Corporate Finance Report: Capital Structure, Investment Appraisal

VerifiedAdded on 2023/01/16

|14

|3917

|46

Report

AI Summary

This report delves into various aspects of corporate finance, commencing with an exploration of capital structure, examining arguments for and against the overall cost of capital, and considering factors influencing the choice between preference shares and debentures. It then analyzes the major factors affecting the amount of debenture finance a company can raise. The report further investigates the investment process and strategy, followed by an in-depth examination of capital budgeting or investment appraisal techniques, including a computation of net present value and profitability indexes. The study emphasizes maximizing shareholder wealth through short- and long-term financial planning and strategic execution, providing a comprehensive overview of corporate finance principles.

CORPORATE FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1 Capital structure.............................................................................................................1

(a)Arguments for and against the company overall cost of capital.............................................1

(b) Factors need to be considered when making choice between preference shares and

debentures as a means of raising long term fund........................................................................2

©Major factors that influence the amount of additional debenture finance that Newham plc

will be able to raise.....................................................................................................................3

Question 2........................................................................................................................................4

a. process and the strategy of an investment...............................................................................4

b. capital budgeting or investment appraisal techniques.............................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

Question 1 Capital structure.............................................................................................................1

(a)Arguments for and against the company overall cost of capital.............................................1

(b) Factors need to be considered when making choice between preference shares and

debentures as a means of raising long term fund........................................................................2

©Major factors that influence the amount of additional debenture finance that Newham plc

will be able to raise.....................................................................................................................3

Question 2........................................................................................................................................4

a. process and the strategy of an investment...............................................................................4

b. capital budgeting or investment appraisal techniques.............................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Corporate finance referred as the division of the finance which deals with the financing,

investment decisions, structuring and the capital. It is primarily concerned to maximising wealth

of the shareholders by way of short and the long-term planning and an execution of the several

strategies. In other words, it an area of the finance which deals with the sources of the funding,

capital structure of the company, actions that the managers takes for increasing firm's value to

shareholders and an analysis or the tools for allocating the financial resources appropriately. The

current report is based on the different aspects of the corporate finance that includes evaluation

of the capital structure, investment process and the strategy. Furthermore, the study presents a

computation of the net present value and the profitability indexes with an application of an

investment appraisal techniques.

Question 1 Capital structure

(a)Arguments for and against the company overall cost of capital

Table 1Value of levered firm

Vu 3,500,000

Tc 20%

D 2,600,000

Vl 4020000

Proposition 1 (M&M 2) of MM model state that value of levered firm is always greater then

value of unlevered firm. This because firm receive tax deductions on the debt amount and due to

this reason, its value increase. It can be said that tax deductible interest payments positively

affect company cash flow and this is the main reason due to which levered firm value is always

greater then same of the unlevered firm. In the above table it can be said that value of the levered

firm is $4020000 which is very high. Hence, it can be said that debt up to certain limit benefit

business firm.

Table 2Debt equity ratio

Value Proportion

1

Corporate finance referred as the division of the finance which deals with the financing,

investment decisions, structuring and the capital. It is primarily concerned to maximising wealth

of the shareholders by way of short and the long-term planning and an execution of the several

strategies. In other words, it an area of the finance which deals with the sources of the funding,

capital structure of the company, actions that the managers takes for increasing firm's value to

shareholders and an analysis or the tools for allocating the financial resources appropriately. The

current report is based on the different aspects of the corporate finance that includes evaluation

of the capital structure, investment process and the strategy. Furthermore, the study presents a

computation of the net present value and the profitability indexes with an application of an

investment appraisal techniques.

Question 1 Capital structure

(a)Arguments for and against the company overall cost of capital

Table 1Value of levered firm

Vu 3,500,000

Tc 20%

D 2,600,000

Vl 4020000

Proposition 1 (M&M 2) of MM model state that value of levered firm is always greater then

value of unlevered firm. This because firm receive tax deductions on the debt amount and due to

this reason, its value increase. It can be said that tax deductible interest payments positively

affect company cash flow and this is the main reason due to which levered firm value is always

greater then same of the unlevered firm. In the above table it can be said that value of the levered

firm is $4020000 which is very high. Hence, it can be said that debt up to certain limit benefit

business firm.

