FIN200 Assignment: Corporate Finance Management and Portfolio Theory

VerifiedAdded on 2023/06/07

|10

|2307

|405

Essay

AI Summary

This essay provides a comprehensive analysis of key concepts in corporate finance management, including the Security Market Line (SML), Capital Market Line (CML), Capital Asset Pricing Model (CAPM), and minimum variance portfolios. It differentiates between the SML and CML, highlighting their graphical representations and underlying principles. The importance of minimum variance portfolios in minimizing risk is discussed within the context of Modern Portfolio Theory (MPT). Furthermore, the essay argues for the relevance of the CAPM equation in calculating required rates of return, comparing it with the Dividend Growth Model (DGM) and Weighted Average Cost of Capital (WACC) model, and emphasizing its consideration of systematic risk. This document is a student's contribution and is available on Desklib, a platform offering study tools and resources for students.

Running head: CORPORATE FINANCE MANAGEMENT

Corporate Finance Management

Name of the Student

Name of the University

Author Note

Corporate Finance Management

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE FINANCE MANAGEMENT

Answer to part (A)

The Security Market Line (SML) is a tool that is used to evaluate the portfolios which

is based on the Capital Asset Pricing Model. The Security Market Line establishes a

relationship between the volatility of risk and the expected returns that are associated with a

portfolio for an individual as well as the inefficient portfolios. The Security Market Line is

the main concept that is used in the Capital Asset Pricing Model. The risk that is associated

with the Security Market Line is presented in terms of beta. Beta is nothing but the security

sensitivity with regards to fluctuations in the market returns. On the other hand, Capital

Market Line is used to represent the risk free rate of return corresponding to an efficient

portfolio. The risk in case of the Capital Market Model is presented in terms of variance or

standard deviation. By standard deviation, it is meant the deviation from the mean value. The

mathematical and graphical representation of the models are provided for a better

understanding of the matter.

Let ( σ m ,rm ¿ be the point corresponding to the market portfolio M and ( σ p , r p ¿be the

point on the capital market line. The equation of the capital market line is denoted by,

r p =rf + r M −r f

σ M

σ p

Where, r p = rate of return of the efficient portfolio and σ p = variance of the expected

portfolio, rM −rf

σ M

is the price of risk as well as the slope of the Capital Market Line.

For any ith individual,

ri−rf =βi (rm−r f ) ,

Where, ri = required rate of return on the ith individual financial asset

Answer to part (A)

The Security Market Line (SML) is a tool that is used to evaluate the portfolios which

is based on the Capital Asset Pricing Model. The Security Market Line establishes a

relationship between the volatility of risk and the expected returns that are associated with a

portfolio for an individual as well as the inefficient portfolios. The Security Market Line is

the main concept that is used in the Capital Asset Pricing Model. The risk that is associated

with the Security Market Line is presented in terms of beta. Beta is nothing but the security

sensitivity with regards to fluctuations in the market returns. On the other hand, Capital

Market Line is used to represent the risk free rate of return corresponding to an efficient

portfolio. The risk in case of the Capital Market Model is presented in terms of variance or

standard deviation. By standard deviation, it is meant the deviation from the mean value. The

mathematical and graphical representation of the models are provided for a better

understanding of the matter.

Let ( σ m ,rm ¿ be the point corresponding to the market portfolio M and ( σ p , r p ¿be the

point on the capital market line. The equation of the capital market line is denoted by,

r p =rf + r M −r f

σ M

σ p

Where, r p = rate of return of the efficient portfolio and σ p = variance of the expected

portfolio, rM −rf

σ M

is the price of risk as well as the slope of the Capital Market Line.

For any ith individual,

ri−rf =βi (rm−r f ) ,

Where, ri = required rate of return on the ith individual financial asset

2CORPORATE FINANCE MANAGEMENT

r f = risk free rate of return

βi = volatility of the ith individual asset

rm= average return on capital market

The above is the equation of the Security Market Line with β portfolio.

