Corporate Finance and Reporting

VerifiedAdded on 2023/06/12

|9

|1585

|398

AI Summary

This article discusses impairment loss for cash generating units and journal entries for impairment loss occurring in 30 June 2015. It provides insights into IAS 36 and its impact on financial statements. The article also covers factors affecting impairment loss, adequate recognition method, and fair value method. The subject is corporate finance and reporting, and the course code and college/university are not mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE FINANCE AND REPORTING

Corporate Finance and Reporting

Name of the Student:

Name of the University:

Authors Note:

Corporate Finance and Reporting

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CORPORATE FINANCE AND REPORTING

1

Table of Contents

Part A: (Impairment loss for cash generating units excluding Goodwill).................................2

Part B: Journal entries prepared for the impairment loss occurring in 30 June 2015................4

Reference and Bibliography:......................................................................................................7

1

Table of Contents

Part A: (Impairment loss for cash generating units excluding Goodwill).................................2

Part B: Journal entries prepared for the impairment loss occurring in 30 June 2015................4

Reference and Bibliography:......................................................................................................7

CORPORATE FINANCE AND REPORTING

2

Part A: (Impairment loss for cash generating units excluding Goodwill)

Goodwill is relatively considered as not and impairment loss that needs to be carried

on during the calculation from the carrying amount of an asset of cash generating unit. The

calculations relatively indicate that the impairment loss is relatively depicted on units such as

plant, brand, and fittings, which are relatively considered one of the cash generating units for

an organisation. The impairment loss is relatively calculated by detecting the carrying amount

of the Asset or cash generating units which is derived after deducting depreciation and

impairment loss of a particular asset. However, certain factors such as recoverable amount,

net selling value, carrying amount and depreciation amount can be used for detecting the

overall impairment loss that an organisation has faced during the fiscal year. The impairment

loss relatively indicates the future declining value of a particular asset, which is considered as

a cash generating unit by the organisation. The impairment loss is calculated with the help of

IAS 36 regulation which indicates the different methods that can be used by companies to

detect their impairment loss in the balance sheet and income statement. This irrelevant

depiction of impairment loss in the financial accounts relatively reduces their financial

strength over time as the assets are the values and losses incurred by the company. From the

evaluation it is indicated that impairment loss is those amount, which exceeds future

undisclosed value of a particular assets the organisation (Chen 2018).

Adequate recognition method is a relatively depicted in IAS 36, which is used by

companies to detect the impairment loss of their assets. Moreover, the carrying amount value

is relatively considered before declaring an impairment loss, as the value needs to be created

and the recoverable amount of the assets. The impairment loss calculated by the organisation

is reflected in the comprehensive income statement, where IAS 16 standard directly in the

kids be fair value method which needs to be maintained by the organisation. The fair value

2

Part A: (Impairment loss for cash generating units excluding Goodwill)

Goodwill is relatively considered as not and impairment loss that needs to be carried

on during the calculation from the carrying amount of an asset of cash generating unit. The

calculations relatively indicate that the impairment loss is relatively depicted on units such as

plant, brand, and fittings, which are relatively considered one of the cash generating units for

an organisation. The impairment loss is relatively calculated by detecting the carrying amount

of the Asset or cash generating units which is derived after deducting depreciation and

impairment loss of a particular asset. However, certain factors such as recoverable amount,

net selling value, carrying amount and depreciation amount can be used for detecting the

overall impairment loss that an organisation has faced during the fiscal year. The impairment

loss relatively indicates the future declining value of a particular asset, which is considered as

a cash generating unit by the organisation. The impairment loss is calculated with the help of

IAS 36 regulation which indicates the different methods that can be used by companies to

detect their impairment loss in the balance sheet and income statement. This irrelevant

depiction of impairment loss in the financial accounts relatively reduces their financial

strength over time as the assets are the values and losses incurred by the company. From the

evaluation it is indicated that impairment loss is those amount, which exceeds future

undisclosed value of a particular assets the organisation (Chen 2018).

