LLP221 Corporate Finance: Financial Modeling and Revenue Projection

VerifiedAdded on 2023/06/12

|15

|3022

|345

Homework Assignment

AI Summary

This assignment solution delves into key corporate finance concepts, beginning with trend extrapolation methods for sales forecasting, comparing historical nominal and real growth rates, weighting historical growth rates, and using fundamentals based on GDP changes. It identifies the historical nominal growth rate as the most effective approach for sales growth. The solution also includes a sensitivity analysis for Take Five Systems, a startup developing a new app, examining various sales levels and growth rates under different scenarios, including changes in development time, unit sales, and selling prices, to determine the most favorable conditions for revenue generation. Finally, it provides a revenue forecast for a membership-based business, comparing actual and forecasted performance to assess the effectiveness of proposed revenue-increasing strategies.

LLP221 Corporate Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK...............................................................................................................................................3

Question 1...............................................................................................................................3

Question 2...............................................................................................................................8

Question 3.............................................................................................................................11

Question 4.............................................................................................................................13

Question 5.............................................................................................................................14

TASK...............................................................................................................................................3

Question 1...............................................................................................................................3

Question 2...............................................................................................................................8

Question 3.............................................................................................................................11

Question 4.............................................................................................................................13

Question 5.............................................................................................................................14

TASK

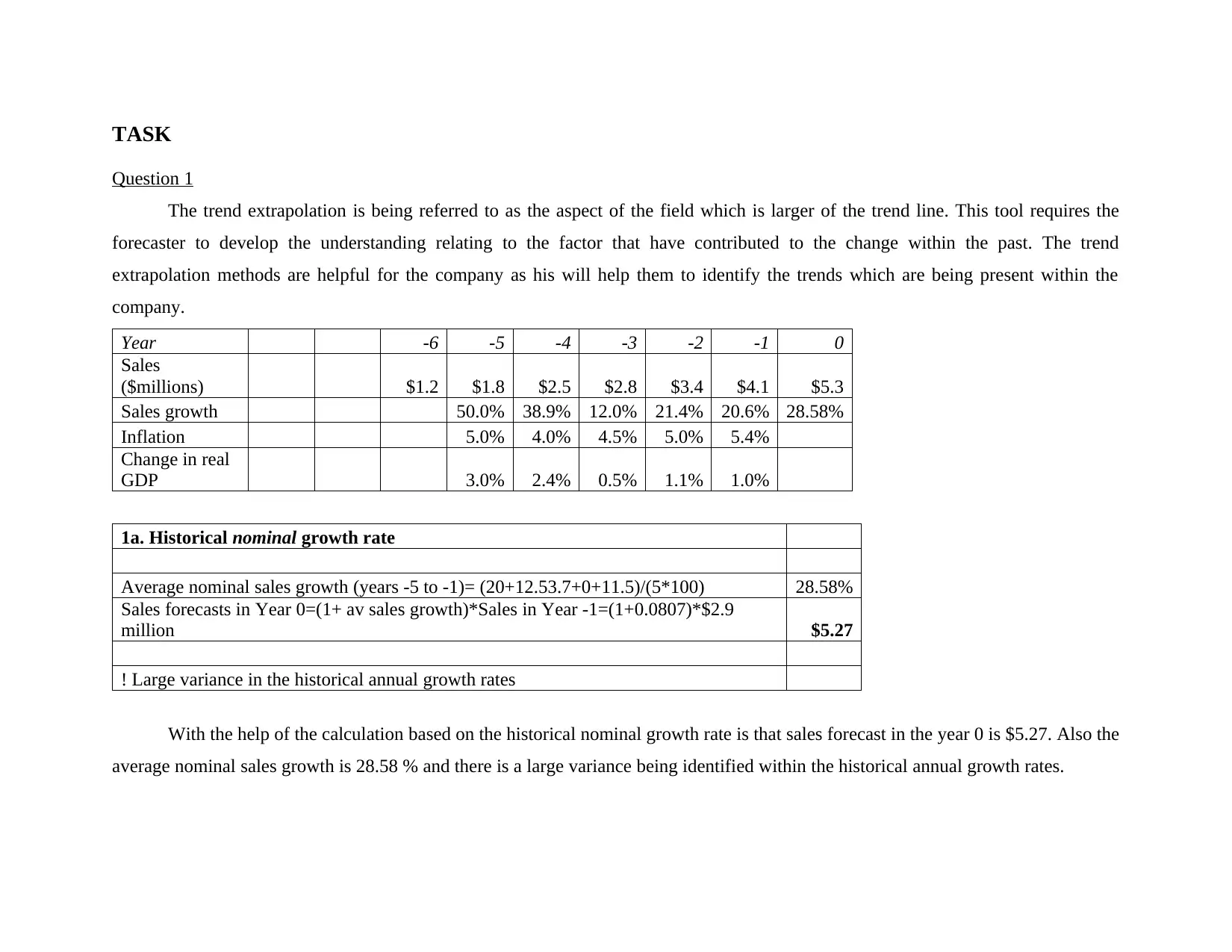

Question 1

The trend extrapolation is being referred to as the aspect of the field which is larger of the trend line. This tool requires the

forecaster to develop the understanding relating to the factor that have contributed to the change within the past. The trend

extrapolation methods are helpful for the company as his will help them to identify the trends which are being present within the

company.

Year -6 -5 -4 -3 -2 -1 0

Sales

($millions) $1.2 $1.8 $2.5 $2.8 $3.4 $4.1 $5.3

Sales growth 50.0% 38.9% 12.0% 21.4% 20.6% 28.58%

Inflation 5.0% 4.0% 4.5% 5.0% 5.4%

Change in real

GDP 3.0% 2.4% 0.5% 1.1% 1.0%

1a. Historical nominal growth rate

Average nominal sales growth (years -5 to -1)= (20+12.53.7+0+11.5)/(5*100) 28.58%

Sales forecasts in Year 0=(1+ av sales growth)*Sales in Year -1=(1+0.0807)*$2.9

million $5.27

! Large variance in the historical annual growth rates

With the help of the calculation based on the historical nominal growth rate is that sales forecast in the year 0 is $5.27. Also the

average nominal sales growth is 28.58 % and there is a large variance being identified within the historical annual growth rates.

Question 1

The trend extrapolation is being referred to as the aspect of the field which is larger of the trend line. This tool requires the

forecaster to develop the understanding relating to the factor that have contributed to the change within the past. The trend

extrapolation methods are helpful for the company as his will help them to identify the trends which are being present within the

company.