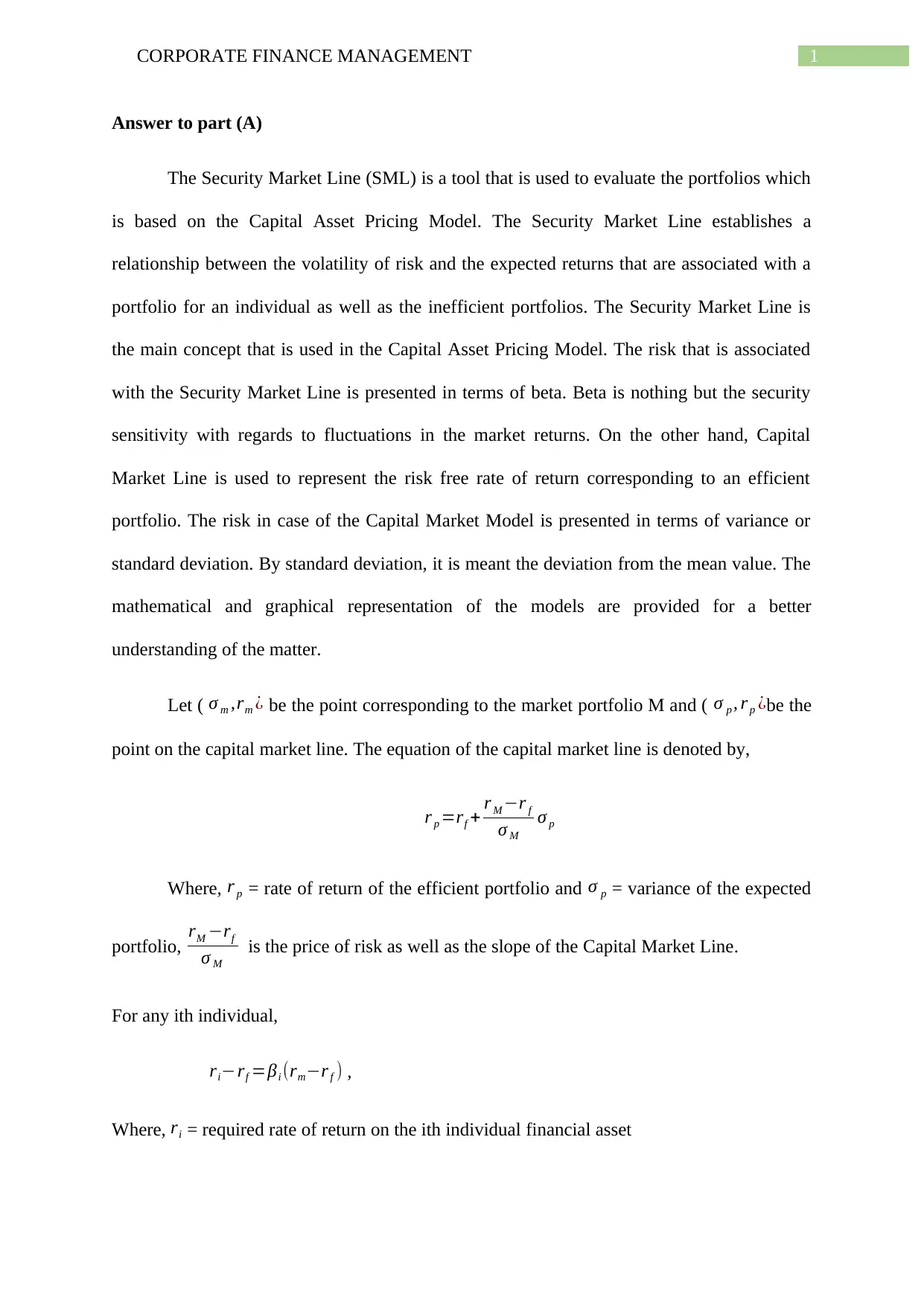

From the two diagrams provided below it can be seen that the Capital Market Line is

the locus of the point of the most efficient portfolio and the risk free rate of returns associated

with that portfolio. The tangent that passes through the efficient portfolio is the Capital Asset