Adequate recognition method is a relatively depicted in IAS 36, which is used by

companies to detect the impairment loss of their assets. Moreover, the carrying amount value

is relatively considered before declaring an impairment loss, as the value needs to be created

and the recoverable amount of the assets. The impairment loss calculated by the organisation

is reflected in the comprehensive income statement, where IAS 16 standard directly in the

kids be fair value method which needs to be maintained by the organisation. The fair value

CORPORATE FINANCE AND REPORTING

3

method the relatively helps in shifting the actual value of the Asset and force the organisation

to conduct impairment loss on there be valued assets.

Impairment loss clause depicted in IAS 36 indicates the organisation to reduce the

Asset Value, when we are not carried more than the actual amount. However, the calculation

of impairment loss relatively nullifies the use of goodwill and certain intangible assets to be

deducted from the Asset Value. With the help of adequate test, the impairment loss of an

asset is detected which has the organisation to minimise the Asset Value over time in their

balance sheet. In this context. Guler (2016) stated that if the fair value of an asset the clients

below the carrying value then relevant impairment loss are recorded by the organisation to

comply with the changing values of the asset. On the other hand, Vasek et al. (2016)

companies directly use the loopholes in accounting measures to inflate their balance sheet

and decline the cash outflow from their operations. The use of impairment loss is used to

reduce the tax expenses and dividend expense by the organisation over the period of time.

The impairment loss can be conducted due to the changes in external sources used by

the organization such as the climb and market value, technology change, increment and

market interest rates, and economic loss. The occurrence of all the above measures would

directly change the relevant net asset value of the organization and increase the chance of

impairment loss. Impairment loss is relatively considered a reduction in asset value, which is

portrayed as a lost in the balance sheet. the payment loss is not considered the actual cash

outflow that is conducted by the organization over the period, while it is a theoretical loss,

which is obtained by the organization due to the production and its assets. IAS relatively

needs the organizations to value their Assets on market basis, which relatively change is the

due to the valuation method. The incremental value does not affect the balance sheet and

income statement of the organization whereas any kind of decline in the values of asset

directly result in impairment loss. Kabir, Rahman and Su (2017) status that the impairment

3

method the relatively helps in shifting the actual value of the Asset and force the organisation

to conduct impairment loss on there be valued assets.

Impairment loss clause depicted in IAS 36 indicates the organisation to reduce the

Asset Value, when we are not carried more than the actual amount. However, the calculation

of impairment loss relatively nullifies the use of goodwill and certain intangible assets to be

deducted from the Asset Value. With the help of adequate test, the impairment loss of an

asset is detected which has the organisation to minimise the Asset Value over time in their

balance sheet. In this context. Guler (2016) stated that if the fair value of an asset the clients

below the carrying value then relevant impairment loss are recorded by the organisation to

comply with the changing values of the asset. On the other hand, Vasek et al. (2016)

companies directly use the loopholes in accounting measures to inflate their balance sheet

and decline the cash outflow from their operations. The use of impairment loss is used to

reduce the tax expenses and dividend expense by the organisation over the period of time.

The impairment loss can be conducted due to the changes in external sources used by

the organization such as the climb and market value, technology change, increment and

market interest rates, and economic loss. The occurrence of all the above measures would

directly change the relevant net asset value of the organization and increase the chance of

impairment loss. Impairment loss is relatively considered a reduction in asset value, which is

portrayed as a lost in the balance sheet. the payment loss is not considered the actual cash

outflow that is conducted by the organization over the period, while it is a theoretical loss,

which is obtained by the organization due to the production and its assets. IAS relatively

needs the organizations to value their Assets on market basis, which relatively change is the

due to the valuation method. The incremental value does not affect the balance sheet and

income statement of the organization whereas any kind of decline in the values of asset

directly result in impairment loss. Kabir, Rahman and Su (2017) status that the impairment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CORPORATE FINANCE AND REPORTING

4

loss does not have any kind of negative impact on their cash flow statement as the expense is

a relatively considered paper transaction rather than cash flow transaction.

