Corporate Finance: Risk and Return Analysis

VerifiedAdded on 2023/03/29

|12

|2833

|485

AI Summary

This document provides an overview of risk and return analysis in corporate finance. It covers topics such as calculating expected rate of return and standard deviation, understanding the reasons for different risk and return profiles among similar companies, and exploring methods for calculating cost of equity. The document also discusses the concept of efficient market hypothesis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

CORPORATE FINANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

1Calculation of expected rate of return and standard deviation of expected return....................3

2 Reasons due to which similar companies have different risk and return profile......................4

3 Plotting of risk and return of portfolio and optimum portfolio.................................................4

4 Identifying whether addition of RFR to optimum portfolio is prudent decision......................6

Question 2........................................................................................................................................8

Two appropriate methods for calculating cost of equity.............................................................8

Calculation of Astringency capital structure................................................................................9

Estimate of weighted average cost of capital.............................................................................10

Question 3......................................................................................................................................11

Efficient market hypothesis.......................................................................................................11

CONCLUSION..............................................................................................................................11

REFERNECES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

1Calculation of expected rate of return and standard deviation of expected return....................3

2 Reasons due to which similar companies have different risk and return profile......................4

3 Plotting of risk and return of portfolio and optimum portfolio.................................................4

4 Identifying whether addition of RFR to optimum portfolio is prudent decision......................6

Question 2........................................................................................................................................8

Two appropriate methods for calculating cost of equity.............................................................8

Calculation of Astringency capital structure................................................................................9

Estimate of weighted average cost of capital.............................................................................10

Question 3......................................................................................................................................11

Efficient market hypothesis.......................................................................................................11

CONCLUSION..............................................................................................................................11

REFERNECES..............................................................................................................................12

INTRODUCTION

Corporate finance is the one of the most important domain that heavily influence the

individual decision making process in respect to investment in securities. In the current report,

varied calculations are performed like expected return and standard deviation for portfolio and

for individual securities. Apart from this, in the report changes that can be observed in return of

portfolio after addition of risk free asset is also reflected. Significance of making investment in

risk free asset is discussed briefly. At end of the report, efficient market hypothesis concept is

explained.

Question 1

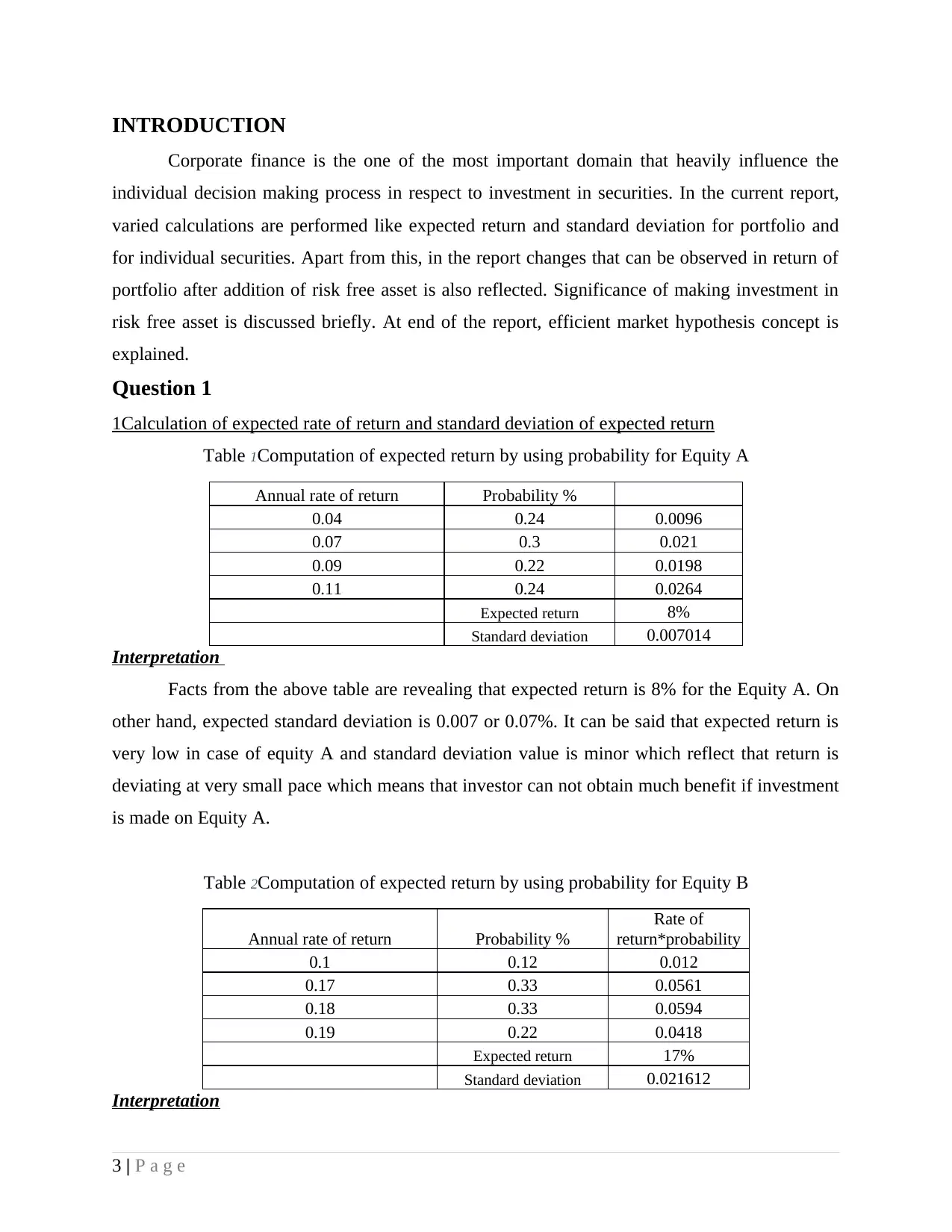

1Calculation of expected rate of return and standard deviation of expected return

Table 1Computation of expected return by using probability for Equity A

Annual rate of return Probability %

0.04 0.24 0.0096

0.07 0.3 0.021

0.09 0.22 0.0198

0.11 0.24 0.0264

Expected return 8%

Standard deviation 0.007014

Interpretation

Facts from the above table are revealing that expected return is 8% for the Equity A. On

other hand, expected standard deviation is 0.007 or 0.07%. It can be said that expected return is

very low in case of equity A and standard deviation value is minor which reflect that return is

deviating at very small pace which means that investor can not obtain much benefit if investment

is made on Equity A.