Line. By efficient portfolio it is meant by the combination of the risky and risk free assets

that a person can buy which will maximize the sharp ratio. In Figure 1 the tangent passing

through the most efficient portfolio is the Capital Market Line. In contrast to that the slope of

the Security Market Line shows the volatility of the risk associated to an individual assets or

of all the portfolios which include inefficient ones. The β that is said in the above equation of

the Security Market Line is the major concern. Beta represents the measure of the changes in

security’s sensitivity with respect to that of the market returns and also the slope of the

Security Market Line. Often beta is considered as a more appropriate measure for the security

risk.

r f = risk free rate of return

βi = volatility of the ith individual asset

rm= average return on capital market

The above is the equation of the Security Market Line with β portfolio.

From the two diagrams provided below it can be seen that the Capital Market Line is

the locus of the point of the most efficient portfolio and the risk free rate of returns associated

with that portfolio. The tangent that passes through the efficient portfolio is the Capital Asset

Line. By efficient portfolio it is meant by the combination of the risky and risk free assets

that a person can buy which will maximize the sharp ratio. In Figure 1 the tangent passing

through the most efficient portfolio is the Capital Market Line. In contrast to that the slope of

the Security Market Line shows the volatility of the risk associated to an individual assets or

of all the portfolios which include inefficient ones. The β that is said in the above equation of

the Security Market Line is the major concern. Beta represents the measure of the changes in

security’s sensitivity with respect to that of the market returns and also the slope of the

Security Market Line. Often beta is considered as a more appropriate measure for the security

risk.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE FINANCE MANAGEMENT

Return Return

Risk β

CML

Efficient Portfolio

1

SML

Figure 1: CML vs SML

Source: By the Author

Answer to part (B)

The Modern Portfolio Theory (MPT) tries to minimize the risks (which can be also

termed as the variance, standard deviation or volatility) that is associated with a portfolio or

an asset without reducing the mean or the expected returns form that asset. Consider that

there are two assets P and Q. Consider that they have equal variance of 10 percent. Now, a

portfolio that consists of both of the above said articles will tend to have a standard deviation

or volatility lower than then original 10 percent. Somehow if the assets are correlated then the

volatility may be greater than 10 percent. The main aim or the main goal of minimizing the

risks is attained by varying the weights of the corresponding portfolios. Further, another

important fact is that the securities cannot be selected as per the individual characteristics, as

the correlation between these securities also needs to be taken into account as lower the level

of correlation between the assets the stronger is the level of diversification. A unique

portfolio can be derived for each level of expected return which has lowest risk. These

portfolios are called mean-variance efficient portfolios as any other combination of such

portfolios do not possess such low risks and the level of expected returns. There the set of all

Return Return

Risk β

CML

Efficient Portfolio

1

SML

Figure 1: CML vs SML

Source: By the Author

Answer to part (B)

The Modern Portfolio Theory (MPT) tries to minimize the risks (which can be also

termed as the variance, standard deviation or volatility) that is associated with a portfolio or

an asset without reducing the mean or the expected returns form that asset. Consider that

there are two assets P and Q. Consider that they have equal variance of 10 percent. Now, a

portfolio that consists of both of the above said articles will tend to have a standard deviation

or volatility lower than then original 10 percent. Somehow if the assets are correlated then the

volatility may be greater than 10 percent. The main aim or the main goal of minimizing the

risks is attained by varying the weights of the corresponding portfolios. Further, another

important fact is that the securities cannot be selected as per the individual characteristics, as

the correlation between these securities also needs to be taken into account as lower the level

of correlation between the assets the stronger is the level of diversification. A unique

portfolio can be derived for each level of expected return which has lowest risk. These

portfolios are called mean-variance efficient portfolios as any other combination of such

portfolios do not possess such low risks and the level of expected returns. There the set of all

