Corporate and Financial Accounting Analysis: HA2032 Report

VerifiedAdded on 2023/06/08

|14

|3562

|318

Report

AI Summary

This report provides an in-depth analysis of corporate and financial accounting, addressing the necessity of regulation in financial reporting and the role of the Australian Accounting Standards Board (AASB) within the International Financial Reporting Standards (IFRS) framework. It investigates the arguments for and against voluntary disclosure of financial information by managers, emphasizing the importance of regulation in preventing market failures and ensuring a level playing field. The report also examines the specific contributions of AASB, including its adoption of IFRS standards, additional guidelines, and technical issue handling, while considering the implications for both for-profit and not-for-profit organizations. Furthermore, it includes a debt-to-equity analysis of Woolworths Limited, Wesfarmers Ltd, Myer Holdings Ltd, and JB Hi Fi Ltd, evaluating their financial positions and performance based on equity components. The report concludes by summarizing the key findings and their implications for corporate financial strategy and economic outlook.

Corporate and Financial Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summery

In present competitive environment, accounting information plays important role for business

performance and economic outlooks. In present world, businesses are mostly dependent on

the financial information and build their strategic as per available information. The report

focused on the effectiveness of the AASB in the IFRS process, debt to equity analysis of

Woolworths limited, Wesfarmers Ltd, Myer Holdings Ltd and JB Hi Fi Ltd. The discussion

shows that regulation helps the business in preventing the potential failure of the market.

AASB provides additional guidelines or the supporting commentary which are not there in

the IASB. All of these help in the following AASB standard without contradicting the IFRS

standards. The position of debt and equity for the business shows that Wesfarmers Ltd

always remained on the less risky side of the industry by sacrificing growth opportunity to

some extent. JB Hi Fi Ltd’s unpredictable data could be a cause of concern for the wrong

strategy of the business.

2

In present competitive environment, accounting information plays important role for business

performance and economic outlooks. In present world, businesses are mostly dependent on

the financial information and build their strategic as per available information. The report

focused on the effectiveness of the AASB in the IFRS process, debt to equity analysis of

Woolworths limited, Wesfarmers Ltd, Myer Holdings Ltd and JB Hi Fi Ltd. The discussion

shows that regulation helps the business in preventing the potential failure of the market.

AASB provides additional guidelines or the supporting commentary which are not there in

the IASB. All of these help in the following AASB standard without contradicting the IFRS

standards. The position of debt and equity for the business shows that Wesfarmers Ltd

always remained on the less risky side of the industry by sacrificing growth opportunity to

some extent. JB Hi Fi Ltd’s unpredictable data could be a cause of concern for the wrong

strategy of the business.

2

Table of Contents

Executive summery....................................................................................................................2

Introduction................................................................................................................................4

Corporate regulation...................................................................................................................4

The necessity of regulation in the financial reporting and accounting..................................4

Accounting standard setting.......................................................................................................5

The IFRS and the AASB’s taking part in this process of global accounting.........................5

Owner’s equity...........................................................................................................................8

Item of equity and the changing pattern of it.........................................................................8

Position of debt to equity analysis.........................................................................................9

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

3

Executive summery....................................................................................................................2

Introduction................................................................................................................................4

Corporate regulation...................................................................................................................4

The necessity of regulation in the financial reporting and accounting..................................4

Accounting standard setting.......................................................................................................5

The IFRS and the AASB’s taking part in this process of global accounting.........................5

Owner’s equity...........................................................................................................................8

Item of equity and the changing pattern of it.........................................................................8

Position of debt to equity analysis.........................................................................................9

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The accounting or the financial information has become highly important for the international

economic outlook. In the current world economic environment the businesses are relying

more and more on the financial system that is based on the capital market. Therefore the

timely, accurate and proper standard based financial information disclosure has become

highly important for the businesses. Considering this the current report would investigate the

requirement of regulation for the financial accounting and reporting process, the role of

AASB in the IFRS processes, the debt and equity position analysis of four listed public

company. This approach would provide a theoretical and practical overview of the corporate

and financial accounting process.