Table 2Computation of expected return by using probability for Equity B

Annual rate of return Probability %

Rate of

return*probability

0.1 0.12 0.012

0.17 0.33 0.0561

0.18 0.33 0.0594

0.19 0.22 0.0418

Expected return 17%

Standard deviation 0.021612

Interpretation

3 | P a g e

Corporate finance is the one of the most important domain that heavily influence the

individual decision making process in respect to investment in securities. In the current report,

varied calculations are performed like expected return and standard deviation for portfolio and

for individual securities. Apart from this, in the report changes that can be observed in return of

portfolio after addition of risk free asset is also reflected. Significance of making investment in

risk free asset is discussed briefly. At end of the report, efficient market hypothesis concept is

explained.

Question 1

1Calculation of expected rate of return and standard deviation of expected return

Table 1Computation of expected return by using probability for Equity A

Annual rate of return Probability %

0.04 0.24 0.0096

0.07 0.3 0.021

0.09 0.22 0.0198

0.11 0.24 0.0264

Expected return 8%

Standard deviation 0.007014

Interpretation

Facts from the above table are revealing that expected return is 8% for the Equity A. On

other hand, expected standard deviation is 0.007 or 0.07%. It can be said that expected return is

very low in case of equity A and standard deviation value is minor which reflect that return is

deviating at very small pace which means that investor can not obtain much benefit if investment

is made on Equity A.

Table 2Computation of expected return by using probability for Equity B

Annual rate of return Probability %

Rate of

return*probability

0.1 0.12 0.012

0.17 0.33 0.0561

0.18 0.33 0.0594

0.19 0.22 0.0418

Expected return 17%

Standard deviation 0.021612

Interpretation

3 | P a g e

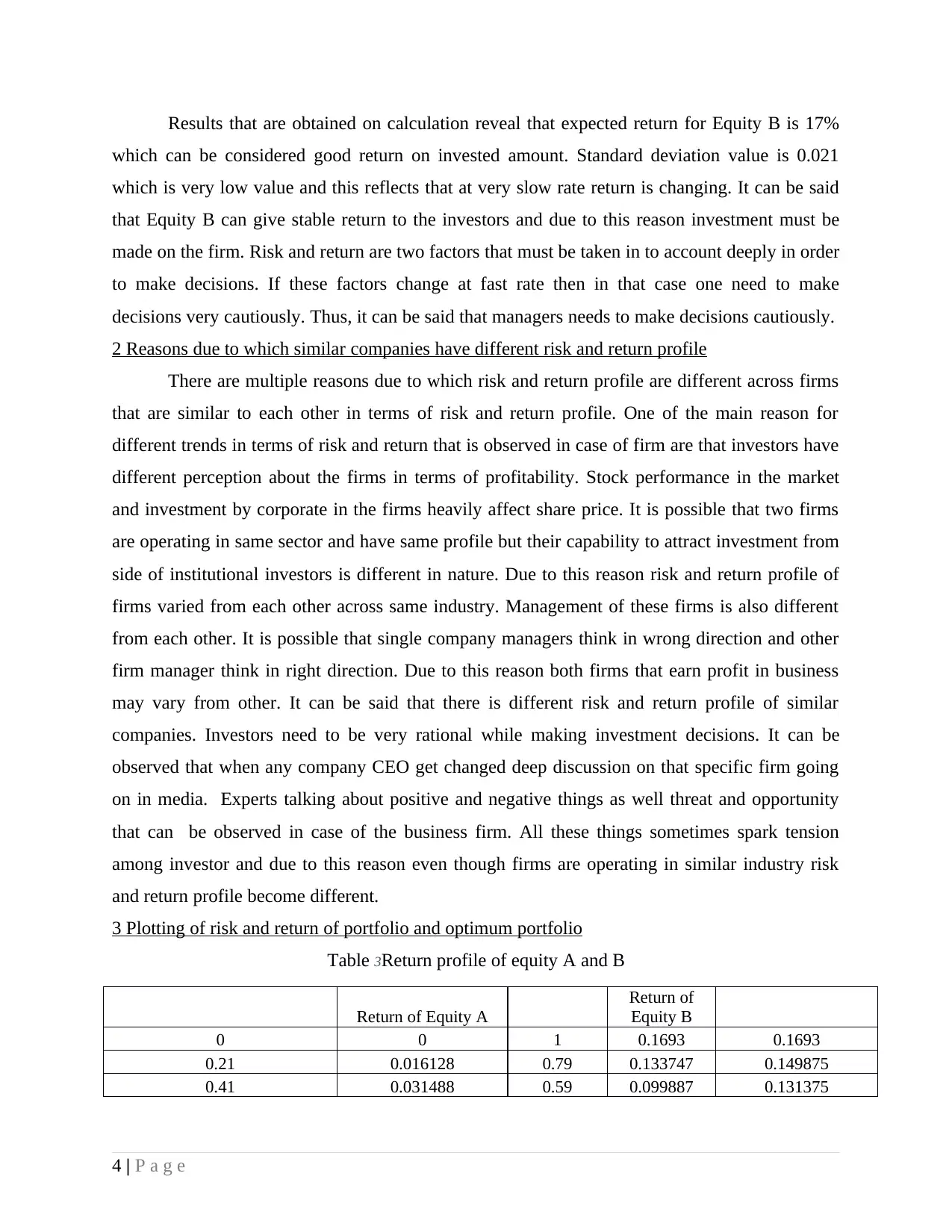

Results that are obtained on calculation reveal that expected return for Equity B is 17%

which can be considered good return on invested amount. Standard deviation value is 0.021

which is very low value and this reflects that at very slow rate return is changing. It can be said

that Equity B can give stable return to the investors and due to this reason investment must be

made on the firm. Risk and return are two factors that must be taken in to account deeply in order

to make decisions. If these factors change at fast rate then in that case one need to make

decisions very cautiously. Thus, it can be said that managers needs to make decisions cautiously.

2 Reasons due to which similar companies have different risk and return profile

There are multiple reasons due to which risk and return profile are different across firms

that are similar to each other in terms of risk and return profile. One of the main reason for

different trends in terms of risk and return that is observed in case of firm are that investors have

different perception about the firms in terms of profitability. Stock performance in the market

and investment by corporate in the firms heavily affect share price. It is possible that two firms

are operating in same sector and have same profile but their capability to attract investment from

side of institutional investors is different in nature. Due to this reason risk and return profile of

firms varied from each other across same industry. Management of these firms is also different

from each other. It is possible that single company managers think in wrong direction and other

firm manager think in right direction. Due to this reason both firms that earn profit in business

may vary from other. It can be said that there is different risk and return profile of similar

companies. Investors need to be very rational while making investment decisions. It can be

observed that when any company CEO get changed deep discussion on that specific firm going

on in media. Experts talking about positive and negative things as well threat and opportunity

that can be observed in case of the business firm. All these things sometimes spark tension

among investor and due to this reason even though firms are operating in similar industry risk

and return profile become different.

