LSC Malta: Kellogg's Dividend Policy - An Internal Management Report

VerifiedAdded on 2023/03/23

|11

|2754

|36

Report

AI Summary

This report, prepared for Kellogg's CFO, delves into the company's dividend policy and its significance. It reviews Kellogg's dividend performance over the past five years, highlighting the increasing dividend trend despite fluctuations in net income and payout ratios. The report also outlines major dividend policy theories, including the Modigliani-Miller theory, Walter's model, and Gordon's model, discussing their assumptions and implications. Ultimately, the report aims to inform a discussion with major shareholders and recommend a future dividend policy that balances shareholder satisfaction with the company's financial health and growth prospects. This document is available on Desklib, a platform offering a wide range of study resources, including past papers and solved assignments, for students.

Running Head: CORPORATE FINANCE 1

CORPORATE FINANCE

[Name of Writer]

[Name of Institution]

CORPORATE FINANCE

[Name of Writer]

[Name of Institution]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 2

Internal Management Information Report:

Title of report: Treasury Department report about Dividend policy to shareholders under

the Order of CFO Kellogg

Introduction:

All For-Profit organizations exist for profit as primary purpose. After realizing profit, the

most difficult decision is how to utilize this profit. Profit distribution decision is not only difficult

but important as well. Decision of profit distribution is managements concern but significantly

affects investors and creditors. Organization can distribute profit as dividend or retain profit for

reinvestment (Ajanthan, 2013). Every organization have choice to choose a mixture of dividend

payment or and profit retain. Portion of profit which is distributed among shareholders called

dividend payout ratio (Gill, Biger & Tibrewala, 2010). Portion of profit retained for investment is

called retention ratio.

Discussion:

Dividend decisions are very important for shareholders because they want to earn more

return. Policy of dividend distribution depends on many factors such as nature of shareholders,

growth chances, market returns and financial status of organization (Iturriaga & Crisóstomo, 2010).

Many shareholders want to receive dividend every year as income from investment. When

majority of shareholders are of such intention then organization is likely to distribute larger

portion of income. Those organizations which are at growth stage do not distribute income as

dividend rather they reinvest for growth purpose (Abreu & Gulamhussen, 2013). If organization is

expecting some lucrative and high yielding projects, then management will decide to reinvest

whole or much portion of income. low payout ratio signals as company has many opportunities

Internal Management Information Report:

Title of report: Treasury Department report about Dividend policy to shareholders under

the Order of CFO Kellogg

Introduction:

All For-Profit organizations exist for profit as primary purpose. After realizing profit, the

most difficult decision is how to utilize this profit. Profit distribution decision is not only difficult

but important as well. Decision of profit distribution is managements concern but significantly

affects investors and creditors. Organization can distribute profit as dividend or retain profit for

reinvestment (Ajanthan, 2013). Every organization have choice to choose a mixture of dividend

payment or and profit retain. Portion of profit which is distributed among shareholders called

dividend payout ratio (Gill, Biger & Tibrewala, 2010). Portion of profit retained for investment is

called retention ratio.

Discussion:

Dividend decisions are very important for shareholders because they want to earn more

return. Policy of dividend distribution depends on many factors such as nature of shareholders,

growth chances, market returns and financial status of organization (Iturriaga & Crisóstomo, 2010).

Many shareholders want to receive dividend every year as income from investment. When

majority of shareholders are of such intention then organization is likely to distribute larger

portion of income. Those organizations which are at growth stage do not distribute income as

dividend rather they reinvest for growth purpose (Abreu & Gulamhussen, 2013). If organization is

expecting some lucrative and high yielding projects, then management will decide to reinvest

whole or much portion of income. low payout ratio signals as company has many opportunities

CORPORATE FINANCE 3

to grow (Fairchild, Guney & Thanatawee, 2014). Although it is not true that companies with high

payout ratio does not have growth prospects. Market returns is also a derivative of dividend

decision policy, suppose market pays more return than current organization then investors

require high dividend payout ratio to invest in market for greater yield. Financial soundness of

organization also affects dividend policy to greater extent (Karasek & Bryant, 2012). Financially

healthy organizations tend to pay more as dividend compared to financially distressed

organizations.

Dividend distribution is not just income distribution but it also signals investors that

organization is capable to generate enough cash for its investors. A large group of investors

believe that constant payment of dividend is a symbol of healthy organization. They believe if

organization is paying dividend so it means they are generating good cash to fulfil both

operations of business and paying investors as well (Thanatawee, 2011). Few shareholders

perceive dividends as a signal of low growth prospects in organization.

Legally organization are not bound to distribute income as dividend but it is purely a

management decision. Management’s opinion drive dividend policy because some pay a constant

dividend while few have never paid dividend in their entire life of organization. Market trend is

the only and strong element capable to regulate dividend policies (Suwanna, 2012).