Therefore, it could be understood that with the help of IAS 36 organizations are able

to detect the impairment loss that needs to be conducted over the period, which is derived

after the valuation process (Iasplus.com 2018). The recoverable amount the disposable

amount and the fair value amount are relatively calculated with the help of impairment loss,

which would help in understanding the level of amount that will be deducted from the Asset

Value and profit and loss account. The overall cash flow projection is relatively based on

reasonable assumptions regarding the current value of the assets held by the organization. On

the other hand, with the help of fair value and carrying value detection organizations are able

to understand the level of impairment loss incurred in their current asset value.

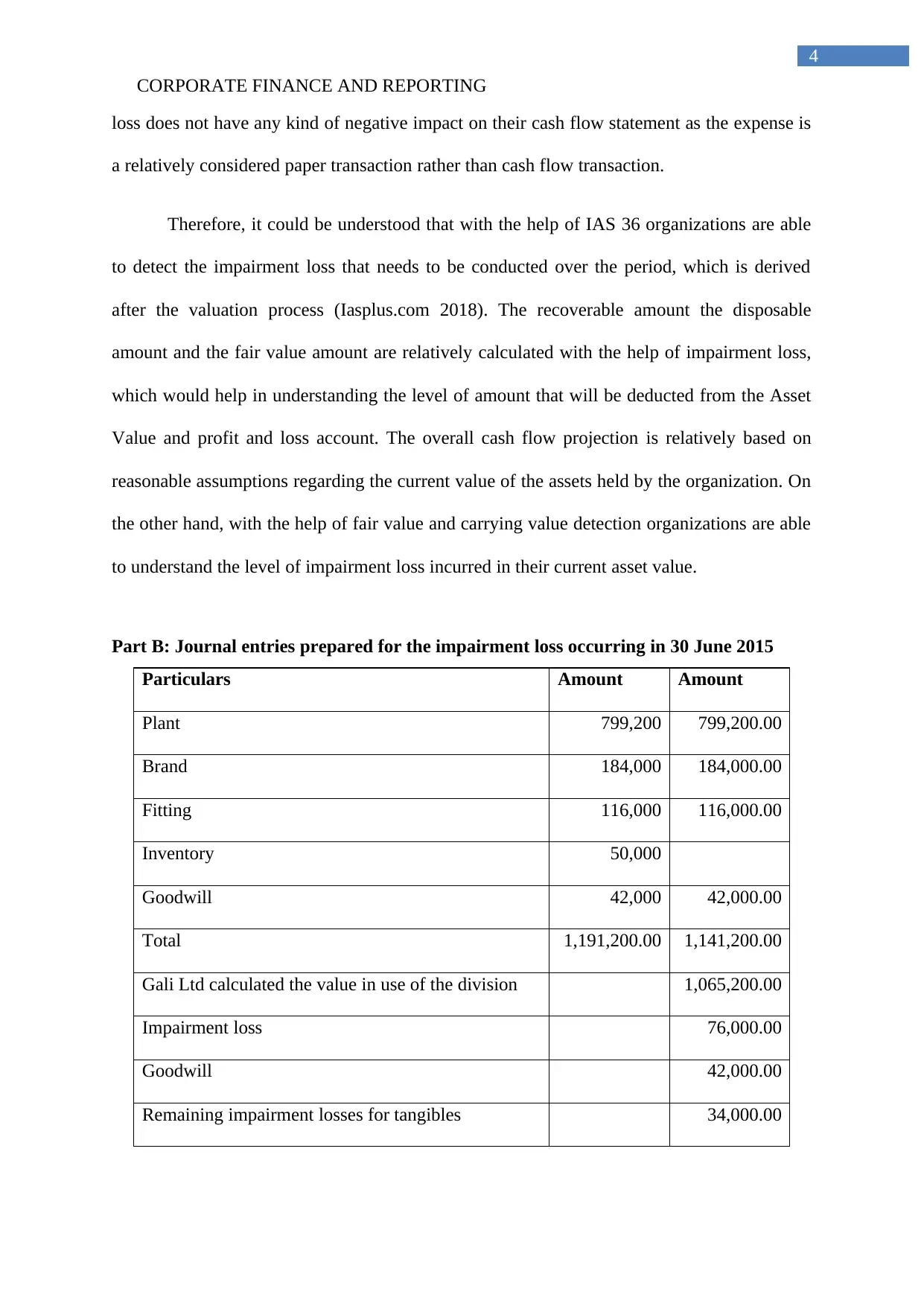

Part B: Journal entries prepared for the impairment loss occurring in 30 June 2015