3 Plotting of risk and return of portfolio and optimum portfolio

Table 3Return profile of equity A and B

Return of Equity A

Return of

Equity B

0 0 1 0.1693 0.1693

0.21 0.016128 0.79 0.133747 0.149875

0.41 0.031488 0.59 0.099887 0.131375

4 | P a g e

which can be considered good return on invested amount. Standard deviation value is 0.021

which is very low value and this reflects that at very slow rate return is changing. It can be said

that Equity B can give stable return to the investors and due to this reason investment must be

made on the firm. Risk and return are two factors that must be taken in to account deeply in order

to make decisions. If these factors change at fast rate then in that case one need to make

decisions very cautiously. Thus, it can be said that managers needs to make decisions cautiously.

2 Reasons due to which similar companies have different risk and return profile

There are multiple reasons due to which risk and return profile are different across firms

that are similar to each other in terms of risk and return profile. One of the main reason for

different trends in terms of risk and return that is observed in case of firm are that investors have

different perception about the firms in terms of profitability. Stock performance in the market

and investment by corporate in the firms heavily affect share price. It is possible that two firms

are operating in same sector and have same profile but their capability to attract investment from

side of institutional investors is different in nature. Due to this reason risk and return profile of

firms varied from each other across same industry. Management of these firms is also different

from each other. It is possible that single company managers think in wrong direction and other

firm manager think in right direction. Due to this reason both firms that earn profit in business

may vary from other. It can be said that there is different risk and return profile of similar

companies. Investors need to be very rational while making investment decisions. It can be

observed that when any company CEO get changed deep discussion on that specific firm going

on in media. Experts talking about positive and negative things as well threat and opportunity

that can be observed in case of the business firm. All these things sometimes spark tension

among investor and due to this reason even though firms are operating in similar industry risk

and return profile become different.

3 Plotting of risk and return of portfolio and optimum portfolio

Table 3Return profile of equity A and B

Return of Equity A

Return of

Equity B

0 0 1 0.1693 0.1693

0.21 0.016128 0.79 0.133747 0.149875

0.41 0.031488 0.59 0.099887 0.131375

4 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

0.61 0.046848 0.39 0.066027 0.112875

0.81 0.062208 0.19 0.032167 0.094375

Table 4Standard deviation of Equity B

STDEV of Equity A

STDEV of

Equity B

0 0 1 0.021612 0.021611629

0.21 0.001472997 0.79 0.017073 0.018546184

0.41 0.002875851 0.59 0.012751 0.015626712

0.61 0.004278705 0.39 0.008429 0.012707241

0.81 0.00568156 0.19 0.004106 0.009787769

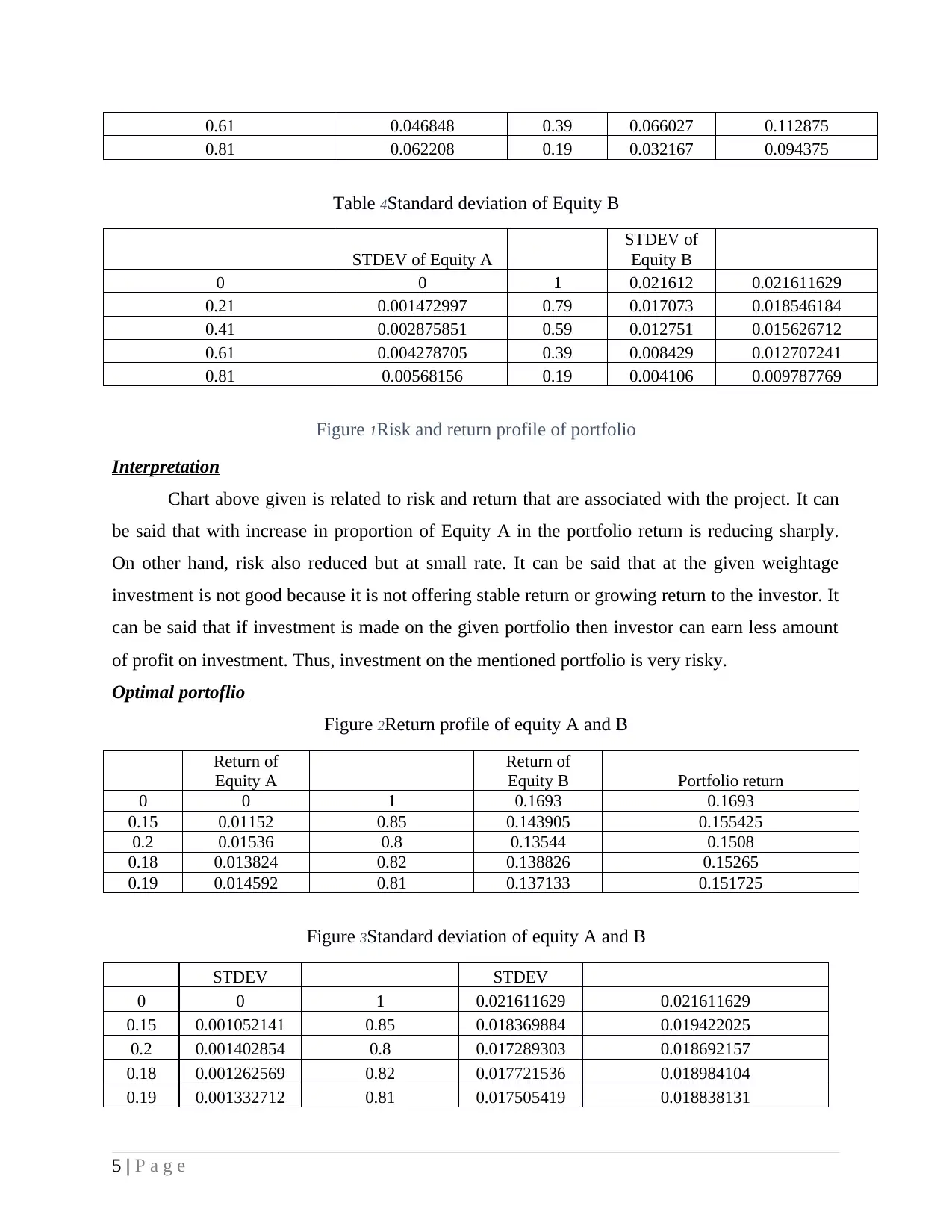

Figure 1Risk and return profile of portfolio

Interpretation

Chart above given is related to risk and return that are associated with the project. It can

be said that with increase in proportion of Equity A in the portfolio return is reducing sharply.

On other hand, risk also reduced but at small rate. It can be said that at the given weightage

investment is not good because it is not offering stable return or growing return to the investor. It

can be said that if investment is made on the given portfolio then investor can earn less amount

of profit on investment. Thus, investment on the mentioned portfolio is very risky.

