Report: Analyzing the Dividend Policy of Kellogg's Corporation

VerifiedAdded on 2021/05/17

|13

|2955

|41

Report

AI Summary

This report provides a comprehensive analysis of Kellogg's dividend policy, examining its significance for investors and its impact on the company's financial performance. The report reviews Kellogg's dividend yield, its turnaround plan, and the determinants influencing its dividend policy. It delves into the company's current financial situation, including its debt levels and strategic acquisitions, and assesses the effects of its dividend policy on its future growth prospects. The report also explores Kellogg's future policies, including its global commitment to address hunger and promote sustainability. The analysis considers the company's past dividend payments, future dividend development, and the factors influencing its dividend strategy, offering insights into the company's financial health and investment potential.

Corporate Finance

Student Name:

Student Id:

Course Name:

0 | P a g e

Student Name:

Student Id:

Course Name:

0 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................2

Importance of the dividend policy.............................................................................................2

Review of Kellogg’s dividend policy........................................................................................3

Determinants of Dividend Policy...............................................................................................4

Situation of the company...........................................................................................................5

The turnaround plan of the company.........................................................................................5

Effect of the dividend policy......................................................................................................6

Future policies............................................................................................................................7

Conclusion..................................................................................................................................8

References..................................................................................................................................9

Appendix..................................................................................................................................11

1 | P a g e

Introduction................................................................................................................................2

Importance of the dividend policy.............................................................................................2

Review of Kellogg’s dividend policy........................................................................................3

Determinants of Dividend Policy...............................................................................................4

Situation of the company...........................................................................................................5

The turnaround plan of the company.........................................................................................5

Effect of the dividend policy......................................................................................................6

Future policies............................................................................................................................7

Conclusion..................................................................................................................................8

References..................................................................................................................................9

Appendix..................................................................................................................................11

1 | P a g e

Introduction

This report is an analysis rather a review of the dividend policy of Kellogg’s which is a large

multinational corporation which belongs to the industry of the packaged goods. This report

will refer to their dividend policies and determine whether it is appropriate or not.

Importance of the dividend policy

For investors, dividend policy is a huge thought to consider in the stock-determination

measure since profits are a major money outpouring for organizations (Berndt, 2019). In

2015 alone for instance, BSE-recorded organizations delivered out money profits in

overabundance of $10 billion. Anyway simultaneously, around 20% of the organizations

recorded did not deliver a dividend by any stretch of the imagination. From the start, it will

appear to be certain that by delivering cash dividends, a business will even now need to offer

back to its investors however much as could be expected. It could seem as obvious, though,

that instead of paying it out a business should still save the money for its shareholders. This is

an important argument to be remembered by both present and prospective company

shareholders (Berndt, 2019). Based on these, the researcher has illustrated the dividend yield

chart in respect of an organizational management mentioned below:

Figure 1: Company Dividend Yield %

Source: (From Web)

2 | P a g e

This report is an analysis rather a review of the dividend policy of Kellogg’s which is a large

multinational corporation which belongs to the industry of the packaged goods. This report

will refer to their dividend policies and determine whether it is appropriate or not.

Importance of the dividend policy

For investors, dividend policy is a huge thought to consider in the stock-determination

measure since profits are a major money outpouring for organizations (Berndt, 2019). In

2015 alone for instance, BSE-recorded organizations delivered out money profits in

overabundance of $10 billion. Anyway simultaneously, around 20% of the organizations

recorded did not deliver a dividend by any stretch of the imagination. From the start, it will

appear to be certain that by delivering cash dividends, a business will even now need to offer

back to its investors however much as could be expected. It could seem as obvious, though,

that instead of paying it out a business should still save the money for its shareholders. This is

an important argument to be remembered by both present and prospective company

shareholders (Berndt, 2019). Based on these, the researcher has illustrated the dividend yield

chart in respect of an organizational management mentioned below:

Figure 1: Company Dividend Yield %

Source: (From Web)

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The term dividend ordinarily alludes to money paid by the organization to its investors out of

income. The word distribution, as opposed to dividend, is utilized when a pay-out is produced

using sources other than existing or accumulated income which is put on hold. It is

nonetheless, suitable to allude to a pay-out as a profit from income. All the more

comprehensively, any immediate installment to investors by the company can be known as a

dividend. Normal cash dividends, extra dividends and special dividends are the basic types of

cash dividends.

The core issue of dividend policy deals with various questions like should the company pay

its shareholders with cash or should it retain the cash, invest it and pay its shareholders back

later. The dividend strategy, therefore is the dividend distribution time pattern. In particular,

should a large percentage of the company’s profits, however small it might be, be paid out by

the company? This is the issue of dividend strategy. Generally, organizations that have

potential of further growth and need capital do not deliver any dividends, while they are paid

by those that have developed and matured (CORRADI, 2020). There are organizations that

deliver a consistent dividend regardless of their performance as opposed to the latter, and

different organizations deliver a little symbolic profit and deliver profits relying upon

execution. Here, every year, profits can vary and it is known as a cyclical dividend strategy.

