Corporate Finance - Question Answer

VerifiedAdded on 2022/08/27

|9

|1198

|25

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: CORPORATE FINANCE 1

CORPORATE FINANCE

CORPORATE FINANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Running Head: CORPORATE FINANCE

Contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................3

Question 3........................................................................................................................................4

Question 4........................................................................................................................................6

Part A...........................................................................................................................................6

Part B............................................................................................................................................6

Question 5........................................................................................................................................7

Part A...........................................................................................................................................7

Part B............................................................................................................................................7

Part C............................................................................................................................................7

References........................................................................................................................................9

Contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................3

Question 3........................................................................................................................................4

Question 4........................................................................................................................................6

Part A...........................................................................................................................................6

Part B............................................................................................................................................6

Question 5........................................................................................................................................7

Part A...........................................................................................................................................7

Part B............................................................................................................................................7

Part C............................................................................................................................................7

References........................................................................................................................................9

Running Head: CORPORATE FINANCE

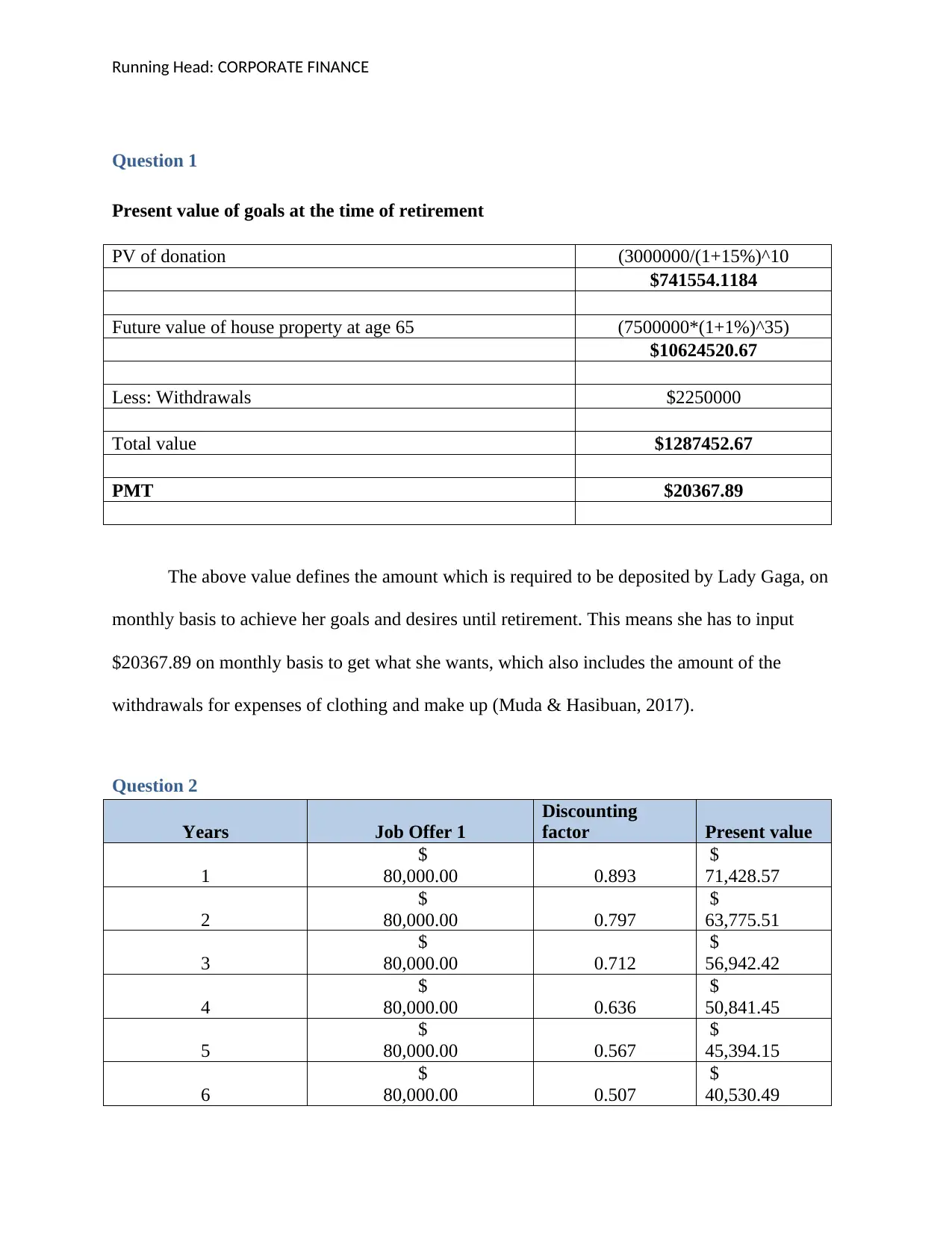

Question 1

Present value of goals at the time of retirement

PV of donation (3000000/(1+15%)^10

$741554.1184

Future value of house property at age 65 (7500000*(1+1%)^35)

$10624520.67

Less: Withdrawals $2250000

Total value $1287452.67

PMT $20367.89

The above value defines the amount which is required to be deposited by Lady Gaga, on

monthly basis to achieve her goals and desires until retirement. This means she has to input

$20367.89 on monthly basis to get what she wants, which also includes the amount of the

withdrawals for expenses of clothing and make up (Muda & Hasibuan, 2017).

Question 2

Years Job Offer 1

Discounting

factor Present value

1

$

80,000.00 0.893

$

71,428.57

2

$

80,000.00 0.797

$

63,775.51

3

$

80,000.00 0.712

$

56,942.42

4

$

80,000.00 0.636

$

50,841.45

5

$

80,000.00 0.567

$

45,394.15

6

$

80,000.00 0.507

$

40,530.49

Question 1

Present value of goals at the time of retirement

PV of donation (3000000/(1+15%)^10

$741554.1184

Future value of house property at age 65 (7500000*(1+1%)^35)

$10624520.67

Less: Withdrawals $2250000

Total value $1287452.67

PMT $20367.89

The above value defines the amount which is required to be deposited by Lady Gaga, on

monthly basis to achieve her goals and desires until retirement. This means she has to input

$20367.89 on monthly basis to get what she wants, which also includes the amount of the

withdrawals for expenses of clothing and make up (Muda & Hasibuan, 2017).

Question 2

Years Job Offer 1

Discounting

factor Present value

1

$

80,000.00 0.893

$

71,428.57

2

$

80,000.00 0.797

$

63,775.51

3

$

80,000.00 0.712

$

56,942.42

4

$

80,000.00 0.636

$

50,841.45

5

$

80,000.00 0.567

$

45,394.15

6

$

80,000.00 0.507

$

40,530.49

Running Head: CORPORATE FINANCE

Total

$

480,000.00

$

328,912.59

Years Job Offer 2

Discounting

factor Present value

1

$

65,000.00 0.893

$

58,035.71

2

$

50,000.00 0.797

$

39,859.69

3

$

50,000.00 0.712

$

35,589.01

4

$

50,000.00 0.636

$

31,775.90

5

$

60,000.00 0.567

$

34,045.61

6

$

60,000.00 0.507

$

30,397.87

Total

$

335,000.00

$

229,703.80

Loss incurred

$

145,000.00

$

99,208.78

As per the above analysis it is evident that if second offer is accepted the loss that I have

it bear is $99208.78. The change that can be proposed for the second job offer could be

indifferent with respect to the present one only when the annual cash flows are equal to $480000

in total and the bonus shall be increased to 15000 and the annual cash flows shall also increase

by 30000 for year 3 4 and 5 and by 20000 for year 5 and 6 respectively (Muda & Hasibuan,

2017).

