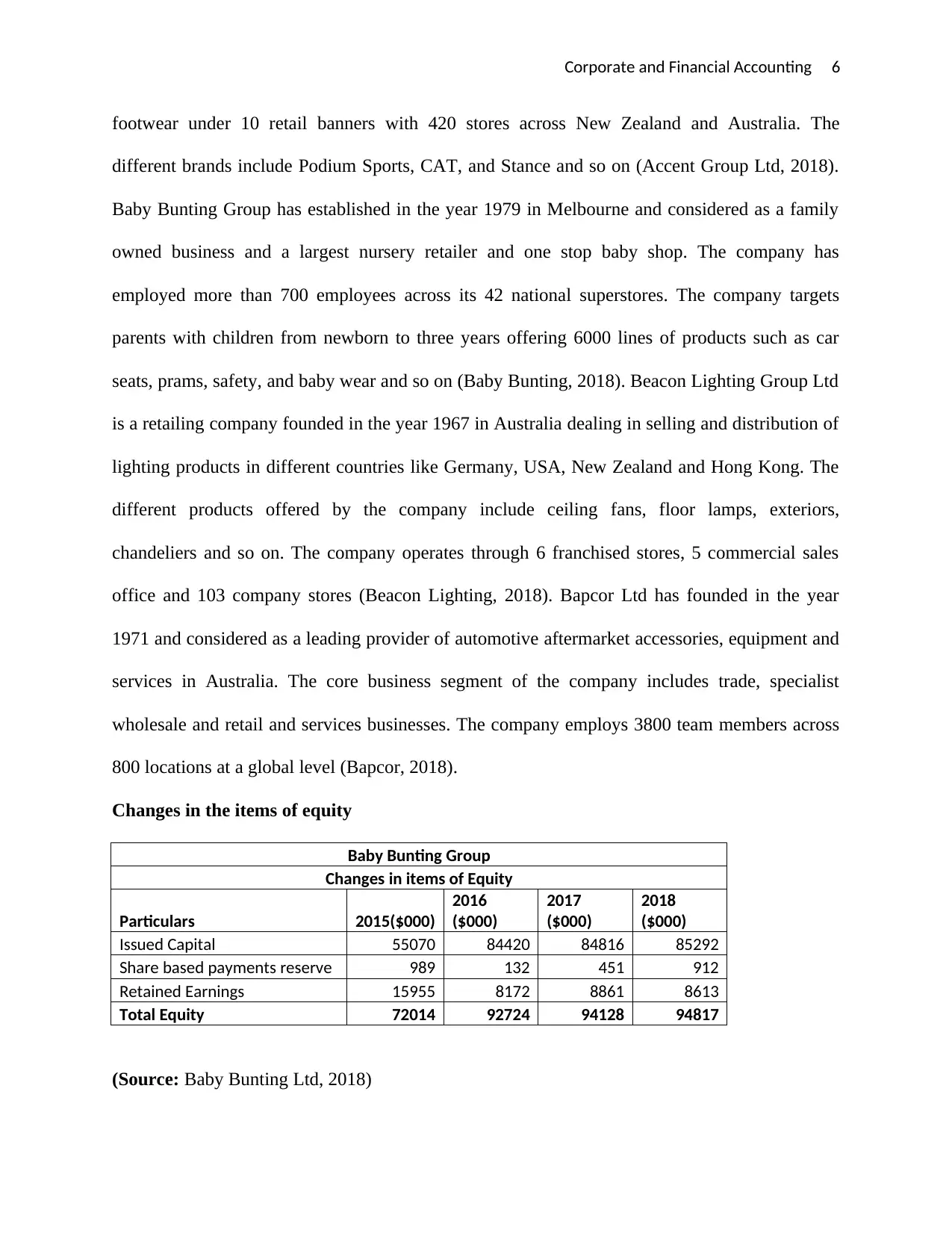

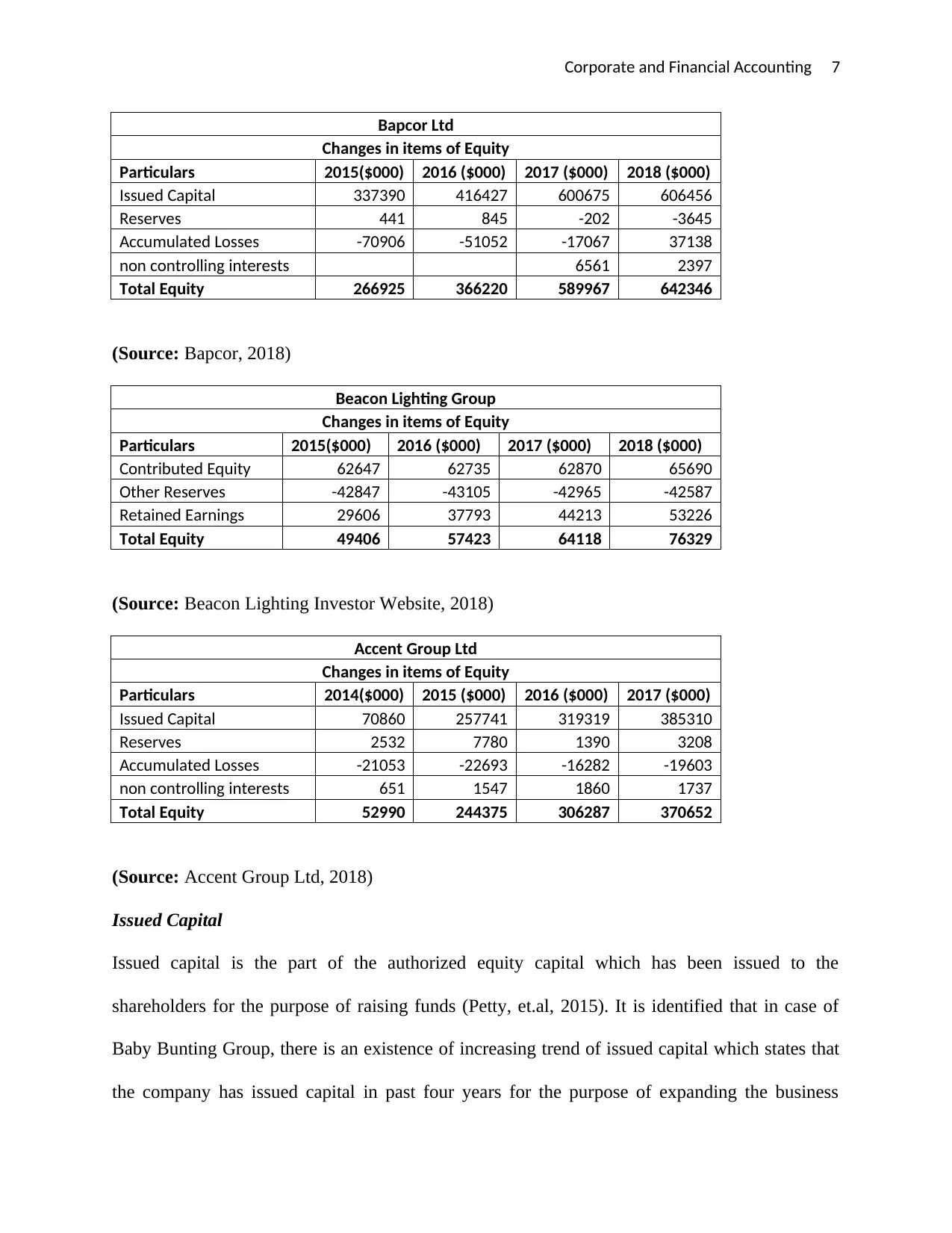

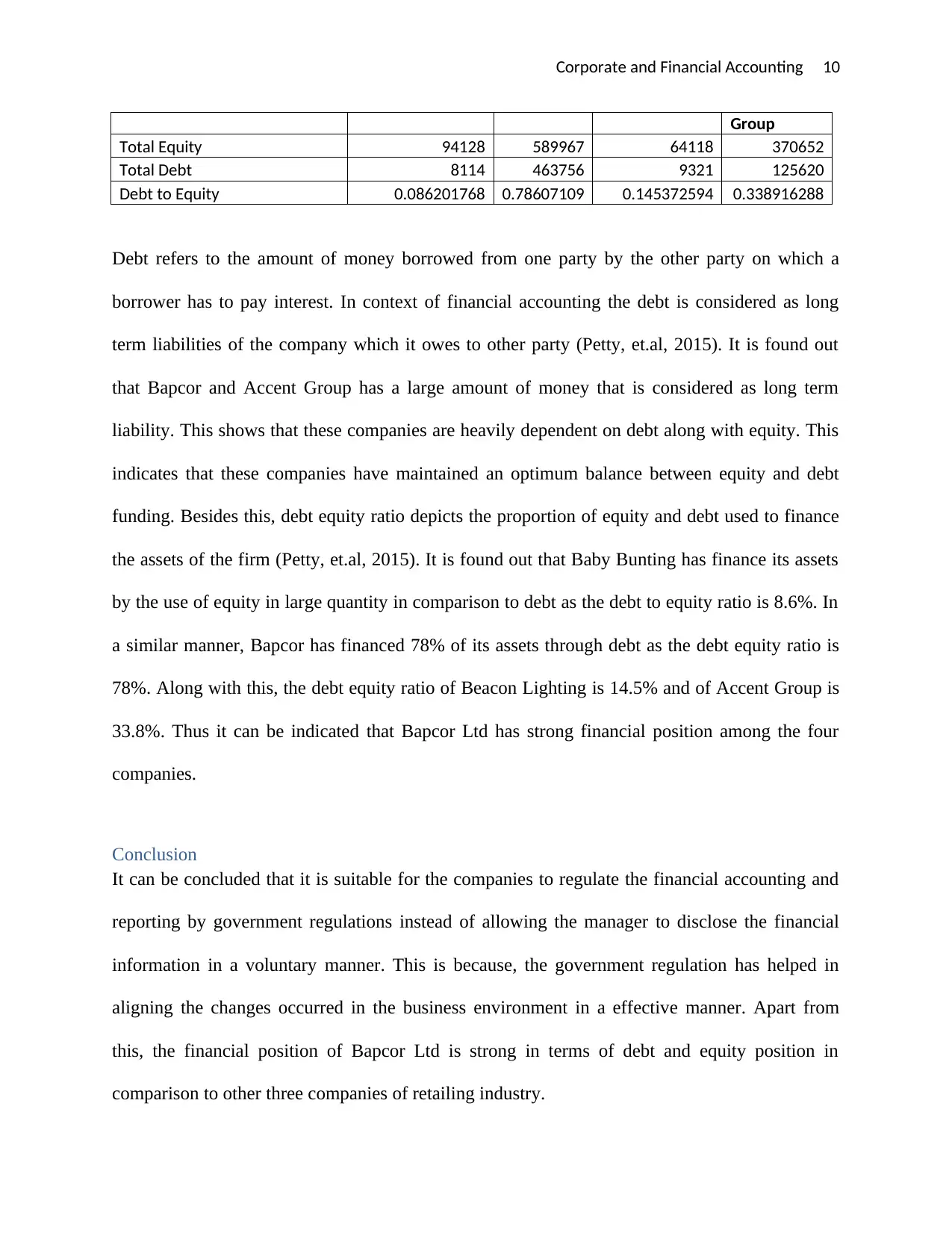

Corporate and Financial Accounting: Importance of Corporate Regulation and Analysis of Owners Equity and Debt-Equity Position of Four Australian Companies

VerifiedAI Summary

This report emphasizes on the importance and role of corporate regulation in the disclosure of the financial information in comparison of the disclosure of the financial accounting information in a voluntary method by a manager. It also focuses on the analysis of the items of equity present in the balance sheet of the four companies of Australia that are listed in ASX related to same industry and find out the reasons for the occurrence of the change. It also entails the information related to the comparative analysis of the debt and equity position of these four firms.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)