Particulars Amount Amount

Plant 799,200 799,200.00

Brand 184,000 184,000.00

Fitting 116,000 116,000.00

Inventory 50,000

Goodwill 42,000 42,000.00

Total 1,191,200.00 1,141,200.00

Gali Ltd calculated the value in use of the division 1,065,200.00

Impairment loss 76,000.00

Goodwill 42,000.00

Remaining impairment losses for tangibles 34,000.00

4

loss does not have any kind of negative impact on their cash flow statement as the expense is

a relatively considered paper transaction rather than cash flow transaction.

Therefore, it could be understood that with the help of IAS 36 organizations are able

to detect the impairment loss that needs to be conducted over the period, which is derived

after the valuation process (Iasplus.com 2018). The recoverable amount the disposable

amount and the fair value amount are relatively calculated with the help of impairment loss,

which would help in understanding the level of amount that will be deducted from the Asset

Value and profit and loss account. The overall cash flow projection is relatively based on

reasonable assumptions regarding the current value of the assets held by the organization. On

the other hand, with the help of fair value and carrying value detection organizations are able

to understand the level of impairment loss incurred in their current asset value.

Part B: Journal entries prepared for the impairment loss occurring in 30 June 2015

Particulars Amount Amount

Plant 799,200 799,200.00

Brand 184,000 184,000.00

Fitting 116,000 116,000.00

Inventory 50,000

Goodwill 42,000 42,000.00

Total 1,191,200.00 1,141,200.00

Gali Ltd calculated the value in use of the division 1,065,200.00

Impairment loss 76,000.00

Goodwill 42,000.00

Remaining impairment losses for tangibles 34,000.00

CORPORATE FINANCE AND REPORTING

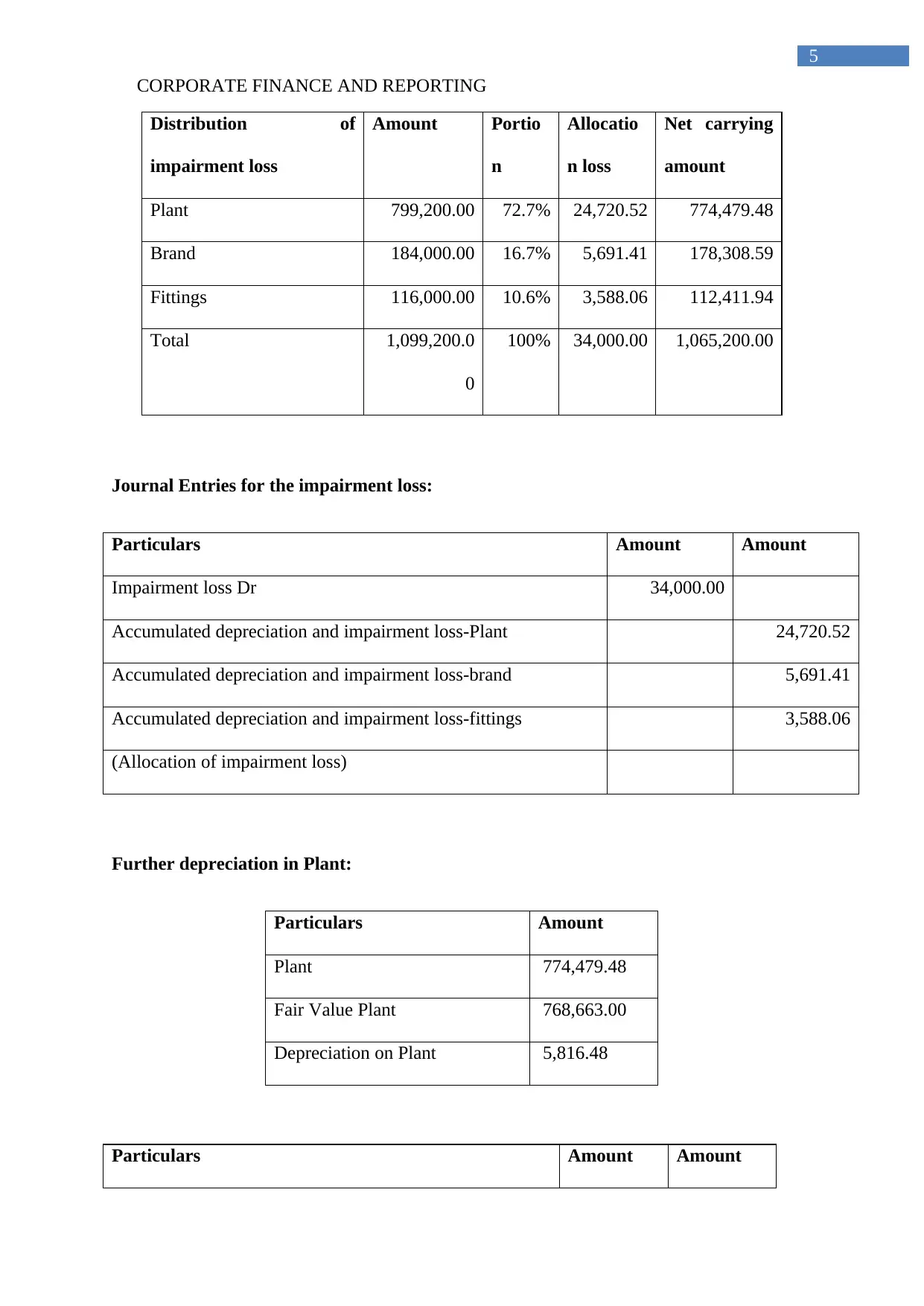

5

Distribution of

impairment loss

Amount Portio

n

Allocatio

n loss

Net carrying

amount

Plant 799,200.00 72.7% 24,720.52 774,479.48

Brand 184,000.00 16.7% 5,691.41 178,308.59

Fittings 116,000.00 10.6% 3,588.06 112,411.94

Total 1,099,200.0

0

100% 34,000.00 1,065,200.00

Journal Entries for the impairment loss:

Particulars Amount Amount

Impairment loss Dr 34,000.00

Accumulated depreciation and impairment loss-Plant 24,720.52

Accumulated depreciation and impairment loss-brand 5,691.41

Accumulated depreciation and impairment loss-fittings 3,588.06

(Allocation of impairment loss)

Further depreciation in Plant:

Particulars Amount

Plant 774,479.48

Fair Value Plant 768,663.00

Depreciation on Plant 5,816.48

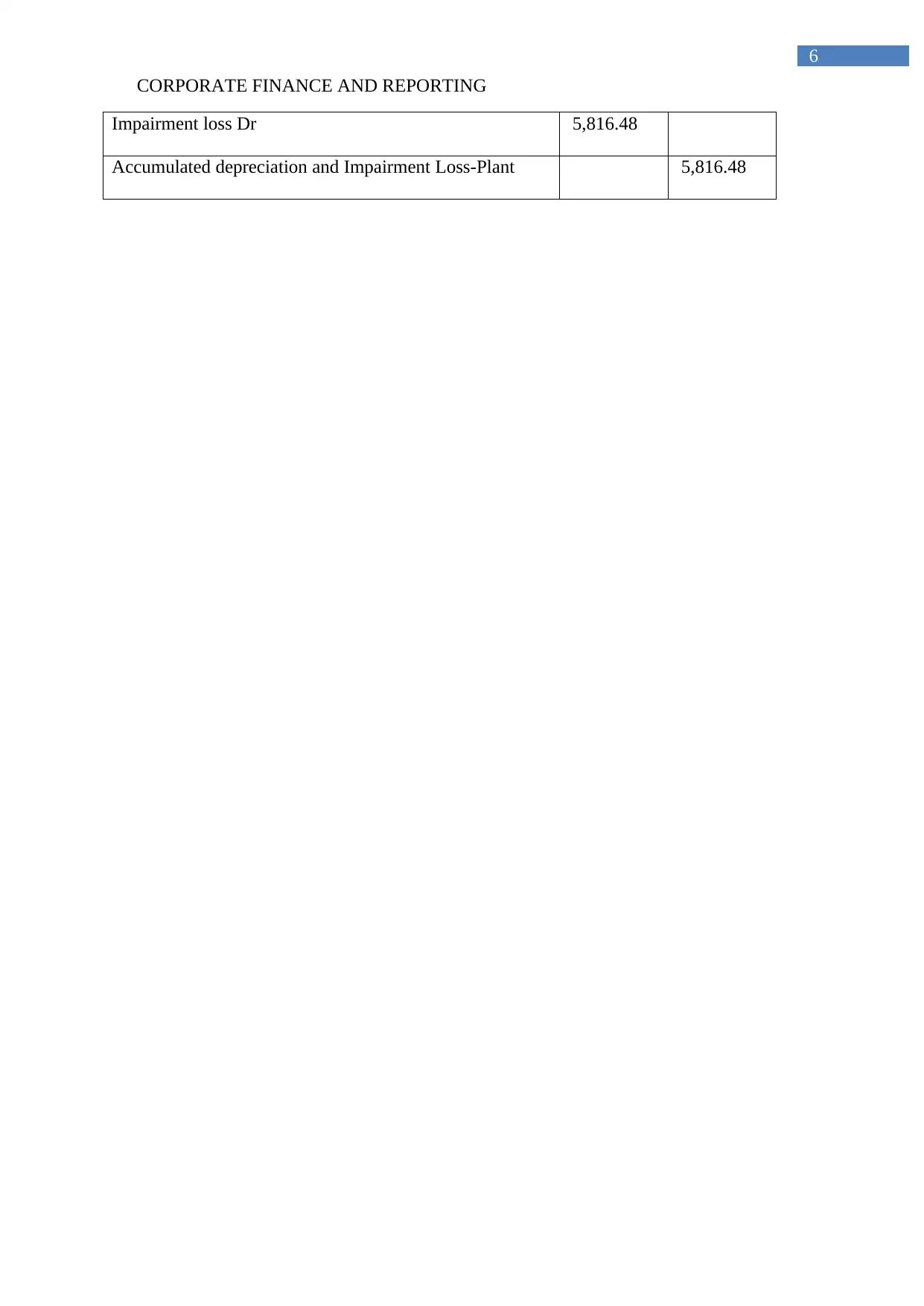

Particulars Amount Amount

5

Distribution of

impairment loss

Amount Portio

n

Allocatio

n loss

Net carrying

amount

Plant 799,200.00 72.7% 24,720.52 774,479.48

Brand 184,000.00 16.7% 5,691.41 178,308.59

Fittings 116,000.00 10.6% 3,588.06 112,411.94

Total 1,099,200.0

0

100% 34,000.00 1,065,200.00

Journal Entries for the impairment loss:

Particulars Amount Amount

Impairment loss Dr 34,000.00

Accumulated depreciation and impairment loss-Plant 24,720.52

Accumulated depreciation and impairment loss-brand 5,691.41

Accumulated depreciation and impairment loss-fittings 3,588.06

(Allocation of impairment loss)

Further depreciation in Plant:

Particulars Amount

Plant 774,479.48

Fair Value Plant 768,663.00

Depreciation on Plant 5,816.48

Particulars Amount Amount

CORPORATE FINANCE AND REPORTING

6

Impairment loss Dr 5,816.48

Accumulated depreciation and Impairment Loss-Plant 5,816.48

6

Impairment loss Dr 5,816.48

Accumulated depreciation and Impairment Loss-Plant 5,816.48

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE AND REPORTING

7

Reference and Bibliography:

Chen, B., Hui, J., Montgomery, K.S., Gella, A., Bolea, I., Sanz, E., Palmiter, R.D. and

Quintana, A., 2017. Loss of Mitochondrial Ndufs4 in Striatal Medium Spiny Neurons

Mediates Progressive Motor Impairment in a Mouse Model of Leigh Syndrome. Frontiers in

molecular neuroscience, 10, p.265.