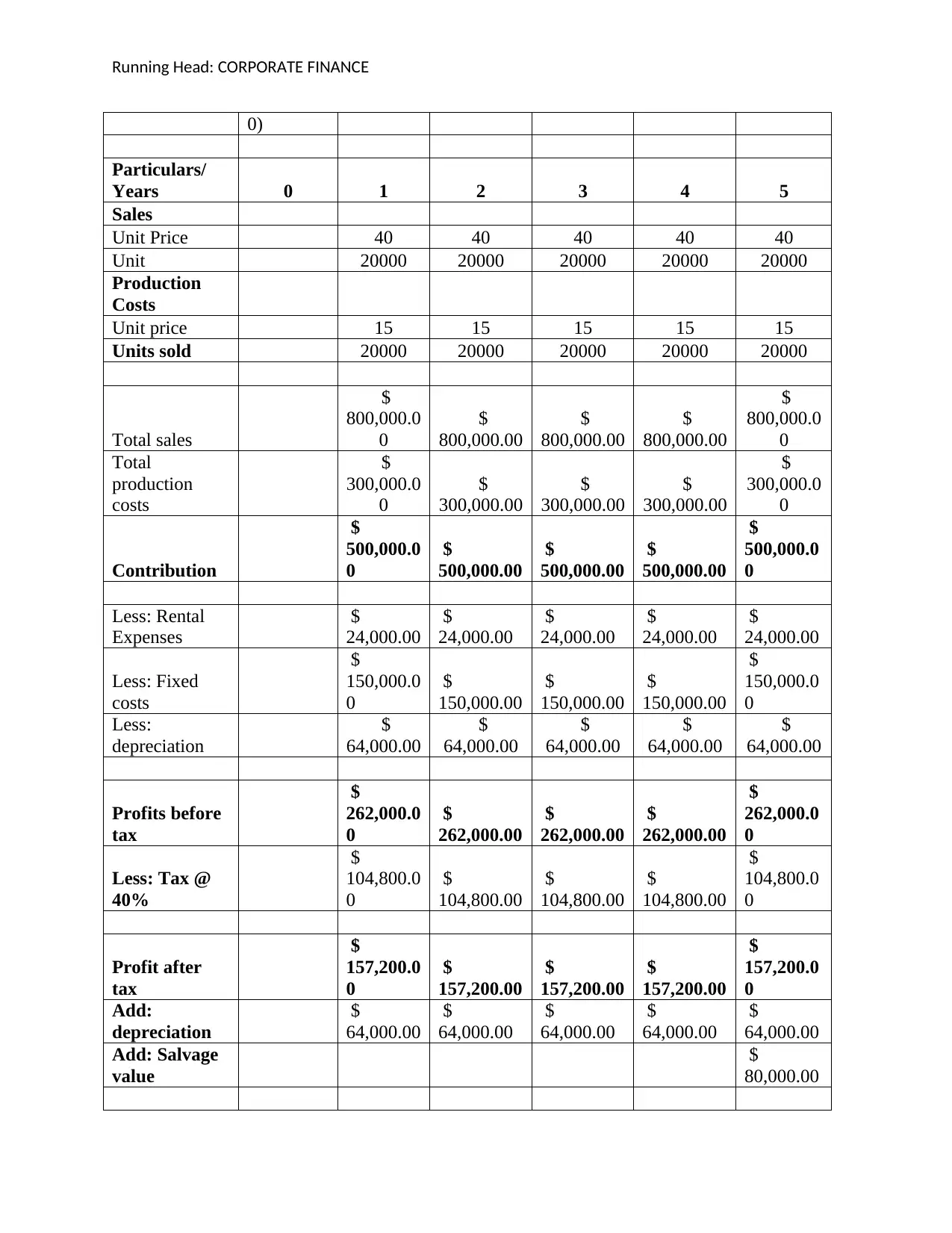

Question 3

Particulars Amount

Initial

Investment

$

(400,000.0

Total

$

480,000.00

$

328,912.59

Years Job Offer 2

Discounting

factor Present value

1

$

65,000.00 0.893

$

58,035.71

2

$

50,000.00 0.797

$

39,859.69

3

$

50,000.00 0.712

$

35,589.01

4

$

50,000.00 0.636

$

31,775.90

5

$

60,000.00 0.567

$

34,045.61

6

$

60,000.00 0.507

$

30,397.87

Total

$

335,000.00

$

229,703.80

Loss incurred

$

145,000.00

$

99,208.78

As per the above analysis it is evident that if second offer is accepted the loss that I have

it bear is $99208.78. The change that can be proposed for the second job offer could be

indifferent with respect to the present one only when the annual cash flows are equal to $480000

in total and the bonus shall be increased to 15000 and the annual cash flows shall also increase

by 30000 for year 3 4 and 5 and by 20000 for year 5 and 6 respectively (Muda & Hasibuan,

2017).

