FIN200 Trimester 2 2018 Project Report: Corporate Finance Analysis

VerifiedAdded on 2023/06/04

|12

|2742

|285

Report

AI Summary

This report provides a comprehensive analysis of key concepts in corporate finance, including the Security Market Line (SML) and Capital Market Line (CML), comparing their graphical representations and underlying principles. It explores the significance of minimum variance portfolios in risk management and portfolio optimization, detailing their methodology and limitations. Furthermore, the report delves into the Capital Asset Pricing Model (CAPM) equation, explaining its relevance in calculating the required rate of return and its practical applications for financial analysts and investors. The analysis highlights the importance of these tools in making informed investment decisions and managing financial risks, providing a strong foundation for understanding corporate finance principles. The report also includes graphical representations and calculations to illustrate the concepts, enhancing the understanding of the readers. The report concludes by emphasizing the practical utility of these tools for financial professionals and investors, reinforcing the significance of their application in the real-world financial environment.

Running Head: Corporate Finance

1

Project Report: Corporate Finance

1

Project Report: Corporate Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Corporate Finance

2

Contents

Introduction...........................................................................................................................................3

SML and CML line...............................................................................................................................3

Minimum variance portfolio..................................................................................................................7

CAPM equation.....................................................................................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

2

Contents

Introduction...........................................................................................................................................3

SML and CML line...............................................................................................................................3

Minimum variance portfolio..................................................................................................................7

CAPM equation.....................................................................................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Running Head: Corporate Finance

3

Introduction:

Identifying the nature of the different corporate financial tools is crucial for the

financial analyst, financial managers and the investors. The different tools take the concern

on the different aspects of an investment and offer different result. It is necessary for the

related parties to identify the necessity and choose the better method accordingly. Such as,

minimum variance portfolio method is better when an investor wants to get lower risk, no

matter what would be the return from the investment. As well, the SML line is used to

represent the related risk position and return on the basis of risk. CAPM method is helpful for

the business and the investors to identify the expected rate of return from the business

(Damodaran, 2011).

In the report, the SML line, CML line, CAPM model and minimum variance portfolio

has been studied and it has been recognized that how an organization could identify the

different investment position of a stock with the help of these tools.

SML and CML line:

Security market line (SML) represents the result of CAPM equation in a graphical

manner. It basically represents the relations among the expected return of the stock and risk

of the stock which is represented in the beta factors. In different words, it could be said that

the security market line of a portfolio and stock represents the expected return which could be

expected from a particular stock or the portfolio against the different beta factors of that stock

or portfolio (Lee and Lee, 2006). The security line is basically based on the equation of

CAPM which is as follows:

E(Ri) = RF + βi × (E(RM) - RF)

The graphical representation of SML line has been presented on the basis of the below

case:

Beta Security

Market

Line: ri

Risk-

Free

Rate

Market

Return

0 5.00% 5% 8%

0.5 6.50% 5% 8%

3

Introduction:

Identifying the nature of the different corporate financial tools is crucial for the

financial analyst, financial managers and the investors. The different tools take the concern

on the different aspects of an investment and offer different result. It is necessary for the

related parties to identify the necessity and choose the better method accordingly. Such as,

minimum variance portfolio method is better when an investor wants to get lower risk, no

matter what would be the return from the investment. As well, the SML line is used to

represent the related risk position and return on the basis of risk. CAPM method is helpful for

the business and the investors to identify the expected rate of return from the business

(Damodaran, 2011).

In the report, the SML line, CML line, CAPM model and minimum variance portfolio

has been studied and it has been recognized that how an organization could identify the

different investment position of a stock with the help of these tools.

SML and CML line:

Security market line (SML) represents the result of CAPM equation in a graphical

manner. It basically represents the relations among the expected return of the stock and risk

of the stock which is represented in the beta factors. In different words, it could be said that

the security market line of a portfolio and stock represents the expected return which could be

expected from a particular stock or the portfolio against the different beta factors of that stock

or portfolio (Lee and Lee, 2006). The security line is basically based on the equation of

CAPM which is as follows:

E(Ri) = RF + βi × (E(RM) - RF)

The graphical representation of SML line has been presented on the basis of the below

case:

Beta Security

Market

Line: ri

Risk-

Free

Rate

Market

Return

0 5.00% 5% 8%

0.5 6.50% 5% 8%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Corporate Finance

4

1 8.00% 5% 8%

1.5 9.50% 5% 8%

2 11.00% 5% 8%

Figure 1: Security Market line

(Damodaran, 2011)

It represents that security market line only focuses on the beta factors of the stock and

the total expected return on the basis of that stock.

Further, capital market line (CML) represents the risk (in the manner of standards

deviation) against the return in a graphical manner. It basically represents the relations among

the expected return of an efficient portfolio and risk of the stock which is represented in the

standard deviation factors (Lumby and Jones, 2007). In different words, it could be said that

the capital market line of a portfolio represents the return which could be expected from a

particular portfolio against the different standard deviation level of that portfolio. The capital

line is basically based on the equation below equation:

4

1 8.00% 5% 8%

1.5 9.50% 5% 8%

2 11.00% 5% 8%

Figure 1: Security Market line

(Damodaran, 2011)

It represents that security market line only focuses on the beta factors of the stock and

the total expected return on the basis of that stock.