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE FINANCE MANAGEMENT

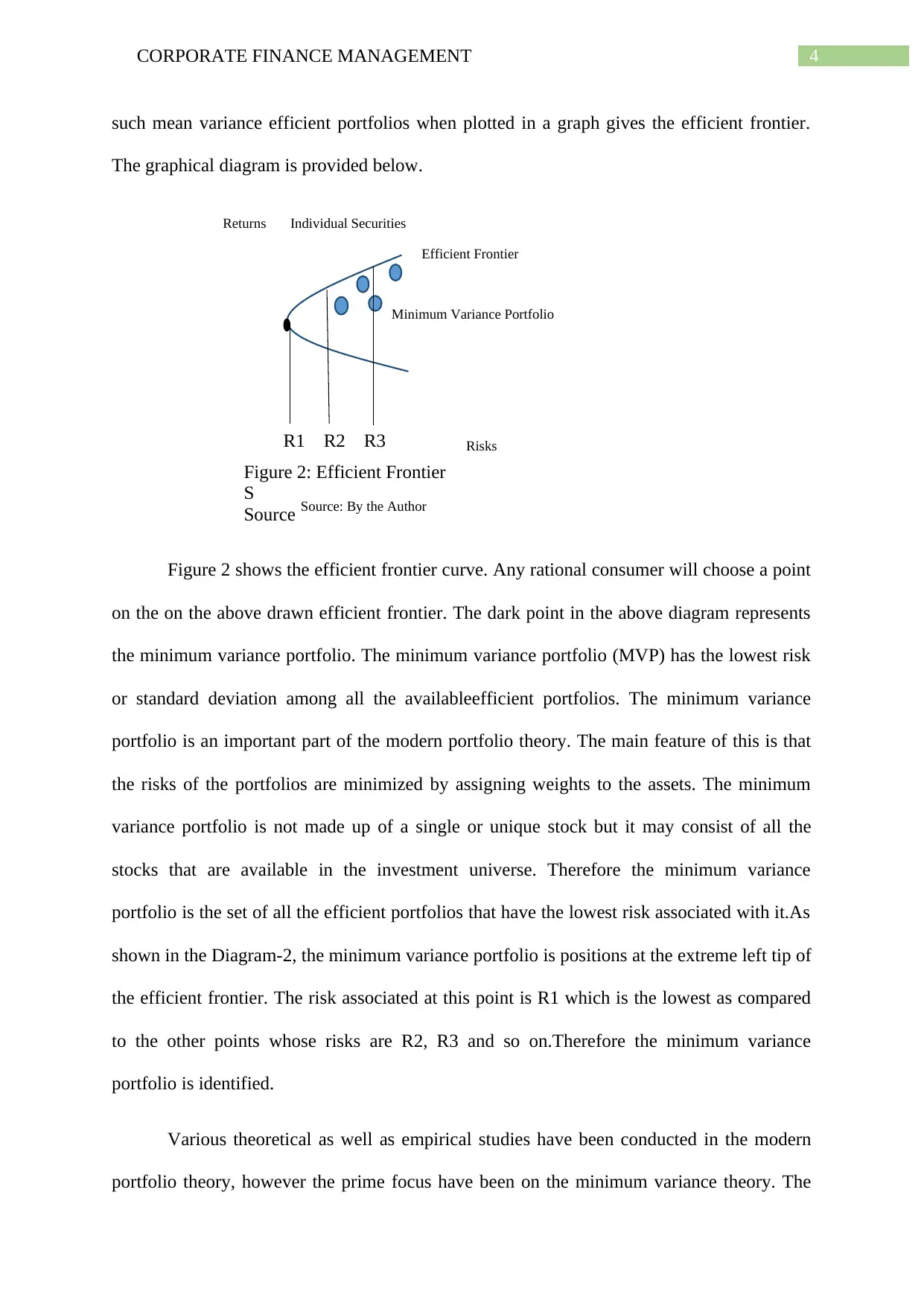

Returns

Risks

Minimum Variance Portfolio

Efficient Frontier

Individual Securities

Figure 2: Efficient Frontier

S

Source

R1 R2 R3

Source: By the Author

such mean variance efficient portfolios when plotted in a graph gives the efficient frontier.

The graphical diagram is provided below.

