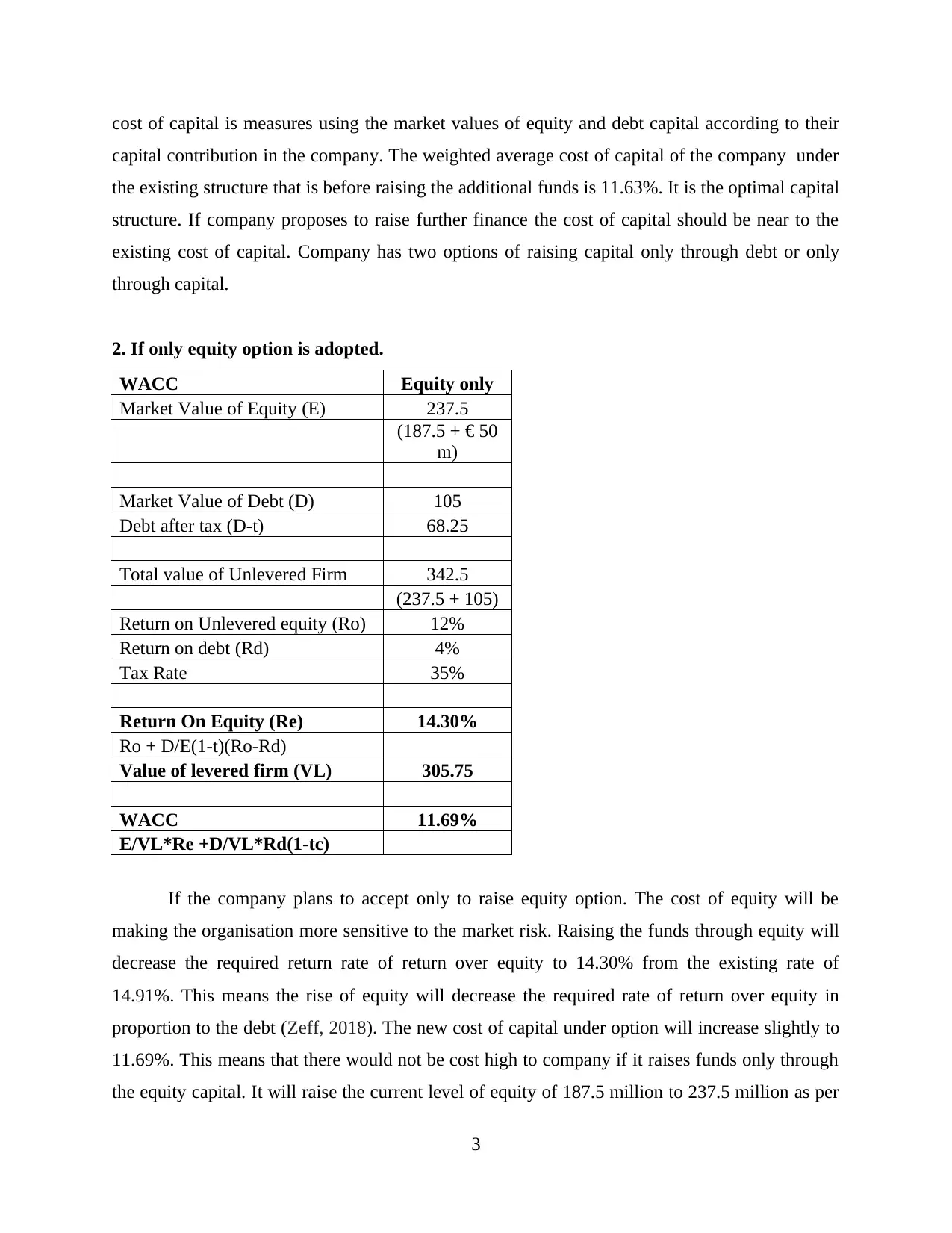

cost of capital is measures using the market values of equity and debt capital according to their

capital contribution in the company. The weighted average cost of capital of the company under

the existing structure that is before raising the additional funds is 11.63%. It is the optimal capital

structure. If company proposes to raise further finance the cost of capital should be near to the

existing cost of capital. Company has two options of raising capital only through debt or only

through capital.