Further, capital market line (CML) represents the risk (in the manner of standards

deviation) against the return in a graphical manner. It basically represents the relations among

the expected return of an efficient portfolio and risk of the stock which is represented in the

standard deviation factors (Lumby and Jones, 2007). In different words, it could be said that

the capital market line of a portfolio represents the return which could be expected from a

particular portfolio against the different standard deviation level of that portfolio. The capital

line is basically based on the equation below equation:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Corporate Finance

5

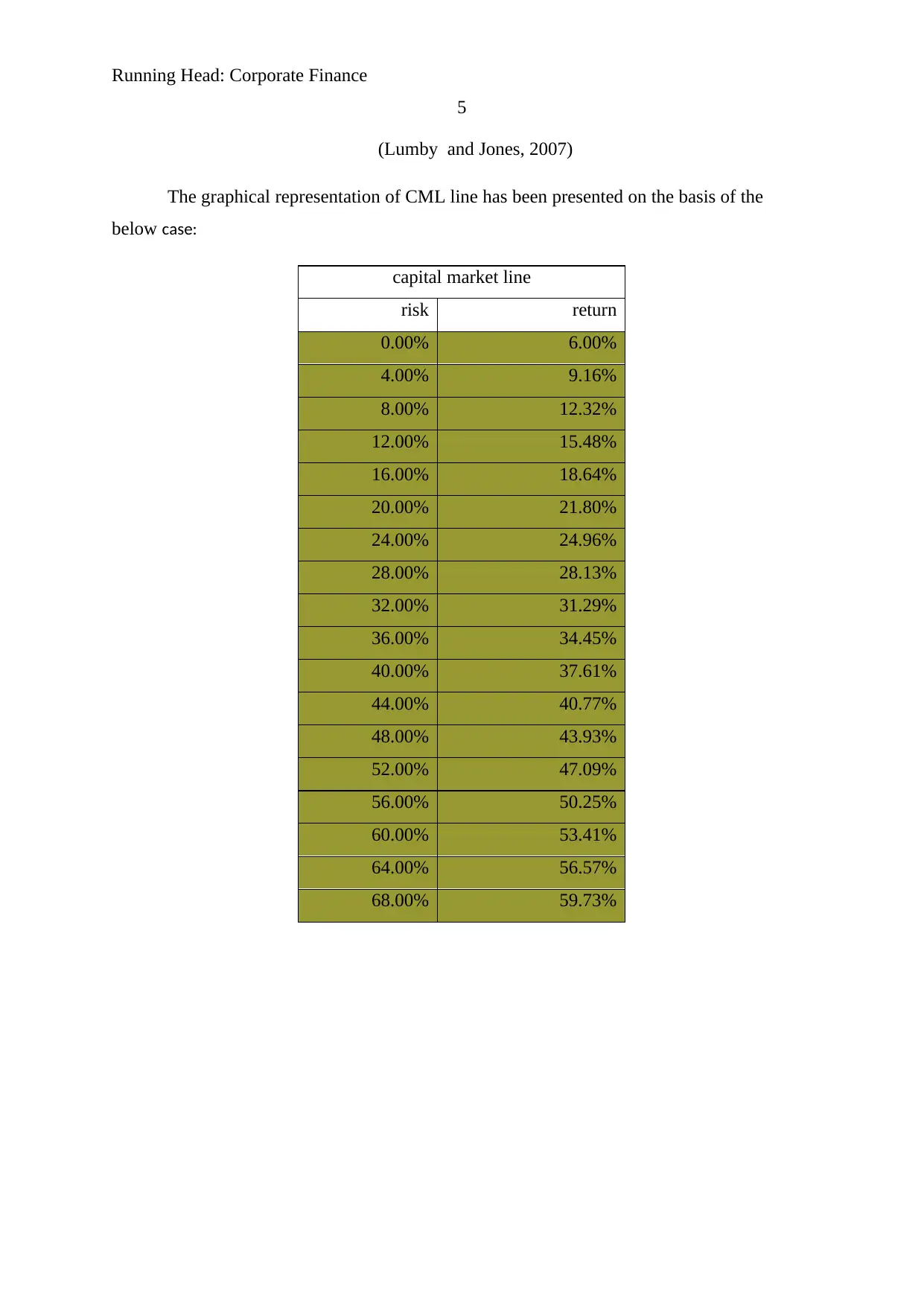

(Lumby and Jones, 2007)

The graphical representation of CML line has been presented on the basis of the

below case:

capital market line

risk return

0.00% 6.00%

4.00% 9.16%

8.00% 12.32%

12.00% 15.48%

16.00% 18.64%

20.00% 21.80%

24.00% 24.96%

28.00% 28.13%

32.00% 31.29%

36.00% 34.45%

40.00% 37.61%

44.00% 40.77%

48.00% 43.93%

52.00% 47.09%

56.00% 50.25%

60.00% 53.41%

64.00% 56.57%

68.00% 59.73%

5

(Lumby and Jones, 2007)