Optimal portoflio

Figure 2Return profile of equity A and B

Return of

Equity A

Return of

Equity B Portfolio return

0 0 1 0.1693 0.1693

0.15 0.01152 0.85 0.143905 0.155425

0.2 0.01536 0.8 0.13544 0.1508

0.18 0.013824 0.82 0.138826 0.15265

0.19 0.014592 0.81 0.137133 0.151725

Figure 3Standard deviation of equity A and B

STDEV STDEV

0 0 1 0.021611629 0.021611629

0.15 0.001052141 0.85 0.018369884 0.019422025

0.2 0.001402854 0.8 0.017289303 0.018692157

0.18 0.001262569 0.82 0.017721536 0.018984104

0.19 0.001332712 0.81 0.017505419 0.018838131

5 | P a g e

0.81 0.062208 0.19 0.032167 0.094375

Table 4Standard deviation of Equity B

STDEV of Equity A

STDEV of

Equity B

0 0 1 0.021612 0.021611629

0.21 0.001472997 0.79 0.017073 0.018546184

0.41 0.002875851 0.59 0.012751 0.015626712

0.61 0.004278705 0.39 0.008429 0.012707241

0.81 0.00568156 0.19 0.004106 0.009787769

Figure 1Risk and return profile of portfolio

Interpretation

Chart above given is related to risk and return that are associated with the project. It can

be said that with increase in proportion of Equity A in the portfolio return is reducing sharply.

On other hand, risk also reduced but at small rate. It can be said that at the given weightage

investment is not good because it is not offering stable return or growing return to the investor. It

can be said that if investment is made on the given portfolio then investor can earn less amount

of profit on investment. Thus, investment on the mentioned portfolio is very risky.

Optimal portoflio

Figure 2Return profile of equity A and B

Return of

Equity A

Return of

Equity B Portfolio return

0 0 1 0.1693 0.1693

0.15 0.01152 0.85 0.143905 0.155425

0.2 0.01536 0.8 0.13544 0.1508

0.18 0.013824 0.82 0.138826 0.15265

0.19 0.014592 0.81 0.137133 0.151725

Figure 3Standard deviation of equity A and B

STDEV STDEV

0 0 1 0.021611629 0.021611629

0.15 0.001052141 0.85 0.018369884 0.019422025

0.2 0.001402854 0.8 0.017289303 0.018692157

0.18 0.001262569 0.82 0.017721536 0.018984104

0.19 0.001332712 0.81 0.017505419 0.018838131

5 | P a g e

Table 5Revised return and risk portfolio

Return of portfolio

Risk in

portfolio

0.1693 0.021611629

0.149875 0.018546184

0.131375 0.015626712

0.112875 0.012707241

0.094375 0.009787769

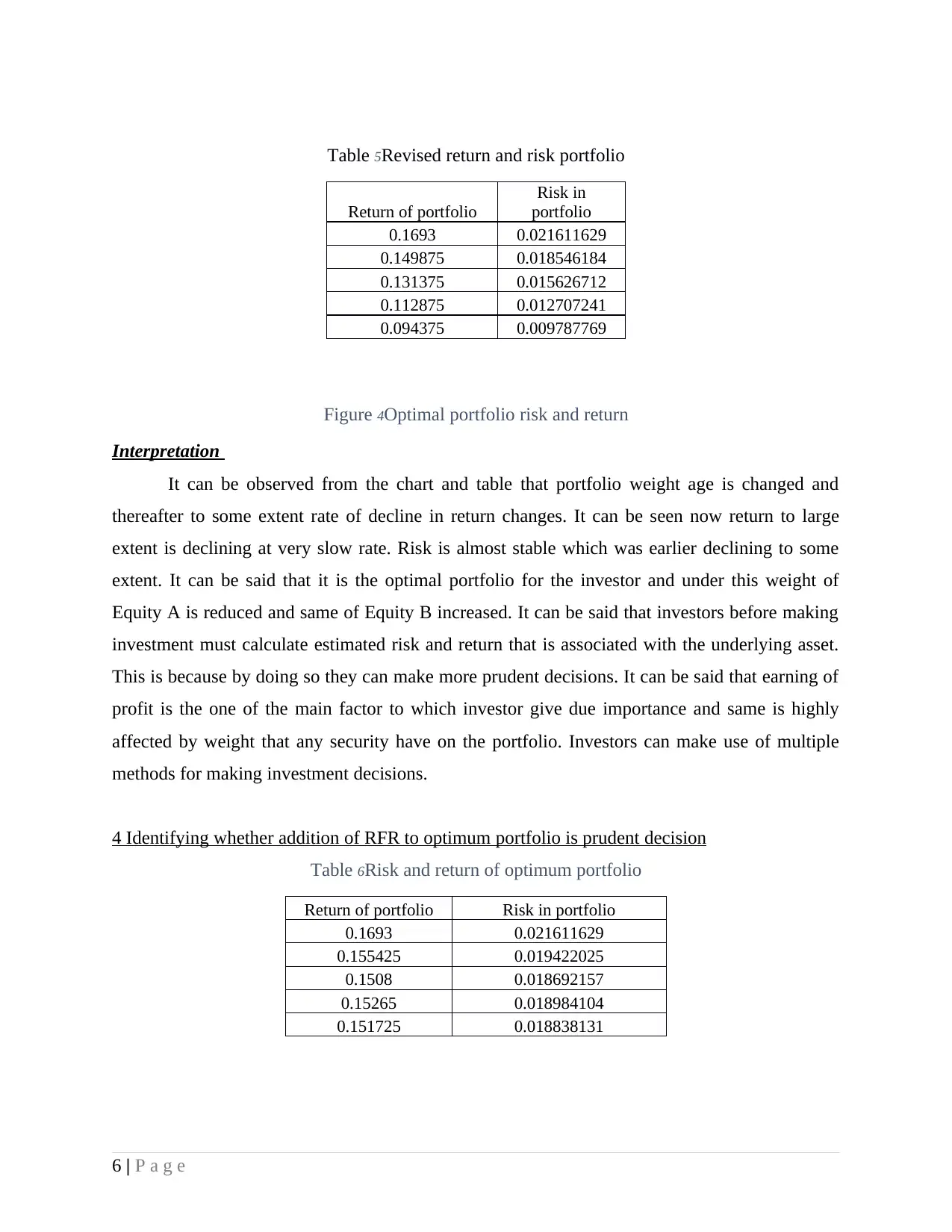

Figure 4Optimal portfolio risk and return

Interpretation

It can be observed from the chart and table that portfolio weight age is changed and

thereafter to some extent rate of decline in return changes. It can be seen now return to large

extent is declining at very slow rate. Risk is almost stable which was earlier declining to some

extent. It can be said that it is the optimal portfolio for the investor and under this weight of

Equity A is reduced and same of Equity B increased. It can be said that investors before making

investment must calculate estimated risk and return that is associated with the underlying asset.