Dividend Analysis:

Kellogg Co is multinational organization that deals with consumer packaged goods and

listed on NYSE under the ticker name of K. Kellogg is financially healthy and growing

organization with a very attractive dividend policy. Kellogg Co has a continuous history of

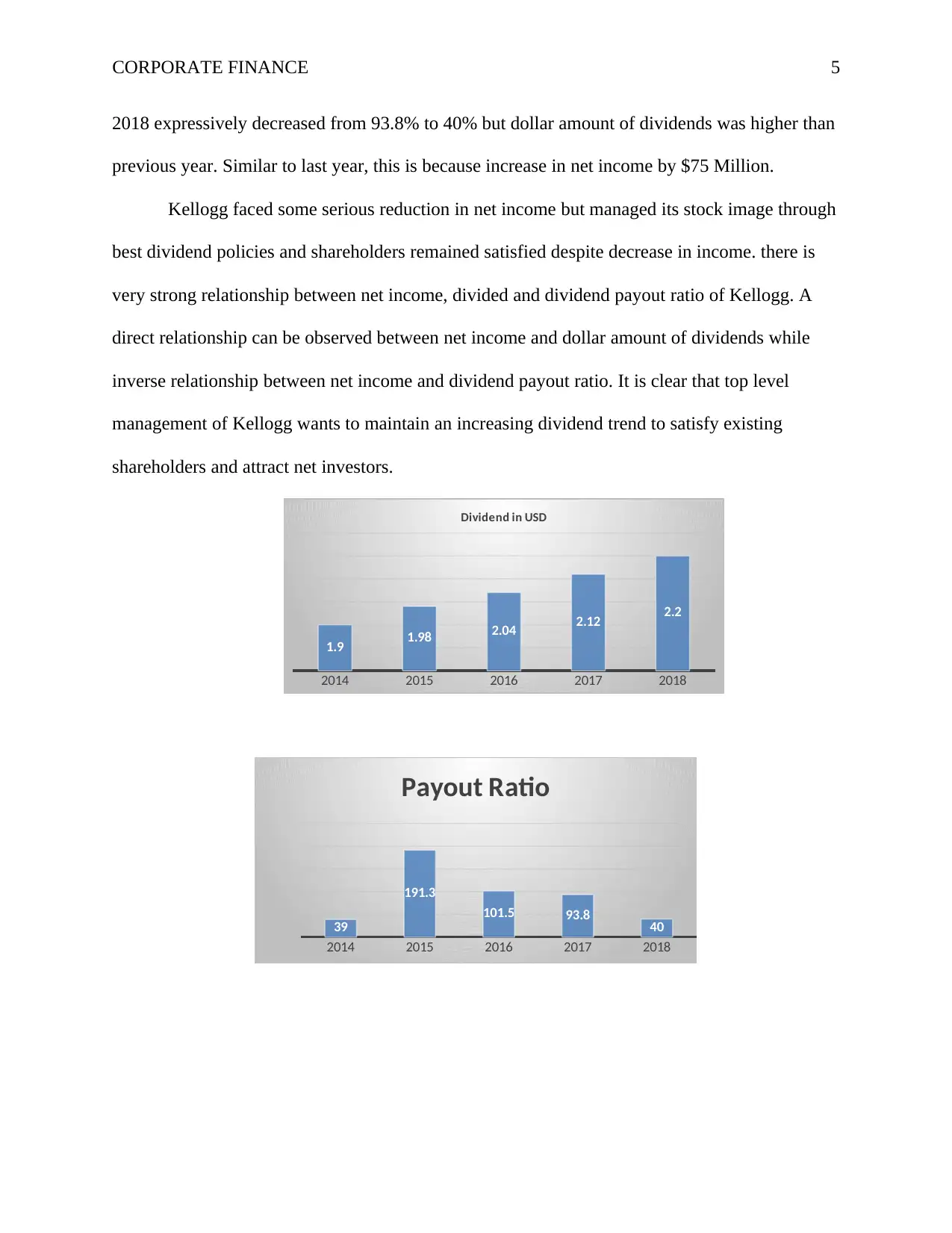

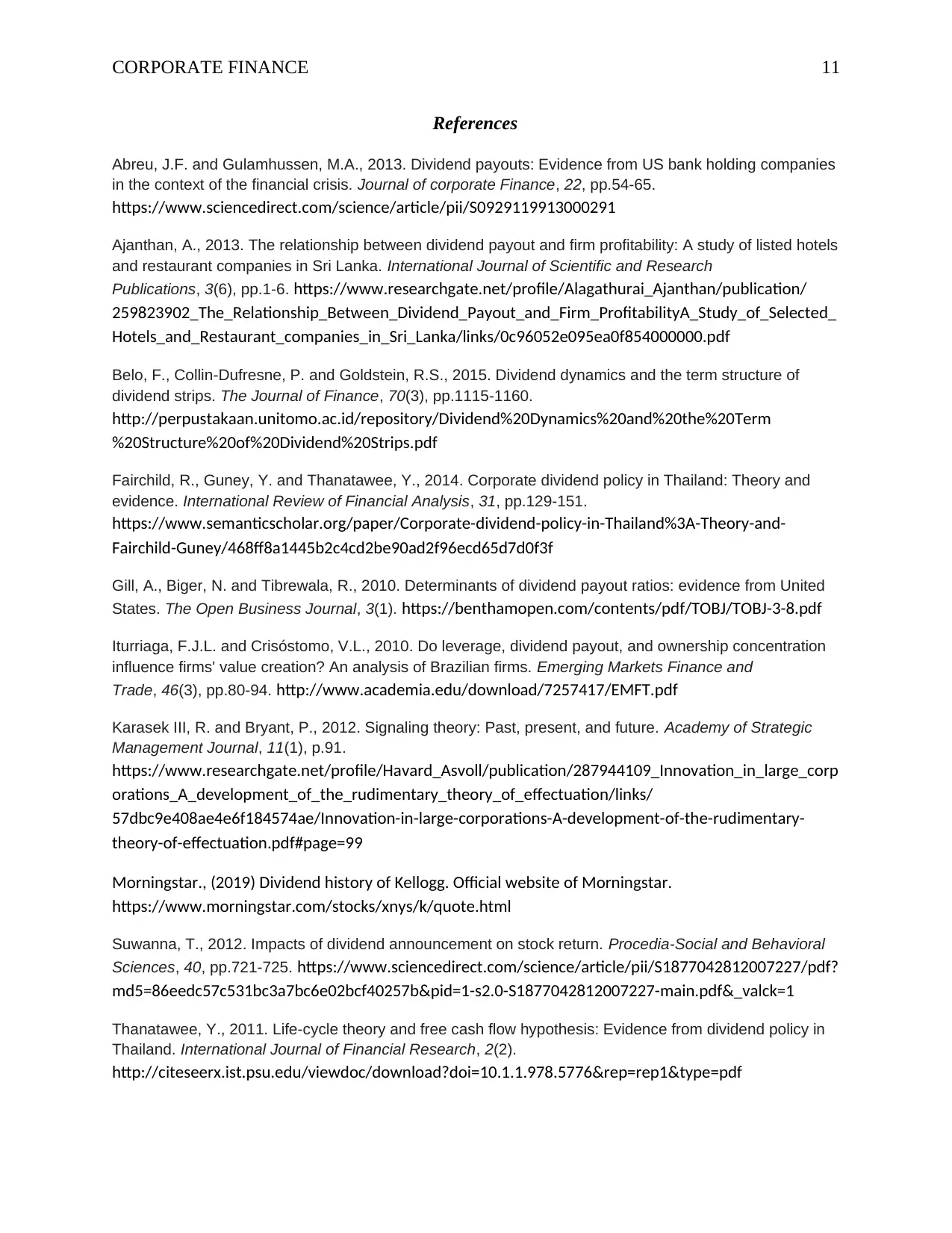

dividend payments due to good net profit. Kellogg paid dividends of $1.9, $1.98, $2.04, $2.12

and $2.20 in 2014, 2015, 2016, 2017 and 2018 respectively as shown in graph below. A careful

to grow (Fairchild, Guney & Thanatawee, 2014). Although it is not true that companies with high

payout ratio does not have growth prospects. Market returns is also a derivative of dividend

decision policy, suppose market pays more return than current organization then investors

require high dividend payout ratio to invest in market for greater yield. Financial soundness of

organization also affects dividend policy to greater extent (Karasek & Bryant, 2012). Financially

healthy organizations tend to pay more as dividend compared to financially distressed

organizations.

Dividend distribution is not just income distribution but it also signals investors that

organization is capable to generate enough cash for its investors. A large group of investors

believe that constant payment of dividend is a symbol of healthy organization. They believe if

organization is paying dividend so it means they are generating good cash to fulfil both

operations of business and paying investors as well (Thanatawee, 2011). Few shareholders

perceive dividends as a signal of low growth prospects in organization.

Legally organization are not bound to distribute income as dividend but it is purely a

management decision. Management’s opinion drive dividend policy because some pay a constant

dividend while few have never paid dividend in their entire life of organization. Market trend is

the only and strong element capable to regulate dividend policies (Suwanna, 2012).

Dividend Analysis:

Kellogg Co is multinational organization that deals with consumer packaged goods and

listed on NYSE under the ticker name of K. Kellogg is financially healthy and growing

organization with a very attractive dividend policy. Kellogg Co has a continuous history of

dividend payments due to good net profit. Kellogg paid dividends of $1.9, $1.98, $2.04, $2.12

and $2.20 in 2014, 2015, 2016, 2017 and 2018 respectively as shown in graph below. A careful