Table 2Debt equity ratio

Value Proportion

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

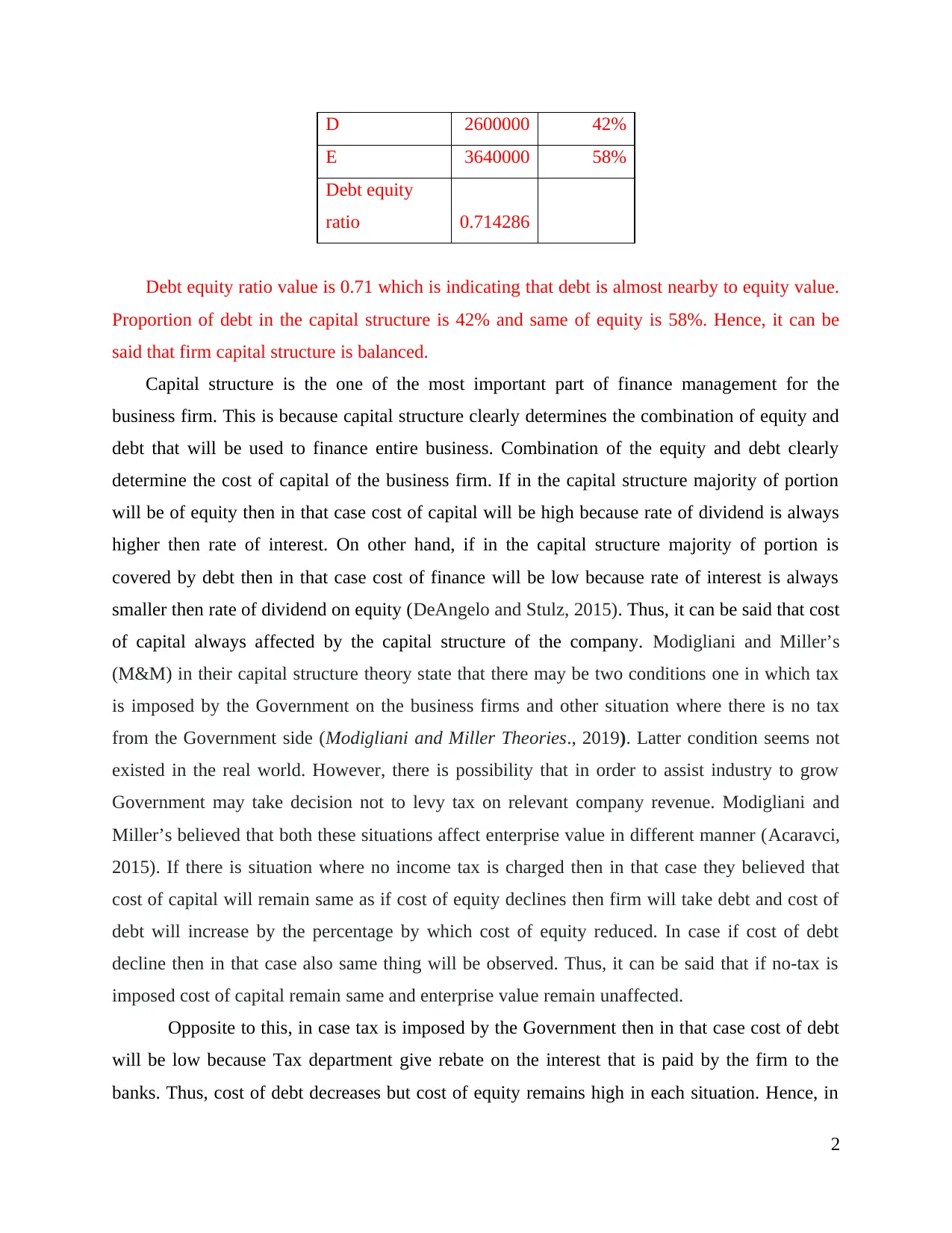

D 2600000 42%

E 3640000 58%

Debt equity

ratio 0.714286

Debt equity ratio value is 0.71 which is indicating that debt is almost nearby to equity value.

Proportion of debt in the capital structure is 42% and same of equity is 58%. Hence, it can be

said that firm capital structure is balanced.

Capital structure is the one of the most important part of finance management for the

business firm. This is because capital structure clearly determines the combination of equity and

debt that will be used to finance entire business. Combination of the equity and debt clearly

determine the cost of capital of the business firm. If in the capital structure majority of portion

will be of equity then in that case cost of capital will be high because rate of dividend is always

higher then rate of interest. On other hand, if in the capital structure majority of portion is

covered by debt then in that case cost of finance will be low because rate of interest is always

smaller then rate of dividend on equity (DeAngelo and Stulz, 2015). Thus, it can be said that cost

of capital always affected by the capital structure of the company. Modigliani and Miller’s

(M&M) in their capital structure theory state that there may be two conditions one in which tax

is imposed by the Government on the business firms and other situation where there is no tax

from the Government side (Modigliani and Miller Theories., 2019). Latter condition seems not

existed in the real world. However, there is possibility that in order to assist industry to grow

Government may take decision not to levy tax on relevant company revenue. Modigliani and

Miller’s believed that both these situations affect enterprise value in different manner (Acaravci,

2015). If there is situation where no income tax is charged then in that case they believed that

cost of capital will remain same as if cost of equity declines then firm will take debt and cost of

debt will increase by the percentage by which cost of equity reduced. In case if cost of debt

decline then in that case also same thing will be observed. Thus, it can be said that if no-tax is

imposed cost of capital remain same and enterprise value remain unaffected.

Opposite to this, in case tax is imposed by the Government then in that case cost of debt

will be low because Tax department give rebate on the interest that is paid by the firm to the

banks. Thus, cost of debt decreases but cost of equity remains high in each situation. Hence, in

2

E 3640000 58%

Debt equity

ratio 0.714286

Debt equity ratio value is 0.71 which is indicating that debt is almost nearby to equity value.

Proportion of debt in the capital structure is 42% and same of equity is 58%. Hence, it can be

said that firm capital structure is balanced.