Corporate regulation

The necessity of regulation in the financial reporting and accounting

The necessity of regulation in the financial accounting and the reporting process has many

justifications but the free market approach state other way. As per this free market approach

the financial information is treated as like the economic assets. This information therefore

would have a natural demand and the supply side would be met by the companies. This

would lead to a natural process of exchange. Therefore this approach would produce the

appropriate amount of information for the different stakeholders and the irrelevant

information as per the demand supply point of view would not be produced (Botzem,

2012). Under this approach of accounting any financial information disclosure the manager

would have the voluntary right to disclose the information. As per this approach the manager

would have the motivation to disclose proper information to keep the company’s resource

base intact. The theoretical model of Agency theory would be useful for the better

understanding development

Agency theory- This theory state that different party based contractual relationship intersects

in the company’s activity. On the other hand stakeholders have their personal interest. The

economic perspective of the agency theory gives rise to the concept of agency and principle

(Ballwieser et al., 2012). The principles are the owner and they select the administrator or the

agent to manage the business on behalf of them. But at the time of operation different

psychological and economic goal are followed by the manager and that may in turn be in

4

The accounting or the financial information has become highly important for the international

economic outlook. In the current world economic environment the businesses are relying

more and more on the financial system that is based on the capital market. Therefore the

timely, accurate and proper standard based financial information disclosure has become

highly important for the businesses. Considering this the current report would investigate the

requirement of regulation for the financial accounting and reporting process, the role of

AASB in the IFRS processes, the debt and equity position analysis of four listed public

company. This approach would provide a theoretical and practical overview of the corporate

and financial accounting process.

Corporate regulation

The necessity of regulation in the financial reporting and accounting

The necessity of regulation in the financial accounting and the reporting process has many

justifications but the free market approach state other way. As per this free market approach

the financial information is treated as like the economic assets. This information therefore

would have a natural demand and the supply side would be met by the companies. This

would lead to a natural process of exchange. Therefore this approach would produce the

appropriate amount of information for the different stakeholders and the irrelevant

information as per the demand supply point of view would not be produced (Botzem,

2012). Under this approach of accounting any financial information disclosure the manager

would have the voluntary right to disclose the information. As per this approach the manager

would have the motivation to disclose proper information to keep the company’s resource

base intact. The theoretical model of Agency theory would be useful for the better

understanding development

Agency theory- This theory state that different party based contractual relationship intersects

in the company’s activity. On the other hand stakeholders have their personal interest. The

economic perspective of the agency theory gives rise to the concept of agency and principle

(Ballwieser et al., 2012). The principles are the owner and they select the administrator or the

agent to manage the business on behalf of them. But at the time of operation different

psychological and economic goal are followed by the manager and that may in turn be in

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

conflict with the profit maximisation goals of the owner. This conflict is reduced by aligning

the goals or their monitoring approach. The monitoring process increases cost for the owners

which in turn would reduce the remuneration for the manger. Therefore as per this theory the

manager would try to provide the reliable information to improve their evaluation and hence

the remuneration. This would reduce the monitoring cost and improve reliability of

accounting and financial information. This context can be taken to the wider market context

and there the quality work of the manager would important for the potential market investors

(Sorrentino, Cossu, , and Smarra, 2015). Under the limited resource base the manager would

be motivated to disclose the financial and accounting information properly to operate

successfully in the market.

Accepting all of the above logic, still it can is possible that all the information are not

disclosed properly by the manager. Under this circumstances that have the chance of privet

information trade (Sorrentino, Cossu, , and Smarra, 2015). Therefore the counter argument

of the voluntary disclosure by the manager would be as follows.

The regulation would help in preventing the potential failure of the market.

The regulation would be the level playing field guarantee and facilitating instrument

for the social choice.

Here the argument is that certain data of accounting process is not the ordinary type of

economic asset and therefore the efficient allocation, balances supply approach of the free

market would fail and lead to market failure. The feature of the accounting and financial

information are not similar to that of the ordinary market good. Therefore the justification of

the ‘underproduction’ in this context is not there and the regulatory approach can only

influence the companies to produce some minimum information for different stakeholders

(Botzem, 2012). The drawback and the potential failure of the free market approach based

voluntary manager’s accounting information disclosure can be overcomes through the well

developed regulatory approach of information disclosure but in this context increasing cost of

this process would have to be borne by the company.

5

the goals or their monitoring approach. The monitoring process increases cost for the owners

which in turn would reduce the remuneration for the manger. Therefore as per this theory the

manager would try to provide the reliable information to improve their evaluation and hence

the remuneration. This would reduce the monitoring cost and improve reliability of

accounting and financial information. This context can be taken to the wider market context

and there the quality work of the manager would important for the potential market investors

(Sorrentino, Cossu, , and Smarra, 2015). Under the limited resource base the manager would

be motivated to disclose the financial and accounting information properly to operate

successfully in the market.