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE 4

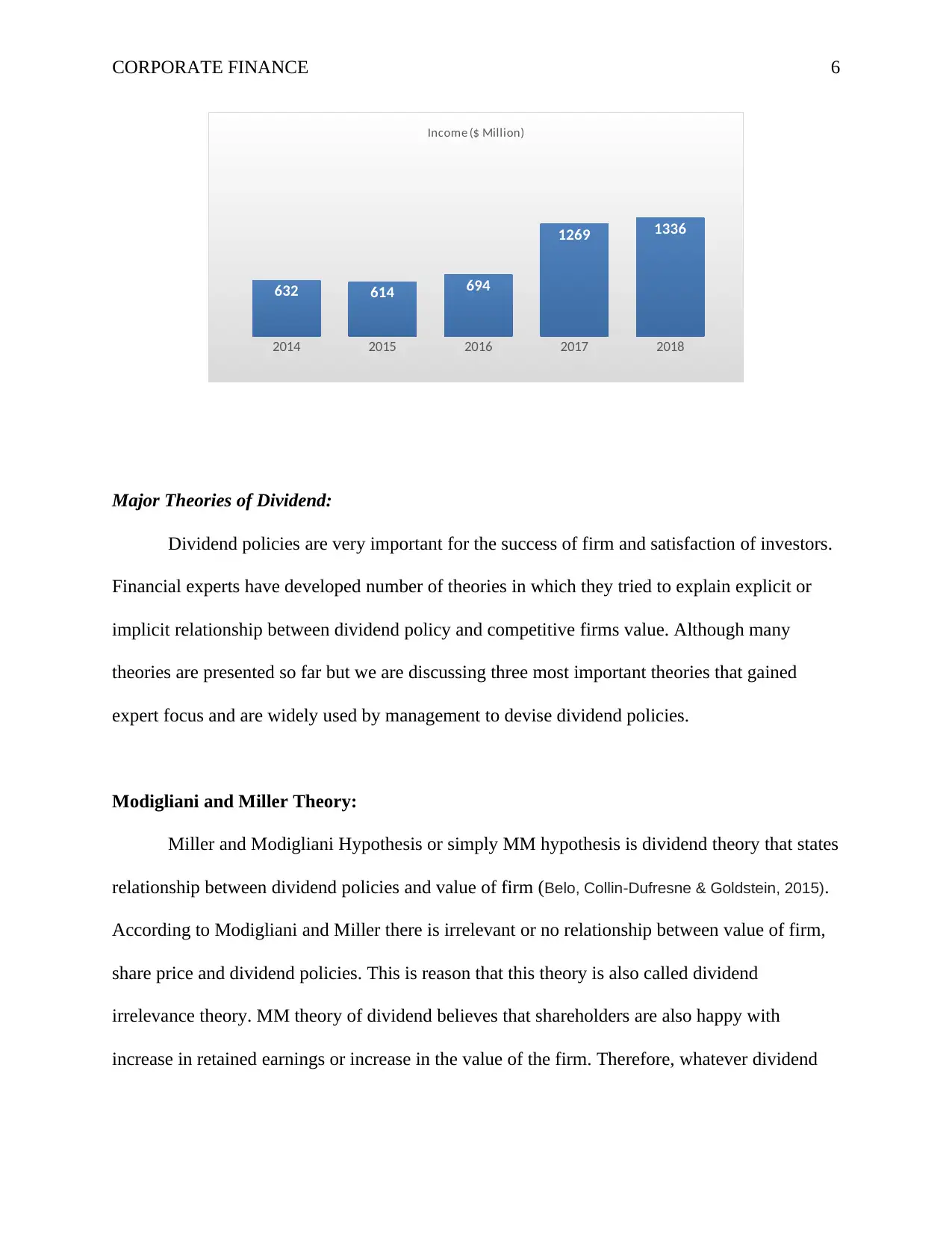

analysis of the dividend payment trend of Kellogg’s reveals that dividends are increasing

continuously. Since 2014, dividend trend is increasing because of increase in net income while in

2015 net income reduced by $18 Million but management didn’t cut dividends. Net income in

2014 was $632 and in 2015 net income reduced to $614 Million. Over last three financial years

2016, 2017 and 2018 net income of Kellogg was $694 Million, $1269 Million and $1336 Million

respectively. A very interesting point is that following the $18 Million reduction in net income,

management increased payout ratio from 39% to 191.3% in 2015. This massive increase in

payout ratio in 2015 signaled shareholders that though organization realized lower income but it

is financially stable. Due to high payout ratio or in 2015, retained earnings of Kellogg decreased

from $6689 Million to $6597 Million. To send positive signal to shareholders in 2015, Kellogg

distributed 100% net income and paid 91.3% of net income from retained earnings making total

of 191.3% payout ratio (moningstar, 2019).

Such a large payout ratio can also be tracked to low growth opportunities. Next year in

2016, Kellogg’s payout ratio was 101.5% and retained earnings reduced by 1.5%. although

payout ratio in 2016 was lower than 2015 but dollar amount of dividends in 2016 well above

from 2015. In 2016, net income increased $80 Million which is mainly due to cut in cost of

revenue. This is what called operating efficiency because Kellogg is a mature organization with

low growth opportunities therefore, management took advantage of low cost of revenue.

Revenue in 2015 was $13525 Million and cost of revenue was $8844 Million while in 2016

revenue was $13014 Million and cost of revenue reduced to $8259 Million.

