HA2032 Corporate & Financial Accounting: Reporting Standards Report

VerifiedAdded on 2023/06/04

|18

|3201

|56

Report

AI Summary

This report provides a detailed analysis of financial accounting and reporting standards, examining the need for regulatory standards versus voluntary reporting by managers. It discusses the role of the Australian Accounting Standards Board (AASB) in influencing global financial reporting standards and the reasons behind the non-mandatory adoption of International Financial Reporting Standards (IFRS) for IASB member countries. The report includes a comparative analysis of owner's equity extracted from the annual financial reports of Rio Tinto, Woolworths Limited, BHP Billiton Limited, and Commonwealth Bank, evaluating their equity positions over four years. The analysis covers aspects such as share capital, retained earnings, and overall equity trends, providing insights into the financial health and stability of these organizations. The report concludes with a summary of the key findings and implications of the analysis.

CORPORATE AND FINANCIAL ACCOUNTING

Page 1 of 18

Page 1 of 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary:

The present report encompasses various aspects of the financial accounting and reporting

standards and its need. The presented report commences with the discussion of the need for

regulatory standards for the financial reporting and the stand of voluntary reporting by the

manager. The report then lists the process by which the AASB influence the global regulation

for financial reporting standards and the reasons of non-mandate of the IFRS for the members

of the IASB. The report then presents the analysis of owner’s equity extracted from the annual

financial reports of four companies. The report concludes with comments on the entire context.

Page 2 of 18

The present report encompasses various aspects of the financial accounting and reporting

standards and its need. The presented report commences with the discussion of the need for

regulatory standards for the financial reporting and the stand of voluntary reporting by the

manager. The report then lists the process by which the AASB influence the global regulation

for financial reporting standards and the reasons of non-mandate of the IFRS for the members

of the IASB. The report then presents the analysis of owner’s equity extracted from the annual

financial reports of four companies. The report concludes with comments on the entire context.

Page 2 of 18

Table of Contents

1.0 Introduction:..............................................................................................................................4

2.0 Corporate regulation: Critical discussion on the voluntary financial disclosures.....................5

3.0 Accounting standards setting:...................................................................................................7

3.1 AASB accountability in the global accounting standard setting process:..............................7

3.2 Compulsion of IFRS for member countries of IASB:..............................................................8

4.0 Owner’s Equity:........................................................................................................................10

4.1 Comparing the equity:.........................................................................................................10

4.1.1 Rio Tinto:.......................................................................................................................10

4.1.2 Woolworths Limited:.....................................................................................................11

4.1.3 BHP Billiton Limited.......................................................................................................12

4.1.4 Commonwealth Bank....................................................................................................13

4.2 Comparative analysis of the debt and equity position:.......................................................14

5.0 Conclusion:...............................................................................................................................16

References:....................................................................................................................................17

Page 3 of 18

1.0 Introduction:..............................................................................................................................4

2.0 Corporate regulation: Critical discussion on the voluntary financial disclosures.....................5

3.0 Accounting standards setting:...................................................................................................7

3.1 AASB accountability in the global accounting standard setting process:..............................7

3.2 Compulsion of IFRS for member countries of IASB:..............................................................8

4.0 Owner’s Equity:........................................................................................................................10

4.1 Comparing the equity:.........................................................................................................10

4.1.1 Rio Tinto:.......................................................................................................................10

4.1.2 Woolworths Limited:.....................................................................................................11

4.1.3 BHP Billiton Limited.......................................................................................................12

4.1.4 Commonwealth Bank....................................................................................................13

4.2 Comparative analysis of the debt and equity position:.......................................................14

5.0 Conclusion:...............................................................................................................................16

References:....................................................................................................................................17

Page 3 of 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.0 Introduction:

The present report discusses the criticality of the mandatory and voluntary financial reporting

for an organisation. This report also discusses the step through which the Australian Accounting

Standard Board can partake in the global standard-setting process. As part of the research, the

study presents a comparative analysis on owner’s equity from the annual statements of four

different organisations.

