Corporate Finance: Investment, Capital Structure and Dividend Policy

VerifiedAdded on 2023/06/04

|8

|1604

|178

Homework Assignment

AI Summary

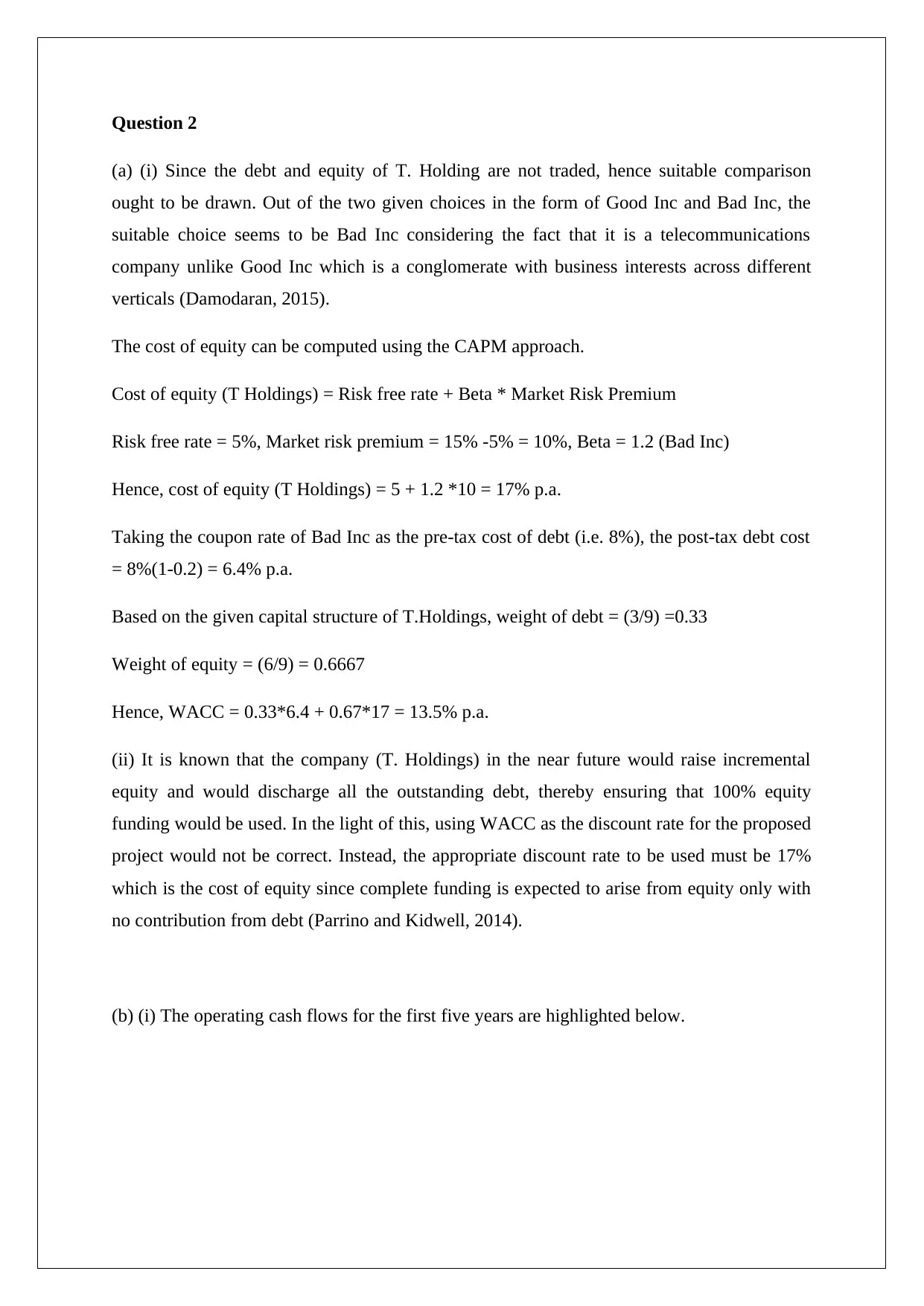

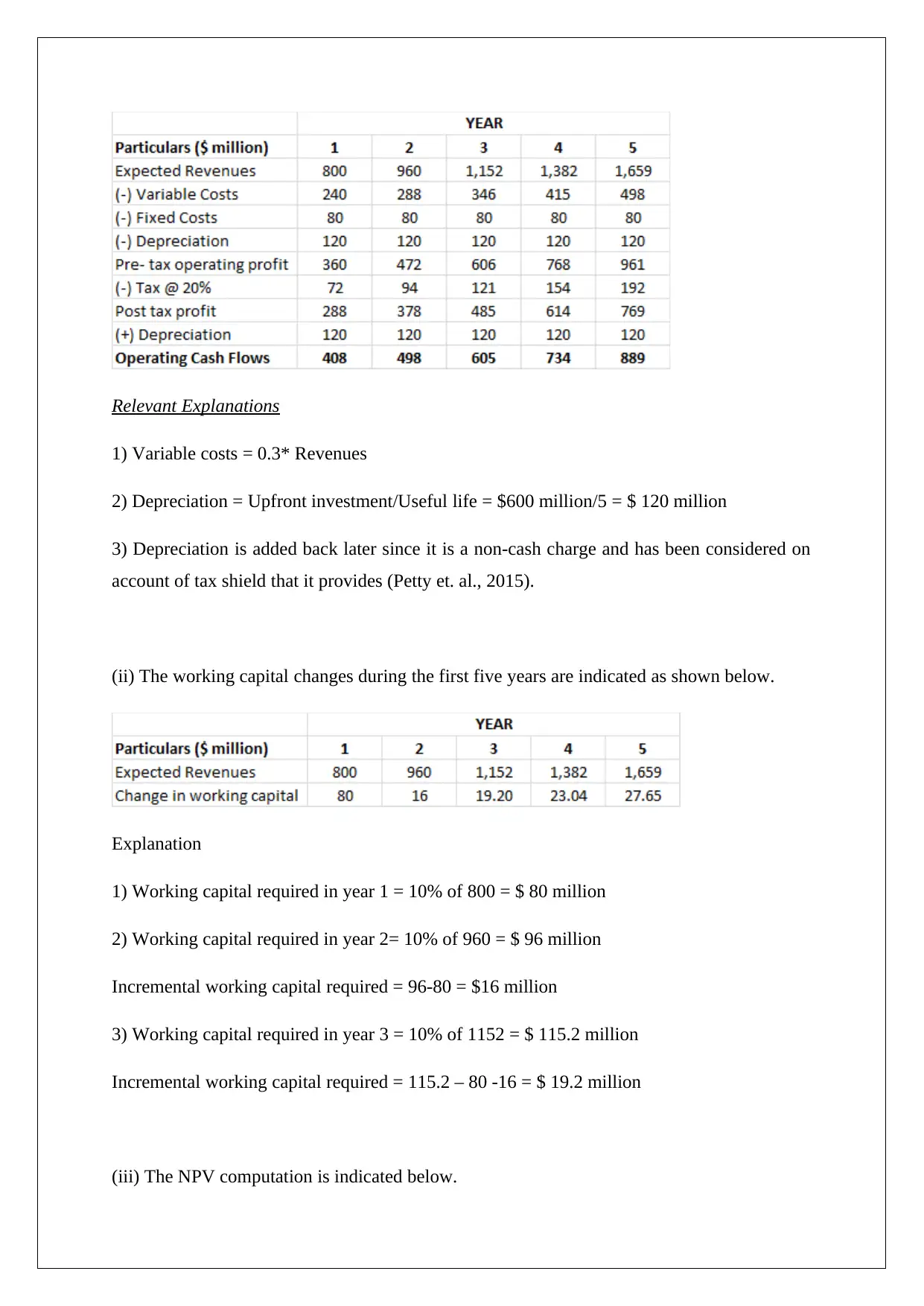

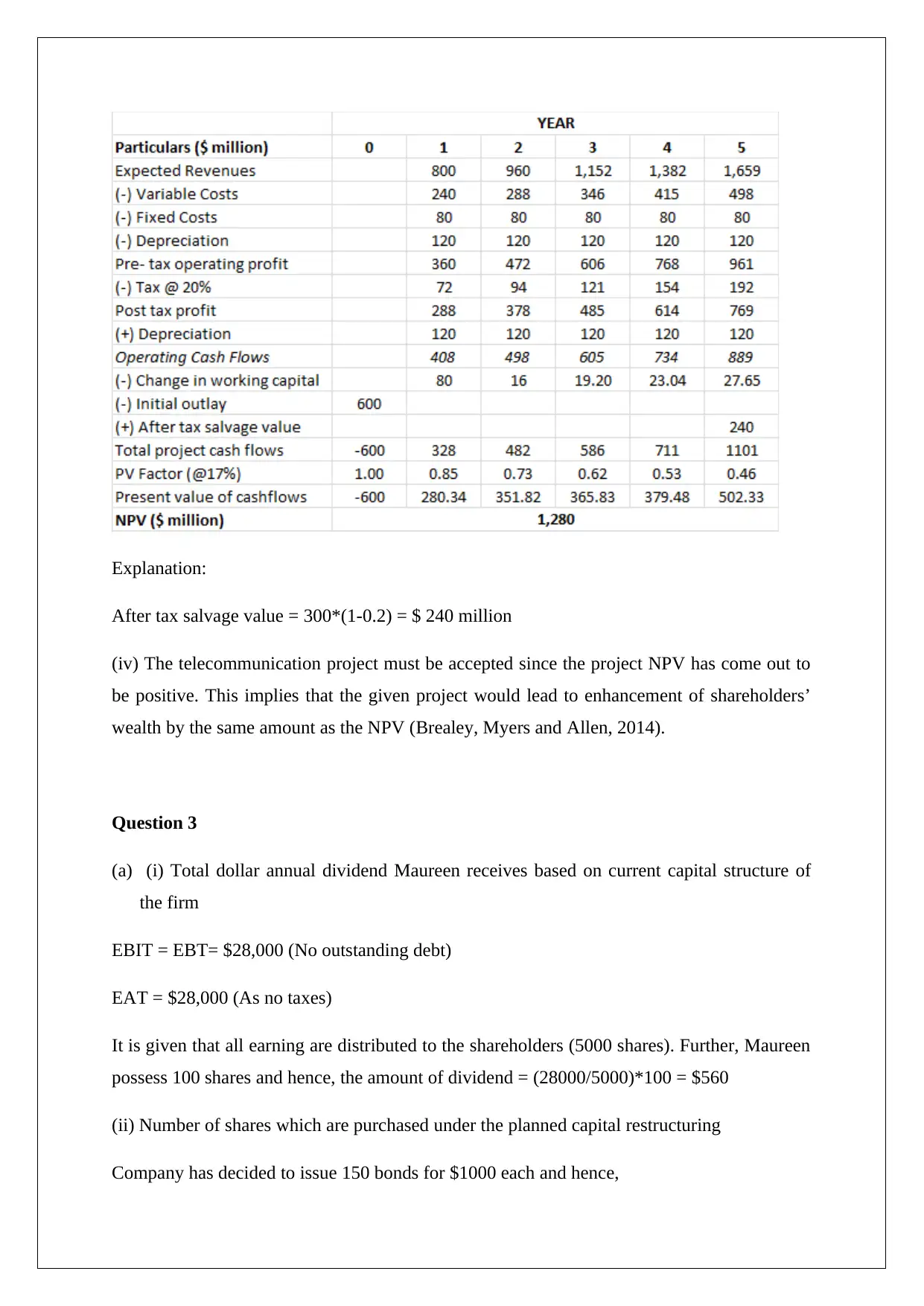

This corporate finance assignment solution addresses key concepts such as capital structure, investment analysis, and dividend policy. It begins by determining the appropriate cost of equity and WACC for T. Holdings, considering its capital structure and potential future equity funding. The solution then evaluates a telecommunications project by calculating operating cash flows, working capital changes, and NPV, ultimately recommending acceptance based on the positive NPV. Furthermore, the assignment analyzes the impact of capital restructuring on dividend payouts, considering both scenarios with and without taxes, and discusses the relevance of Miller & Modigliani propositions. The analysis includes calculating dividend amounts for different capital structures and evaluating Maureen's cash flows under homemade leverage, providing a comprehensive overview of corporate finance principles. Desklib offers a wide range of study tools, including past papers and solved assignments, to aid students in their academic pursuits.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.