Accepting all of the above logic, still it can is possible that all the information are not

disclosed properly by the manager. Under this circumstances that have the chance of privet

information trade (Sorrentino, Cossu, , and Smarra, 2015). Therefore the counter argument

of the voluntary disclosure by the manager would be as follows.

The regulation would help in preventing the potential failure of the market.

The regulation would be the level playing field guarantee and facilitating instrument

for the social choice.

Here the argument is that certain data of accounting process is not the ordinary type of

economic asset and therefore the efficient allocation, balances supply approach of the free

market would fail and lead to market failure. The feature of the accounting and financial

information are not similar to that of the ordinary market good. Therefore the justification of

the ‘underproduction’ in this context is not there and the regulatory approach can only

influence the companies to produce some minimum information for different stakeholders

(Botzem, 2012). The drawback and the potential failure of the free market approach based

voluntary manager’s accounting information disclosure can be overcomes through the well

developed regulatory approach of information disclosure but in this context increasing cost of

this process would have to be borne by the company.

5

Accounting standard setting

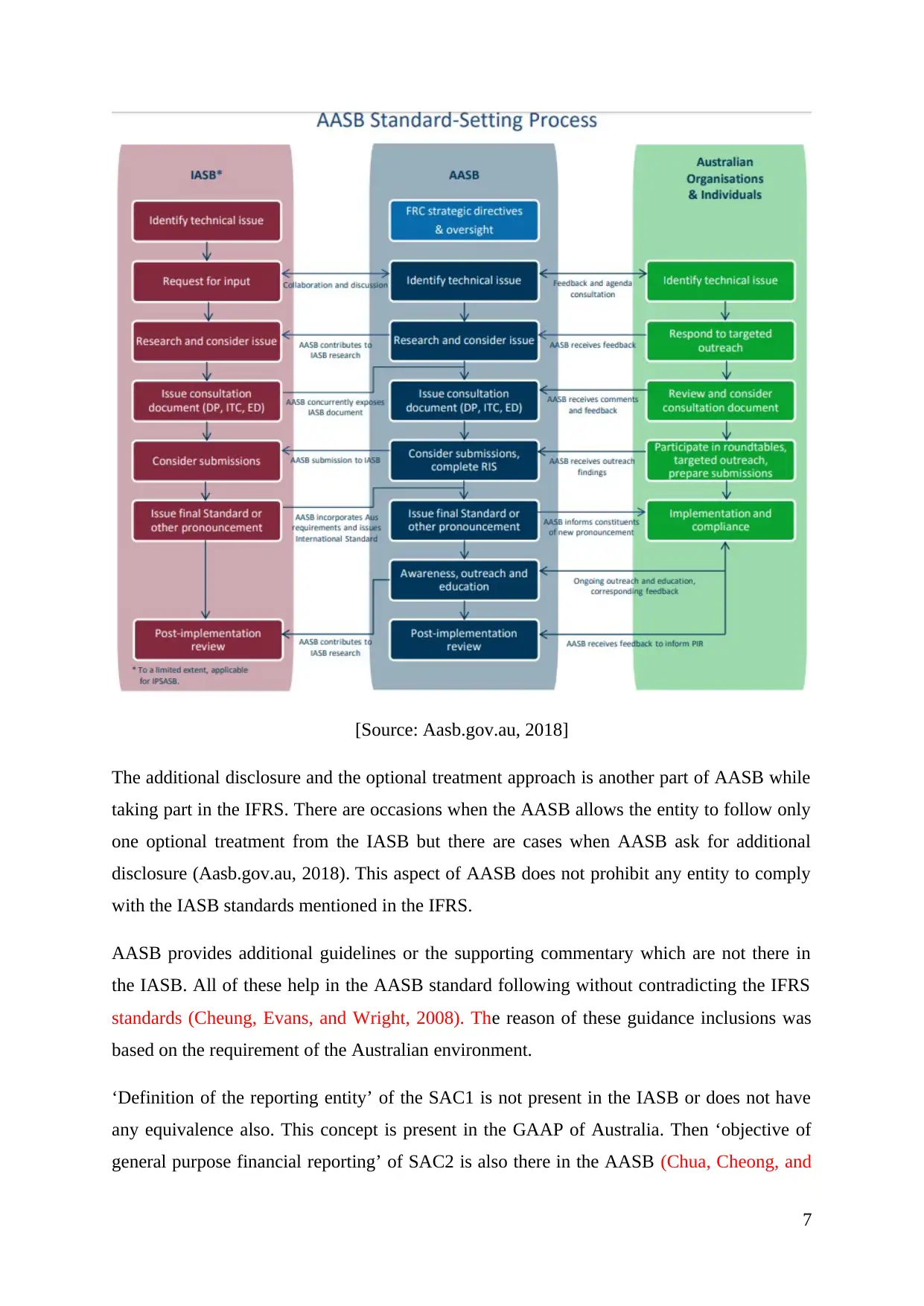

The IFRS and the AASB’s taking part in this process of global accounting

Main approach that is followed by the AASB in the IFRS is the content and wording adoption

from the IASB’s IFRS standard. The development of AASB is done as the IASB’s Australian

equivalence (Chalmers, Clinch, and Godfrey, 2011). Therefore the adopted words are

changed following the accommodation requirements of the Australian legislative processes

and environment. IFRS is highly focused to be applied for the for-profit business entities.

Therefore the AASB’s new text inclusion is based on the additional or different requirements

of the not-for-profit organisations. There is no complication or confusion of these regulations

for the for-profit business entity (Cotter,Tarca, and Wee,2012). But the not-for-profit

organisation would not be able to comply with the IASB standards when it is complying with

the AASB standard because of the different approach of AASB for dealing with the not-for-

profit organisation.

6

The IFRS and the AASB’s taking part in this process of global accounting

Main approach that is followed by the AASB in the IFRS is the content and wording adoption

from the IASB’s IFRS standard. The development of AASB is done as the IASB’s Australian

equivalence (Chalmers, Clinch, and Godfrey, 2011). Therefore the adopted words are

changed following the accommodation requirements of the Australian legislative processes

and environment. IFRS is highly focused to be applied for the for-profit business entities.

Therefore the AASB’s new text inclusion is based on the additional or different requirements