Page 4 of 18

The present report discusses the criticality of the mandatory and voluntary financial reporting

for an organisation. This report also discusses the step through which the Australian Accounting

Standard Board can partake in the global standard-setting process. As part of the research, the

study presents a comparative analysis on owner’s equity from the annual statements of four

different organisations.

Page 4 of 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.0 Corporate regulation: Critical discussion on the voluntary financial disclosures

A financial report of a company available to internal and external groups represents the

published document of the company’s position and performance in financial terms. The reports

are classified categorically based on a standard form (Lion, 2012). This information is used by

various stakeholders like investors, analyst groups, government, shareholders, employees and

the general public. The vested interest in the financial performance of a company of the

different stakeholders varies. Each of the stakeholders would require the information in their

own perception, for the ease of understanding and analysis to extract useful insights and future

indulgence with the organisation. Provided, the stakeholders prepare the reports for

accompanying, the information would vary significantly. To interpret the financial reports in a

systematic way, synchronisation and uniformity are necessary for the presentation of the

information. Therefore, the need for regulated financial accounting and reporting arise. Sunder

(2016) also argued that limiting managerial discretion in publishing the reports improves the

quality of the information and overall report.

The owner or board of business delegates the leading functions of the enterprise to the

managers who are responsible for the performance of individual accounts. Although there are

no set standards of the voluntary disclosures by managers, these are often used by companies

in addition to the mandatory reporting to increase potential investors and reduce the cost of

investment. On the hind side, voluntary disclosure can hinder the firm’s competitive advantages

in the market or allow a capital market to conduct an apt evaluation of the company’s shares.

Both the factors can limit the performance of the company in the future. In this regards

Page 5 of 18

A financial report of a company available to internal and external groups represents the

published document of the company’s position and performance in financial terms. The reports

are classified categorically based on a standard form (Lion, 2012). This information is used by

various stakeholders like investors, analyst groups, government, shareholders, employees and

the general public. The vested interest in the financial performance of a company of the

different stakeholders varies. Each of the stakeholders would require the information in their

own perception, for the ease of understanding and analysis to extract useful insights and future

indulgence with the organisation. Provided, the stakeholders prepare the reports for

accompanying, the information would vary significantly. To interpret the financial reports in a

systematic way, synchronisation and uniformity are necessary for the presentation of the

information. Therefore, the need for regulated financial accounting and reporting arise. Sunder

(2016) also argued that limiting managerial discretion in publishing the reports improves the

quality of the information and overall report.

The owner or board of business delegates the leading functions of the enterprise to the

managers who are responsible for the performance of individual accounts. Although there are

no set standards of the voluntary disclosures by managers, these are often used by companies

in addition to the mandatory reporting to increase potential investors and reduce the cost of

investment. On the hind side, voluntary disclosure can hinder the firm’s competitive advantages

in the market or allow a capital market to conduct an apt evaluation of the company’s shares.

Both the factors can limit the performance of the company in the future. In this regards

Page 5 of 18

Cianciaruso and Sridhar (2018) stated that management may publish reports given the capital

agency cost reduction is lesser than the cost of information publication for the market.

Therefore, voluntary disclosure can be employed by a firm if that could reap some positive

benefit without impacting the performance and long-term goals.

Page 6 of 18

agency cost reduction is lesser than the cost of information publication for the market.

Therefore, voluntary disclosure can be employed by a firm if that could reap some positive

benefit without impacting the performance and long-term goals.

Page 6 of 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3.0 Accounting standards setting:

3.1 AASB accountability in the global accounting standard setting process:

The Australian Accounting Standard Board (AASB) develops and maintains the set of regulations

applicable to the financial reporting standards of the private and public sector entities in the

Australian economy. This board follows and influence the guidelines of the International

Accounting Standard Board (IASB) to set the accounting standards. As Australia has adopted the

International Financial Reporting Standards (IFRS), any issue on the program would also reflect

in the Australian Securities and Investments Commission Act 2001 (Aasb.gov.au, 2018).