Thus, the corporations' dividend strategy is tricky. There are a few unplausible clarifications

why dividend strategies may be pertinent, and many of the policy arguments are

economically illogical. Indeed, even so without a doubt deciding the appropriate dividend

policy is a significant issue.

Review of Kellogg’s dividend policy

3 | P a g e

income. The word distribution, as opposed to dividend, is utilized when a pay-out is produced

using sources other than existing or accumulated income which is put on hold. It is

nonetheless, suitable to allude to a pay-out as a profit from income. All the more

comprehensively, any immediate installment to investors by the company can be known as a

dividend. Normal cash dividends, extra dividends and special dividends are the basic types of

cash dividends.

The core issue of dividend policy deals with various questions like should the company pay

its shareholders with cash or should it retain the cash, invest it and pay its shareholders back

later. The dividend strategy, therefore is the dividend distribution time pattern. In particular,

should a large percentage of the company’s profits, however small it might be, be paid out by

the company? This is the issue of dividend strategy. Generally, organizations that have

potential of further growth and need capital do not deliver any dividends, while they are paid

by those that have developed and matured (CORRADI, 2020). There are organizations that

deliver a consistent dividend regardless of their performance as opposed to the latter, and

different organizations deliver a little symbolic profit and deliver profits relying upon

execution. Here, every year, profits can vary and it is known as a cyclical dividend strategy.

Thus, the corporations' dividend strategy is tricky. There are a few unplausible clarifications

why dividend strategies may be pertinent, and many of the policy arguments are

economically illogical. Indeed, even so without a doubt deciding the appropriate dividend

policy is a significant issue.

Review of Kellogg’s dividend policy

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

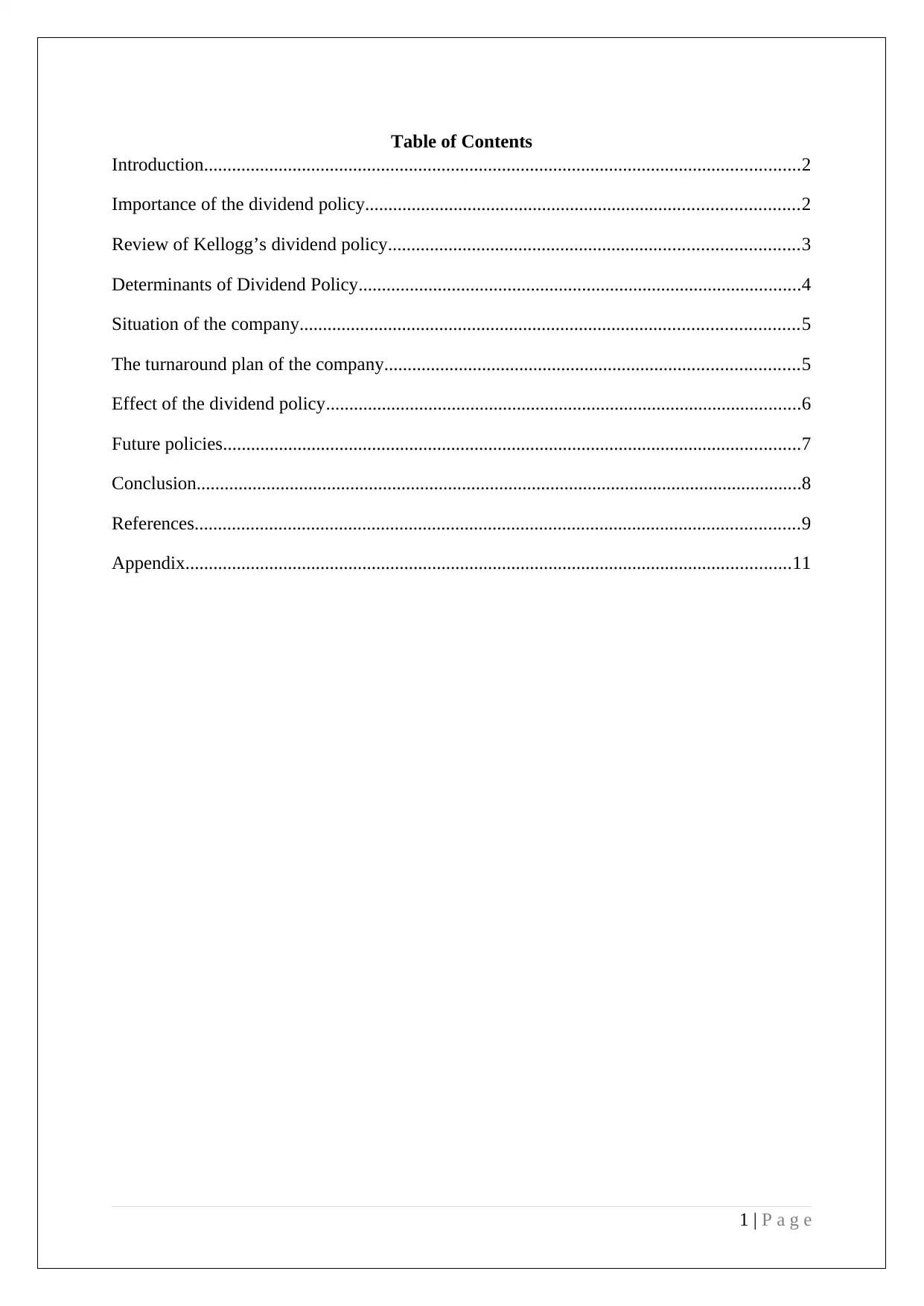

Figure 2: Company Dividend Yield % based on the 5 years average

Source: (From Web)

