Corporate Finance Assignment Example

VerifiedAdded on 2021/06/16

|13

|2780

|46

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Corporate Finance

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Abstract

The tertiary industry is like nervous in our body. The economy cannot move without it. The

tertiary industry is a very large industry. It gives employment to many employees. Here in this

study, we are going to discuss the benefits retirement plan is more beneficial for the employees

of tertiary industry. All the aspects of the plans will be discussed as to give a complete

knowledge to the employees and make easy for them in choosing the best plans.

2

The tertiary industry is like nervous in our body. The economy cannot move without it. The

tertiary industry is a very large industry. It gives employment to many employees. Here in this

study, we are going to discuss the benefits retirement plan is more beneficial for the employees

of tertiary industry. All the aspects of the plans will be discussed as to give a complete

knowledge to the employees and make easy for them in choosing the best plans.

2

Contents

Abstract............................................................................................................................................2

Introduction......................................................................................................................................4

Investment choice plan....................................................................................................................6

Understand the fund.................................................................................................................6

Comparing the funds................................................................................................................7

Define benefit plan..........................................................................................................................7

Calculation of define benefit plan................................................................................................7

Unfunded benefit plan..................................................................................................................8

Decision making facts..................................................................................................................8

Comparison between define benefit plan and investment choice plan..........................................10

Hypothesis..................................................................................................................................11

Efficient Market.........................................................................................................................11

References......................................................................................................................................12

3

Abstract............................................................................................................................................2

Introduction......................................................................................................................................4

Investment choice plan....................................................................................................................6

Understand the fund.................................................................................................................6

Comparing the funds................................................................................................................7

Define benefit plan..........................................................................................................................7

Calculation of define benefit plan................................................................................................7

Unfunded benefit plan..................................................................................................................8

Decision making facts..................................................................................................................8

Comparison between define benefit plan and investment choice plan..........................................10

Hypothesis..................................................................................................................................11

Efficient Market.........................................................................................................................11

References......................................................................................................................................12

3

Introduction

There are three types of sectors prevailing in the economy the primary sector - raw materials,

secondary sector- manufacturing, and the third sector - tertiary sectors. With the time the

proportion of employees to work in tertiary sector is increasing. In this assignment, the

discussion is related to retirement schemes or retirement plans has been made. This discussion

has been made for the benefit of an employee looking for better retirement plans i.e. after

comparing various retirement plans. In this report, some important factors have been discussed

for the tertiary sector employees for the selection of better plan superannuation plan. Comparison

of a defined benefit plan and investment choice plan has been considered. There are some issues

or some considerations related to the decision-making process that should be considered while

selecting the best plan.

4

There are three types of sectors prevailing in the economy the primary sector - raw materials,

secondary sector- manufacturing, and the third sector - tertiary sectors. With the time the

proportion of employees to work in tertiary sector is increasing. In this assignment, the

discussion is related to retirement schemes or retirement plans has been made. This discussion

has been made for the benefit of an employee looking for better retirement plans i.e. after

comparing various retirement plans. In this report, some important factors have been discussed

for the tertiary sector employees for the selection of better plan superannuation plan. Comparison

of a defined benefit plan and investment choice plan has been considered. There are some issues

or some considerations related to the decision-making process that should be considered while