of the not-for-profit organisations. There is no complication or confusion of these regulations

for the for-profit business entity (Cotter,Tarca, and Wee,2012). But the not-for-profit

organisation would not be able to comply with the IASB standards when it is complying with

the AASB standard because of the different approach of AASB for dealing with the not-for-

profit organisation.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

[Source: Aasb.gov.au, 2018]

The additional disclosure and the optional treatment approach is another part of AASB while

taking part in the IFRS. There are occasions when the AASB allows the entity to follow only

one optional treatment from the IASB but there are cases when AASB ask for additional

disclosure (Aasb.gov.au, 2018). This aspect of AASB does not prohibit any entity to comply

with the IASB standards mentioned in the IFRS.

AASB provides additional guidelines or the supporting commentary which are not there in

the IASB. All of these help in the AASB standard following without contradicting the IFRS

standards (Cheung, Evans, and Wright, 2008). The reason of these guidance inclusions was

based on the requirement of the Australian environment.

‘Definition of the reporting entity’ of the SAC1 is not present in the IASB or does not have

any equivalence also. This concept is present in the GAAP of Australia. Then ‘objective of

general purpose financial reporting’ of SAC2 is also there in the AASB (Chua, Cheong, and

7

The additional disclosure and the optional treatment approach is another part of AASB while

taking part in the IFRS. There are occasions when the AASB allows the entity to follow only

one optional treatment from the IASB but there are cases when AASB ask for additional

disclosure (Aasb.gov.au, 2018). This aspect of AASB does not prohibit any entity to comply

with the IASB standards mentioned in the IFRS.

AASB provides additional guidelines or the supporting commentary which are not there in

the IASB. All of these help in the AASB standard following without contradicting the IFRS

standards (Cheung, Evans, and Wright, 2008). The reason of these guidance inclusions was

based on the requirement of the Australian environment.

‘Definition of the reporting entity’ of the SAC1 is not present in the IASB or does not have

any equivalence also. This concept is present in the GAAP of Australia. Then ‘objective of

general purpose financial reporting’ of SAC2 is also there in the AASB (Chua, Cheong, and

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gould, 2012). All of these are applicable for the matters that are only in the AASB but this

approach are not in conflict with the disclosure, measurement and recognition of the

standards terms.

There are some other AASB standards like the standards for the materiality which are not so

different from the IFRS but more comprehensive in nature (Cheung et al., 2008). All of these

factors do not change the AASB’s approach of regulation much from the IASB.