Following steps take place through which AASB affect the IFRS:

Issue identification:

Members of AASB board or individual companies identify some technical issue that needs

consideration related to improve relevance or efficiency and reduce cost.

Include issue in a research agenda:

The AASB prepares a project agenda to assess the potentiality of the amendments related to

the issue.

Research and consideration:

The board then discusses the agenda with the members considering the scope, alternative

approaches and timeline to implement the changes necessary.

Stakeholder consultation:

Page 7 of 18

3.1 AASB accountability in the global accounting standard setting process:

The Australian Accounting Standard Board (AASB) develops and maintains the set of regulations

applicable to the financial reporting standards of the private and public sector entities in the

Australian economy. This board follows and influence the guidelines of the International

Accounting Standard Board (IASB) to set the accounting standards. As Australia has adopted the

International Financial Reporting Standards (IFRS), any issue on the program would also reflect

in the Australian Securities and Investments Commission Act 2001 (Aasb.gov.au, 2018).

Following steps take place through which AASB affect the IFRS:

Issue identification:

Members of AASB board or individual companies identify some technical issue that needs

consideration related to improve relevance or efficiency and reduce cost.

Include issue in a research agenda:

The AASB prepares a project agenda to assess the potentiality of the amendments related to

the issue.

Research and consideration:

The board then discusses the agenda with the members considering the scope, alternative

approaches and timeline to implement the changes necessary.

Stakeholder consultation:

Page 7 of 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Post the research on the project scope, AASB presents the related documents for public

feedback and stakeholder discussion.

Pronouncement:

The issue consideration by AASB results in the formation of a standard, framework or further

interpretation of the perspective.

Submission to IASB:

AASB then formally submits the interpretation or framework to the IASB for consideration. This

process contributes towards the setting of improved quality international accounting standards.

3.2 Compulsion of IFRS for member countries of IASB:

IFRS are standard guidelines which are free from specific regulations that are applicable to the

member countries of the IASB. Some of the reasons for the non-compulsion of the IFRS for the

member countries are:

Accounting standards may have legal obligations in some legislation. This can hinder the

actual convergence with the IFRS rules. Thus, it can require co-operation with domestic

regulators. It may require parliamentary approval too (Prabhakar, 2013).

The constituents of IASB are numerous and having varied economic statures. The board

may face difficulties in communicating clearly with the relevant member regarding the

implementation of standards. IASB encourages letters from the member constituencies

with comments and consultative feedback (Kwak and Wang, 2015).

Page 8 of 18

feedback and stakeholder discussion.

Pronouncement:

The issue consideration by AASB results in the formation of a standard, framework or further

interpretation of the perspective.

Submission to IASB:

AASB then formally submits the interpretation or framework to the IASB for consideration. This

process contributes towards the setting of improved quality international accounting standards.

3.2 Compulsion of IFRS for member countries of IASB:

IFRS are standard guidelines which are free from specific regulations that are applicable to the

member countries of the IASB. Some of the reasons for the non-compulsion of the IFRS for the

member countries are:

Accounting standards may have legal obligations in some legislation. This can hinder the

actual convergence with the IFRS rules. Thus, it can require co-operation with domestic

regulators. It may require parliamentary approval too (Prabhakar, 2013).

The constituents of IASB are numerous and having varied economic statures. The board

may face difficulties in communicating clearly with the relevant member regarding the

implementation of standards. IASB encourages letters from the member constituencies

with comments and consultative feedback (Kwak and Wang, 2015).

Page 8 of 18

The accounting standard boards of individual countries know what is well suited

according to the needs of the state. The respective standard boards use the

international guideline to align the reporting towards a global structure (Kampanje,

2013).

Page 9 of 18

according to the needs of the state. The respective standard boards use the

international guideline to align the reporting towards a global structure (Kampanje,

2013).