The graphical representation of CML line has been presented on the basis of the

below case:

capital market line

risk return

0.00% 6.00%

4.00% 9.16%

8.00% 12.32%

12.00% 15.48%

16.00% 18.64%

20.00% 21.80%

24.00% 24.96%

28.00% 28.13%

32.00% 31.29%

36.00% 34.45%

40.00% 37.61%

44.00% 40.77%

48.00% 43.93%

52.00% 47.09%

56.00% 50.25%

60.00% 53.41%

64.00% 56.57%

68.00% 59.73%

Running Head: Corporate Finance

6

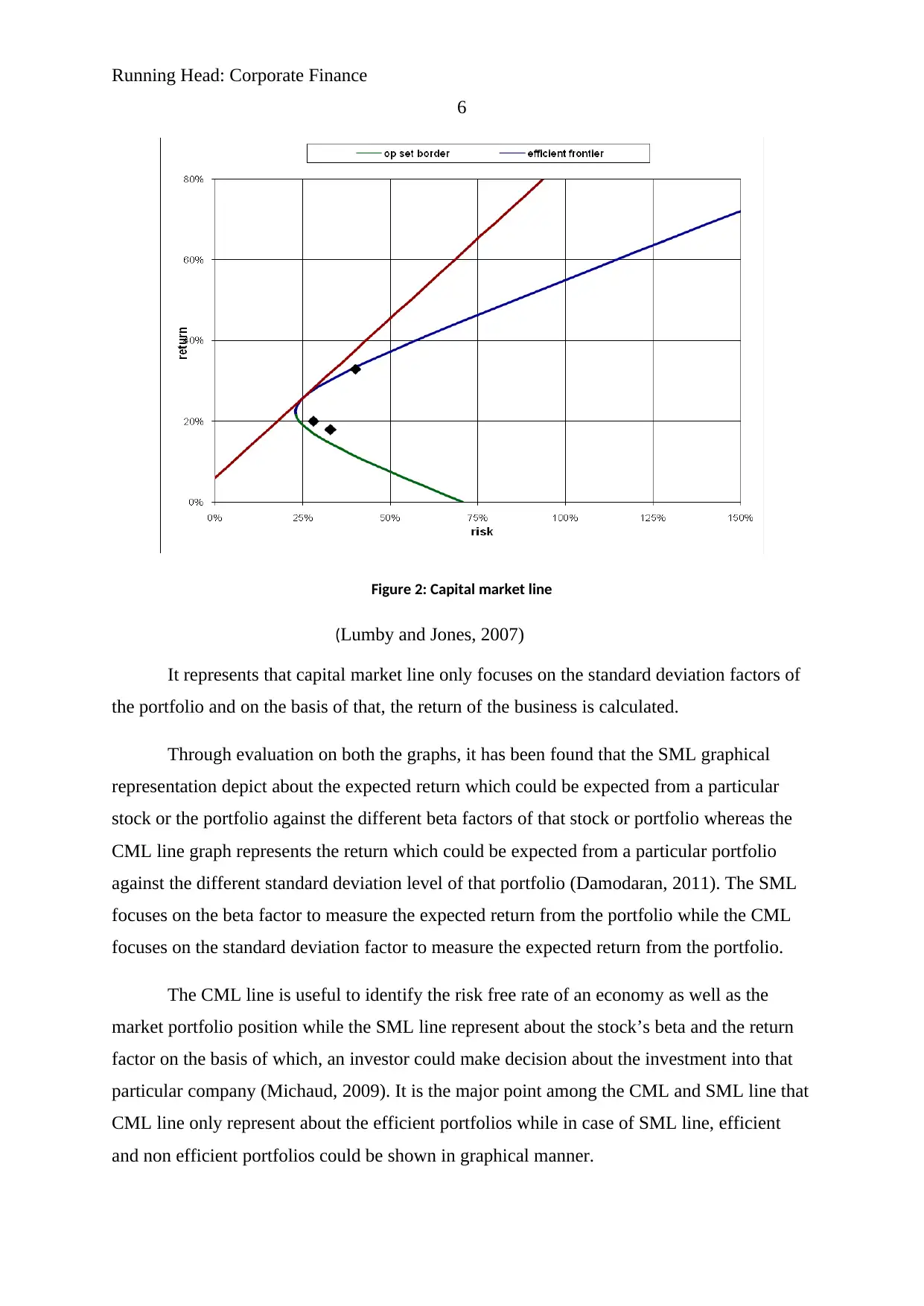

Figure 2: Capital market line

(Lumby and Jones, 2007)

It represents that capital market line only focuses on the standard deviation factors of

the portfolio and on the basis of that, the return of the business is calculated.

Through evaluation on both the graphs, it has been found that the SML graphical

representation depict about the expected return which could be expected from a particular

stock or the portfolio against the different beta factors of that stock or portfolio whereas the

CML line graph represents the return which could be expected from a particular portfolio

against the different standard deviation level of that portfolio (Damodaran, 2011). The SML

focuses on the beta factor to measure the expected return from the portfolio while the CML

focuses on the standard deviation factor to measure the expected return from the portfolio.