selecting the best plan.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

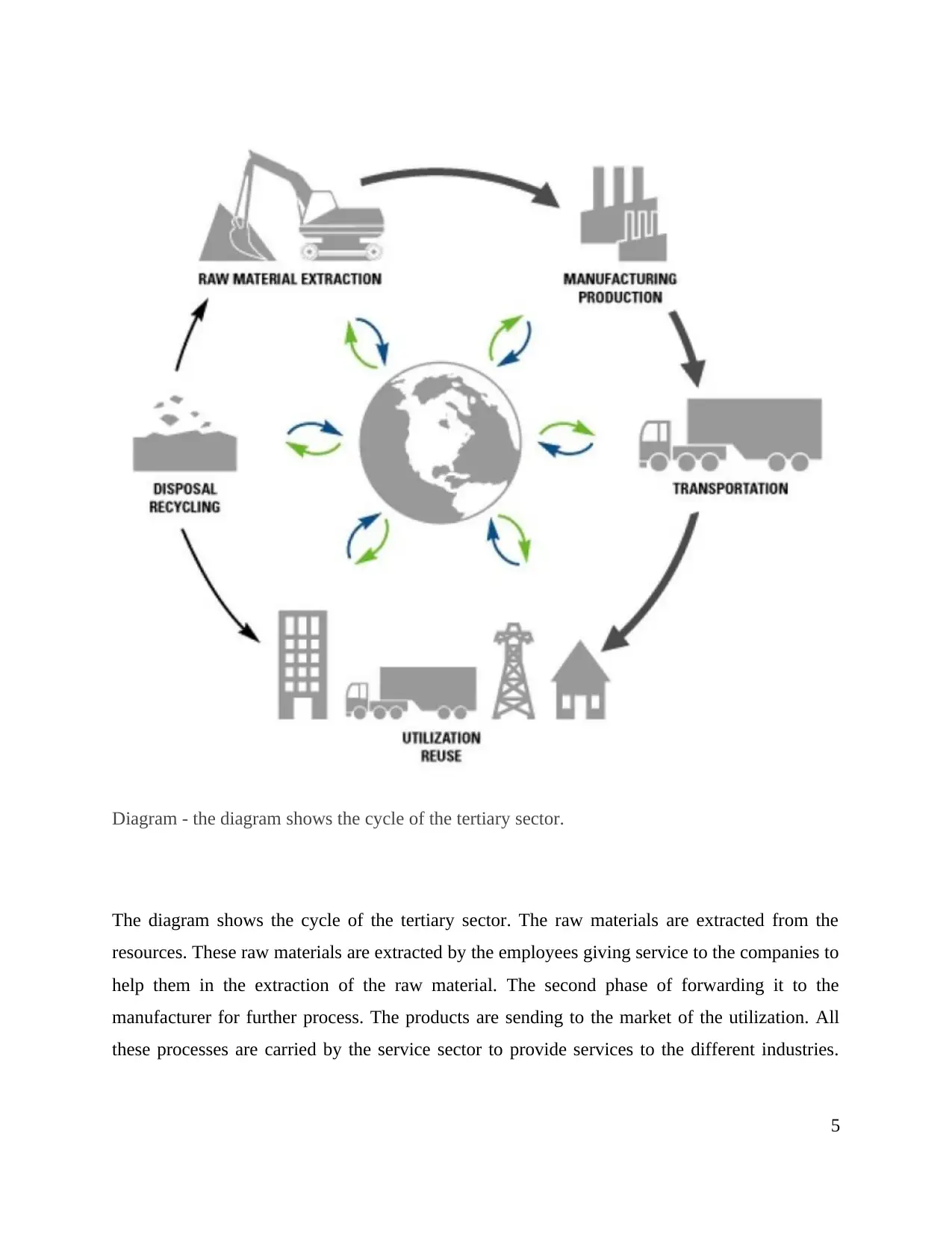

Diagram - the diagram shows the cycle of the tertiary sector.

The diagram shows the cycle of the tertiary sector. The raw materials are extracted from the

resources. These raw materials are extracted by the employees giving service to the companies to

help them in the extraction of the raw material. The second phase of forwarding it to the

manufacturer for further process. The products are sending to the market of the utilization. All

these processes are carried by the service sector to provide services to the different industries.

5

The diagram shows the cycle of the tertiary sector. The raw materials are extracted from the

resources. These raw materials are extracted by the employees giving service to the companies to

help them in the extraction of the raw material. The second phase of forwarding it to the

manufacturer for further process. The products are sending to the market of the utilization. All

these processes are carried by the service sector to provide services to the different industries.