From the month of September, Kellogg(K) shares have plunged more than 20%, sending the

profit yield of the stock up to around 4 percent, its most significant level in 19 years. The

turnaround system for Kellogg depends on a multi-tiered methodology. That is inclusive of

brand acquisitions with the present clients that are on pattern." In 2017, when Kellogg paid

$600 million for RXBAR, an all-characteristic protein bar producer, one of the organization's

most remarkable acquisitions occurred. Although the pay-out ratio of the company seems

likely to hover well above the long-term objective of management for now the dividend of

Kellogg continues to look secure (Carreno and Dolle, 2017). The company also receives a

credit rating of the company S&P and their investment grade, giving it readily available

flexibility based on finances as it continues to seek acquisitions. These factors, do not

inherently suggest that Kellogg’s is a good long-term dividend growth stock. Kellogg’s is

already under a lot of debt in the past decade to finance its strategic acquisitions while

benefiting from relatively low interest rates. With quite a bit of its free income presently

heading off to its stable yet moderate developing profit, reasonable development stays a

danger, and acquisitions being a key development methodology, it very well may be more

troublesome later on to continue its present FICO assessment (Gowdy and Winston, 2016).

The primary reason for the company assessing its strengths along with considering investing

declining brands that are focused on selling sluggish or growth items which contribute to

negative growth like snacks and cookies is the requirement for financing the restructuring

plans as well as preserve a balance sheet which is healthy. Management claims that in 2018

sales of these possible divestitures amounted to around $900 million and the profits will go to

debt reduction in front of future acquisitions and potentially buybacks which are

4 | P a g e

Source: (From Web)

From the month of September, Kellogg(K) shares have plunged more than 20%, sending the

profit yield of the stock up to around 4 percent, its most significant level in 19 years. The

turnaround system for Kellogg depends on a multi-tiered methodology. That is inclusive of

brand acquisitions with the present clients that are on pattern." In 2017, when Kellogg paid

$600 million for RXBAR, an all-characteristic protein bar producer, one of the organization's

most remarkable acquisitions occurred. Although the pay-out ratio of the company seems

likely to hover well above the long-term objective of management for now the dividend of

Kellogg continues to look secure (Carreno and Dolle, 2017). The company also receives a

credit rating of the company S&P and their investment grade, giving it readily available

flexibility based on finances as it continues to seek acquisitions. These factors, do not

inherently suggest that Kellogg’s is a good long-term dividend growth stock. Kellogg’s is

already under a lot of debt in the past decade to finance its strategic acquisitions while

benefiting from relatively low interest rates. With quite a bit of its free income presently

heading off to its stable yet moderate developing profit, reasonable development stays a

danger, and acquisitions being a key development methodology, it very well may be more

troublesome later on to continue its present FICO assessment (Gowdy and Winston, 2016).

The primary reason for the company assessing its strengths along with considering investing

declining brands that are focused on selling sluggish or growth items which contribute to

negative growth like snacks and cookies is the requirement for financing the restructuring

plans as well as preserve a balance sheet which is healthy. Management claims that in 2018

sales of these possible divestitures amounted to around $900 million and the profits will go to

debt reduction in front of future acquisitions and potentially buybacks which are

4 | P a g e

opportunistic. The good news is that, amid the company's divestitures and cost-cutting plans,

Kellogg's profit should stay steady, regardless of whether a downturn hits and credit markets

fix (Holdorf, 2017). The company of Kellogg has cash flow and I plenty which still is thrown

off, and recession-resistant demand is enjoyed by most of its products. For the near future,

however, cautious investors should not hope for something else than low single-digit yearly

income and profit development. If Kellogg's turnaround continues to fail, perhaps because of

prolonged cereal weakness, a profit freeze would also not be unlikely, particularly if the

organization's salary out proportion and duty continued to fall higher..

Determinants of Dividend Policy

There are different variables that decide the dividend policy of businesses. These incorporate

developments, the capacity to bring assets up in the capital business sectors, age, organization

size, charges on profit receipt issues, and so forth. For instance, in nations where investor

profits are burdened higher than capital increases, investors normally tend not to deliver

profits to organizations (Kalaj and Lamel, 2020).