The CML line is useful to identify the risk free rate of an economy as well as the

market portfolio position while the SML line represent about the stock’s beta and the return

factor on the basis of which, an investor could make decision about the investment into that

particular company (Michaud, 2009). It is the major point among the CML and SML line that

CML line only represent about the efficient portfolios while in case of SML line, efficient

and non efficient portfolios could be shown in graphical manner.

6

Figure 2: Capital market line

(Lumby and Jones, 2007)

It represents that capital market line only focuses on the standard deviation factors of

the portfolio and on the basis of that, the return of the business is calculated.

Through evaluation on both the graphs, it has been found that the SML graphical

representation depict about the expected return which could be expected from a particular

stock or the portfolio against the different beta factors of that stock or portfolio whereas the

CML line graph represents the return which could be expected from a particular portfolio

against the different standard deviation level of that portfolio (Damodaran, 2011). The SML

focuses on the beta factor to measure the expected return from the portfolio while the CML

focuses on the standard deviation factor to measure the expected return from the portfolio.

The CML line is useful to identify the risk free rate of an economy as well as the

market portfolio position while the SML line represent about the stock’s beta and the return

factor on the basis of which, an investor could make decision about the investment into that

particular company (Michaud, 2009). It is the major point among the CML and SML line that

CML line only represent about the efficient portfolios while in case of SML line, efficient

and non efficient portfolios could be shown in graphical manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Corporate Finance

7

On the basis of the above definitions of CML and SML and their graphical

comparison, it has been found that both of the methods must be followed and applied by the

financial analyst, financial manager and the investors to get the same outcome from the

different figures on the basis of the needs and nature of investment.

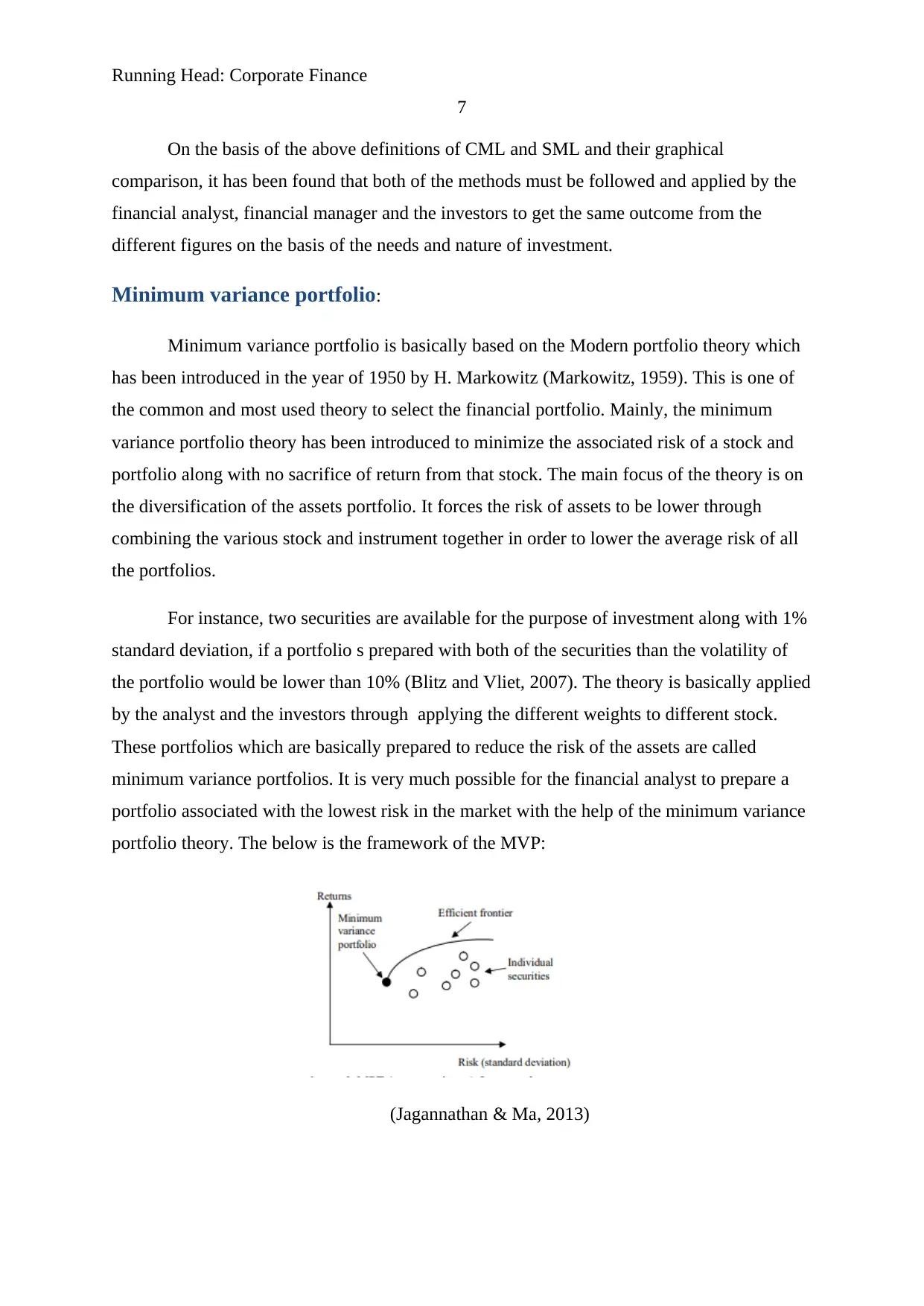

Minimum variance portfolio:

Minimum variance portfolio is basically based on the Modern portfolio theory which

has been introduced in the year of 1950 by H. Markowitz (Markowitz, 1959). This is one of

the common and most used theory to select the financial portfolio. Mainly, the minimum

variance portfolio theory has been introduced to minimize the associated risk of a stock and

portfolio along with no sacrifice of return from that stock. The main focus of the theory is on

the diversification of the assets portfolio. It forces the risk of assets to be lower through

combining the various stock and instrument together in order to lower the average risk of all

the portfolios.

For instance, two securities are available for the purpose of investment along with 1%

standard deviation, if a portfolio s prepared with both of the securities than the volatility of

the portfolio would be lower than 10% (Blitz and Vliet, 2007). The theory is basically applied

by the analyst and the investors through applying the different weights to different stock.

These portfolios which are basically prepared to reduce the risk of the assets are called

minimum variance portfolios. It is very much possible for the financial analyst to prepare a

portfolio associated with the lowest risk in the market with the help of the minimum variance

portfolio theory. The below is the framework of the MVP:

(Jagannathan & Ma, 2013)

7

On the basis of the above definitions of CML and SML and their graphical

comparison, it has been found that both of the methods must be followed and applied by the

financial analyst, financial manager and the investors to get the same outcome from the

different figures on the basis of the needs and nature of investment.

Minimum variance portfolio:

Minimum variance portfolio is basically based on the Modern portfolio theory which

has been introduced in the year of 1950 by H. Markowitz (Markowitz, 1959). This is one of

the common and most used theory to select the financial portfolio. Mainly, the minimum

variance portfolio theory has been introduced to minimize the associated risk of a stock and

portfolio along with no sacrifice of return from that stock. The main focus of the theory is on

the diversification of the assets portfolio. It forces the risk of assets to be lower through

combining the various stock and instrument together in order to lower the average risk of all

the portfolios.

For instance, two securities are available for the purpose of investment along with 1%

standard deviation, if a portfolio s prepared with both of the securities than the volatility of

the portfolio would be lower than 10% (Blitz and Vliet, 2007). The theory is basically applied

by the analyst and the investors through applying the different weights to different stock.

These portfolios which are basically prepared to reduce the risk of the assets are called

minimum variance portfolios. It is very much possible for the financial analyst to prepare a

portfolio associated with the lowest risk in the market with the help of the minimum variance

portfolio theory. The below is the framework of the MVP:

(Jagannathan & Ma, 2013)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Corporate Finance