5

These tertiary sectors are very important for the moving of the services. If at any point they are a

lack of the services than the chain breaks and the further process is hindered.

The employees working in the tertiary sector have all the rights to choose and to invest their

superannuation as per there wish. The employees cannot invest the superannuation as per his

wish. The superannuation or the retirement fund or the pension fund is the last remuneration

received by the employees from their company as full and final. Employees have two options to

select the plan to invest their superannuation for retirement. The defined benefit plan and the

investment choice plan. The detail benefits and the drawback of the process to invest is explained

an asunder.

Investment choice plan

Retirement planning is to plan and determine the income and what lifestyle one wants to live and

to put into action the planning done to achieve the goals. As early the employees start saving for

their future and make an investment in the mutual funds, stocks, and employer-sponsored plans

or any other way of investment for long period the more the money will grow. The investment

choice plan is the market-based plan. In which the employees invest their money in the shares,

mutual funds, and other market-related plans. The returns are very good and no fixed amount to

can define at the initial stage. An estimate of profits can be made and with the past performance

of the fund.

Which fund to choose is a very important decision as it will hold all the income of the employees

and the future plans? The employees have options such as balanced fund, growth funds, and

conservative funds. In this study, we have discussed in detail the steps to be followed to

determine before finalizing any fund.

Understand the fund

To invest in any fund the employees should first understand the fund. The performance of the

fund in the past years should be studied. In what market position the funds are in profit and when

the market sinks. These studies give a data of time to invest in a particular fund.

6

lack of the services than the chain breaks and the further process is hindered.

The employees working in the tertiary sector have all the rights to choose and to invest their

superannuation as per there wish. The employees cannot invest the superannuation as per his

wish. The superannuation or the retirement fund or the pension fund is the last remuneration

received by the employees from their company as full and final. Employees have two options to

select the plan to invest their superannuation for retirement. The defined benefit plan and the

investment choice plan. The detail benefits and the drawback of the process to invest is explained

an asunder.

Investment choice plan

Retirement planning is to plan and determine the income and what lifestyle one wants to live and

to put into action the planning done to achieve the goals. As early the employees start saving for

their future and make an investment in the mutual funds, stocks, and employer-sponsored plans

or any other way of investment for long period the more the money will grow. The investment

choice plan is the market-based plan. In which the employees invest their money in the shares,

mutual funds, and other market-related plans. The returns are very good and no fixed amount to

can define at the initial stage. An estimate of profits can be made and with the past performance

of the fund.

Which fund to choose is a very important decision as it will hold all the income of the employees

and the future plans? The employees have options such as balanced fund, growth funds, and

conservative funds. In this study, we have discussed in detail the steps to be followed to

determine before finalizing any fund.

Understand the fund

To invest in any fund the employees should first understand the fund. The performance of the

fund in the past years should be studied. In what market position the funds are in profit and when

the market sinks. These studies give a data of time to invest in a particular fund.

6

Comparing the funds

The employees should compare the funds and do a deep study of the plans should be done. In

how much time the funds will give returns? What is the rate of growth? All these facts should be

compared to get the best fund as per employee’s requirement.

Define benefit plan

The most common and easy word introduction of a defined benefit plan is final salary. This

scheme provides the employees with a particular leave of benefit related to years they have

worked and how much salary they drew in their service years in one company. To calculate the

defined benefit plan is linked to the employee's income/ and the no of years he has given his

services. The employer also contributes to the ratio of employee’s services time and income. The

managers who regulate the define benefit plan make it confirm that both the parties the

employees and the employer have made their contributions. The defined benefit plan is safe as it

is not a market linked plan. The need for the employees at the time of retirement is the base that

the employees decide at the initial time of the plan. This desires amount is then calculated as per

the current income and the no of the year left in retirement. The amount which will be received

at the time of retirement is pre-decided. The premium or contribution is done according to that.