2. If only equity option is adopted.

WACC Equity only

Market Value of Equity (E) 237.5

(187.5 + € 50

m)

Market Value of Debt (D) 105

Debt after tax (D-t) 68.25

Total value of Unlevered Firm 342.5

(237.5 + 105)

Return on Unlevered equity (Ro) 12%

Return on debt (Rd) 4%

Tax Rate 35%

Return On Equity (Re) 14.30%

Ro + D/E(1-t)(Ro-Rd)

Value of levered firm (VL) 305.75

WACC 11.69%

E/VL*Re +D/VL*Rd(1-tc)

If the company plans to accept only to raise equity option. The cost of equity will be

making the organisation more sensitive to the market risk. Raising the funds through equity will

decrease the required return rate of return over equity to 14.30% from the existing rate of

14.91%. This means the rise of equity will decrease the required rate of return over equity in

proportion to the debt (Zeff, 2018). The new cost of capital under option will increase slightly to

11.69%. This means that there would not be cost high to company if it raises funds only through

the equity capital. It will raise the current level of equity of 187.5 million to 237.5 million as per

3

capital contribution in the company. The weighted average cost of capital of the company under

the existing structure that is before raising the additional funds is 11.63%. It is the optimal capital

structure. If company proposes to raise further finance the cost of capital should be near to the

existing cost of capital. Company has two options of raising capital only through debt or only

through capital.

2. If only equity option is adopted.

WACC Equity only

Market Value of Equity (E) 237.5

(187.5 + € 50

m)

Market Value of Debt (D) 105

Debt after tax (D-t) 68.25

Total value of Unlevered Firm 342.5

(237.5 + 105)

Return on Unlevered equity (Ro) 12%

Return on debt (Rd) 4%

Tax Rate 35%

Return On Equity (Re) 14.30%

Ro + D/E(1-t)(Ro-Rd)

Value of levered firm (VL) 305.75

WACC 11.69%

E/VL*Re +D/VL*Rd(1-tc)

If the company plans to accept only to raise equity option. The cost of equity will be

making the organisation more sensitive to the market risk. Raising the funds through equity will

decrease the required return rate of return over equity to 14.30% from the existing rate of

14.91%. This means the rise of equity will decrease the required rate of return over equity in

proportion to the debt (Zeff, 2018). The new cost of capital under option will increase slightly to

11.69%. This means that there would not be cost high to company if it raises funds only through

the equity capital. It will raise the current level of equity of 187.5 million to 237.5 million as per

3

the market value of equity shares. Cost of market debt is unchanged under this option. Under this

option company will not be available with any of the extra tax benefits as in case of debt capital.

3. If only debt capital is adopted.

WACC Debt only

Market Value of Equity (E) 187.5

(150*1.25)

Market Value of Debt (D) 155

Debt after tax (D-t) 100.75

Total value of Unlevered Firm 342.5

(187.5 + 155)

Return on Unlevered equity (Ro) 12%

Return on debt (Rd) 4%

Tax Rate 35%

Return On Equity (Re) 16.30%

Ro + D/E(1-t)(Ro-Rd)

Value of levered firm (VL) 288.25

WACC 11.51%

E/VL*Re +D/VL*Rd(1-tc)

If company plans to raise funds only using debt capital for the proposed financial plan it

will have the following implications. Company usually adopts the debt option for raisig funds as

the cost of debt is lower than the cost of equity. Also using the debt option company is available

with the tax shields as specified under the M&M approach. However raising funds only through

the debt option can also be harmful for the company. If company uses this option the prposed

required rate of return on equity will rise to 16.31% from the existing rate of 14.91%. the rise is

seen due to the proportional increase in debt capital as it reduces the cost of capital due to the tax

benefits available with it. If company adopts this option the cost of capital of the company will

be 11.51% which is lowest under all the three scenarios. Raising funds only through debt option

will be decreasing the cost of capital but the require rate of return and financial risks associated

with the business will also rise.

Recommendation

4

option company will not be available with any of the extra tax benefits as in case of debt capital.