Capital structure is the one of the most important part of finance management for the

business firm. This is because capital structure clearly determines the combination of equity and

debt that will be used to finance entire business. Combination of the equity and debt clearly

determine the cost of capital of the business firm. If in the capital structure majority of portion

will be of equity then in that case cost of capital will be high because rate of dividend is always

higher then rate of interest. On other hand, if in the capital structure majority of portion is

covered by debt then in that case cost of finance will be low because rate of interest is always

smaller then rate of dividend on equity (DeAngelo and Stulz, 2015). Thus, it can be said that cost

of capital always affected by the capital structure of the company. Modigliani and Miller’s

(M&M) in their capital structure theory state that there may be two conditions one in which tax

is imposed by the Government on the business firms and other situation where there is no tax

from the Government side (Modigliani and Miller Theories., 2019). Latter condition seems not

existed in the real world. However, there is possibility that in order to assist industry to grow

Government may take decision not to levy tax on relevant company revenue. Modigliani and

Miller’s believed that both these situations affect enterprise value in different manner (Acaravci,

2015). If there is situation where no income tax is charged then in that case they believed that

cost of capital will remain same as if cost of equity declines then firm will take debt and cost of

debt will increase by the percentage by which cost of equity reduced. In case if cost of debt

decline then in that case also same thing will be observed. Thus, it can be said that if no-tax is

imposed cost of capital remain same and enterprise value remain unaffected.

Opposite to this, in case tax is imposed by the Government then in that case cost of debt

will be low because Tax department give rebate on the interest that is paid by the firm to the

banks. Thus, cost of debt decreases but cost of equity remains high in each situation. Hence, in

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this case cost of capital can be minimized by adding more and more debt in the capital structure.

Enterprise value also increased in case tax is charged by the Government and more loan is taken

by the firm. This is because due to tax rebate less amount will be deducted from the cash inflow

amount which ultimately lead to traction in the net cash flow which means that enterprise value

will increase. Thus, it can be said that capital structure greatly affects cost of capital for the firm

and by taking more debt it can be reduced to large extent.

(b) Factors need to be considered when making choice between preference shares and debentures

as a means of raising long term fund

There are both positive and negative sides of the preference shares and debentures and it

depend on the conditions firm is facing and other factors that which source of finance firm think

is more appropriate for it. Cost of capital: Cost of capital is the one of the main factor that affect company a lot and

it become very important for the firm to ensure that it have optimum capital structure. In

case any company cost of equity is already high then it must opt for debt because if there

will be higher amount of debt then in that case cost of capital will be low. On other hand,

if there is situation where in the capital structure majority of portion is cover by debt then

in that case company go for equity (Vătavu, 2015). This is because if in the capital

structure there is high amount of debt then in that case burden of debt increased on the

company. In such situation if profitability of the firm is low then in that case burden

further increase. Thus, in such kind of scenario it is better for the firm to issue equity in

the market because by doing so burden of interest payment can be reduced. Necessity of payment: In case of debt it become necessary for the firm to pay interest

amount to the banks or bond holders or debenture holders irrespective of the company

profitability. If firm is already earning less profit then in that case further payment of debt

will affect its business performance. Such kind of thing is not observed in case of equity

as it depends on the company whether it feel appropriate to pay dividend to the

shareholders in the particular year (Faccio and Xu, 2015). Thus, in terms of payment of

cost of finance there is flexibility in case of equity and if proportion of preferred stock is

less in equity then company can go for it. Current capital structure: State of the current capital structure greatly affect choice of

equity and debt. If in the capital structure debt have 70% share then firm must go for

3

Enterprise value also increased in case tax is charged by the Government and more loan is taken

by the firm. This is because due to tax rebate less amount will be deducted from the cash inflow

amount which ultimately lead to traction in the net cash flow which means that enterprise value

will increase. Thus, it can be said that capital structure greatly affects cost of capital for the firm

and by taking more debt it can be reduced to large extent.

(b) Factors need to be considered when making choice between preference shares and debentures

as a means of raising long term fund

There are both positive and negative sides of the preference shares and debentures and it

depend on the conditions firm is facing and other factors that which source of finance firm think

is more appropriate for it. Cost of capital: Cost of capital is the one of the main factor that affect company a lot and

it become very important for the firm to ensure that it have optimum capital structure. In

case any company cost of equity is already high then it must opt for debt because if there

will be higher amount of debt then in that case cost of capital will be low. On other hand,

if there is situation where in the capital structure majority of portion is cover by debt then

in that case company go for equity (Vătavu, 2015). This is because if in the capital

structure there is high amount of debt then in that case burden of debt increased on the

company. In such situation if profitability of the firm is low then in that case burden

further increase. Thus, in such kind of scenario it is better for the firm to issue equity in

the market because by doing so burden of interest payment can be reduced. Necessity of payment: In case of debt it become necessary for the firm to pay interest

amount to the banks or bond holders or debenture holders irrespective of the company

profitability. If firm is already earning less profit then in that case further payment of debt

will affect its business performance. Such kind of thing is not observed in case of equity

as it depends on the company whether it feel appropriate to pay dividend to the

shareholders in the particular year (Faccio and Xu, 2015). Thus, in terms of payment of

cost of finance there is flexibility in case of equity and if proportion of preferred stock is

less in equity then company can go for it. Current capital structure: State of the current capital structure greatly affect choice of

equity and debt. If in the capital structure debt have 70% share then firm must go for

3

equity so that interest burden can be reduced. On other hand, portion of equity in the

capital structure is 70% then in that case firm must take debt from the market so that

capital structure can be balanced and cost of equity can be minimized. Economic conditions: Economic conditions of the nation greatly affect business firm. If

the global economy and domestic economy is in recession then in that case people make

less investment. Hence, in that situation if IPO or FPO is launched by the business firms

less shares are subscribed and firm receive less amount of capital they intend to receive.