This is because by doing so they can make more prudent decisions. It can be said that earning of

profit is the one of the main factor to which investor give due importance and same is highly

affected by weight that any security have on the portfolio. Investors can make use of multiple

methods for making investment decisions.

4 Identifying whether addition of RFR to optimum portfolio is prudent decision

Table 6Risk and return of optimum portfolio

Return of portfolio Risk in portfolio

0.1693 0.021611629

0.155425 0.019422025

0.1508 0.018692157

0.15265 0.018984104

0.151725 0.018838131

6 | P a g e

Return of portfolio

Risk in

portfolio

0.1693 0.021611629

0.149875 0.018546184

0.131375 0.015626712

0.112875 0.012707241

0.094375 0.009787769

Figure 4Optimal portfolio risk and return

Interpretation

It can be observed from the chart and table that portfolio weight age is changed and

thereafter to some extent rate of decline in return changes. It can be seen now return to large

extent is declining at very slow rate. Risk is almost stable which was earlier declining to some

extent. It can be said that it is the optimal portfolio for the investor and under this weight of

Equity A is reduced and same of Equity B increased. It can be said that investors before making

investment must calculate estimated risk and return that is associated with the underlying asset.

This is because by doing so they can make more prudent decisions. It can be said that earning of

profit is the one of the main factor to which investor give due importance and same is highly

affected by weight that any security have on the portfolio. Investors can make use of multiple

methods for making investment decisions.

4 Identifying whether addition of RFR to optimum portfolio is prudent decision

Table 6Risk and return of optimum portfolio

Return of portfolio Risk in portfolio

0.1693 0.021611629

0.155425 0.019422025

0.1508 0.018692157

0.15265 0.018984104

0.151725 0.018838131

6 | P a g e

Table 7Return of portfolio and change in return after addition of RFR

Return of

portfolio

Risk free rate of

return

Summation of

return

Increase in return after addition of

RFR asset

16.930% 5% 21.930% 5%

15.543% 5% 20.543% 5%

15.080% 5% 20.080% 5%

15.265% 5% 20.265% 5%

15.173% 5% 20.173% 5%

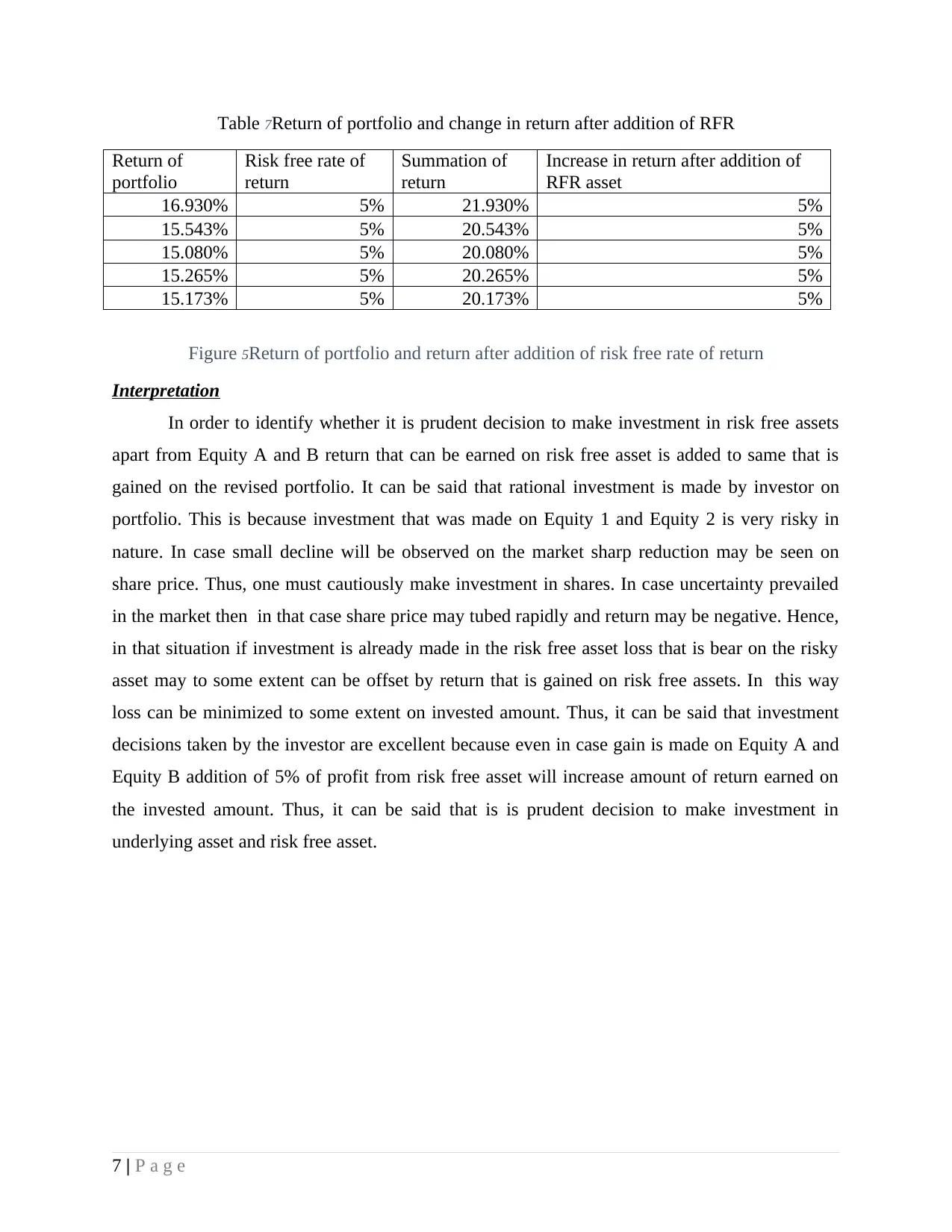

Figure 5Return of portfolio and return after addition of risk free rate of return

Interpretation

In order to identify whether it is prudent decision to make investment in risk free assets

apart from Equity A and B return that can be earned on risk free asset is added to same that is

gained on the revised portfolio. It can be said that rational investment is made by investor on

portfolio. This is because investment that was made on Equity 1 and Equity 2 is very risky in

nature. In case small decline will be observed on the market sharp reduction may be seen on

share price. Thus, one must cautiously make investment in shares. In case uncertainty prevailed

in the market then in that case share price may tubed rapidly and return may be negative. Hence,

in that situation if investment is already made in the risk free asset loss that is bear on the risky

asset may to some extent can be offset by return that is gained on risk free assets. In this way

loss can be minimized to some extent on invested amount. Thus, it can be said that investment

decisions taken by the investor are excellent because even in case gain is made on Equity A and

Equity B addition of 5% of profit from risk free asset will increase amount of return earned on

the invested amount. Thus, it can be said that is is prudent decision to make investment in

underlying asset and risk free asset.