3. If only debt capital is adopted.

WACC Debt only

Market Value of Equity (E) 187.5

(150*1.25)

Market Value of Debt (D) 155

Debt after tax (D-t) 100.75

Total value of Unlevered Firm 342.5

(187.5 + 155)

Return on Unlevered equity (Ro) 12%

Return on debt (Rd) 4%

Tax Rate 35%

Return On Equity (Re) 16.30%

Ro + D/E(1-t)(Ro-Rd)

Value of levered firm (VL) 288.25

WACC 11.51%

E/VL*Re +D/VL*Rd(1-tc)

If company plans to raise funds only using debt capital for the proposed financial plan it

will have the following implications. Company usually adopts the debt option for raisig funds as

the cost of debt is lower than the cost of equity. Also using the debt option company is available

with the tax shields as specified under the M&M approach. However raising funds only through

the debt option can also be harmful for the company. If company uses this option the prposed

required rate of return on equity will rise to 16.31% from the existing rate of 14.91%. the rise is

seen due to the proportional increase in debt capital as it reduces the cost of capital due to the tax

benefits available with it. If company adopts this option the cost of capital of the company will

be 11.51% which is lowest under all the three scenarios. Raising funds only through debt option

will be decreasing the cost of capital but the require rate of return and financial risks associated

with the business will also rise.

Recommendation

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Under the current capital structure company is having the cost of capital of 11.63%. From

the option of only debt or only equity it will be having the lowest cost of capital under debt.

Under the MM approach the cost of equity will decrease in equity option. While in the debt

option cost of equity will rise to 16.30%. Though the option of debt appears to be more

beneficial due to its lower cost of capital. But at the same it will also be raising the required rate

of return over equity also. The financial risks will also raise drawing the profitability and aspect

of growth down (Allen, Ramanna, and Roychowdhury, 2018) On the other equity option will be

more even when the tax benefits are not available. Required rate of return is decreased due to the

share of profits in larger proportion of shareholders without bring the profitability of the

company. This will also not increase the financial risks of the business as the proportion of debt

is decreased with rise in equity capital of company.

Investment Proposal

Company is planning to produce new product Azam. The proposed investment plan

requires the business of to purchase the new machinery costing 250000 with the residual value

that will be achieved. The company is required to analyse the viability of the proposed plan of

the business.

5

the option of only debt or only equity it will be having the lowest cost of capital under debt.

Under the MM approach the cost of equity will decrease in equity option. While in the debt

option cost of equity will rise to 16.30%. Though the option of debt appears to be more

beneficial due to its lower cost of capital. But at the same it will also be raising the required rate

of return over equity also. The financial risks will also raise drawing the profitability and aspect

of growth down (Allen, Ramanna, and Roychowdhury, 2018) On the other equity option will be

more even when the tax benefits are not available. Required rate of return is decreased due to the

share of profits in larger proportion of shareholders without bring the profitability of the

company. This will also not increase the financial risks of the business as the proportion of debt

is decreased with rise in equity capital of company.

Investment Proposal

Company is planning to produce new product Azam. The proposed investment plan

requires the business of to purchase the new machinery costing 250000 with the residual value

that will be achieved. The company is required to analyse the viability of the proposed plan of