Question 3

Particulars Amount

Initial

Investment

$

(400,000.0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Running Head: CORPORATE FINANCE

0)

Particulars/

Years 0 1 2 3 4 5

Sales

Unit Price 40 40 40 40 40

Unit 20000 20000 20000 20000 20000

Production

Costs

Unit price 15 15 15 15 15

Units sold 20000 20000 20000 20000 20000

Total sales

$

800,000.0

0

$

800,000.00

$

800,000.00

$

800,000.00

$

800,000.0

0

Total

production

costs

$

300,000.0

0

$

300,000.00

$

300,000.00

$

300,000.00

$

300,000.0

0

Contribution

$

500,000.0

0

$

500,000.00

$

500,000.00

$

500,000.00

$

500,000.0

0

Less: Rental

Expenses

$

24,000.00

$

24,000.00

$

24,000.00

$

24,000.00

$

24,000.00

Less: Fixed

costs

$

150,000.0

0

$

150,000.00

$

150,000.00

$

150,000.00

$

150,000.0

0

Less:

depreciation

$

64,000.00

$

64,000.00

$

64,000.00

$

64,000.00

$

64,000.00

Profits before

tax

$

262,000.0

0

$

262,000.00

$

262,000.00

$

262,000.00

$

262,000.0

0

Less: Tax @

40%

$

104,800.0

0

$

104,800.00

$

104,800.00

$

104,800.00

$

104,800.0

0

Profit after

tax

$

157,200.0

0

$

157,200.00

$

157,200.00

$

157,200.00

$

157,200.0

0

Add:

depreciation

$

64,000.00

$

64,000.00

$

64,000.00

$

64,000.00

$

64,000.00

Add: Salvage

value

$

80,000.00

0)

Particulars/

Years 0 1 2 3 4 5

Sales

Unit Price 40 40 40 40 40

Unit 20000 20000 20000 20000 20000

Production

Costs

Unit price 15 15 15 15 15

Units sold 20000 20000 20000 20000 20000

Total sales

$

800,000.0

0

$

800,000.00

$

800,000.00

$

800,000.00

$

800,000.0

0

Total

production

costs

$

300,000.0

0

$

300,000.00

$

300,000.00

$

300,000.00

$

300,000.0

0

Contribution

$

500,000.0

0

$

500,000.00

$

500,000.00

$

500,000.00

$

500,000.0

0

Less: Rental

Expenses

$

24,000.00

$

24,000.00

$

24,000.00

$

24,000.00

$

24,000.00

Less: Fixed

costs

$

150,000.0

0

$

150,000.00

$

150,000.00

$

150,000.00

$

150,000.0

0

Less:

depreciation

$

64,000.00

$

64,000.00

$

64,000.00

$

64,000.00

$

64,000.00

Profits before

tax

$

262,000.0

0

$

262,000.00

$

262,000.00

$

262,000.00

$

262,000.0

0

Less: Tax @

40%

$

104,800.0

0

$

104,800.00

$

104,800.00

$

104,800.00

$

104,800.0

0

Profit after

tax

$

157,200.0

0

$

157,200.00

$

157,200.00

$

157,200.00

$

157,200.0

0

Add:

depreciation

$

64,000.00

$

64,000.00

$

64,000.00

$

64,000.00

$

64,000.00

Add: Salvage

value

$

80,000.00

Running Head: CORPORATE FINANCE

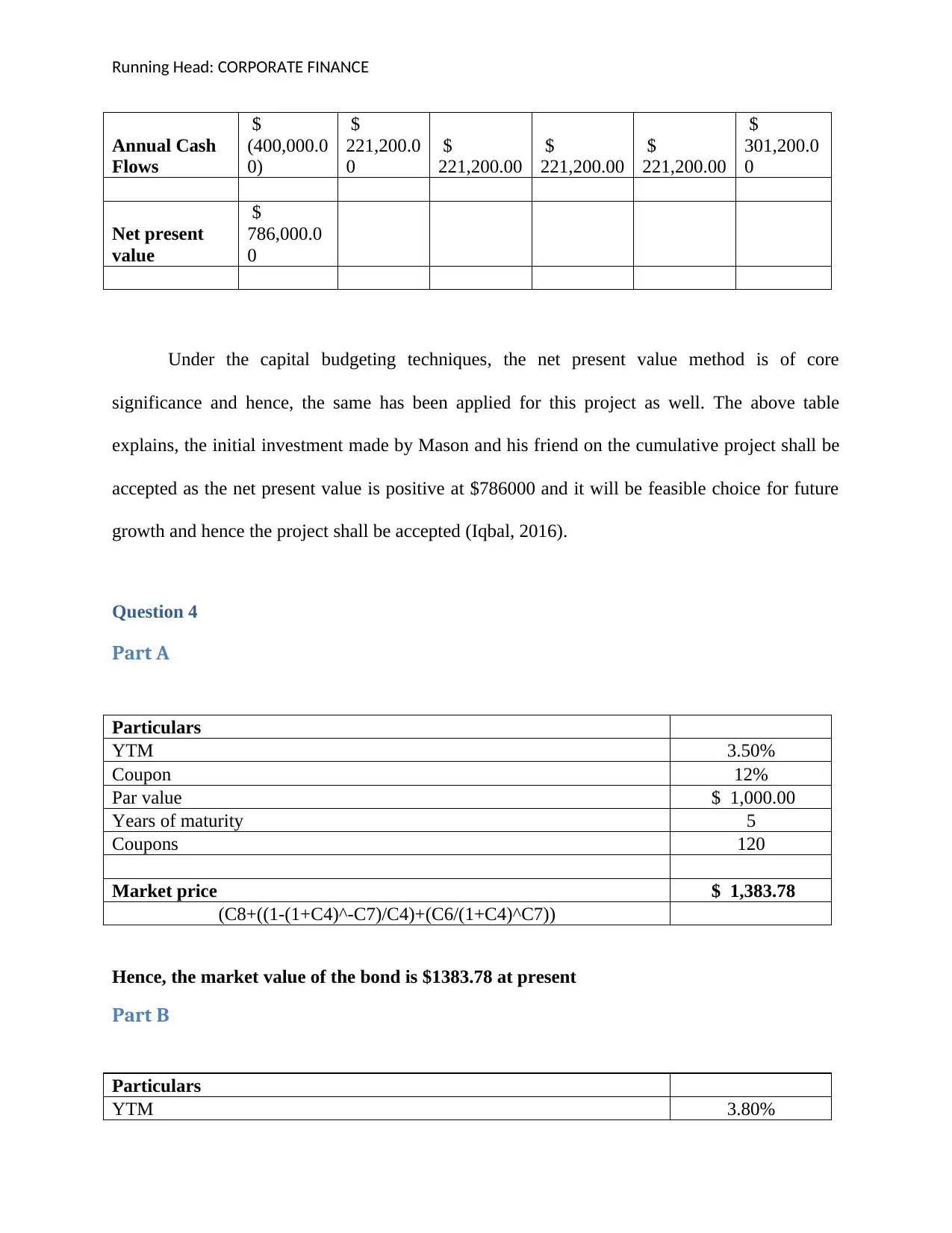

Annual Cash

Flows

$

(400,000.0

0)

$

221,200.0

0

$

221,200.00

$

221,200.00

$

221,200.00

$

301,200.0

0

Net present

value

$

786,000.0

0

Under the capital budgeting techniques, the net present value method is of core

significance and hence, the same has been applied for this project as well. The above table

explains, the initial investment made by Mason and his friend on the cumulative project shall be

accepted as the net present value is positive at $786000 and it will be feasible choice for future

growth and hence the project shall be accepted (Iqbal, 2016).

Question 4

Part A

Particulars

YTM 3.50%

Coupon 12%

Par value $ 1,000.00

Years of maturity 5

Coupons 120

Market price $ 1,383.78

(C8+((1-(1+C4)^-C7)/C4)+(C6/(1+C4)^C7))

Hence, the market value of the bond is $1383.78 at present

Part B

Particulars

YTM 3.80%

Annual Cash

Flows

$

(400,000.0

0)

$

221,200.0

0

$

221,200.00

$

221,200.00

$

221,200.00

$

301,200.0

0

Net present

value

$

786,000.0

0

Under the capital budgeting techniques, the net present value method is of core

significance and hence, the same has been applied for this project as well. The above table

explains, the initial investment made by Mason and his friend on the cumulative project shall be

accepted as the net present value is positive at $786000 and it will be feasible choice for future

growth and hence the project shall be accepted (Iqbal, 2016).