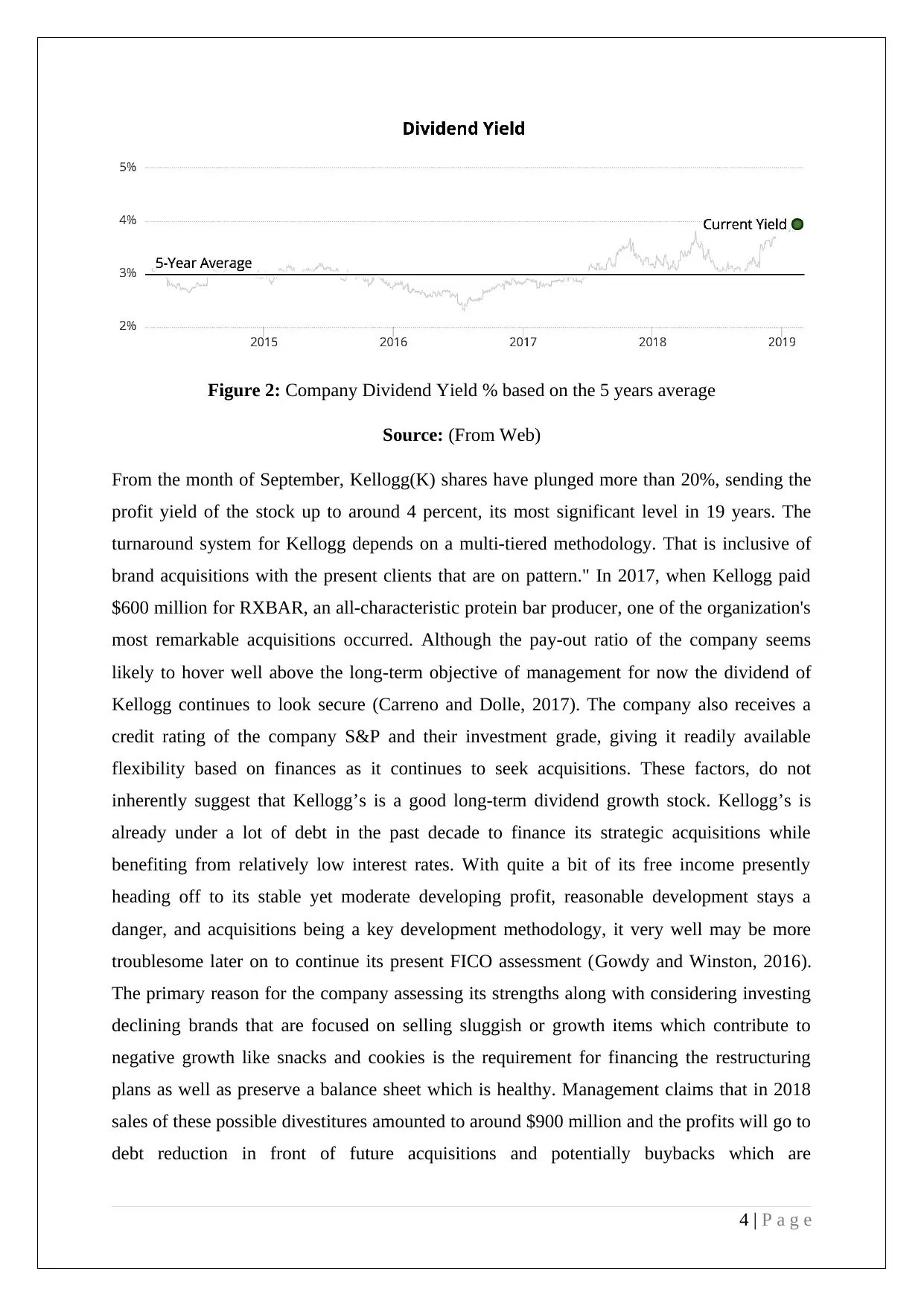

Situation of the company

Basically, although Kellogg's thesis has not broken down, over the years it has deteriorated

somewhat (Kideckel, 2018). The long-promised turnaround by management continues to take

more time than most investors anticipated to return the business to sustainable growth. It has

also been mixed with signs that Kellogg has fumbled a portion of its brands over the long

haul and could remain moored by its gigantic grain area, forthcoming financial specialists

need to find out if they need to claim in their portfolio a 4 percent get back with a moderate

profit development profile and an exceptionally unsure long haul viewpoint (Markel, 2017).

Figure 3: Company Situation based on the present share price and Market Volume

Source: (From Web)

5 | P a g e

Kellogg's profit should stay steady, regardless of whether a downturn hits and credit markets

fix (Holdorf, 2017). The company of Kellogg has cash flow and I plenty which still is thrown

off, and recession-resistant demand is enjoyed by most of its products. For the near future,

however, cautious investors should not hope for something else than low single-digit yearly

income and profit development. If Kellogg's turnaround continues to fail, perhaps because of

prolonged cereal weakness, a profit freeze would also not be unlikely, particularly if the

organization's salary out proportion and duty continued to fall higher..

Determinants of Dividend Policy

There are different variables that decide the dividend policy of businesses. These incorporate

developments, the capacity to bring assets up in the capital business sectors, age, organization

size, charges on profit receipt issues, and so forth. For instance, in nations where investor

profits are burdened higher than capital increases, investors normally tend not to deliver

profits to organizations (Kalaj and Lamel, 2020).

Situation of the company

Basically, although Kellogg's thesis has not broken down, over the years it has deteriorated

somewhat (Kideckel, 2018). The long-promised turnaround by management continues to take

more time than most investors anticipated to return the business to sustainable growth. It has

also been mixed with signs that Kellogg has fumbled a portion of its brands over the long

haul and could remain moored by its gigantic grain area, forthcoming financial specialists

need to find out if they need to claim in their portfolio a 4 percent get back with a moderate

profit development profile and an exceptionally unsure long haul viewpoint (Markel, 2017).