7 | P a g e

Return of

portfolio

Risk free rate of

return

Summation of

return

Increase in return after addition of

RFR asset

16.930% 5% 21.930% 5%

15.543% 5% 20.543% 5%

15.080% 5% 20.080% 5%

15.265% 5% 20.265% 5%

15.173% 5% 20.173% 5%

Figure 5Return of portfolio and return after addition of risk free rate of return

Interpretation

In order to identify whether it is prudent decision to make investment in risk free assets

apart from Equity A and B return that can be earned on risk free asset is added to same that is

gained on the revised portfolio. It can be said that rational investment is made by investor on

portfolio. This is because investment that was made on Equity 1 and Equity 2 is very risky in

nature. In case small decline will be observed on the market sharp reduction may be seen on

share price. Thus, one must cautiously make investment in shares. In case uncertainty prevailed

in the market then in that case share price may tubed rapidly and return may be negative. Hence,

in that situation if investment is already made in the risk free asset loss that is bear on the risky

asset may to some extent can be offset by return that is gained on risk free assets. In this way

loss can be minimized to some extent on invested amount. Thus, it can be said that investment

decisions taken by the investor are excellent because even in case gain is made on Equity A and

Equity B addition of 5% of profit from risk free asset will increase amount of return earned on

the invested amount. Thus, it can be said that is is prudent decision to make investment in

underlying asset and risk free asset.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 2

Two appropriate methods for calculating cost of equity

Table 8Calculation of cost of equity by using CAPM model

RFR 1.75

Market premium 0.11

Beta 0.82

Cost of equity 1.8402

Interpretation

Cost of equity is 1.84 which reflect that cost of equity is low for the business firm. Under

this calculation CAPM model is used for calculation of cost of equity. In order to compute cost

of equity under this model varied elements are used like RFR, market premium and beta. Beta

refers to the value that reflect the relationship between index values and share price. Percentage

change in share price and index is calculated and by using slope function of usually excel beta is

computed. RFR rate refers to the risk free rate of interest that is charged on the bonds and guilt

funds of government. It is the return that is expected to be earn in every condition on equity even

market failed because risk free return is already very low.

Table 9Cost of equity by using divided growth model

Dividend per share 0.45

Current market price of stock 4479

Growth rate of dividend 34%

Cost of equity 34.34%

Dividend growth model is another alternative that is available to investors for making prudent

decisions. Under this model there are number of elements like dividend per share, current market

price and growth rate of dividend. Dividend per share reflect the dividend amount that is

received on each unit of shares. On other hand, current market price refers to the real time share

price of the specific company shares. Growth rate of dividend refers to the rate at which dividend

is growing on yearly basis. Relevant calculation can be seen below.

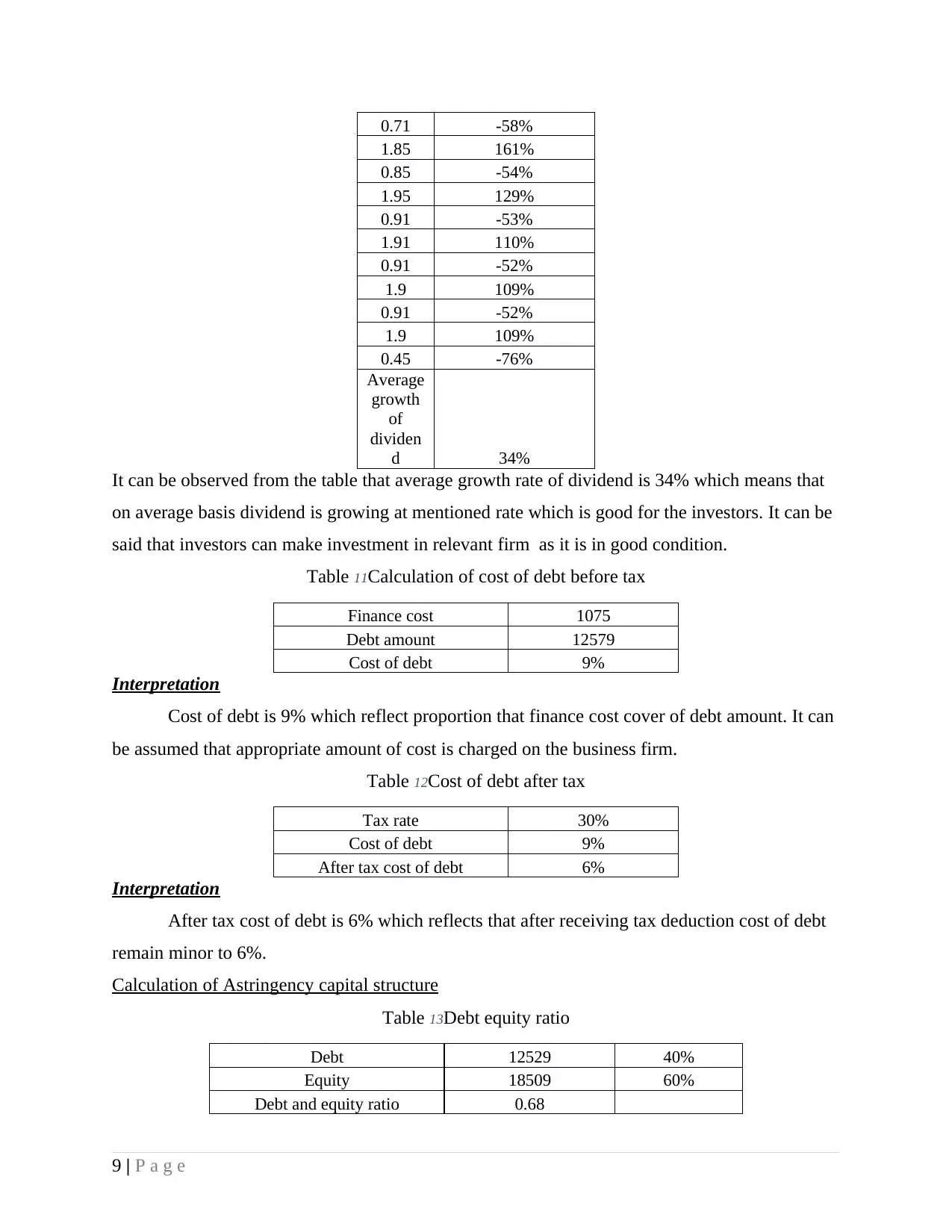

Table 10Growth rate of dividend

1.35

0.55 -59%

1.51 175%

0.59 -61%

1.71 190%

8 | P a g e

Two appropriate methods for calculating cost of equity

Table 8Calculation of cost of equity by using CAPM model

RFR 1.75

Market premium 0.11

Beta 0.82

Cost of equity 1.8402

Interpretation

Cost of equity is 1.84 which reflect that cost of equity is low for the business firm. Under

this calculation CAPM model is used for calculation of cost of equity. In order to compute cost

of equity under this model varied elements are used like RFR, market premium and beta. Beta

refers to the value that reflect the relationship between index values and share price. Percentage

change in share price and index is calculated and by using slope function of usually excel beta is

computed. RFR rate refers to the risk free rate of interest that is charged on the bonds and guilt

funds of government. It is the return that is expected to be earn in every condition on equity even

market failed because risk free return is already very low.