In this process of taking part some other aspect are followed to support other issues. The

technical issues in this process addressed differently. IFRS or the IASB mainly identifies the

technical issues of this process. Then those issues would be taken from the work program of

IFRS into the work program of AASB. The issue-by-issue approach is followed in a non-

substantive and substantive manner by the AASB (Aasb.gov.au, 2018). Then there could be

other issues which are technical nature identified by the board member of AASB. These

issues which are for-profit organisations’ are then referred to IFRS or the IASB. This is the

consolidation process of technical issue identified by AASB. Other stakeholder can also

identify the issues and approach to AASB for advice. The project proposal of the identified

issue is prepared by the AASB to be included in their agenda to be decided by the board of

AASB (Chua, Cheong, and Gould, 2012). After the consolidation process based on the

research, wonder stakeholder consultation, the pronouncement is issued. The financial

implementation of the standard is done by the AASB of the proposed internal changes.

The IFRS standards based on the principle and not on the clear rule based approaches. This

approach gives lot of flexibility for the member country business entities to adopt the

standard in their accounting process but have chance of window dressing than honest

representation of the information (Morris, Gray, Pickering and Aisbitt, 2013). Moreover the

standards of IFRS are not made compulsory for IASB member countries. The reason of this

on compulsory approach is the value based adoption of the process rather than creation of an

artificial uniformity of accounting process. The business and business environment varies in

different countries. This wide variety may not suite the standard to different countries and

because of that reason the standard is not made compulsory for the members (Morris,

Gray,Pickering, and Aisbitt, 2013). But it is though that the standard would be useful in the

globalised business context and the system has some direct benefit like the cheaper capital,

compatibility benefit for the investors, lower cost of accounting and so on. In a non

compulsory more the adoption would happen on the basis of these values.

8

approach are not in conflict with the disclosure, measurement and recognition of the

standards terms.

There are some other AASB standards like the standards for the materiality which are not so

different from the IFRS but more comprehensive in nature (Cheung et al., 2008). All of these

factors do not change the AASB’s approach of regulation much from the IASB.

In this process of taking part some other aspect are followed to support other issues. The

technical issues in this process addressed differently. IFRS or the IASB mainly identifies the

technical issues of this process. Then those issues would be taken from the work program of

IFRS into the work program of AASB. The issue-by-issue approach is followed in a non-

substantive and substantive manner by the AASB (Aasb.gov.au, 2018). Then there could be

other issues which are technical nature identified by the board member of AASB. These

issues which are for-profit organisations’ are then referred to IFRS or the IASB. This is the

consolidation process of technical issue identified by AASB. Other stakeholder can also

identify the issues and approach to AASB for advice. The project proposal of the identified

issue is prepared by the AASB to be included in their agenda to be decided by the board of

AASB (Chua, Cheong, and Gould, 2012). After the consolidation process based on the

research, wonder stakeholder consultation, the pronouncement is issued. The financial

implementation of the standard is done by the AASB of the proposed internal changes.

The IFRS standards based on the principle and not on the clear rule based approaches. This

approach gives lot of flexibility for the member country business entities to adopt the

standard in their accounting process but have chance of window dressing than honest

representation of the information (Morris, Gray, Pickering and Aisbitt, 2013). Moreover the

standards of IFRS are not made compulsory for IASB member countries. The reason of this

on compulsory approach is the value based adoption of the process rather than creation of an

artificial uniformity of accounting process. The business and business environment varies in

different countries. This wide variety may not suite the standard to different countries and

because of that reason the standard is not made compulsory for the members (Morris,

Gray,Pickering, and Aisbitt, 2013). But it is though that the standard would be useful in the

globalised business context and the system has some direct benefit like the cheaper capital,

compatibility benefit for the investors, lower cost of accounting and so on. In a non

compulsory more the adoption would happen on the basis of these values.

8

Owner’s equity

Item of equity and the changing pattern of it

As studies conducted by Khan, (2015), said that equity also referred as the net assets, the

organization ownership’s claim to organization assists after liabilities of organization is paid

off. In other word, equity of an organization is computed by subtracting organization

liabilities from organization assets. In order to successfully evaluated and analyzed the

performance of the organization based on equity, Woolworths limited, Wesfarmers Ltd, Myer

Holdings Ltd and JB Hi Fi Ltd are selected. All organizations are based on the retail sectors

and performing well in Australia market and also listed in Australian Exchange securities

Exchange. While comparing the equity performance of an organization Wesfarmers, it is seen

that shareholders’ equity of the organization is increased by 4.3% from $22,949 million to