In 2017, dollar amount of dividends increased significantly with lower payout ratio. This

change is due to huge increase in net income. Net income in 2016 was $994 Million while in

2017 income was $1269 Million with about $275 Million increase in income. Payout ratio in

analysis of the dividend payment trend of Kellogg’s reveals that dividends are increasing

continuously. Since 2014, dividend trend is increasing because of increase in net income while in

2015 net income reduced by $18 Million but management didn’t cut dividends. Net income in

2014 was $632 and in 2015 net income reduced to $614 Million. Over last three financial years

2016, 2017 and 2018 net income of Kellogg was $694 Million, $1269 Million and $1336 Million

respectively. A very interesting point is that following the $18 Million reduction in net income,

management increased payout ratio from 39% to 191.3% in 2015. This massive increase in

payout ratio in 2015 signaled shareholders that though organization realized lower income but it

is financially stable. Due to high payout ratio or in 2015, retained earnings of Kellogg decreased

from $6689 Million to $6597 Million. To send positive signal to shareholders in 2015, Kellogg

distributed 100% net income and paid 91.3% of net income from retained earnings making total

of 191.3% payout ratio (moningstar, 2019).

Such a large payout ratio can also be tracked to low growth opportunities. Next year in

2016, Kellogg’s payout ratio was 101.5% and retained earnings reduced by 1.5%. although

payout ratio in 2016 was lower than 2015 but dollar amount of dividends in 2016 well above

from 2015. In 2016, net income increased $80 Million which is mainly due to cut in cost of

revenue. This is what called operating efficiency because Kellogg is a mature organization with

low growth opportunities therefore, management took advantage of low cost of revenue.

Revenue in 2015 was $13525 Million and cost of revenue was $8844 Million while in 2016

revenue was $13014 Million and cost of revenue reduced to $8259 Million.

In 2017, dollar amount of dividends increased significantly with lower payout ratio. This

change is due to huge increase in net income. Net income in 2016 was $994 Million while in

2017 income was $1269 Million with about $275 Million increase in income. Payout ratio in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 5

2018 expressively decreased from 93.8% to 40% but dollar amount of dividends was higher than

previous year. Similar to last year, this is because increase in net income by $75 Million.

Kellogg faced some serious reduction in net income but managed its stock image through

best dividend policies and shareholders remained satisfied despite decrease in income. there is

very strong relationship between net income, divided and dividend payout ratio of Kellogg. A

direct relationship can be observed between net income and dollar amount of dividends while

inverse relationship between net income and dividend payout ratio. It is clear that top level

management of Kellogg wants to maintain an increasing dividend trend to satisfy existing

shareholders and attract net investors.

2014 2015 2016 2017 2018

1.9 1.98 2.04 2.12 2.2

Dividend in USD

2014 2015 2016 2017 2018

39

191.3

101.5 93.8 40

Payout Ratio

2018 expressively decreased from 93.8% to 40% but dollar amount of dividends was higher than

previous year. Similar to last year, this is because increase in net income by $75 Million.

Kellogg faced some serious reduction in net income but managed its stock image through

best dividend policies and shareholders remained satisfied despite decrease in income. there is

very strong relationship between net income, divided and dividend payout ratio of Kellogg. A

direct relationship can be observed between net income and dollar amount of dividends while

inverse relationship between net income and dividend payout ratio. It is clear that top level

management of Kellogg wants to maintain an increasing dividend trend to satisfy existing

shareholders and attract net investors.

2014 2015 2016 2017 2018

1.9 1.98 2.04 2.12 2.2

Dividend in USD

2014 2015 2016 2017 2018

39

191.3

101.5 93.8 40

Payout Ratio

CORPORATE FINANCE 6

2014 2015 2016 2017 2018

632 614 694

1269 1336

Income ($ Million)

Major Theories of Dividend:

Dividend policies are very important for the success of firm and satisfaction of investors.

Financial experts have developed number of theories in which they tried to explain explicit or

implicit relationship between dividend policy and competitive firms value. Although many

theories are presented so far but we are discussing three most important theories that gained

expert focus and are widely used by management to devise dividend policies.

Modigliani and Miller Theory:

Miller and Modigliani Hypothesis or simply MM hypothesis is dividend theory that states

relationship between dividend policies and value of firm (Belo, Collin‐Dufresne & Goldstein, 2015).

According to Modigliani and Miller there is irrelevant or no relationship between value of firm,

share price and dividend policies. This is reason that this theory is also called dividend

irrelevance theory. MM theory of dividend believes that shareholders are also happy with

increase in retained earnings or increase in the value of the firm. Therefore, whatever dividend

2014 2015 2016 2017 2018

632 614 694

1269 1336

Income ($ Million)

Major Theories of Dividend:

Dividend policies are very important for the success of firm and satisfaction of investors.

Financial experts have developed number of theories in which they tried to explain explicit or

implicit relationship between dividend policy and competitive firms value. Although many

theories are presented so far but we are discussing three most important theories that gained

expert focus and are widely used by management to devise dividend policies.

Modigliani and Miller Theory:

Miller and Modigliani Hypothesis or simply MM hypothesis is dividend theory that states

relationship between dividend policies and value of firm (Belo, Collin‐Dufresne & Goldstein, 2015).