Figure 2 shows the efficient frontier curve. Any rational consumer will choose a point

on the on the above drawn efficient frontier. The dark point in the above diagram represents

the minimum variance portfolio. The minimum variance portfolio (MVP) has the lowest risk

or standard deviation among all the availableefficient portfolios. The minimum variance

portfolio is an important part of the modern portfolio theory. The main feature of this is that

the risks of the portfolios are minimized by assigning weights to the assets. The minimum

variance portfolio is not made up of a single or unique stock but it may consist of all the

stocks that are available in the investment universe. Therefore the minimum variance

portfolio is the set of all the efficient portfolios that have the lowest risk associated with it.As

shown in the Diagram-2, the minimum variance portfolio is positions at the extreme left tip of

the efficient frontier. The risk associated at this point is R1 which is the lowest as compared

to the other points whose risks are R2, R3 and so on.Therefore the minimum variance

portfolio is identified.

Various theoretical as well as empirical studies have been conducted in the modern

portfolio theory, however the prime focus have been on the minimum variance theory. The

Returns

Risks

Minimum Variance Portfolio

Efficient Frontier

Individual Securities

Figure 2: Efficient Frontier

S

Source

R1 R2 R3

Source: By the Author

such mean variance efficient portfolios when plotted in a graph gives the efficient frontier.

The graphical diagram is provided below.

Figure 2 shows the efficient frontier curve. Any rational consumer will choose a point

on the on the above drawn efficient frontier. The dark point in the above diagram represents

the minimum variance portfolio. The minimum variance portfolio (MVP) has the lowest risk

or standard deviation among all the availableefficient portfolios. The minimum variance

portfolio is an important part of the modern portfolio theory. The main feature of this is that

the risks of the portfolios are minimized by assigning weights to the assets. The minimum

variance portfolio is not made up of a single or unique stock but it may consist of all the

stocks that are available in the investment universe. Therefore the minimum variance

portfolio is the set of all the efficient portfolios that have the lowest risk associated with it.As

shown in the Diagram-2, the minimum variance portfolio is positions at the extreme left tip of

the efficient frontier. The risk associated at this point is R1 which is the lowest as compared

to the other points whose risks are R2, R3 and so on.Therefore the minimum variance

portfolio is identified.

Various theoretical as well as empirical studies have been conducted in the modern

portfolio theory, however the prime focus have been on the minimum variance theory. The

5CORPORATE FINANCE MANAGEMENT

importance of the minimum variance portfolio can be described as follows. There exists a

large number of companies who are running their investment funds strategy that are solely

based on the minimum variance optimization. Further, the minimum variance theory has also

drawn attention of the stock exchange. The index providers are also benefited from the

minimum variance theory. There exists three reasons for the prevalence of the minimum

variance portfolio. Firstly most of the empirical studies that has been conducted till date

shows that the minimum variance portfolio has performed relatively well than any other

indexes. Secondly, when the optimization is conducted, the optimization of minimum

variance portfolio does not require considering the expected returns forecasts. In other words

the optimization is independent from the expected returns forecast. These expected returns

forecast are the major source of errors that arise due to estimation. Lastly, it has been seen

that the participant in the market are primarily risk averse in nature. This phenomenon

stimulates the creation of the financial products with a managed volatility. In this case the

minimum variance theory serves to the needs of the investors.

Answer to part (C)

The Capital Asset Pricing Model (CAPM) establishes a linear relationship between

the required rates of return and the systematic risk associated with that investment. This

investment might be in the form stock market securities or in the form of business operation.

The Capital Asset Pricing Model incorporates the Security Market Line concept. The general

equation of the model is,

ri−rf =βi (rm−r f )

ri=rf + βi (r m−r f )

Where, ri = required rate of return on the ith individual financial asset

r f = risk free rate of return

importance of the minimum variance portfolio can be described as follows. There exists a

large number of companies who are running their investment funds strategy that are solely

based on the minimum variance optimization. Further, the minimum variance theory has also

drawn attention of the stock exchange. The index providers are also benefited from the

minimum variance theory. There exists three reasons for the prevalence of the minimum

variance portfolio. Firstly most of the empirical studies that has been conducted till date

shows that the minimum variance portfolio has performed relatively well than any other

indexes. Secondly, when the optimization is conducted, the optimization of minimum

variance portfolio does not require considering the expected returns forecasts. In other words

the optimization is independent from the expected returns forecast. These expected returns

forecast are the major source of errors that arise due to estimation. Lastly, it has been seen

that the participant in the market are primarily risk averse in nature. This phenomenon

stimulates the creation of the financial products with a managed volatility. In this case the

minimum variance theory serves to the needs of the investors.