The defined benefit plan also includes a pension for the employees. The number of years the

employees will get the pension is also fixed. Another variable is that it represents the amount

which is received at the time of retirement. When the scheme will end that time also the

employees will get some amount other than the fixed amount this part is Accrual rate.

Calculation of defined benefit plan

Number of years employees worked in a company * salary of the employee at the time of

retirement * accrual rate

The formula to calculate the defined benefit plan is fix. This includes the number of years

worked by the employees in the tertiary sector, his salary and the accrual rate of interest. Some

7

The employees should compare the funds and do a deep study of the plans should be done. In

how much time the funds will give returns? What is the rate of growth? All these facts should be

compared to get the best fund as per employee’s requirement.

Define benefit plan

The most common and easy word introduction of a defined benefit plan is final salary. This

scheme provides the employees with a particular leave of benefit related to years they have

worked and how much salary they drew in their service years in one company. To calculate the

defined benefit plan is linked to the employee's income/ and the no of years he has given his

services. The employer also contributes to the ratio of employee’s services time and income. The

managers who regulate the define benefit plan make it confirm that both the parties the

employees and the employer have made their contributions. The defined benefit plan is safe as it

is not a market linked plan. The need for the employees at the time of retirement is the base that

the employees decide at the initial time of the plan. This desires amount is then calculated as per

the current income and the no of the year left in retirement. The amount which will be received

at the time of retirement is pre-decided. The premium or contribution is done according to that.

The defined benefit plan also includes a pension for the employees. The number of years the

employees will get the pension is also fixed. Another variable is that it represents the amount

which is received at the time of retirement. When the scheme will end that time also the

employees will get some amount other than the fixed amount this part is Accrual rate.

Calculation of defined benefit plan

Number of years employees worked in a company * salary of the employee at the time of

retirement * accrual rate

The formula to calculate the defined benefit plan is fix. This includes the number of years

worked by the employees in the tertiary sector, his salary and the accrual rate of interest. Some

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

other benefits are also received by the employees by defined benefit plan like the get various tax

benefits, a big amount is received at the maturity.

Unfunded benefit plan

Define benefit plan has two options funded and unfunded benefit plans. The unfunded benefit

plan does not include the investment done in the assets. The funded benefit plans are funds

which consider the investment in the assets. The funded benefit plans are safe as they have a

support of the assets based companies whereas the unfunded plans lack this backing. One lacking

is observed in funded benefit plan is that it sine is not paid to the employees at the retirement or

maturity of the plans as this amount is considered as Uncalculated at the beginning of the

calculation of the maturity amount.

Decision making facts

The market situation called inflation is very harmful as it increases the living cost and the

allowance also. Investments made for short period incurred great losses. The graphics description

shows a dip at a great volume. Such market situation is not affected in the long term. The

investment in defined benefit plan is done for the long term, as a rest of which the effect of

inflation is not seen in these plans. The defined benefit plan is not market linked; whatever be the

market conditions these plans are safe. The investment of these plans is done in secure funds,

which have great support. Define benefit plans are therefore safe to invest. The fluctuation in the

market does not affect the amount invested and amount of maturity.

The amount to be received on maturity or retirement is decided by the employees as per there

future requirements. If a higher amount is desired by an employee in future then they need to

save more in current time in terms of the benefit plan.

Time is the most important factor to decide the fund. The growth of the money depends on the

time for how much funds are invested. These funds have a life cycle to perform. Some are for

short-term and some are for long term. The short-term funds give benefits in short terms while

the long term funds need time much more time to perform.

8

benefits, a big amount is received at the maturity.

Unfunded benefit plan

Define benefit plan has two options funded and unfunded benefit plans. The unfunded benefit

plan does not include the investment done in the assets. The funded benefit plans are funds

which consider the investment in the assets. The funded benefit plans are safe as they have a

support of the assets based companies whereas the unfunded plans lack this backing. One lacking

is observed in funded benefit plan is that it sine is not paid to the employees at the retirement or

maturity of the plans as this amount is considered as Uncalculated at the beginning of the

calculation of the maturity amount.