the business.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

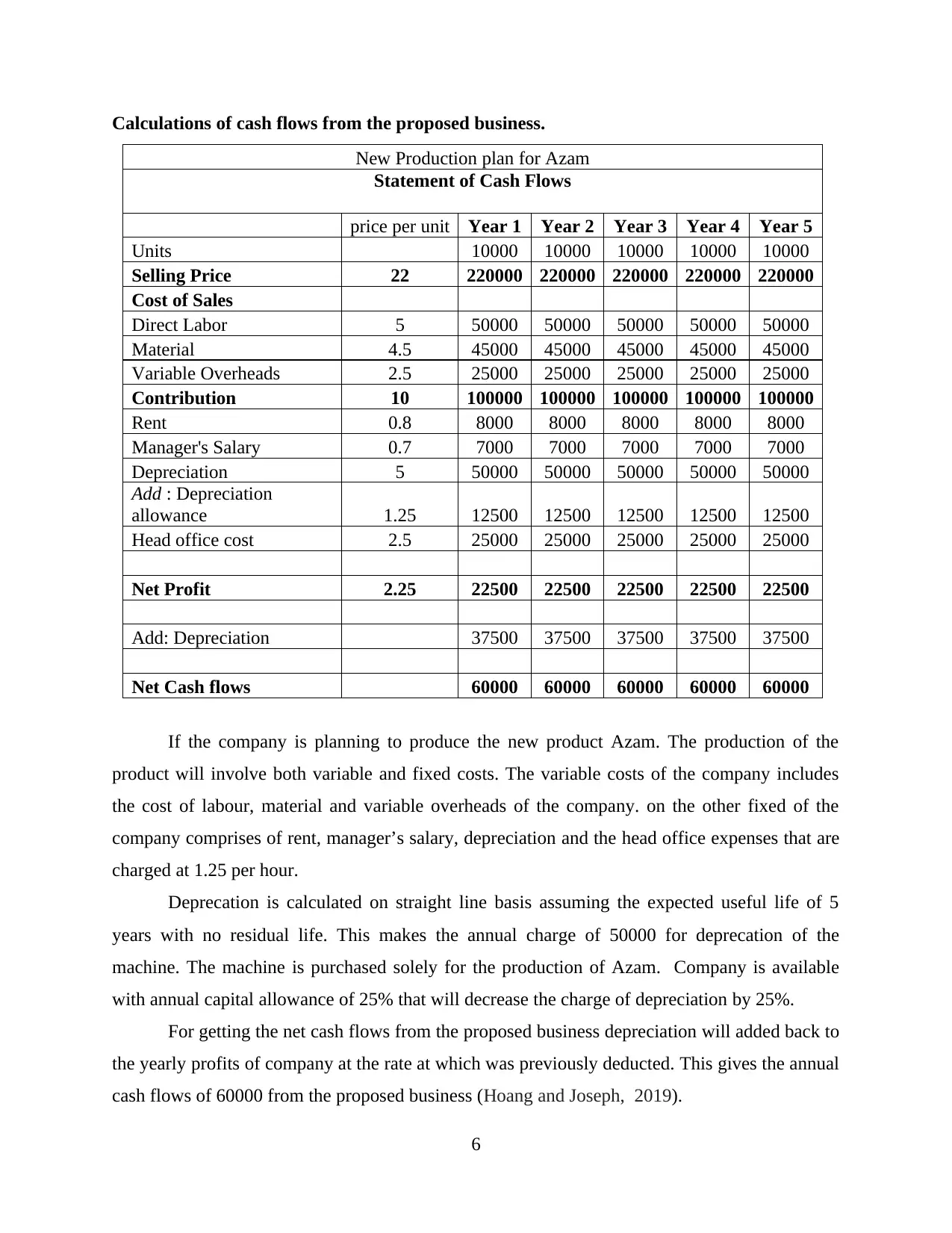

Calculations of cash flows from the proposed business.

New Production plan for Azam

Statement of Cash Flows

price per unit Year 1 Year 2 Year 3 Year 4 Year 5

Units 10000 10000 10000 10000 10000

Selling Price 22 220000 220000 220000 220000 220000

Cost of Sales

Direct Labor 5 50000 50000 50000 50000 50000

Material 4.5 45000 45000 45000 45000 45000

Variable Overheads 2.5 25000 25000 25000 25000 25000

Contribution 10 100000 100000 100000 100000 100000

Rent 0.8 8000 8000 8000 8000 8000

Manager's Salary 0.7 7000 7000 7000 7000 7000

Depreciation 5 50000 50000 50000 50000 50000

Add : Depreciation

allowance 1.25 12500 12500 12500 12500 12500

Head office cost 2.5 25000 25000 25000 25000 25000

Net Profit 2.25 22500 22500 22500 22500 22500

Add: Depreciation 37500 37500 37500 37500 37500

Net Cash flows 60000 60000 60000 60000 60000

If the company is planning to produce the new product Azam. The production of the

product will involve both variable and fixed costs. The variable costs of the company includes

the cost of labour, material and variable overheads of the company. on the other fixed of the

company comprises of rent, manager’s salary, depreciation and the head office expenses that are

charged at 1.25 per hour.