Question 4

Part A

Particulars

YTM 3.50%

Coupon 12%

Par value $ 1,000.00

Years of maturity 5

Coupons 120

Market price $ 1,383.78

(C8+((1-(1+C4)^-C7)/C4)+(C6/(1+C4)^C7))

Hence, the market value of the bond is $1383.78 at present

Part B

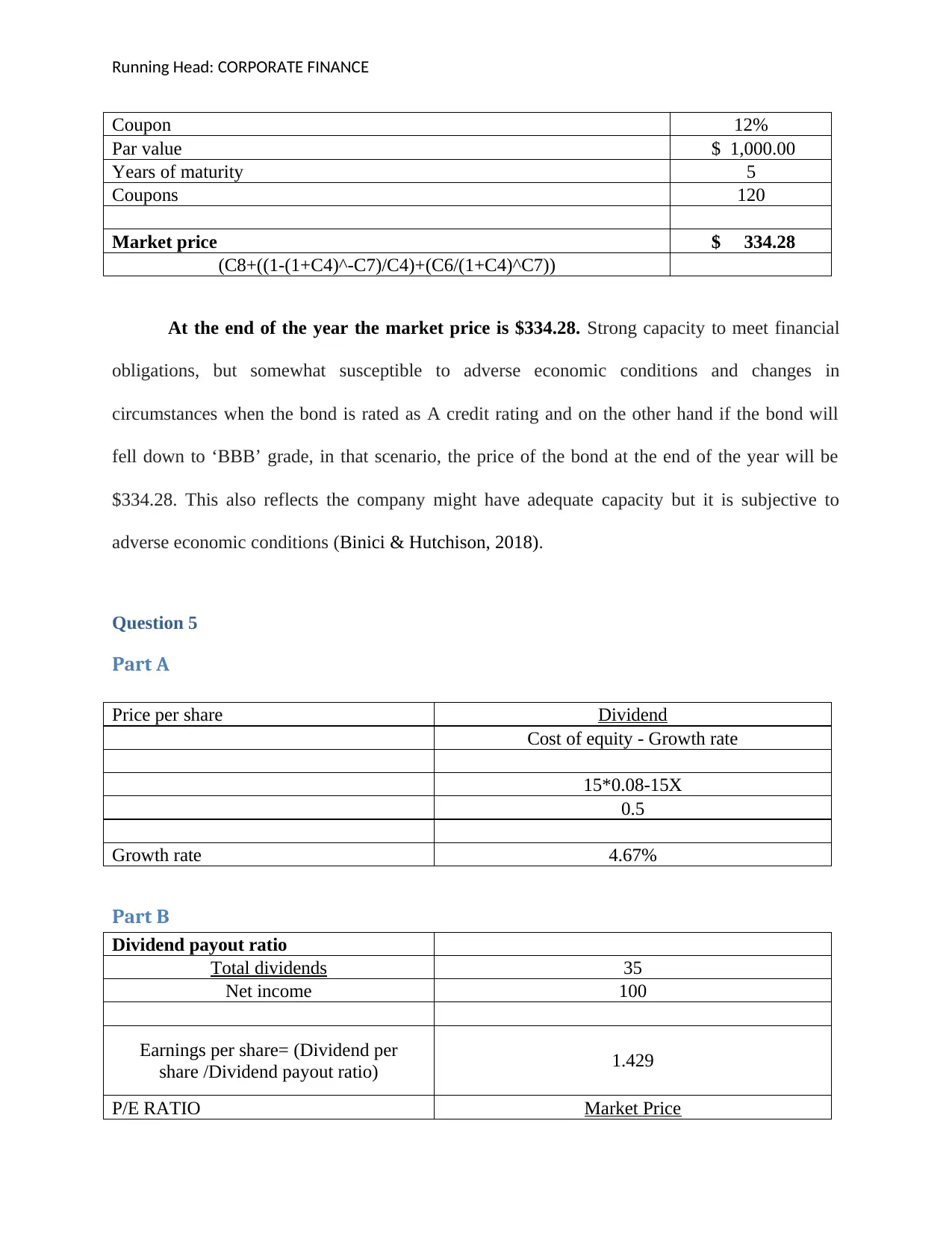

Particulars

YTM 3.80%

Running Head: CORPORATE FINANCE

Coupon 12%

Par value $ 1,000.00

Years of maturity 5

Coupons 120

Market price $ 334.28

(C8+((1-(1+C4)^-C7)/C4)+(C6/(1+C4)^C7))

At the end of the year the market price is $334.28. Strong capacity to meet financial

obligations, but somewhat susceptible to adverse economic conditions and changes in

circumstances when the bond is rated as A credit rating and on the other hand if the bond will

fell down to ‘BBB’ grade, in that scenario, the price of the bond at the end of the year will be

$334.28. This also reflects the company might have adequate capacity but it is subjective to

adverse economic conditions (Binici & Hutchison, 2018).