Decision making facts

The market situation called inflation is very harmful as it increases the living cost and the

allowance also. Investments made for short period incurred great losses. The graphics description

shows a dip at a great volume. Such market situation is not affected in the long term. The

investment in defined benefit plan is done for the long term, as a rest of which the effect of

inflation is not seen in these plans. The defined benefit plan is not market linked; whatever be the

market conditions these plans are safe. The investment of these plans is done in secure funds,

which have great support. Define benefit plans are therefore safe to invest. The fluctuation in the

market does not affect the amount invested and amount of maturity.

The amount to be received on maturity or retirement is decided by the employees as per there

future requirements. If a higher amount is desired by an employee in future then they need to

save more in current time in terms of the benefit plan.

Time is the most important factor to decide the fund. The growth of the money depends on the

time for how much funds are invested. These funds have a life cycle to perform. Some are for

short-term and some are for long term. The short-term funds give benefits in short terms while

the long term funds need time much more time to perform.

8

Taxes are another important factor that should be considered by the territory sector employee

while selecting best superannuation or retirement plan. Taxes are compulsory to be paid over the

income generated by the employee on any investment. In case of investment choice plan, tax

expense for the employee will be higher ass compared to the defined benefit plan. On the other

hand, if the defined benefit plan is matured before the set period of time i.e. lock-in period then

there will be tax expense on the same. Therefore tertiary sector employee needs to consider tax

expense issue while selecting superannuation plan.

9

while selecting best superannuation or retirement plan. Taxes are compulsory to be paid over the

income generated by the employee on any investment. In case of investment choice plan, tax

expense for the employee will be higher ass compared to the defined benefit plan. On the other

hand, if the defined benefit plan is matured before the set period of time i.e. lock-in period then

there will be tax expense on the same. Therefore tertiary sector employee needs to consider tax

expense issue while selecting superannuation plan.