$23,941 million from 2015 to 2016. In addition to this, it can be observed that reserve

performance of the business is increased about 14% from FY2016 to FY2017, but in

FY2016/15 and FY2015/14 it performance is decreased about 27% and 45% respectively. In

addition to this, organization performance in regards to retained earnings is increased by 73%

and issued capital is decreased by 3%. While comparing these performances with Woolworth

limited then it is observed that organization performance in contributed equity, reserves,

retain earnings is deceased from FY2016/17 to FY2016/15. On the other hand, it is seen that

Myer holding lit performance in terms of reserves and retained earnings is deceased by 22%

and 9% [retained earnings (FY2016/17; $342.146m, FY2016/14; $ 49.3m; FY2016/14; $

56.521m)]. Therefore from the findings and analysis it can be seen that, performance of the

organization JB Hi Fi Ltd is well as the company can achieve positive trends in FY2016/17 as

compared to other organization in same sectors. In addition to this, performance of the

organization JB Hi Fi Ltd in context to retained earnings is increased by 50%, 54% and 16%

from period of 2014 to 2017. From the findings and analysis, it can be said that positive

trend in retained earnings of the organization JB Hi Fi Ltd is due to positive net earnings in

same time period.

Position of debt to equity analysis

The position of debt and equity for the business needs to be constantly assessed to manage

the risk of doing business. Debt is an obligation for the company, whereas the equity is also a

liability for the business but is not mandatory for the business to be redeemed. Therefore debt

9

Item of equity and the changing pattern of it

As studies conducted by Khan, (2015), said that equity also referred as the net assets, the

organization ownership’s claim to organization assists after liabilities of organization is paid

off. In other word, equity of an organization is computed by subtracting organization

liabilities from organization assets. In order to successfully evaluated and analyzed the

performance of the organization based on equity, Woolworths limited, Wesfarmers Ltd, Myer

Holdings Ltd and JB Hi Fi Ltd are selected. All organizations are based on the retail sectors

and performing well in Australia market and also listed in Australian Exchange securities

Exchange. While comparing the equity performance of an organization Wesfarmers, it is seen

that shareholders’ equity of the organization is increased by 4.3% from $22,949 million to

$23,941 million from 2015 to 2016. In addition to this, it can be observed that reserve

performance of the business is increased about 14% from FY2016 to FY2017, but in

FY2016/15 and FY2015/14 it performance is decreased about 27% and 45% respectively. In

addition to this, organization performance in regards to retained earnings is increased by 73%

and issued capital is decreased by 3%. While comparing these performances with Woolworth

limited then it is observed that organization performance in contributed equity, reserves,

retain earnings is deceased from FY2016/17 to FY2016/15. On the other hand, it is seen that

Myer holding lit performance in terms of reserves and retained earnings is deceased by 22%

and 9% [retained earnings (FY2016/17; $342.146m, FY2016/14; $ 49.3m; FY2016/14; $

56.521m)]. Therefore from the findings and analysis it can be seen that, performance of the

organization JB Hi Fi Ltd is well as the company can achieve positive trends in FY2016/17 as

compared to other organization in same sectors. In addition to this, performance of the

organization JB Hi Fi Ltd in context to retained earnings is increased by 50%, 54% and 16%

from period of 2014 to 2017. From the findings and analysis, it can be said that positive

trend in retained earnings of the organization JB Hi Fi Ltd is due to positive net earnings in

same time period.

Position of debt to equity analysis

The position of debt and equity for the business needs to be constantly assessed to manage

the risk of doing business. Debt is an obligation for the company, whereas the equity is also a

liability for the business but is not mandatory for the business to be redeemed. Therefore debt

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is risky for the business. This business position can be understood from the debt to equity

ratio of the business (Delen, Kuzey, and Uyar, 2013). The ratio is calculated by dividing total

liability by total equity. This is the leveraging position identification for the organisation. The

analysis of this ratio can be done through multiple year analysis of the same company and

also for the similar industry companies.