Answer to part (C)

The Capital Asset Pricing Model (CAPM) establishes a linear relationship between

the required rates of return and the systematic risk associated with that investment. This

investment might be in the form stock market securities or in the form of business operation.

The Capital Asset Pricing Model incorporates the Security Market Line concept. The general

equation of the model is,

ri−rf =βi (rm−r f )

ri=rf + βi (r m−r f )

Where, ri = required rate of return on the ith individual financial asset

r f = risk free rate of return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE FINANCE MANAGEMENT

βi = volatility of the ith individual asset

rm= average return on capital market

The Capital Asset Model has an upper advantage and is more relevant than any other

equation while calculating the required rate of return. While calculating the rate of return the

Capital Asset Pricing Model model considers only the systematic risk. The systematic risks

are those risks that cannot be diversified. These systematic risks are caused due to external

factors occurring to an organisation. These risks cannot be controlled by nature. The beta that

is used in the Capital Asset Pricing Model takes into account these systematic risks. In any

other model these are not included. This fact is quite realistic as most of the investors have a

diversified portfolio and the unsystematic risks associated with these portfolios are essentially

eliminated. Another factor that can be stated relating to the relevance of the Capital Asset

Pricing Model equation is that the model generates a theoretical relationship between the

required return rates and the systematic risks associated with the assets which is a matter of

frequent discussion. The equation when implied in real life scenario has a great relevance.

The Dividend Growth Model (DGM) that also tries to calculate the return rates but, the

Capital Asset Pricing Model is far more superior. The Dividend Growth Model assumes that

the rate of growth of dividends is constant in perpetuity. The value of the stock is equal to the

following year’s dividends divided by difference between the required rate of return and the

constant growth rate in dividends that is assumed (McKenzie and Partington 2013).the model

is further divided into two categories the stable model and the multistage growth model. The

equation for the stable model can be represented as follows:

P= d1

k −g , where, P = value of stock, d1 is the next year’s dividends, k = rate of return

and g is the constant rate of growth. The Dividend Growth Model explicitly takes into

account the company’s level of the systematic risks relative to that of the stock as a whole.

βi = volatility of the ith individual asset

rm= average return on capital market

The Capital Asset Model has an upper advantage and is more relevant than any other

equation while calculating the required rate of return. While calculating the rate of return the

Capital Asset Pricing Model model considers only the systematic risk. The systematic risks

are those risks that cannot be diversified. These systematic risks are caused due to external

factors occurring to an organisation. These risks cannot be controlled by nature. The beta that

is used in the Capital Asset Pricing Model takes into account these systematic risks. In any

other model these are not included. This fact is quite realistic as most of the investors have a

diversified portfolio and the unsystematic risks associated with these portfolios are essentially

eliminated. Another factor that can be stated relating to the relevance of the Capital Asset

Pricing Model equation is that the model generates a theoretical relationship between the

required return rates and the systematic risks associated with the assets which is a matter of

frequent discussion. The equation when implied in real life scenario has a great relevance.

The Dividend Growth Model (DGM) that also tries to calculate the return rates but, the

Capital Asset Pricing Model is far more superior. The Dividend Growth Model assumes that

the rate of growth of dividends is constant in perpetuity. The value of the stock is equal to the

following year’s dividends divided by difference between the required rate of return and the

constant growth rate in dividends that is assumed (McKenzie and Partington 2013).the model

is further divided into two categories the stable model and the multistage growth model. The

equation for the stable model can be represented as follows:

P= d1

k −g , where, P = value of stock, d1 is the next year’s dividends, k = rate of return

and g is the constant rate of growth. The Dividend Growth Model explicitly takes into

account the company’s level of the systematic risks relative to that of the stock as a whole.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE FINANCE MANAGEMENT