9

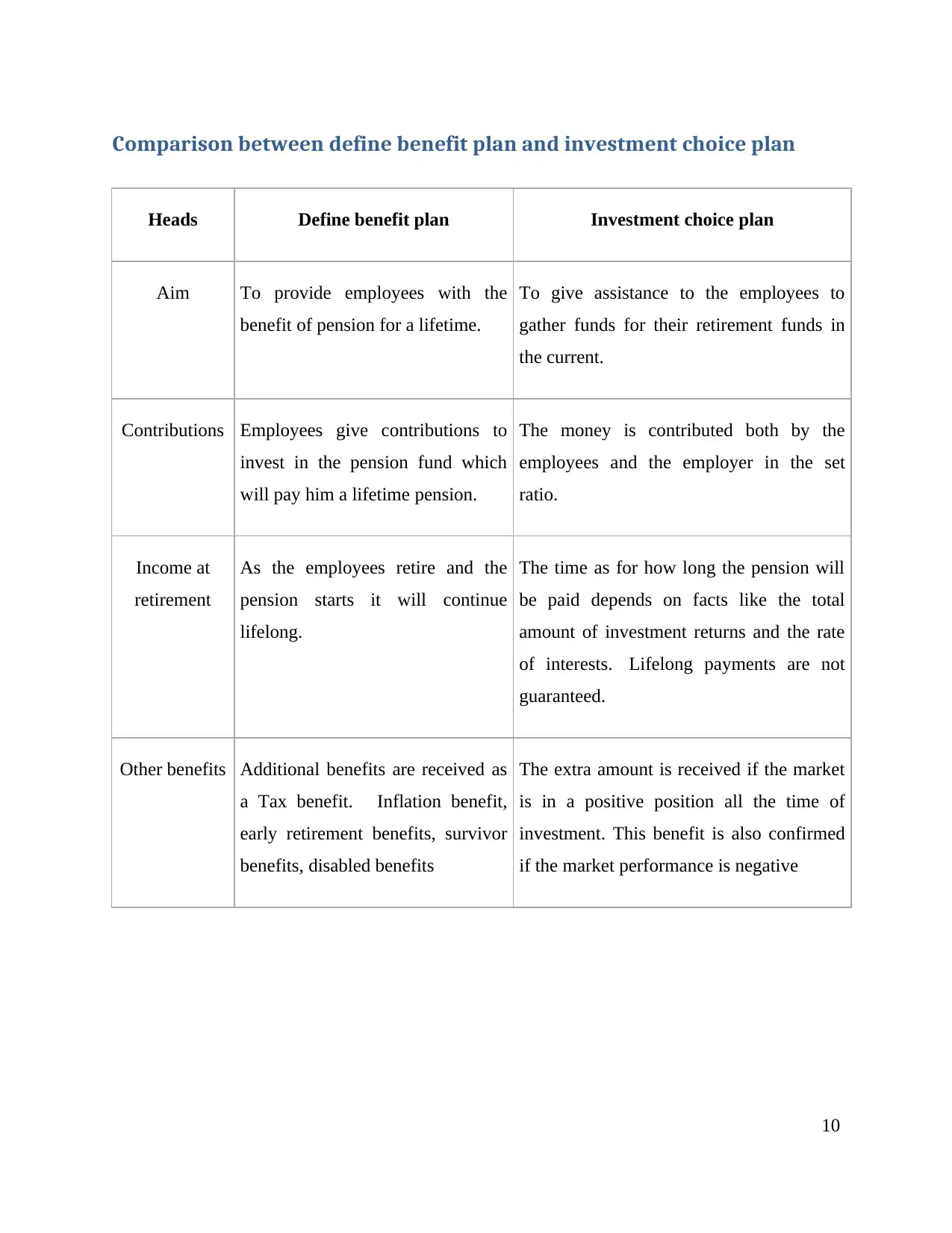

Comparison between define benefit plan and investment choice plan

Heads Define benefit plan Investment choice plan

Aim To provide employees with the

benefit of pension for a lifetime.

To give assistance to the employees to

gather funds for their retirement funds in

the current.

Contributions Employees give contributions to

invest in the pension fund which

will pay him a lifetime pension.

The money is contributed both by the

employees and the employer in the set

ratio.

Income at

retirement

As the employees retire and the

pension starts it will continue

lifelong.

The time as for how long the pension will

be paid depends on facts like the total

amount of investment returns and the rate

of interests. Lifelong payments are not

guaranteed.

Other benefits Additional benefits are received as

a Tax benefit. Inflation benefit,

early retirement benefits, survivor

benefits, disabled benefits

The extra amount is received if the market

is in a positive position all the time of

investment. This benefit is also confirmed

if the market performance is negative

10

Heads Define benefit plan Investment choice plan

Aim To provide employees with the

benefit of pension for a lifetime.

To give assistance to the employees to

gather funds for their retirement funds in

the current.

Contributions Employees give contributions to

invest in the pension fund which

will pay him a lifetime pension.

The money is contributed both by the

employees and the employer in the set

ratio.

Income at

retirement

As the employees retire and the

pension starts it will continue

lifelong.

The time as for how long the pension will

be paid depends on facts like the total

amount of investment returns and the rate

of interests. Lifelong payments are not

guaranteed.

Other benefits Additional benefits are received as

a Tax benefit. Inflation benefit,

early retirement benefits, survivor

benefits, disabled benefits

The extra amount is received if the market

is in a positive position all the time of

investment. This benefit is also confirmed

if the market performance is negative

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Hypothesis

Efficient Market

The efficient market is the market which processes the information efficiently. A quick and

correct adjustment of new information is done in the effective market. The information related to

prices of any fund is correctly evaluation of all the information available in present time. That’s

the reasons in the efficient market provided information is full a reflection of the available data.

A market in which the market price of the securities is unbiased estimates of the intrinsic value

of the securities- Wilfred O’Brien.