According to Modigliani and Miller there is irrelevant or no relationship between value of firm,

share price and dividend policies. This is reason that this theory is also called dividend

irrelevance theory. MM theory of dividend believes that shareholders are also happy with

increase in retained earnings or increase in the value of the firm. Therefore, whatever dividend

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE 7

policy management use is totally irrelevant with shareholder’s satisfaction or value of the firm.

MM hypothesis assumes few assumptions under which this theory will work correctly.

a. Perfect Capital Market

Under the perfect market assumption, Modigliani and Miller states that all investors must

be rational and can access free and fair information. In other words, information must be free and

symmetric. There must be no floatation cost and no investor should be capable enough to directly

or indirectly influence the market.

b. No tax

Second assumption of MM theory is absence of tax and dividends and capital gain or

gain through increase in share price must be taxed at same rate.

c. Steady investment policy

It is fact that every investment will yield different returns and face different levels of risk

but MM theory assumes that firms should have similar investment policy.

d. Certain future profits

MM theory also states that investor must be certain about future returns and risk. There

must be no risk involved and investors should be aware of future profit and dividends. Two firms

must be similar in terms of profit, dividend and risk.

According to MM theory, investors determine firm worth not by dividend policies but

capability of assets to earn and investment polices of management. Under above assumption,

Modigliani and Miller calculated firm value under dividend and no dividend situation but result

policy management use is totally irrelevant with shareholder’s satisfaction or value of the firm.

MM hypothesis assumes few assumptions under which this theory will work correctly.

a. Perfect Capital Market

Under the perfect market assumption, Modigliani and Miller states that all investors must

be rational and can access free and fair information. In other words, information must be free and

symmetric. There must be no floatation cost and no investor should be capable enough to directly

or indirectly influence the market.

b. No tax

Second assumption of MM theory is absence of tax and dividends and capital gain or

gain through increase in share price must be taxed at same rate.

c. Steady investment policy

It is fact that every investment will yield different returns and face different levels of risk

but MM theory assumes that firms should have similar investment policy.

d. Certain future profits

MM theory also states that investor must be certain about future returns and risk. There

must be no risk involved and investors should be aware of future profit and dividends. Two firms

must be similar in terms of profit, dividend and risk.

According to MM theory, investors determine firm worth not by dividend policies but

capability of assets to earn and investment polices of management. Under above assumption,

Modigliani and Miller calculated firm value under dividend and no dividend situation but result

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 8

was same. Although MM Theory works better in above 4 assumptions but in real world, these

assumptions are only assumption. Symmetric information is an abnormal assumption because

information is distributed uneven. Taxed on dividends and capital gain cannot be same in any

situation. Investment policies of any organization cannot be same but frequently changes with

changes in required rate of return, cost of capital and other external factors. The most criticized

assumption of MM theory was certainty about return. In real world settings, two firms cannot be

identical in profit and risk.

Walters Model:

Walters model of dividend states that there is direct relationship between dividend policy

and investment policy. These two policies cannot be studied separately because of huge

interdependence. In his theory he clearly defined that firm’s internal rate of return (IRR) and

return required (k) by shareholders is strongly related (. Walter explained that dividend policy

must be formulated after studying the relationship between IRR and k. based on the relationship

of IRR and K, Walter divided firms in three categories growth firms, declining firms and normal

firms.

Firms are growing if internal rate of return or IRR is greater than K. in such firms,

management must formulate dividend policy accordingly. Management of growing firms should

reinvest whole profit or maintain zero payout ratio or 100% retention ratio.

Declining firms realize IRR less than K. organization do not have opportunities to invest to

generate attractive return. In such firms, management should distribute whole income as dividend. In

declining firms, retaining profits are no longer profitable because of low profitable investment

opportunities.

was same. Although MM Theory works better in above 4 assumptions but in real world, these

assumptions are only assumption. Symmetric information is an abnormal assumption because

information is distributed uneven. Taxed on dividends and capital gain cannot be same in any

situation. Investment policies of any organization cannot be same but frequently changes with

changes in required rate of return, cost of capital and other external factors. The most criticized

assumption of MM theory was certainty about return. In real world settings, two firms cannot be

identical in profit and risk.

Walters Model:

Walters model of dividend states that there is direct relationship between dividend policy

and investment policy. These two policies cannot be studied separately because of huge

interdependence. In his theory he clearly defined that firm’s internal rate of return (IRR) and

return required (k) by shareholders is strongly related (. Walter explained that dividend policy

must be formulated after studying the relationship between IRR and k. based on the relationship

of IRR and K, Walter divided firms in three categories growth firms, declining firms and normal

firms.

Firms are growing if internal rate of return or IRR is greater than K. in such firms,

management must formulate dividend policy accordingly. Management of growing firms should

reinvest whole profit or maintain zero payout ratio or 100% retention ratio.

Declining firms realize IRR less than K. organization do not have opportunities to invest to

generate attractive return. In such firms, management should distribute whole income as dividend. In

declining firms, retaining profits are no longer profitable because of low profitable investment

opportunities.