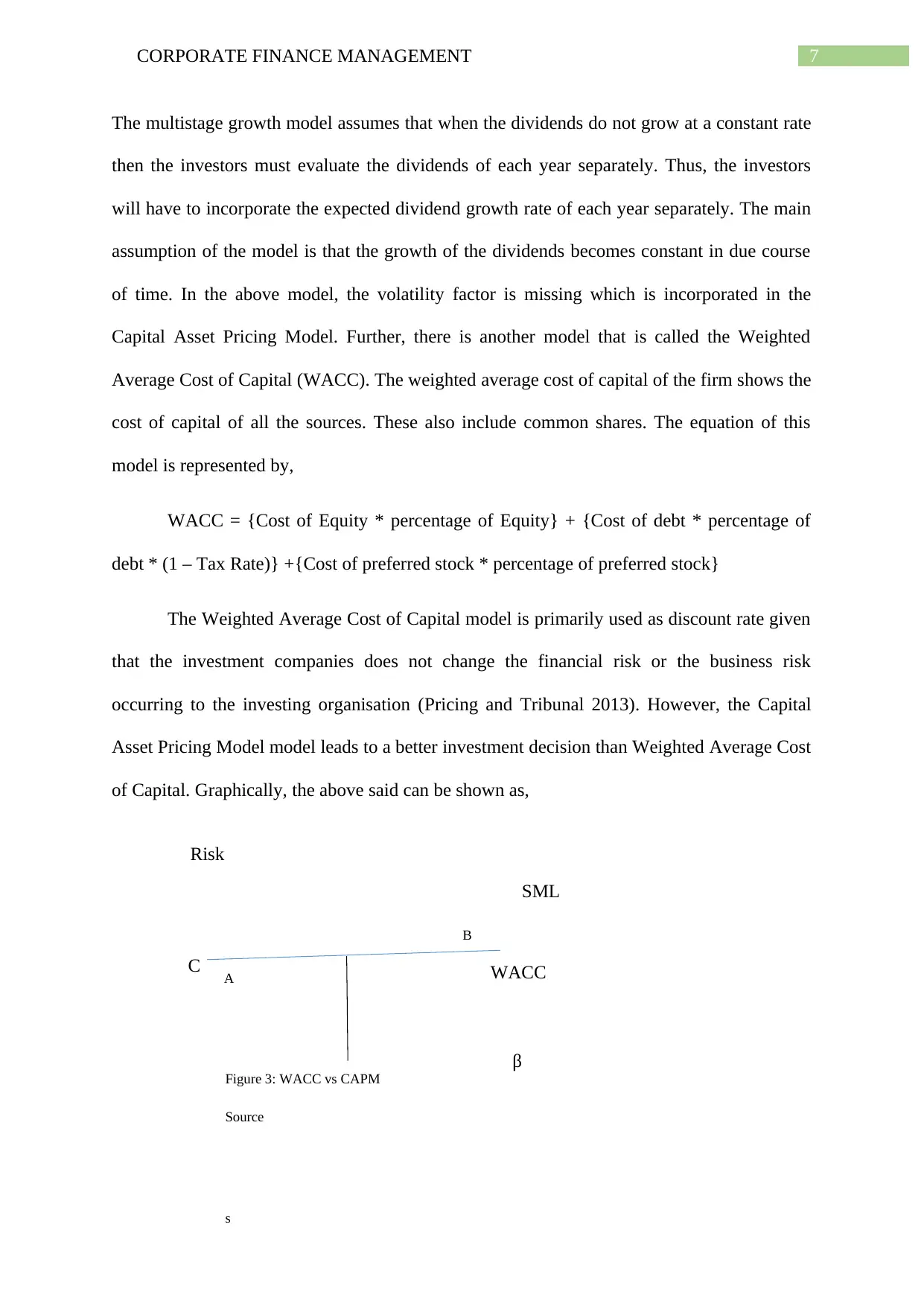

B

A

C

SML

WACC

Risk

β

Figure 3: WACC vs CAPM

Source

s

The multistage growth model assumes that when the dividends do not grow at a constant rate

then the investors must evaluate the dividends of each year separately. Thus, the investors

will have to incorporate the expected dividend growth rate of each year separately. The main

assumption of the model is that the growth of the dividends becomes constant in due course

of time. In the above model, the volatility factor is missing which is incorporated in the