Question 5

Part A

Price per share Dividend

Cost of equity - Growth rate

15*0.08-15X

0.5

Growth rate 4.67%

Part B

Dividend payout ratio

Total dividends 35

Net income 100

Earnings per share= (Dividend per

share /Dividend payout ratio) 1.429

P/E RATIO Market Price

Coupon 12%

Par value $ 1,000.00

Years of maturity 5

Coupons 120

Market price $ 334.28

(C8+((1-(1+C4)^-C7)/C4)+(C6/(1+C4)^C7))

At the end of the year the market price is $334.28. Strong capacity to meet financial

obligations, but somewhat susceptible to adverse economic conditions and changes in

circumstances when the bond is rated as A credit rating and on the other hand if the bond will

fell down to ‘BBB’ grade, in that scenario, the price of the bond at the end of the year will be

$334.28. This also reflects the company might have adequate capacity but it is subjective to

adverse economic conditions (Binici & Hutchison, 2018).

Question 5

Part A

Price per share Dividend

Cost of equity - Growth rate

15*0.08-15X

0.5

Growth rate 4.67%

Part B

Dividend payout ratio

Total dividends 35

Net income 100

Earnings per share= (Dividend per

share /Dividend payout ratio) 1.429

P/E RATIO Market Price

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE FINANCE

EPS

15

1.429

P/E RATIO 10.5

Part C

If the management changes the strategy, the payout ratio will be reduced to 20% from

35% and this indicates that the growth strategy will also reduce to 7% from 12%. This clearly

implies that shareholders will have to bear enough losses and this will not at all maximize the

shareholder value, instead will reduce it. The dividend payout ratio which determines how much

value will be returned to the respective shareholders if fells down, it has a negative image on

mindset of shareholders and hence, this is not at all good strategy for MC, Company (Fitri,

Hosen & Muhari, 2016).

EPS

15

1.429

P/E RATIO 10.5

Part C

If the management changes the strategy, the payout ratio will be reduced to 20% from

35% and this indicates that the growth strategy will also reduce to 7% from 12%. This clearly

implies that shareholders will have to bear enough losses and this will not at all maximize the

shareholder value, instead will reduce it. The dividend payout ratio which determines how much

value will be returned to the respective shareholders if fells down, it has a negative image on

mindset of shareholders and hence, this is not at all good strategy for MC, Company (Fitri,

Hosen & Muhari, 2016).

Running Head: CORPORATE FINANCE

References

Binici, M., & Hutchison, M. (2018). Do credit rating agencies provide valuable information in

market evaluation of sovereign default Risk?. Journal of International Money and

Finance, 85, 58-75.

Fitri, R. R., Hosen, M. N., & Muhari, S. (2016). Analysis of factors that impact dividend payout

ratio on listed companies at Jakarta islamic index. International Journal of Academic

Research in Accounting, Finance and Management Sciences, 6(2), 87-97.

Iqbal, M. M. (2016). Two Flaws of the Net Present Value Criterion. Journal of Business &

Economics, 8(1).

Muda, I., & Hasibuan, A. N. (2017). Public Discovery of the Concept of Time Value of Money

with Economic Value of Time. Proceedings of MICoMS, 251-257.

References

Binici, M., & Hutchison, M. (2018). Do credit rating agencies provide valuable information in

market evaluation of sovereign default Risk?. Journal of International Money and

Finance, 85, 58-75.

Fitri, R. R., Hosen, M. N., & Muhari, S. (2016). Analysis of factors that impact dividend payout

ratio on listed companies at Jakarta islamic index. International Journal of Academic

Research in Accounting, Finance and Management Sciences, 6(2), 87-97.

Iqbal, M. M. (2016). Two Flaws of the Net Present Value Criterion. Journal of Business &

Economics, 8(1).

Muda, I., & Hasibuan, A. N. (2017). Public Discovery of the Concept of Time Value of Money

with Economic Value of Time. Proceedings of MICoMS, 251-257.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.