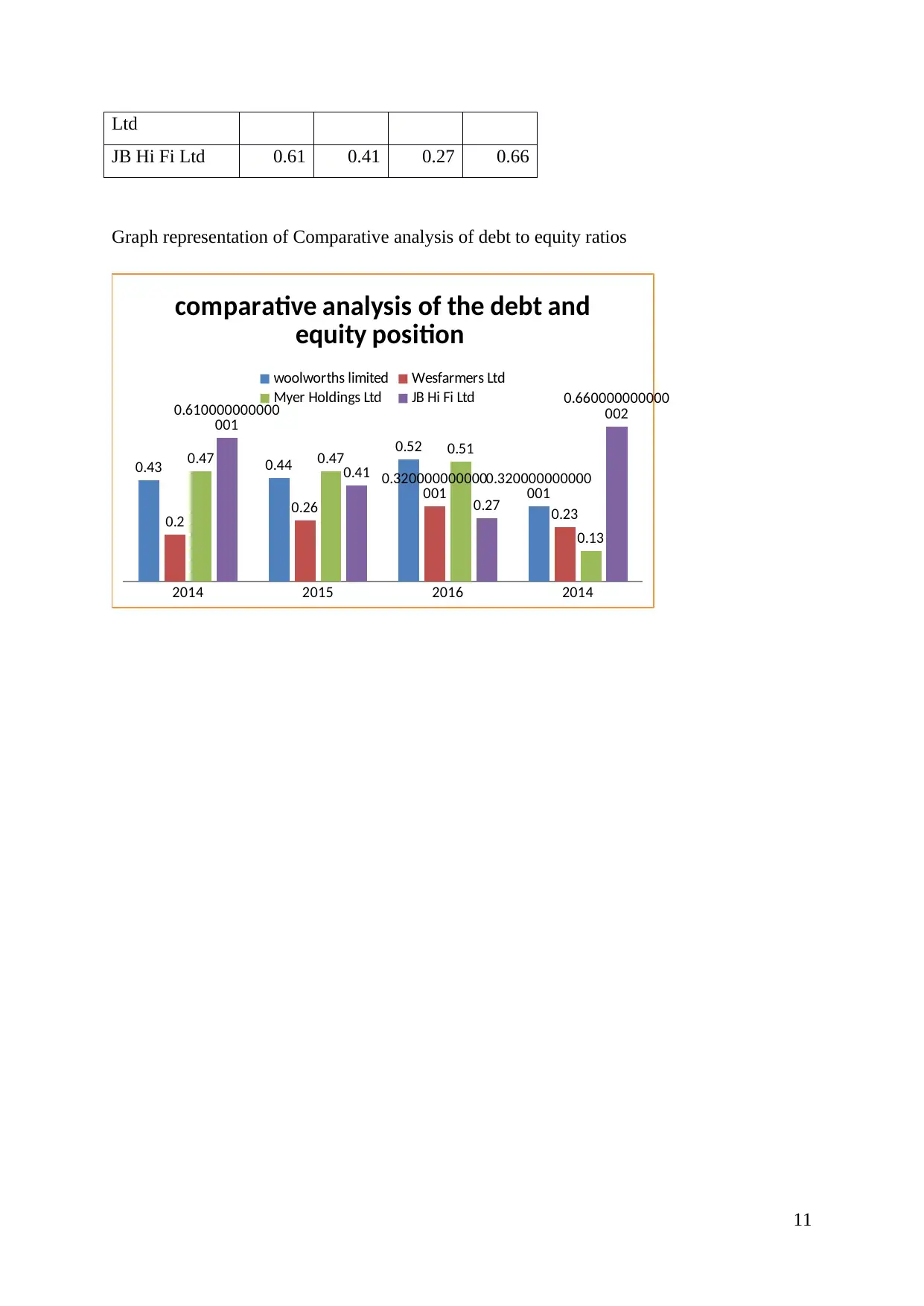

In the table below the debt to equity ratio of different company is shown for four years of

four companies. In case of Woolworths limited the ratio increased from 2014 to 2016 and

crossed the halfway market but again dropped significantly in 2017 to 0.32. Therefore the

business continues to increase their debt risk to fund their growth driving activity but a

pragmatic approach is taken in the 2017 (Liang, Lu,Tsai, and Shih, 2016). For Wesfarmers

Ltd the trend is similar but the ratio is lower than Woolworths limited. The cases of Myer

Holdings Ltd also have the higher ratio and growing trend like the Woolworths limited. There

had much more strict corrective measure in 2017 where the ratio dropped from .51 to .13.

This aspect also means a sudden drop in the business or the economic activity in the

organisation. Considering first three organisations it can be said that the growth prospects of

the retail business in the 2017 were not as bullish as of the previous three years (Liang, Lu,

Tsai, and Shih, 2016). The case of JB Hi Fi Ltd is somewhat different. The ratio is highly

fluctuating in nature. In the 2017 the ratio reached highest of 0.66 for the company and the

industry. The industry average considering the past four years of data is around 0.39.