Thus, in such kind of situation it become better for the firm to issue debentures. However,

in such situation if firm interest payment capability is not strong then in that case it must

go for preferred stock.

©Major factors that influence the amount of additional debenture finance that Newham plc will

be able to raise

In case Newham PLC already have debt in the capital structure it is very important to take

into account number of factors to decide whether firm must further take debt from the market.

Further taking debt through debenture may prove risky for the firm and may create extra burden

on it Current interest payment liability: In case Newham already have very high amount of

interest payment liability then in that case it must abstain from further issue of debenture

(Pindado, Requejo and de La Torre, 2015). This is because issue of debenture will

increase interest payment liability which may prove dangerous for the company. If

interest payment liability is less then in that case firm can Newham can think about

further issue of debenture in the market. Debt burden: Current debt burden must also be taken into consideration by the

mentioned business firm. In case debt burden is already high then in that case it may not

be wise decision to further issue debenture in the market. Thus, consideration of the

existing debt burden is very important while firm is thinking about financing its business

through debt. Economic conditions: Economic condition of the nation greatly affect firm’s financial

conditions. Not only firm people economic condition also severely gets affected due to

economic condition of the nation (Allen, Carletti and Marquez, 2015). In such scenario

4

capital structure is 70% then in that case firm must take debt from the market so that

capital structure can be balanced and cost of equity can be minimized. Economic conditions: Economic conditions of the nation greatly affect business firm. If

the global economy and domestic economy is in recession then in that case people make

less investment. Hence, in that situation if IPO or FPO is launched by the business firms

less shares are subscribed and firm receive less amount of capital they intend to receive.

Thus, in such kind of situation it become better for the firm to issue debentures. However,

in such situation if firm interest payment capability is not strong then in that case it must

go for preferred stock.

©Major factors that influence the amount of additional debenture finance that Newham plc will

be able to raise

In case Newham PLC already have debt in the capital structure it is very important to take

into account number of factors to decide whether firm must further take debt from the market.

Further taking debt through debenture may prove risky for the firm and may create extra burden

on it Current interest payment liability: In case Newham already have very high amount of

interest payment liability then in that case it must abstain from further issue of debenture

(Pindado, Requejo and de La Torre, 2015). This is because issue of debenture will

increase interest payment liability which may prove dangerous for the company. If

interest payment liability is less then in that case firm can Newham can think about

further issue of debenture in the market. Debt burden: Current debt burden must also be taken into consideration by the

mentioned business firm. In case debt burden is already high then in that case it may not

be wise decision to further issue debenture in the market. Thus, consideration of the

existing debt burden is very important while firm is thinking about financing its business

through debt. Economic conditions: Economic condition of the nation greatly affect firm’s financial

conditions. Not only firm people economic condition also severely gets affected due to

economic condition of the nation (Allen, Carletti and Marquez, 2015). In such scenario

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

people often prefer to make investment in safe financial instruments like debt so that they

can receive fixed rate on interest on debt. Thus, in case of economic turmoil if firm

financially is strong it can think about further issue of debentures in the market. Industry condition: Industry condition greatly affect firm financial condition. If in

industry there are already large number of well set players then in that case it become

hard for any firm to capture market and differentiate itself from the rivals. Thus, firm can

not earn substantial amount of profit in the business. In such kind of situation further

issue of debenture prove risky for the firm.

Question 2

a. process and the strategy of an investment

Characteristics of the FM system in order to evaluate, control and monitor the

capital expenditure of the projects are as follows-

Estimating capital requirements of an enterprise- Under the system of FM, finance

manager exercise maximum care in respect of anticipating financial requirement of the company.

For doing this effectively, they make use of the long range techniques as every business

organization needs funds not for the long run purposes for an investment in the fixed assets and

also fro the short term in order to have adequate working capital. This acts as the most important

measure in properly evaluating and determining the capital expenditure accurately so that

suitable investment decisions could be taken.

Determining capital structure of firm- It relates with the proportion and the kind of the

different securities. Financial manager should decide the proportion and the kind of the several

sources of the capital after the need of the capital funds has been assessed (Warren and Jack,

2018). Under this decisions are taken relating to mix of the debt and an equity in respect of

raising the funds from several sources. This feature helps in striking out an ideal balance between

the debt and the own funds. Finalising choice in relation to sources of the finance- capital

structure that is finalised by a management decides final choice between several sources of the

finance. The most important sources are considered as the shareholders, financial institution and

the debenture holders. The final choice depends on the careful evaluation of costs and the other

conditions that are included in these sources.