Year -6 -5 -4 -3 -2 -1 0

Sales

($millions) $1.2 $1.8 $2.5 $2.8 $3.4 $4.1 $5.3

Sales growth 50.0% 38.9% 12.0% 21.4% 20.6% 28.58%

Inflation 5.0% 4.0% 4.5% 5.0% 5.4%

Change in real

GDP 3.0% 2.4% 0.5% 1.1% 1.0%

1a. Historical nominal growth rate

Average nominal sales growth (years -5 to -1)= (20+12.53.7+0+11.5)/(5*100) 28.58%

Sales forecasts in Year 0=(1+ av sales growth)*Sales in Year -1=(1+0.0807)*$2.9

million $5.27

! Large variance in the historical annual growth rates

With the help of the calculation based on the historical nominal growth rate is that sales forecast in the year 0 is $5.27. Also the

average nominal sales growth is 28.58 % and there is a large variance being identified within the historical annual growth rates.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

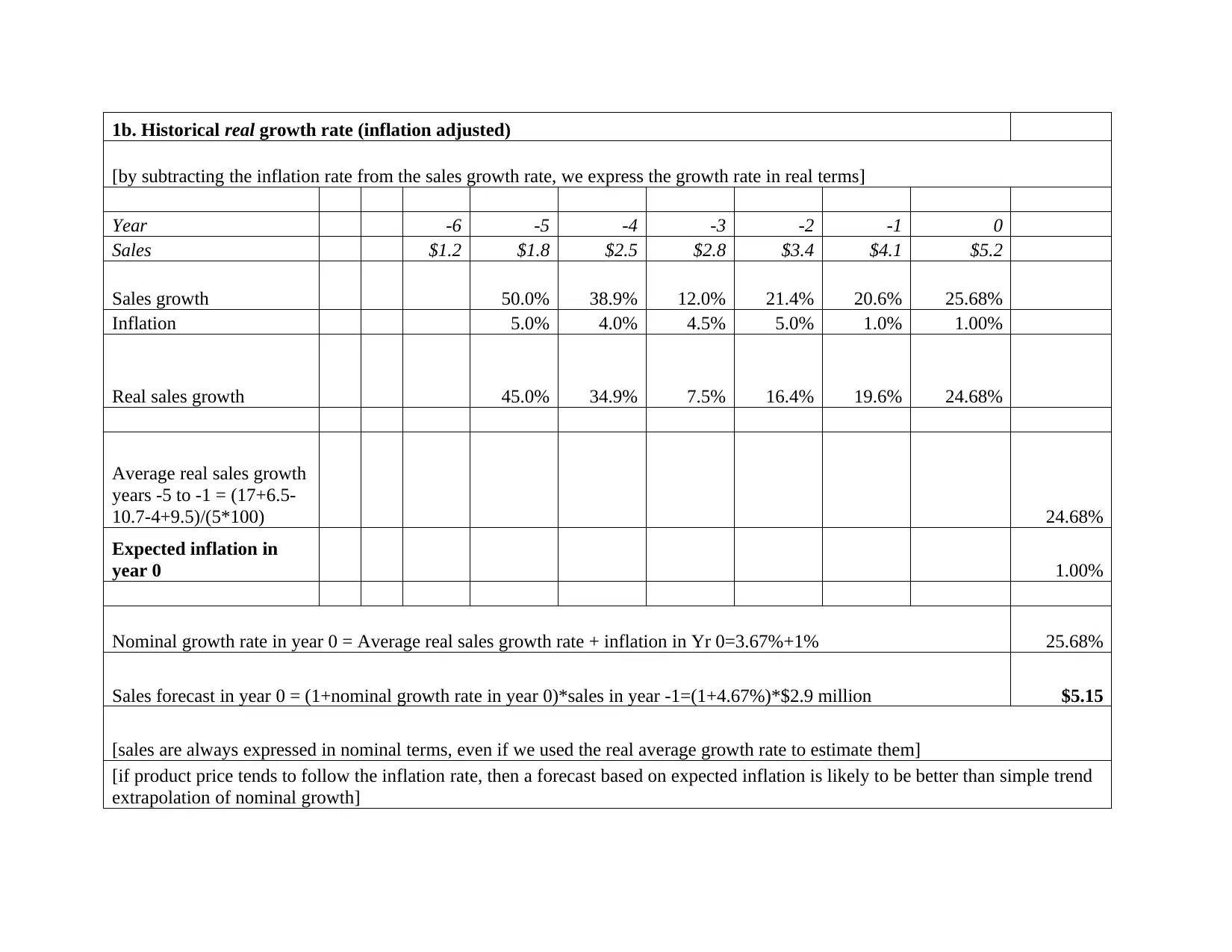

1b. Historical real growth rate (inflation adjusted)

[by subtracting the inflation rate from the sales growth rate, we express the growth rate in real terms]

Year -6 -5 -4 -3 -2 -1 0

Sales $1.2 $1.8 $2.5 $2.8 $3.4 $4.1 $5.2

Sales growth 50.0% 38.9% 12.0% 21.4% 20.6% 25.68%

Inflation 5.0% 4.0% 4.5% 5.0% 1.0% 1.00%

Real sales growth 45.0% 34.9% 7.5% 16.4% 19.6% 24.68%

Average real sales growth

years -5 to -1 = (17+6.5-

10.7-4+9.5)/(5*100) 24.68%

Expected inflation in

year 0 1.00%

Nominal growth rate in year 0 = Average real sales growth rate + inflation in Yr 0=3.67%+1% 25.68%

Sales forecast in year 0 = (1+nominal growth rate in year 0)*sales in year -1=(1+4.67%)*$2.9 million $5.15

[sales are always expressed in nominal terms, even if we used the real average growth rate to estimate them]

[if product price tends to follow the inflation rate, then a forecast based on expected inflation is likely to be better than simple trend

extrapolation of nominal growth]

[by subtracting the inflation rate from the sales growth rate, we express the growth rate in real terms]

Year -6 -5 -4 -3 -2 -1 0

Sales $1.2 $1.8 $2.5 $2.8 $3.4 $4.1 $5.2

Sales growth 50.0% 38.9% 12.0% 21.4% 20.6% 25.68%

Inflation 5.0% 4.0% 4.5% 5.0% 1.0% 1.00%

Real sales growth 45.0% 34.9% 7.5% 16.4% 19.6% 24.68%

Average real sales growth

years -5 to -1 = (17+6.5-

10.7-4+9.5)/(5*100) 24.68%

Expected inflation in

year 0 1.00%

Nominal growth rate in year 0 = Average real sales growth rate + inflation in Yr 0=3.67%+1% 25.68%

Sales forecast in year 0 = (1+nominal growth rate in year 0)*sales in year -1=(1+4.67%)*$2.9 million $5.15

[sales are always expressed in nominal terms, even if we used the real average growth rate to estimate them]

[if product price tends to follow the inflation rate, then a forecast based on expected inflation is likely to be better than simple trend

extrapolation of nominal growth]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In addition to this with the help of real growth rate that is inflation adjusted it is clear that the sales forecast for the year 0 is

s$5.15. But in actual the sales for the year is $5.2 and the nominal growth rate within the year 0 is 25.68% and in against of this the

average real sales growth is only 24.68%. This particularly implies that in case of inflation adjusted rate, the growth rate is mote but

the sales forecast is very slight different from the past performance. It is also assumed that the sales are always expressed in the terms

of nominal value even in case the real average growth rate is estimated. Also, in case the prices of the product tend to comply with the

inflation rate then this forecast based on the inflation will be better in comparison to the simply trend extrapolation of the nominal

growth rate. On the other hand, in case the inflation is not included then the company go with the nominal growth rate.