Deprecation is calculated on straight line basis assuming the expected useful life of 5

years with no residual life. This makes the annual charge of 50000 for deprecation of the

machine. The machine is purchased solely for the production of Azam. Company is available

with annual capital allowance of 25% that will decrease the charge of depreciation by 25%.

For getting the net cash flows from the proposed business depreciation will added back to

the yearly profits of company at the rate at which was previously deducted. This gives the annual

cash flows of 60000 from the proposed business (Hoang and Joseph, 2019).

6

New Production plan for Azam

Statement of Cash Flows

price per unit Year 1 Year 2 Year 3 Year 4 Year 5

Units 10000 10000 10000 10000 10000

Selling Price 22 220000 220000 220000 220000 220000

Cost of Sales

Direct Labor 5 50000 50000 50000 50000 50000

Material 4.5 45000 45000 45000 45000 45000

Variable Overheads 2.5 25000 25000 25000 25000 25000

Contribution 10 100000 100000 100000 100000 100000

Rent 0.8 8000 8000 8000 8000 8000

Manager's Salary 0.7 7000 7000 7000 7000 7000

Depreciation 5 50000 50000 50000 50000 50000

Add : Depreciation

allowance 1.25 12500 12500 12500 12500 12500

Head office cost 2.5 25000 25000 25000 25000 25000

Net Profit 2.25 22500 22500 22500 22500 22500

Add: Depreciation 37500 37500 37500 37500 37500

Net Cash flows 60000 60000 60000 60000 60000

If the company is planning to produce the new product Azam. The production of the

product will involve both variable and fixed costs. The variable costs of the company includes

the cost of labour, material and variable overheads of the company. on the other fixed of the

company comprises of rent, manager’s salary, depreciation and the head office expenses that are

charged at 1.25 per hour.

Deprecation is calculated on straight line basis assuming the expected useful life of 5

years with no residual life. This makes the annual charge of 50000 for deprecation of the

machine. The machine is purchased solely for the production of Azam. Company is available

with annual capital allowance of 25% that will decrease the charge of depreciation by 25%.

For getting the net cash flows from the proposed business depreciation will added back to

the yearly profits of company at the rate at which was previously deducted. This gives the annual

cash flows of 60000 from the proposed business (Hoang and Joseph, 2019).