Page 9 of 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

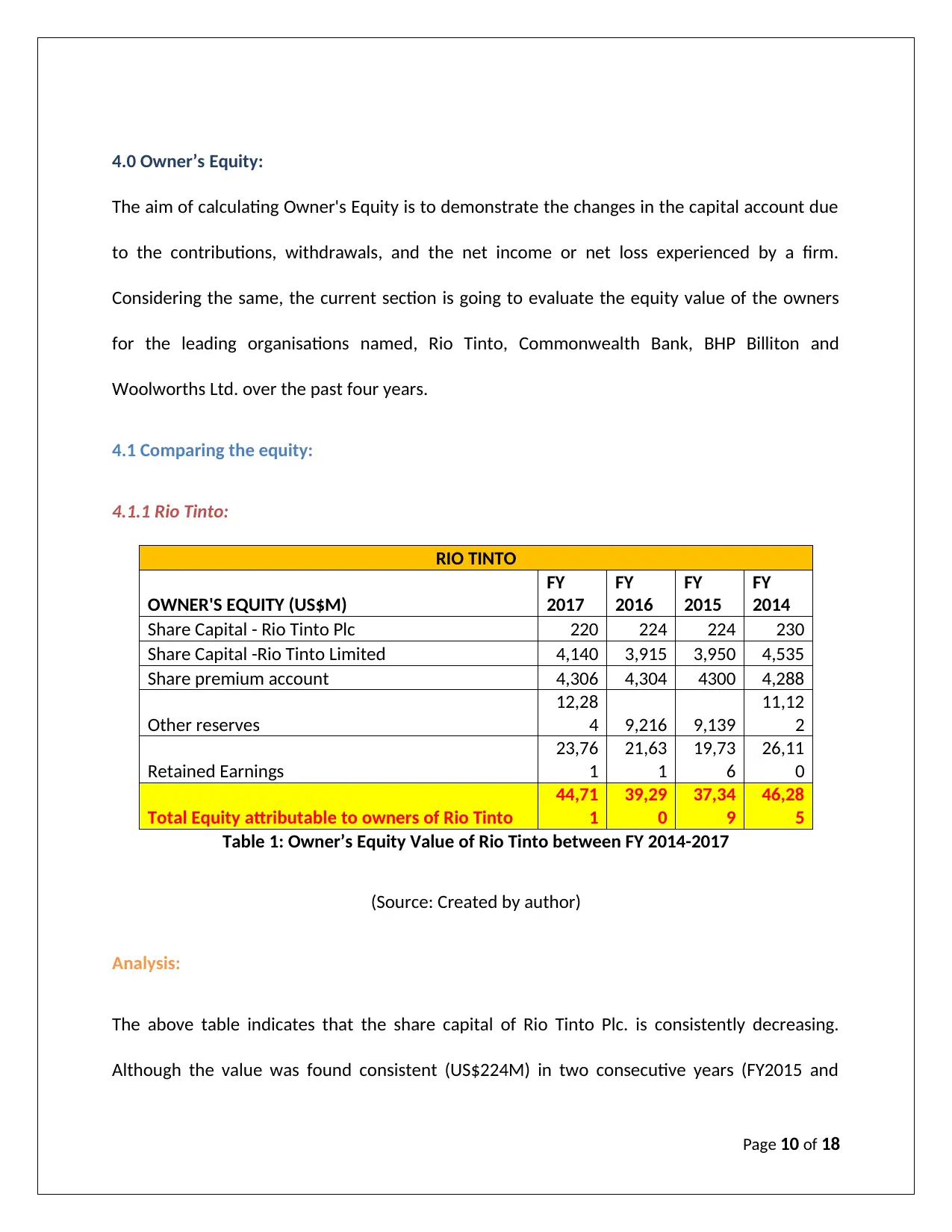

4.0 Owner’s Equity:

The aim of calculating Owner's Equity is to demonstrate the changes in the capital account due

to the contributions, withdrawals, and the net income or net loss experienced by a firm.