5

can receive fixed rate on interest on debt. Thus, in case of economic turmoil if firm

financially is strong it can think about further issue of debentures in the market. Industry condition: Industry condition greatly affect firm financial condition. If in

industry there are already large number of well set players then in that case it become

hard for any firm to capture market and differentiate itself from the rivals. Thus, firm can

not earn substantial amount of profit in the business. In such kind of situation further

issue of debenture prove risky for the firm.

Question 2

a. process and the strategy of an investment

Characteristics of the FM system in order to evaluate, control and monitor the

capital expenditure of the projects are as follows-

Estimating capital requirements of an enterprise- Under the system of FM, finance

manager exercise maximum care in respect of anticipating financial requirement of the company.

For doing this effectively, they make use of the long range techniques as every business

organization needs funds not for the long run purposes for an investment in the fixed assets and

also fro the short term in order to have adequate working capital. This acts as the most important

measure in properly evaluating and determining the capital expenditure accurately so that

suitable investment decisions could be taken.

Determining capital structure of firm- It relates with the proportion and the kind of the

different securities. Financial manager should decide the proportion and the kind of the several

sources of the capital after the need of the capital funds has been assessed (Warren and Jack,

2018). Under this decisions are taken relating to mix of the debt and an equity in respect of

raising the funds from several sources. This feature helps in striking out an ideal balance between

the debt and the own funds. Finalising choice in relation to sources of the finance- capital

structure that is finalised by a management decides final choice between several sources of the

finance. The most important sources are considered as the shareholders, financial institution and

the debenture holders. The final choice depends on the careful evaluation of costs and the other

conditions that are included in these sources.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Deciding pattern of investing the funds- The finance manager should prudently invest

funds procured in several assets in such judicious manner for the purpose of optimising return on

an investment without the jeopardising long run survival of an entity (Schnupp and Möller,

2018). He make use of the two main techniques that is capital budgeting and the opportunity cost

analysis which guides him in finalising an investment of the long run funds through clear

assessment of the different alternatives.

Procedure that the company needs to follow for reviewing their larger capital expenditure

proposals is as follows-

Identifying projects- the first and the foremost step is generating the proposal for an

investment. There can be several reasons in taking up for an investments within the business. It

can relate with an addition of the new line of product or making expansion in the existing

business. It could relates with the proposal for wither increasing production or reducing an

output cost.

Screening and an evaluation of the project- In the next step, it includes selection of all

the correct criteria in judging desirability of the project. This matches with an objective of an

enterprise that is maximising the market value (Roy, Rudra and Prasad, 2017). In this step the

tools in relation time value of the money concept is been used for the purpose of reviewing the

proposal in an effective way. Under this, estimation regarding benefits and the cost has to be

made along with the total of the cash outflows and inflows with an uncertainties and the risk

attached with proposal need to be assessed thoroughly and an appropriate provisioning is been

done.

Selection of the project- The capital expenditure proposal is been approved on the basis

of the selection criteria and the process of screening that is been defined for each firm with

keeping in mind an objectives of an investment that is being undertaken. Once a proposal is been

finalized, different alternatives in raising and procuring the funds has to be explored by finance

team (Srithongrung, Yusuf and Kriz, 2019). This known as the capital budget in which detailed

process for the periodical reports and tracing of the proposal for lifetime required to be

streamlined in an initial phase. Final approvals are taken on the basis of market conditions,

profitability, viability and an economic constituents.

6

funds procured in several assets in such judicious manner for the purpose of optimising return on

an investment without the jeopardising long run survival of an entity (Schnupp and Möller,

2018). He make use of the two main techniques that is capital budgeting and the opportunity cost

analysis which guides him in finalising an investment of the long run funds through clear

assessment of the different alternatives.

Procedure that the company needs to follow for reviewing their larger capital expenditure

proposals is as follows-

Identifying projects- the first and the foremost step is generating the proposal for an

investment. There can be several reasons in taking up for an investments within the business. It

can relate with an addition of the new line of product or making expansion in the existing

business. It could relates with the proposal for wither increasing production or reducing an

output cost.

Screening and an evaluation of the project- In the next step, it includes selection of all

the correct criteria in judging desirability of the project. This matches with an objective of an

enterprise that is maximising the market value (Roy, Rudra and Prasad, 2017). In this step the

tools in relation time value of the money concept is been used for the purpose of reviewing the

proposal in an effective way. Under this, estimation regarding benefits and the cost has to be

made along with the total of the cash outflows and inflows with an uncertainties and the risk

attached with proposal need to be assessed thoroughly and an appropriate provisioning is been

done.

Selection of the project- The capital expenditure proposal is been approved on the basis

of the selection criteria and the process of screening that is been defined for each firm with

keeping in mind an objectives of an investment that is being undertaken. Once a proposal is been

finalized, different alternatives in raising and procuring the funds has to be explored by finance

team (Srithongrung, Yusuf and Kriz, 2019). This known as the capital budget in which detailed

process for the periodical reports and tracing of the proposal for lifetime required to be

streamlined in an initial phase. Final approvals are taken on the basis of market conditions,

profitability, viability and an economic constituents.