Figure 3: Company Situation based on the present share price and Market Volume

Source: (From Web)

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The turnaround plan of the company

The turnaround system for Kellogg depends on a multi-pronged methodology. That is

inclusive of brand acquisitions with the present clients that are on pattern." In 2017, when

Kellogg paid $600 million for RXBAR, an all-characteristic protein bar producer, one of the

organization's most remarkable acquisitions occurred (Markel, 2017). Meanwhile the firm is

currently experiencing respectable organic growth in international markets, inclusive of:

Europe has 3% thanks to Pringles' introduction and the extension to the Middle East

as well as Russia

7% regarded to be in America (Latin) (Lazar, 2018)

In Asia Pacific, 5 percent

In reality, a higher extent of Kellogg's income is created from developing business sectors

than everything except two of its friends, thanks partially to a $420 million arrangement in

2018 to develop its African area. But only two aspects of a three-pronged plan to return the

business to sustainable growth are aimed at stronger overseas growth and expanding its

healthier products. The last angle is reduction in cost, explicitly "Venture K," acquainted in

2013 and planned with both smooth out the gracefully chain of Kellogg, just as make it

simpler to consolidate its better performing brands into new item dispatches (Sethi and Bafna,

2018). The aim of management was to cut costs by $475 million due to these efforts (Markel,

2017). In 2017, Kellogg’s likewise moved from an immediate store conveyance model to one

focused on stockrooms (like a large portion of its opponents use for around 25 percent of its

items. This diminished working costs by around $650 million toward the finish of 2019,

reflecting around a 6 percent decrease in the expense of merchandise sold. Over the long

haul, the executives anticipate that a reshuffling of its brands, joined with more grounded

development abroad and progressing cost-reduction exercises, will assist in changing EPS as

well as profit development of 7% in an annual period. It is anticipated that profitable growth

will be powered by a greater emphasis on snacks, solidified nourishments and developing

business sectors, which are all normal to ascend at a low-to-mid single-digit rate, while oats

are required to stay stable.

6 | P a g e

The turnaround system for Kellogg depends on a multi-pronged methodology. That is

inclusive of brand acquisitions with the present clients that are on pattern." In 2017, when

Kellogg paid $600 million for RXBAR, an all-characteristic protein bar producer, one of the

organization's most remarkable acquisitions occurred (Markel, 2017). Meanwhile the firm is

currently experiencing respectable organic growth in international markets, inclusive of:

Europe has 3% thanks to Pringles' introduction and the extension to the Middle East

as well as Russia

7% regarded to be in America (Latin) (Lazar, 2018)

In Asia Pacific, 5 percent

In reality, a higher extent of Kellogg's income is created from developing business sectors

than everything except two of its friends, thanks partially to a $420 million arrangement in

2018 to develop its African area. But only two aspects of a three-pronged plan to return the

business to sustainable growth are aimed at stronger overseas growth and expanding its

healthier products. The last angle is reduction in cost, explicitly "Venture K," acquainted in

2013 and planned with both smooth out the gracefully chain of Kellogg, just as make it

simpler to consolidate its better performing brands into new item dispatches (Sethi and Bafna,

2018). The aim of management was to cut costs by $475 million due to these efforts (Markel,

2017). In 2017, Kellogg’s likewise moved from an immediate store conveyance model to one

focused on stockrooms (like a large portion of its opponents use for around 25 percent of its

items. This diminished working costs by around $650 million toward the finish of 2019,

reflecting around a 6 percent decrease in the expense of merchandise sold. Over the long

haul, the executives anticipate that a reshuffling of its brands, joined with more grounded

development abroad and progressing cost-reduction exercises, will assist in changing EPS as

well as profit development of 7% in an annual period. It is anticipated that profitable growth

will be powered by a greater emphasis on snacks, solidified nourishments and developing

business sectors, which are all normal to ascend at a low-to-mid single-digit rate, while oats

are required to stay stable.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Effect of the dividend policy

Taking a look at profit development, the current annualized profit of $2.28 for the

organization is up 0.9% from a year ago. Kellogg has raised its profit multiple times on a

year-on-year premise in the course of the most recent 5 years, with a yearly normal ascent of

3.52 percent. Future profit development, looking forward would depend on income

development and pay-out proportion, which is the extent of the yearly income per portion of a

business that it delivers out as a profit. The current pay out proportion for Kellogg is 58

percent. Kellogg’s expects profits to also increase this fiscal year. The 2020 Zacks Consensus

Estimate is $4.02 per share, which reflects a growth rate of 2.03 percent year-over-year

(Thompson, 2018).

Rate of dividend Date of recording Pay date Amount Frequency

November 12/01/2020 15/12/2020 $0.58 Quarterly

basis.

October 9/1/2020 15/09/2020 $0.58 Quarterly

basis.

September 18/1/2020 26/1/2020 $0.58 Quarterly

basis.