6

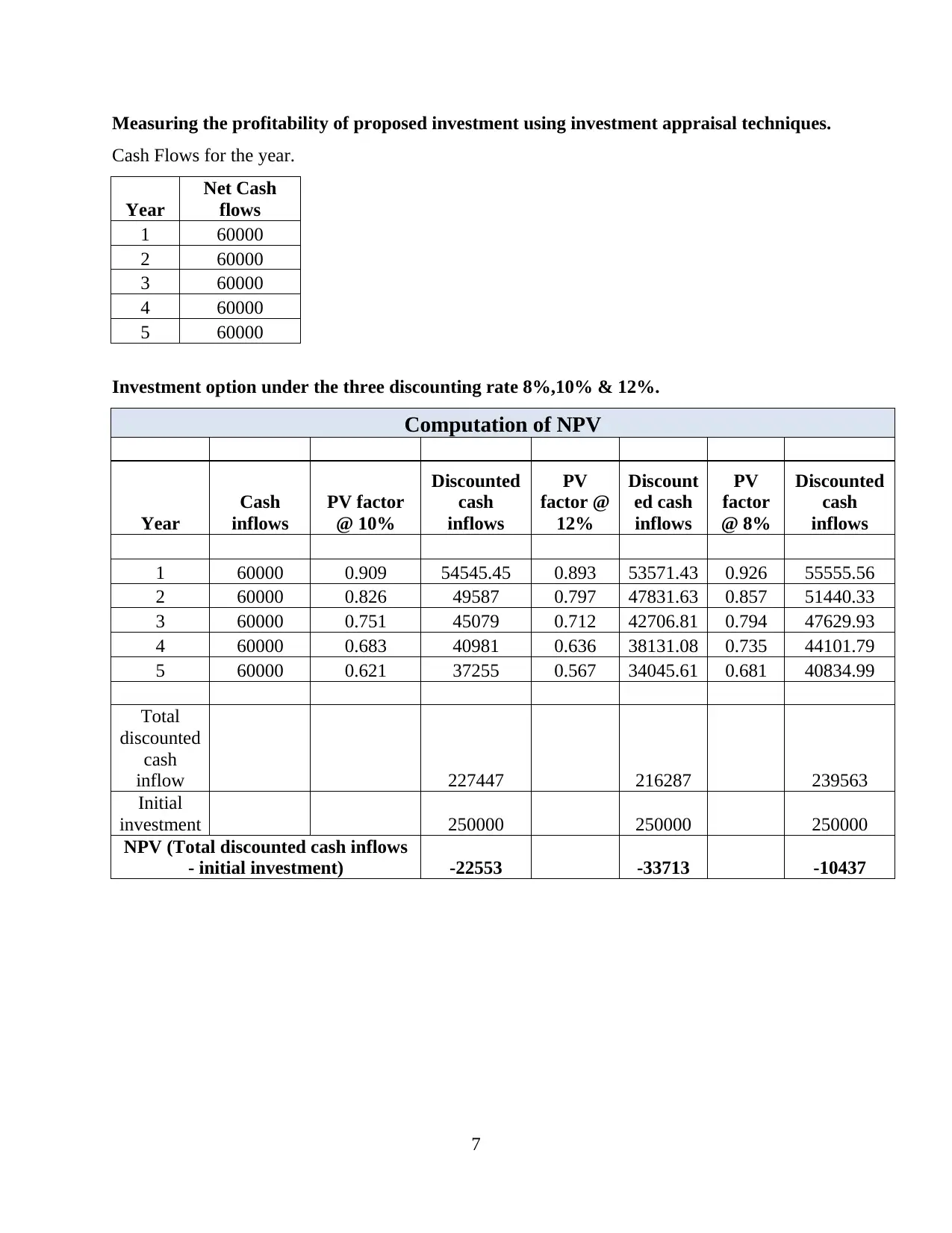

Measuring the profitability of proposed investment using investment appraisal techniques.

Cash Flows for the year.

Year

Net Cash

flows

1 60000

2 60000

3 60000

4 60000

5 60000

Investment option under the three discounting rate 8%,10% & 12%.

Computation of NPV

Year

Cash

inflows

PV factor

@ 10%

Discounted

cash

inflows

PV

factor @

12%

Discount

ed cash

inflows

PV

factor

@ 8%

Discounted

cash

inflows

1 60000 0.909 54545.45 0.893 53571.43 0.926 55555.56

2 60000 0.826 49587 0.797 47831.63 0.857 51440.33

3 60000 0.751 45079 0.712 42706.81 0.794 47629.93

4 60000 0.683 40981 0.636 38131.08 0.735 44101.79

5 60000 0.621 37255 0.567 34045.61 0.681 40834.99

Total

discounted

cash

inflow 227447 216287 239563

Initial

investment 250000 250000 250000

NPV (Total discounted cash inflows

- initial investment) -22553 -33713 -10437

7

Cash Flows for the year.

Year

Net Cash

flows

1 60000

2 60000

3 60000

4 60000

5 60000

Investment option under the three discounting rate 8%,10% & 12%.

