Corporate Finance and Reporting: Impairment Loss and Journal Entries

VerifiedAdded on 2023/06/12

|9

|1585

|398

Report

AI Summary

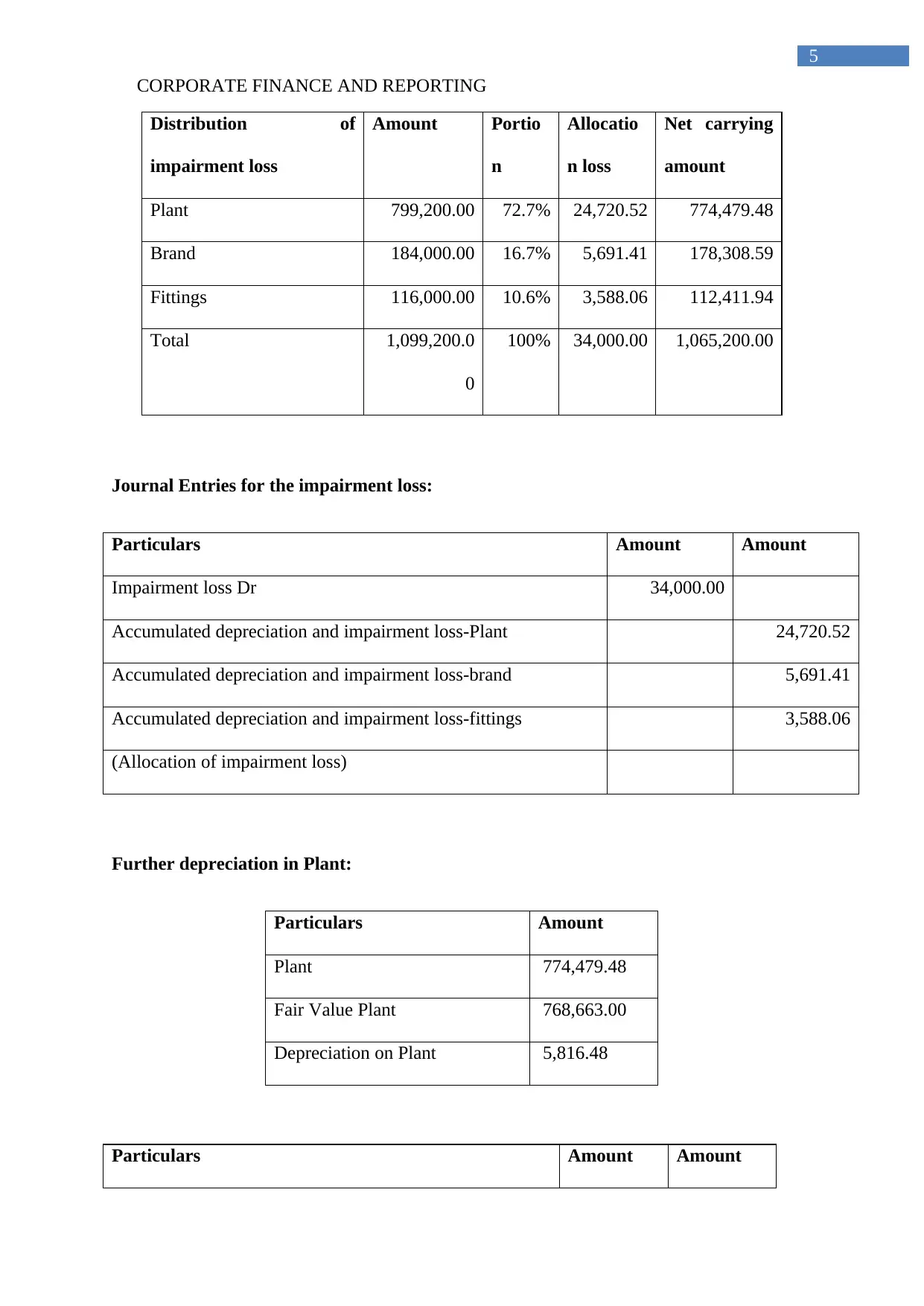

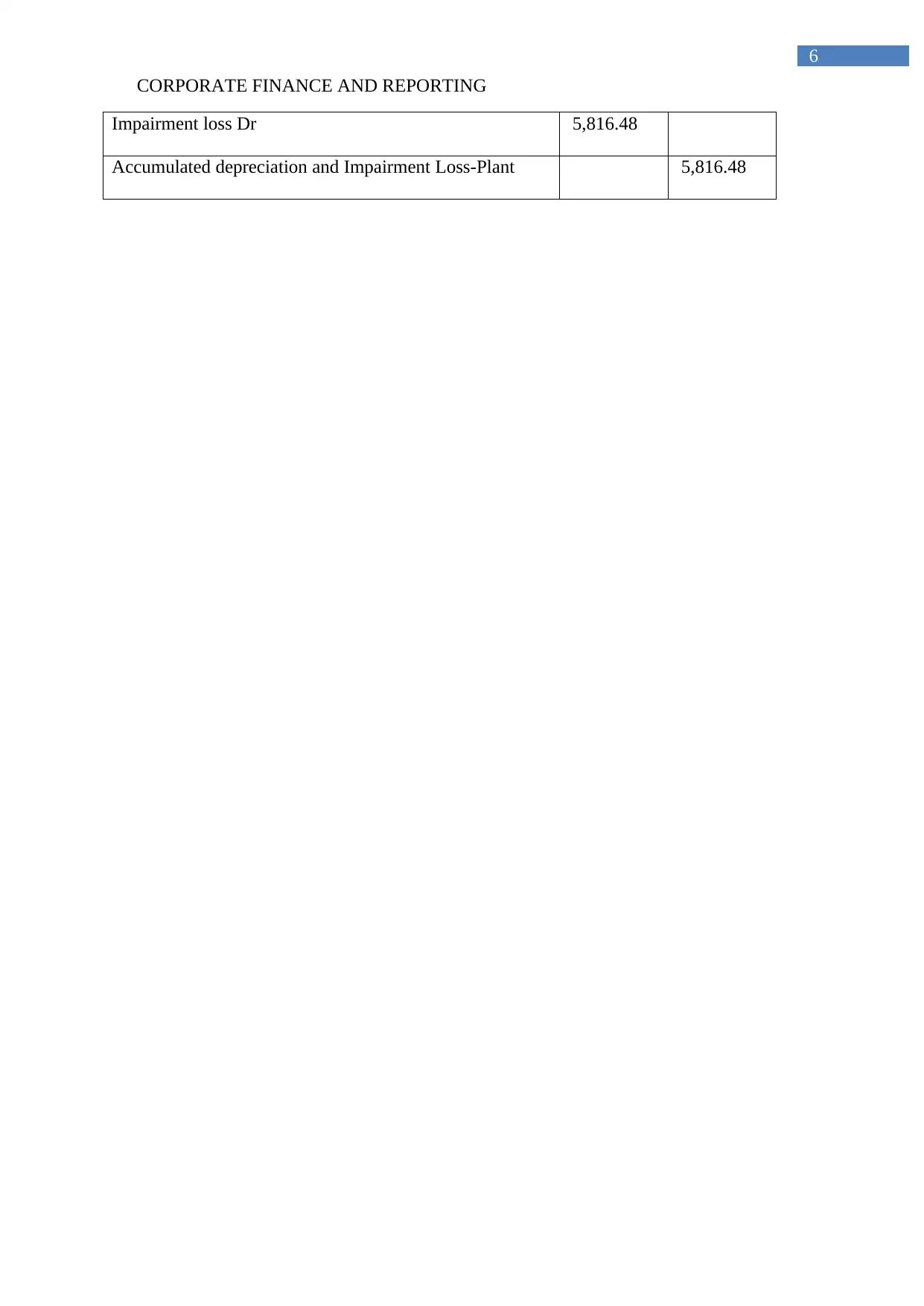

This report provides an analysis of impairment loss within the context of corporate finance and reporting. It begins by discussing the concept of impairment loss for cash-generating units, excluding goodwill, and explains how it is calculated using factors like carrying amount, recoverable amount, and net selling value, in accordance with IAS 36 regulations. The report highlights the impact of impairment loss on financial statements and its role in reflecting the declining value of assets. It further explores how companies may use impairment loss to manage their tax expenses and dividend payouts. The second part of the report presents journal entries for an impairment loss scenario occurring on June 30, 2015, demonstrating the allocation of the loss across different assets like plant, brand, and fittings. The document concludes by detailing the further depreciation of the plant asset after the initial impairment loss.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.