Capital Asset Pricing Model. Further, there is another model that is called the Weighted

Average Cost of Capital (WACC). The weighted average cost of capital of the firm shows the

cost of capital of all the sources. These also include common shares. The equation of this

model is represented by,

WACC = {Cost of Equity * percentage of Equity} + {Cost of debt * percentage of

debt * (1 – Tax Rate)} +{Cost of preferred stock * percentage of preferred stock}

The Weighted Average Cost of Capital model is primarily used as discount rate given

that the investment companies does not change the financial risk or the business risk

occurring to the investing organisation (Pricing and Tribunal 2013). However, the Capital

Asset Pricing Model model leads to a better investment decision than Weighted Average Cost

of Capital. Graphically, the above said can be shown as,

B

A

C

SML

WACC

Risk

β

Figure 3: WACC vs CAPM

Source

s

The multistage growth model assumes that when the dividends do not grow at a constant rate

then the investors must evaluate the dividends of each year separately. Thus, the investors

will have to incorporate the expected dividend growth rate of each year separately. The main

assumption of the model is that the growth of the dividends becomes constant in due course

of time. In the above model, the volatility factor is missing which is incorporated in the

Capital Asset Pricing Model. Further, there is another model that is called the Weighted

Average Cost of Capital (WACC). The weighted average cost of capital of the firm shows the

cost of capital of all the sources. These also include common shares. The equation of this

model is represented by,

WACC = {Cost of Equity * percentage of Equity} + {Cost of debt * percentage of

debt * (1 – Tax Rate)} +{Cost of preferred stock * percentage of preferred stock}

The Weighted Average Cost of Capital model is primarily used as discount rate given

that the investment companies does not change the financial risk or the business risk

occurring to the investing organisation (Pricing and Tribunal 2013). However, the Capital

Asset Pricing Model model leads to a better investment decision than Weighted Average Cost

of Capital. Graphically, the above said can be shown as,

8CORPORATE FINANCE MANAGEMENT

From the diagram, point A is not feasible in case of Weighted Average Cost of

Capital as the internal rate of return is less than the Weighted Average Cost of Capital

intercept C whereas if Capital Asset Pricing Model would have been considered then, A

would have been a feasible option. Similarly, for point B, it would have been feasible for

Weighted Average Cost of Capital. The point B is has a rate of return much higher than the

internal rate of return. Thus, considering the Weighted Average Cost of Capital model this

point B would have been feasible. However, when Capital Asset Pricing Model is considered

then this point is not all a feasible point. Point B provides insufficient compensations for the

level of systematic risks. There it can be clearly how the Capital Asset Pricing Model is far

superior than any of the existing theories.

From the diagram, point A is not feasible in case of Weighted Average Cost of

Capital as the internal rate of return is less than the Weighted Average Cost of Capital

intercept C whereas if Capital Asset Pricing Model would have been considered then, A

would have been a feasible option. Similarly, for point B, it would have been feasible for

Weighted Average Cost of Capital. The point B is has a rate of return much higher than the

internal rate of return. Thus, considering the Weighted Average Cost of Capital model this

point B would have been feasible. However, when Capital Asset Pricing Model is considered

then this point is not all a feasible point. Point B provides insufficient compensations for the

level of systematic risks. There it can be clearly how the Capital Asset Pricing Model is far

superior than any of the existing theories.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE FINANCE MANAGEMENT

Reference

McKenzie, M. and Partington, G., 2013. The dividend growth model (DGM). Report to the

AER.

Pricing, I. and Tribunal, R., 2013. Review of WACC methodology. Research–Final report.

Reference

McKenzie, M. and Partington, G., 2013. The dividend growth model (DGM). Report to the

AER.

Pricing, I. and Tribunal, R., 2013. Review of WACC methodology. Research–Final report.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.