8

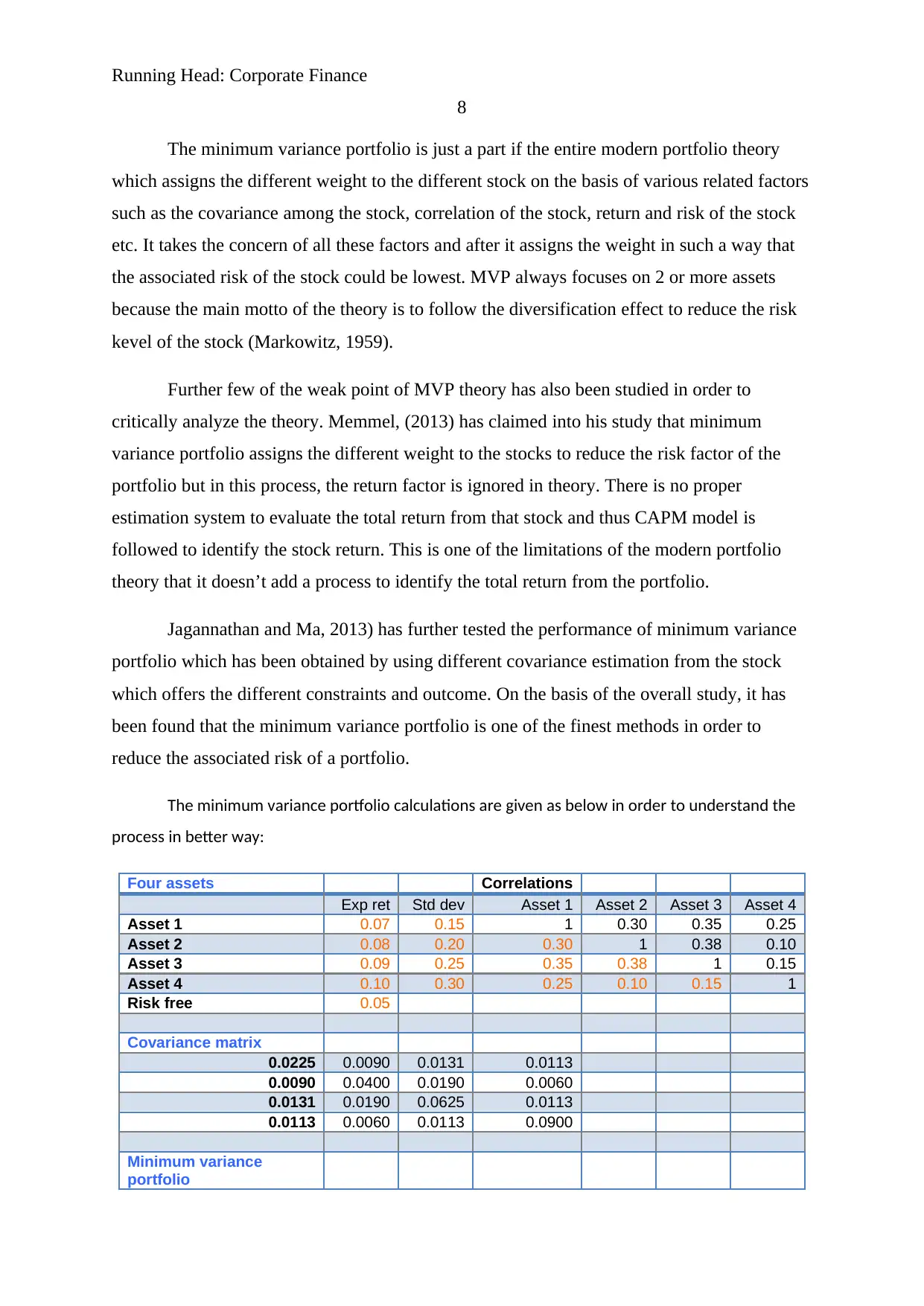

The minimum variance portfolio is just a part if the entire modern portfolio theory

which assigns the different weight to the different stock on the basis of various related factors

such as the covariance among the stock, correlation of the stock, return and risk of the stock

etc. It takes the concern of all these factors and after it assigns the weight in such a way that

the associated risk of the stock could be lowest. MVP always focuses on 2 or more assets

because the main motto of the theory is to follow the diversification effect to reduce the risk

kevel of the stock (Markowitz, 1959).

Further few of the weak point of MVP theory has also been studied in order to

critically analyze the theory. Memmel, (2013) has claimed into his study that minimum

variance portfolio assigns the different weight to the stocks to reduce the risk factor of the

portfolio but in this process, the return factor is ignored in theory. There is no proper

estimation system to evaluate the total return from that stock and thus CAPM model is

followed to identify the stock return. This is one of the limitations of the modern portfolio

theory that it doesn’t add a process to identify the total return from the portfolio.

Jagannathan and Ma, 2013) has further tested the performance of minimum variance

portfolio which has been obtained by using different covariance estimation from the stock

which offers the different constraints and outcome. On the basis of the overall study, it has

been found that the minimum variance portfolio is one of the finest methods in order to

reduce the associated risk of a portfolio.

The minimum variance portfolio calculations are given as below in order to understand the

process in better way:

Four assets Correlations

Exp ret Std dev Asset 1 Asset 2 Asset 3 Asset 4

Asset 1 0.07 0.15 1 0.30 0.35 0.25

Asset 2 0.08 0.20 0.30 1 0.38 0.10

Asset 3 0.09 0.25 0.35 0.38 1 0.15

Asset 4 0.10 0.30 0.25 0.10 0.15 1

Risk free 0.05

Covariance matrix

0.0225 0.0090 0.0131 0.0113

0.0090 0.0400 0.0190 0.0060

0.0131 0.0190 0.0625 0.0113

0.0113 0.0060 0.0113 0.0900

Minimum variance

portfolio

8

The minimum variance portfolio is just a part if the entire modern portfolio theory

which assigns the different weight to the different stock on the basis of various related factors

such as the covariance among the stock, correlation of the stock, return and risk of the stock

etc. It takes the concern of all these factors and after it assigns the weight in such a way that

the associated risk of the stock could be lowest. MVP always focuses on 2 or more assets

because the main motto of the theory is to follow the diversification effect to reduce the risk

kevel of the stock (Markowitz, 1959).

Further few of the weak point of MVP theory has also been studied in order to

critically analyze the theory. Memmel, (2013) has claimed into his study that minimum

variance portfolio assigns the different weight to the stocks to reduce the risk factor of the

portfolio but in this process, the return factor is ignored in theory. There is no proper

estimation system to evaluate the total return from that stock and thus CAPM model is

followed to identify the stock return. This is one of the limitations of the modern portfolio

theory that it doesn’t add a process to identify the total return from the portfolio.

Jagannathan and Ma, 2013) has further tested the performance of minimum variance

portfolio which has been obtained by using different covariance estimation from the stock

which offers the different constraints and outcome. On the basis of the overall study, it has

been found that the minimum variance portfolio is one of the finest methods in order to

reduce the associated risk of a portfolio.