In the Efficient Market, the pension fund manager does not play an important role. As all the

decision is made on the current situations of the company, as a result, the decision can be made

by the individuals themselves. In this situation, there is no need for the pension fund

manager. The role of the pension fund manager is hampered in the efficient market. The

employees do not need the old data and records they do not compare or study the past

performance of the fund in the market. Which time of the market is good for investment or which

sector benefit only studied? The data with the pension fund manager are not used as the current

prices are used for the investment. In such market, the individuals are in a situation to invest and

take a decision regarding the funds. No file of old records are required and no study is to be

made for the investment by the pension fund manager, he need not update himself and take pains

to collect the current information for various funds. The fund's manager just has to perform the

duties to fill the form and put the amount as per the wish of the customer.

In reality, no such market prevails, no funds are invested just on the current prices. A complete

study is done and the comparison is done between various funds of for different time and tenure.

Every individual needs the help of the pension fund manager to manager and gives relevant

information to the customers. This hypothesis of an efficient market is not practical and does not

prevail in the real market. No funds are invested in only there price bases.

11

Efficient Market

The efficient market is the market which processes the information efficiently. A quick and

correct adjustment of new information is done in the effective market. The information related to

prices of any fund is correctly evaluation of all the information available in present time. That’s

the reasons in the efficient market provided information is full a reflection of the available data.

A market in which the market price of the securities is unbiased estimates of the intrinsic value

of the securities- Wilfred O’Brien.

In the Efficient Market, the pension fund manager does not play an important role. As all the

decision is made on the current situations of the company, as a result, the decision can be made

by the individuals themselves. In this situation, there is no need for the pension fund

manager. The role of the pension fund manager is hampered in the efficient market. The

employees do not need the old data and records they do not compare or study the past

performance of the fund in the market. Which time of the market is good for investment or which

sector benefit only studied? The data with the pension fund manager are not used as the current

prices are used for the investment. In such market, the individuals are in a situation to invest and

take a decision regarding the funds. No file of old records are required and no study is to be

made for the investment by the pension fund manager, he need not update himself and take pains

to collect the current information for various funds. The fund's manager just has to perform the

duties to fill the form and put the amount as per the wish of the customer.

In reality, no such market prevails, no funds are invested just on the current prices. A complete

study is done and the comparison is done between various funds of for different time and tenure.

Every individual needs the help of the pension fund manager to manager and gives relevant

information to the customers. This hypothesis of an efficient market is not practical and does not

prevail in the real market. No funds are invested in only there price bases.

11

References

Anon, 2012. Defined-benefit plan inside a 401(k). Best's Review, 113(1), p.51.

Anon, 2012. Mip strategy offers a choice combination.(maximum investment plan)(Column).

Money Marketing, p.50.

Anon, 2015. Multiemployer defined benefit plan demographics in 2012. Pension Benefits, 24(8),

p.12.

Anonymous, 2011. How Does Your Retirement Plan Stack Up?-2011. Pension Benefits, 20(11),

pp.3–4.

Auster, Rolf, 2005. Qualified plans, income taxes, and investment choice. The Journal of

Pension Planning & Compliance, 31(3), pp.87–93.

Campbell, J. & Schwartz, W., 2011. Defined Benefit Plan Headache: Rule Changes Boost

Volatility of Pension Cash Flow. The Journal of Corporate Accounting & Finance, 23(1), pp.47–

57.

Campbell, J., & Schwartz, W. (2011). Defined Benefit Plan Headache: Rule Changes Boost

Volatility of Pension Cash Flow. The Journal of Corporate Accounting & Finance, 23(1), 47-57.

Choy, Lin & Officer, 2014. Does freezing a defined benefit pension plan affect firm risk?

Journal of Accounting and Economics, 57(1), pp.1–21.

Dowdell, T., Klamm, B. & Spindle, R., 2010. Predicting cash flows related to defined benefit

plan contributions. Journal of Pension Economics & Finance, 9(4), pp.505–532.