Considering the same, the current section is going to evaluate the equity value of the owners

for the leading organisations named, Rio Tinto, Commonwealth Bank, BHP Billiton and

Woolworths Ltd. over the past four years.

4.1 Comparing the equity:

4.1.1 Rio Tinto:

RIO TINTO

OWNER'S EQUITY (US$M)

FY

2017

FY

2016

FY

2015

FY

2014

Share Capital - Rio Tinto Plc 220 224 224 230

Share Capital -Rio Tinto Limited 4,140 3,915 3,950 4,535

Share premium account 4,306 4,304 4300 4,288

Other reserves

12,28

4 9,216 9,139

11,12

2

Retained Earnings

23,76

1

21,63

1

19,73

6

26,11

0

Total Equity attributable to owners of Rio Tinto

44,71

1

39,29

0

37,34

9

46,28

5

Table 1: Owner’s Equity Value of Rio Tinto between FY 2014-2017

(Source: Created by author)

Analysis:

The above table indicates that the share capital of Rio Tinto Plc. is consistently decreasing.

Although the value was found consistent (US$224M) in two consecutive years (FY2015 and

Page 10 of 18

The aim of calculating Owner's Equity is to demonstrate the changes in the capital account due

to the contributions, withdrawals, and the net income or net loss experienced by a firm.

Considering the same, the current section is going to evaluate the equity value of the owners

for the leading organisations named, Rio Tinto, Commonwealth Bank, BHP Billiton and

Woolworths Ltd. over the past four years.

4.1 Comparing the equity:

4.1.1 Rio Tinto:

RIO TINTO

OWNER'S EQUITY (US$M)

FY

2017

FY

2016

FY

2015

FY

2014

Share Capital - Rio Tinto Plc 220 224 224 230

Share Capital -Rio Tinto Limited 4,140 3,915 3,950 4,535

Share premium account 4,306 4,304 4300 4,288

Other reserves

12,28

4 9,216 9,139

11,12

2

Retained Earnings

23,76

1

21,63

1

19,73

6

26,11

0

Total Equity attributable to owners of Rio Tinto

44,71

1

39,29

0

37,34

9

46,28

5

Table 1: Owner’s Equity Value of Rio Tinto between FY 2014-2017

(Source: Created by author)

Analysis:

The above table indicates that the share capital of Rio Tinto Plc. is consistently decreasing.

Although the value was found consistent (US$224M) in two consecutive years (FY2015 and

Page 10 of 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2016), it was reduced in the FY 2017 (US$220M). Similarly, the share capital of Rio Tinto

Limited, as the value decreased up to US$3,915M in FY 2016, compared to the FY2014, which

was US$4,535M. However, the annual report of FY2017 indicates an improvement and growth

in the share capital of Rio Tinto Limited (US$4,140M). Hence, it can be stated that the company

has issued shares in the market to acquire fund for the business. Thus, the overall business

condition is good.

However, the share premium account shows a consistent improvement since FY2014 (4,306 in

FY2017) and the overall capital utilization towards the business is positive. In addition,

comparing the retained earning value from FY2014 to FY2017, it can be inferred that with

fluctuations, the company is proceeding towards the sustainability (Riotinto.com, 2018). Finally,

contrasting the annual reports of consecutive 4 financial years, it is clear that Rio Tinto’s net

worth of the business is increasing.

4.1.2 Woolworths Limited:

Woolworths Limited

OWNER'S EQUITY (US$M)

FY

2017

FY

2016

FY

2015

FY

2014

Shareholders’ equity 9,526 8,471 10,834 10,253

Total Equity attributable to owners of Woolworths Limited 9,876 8,782

11,13

2

10,52

5

Table 2: Owner’s Equity Value of Woolworths Limited between FY2014-2017

(Source: Created by author)

Analysis:

Page 11 of 18

Limited, as the value decreased up to US$3,915M in FY 2016, compared to the FY2014, which

was US$4,535M. However, the annual report of FY2017 indicates an improvement and growth

in the share capital of Rio Tinto Limited (US$4,140M). Hence, it can be stated that the company

has issued shares in the market to acquire fund for the business. Thus, the overall business

condition is good.