August 20/02/2020 26/02/2020 $0.58 Quarterly

basis.

Kellogg, which manufactures such popular food and snack products as Pop Tarts, Rice

Krispies, and Frosted Flakes, did not hesitate to point out that since 1925, this is the 382nd

profit that it has declared on its regular stock. It has been a steady and effective profit payer

throughout the long term, if not an energetic raiser, as an exceptionally adult firm. Its

dissemination has expanded consistently from $0.43 per offer to the current level since mid-

2011. The company's new dividend announcement comes not exactly seven days before its

Q1 results for monetary 2020 are relied upon to be uncovered. This should occur before the

market opens on Thursday, April 30th. 16 experts checking Kellogg altogether anticipate that

it should record a humble disintegration in per-share net benefits, to $ 0.95 for the quarter

versus $ 1.01 in Q1 2019, as indicated by Yahoo! Account. Deals are foreseen to fall by

nearly 5% to $3.38 billion (van der Vennet and Cassella, 2020).

Future policies

7 | P a g e

Taking a look at profit development, the current annualized profit of $2.28 for the

organization is up 0.9% from a year ago. Kellogg has raised its profit multiple times on a

year-on-year premise in the course of the most recent 5 years, with a yearly normal ascent of

3.52 percent. Future profit development, looking forward would depend on income

development and pay-out proportion, which is the extent of the yearly income per portion of a

business that it delivers out as a profit. The current pay out proportion for Kellogg is 58

percent. Kellogg’s expects profits to also increase this fiscal year. The 2020 Zacks Consensus

Estimate is $4.02 per share, which reflects a growth rate of 2.03 percent year-over-year

(Thompson, 2018).

Rate of dividend Date of recording Pay date Amount Frequency

November 12/01/2020 15/12/2020 $0.58 Quarterly

basis.

October 9/1/2020 15/09/2020 $0.58 Quarterly

basis.

September 18/1/2020 26/1/2020 $0.58 Quarterly

basis.

August 20/02/2020 26/02/2020 $0.58 Quarterly

basis.

Kellogg, which manufactures such popular food and snack products as Pop Tarts, Rice

Krispies, and Frosted Flakes, did not hesitate to point out that since 1925, this is the 382nd

profit that it has declared on its regular stock. It has been a steady and effective profit payer

throughout the long term, if not an energetic raiser, as an exceptionally adult firm. Its

dissemination has expanded consistently from $0.43 per offer to the current level since mid-

2011. The company's new dividend announcement comes not exactly seven days before its

Q1 results for monetary 2020 are relied upon to be uncovered. This should occur before the

market opens on Thursday, April 30th. 16 experts checking Kellogg altogether anticipate that

it should record a humble disintegration in per-share net benefits, to $ 0.95 for the quarter

versus $ 1.01 in Q1 2019, as indicated by Yahoo! Account. Deals are foreseen to fall by

nearly 5% to $3.38 billion (van der Vennet and Cassella, 2020).

Future policies

7 | P a g e

Kellogg’s has now adopted a marketing strategy aimed at global commitment help and aims

to end hunger and create a better world for 3 billion people by 2030.

It will ensure the following steps to carry out its vision:

Nourishment of 1 billion people by providing food, nutrients which are required and

addressing hunger accordingly

Feed around 375 million people just through food donations and feeding programs

specially organised for children

Nurture the planet by supporting around one million farmers inclusive of women and

smallholders (CORRADI, 2020)

Conserve all-natural resources from the start to the end of the value chain, which

refers to responsibly acting towards sourcing ingredients while reducing food waste to

the providing of recyclable, reusable or packaging which can be composted.

Encourage volunteering of employees while ensuring a supply chain of ethical values

and also supporting inclusion along with diversity.

By ensuring these steps Kellogg’s promises to achieve its mission to wipe the world hunger

index and simultaneously ensure that no matter how poor a person is can afford a meal such

that their family never sleeps hungry.

Conclusion

For over a century, Kellogg's different arrangement of enormous and notable brands has

served financial specialists well. All organizations, anyway need to conform to developing

client tastes, and over the previous decade, Kellogg has truly neglected. Although the

turnaround plan of management sounds rational, and the long-term growth guidance of the

company (approximately 7 percent cash flow and dividend growth per year) looks promising

at first glance, investors have reason to be doubtful that it will execute that plan (Markel,

2017).

At least, for maintaining a balance sheet which is and finance its ongoing turnaround,

Kellogg, though potentially a secure income investment, would probably need to increase its

dividend slowly than it has in the past. Investing in businesses with better long-term outlooks

and smoother pathways to sustainable growth is a choice for cautious investors. Many parts

of the portfolio of Kellogg continue to remain in the crosshairs of evolving customer tastes,

8 | P a g e

to end hunger and create a better world for 3 billion people by 2030.

It will ensure the following steps to carry out its vision:

Nourishment of 1 billion people by providing food, nutrients which are required and

addressing hunger accordingly

Feed around 375 million people just through food donations and feeding programs

specially organised for children

Nurture the planet by supporting around one million farmers inclusive of women and

smallholders (CORRADI, 2020)

Conserve all-natural resources from the start to the end of the value chain, which

refers to responsibly acting towards sourcing ingredients while reducing food waste to

the providing of recyclable, reusable or packaging which can be composted.