The minimum variance portfolio calculations are given as below in order to understand the

process in better way:

Four assets Correlations

Exp ret Std dev Asset 1 Asset 2 Asset 3 Asset 4

Asset 1 0.07 0.15 1 0.30 0.35 0.25

Asset 2 0.08 0.20 0.30 1 0.38 0.10

Asset 3 0.09 0.25 0.35 0.38 1 0.15

Asset 4 0.10 0.30 0.25 0.10 0.15 1

Risk free 0.05

Covariance matrix

0.0225 0.0090 0.0131 0.0113

0.0090 0.0400 0.0190 0.0060

0.0131 0.0190 0.0625 0.0113

0.0113 0.0060 0.0113 0.0900

Minimum variance

portfolio

Running Head: Corporate Finance

9

Weight 1 0.586

Weight 2 0.260

Weight 3 0.059

Weight 4 0.095

Exp ret 0.077

Std dev 0.132

(Michaud, 2009)

It explains that after applying the theory of minimum variance portfolio, the associate

risk of the portfolio has been 0.132 which is lowest in comparison with the individual stock

risk position.

CAPM equation:

CAPM method is an economical theory which is used by the investors and the

financial analyst to represent about the relations among the expected return and risk position

of an assets or the portfolio of the asset (Memmel, 2013). The CAPM theory explains that

only the systematic risk affect the return of an assets and this risk cannot be eliminated even

with the diversification of the assets. The theory further represents that the expected return

from an assets or a portfolio is always equivalent to the risk free security rate which is added

with the market premium of capital market and multiplied by the asset’s beta factor (i.e. the

systematic risk of the stock). The equation of the CAPM is as follows:

E(Ri) = RF + βi × (E(RM) - RF)

Where,

E(Ri) stands for the expected return from the stock or the portfolio

RF stands for the risk free rate of the economy

Βi stands for the beta factor of asset or the portfolio

(E(RM) - RF) stands for the market premium (Michaud, 2009)..

The equation of the CAPM represent that it focuses on the individual beta factor of

the company which is the systematic risk of the company and impact the return from that

particular stock (Ross, Westerfield And Jaffe, 2007). The systematic risk can never be

eliminated in the investment position even through using the diversification method and thus

9

Weight 1 0.586

Weight 2 0.260

Weight 3 0.059

Weight 4 0.095

Exp ret 0.077

Std dev 0.132

(Michaud, 2009)

It explains that after applying the theory of minimum variance portfolio, the associate

risk of the portfolio has been 0.132 which is lowest in comparison with the individual stock

risk position.

CAPM equation:

CAPM method is an economical theory which is used by the investors and the

financial analyst to represent about the relations among the expected return and risk position

of an assets or the portfolio of the asset (Memmel, 2013). The CAPM theory explains that

only the systematic risk affect the return of an assets and this risk cannot be eliminated even

with the diversification of the assets. The theory further represents that the expected return

from an assets or a portfolio is always equivalent to the risk free security rate which is added

with the market premium of capital market and multiplied by the asset’s beta factor (i.e. the

systematic risk of the stock). The equation of the CAPM is as follows:

E(Ri) = RF + βi × (E(RM) - RF)

Where,

E(Ri) stands for the expected return from the stock or the portfolio

RF stands for the risk free rate of the economy

Βi stands for the beta factor of asset or the portfolio

(E(RM) - RF) stands for the market premium (Michaud, 2009)..

The equation of the CAPM represent that it focuses on the individual beta factor of

the company which is the systematic risk of the company and impact the return from that

particular stock (Ross, Westerfield And Jaffe, 2007). The systematic risk can never be

eliminated in the investment position even through using the diversification method and thus

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Corporate Finance

10

it is important for the business to measure the beta factor which is not calculated by the other

methods.

Further, the CAPM equation focuses on the risk free rate of the economy. This rate is

collected from the Australian government bond rates and it represents the minimum return

which could be got by any investor without the association of any kind of risk (Xiao, Faff

Gharghori and Min, 2017). Further the market risk premium represent the total return which

could be get by an investor through a risky return. All of these factors play crucial role in the

expected return from a stock or the portfolio (Mazzola and Gerace, 2015). And CAPM model

considers the all. Thus, it could be said that it is one of the best method to calculate the

required rate of return from a particular project.

Conclusion:

On the basis of the study on various tools to identify the different corporate financial

tools, it has been found that all the methods are quite crucial for the financial analyst,

financial managers and the investors to get the different constraints and the outcome from the

methods. The different tools focuses on different factors and thus outcome of all the methods

are also different. It is necessary for the financial analyst, financial managers and the

investors to identify the nature and needs of the investment and must apply the tool

accordingly.

On the basis of the study on CML and SML and their graphical comparison, it has

been found that both the lines take the different risk factors to identify the return level from

the stock. Further, the minimum variance portfolio method is a great method in case of an

investor wants to get lower risk along with the ignorance on the risk factor. As well, CAPM

method is helpful for the business and the investors to identify the expected rate of return

from the business.

10

it is important for the business to measure the beta factor which is not calculated by the other

methods.