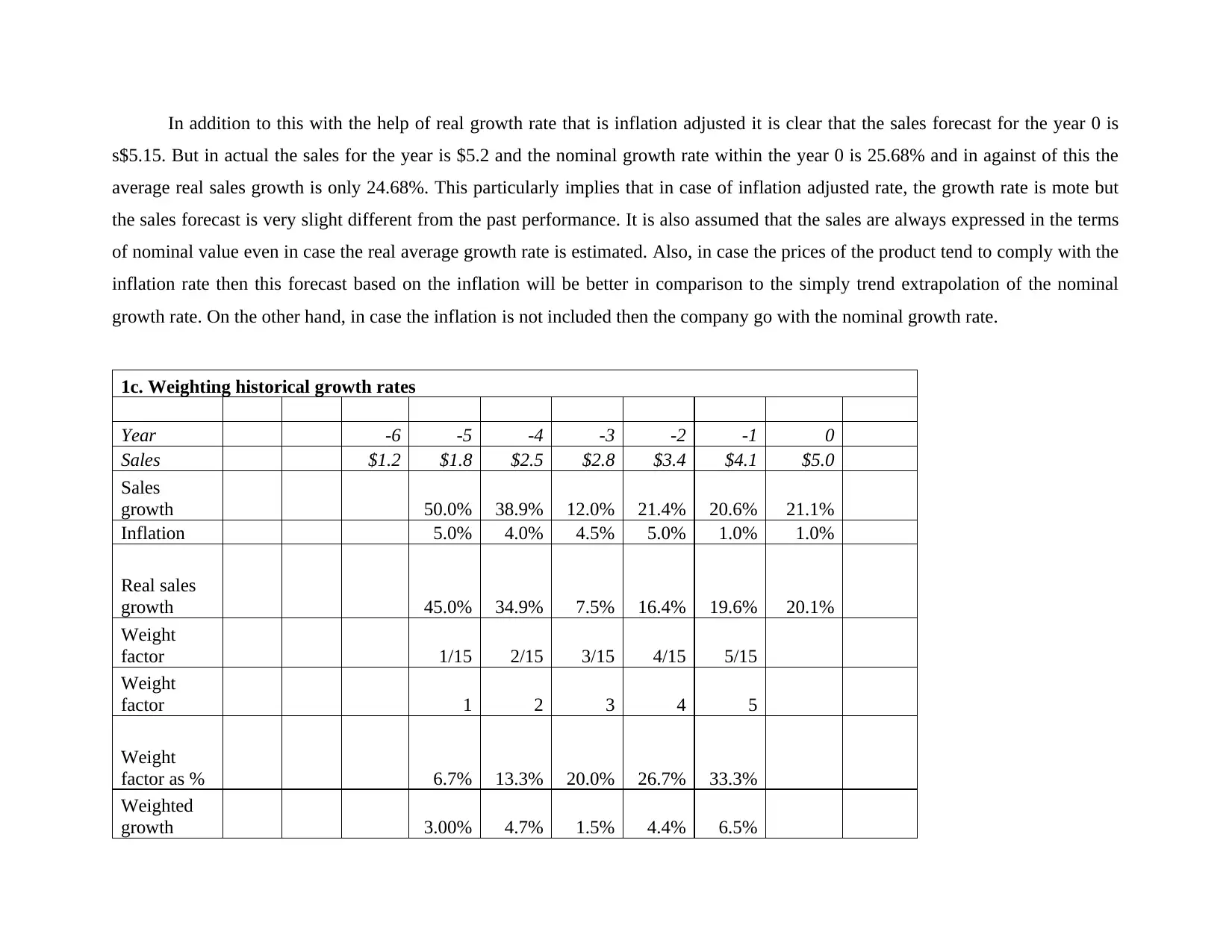

1c. Weighting historical growth rates

Year -6 -5 -4 -3 -2 -1 0

Sales $1.2 $1.8 $2.5 $2.8 $3.4 $4.1 $5.0

Sales

growth 50.0% 38.9% 12.0% 21.4% 20.6% 21.1%

Inflation 5.0% 4.0% 4.5% 5.0% 1.0% 1.0%

Real sales

growth 45.0% 34.9% 7.5% 16.4% 19.6% 20.1%

Weight

factor 1/15 2/15 3/15 4/15 5/15

Weight

factor 1 2 3 4 5

Weight

factor as % 6.7% 13.3% 20.0% 26.7% 33.3%

Weighted

growth 3.00% 4.7% 1.5% 4.4% 6.5%

s$5.15. But in actual the sales for the year is $5.2 and the nominal growth rate within the year 0 is 25.68% and in against of this the

average real sales growth is only 24.68%. This particularly implies that in case of inflation adjusted rate, the growth rate is mote but

the sales forecast is very slight different from the past performance. It is also assumed that the sales are always expressed in the terms

of nominal value even in case the real average growth rate is estimated. Also, in case the prices of the product tend to comply with the

inflation rate then this forecast based on the inflation will be better in comparison to the simply trend extrapolation of the nominal

growth rate. On the other hand, in case the inflation is not included then the company go with the nominal growth rate.

1c. Weighting historical growth rates

Year -6 -5 -4 -3 -2 -1 0

Sales $1.2 $1.8 $2.5 $2.8 $3.4 $4.1 $5.0

Sales

growth 50.0% 38.9% 12.0% 21.4% 20.6% 21.1%

Inflation 5.0% 4.0% 4.5% 5.0% 1.0% 1.0%

Real sales

growth 45.0% 34.9% 7.5% 16.4% 19.6% 20.1%

Weight

factor 1/15 2/15 3/15 4/15 5/15

Weight

factor 1 2 3 4 5

Weight

factor as % 6.7% 13.3% 20.0% 26.7% 33.3%

Weighted

growth 3.00% 4.7% 1.5% 4.4% 6.5%

Real sales growth = (1.1+0.9-2.1-1.1+3.2)/100 20.06%

[this weighted forecast is below the average real sales forecast of 3.67%, in large part because the high

growth rate of 17% in year -5 carries less weight in the weighted average than the negative growth rates

in years -3 and -2]

By evaluating the above calculation based on the weighting historical growth rate it is clear that when the weight factor is

being allotted then the real sales growth rate is 20.06 %. By assigning the weights it is clear that the real sales growth rate has declined

more. Thus, with this it is clear that the use of weight is not good for the company because the real forecast of sales is 3.67 % and

because year 5 carries less weight as compared to the weighted average. Also there is negative growth rate in years -3 and -2 and

because of this as well the real sales growth of the company has been reduced.

1d. Based on fundamentals

Year -6 -5 -4 -3 -2 -1 0

Sales $1.2 $1.8 $2.5 $2.8 $3.4 $4.1 $4.4

Sales

Growth 50.0% 38.9% 12.0% 21.4% 20.6% 8.5%

Change in

real GDP 3.0% 2.4% 0.5% 1.1% 1.5% 2.5%

Real sales

growth 45.0% 34.9% 7.5% 16.4% 19.6% 7.5%

[this weighted forecast is below the average real sales forecast of 3.67%, in large part because the high

growth rate of 17% in year -5 carries less weight in the weighted average than the negative growth rates

in years -3 and -2]

By evaluating the above calculation based on the weighting historical growth rate it is clear that when the weight factor is

being allotted then the real sales growth rate is 20.06 %. By assigning the weights it is clear that the real sales growth rate has declined

more. Thus, with this it is clear that the use of weight is not good for the company because the real forecast of sales is 3.67 % and

because year 5 carries less weight as compared to the weighted average. Also there is negative growth rate in years -3 and -2 and

because of this as well the real sales growth of the company has been reduced.