Table 9Cost of equity by using divided growth model

Dividend per share 0.45

Current market price of stock 4479

Growth rate of dividend 34%

Cost of equity 34.34%

Dividend growth model is another alternative that is available to investors for making prudent

decisions. Under this model there are number of elements like dividend per share, current market

price and growth rate of dividend. Dividend per share reflect the dividend amount that is

received on each unit of shares. On other hand, current market price refers to the real time share

price of the specific company shares. Growth rate of dividend refers to the rate at which dividend

is growing on yearly basis. Relevant calculation can be seen below.

Table 10Growth rate of dividend

1.35

0.55 -59%

1.51 175%

0.59 -61%

1.71 190%

8 | P a g e

0.71 -58%

1.85 161%

0.85 -54%

1.95 129%

0.91 -53%

1.91 110%

0.91 -52%

1.9 109%

0.91 -52%

1.9 109%

0.45 -76%

Average

growth

of

dividen

d 34%

It can be observed from the table that average growth rate of dividend is 34% which means that

on average basis dividend is growing at mentioned rate which is good for the investors. It can be

said that investors can make investment in relevant firm as it is in good condition.

Table 11Calculation of cost of debt before tax

Finance cost 1075

Debt amount 12579

Cost of debt 9%

Interpretation

Cost of debt is 9% which reflect proportion that finance cost cover of debt amount. It can

be assumed that appropriate amount of cost is charged on the business firm.

Table 12Cost of debt after tax

Tax rate 30%

Cost of debt 9%

After tax cost of debt 6%

Interpretation

After tax cost of debt is 6% which reflects that after receiving tax deduction cost of debt

remain minor to 6%.

Calculation of Astringency capital structure

Table 13Debt equity ratio

Debt 12529 40%

Equity 18509 60%

Debt and equity ratio 0.68

9 | P a g e

1.85 161%

0.85 -54%

1.95 129%

0.91 -53%

1.91 110%

0.91 -52%

1.9 109%

0.91 -52%

1.9 109%

0.45 -76%

Average

growth

of

dividen

d 34%

It can be observed from the table that average growth rate of dividend is 34% which means that

on average basis dividend is growing at mentioned rate which is good for the investors. It can be

said that investors can make investment in relevant firm as it is in good condition.

Table 11Calculation of cost of debt before tax

Finance cost 1075

Debt amount 12579

Cost of debt 9%

Interpretation

Cost of debt is 9% which reflect proportion that finance cost cover of debt amount. It can

be assumed that appropriate amount of cost is charged on the business firm.

Table 12Cost of debt after tax

Tax rate 30%

Cost of debt 9%

After tax cost of debt 6%

Interpretation

After tax cost of debt is 6% which reflects that after receiving tax deduction cost of debt

remain minor to 6%.

Calculation of Astringency capital structure

Table 13Debt equity ratio

Debt 12529 40%

Equity 18509 60%

Debt and equity ratio 0.68

9 | P a g e

31038

Interpretation

Debt equity ratio is 0.68 which reflect that proportion of debt is less then equity. Debt

cover 40% of capital structure and equity cover 60% of same. Hence, it can be said that capital

structure is balanced.

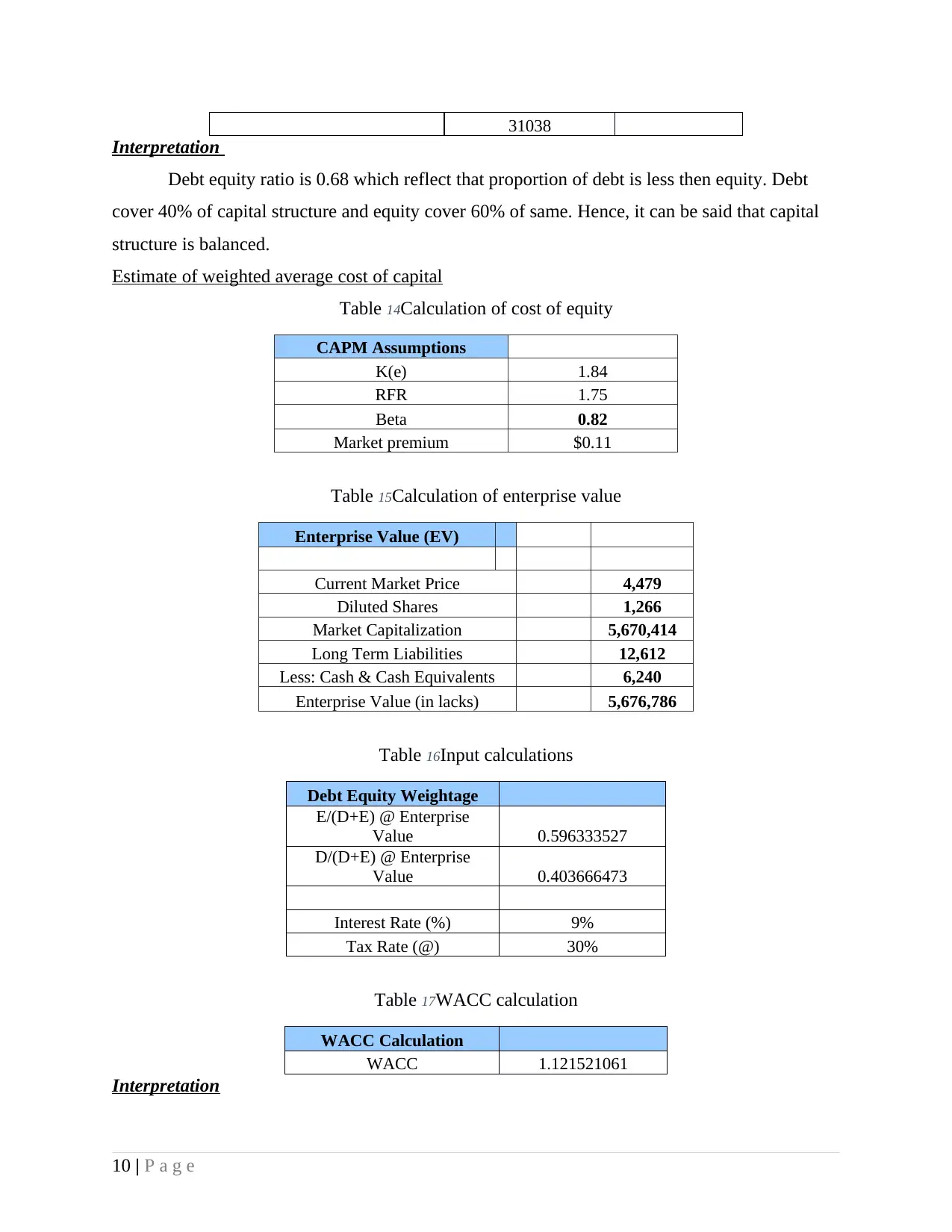

Estimate of weighted average cost of capital

Table 14Calculation of cost of equity

CAPM Assumptions

K(e) 1.84

RFR 1.75

Beta 0.82

Market premium $0.11

Table 15Calculation of enterprise value

Enterprise Value (EV)