Chen, L., 2018. 106. Research on the Formulation and Evolution of the Impairment Loss

Model of Financial Assets Based on the Expected Loss Model. Boletín Técnico, ISSN: 0376-

723X, 55(18).

Guler, L., 2016. Has SFAS 142 improved the usefulness of goodwill impairment loss and

goodwill balances for investors?. Review of Managerial Science, pp.1-34.

Iasplus.com. (2018). IAS 36 — Impairment of Assets. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias36 [Accessed 9 Jan. 2018].

Kabir, H., Rahman, A.R. and Su, L., 2017. The Association between Goodwill Impairment

Loss and Goodwill Impairment Test-Related Disclosures in Australia.

Matos, N., Castro, L., Boschetti, D. and Glisoi, S., 2015. Comparative Analysis of Functional

Profile of People with Intellectual Disability Aged with the Diagnosis of Degree of

Impairment Loss of Childhood-Adolescence. European Psychiatry, 30, p.1472.

Pagnussat, N., Almeida, A.S., Marques, D.M., Nunes, F., Chenet, G.C., Botton, P.H.S.,

Mioranzza, S., Loss, C.M., Cunha, R.A. and Porciúncula, L.O., 2015. Adenosine A2A

receptors are necessary and sufficient to trigger memory impairment in adult mice. British

journal of pharmacology, 172(15), pp.3831-3845.

7

Reference and Bibliography:

Chen, B., Hui, J., Montgomery, K.S., Gella, A., Bolea, I., Sanz, E., Palmiter, R.D. and

Quintana, A., 2017. Loss of Mitochondrial Ndufs4 in Striatal Medium Spiny Neurons

Mediates Progressive Motor Impairment in a Mouse Model of Leigh Syndrome. Frontiers in

molecular neuroscience, 10, p.265.

Chen, L., 2018. 106. Research on the Formulation and Evolution of the Impairment Loss

Model of Financial Assets Based on the Expected Loss Model. Boletín Técnico, ISSN: 0376-

723X, 55(18).

Guler, L., 2016. Has SFAS 142 improved the usefulness of goodwill impairment loss and

goodwill balances for investors?. Review of Managerial Science, pp.1-34.

Iasplus.com. (2018). IAS 36 — Impairment of Assets. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias36 [Accessed 9 Jan. 2018].

Kabir, H., Rahman, A.R. and Su, L., 2017. The Association between Goodwill Impairment

Loss and Goodwill Impairment Test-Related Disclosures in Australia.

Matos, N., Castro, L., Boschetti, D. and Glisoi, S., 2015. Comparative Analysis of Functional

Profile of People with Intellectual Disability Aged with the Diagnosis of Degree of

Impairment Loss of Childhood-Adolescence. European Psychiatry, 30, p.1472.

Pagnussat, N., Almeida, A.S., Marques, D.M., Nunes, F., Chenet, G.C., Botton, P.H.S.,

Mioranzza, S., Loss, C.M., Cunha, R.A. and Porciúncula, L.O., 2015. Adenosine A2A

receptors are necessary and sufficient to trigger memory impairment in adult mice. British

journal of pharmacology, 172(15), pp.3831-3845.

CORPORATE FINANCE AND REPORTING

8

Vasek, M.J., Garber, C., Dorsey, D., Durrant, D.M., Bollman, B., Soung, A., Yu, J., Perez-

Torres, C., Frouin, A., Wilton, D.K. and Funk, K., 2016. A complement–microglial axis

drives synapse loss during virus-induced memory impairment. Nature, 534(7608), p.538.

8

Vasek, M.J., Garber, C., Dorsey, D., Durrant, D.M., Bollman, B., Soung, A., Yu, J., Perez-

Torres, C., Frouin, A., Wilton, D.K. and Funk, K., 2016. A complement–microglial axis

drives synapse loss during virus-induced memory impairment. Nature, 534(7608), p.538.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.