Further, the CAPM equation focuses on the risk free rate of the economy. This rate is

collected from the Australian government bond rates and it represents the minimum return

which could be got by any investor without the association of any kind of risk (Xiao, Faff

Gharghori and Min, 2017). Further the market risk premium represent the total return which

could be get by an investor through a risky return. All of these factors play crucial role in the

expected return from a stock or the portfolio (Mazzola and Gerace, 2015). And CAPM model

considers the all. Thus, it could be said that it is one of the best method to calculate the

required rate of return from a particular project.

Conclusion:

On the basis of the study on various tools to identify the different corporate financial

tools, it has been found that all the methods are quite crucial for the financial analyst,

financial managers and the investors to get the different constraints and the outcome from the

methods. The different tools focuses on different factors and thus outcome of all the methods

are also different. It is necessary for the financial analyst, financial managers and the

investors to identify the nature and needs of the investment and must apply the tool

accordingly.

On the basis of the study on CML and SML and their graphical comparison, it has

been found that both the lines take the different risk factors to identify the return level from

the stock. Further, the minimum variance portfolio method is a great method in case of an

investor wants to get lower risk along with the ignorance on the risk factor. As well, CAPM

method is helpful for the business and the investors to identify the expected rate of return

from the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Corporate Finance

11

References:

Appel, D. 2008. Low volatility, high return strategies get a look. [online]. available at:

http://www.pionline.com/apps/pbcs.dll/article?aid=/20081103/reg/811039995/1011/

portfoliostrategies [accessed 18/9/18].

Blitz, D., and Vliet, P. 2007. The volatility effect: lower risk without lower return. ERIM

Report Series Research in Management. [online]. available at:

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=980865 [accessed 18/9/18].

Damodaran, A, 2011, Applied corporate finance. 3rd edition, John Wiley & sons, USA.

Jagannathan, R. and Ma, T. 2013. Risk reduction in large portfolios: Why imposing the

wrong constrains helps. The Journal of Finance, 58(4), 1651-1684.

Lee.C.F and Lee, A, C,.2006. Encyclopedia of finance. Springer science, new York.

Lumby,S and Jones,C,.2007, Corporate finance theory & practice, 7th edition, Thomson,

London.

Markowitz, H. 1959. Portfolio selection: Efficient diversification of investments. New York:

John Wiley & Sons, Inc.

Mazzola, P. and Gerace, D., 2015. A comparison between a dynamic and static approach to

asset management using CAPM models on the Australian securities market. Australasian

Accounting, Business and Finance Journal, 9(2), pp.43-58.

Memmel, C. 2013. Performance hypothesis testing with the Sharpe ratio. Finance Letters 1,

pp. 21-23.

Michaud, R. 2009. Efficient asset management. Boston, MA: Harvard Business School Press.

Michaud, R. 2009. The Markowitz optimization enigma: is “optimized” optimal? Financial

Analysts Journal. 25(2), 2013-240.

Ross, S, A,. Westerfield, R, W,. And Jaffe, J,.2007. Corporate Finance. the McGraw-hill,

India

11

References:

Appel, D. 2008. Low volatility, high return strategies get a look. [online]. available at:

http://www.pionline.com/apps/pbcs.dll/article?aid=/20081103/reg/811039995/1011/

portfoliostrategies [accessed 18/9/18].

Blitz, D., and Vliet, P. 2007. The volatility effect: lower risk without lower return. ERIM

Report Series Research in Management. [online]. available at:

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=980865 [accessed 18/9/18].

Damodaran, A, 2011, Applied corporate finance. 3rd edition, John Wiley & sons, USA.

Jagannathan, R. and Ma, T. 2013. Risk reduction in large portfolios: Why imposing the

wrong constrains helps. The Journal of Finance, 58(4), 1651-1684.

Lee.C.F and Lee, A, C,.2006. Encyclopedia of finance. Springer science, new York.

Lumby,S and Jones,C,.2007, Corporate finance theory & practice, 7th edition, Thomson,

London.

Markowitz, H. 1959. Portfolio selection: Efficient diversification of investments. New York:

John Wiley & Sons, Inc.

Mazzola, P. and Gerace, D., 2015. A comparison between a dynamic and static approach to

asset management using CAPM models on the Australian securities market. Australasian

Accounting, Business and Finance Journal, 9(2), pp.43-58.

Memmel, C. 2013. Performance hypothesis testing with the Sharpe ratio. Finance Letters 1,

pp. 21-23.

Michaud, R. 2009. Efficient asset management. Boston, MA: Harvard Business School Press.

Michaud, R. 2009. The Markowitz optimization enigma: is “optimized” optimal? Financial

Analysts Journal. 25(2), 2013-240.

Ross, S, A,. Westerfield, R, W,. And Jaffe, J,.2007. Corporate Finance. the McGraw-hill,

India

Running Head: Corporate Finance

12

Xiao, Y., Faff, R., Gharghori, P. and Min, B.K., 2017. The Financial Performance of Socially

Responsible Investments: Insights from the Intertemporal CAPM. Journal of Business

Ethics, 146(2), pp.353-364.

12

Xiao, Y., Faff, R., Gharghori, P. and Min, B.K., 2017. The Financial Performance of Socially

Responsible Investments: Insights from the Intertemporal CAPM. Journal of Business

Ethics, 146(2), pp.353-364.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.