Current Market Price 4,479

Diluted Shares 1,266

Market Capitalization 5,670,414

Long Term Liabilities 12,612

Less: Cash & Cash Equivalents 6,240

Enterprise Value (in lacks) 5,676,786

Table 16Input calculations

Debt Equity Weightage

E/(D+E) @ Enterprise

Value 0.596333527

D/(D+E) @ Enterprise

Value 0.403666473

Interest Rate (%) 9%

Tax Rate (@) 30%

Table 17WACC calculation

WACC Calculation

WACC 1.121521061

Interpretation

10 | P a g e

Interpretation

Debt equity ratio is 0.68 which reflect that proportion of debt is less then equity. Debt

cover 40% of capital structure and equity cover 60% of same. Hence, it can be said that capital

structure is balanced.

Estimate of weighted average cost of capital

Table 14Calculation of cost of equity

CAPM Assumptions

K(e) 1.84

RFR 1.75

Beta 0.82

Market premium $0.11

Table 15Calculation of enterprise value

Enterprise Value (EV)

Current Market Price 4,479

Diluted Shares 1,266

Market Capitalization 5,670,414

Long Term Liabilities 12,612

Less: Cash & Cash Equivalents 6,240

Enterprise Value (in lacks) 5,676,786

Table 16Input calculations

Debt Equity Weightage

E/(D+E) @ Enterprise

Value 0.596333527

D/(D+E) @ Enterprise

Value 0.403666473

Interest Rate (%) 9%

Tax Rate (@) 30%

Table 17WACC calculation

WACC Calculation

WACC 1.121521061

Interpretation

10 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Cost of equity is computed by using CAPM model which is explained above. Cost of

debt is computed by identifying percentage of interest of debt amount. Weight of equity is

multiplied to cost of same and same approach is followed for debt. Finally, weighted average

cost of capital is computed and its value is 1.21% which is very low and it can be said that cost

of finance is very low for the firm.

Question 3

Efficient market hypothesis

Efficient market hypothesis reflects that any investor can not earn more than return that

market generated. Share price fluctuation contain impact of information that is in the market.

According to intensity of news relevant change's comes in the share price. It is difficult for fund

managers to outperform market because price keeps on changing consistently and in such

conditions good amount return can not be gained (What is efficient market hypothesis, 2017). It

is hard for them to make accurate estimation of changes that may occur in share price due to any

news. Table 1 indicate that EMH is not perfect theory because when any news come investors

react to same. They become panic on single bad news sale their open positions without thinking

rationally. This is the reason due to which percentage outperformed is high in table 1. Portfolio

managers know investors behaviour and on that basis when news come in market they formulate

hypothesis to ensure that portfolio will generate positive return for them. It can be observed that

in many mutual fund schemes portfolio turnover is very high and this happened because fund

managers on the basis of experience make idea about panic level of investors and on time them

make decisions. In this way even market declined they safely earn appropriate amount of return

for investors.

CONCLUSION

On the basis of above discussion it is concluded that there is huge importance of

corporate finance domain for the investors because same help them in making prudent decisions.

There are number of methods that are used by managers for making investment decisions for

their investors. It is also concluded that investors must try to develop their knowledge about the

market because by doing so they can make prudent decisions about the market. Number of

techniques can be used to make wise decisions. Investors on the basis of results must decide

whether to invest or not in specific security.

11 | P a g e

debt is computed by identifying percentage of interest of debt amount. Weight of equity is

multiplied to cost of same and same approach is followed for debt. Finally, weighted average

cost of capital is computed and its value is 1.21% which is very low and it can be said that cost

of finance is very low for the firm.

Question 3

Efficient market hypothesis

Efficient market hypothesis reflects that any investor can not earn more than return that

market generated. Share price fluctuation contain impact of information that is in the market.

According to intensity of news relevant change's comes in the share price. It is difficult for fund

managers to outperform market because price keeps on changing consistently and in such

conditions good amount return can not be gained (What is efficient market hypothesis, 2017). It

is hard for them to make accurate estimation of changes that may occur in share price due to any

news. Table 1 indicate that EMH is not perfect theory because when any news come investors

react to same. They become panic on single bad news sale their open positions without thinking

rationally. This is the reason due to which percentage outperformed is high in table 1. Portfolio

managers know investors behaviour and on that basis when news come in market they formulate

hypothesis to ensure that portfolio will generate positive return for them. It can be observed that

in many mutual fund schemes portfolio turnover is very high and this happened because fund

managers on the basis of experience make idea about panic level of investors and on time them

make decisions. In this way even market declined they safely earn appropriate amount of return

for investors.

CONCLUSION

On the basis of above discussion it is concluded that there is huge importance of

corporate finance domain for the investors because same help them in making prudent decisions.

There are number of methods that are used by managers for making investment decisions for

their investors. It is also concluded that investors must try to develop their knowledge about the

market because by doing so they can make prudent decisions about the market. Number of

techniques can be used to make wise decisions. Investors on the basis of results must decide

whether to invest or not in specific security.

11 | P a g e

REFERNECES

Books and Journals

What is efficient market hypothesis, 2017. [Online]. Available through:<

http://www.nasdaq.com/article/investing-basics-what-is-the-efficient-market-hypothesis-

and-what-are-its-shortcomings-cm530860>. [Accessed on 3rd August 2017].

12 | P a g e

Books and Journals

What is efficient market hypothesis, 2017. [Online]. Available through:<

http://www.nasdaq.com/article/investing-basics-what-is-the-efficient-market-hypothesis-

and-what-are-its-shortcomings-cm530860>. [Accessed on 3rd August 2017].

12 | P a g e

1 out of 12

Related Documents

![[SOLVED] JB HiFi Ltd Investment Analysis](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fwh%2F8a736aa746774d07b1a1dbe34576782e.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.