Therefore Wesfarmers Ltd always remained on the less risky side of the industry by

sacrificing growth opportunity to some extent (Delen, Kuzey, and Uyar, 2013). JB Hi Fi

Ltd’s unpredictable data could be a cause of concern for the wrong strategy of the business.

When the business is becoming risky the investor is taking more risk. Therefore the investor

can expect better return from the stock.

Debt to equity

ratios 2014 2015 2016 2017

Woolworths

limited 0.43 0.44 0.52 0.32

Wesfarmers

Ltd 0.2 0.26 0.32 0.23

Myer Holdings 0.47 0.47 0.51 0.13

10

ratio of the business (Delen, Kuzey, and Uyar, 2013). The ratio is calculated by dividing total

liability by total equity. This is the leveraging position identification for the organisation. The

analysis of this ratio can be done through multiple year analysis of the same company and

also for the similar industry companies.

In the table below the debt to equity ratio of different company is shown for four years of

four companies. In case of Woolworths limited the ratio increased from 2014 to 2016 and

crossed the halfway market but again dropped significantly in 2017 to 0.32. Therefore the

business continues to increase their debt risk to fund their growth driving activity but a

pragmatic approach is taken in the 2017 (Liang, Lu,Tsai, and Shih, 2016). For Wesfarmers

Ltd the trend is similar but the ratio is lower than Woolworths limited. The cases of Myer

Holdings Ltd also have the higher ratio and growing trend like the Woolworths limited. There

had much more strict corrective measure in 2017 where the ratio dropped from .51 to .13.

This aspect also means a sudden drop in the business or the economic activity in the

organisation. Considering first three organisations it can be said that the growth prospects of

the retail business in the 2017 were not as bullish as of the previous three years (Liang, Lu,

Tsai, and Shih, 2016). The case of JB Hi Fi Ltd is somewhat different. The ratio is highly

fluctuating in nature. In the 2017 the ratio reached highest of 0.66 for the company and the

industry. The industry average considering the past four years of data is around 0.39.

Therefore Wesfarmers Ltd always remained on the less risky side of the industry by

sacrificing growth opportunity to some extent (Delen, Kuzey, and Uyar, 2013). JB Hi Fi

Ltd’s unpredictable data could be a cause of concern for the wrong strategy of the business.

When the business is becoming risky the investor is taking more risk. Therefore the investor

can expect better return from the stock.

Debt to equity

ratios 2014 2015 2016 2017

Woolworths

limited 0.43 0.44 0.52 0.32

Wesfarmers

Ltd 0.2 0.26 0.32 0.23

Myer Holdings 0.47 0.47 0.51 0.13

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ltd

JB Hi Fi Ltd 0.61 0.41 0.27 0.66

Graph representation of Comparative analysis of debt to equity ratios

2014 2015 2016 2014

0.43 0.44

0.52

0.320000000000

001

0.2 0.26

0.320000000000

001

0.23

0.47 0.47 0.51

0.13

0.610000000000

001

0.41

0.27

0.660000000000

002

comparative analysis of the debt and

equity position

woolworths limited Wesfarmers Ltd

Myer Holdings Ltd JB Hi Fi Ltd

11

JB Hi Fi Ltd 0.61 0.41 0.27 0.66

Graph representation of Comparative analysis of debt to equity ratios

2014 2015 2016 2014

0.43 0.44

0.52

0.320000000000

001

0.2 0.26

0.320000000000

001

0.23

0.47 0.47 0.51

0.13

0.610000000000

001

0.41

0.27

0.660000000000

002

comparative analysis of the debt and

equity position

woolworths limited Wesfarmers Ltd

Myer Holdings Ltd JB Hi Fi Ltd

11

Conclusion

The financial and accounting information evaluation was able to provide proper insight for

the corporate accounting process. The need for the regulatory approach and the analysis of

AASB relation with IFRS provided the requirements of standardised approach of accounting.

The company analysis is showing the approach of interpretation and usefulness of accounting

and financial information for different stakeholder.

12

The financial and accounting information evaluation was able to provide proper insight for

the corporate accounting process. The need for the regulatory approach and the analysis of

AASB relation with IFRS provided the requirements of standardised approach of accounting.

The company analysis is showing the approach of interpretation and usefulness of accounting

and financial information for different stakeholder.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.