6

Implementation- Different responsibilities such as execution of the proposal, project

completion within the specified time frame and a reduction of the costs are been allotted.

Thereafter the management takes up a task in monitoring and containing an execution of

proposals.

Review of performance- the last and the final step is to make comparison of the actual

figures with that of standard one (Alkaraan, 2017). The results that are unfavourable is been

identified and by removing the several difficulties of a proposal enables for the future selection

and an execution of projects.

b. capital budgeting or investment appraisal techniques

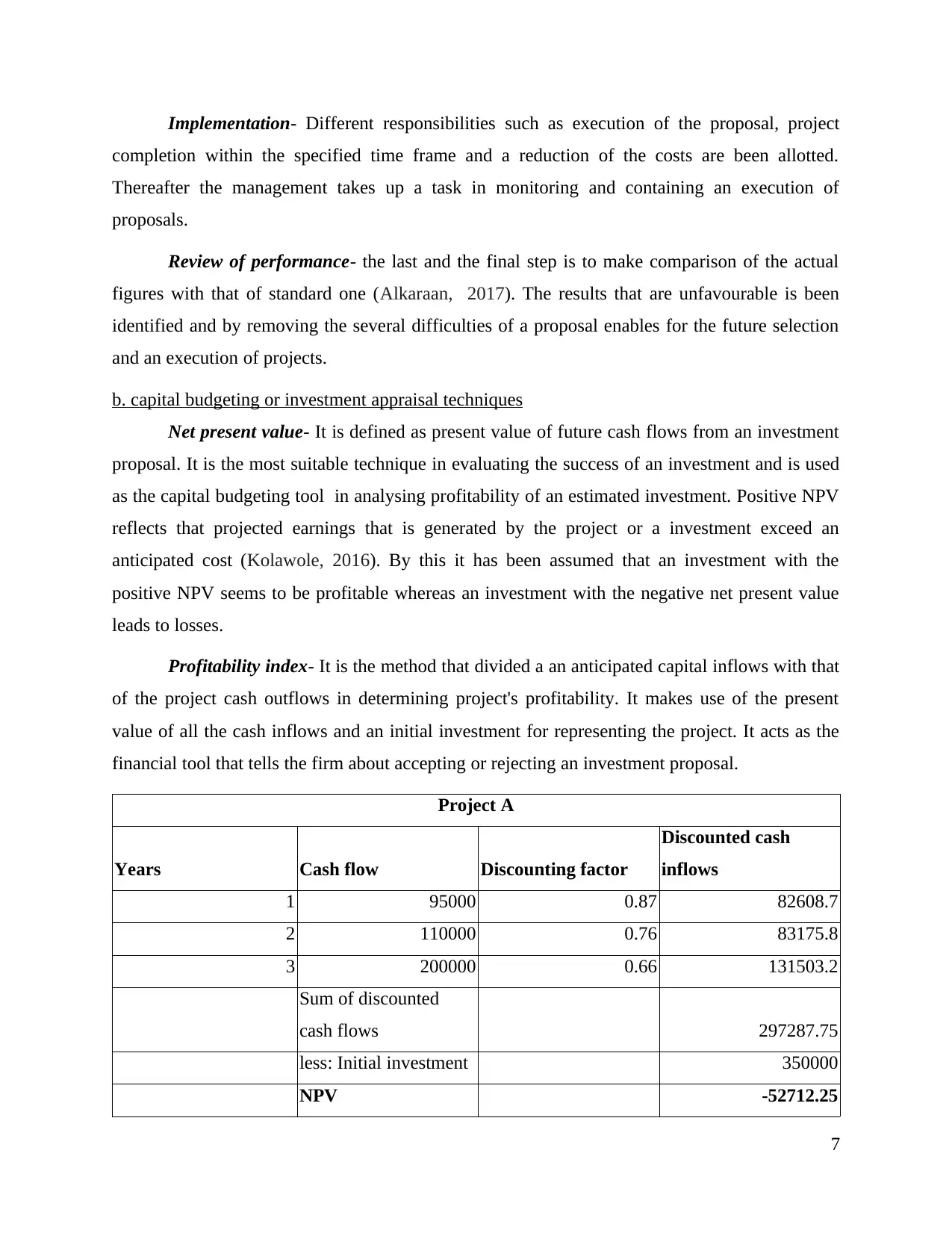

Net present value- It is defined as present value of future cash flows from an investment

proposal. It is the most suitable technique in evaluating the success of an investment and is used

as the capital budgeting tool in analysing profitability of an estimated investment. Positive NPV

reflects that projected earnings that is generated by the project or a investment exceed an

anticipated cost (Kolawole, 2016). By this it has been assumed that an investment with the

positive NPV seems to be profitable whereas an investment with the negative net present value

leads to losses.

Profitability index- It is the method that divided a an anticipated capital inflows with that

of the project cash outflows in determining project's profitability. It makes use of the present

value of all the cash inflows and an initial investment for representing the project. It acts as the

financial tool that tells the firm about accepting or rejecting an investment proposal.