Computation of NPV

Year

Cash

inflows

PV factor

@ 10%

Discounted

cash

inflows

PV

factor @

12%

Discount

ed cash

inflows

PV

factor

@ 8%

Discounted

cash

inflows

1 60000 0.909 54545.45 0.893 53571.43 0.926 55555.56

2 60000 0.826 49587 0.797 47831.63 0.857 51440.33

3 60000 0.751 45079 0.712 42706.81 0.794 47629.93

4 60000 0.683 40981 0.636 38131.08 0.735 44101.79

5 60000 0.621 37255 0.567 34045.61 0.681 40834.99

Total

discounted

cash

inflow 227447 216287 239563

Initial

investment 250000 250000 250000

NPV (Total discounted cash inflows

- initial investment) -22553 -33713 -10437

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

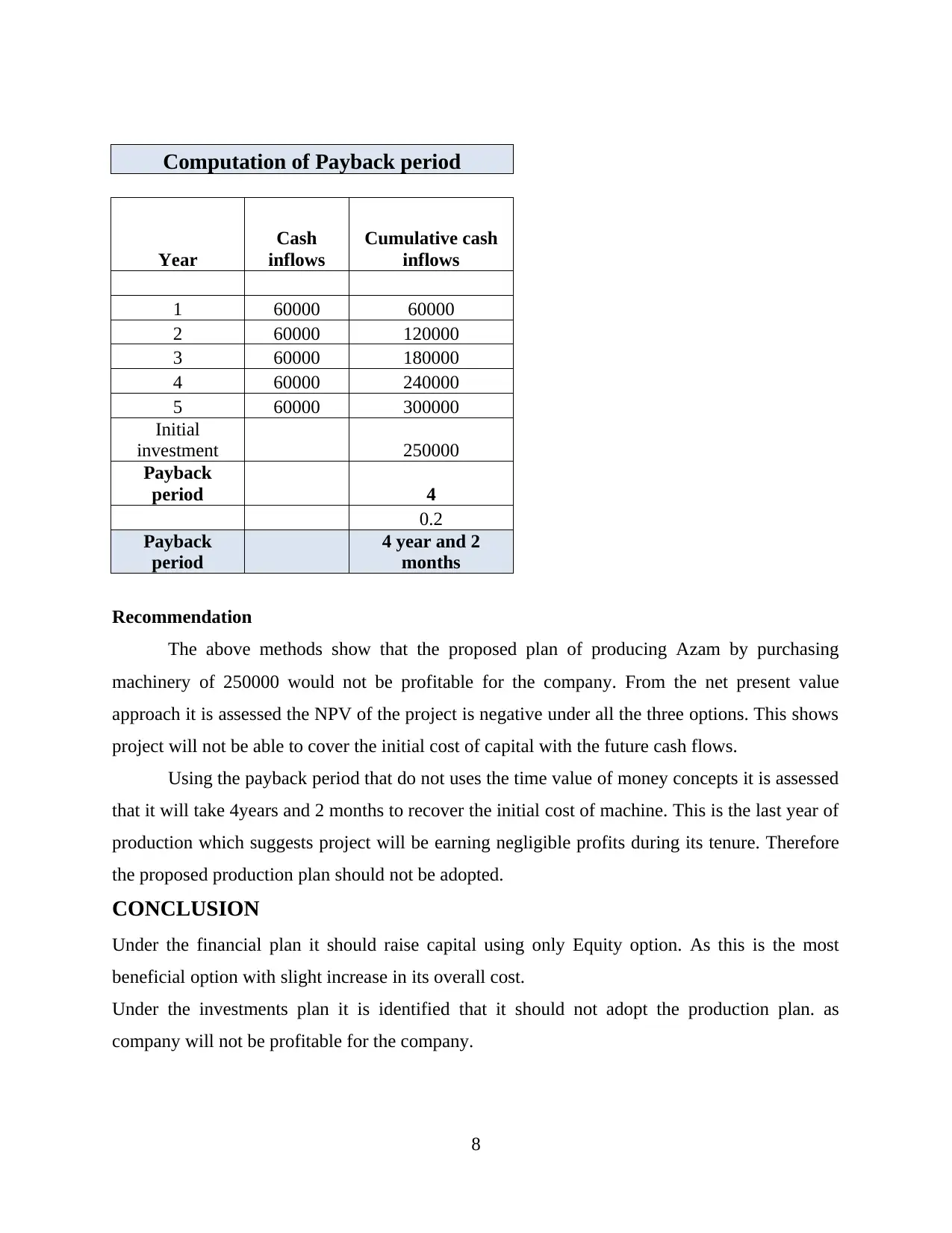

Computation of Payback period

Year

Cash

inflows

Cumulative cash

inflows

1 60000 60000

2 60000 120000

3 60000 180000

4 60000 240000

5 60000 300000

Initial

investment 250000

Payback

period 4

0.2

Payback

period

4 year and 2

months

Recommendation

The above methods show that the proposed plan of producing Azam by purchasing

machinery of 250000 would not be profitable for the company. From the net present value

approach it is assessed the NPV of the project is negative under all the three options. This shows

project will not be able to cover the initial cost of capital with the future cash flows.