1d. Based on fundamentals

Year -6 -5 -4 -3 -2 -1 0

Sales $1.2 $1.8 $2.5 $2.8 $3.4 $4.1 $4.4

Sales

Growth 50.0% 38.9% 12.0% 21.4% 20.6% 8.5%

Change in

real GDP 3.0% 2.4% 0.5% 1.1% 1.5% 2.5%

Real sales

growth 45.0% 34.9% 7.5% 16.4% 19.6% 7.5%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

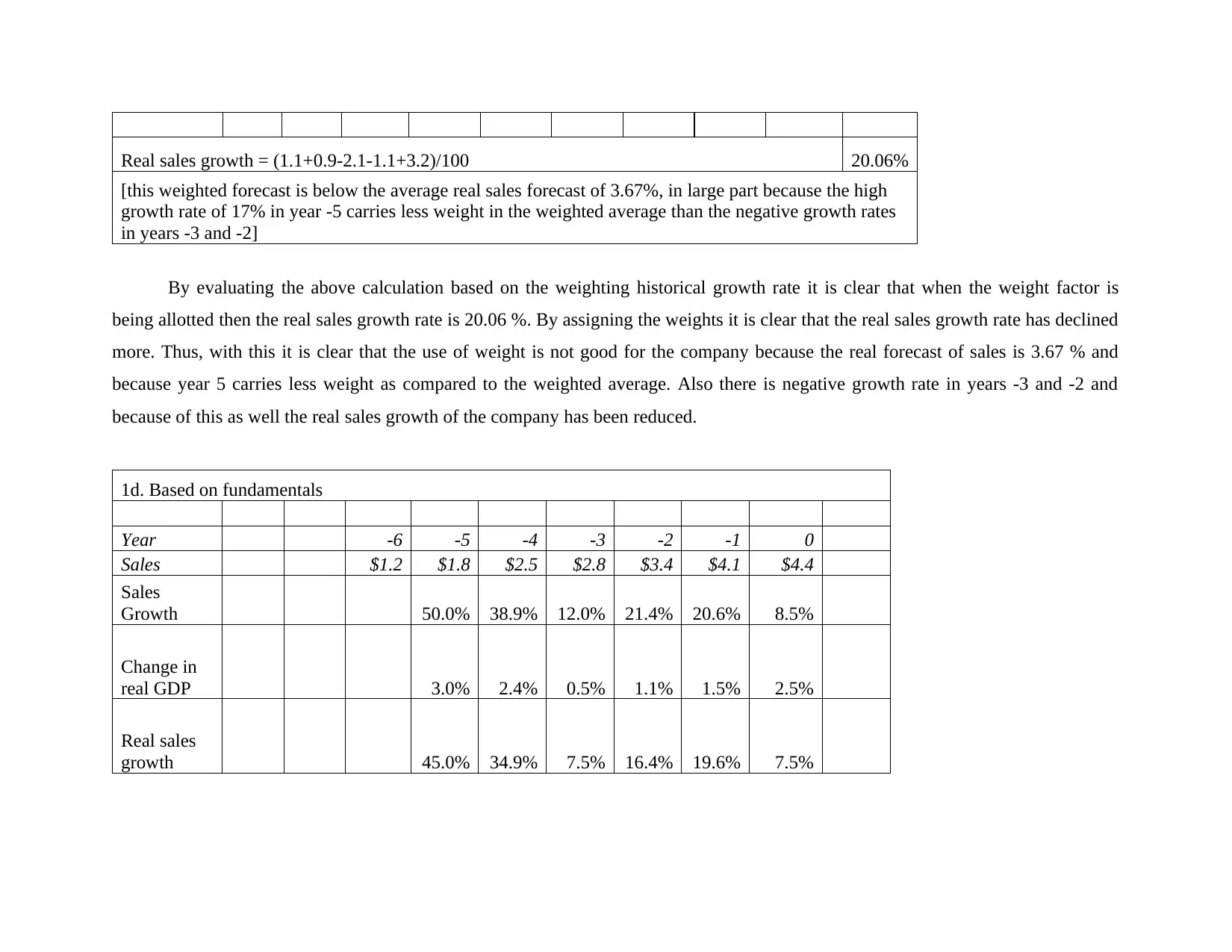

Real sales

growth/

Change in

GDP 15x 15x 15x 15x 13x

Expected

sales

growth (x5) 15.0% 12.0% 2.5% 5.5% 7.5%

Difference 30.0% 22.9% 5.0% 10.9% 12.1%

- by looking at historic ratio of real sales growth to GDP we can assume that the relationship is

approx. 5x real sales growth to GDP

Expected real GDP growth Year 0 1.50%

Forecasted real growth rate in year 0 is 1.5%*5.0 7.50%

In the present case the calculation is based on the relation being present in the real sales growth and the annual change in real

GDP. In this situation it is assumed that the forecast will include the change in real GDP of year 0 will be 2.5 % and in case of year 1

it will be average of the past four years that is 0 to -4 years. The above calculation evaluated that the forecasted real growth is 7.50 %.

This is also less in comparison to the previous calculation and not good for the company. Hence, for this the working efficiency of the

company will be affected as the growth rate is smaller.

1e

growth/

Change in

GDP 15x 15x 15x 15x 13x

Expected

sales

growth (x5) 15.0% 12.0% 2.5% 5.5% 7.5%

Difference 30.0% 22.9% 5.0% 10.9% 12.1%

- by looking at historic ratio of real sales growth to GDP we can assume that the relationship is

approx. 5x real sales growth to GDP

Expected real GDP growth Year 0 1.50%

Forecasted real growth rate in year 0 is 1.5%*5.0 7.50%

In the present case the calculation is based on the relation being present in the real sales growth and the annual change in real

GDP. In this situation it is assumed that the forecast will include the change in real GDP of year 0 will be 2.5 % and in case of year 1

it will be average of the past four years that is 0 to -4 years. The above calculation evaluated that the forecasted real growth is 7.50 %.

This is also less in comparison to the previous calculation and not good for the company. Hence, for this the working efficiency of the

company will be affected as the growth rate is smaller.

1e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

On the basis of all the above table and calculation it is clear that the approach which will be best suited for the effective working

is based on the historical nominal growth rate because it is providing the best outcome for the sales growth. This is particularly

because of the reason that this is the only approach which is providing for the maximum growth rate in the sales. Hence, it will

provide the benefit of the forecasting the working in better and this will help in providing better forecasting of sales and will improve

the operational efficiency of the business.