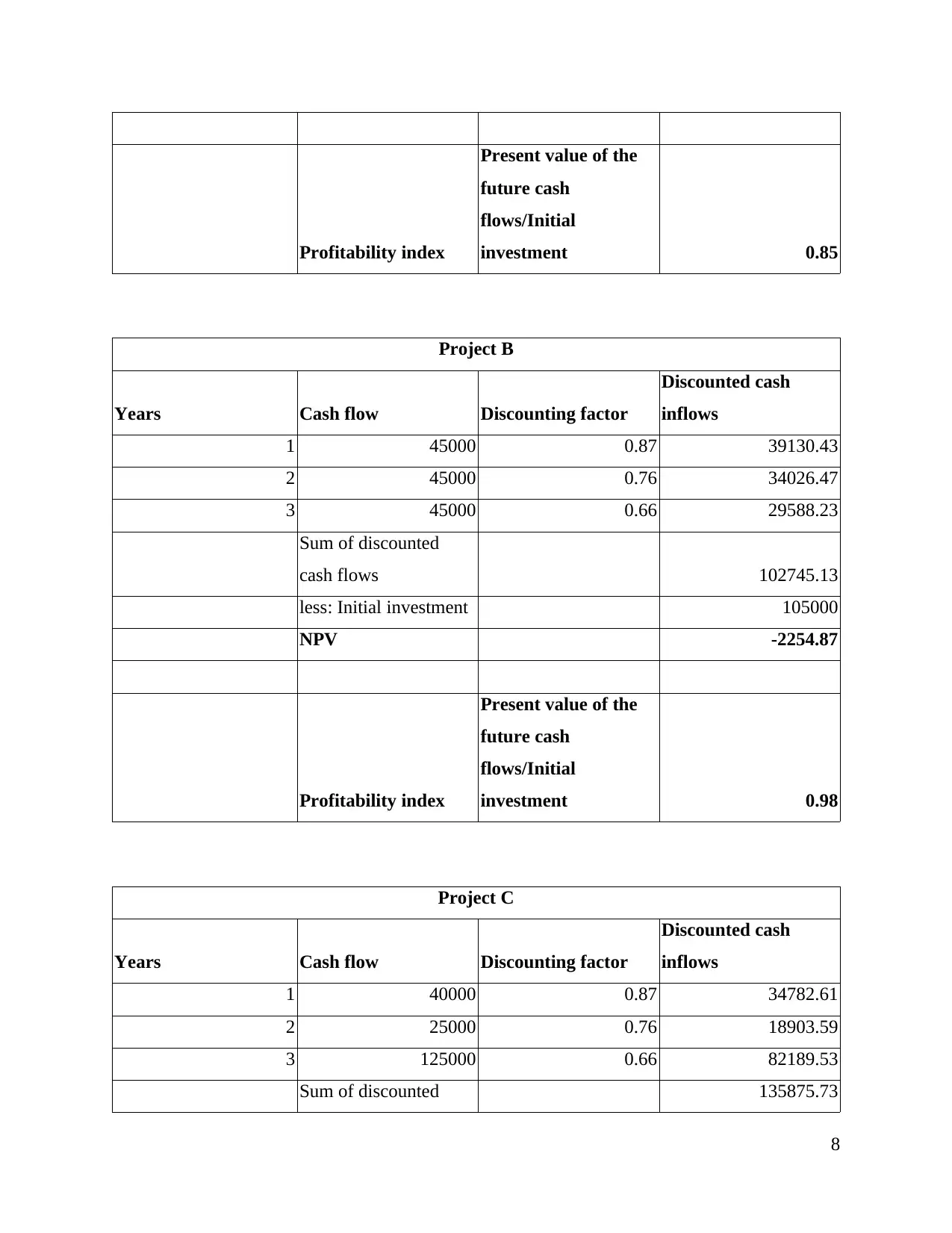

Project A

Years Cash flow Discounting factor

Discounted cash

inflows

1 95000 0.87 82608.7

2 110000 0.76 83175.8

3 200000 0.66 131503.2

Sum of discounted

cash flows 297287.75

less: Initial investment 350000

NPV -52712.25

7

completion within the specified time frame and a reduction of the costs are been allotted.

Thereafter the management takes up a task in monitoring and containing an execution of

proposals.

Review of performance- the last and the final step is to make comparison of the actual

figures with that of standard one (Alkaraan, 2017). The results that are unfavourable is been

identified and by removing the several difficulties of a proposal enables for the future selection

and an execution of projects.

b. capital budgeting or investment appraisal techniques

Net present value- It is defined as present value of future cash flows from an investment

proposal. It is the most suitable technique in evaluating the success of an investment and is used

as the capital budgeting tool in analysing profitability of an estimated investment. Positive NPV

reflects that projected earnings that is generated by the project or a investment exceed an

anticipated cost (Kolawole, 2016). By this it has been assumed that an investment with the

positive NPV seems to be profitable whereas an investment with the negative net present value

leads to losses.

Profitability index- It is the method that divided a an anticipated capital inflows with that

of the project cash outflows in determining project's profitability. It makes use of the present

value of all the cash inflows and an initial investment for representing the project. It acts as the

financial tool that tells the firm about accepting or rejecting an investment proposal.