CORPORATE FINANCE 9

Normal firms are those whose IRR and required rate of return is equal. In such organization,

dividend policy does not affect share price or firm value. Management can devise any strategy because

it will not affect firm value. Following are assumption of Walter theory.

a. Retained earnings only source of finance

Walther model assumes that all financing of firms projects is financed by retained

earnings and no external source of finance is used.

b. IRR = K

Walther model assumes that internal rate of return and required rate of return are equal.

c. Firm has long life

Walter also assumed that firms has a long life.

Gordon Model:

Myron Gordon Model states that connection between required rate of return and capital

cost along with dividend distribution policy of the organization will determine the price of the

stock. Gordon presented three most important conditions and impact on the share price of the

organization. Gordon describes internal rate of return is greater than required rate return then

price will increase due to high retention ratio. Which means in such situation, management

should increase retention ratio. Another situation is where internal rate of return is less than rate

of return then price decrease due to low retention or high payout ratio. If internal rate return is

equal to required rate of return, then dividend policy will not affect the share price.

Similar to other dividend policy model, Gordon also assumes some assumption which are

constant IRR, constant cost of capital, perpetual earnings, no corporate taxes and constant

retention ratio. This theory will work under these assumptions.

Normal firms are those whose IRR and required rate of return is equal. In such organization,

dividend policy does not affect share price or firm value. Management can devise any strategy because

it will not affect firm value. Following are assumption of Walter theory.

a. Retained earnings only source of finance

Walther model assumes that all financing of firms projects is financed by retained

earnings and no external source of finance is used.

b. IRR = K

Walther model assumes that internal rate of return and required rate of return are equal.

c. Firm has long life

Walter also assumed that firms has a long life.

Gordon Model:

Myron Gordon Model states that connection between required rate of return and capital

cost along with dividend distribution policy of the organization will determine the price of the

stock. Gordon presented three most important conditions and impact on the share price of the

organization. Gordon describes internal rate of return is greater than required rate return then

price will increase due to high retention ratio. Which means in such situation, management

should increase retention ratio. Another situation is where internal rate of return is less than rate

of return then price decrease due to low retention or high payout ratio. If internal rate return is

equal to required rate of return, then dividend policy will not affect the share price.

Similar to other dividend policy model, Gordon also assumes some assumption which are

constant IRR, constant cost of capital, perpetual earnings, no corporate taxes and constant

retention ratio. This theory will work under these assumptions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE 10

Recommendation:

Dividend theories discussed above will only work under assumptions discussed above. In

real world however, dividend policies must be devised keeping in view factors in real market.

Kellogg’s current management depends on the view that dividend policy affect price and

investment. Current strategy of Kellogg matches with theory of Walter who states that dividend

policies is strongly affected by relationship between internal rate of return and required rate of

return. It is hence recommended that, dividend distribution affect both share price and

investment in terms of Kellogg. Instead of increasing dividend significantly, Kellogg

Corporation should main steady dividend payout ratio.

Recommendation:

Dividend theories discussed above will only work under assumptions discussed above. In

real world however, dividend policies must be devised keeping in view factors in real market.

Kellogg’s current management depends on the view that dividend policy affect price and

investment. Current strategy of Kellogg matches with theory of Walter who states that dividend

policies is strongly affected by relationship between internal rate of return and required rate of

return. It is hence recommended that, dividend distribution affect both share price and

investment in terms of Kellogg. Instead of increasing dividend significantly, Kellogg

Corporation should main steady dividend payout ratio.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE 11

References

Abreu, J.F. and Gulamhussen, M.A., 2013. Dividend payouts: Evidence from US bank holding companies

in the context of the financial crisis. Journal of corporate Finance, 22, pp.54-65.

https://www.sciencedirect.com/science/article/pii/S0929119913000291

Ajanthan, A., 2013. The relationship between dividend payout and firm profitability: A study of listed hotels

and restaurant companies in Sri Lanka. International Journal of Scientific and Research

Publications, 3(6), pp.1-6. https://www.researchgate.net/profile/Alagathurai_Ajanthan/publication/

259823902_The_Relationship_Between_Dividend_Payout_and_Firm_ProfitabilityA_Study_of_Selected_

Hotels_and_Restaurant_companies_in_Sri_Lanka/links/0c96052e095ea0f854000000.pdf

Belo, F., Collin‐Dufresne, P. and Goldstein, R.S., 2015. Dividend dynamics and the term structure of

dividend strips. The Journal of Finance, 70(3), pp.1115-1160.

http://perpustakaan.unitomo.ac.id/repository/Dividend%20Dynamics%20and%20the%20Term

%20Structure%20of%20Dividend%20Strips.pdf

Fairchild, R., Guney, Y. and Thanatawee, Y., 2014. Corporate dividend policy in Thailand: Theory and

evidence. International Review of Financial Analysis, 31, pp.129-151.

https://www.semanticscholar.org/paper/Corporate-dividend-policy-in-Thailand%3A-Theory-and-

Fairchild-Guney/468ff8a1445b2c4cd2be90ad2f96ecd65d7d0f3f

Gill, A., Biger, N. and Tibrewala, R., 2010. Determinants of dividend payout ratios: evidence from United