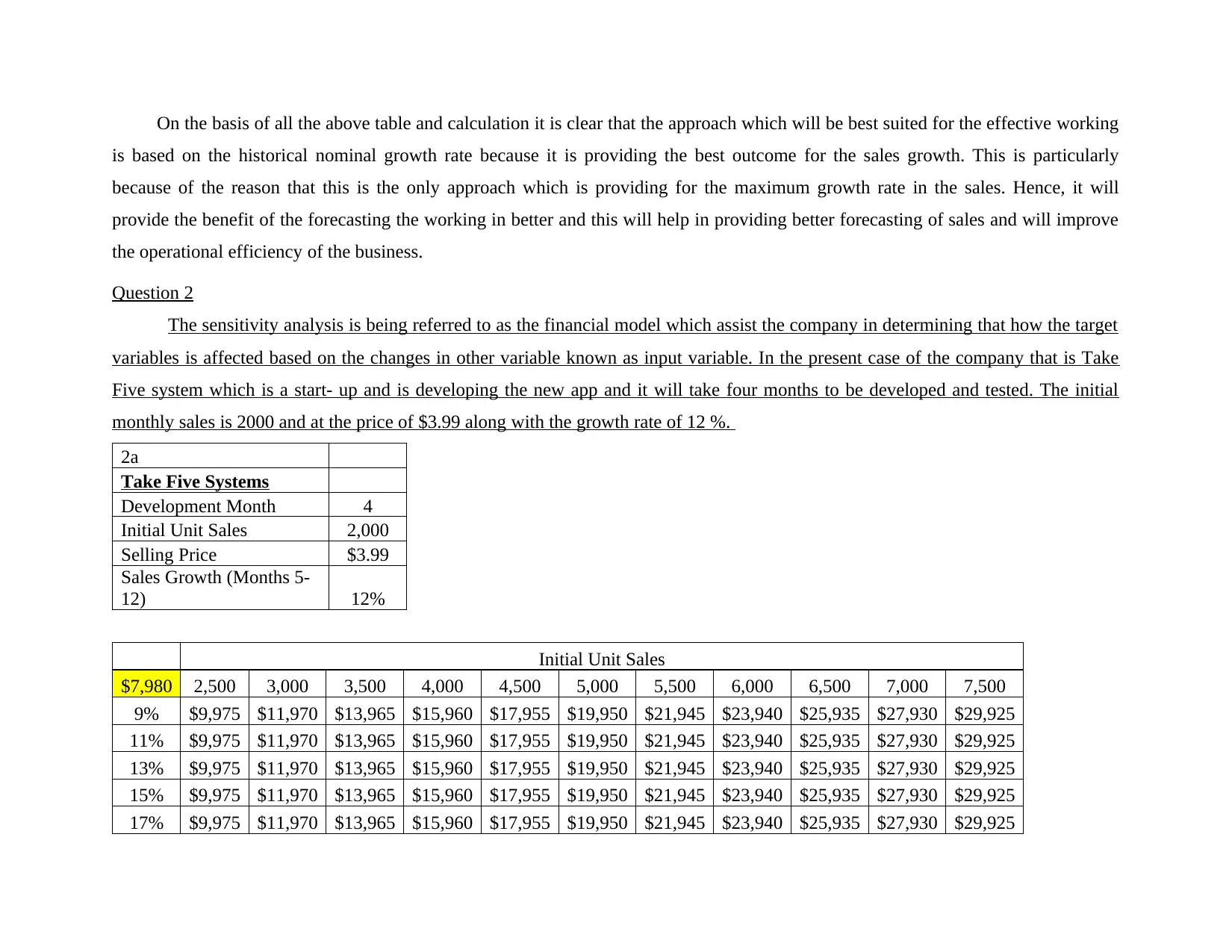

Question 2

The sensitivity analysis is being referred to as the financial model which assist the company in determining that how the target

variables is affected based on the changes in other variable known as input variable. In the present case of the company that is Take

Five system which is a start- up and is developing the new app and it will take four months to be developed and tested. The initial

monthly sales is 2000 and at the price of $3.99 along with the growth rate of 12 %.

2a

Take Five Systems

Development Month 4

Initial Unit Sales 2,000

Selling Price $3.99

Sales Growth (Months 5-

12) 12%

Initial Unit Sales

$7,980 2,500 3,000 3,500 4,000 4,500 5,000 5,500 6,000 6,500 7,000 7,500

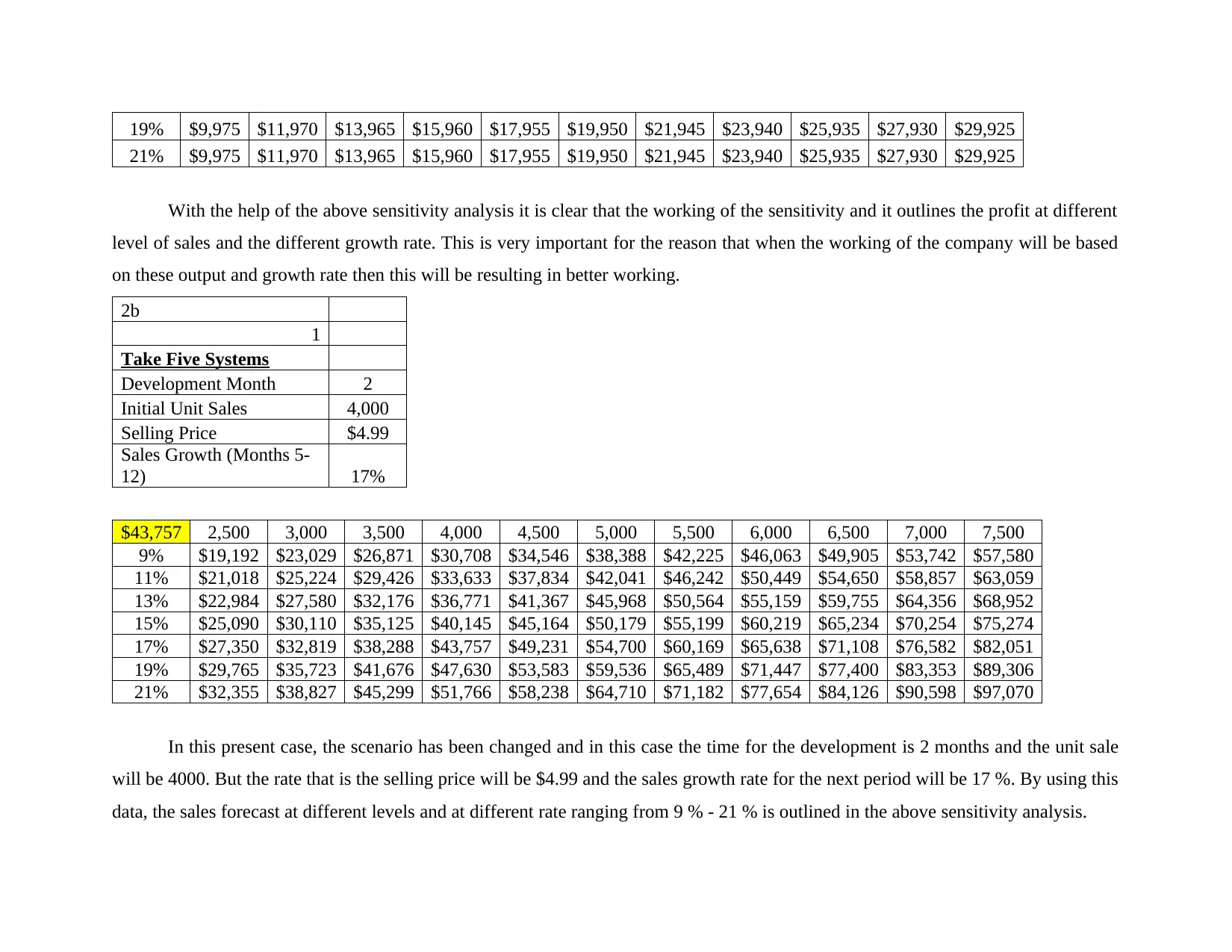

9% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

11% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

13% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

15% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

17% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

is based on the historical nominal growth rate because it is providing the best outcome for the sales growth. This is particularly

because of the reason that this is the only approach which is providing for the maximum growth rate in the sales. Hence, it will

provide the benefit of the forecasting the working in better and this will help in providing better forecasting of sales and will improve

the operational efficiency of the business.