Project A

Years Cash flow Discounting factor

Discounted cash

inflows

1 95000 0.87 82608.7

2 110000 0.76 83175.8

3 200000 0.66 131503.2

Sum of discounted

cash flows 297287.75

less: Initial investment 350000

NPV -52712.25

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profitability index

Present value of the

future cash

flows/Initial

investment 0.85

Project B

Years Cash flow Discounting factor

Discounted cash

inflows

1 45000 0.87 39130.43

2 45000 0.76 34026.47

3 45000 0.66 29588.23

Sum of discounted

cash flows 102745.13

less: Initial investment 105000

NPV -2254.87

Profitability index

Present value of the

future cash

flows/Initial

investment 0.98

Project C

Years Cash flow Discounting factor

Discounted cash

inflows

1 40000 0.87 34782.61

2 25000 0.76 18903.59

3 125000 0.66 82189.53

Sum of discounted 135875.73

8

Present value of the

future cash

flows/Initial

investment 0.85

Project B

Years Cash flow Discounting factor

Discounted cash

inflows

1 45000 0.87 39130.43

2 45000 0.76 34026.47

3 45000 0.66 29588.23

Sum of discounted

cash flows 102745.13

less: Initial investment 105000

NPV -2254.87

Profitability index

Present value of the

future cash

flows/Initial

investment 0.98

Project C

Years Cash flow Discounting factor

Discounted cash

inflows

1 40000 0.87 34782.61

2 25000 0.76 18903.59

3 125000 0.66 82189.53

Sum of discounted 135875.73

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cash flows

less: Initial investment 35000

NPV 100875.73

Profitability index

Present value of the

future cash

flows/Initial

investment 3.9

Interpretation- From the analysis it has been presented that project C is the most suitable

proposal that needs to be selected by the company because it resulted a positive value of NPV

that equates to 100875 which clearly states that the project will be generating higher profits.

Similarly, profitability index that is greater than 1 is seen as better and an investment must be

accepted. Therefore as profitability index of Project C evaluated as higher than 1 that is 3.8

which in turn indicates that this project must be accepted by the firm in order to earn larger

profitability or to attain more and more success in the future periods. This shows that present

value of the future cash flows is higher than the initial outlay which in turn states that the firm

will be earning more and more profits. The other two projects are not considered as appropriate

because it accounted a negative value of NPV and the profitability index of both the projects is

less than 1 which represents that the company will incur losses by selecting project A and Project

B and it will not counted as best for the firm to gain the competitive edge and success within an

industry. By selecting the project C for an investment purpose, an organization could be able to

invest the surplus cash or the profits in money market at the rate of 10% because it depicts a

larger amount of the profitability generation in the future. It also helps the company in limiting

an expenditure and it not have to borrow that is counted as best for its shareholders and all the

stakeholders. This enables the firm in achieving the objective of the profit maximisation and the

wealth maximisation within the market. Thus, among the three projects an entity must opt for

making investment in project C.

CONCLUSION

On the basis of above discussion, it is concluded that there is significant importance of the

finance management for the business firm because it assists it in making effective utilization of

9

less: Initial investment 35000

NPV 100875.73

Profitability index

Present value of the

future cash

flows/Initial

investment 3.9

Interpretation- From the analysis it has been presented that project C is the most suitable

proposal that needs to be selected by the company because it resulted a positive value of NPV

that equates to 100875 which clearly states that the project will be generating higher profits.

Similarly, profitability index that is greater than 1 is seen as better and an investment must be

accepted. Therefore as profitability index of Project C evaluated as higher than 1 that is 3.8

which in turn indicates that this project must be accepted by the firm in order to earn larger

profitability or to attain more and more success in the future periods. This shows that present

value of the future cash flows is higher than the initial outlay which in turn states that the firm

will be earning more and more profits. The other two projects are not considered as appropriate

because it accounted a negative value of NPV and the profitability index of both the projects is

less than 1 which represents that the company will incur losses by selecting project A and Project

B and it will not counted as best for the firm to gain the competitive edge and success within an

industry. By selecting the project C for an investment purpose, an organization could be able to

invest the surplus cash or the profits in money market at the rate of 10% because it depicts a

larger amount of the profitability generation in the future. It also helps the company in limiting

an expenditure and it not have to borrow that is counted as best for its shareholders and all the

stakeholders. This enables the firm in achieving the objective of the profit maximisation and the

wealth maximisation within the market. Thus, among the three projects an entity must opt for

making investment in project C.

CONCLUSION

On the basis of above discussion, it is concluded that there is significant importance of the

finance management for the business firm because it assists it in making effective utilization of

9

cash in the business. Capital structure heavily affect business firm cost of capital. Due to high

cost of capital sometimes loss in the business get increased. Thus, business firms must prepare

appropriate capital structure so that cost of capital can be minimized. It is also concluded that

firm must choose project C because its NPV is high and positive.

10

cost of capital sometimes loss in the business get increased. Thus, business firms must prepare

appropriate capital structure so that cost of capital can be minimized. It is also concluded that

firm must choose project C because its NPV is high and positive.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.