However, the share premium account shows a consistent improvement since FY2014 (4,306 in

FY2017) and the overall capital utilization towards the business is positive. In addition,

comparing the retained earning value from FY2014 to FY2017, it can be inferred that with

fluctuations, the company is proceeding towards the sustainability (Riotinto.com, 2018). Finally,

contrasting the annual reports of consecutive 4 financial years, it is clear that Rio Tinto’s net

worth of the business is increasing.

4.1.2 Woolworths Limited:

Woolworths Limited

OWNER'S EQUITY (US$M)

FY

2017

FY

2016

FY

2015

FY

2014

Shareholders’ equity 9,526 8,471 10,834 10,253

Total Equity attributable to owners of Woolworths Limited 9,876 8,782

11,13

2

10,52

5

Table 2: Owner’s Equity Value of Woolworths Limited between FY2014-2017

(Source: Created by author)

Analysis:

Page 11 of 18

It may be noted that the break-up of equity for the firm has not been available from the annual

report of the company. The above finding indicates that FY2015 was remarkably good for the

company, as the shareholder’s equity value was increased up to US$10,834M, which was

US$10,253M in the FY 2014. However, in the FY2016 shareholder’s equity dropped into

US$8,471M and it indicates that the net worth value of the business has decreased. Thus, the

selling value is found comparatively lesser than the previous financial year. It also indicates that

the investors might not be willing to invest for the further business expansion. The decrease in

shareholder’s equity also states that the company is not acquiring its true market potential. The

lack of growth potential also indicates that the company has bought back the shares to

reconstruct or restructure the capital of the business, which is a threat for the business in

meeting the stability.

However, from annual report of FY2017, it is evident that the company has increased

shareholder’s equity by more than 10% compared to the previous year. It shows a good sign of

moving towards stability with fluctuations (Woolworthsgroup.com.au, 2018). Hence, it can be

considered that the company has issued shares in the market. Thus, considering the growth

pattern in owner’s equity, the investors might be interested to invest in Woolworths. After

comparing and contrasting the owner’s equity report for four consecutive years, it can be

inferred that overall business is intending towards growth and the approach can provide

stability in the future.

4.1.3 BHP Billiton Limited

BHP BILLITON

OWNER'S EQUITY (US$M) FY FY FY FY

Page 12 of 18

report of the company. The above finding indicates that FY2015 was remarkably good for the

company, as the shareholder’s equity value was increased up to US$10,834M, which was

US$10,253M in the FY 2014. However, in the FY2016 shareholder’s equity dropped into

US$8,471M and it indicates that the net worth value of the business has decreased. Thus, the

selling value is found comparatively lesser than the previous financial year. It also indicates that

the investors might not be willing to invest for the further business expansion. The decrease in

shareholder’s equity also states that the company is not acquiring its true market potential. The

lack of growth potential also indicates that the company has bought back the shares to

reconstruct or restructure the capital of the business, which is a threat for the business in

meeting the stability.

However, from annual report of FY2017, it is evident that the company has increased

shareholder’s equity by more than 10% compared to the previous year. It shows a good sign of

moving towards stability with fluctuations (Woolworthsgroup.com.au, 2018). Hence, it can be

considered that the company has issued shares in the market. Thus, considering the growth

pattern in owner’s equity, the investors might be interested to invest in Woolworths. After

comparing and contrasting the owner’s equity report for four consecutive years, it can be

inferred that overall business is intending towards growth and the approach can provide

stability in the future.

4.1.3 BHP Billiton Limited

BHP BILLITON

OWNER'S EQUITY (US$M) FY FY FY FY

Page 12 of 18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.