Using the payback period that do not uses the time value of money concepts it is assessed

that it will take 4years and 2 months to recover the initial cost of machine. This is the last year of

production which suggests project will be earning negligible profits during its tenure. Therefore

the proposed production plan should not be adopted.

CONCLUSION

Under the financial plan it should raise capital using only Equity option. As this is the most

beneficial option with slight increase in its overall cost.

Under the investments plan it is identified that it should not adopt the production plan. as

company will not be profitable for the company.

8

Year

Cash

inflows

Cumulative cash

inflows

1 60000 60000

2 60000 120000

3 60000 180000

4 60000 240000

5 60000 300000

Initial

investment 250000

Payback

period 4

0.2

Payback

period

4 year and 2

months

Recommendation

The above methods show that the proposed plan of producing Azam by purchasing

machinery of 250000 would not be profitable for the company. From the net present value

approach it is assessed the NPV of the project is negative under all the three options. This shows

project will not be able to cover the initial cost of capital with the future cash flows.

Using the payback period that do not uses the time value of money concepts it is assessed

that it will take 4years and 2 months to recover the initial cost of machine. This is the last year of

production which suggests project will be earning negligible profits during its tenure. Therefore

the proposed production plan should not be adopted.

CONCLUSION

Under the financial plan it should raise capital using only Equity option. As this is the most

beneficial option with slight increase in its overall cost.

Under the investments plan it is identified that it should not adopt the production plan. as

company will not be profitable for the company.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Allen, A.M., Ramanna, K. and Roychowdhury, S., 2018. Auditor lobbying on accounting

standards. Journal of Law, Finance & Accounting, Forthcoming.

Zeff, S.A., 2018. An Introduction to Corporate Accounting Standards: Detecting Paton's and

Littleton's Influences. Accounting Historians Journal, 45(1), pp.45-67.

Hoang, T.C. and Joseph, D.M., 2019. The effect of new corporate accounting regime on earnings

management: Evidence from Vietnam. Journal of International Studies, 12(1), pp.93-104.

Mulatinho, C.E.S. and et.al., 2019. Convergence of Accounting Standards to International

Standards and Earnings Management in Brazilian Companies. In International Financial

Reporting Standards and New Directions in Earnings Management (pp. 256-273). IGI

Global.

Jonick, C. and Benson, D., 2018. The New Accounting Standard for Revenue Recognition: Do

Implementation Issues Differ for Fortune 500 Companies?. Journal of Corporate

Accounting & Finance, 29(2), pp.22-33.

9

Books and Journals

Allen, A.M., Ramanna, K. and Roychowdhury, S., 2018. Auditor lobbying on accounting

standards. Journal of Law, Finance & Accounting, Forthcoming.

Zeff, S.A., 2018. An Introduction to Corporate Accounting Standards: Detecting Paton's and

Littleton's Influences. Accounting Historians Journal, 45(1), pp.45-67.

Hoang, T.C. and Joseph, D.M., 2019. The effect of new corporate accounting regime on earnings

management: Evidence from Vietnam. Journal of International Studies, 12(1), pp.93-104.

Mulatinho, C.E.S. and et.al., 2019. Convergence of Accounting Standards to International

Standards and Earnings Management in Brazilian Companies. In International Financial

Reporting Standards and New Directions in Earnings Management (pp. 256-273). IGI

Global.

Jonick, C. and Benson, D., 2018. The New Accounting Standard for Revenue Recognition: Do

Implementation Issues Differ for Fortune 500 Companies?. Journal of Corporate

Accounting & Finance, 29(2), pp.22-33.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.