Question 2

The sensitivity analysis is being referred to as the financial model which assist the company in determining that how the target

variables is affected based on the changes in other variable known as input variable. In the present case of the company that is Take

Five system which is a start- up and is developing the new app and it will take four months to be developed and tested. The initial

monthly sales is 2000 and at the price of $3.99 along with the growth rate of 12 %.

2a

Take Five Systems

Development Month 4

Initial Unit Sales 2,000

Selling Price $3.99

Sales Growth (Months 5-

12) 12%

Initial Unit Sales

$7,980 2,500 3,000 3,500 4,000 4,500 5,000 5,500 6,000 6,500 7,000 7,500

9% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

11% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

13% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

15% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

17% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

19% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

21% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

With the help of the above sensitivity analysis it is clear that the working of the sensitivity and it outlines the profit at different

level of sales and the different growth rate. This is very important for the reason that when the working of the company will be based

on these output and growth rate then this will be resulting in better working.

2b

1

Take Five Systems

Development Month 2

Initial Unit Sales 4,000

Selling Price $4.99

Sales Growth (Months 5-

12) 17%

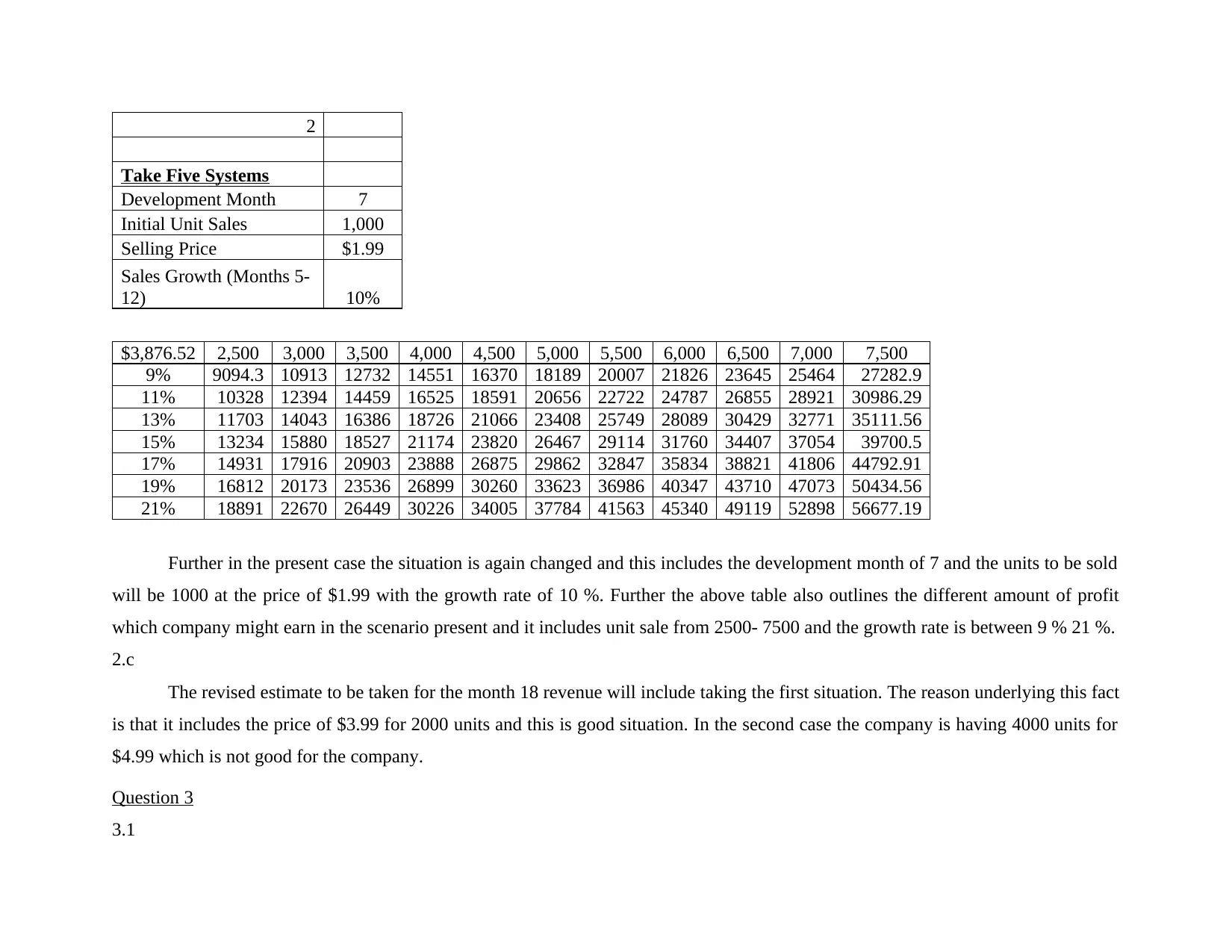

$43,757 2,500 3,000 3,500 4,000 4,500 5,000 5,500 6,000 6,500 7,000 7,500

9% $19,192 $23,029 $26,871 $30,708 $34,546 $38,388 $42,225 $46,063 $49,905 $53,742 $57,580

11% $21,018 $25,224 $29,426 $33,633 $37,834 $42,041 $46,242 $50,449 $54,650 $58,857 $63,059

13% $22,984 $27,580 $32,176 $36,771 $41,367 $45,968 $50,564 $55,159 $59,755 $64,356 $68,952

15% $25,090 $30,110 $35,125 $40,145 $45,164 $50,179 $55,199 $60,219 $65,234 $70,254 $75,274

17% $27,350 $32,819 $38,288 $43,757 $49,231 $54,700 $60,169 $65,638 $71,108 $76,582 $82,051

19% $29,765 $35,723 $41,676 $47,630 $53,583 $59,536 $65,489 $71,447 $77,400 $83,353 $89,306

21% $32,355 $38,827 $45,299 $51,766 $58,238 $64,710 $71,182 $77,654 $84,126 $90,598 $97,070

In this present case, the scenario has been changed and in this case the time for the development is 2 months and the unit sale

will be 4000. But the rate that is the selling price will be $4.99 and the sales growth rate for the next period will be 17 %. By using this

data, the sales forecast at different levels and at different rate ranging from 9 % - 21 % is outlined in the above sensitivity analysis.

21% $9,975 $11,970 $13,965 $15,960 $17,955 $19,950 $21,945 $23,940 $25,935 $27,930 $29,925

With the help of the above sensitivity analysis it is clear that the working of the sensitivity and it outlines the profit at different

level of sales and the different growth rate. This is very important for the reason that when the working of the company will be based

on these output and growth rate then this will be resulting in better working.