Encourage volunteering of employees while ensuring a supply chain of ethical values

and also supporting inclusion along with diversity.

By ensuring these steps Kellogg’s promises to achieve its mission to wipe the world hunger

index and simultaneously ensure that no matter how poor a person is can afford a meal such

that their family never sleeps hungry.

Conclusion

For over a century, Kellogg's different arrangement of enormous and notable brands has

served financial specialists well. All organizations, anyway need to conform to developing

client tastes, and over the previous decade, Kellogg has truly neglected. Although the

turnaround plan of management sounds rational, and the long-term growth guidance of the

company (approximately 7 percent cash flow and dividend growth per year) looks promising

at first glance, investors have reason to be doubtful that it will execute that plan (Markel,

2017).

At least, for maintaining a balance sheet which is and finance its ongoing turnaround,

Kellogg, though potentially a secure income investment, would probably need to increase its

dividend slowly than it has in the past. Investing in businesses with better long-term outlooks

and smoother pathways to sustainable growth is a choice for cautious investors. Many parts

of the portfolio of Kellogg continue to remain in the crosshairs of evolving customer tastes,

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and the long-term track record of management's adaptation of the company does not inspire

much confidence.

References

Berndt, A., 2019. BREAKFAST GONE BAD… the case of Kellogg’s rice

Krispies®. Emerald Emerging Markets Case Studies.

Carreno, I. and Dolle, T., 2017. The Relationship between Public Health and IP Rights: Chile

Prosecutes Kellogg's, Nestle and Masterfoods for Using Cartons Aimed at Attracting

Children. Eur. J. Risk Reg., 8, p.170.

CORRADI, C., 2020. CSR and corporate image: a comparative analysis of the environmental

theme in Barilla's and Kellogg's CSR reports.

Gowdy, J. and Winston, A., 2016. Evaluation of General Mills' and Kellogg's GHG

Emissions Targets and Plans: Independent Assessment conducted by Winston Eco-Strategies

for Oxfam's Behind the Brands Initiative.

Holdorf, D., 2017. Incorporating Climate Change and Sustainability into Kellogg’s

Decisionmaking (No. 1958-2017-2594).

Kalaj, D. and Lamel, B., 2020. Minimisers and Kellogg’s theorem. Mathematische Annalen,

pp.1-30.

9 | P a g e

much confidence.

References

Berndt, A., 2019. BREAKFAST GONE BAD… the case of Kellogg’s rice

Krispies®. Emerald Emerging Markets Case Studies.

Carreno, I. and Dolle, T., 2017. The Relationship between Public Health and IP Rights: Chile

Prosecutes Kellogg's, Nestle and Masterfoods for Using Cartons Aimed at Attracting

Children. Eur. J. Risk Reg., 8, p.170.

CORRADI, C., 2020. CSR and corporate image: a comparative analysis of the environmental

theme in Barilla's and Kellogg's CSR reports.

Gowdy, J. and Winston, A., 2016. Evaluation of General Mills' and Kellogg's GHG

Emissions Targets and Plans: Independent Assessment conducted by Winston Eco-Strategies

for Oxfam's Behind the Brands Initiative.

Holdorf, D., 2017. Incorporating Climate Change and Sustainability into Kellogg’s

Decisionmaking (No. 1958-2017-2594).

Kalaj, D. and Lamel, B., 2020. Minimisers and Kellogg’s theorem. Mathematische Annalen,

pp.1-30.

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Kideckel, M.S., 2018. The Kelloggs: Battling Brothers of Battle Creek. ByHoward Markel.

New York: Pantheon Books, 2017. xxix+ 506 pp. Photographs, notes, index. Cloth, $35.00.

ISBN: 978-0-307-90727-1. Business History Review, 92(3), pp.580-582.

Lazar, P., 2018. The Kelloggs: The Battling Brothers of Battle Creek. Family

medicine, 50(4), pp.313-314.

Markel, H., 2017. How Dr. Kellogg's World-Renowned Health Spa Made Him a Wellness

Titan.

Markel, H., 2017. The Secret Ingredient in Kellogg's Corn Flakes Is Seventh-Day Adventism.

Sethi, R. and Bafna, P., 2018. A case study on ipr infringement: Kellogg's company V/S

national biscuit company. ZENITH International Journal of Multidisciplinary Research, 8(7),

pp.339-342.

Thompson, P.B., 2018. Howard Markel, The Kelloggs: The Battling Brothers of Battle

Creek. Agriculture and Human Values, 35(3), pp.737-738.

van der Vennet, R. and Cassella, C., 2020. Do Mandalas Exhibit Archetypal Patterns Based

on Kellogg’s MARI? A Pilot Study. Canadian Journal of Counselling &

Psychotherapy/Revue Canadienne de Counseling et de Psychothérapie, 54(3).

10 | P a g e

New York: Pantheon Books, 2017. xxix+ 506 pp. Photographs, notes, index. Cloth, $35.00.

ISBN: 978-0-307-90727-1. Business History Review, 92(3), pp.580-582.