States. The Open Business Journal, 3(1). https://benthamopen.com/contents/pdf/TOBJ/TOBJ-3-8.pdf

Iturriaga, F.J.L. and Crisóstomo, V.L., 2010. Do leverage, dividend payout, and ownership concentration

influence firms' value creation? An analysis of Brazilian firms. Emerging Markets Finance and

Trade, 46(3), pp.80-94. http://www.academia.edu/download/7257417/EMFT.pdf

Karasek III, R. and Bryant, P., 2012. Signaling theory: Past, present, and future. Academy of Strategic

Management Journal, 11(1), p.91.

https://www.researchgate.net/profile/Havard_Asvoll/publication/287944109_Innovation_in_large_corp

orations_A_development_of_the_rudimentary_theory_of_effectuation/links/

57dbc9e408ae4e6f184574ae/Innovation-in-large-corporations-A-development-of-the-rudimentary-

theory-of-effectuation.pdf#page=99

Morningstar., (2019) Dividend history of Kellogg. Official website of Morningstar.

https://www.morningstar.com/stocks/xnys/k/quote.html

Suwanna, T., 2012. Impacts of dividend announcement on stock return. Procedia-Social and Behavioral

Sciences, 40, pp.721-725. https://www.sciencedirect.com/science/article/pii/S1877042812007227/pdf?

md5=86eedc57c531bc3a7bc6e02bcf40257b&pid=1-s2.0-S1877042812007227-main.pdf&_valck=1

Thanatawee, Y., 2011. Life-cycle theory and free cash flow hypothesis: Evidence from dividend policy in

Thailand. International Journal of Financial Research, 2(2).

http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.978.5776&rep=rep1&type=pdf

References

Abreu, J.F. and Gulamhussen, M.A., 2013. Dividend payouts: Evidence from US bank holding companies

in the context of the financial crisis. Journal of corporate Finance, 22, pp.54-65.

https://www.sciencedirect.com/science/article/pii/S0929119913000291

Ajanthan, A., 2013. The relationship between dividend payout and firm profitability: A study of listed hotels

and restaurant companies in Sri Lanka. International Journal of Scientific and Research

Publications, 3(6), pp.1-6. https://www.researchgate.net/profile/Alagathurai_Ajanthan/publication/

259823902_The_Relationship_Between_Dividend_Payout_and_Firm_ProfitabilityA_Study_of_Selected_

Hotels_and_Restaurant_companies_in_Sri_Lanka/links/0c96052e095ea0f854000000.pdf

Belo, F., Collin‐Dufresne, P. and Goldstein, R.S., 2015. Dividend dynamics and the term structure of

dividend strips. The Journal of Finance, 70(3), pp.1115-1160.

http://perpustakaan.unitomo.ac.id/repository/Dividend%20Dynamics%20and%20the%20Term

%20Structure%20of%20Dividend%20Strips.pdf

Fairchild, R., Guney, Y. and Thanatawee, Y., 2014. Corporate dividend policy in Thailand: Theory and

evidence. International Review of Financial Analysis, 31, pp.129-151.

https://www.semanticscholar.org/paper/Corporate-dividend-policy-in-Thailand%3A-Theory-and-

Fairchild-Guney/468ff8a1445b2c4cd2be90ad2f96ecd65d7d0f3f

Gill, A., Biger, N. and Tibrewala, R., 2010. Determinants of dividend payout ratios: evidence from United

States. The Open Business Journal, 3(1). https://benthamopen.com/contents/pdf/TOBJ/TOBJ-3-8.pdf

Iturriaga, F.J.L. and Crisóstomo, V.L., 2010. Do leverage, dividend payout, and ownership concentration

influence firms' value creation? An analysis of Brazilian firms. Emerging Markets Finance and

Trade, 46(3), pp.80-94. http://www.academia.edu/download/7257417/EMFT.pdf

Karasek III, R. and Bryant, P., 2012. Signaling theory: Past, present, and future. Academy of Strategic

Management Journal, 11(1), p.91.

https://www.researchgate.net/profile/Havard_Asvoll/publication/287944109_Innovation_in_large_corp

orations_A_development_of_the_rudimentary_theory_of_effectuation/links/

57dbc9e408ae4e6f184574ae/Innovation-in-large-corporations-A-development-of-the-rudimentary-

theory-of-effectuation.pdf#page=99

Morningstar., (2019) Dividend history of Kellogg. Official website of Morningstar.

https://www.morningstar.com/stocks/xnys/k/quote.html

Suwanna, T., 2012. Impacts of dividend announcement on stock return. Procedia-Social and Behavioral

Sciences, 40, pp.721-725. https://www.sciencedirect.com/science/article/pii/S1877042812007227/pdf?

md5=86eedc57c531bc3a7bc6e02bcf40257b&pid=1-s2.0-S1877042812007227-main.pdf&_valck=1

Thanatawee, Y., 2011. Life-cycle theory and free cash flow hypothesis: Evidence from dividend policy in

Thailand. International Journal of Financial Research, 2(2).

http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.978.5776&rep=rep1&type=pdf

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.