2b

1

Take Five Systems

Development Month 2

Initial Unit Sales 4,000

Selling Price $4.99

Sales Growth (Months 5-

12) 17%

$43,757 2,500 3,000 3,500 4,000 4,500 5,000 5,500 6,000 6,500 7,000 7,500

9% $19,192 $23,029 $26,871 $30,708 $34,546 $38,388 $42,225 $46,063 $49,905 $53,742 $57,580

11% $21,018 $25,224 $29,426 $33,633 $37,834 $42,041 $46,242 $50,449 $54,650 $58,857 $63,059

13% $22,984 $27,580 $32,176 $36,771 $41,367 $45,968 $50,564 $55,159 $59,755 $64,356 $68,952

15% $25,090 $30,110 $35,125 $40,145 $45,164 $50,179 $55,199 $60,219 $65,234 $70,254 $75,274

17% $27,350 $32,819 $38,288 $43,757 $49,231 $54,700 $60,169 $65,638 $71,108 $76,582 $82,051

19% $29,765 $35,723 $41,676 $47,630 $53,583 $59,536 $65,489 $71,447 $77,400 $83,353 $89,306

21% $32,355 $38,827 $45,299 $51,766 $58,238 $64,710 $71,182 $77,654 $84,126 $90,598 $97,070

In this present case, the scenario has been changed and in this case the time for the development is 2 months and the unit sale

will be 4000. But the rate that is the selling price will be $4.99 and the sales growth rate for the next period will be 17 %. By using this

data, the sales forecast at different levels and at different rate ranging from 9 % - 21 % is outlined in the above sensitivity analysis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2

Take Five Systems

Development Month 7

Initial Unit Sales 1,000

Selling Price $1.99

Sales Growth (Months 5-

12) 10%

$3,876.52 2,500 3,000 3,500 4,000 4,500 5,000 5,500 6,000 6,500 7,000 7,500

9% 9094.3 10913 12732 14551 16370 18189 20007 21826 23645 25464 27282.9

11% 10328 12394 14459 16525 18591 20656 22722 24787 26855 28921 30986.29

13% 11703 14043 16386 18726 21066 23408 25749 28089 30429 32771 35111.56

15% 13234 15880 18527 21174 23820 26467 29114 31760 34407 37054 39700.5

17% 14931 17916 20903 23888 26875 29862 32847 35834 38821 41806 44792.91

19% 16812 20173 23536 26899 30260 33623 36986 40347 43710 47073 50434.56

21% 18891 22670 26449 30226 34005 37784 41563 45340 49119 52898 56677.19

Further in the present case the situation is again changed and this includes the development month of 7 and the units to be sold

will be 1000 at the price of $1.99 with the growth rate of 10 %. Further the above table also outlines the different amount of profit

which company might earn in the scenario present and it includes unit sale from 2500- 7500 and the growth rate is between 9 % 21 %.

2.c

The revised estimate to be taken for the month 18 revenue will include taking the first situation. The reason underlying this fact

is that it includes the price of $3.99 for 2000 units and this is good situation. In the second case the company is having 4000 units for

$4.99 which is not good for the company.

Question 3

3.1

Take Five Systems

Development Month 7

Initial Unit Sales 1,000

Selling Price $1.99

Sales Growth (Months 5-

12) 10%

$3,876.52 2,500 3,000 3,500 4,000 4,500 5,000 5,500 6,000 6,500 7,000 7,500

9% 9094.3 10913 12732 14551 16370 18189 20007 21826 23645 25464 27282.9

11% 10328 12394 14459 16525 18591 20656 22722 24787 26855 28921 30986.29

13% 11703 14043 16386 18726 21066 23408 25749 28089 30429 32771 35111.56

15% 13234 15880 18527 21174 23820 26467 29114 31760 34407 37054 39700.5

17% 14931 17916 20903 23888 26875 29862 32847 35834 38821 41806 44792.91

19% 16812 20173 23536 26899 30260 33623 36986 40347 43710 47073 50434.56

21% 18891 22670 26449 30226 34005 37784 41563 45340 49119 52898 56677.19

Further in the present case the situation is again changed and this includes the development month of 7 and the units to be sold

will be 1000 at the price of $1.99 with the growth rate of 10 %. Further the above table also outlines the different amount of profit

which company might earn in the scenario present and it includes unit sale from 2500- 7500 and the growth rate is between 9 % 21 %.

2.c

The revised estimate to be taken for the month 18 revenue will include taking the first situation. The reason underlying this fact

is that it includes the price of $3.99 for 2000 units and this is good situation. In the second case the company is having 4000 units for

$4.99 which is not good for the company.

Question 3

3.1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

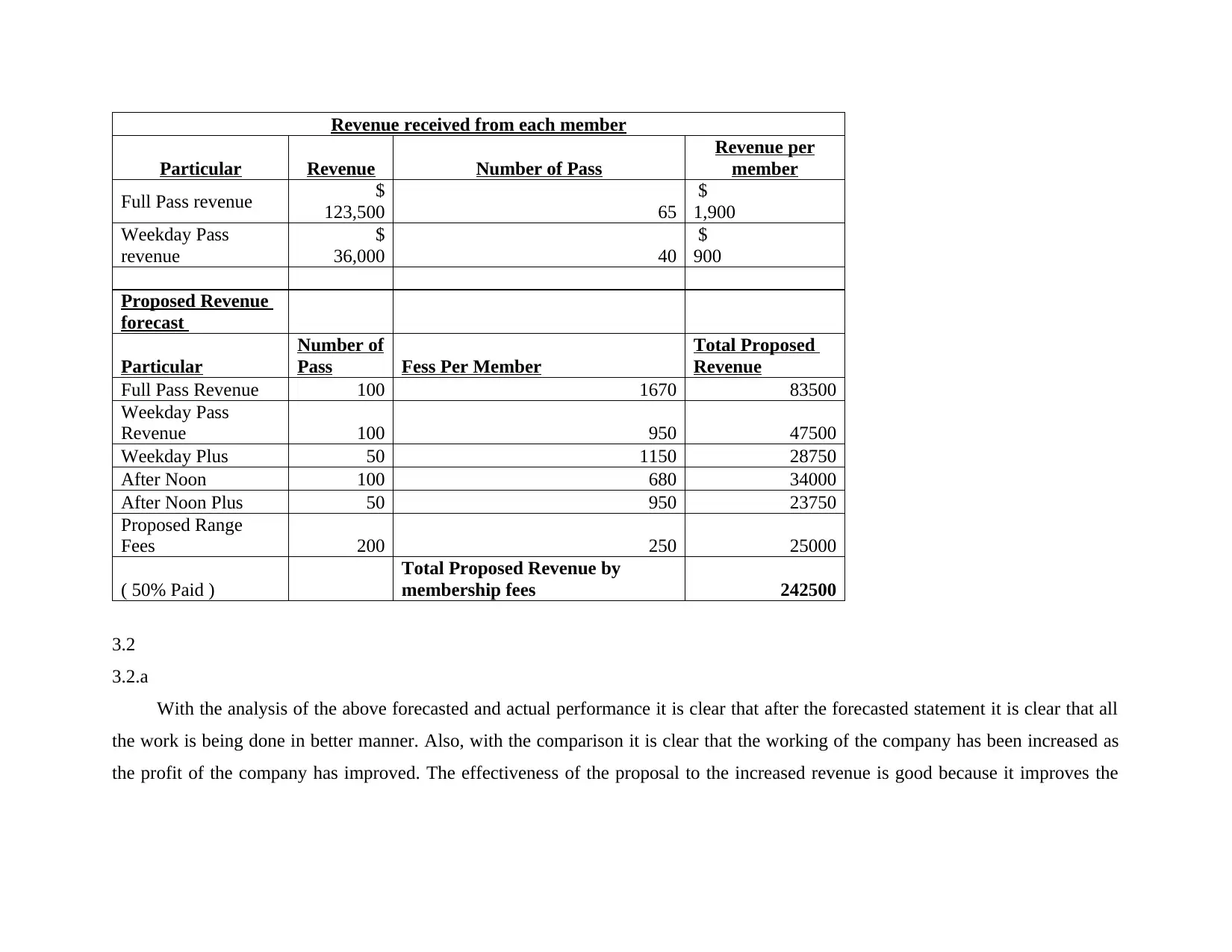

Revenue received from each member

Particular Revenue Number of Pass

Revenue per

member

Full Pass revenue $

123,500 65

$

1,900

Weekday Pass

revenue

$

36,000 40

$

900

Proposed Revenue

forecast

Particular

Number of

Pass Fess Per Member

Total Proposed

Revenue

Full Pass Revenue 100 1670 83500

Weekday Pass

Revenue 100 950 47500

Weekday Plus 50 1150 28750

After Noon 100 680 34000

After Noon Plus 50 950 23750

Proposed Range

Fees 200 250 25000

( 50% Paid )