Lazar, P., 2018. The Kelloggs: The Battling Brothers of Battle Creek. Family

medicine, 50(4), pp.313-314.

Markel, H., 2017. How Dr. Kellogg's World-Renowned Health Spa Made Him a Wellness

Titan.

Markel, H., 2017. The Secret Ingredient in Kellogg's Corn Flakes Is Seventh-Day Adventism.

Sethi, R. and Bafna, P., 2018. A case study on ipr infringement: Kellogg's company V/S

national biscuit company. ZENITH International Journal of Multidisciplinary Research, 8(7),

pp.339-342.

Thompson, P.B., 2018. Howard Markel, The Kelloggs: The Battling Brothers of Battle

Creek. Agriculture and Human Values, 35(3), pp.737-738.

van der Vennet, R. and Cassella, C., 2020. Do Mandalas Exhibit Archetypal Patterns Based

on Kellogg’s MARI? A Pilot Study. Canadian Journal of Counselling &

Psychotherapy/Revue Canadienne de Counseling et de Psychothérapie, 54(3).

10 | P a g e

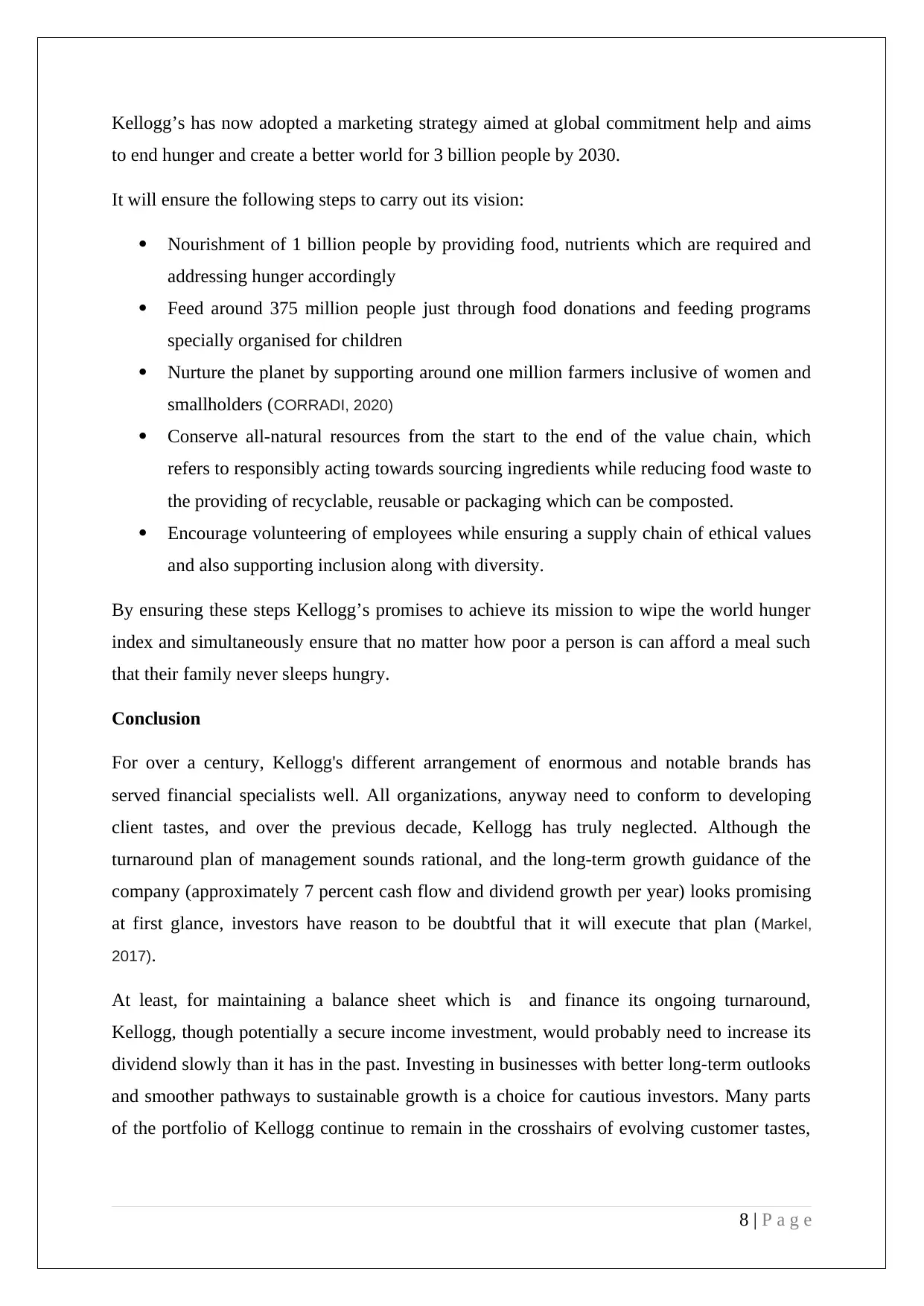

Appendix

1. Stock market price of the company

2. Kellogg’s Market capability

11 | P a g e

1. Stock market price of the company

2. Kellogg’s Market capability

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.