Gerrans, P. & Clark, G., 2013. Pension plan participant choice: Evidence on defined benefit and

defined contribution preferences. Journal of Pension Economics & Finance, 12(4), pp.351–378.

Kristjanpoller, W.D. & Olson, J.E., 2015. Choice of Retirement Funds in Chile: Are Chilean

Women More Risk Averse than Men? , 72(1-2), p.50.

12

Anon, 2012. Defined-benefit plan inside a 401(k). Best's Review, 113(1), p.51.

Anon, 2012. Mip strategy offers a choice combination.(maximum investment plan)(Column).

Money Marketing, p.50.

Anon, 2015. Multiemployer defined benefit plan demographics in 2012. Pension Benefits, 24(8),

p.12.

Anonymous, 2011. How Does Your Retirement Plan Stack Up?-2011. Pension Benefits, 20(11),

pp.3–4.

Auster, Rolf, 2005. Qualified plans, income taxes, and investment choice. The Journal of

Pension Planning & Compliance, 31(3), pp.87–93.

Campbell, J. & Schwartz, W., 2011. Defined Benefit Plan Headache: Rule Changes Boost

Volatility of Pension Cash Flow. The Journal of Corporate Accounting & Finance, 23(1), pp.47–

57.

Campbell, J., & Schwartz, W. (2011). Defined Benefit Plan Headache: Rule Changes Boost

Volatility of Pension Cash Flow. The Journal of Corporate Accounting & Finance, 23(1), 47-57.

Choy, Lin & Officer, 2014. Does freezing a defined benefit pension plan affect firm risk?

Journal of Accounting and Economics, 57(1), pp.1–21.

Dowdell, T., Klamm, B. & Spindle, R., 2010. Predicting cash flows related to defined benefit

plan contributions. Journal of Pension Economics & Finance, 9(4), pp.505–532.

Gerrans, P. & Clark, G., 2013. Pension plan participant choice: Evidence on defined benefit and

defined contribution preferences. Journal of Pension Economics & Finance, 12(4), pp.351–378.

Kristjanpoller, W.D. & Olson, J.E., 2015. Choice of Retirement Funds in Chile: Are Chilean

Women More Risk Averse than Men? , 72(1-2), p.50.

12

Kristjanpoller, W.D. & Olson, J.E., 2015. The effect of financial knowledge and demographic

variables on passive and active investment in Chile's pension plan. , 14(3), pp.293–314.

Maurer, Mitchell, & Rogalla. (2009). Managing contribution and capital market risk in a funded

public defined benefit plan: Impact of CVaR cost constraints. Insurance Mathematics and

Economics, 45(1), 25-34.

Mitchell, O., Utkus, S. & Yang, T., 2007. Turning Workers into Savers? Incentives, Liquidity,

and Choice in 401(k) Plan Design. National Tax Journal, 60(3), pp.469–489.

Stockton, K. (2017). Survey of defined benefit plan sponsors. Pension Benefits, 26(1), 7-8.

Webb, D.C., 2011. Pension Plan Funding, Technology Choice, and the Equity Risk Premium.

Scandinavian Journal of Economics, 113(3), pp.493–524.

13

variables on passive and active investment in Chile's pension plan. , 14(3), pp.293–314.

Maurer, Mitchell, & Rogalla. (2009). Managing contribution and capital market risk in a funded

public defined benefit plan: Impact of CVaR cost constraints. Insurance Mathematics and

Economics, 45(1), 25-34.

Mitchell, O., Utkus, S. & Yang, T., 2007. Turning Workers into Savers? Incentives, Liquidity,

and Choice in 401(k) Plan Design. National Tax Journal, 60(3), pp.469–489.

Stockton, K. (2017). Survey of defined benefit plan sponsors. Pension Benefits, 26(1), 7-8.

Webb, D.C., 2011. Pension Plan Funding, Technology Choice, and the Equity Risk Premium.

Scandinavian Journal of Economics, 113(3), pp.493–524.

13

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.