Total Proposed Revenue by

membership fees 242500

3.2

3.2.a

With the analysis of the above forecasted and actual performance it is clear that after the forecasted statement it is clear that all

the work is being done in better manner. Also, with the comparison it is clear that the working of the company has been increased as

the profit of the company has improved. The effectiveness of the proposal to the increased revenue is good because it improves the

Particular Revenue Number of Pass

Revenue per

member

Full Pass revenue $

123,500 65

$

1,900

Weekday Pass

revenue

$

36,000 40

$

900

Proposed Revenue

forecast

Particular

Number of

Pass Fess Per Member

Total Proposed

Revenue

Full Pass Revenue 100 1670 83500

Weekday Pass

Revenue 100 950 47500

Weekday Plus 50 1150 28750

After Noon 100 680 34000

After Noon Plus 50 950 23750

Proposed Range

Fees 200 250 25000

( 50% Paid )

Total Proposed Revenue by

membership fees 242500

3.2

3.2.a

With the analysis of the above forecasted and actual performance it is clear that after the forecasted statement it is clear that all

the work is being done in better manner. Also, with the comparison it is clear that the working of the company has been increased as

the profit of the company has improved. The effectiveness of the proposal to the increased revenue is good because it improves the

working efficiency of the company. All the assumption of the company was also correct and appropriate because on the basis of this

only the new proposed revenue was calculated and as a result of this the profitability increased to a great extent.

3.2.b

Based on the above both calculation it is necessary that some of the recommendation is being provided to the company. these

recommendation involves the following-

It is recommended to the company that they must also provide membership to the Weekday plus, afternoon and afternoon plus

category as well. this is particularly because of the reason that it is not having current actual membership.

Along with this it is also recommended to company that they must provide some discount on taking the membership. The

reason underlying this fact is that when the company will be providing different discount then this will be attracting more of

the people and as a result of this sales will increase and ultimately the profits.

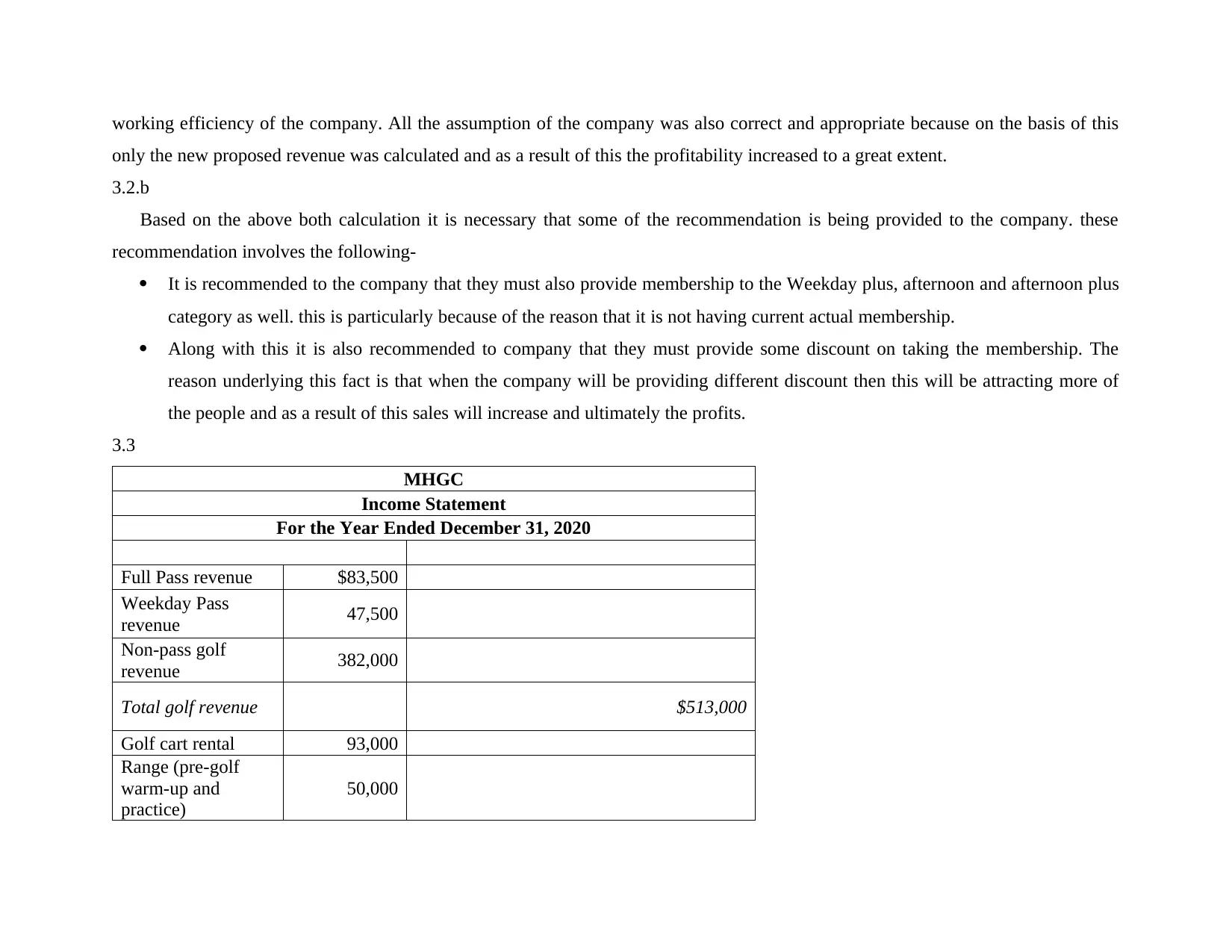

3.3

MHGC

Income Statement

For the Year Ended December 31, 2020

Full Pass revenue $83,500

Weekday Pass

revenue 47,500

Non-pass golf

revenue 382,000

Total golf revenue $513,000

Golf cart rental 93,000

Range (pre-golf

warm-up and

practice)

50,000

only the new proposed revenue was calculated and as a result of this the profitability increased to a great extent.

3.2.b

Based on the above both calculation it is necessary that some of the recommendation is being provided to the company. these

recommendation involves the following-

It is recommended to the company that they must also provide membership to the Weekday plus, afternoon and afternoon plus

category as well. this is particularly because of the reason that it is not having current actual membership.

Along with this it is also recommended to company that they must provide some discount on taking the membership. The

reason underlying this fact is that when the company will be providing different discount then this will be attracting more of

the people and as a result of this sales will increase and ultimately the profits.

3.3

MHGC

Income Statement

For the Year Ended December 31, 2020

Full Pass revenue $83,500

Weekday Pass

revenue 47,500

Non-pass golf

revenue 382,000

Total golf revenue $513,000

Golf cart rental 93,000

Range (pre-golf

warm-up and

practice)

50,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.