Equity and liability of Woolworths and Wesfarmers

VerifiedAdded on 2021/02/20

|12

|2429

|379

AI Summary

3 3) Items recorded under liability section.4 4) Movement of items recorded under liability section.5 5) Benefits and limitations of sources of funds.6 PART B7 Concept of small company, large company and reporting entity. The items that are recorded in owner's equity section of Wools Worth and Wesfarmers are as follows - Reserves - In financial accounting, reserves are the item that is recorded under owners’ equity section and contains a credit balance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

CORPORATE FINANCIAL

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Abstract

The Report has described the items that comes under equity and liability section of two

firms that are Woolworths and Wesfarmers. Advantage and disadvantage of sources of funds. It

also explains meaning of small, large proprietary company and reporting entity.

The Report has described the items that comes under equity and liability section of two

firms that are Woolworths and Wesfarmers. Advantage and disadvantage of sources of funds. It

also explains meaning of small, large proprietary company and reporting entity.

Table of Contents

Abstract............................................................................................................................................2

INTRODUCTION...........................................................................................................................2

PART A...........................................................................................................................................2

1)Items recorded under owner's equity section............................................................................2

2. Explaining the change in the items recorded under an owner’s equity segment of the balance

sheet.............................................................................................................................................3

3) Items recorded under liability section.....................................................................................4

4) Movement of items recorded under liability section...............................................................5

5) Benefits and limitations of sources of funds...........................................................................6

PART B............................................................................................................................................7

Concept of small company, large company and reporting entity................................................7

CONCLUSION................................................................................................................................9

REFERENCES................................................................................................................................9

1

Abstract............................................................................................................................................2

INTRODUCTION...........................................................................................................................2

PART A...........................................................................................................................................2

1)Items recorded under owner's equity section............................................................................2

2. Explaining the change in the items recorded under an owner’s equity segment of the balance

sheet.............................................................................................................................................3

3) Items recorded under liability section.....................................................................................4

4) Movement of items recorded under liability section...............................................................5

5) Benefits and limitations of sources of funds...........................................................................6

PART B............................................................................................................................................7

Concept of small company, large company and reporting entity................................................7

CONCLUSION................................................................................................................................9

REFERENCES................................................................................................................................9

1

INTRODUCTION

Financial accounting is related with reporting of historical nature information. It can be

described as the field of accounting related with analysis and reporting of financial transactions.

The Report is based on two companies. Woolworths Group was founded in year 1924. It is

Headquartered in New South Wales, Australia. It offers products through chain of supermarkets

etc. Wesfarmers belongs to conglomerate industry. It was founded in year 1914. Headquarter is

located in Western Australia. It operates department stores etc. The Report will outline items that

are recorded under equity and liability section. Movement in items of equity and liability section,

sources of funds used by companies. It will also explain small, large proprietary firm and

reporting entity with difference among these.

PART A

1)Items recorded under owner's equity section.

Owner' equity

It refers to the part of the value of all the assets that owner can claim in case of sole

proprietorship or partnership firm or by the shareholders in case of company. The items that are

recorded in owner's equity section of Wools Worth and Wesfarmers are as follows -

Reserves -

In financial accounting, reserves are the item that is recorded under owners’ equity

section and contains a credit balance. It can be component of any part of equity of shareholders

except basic or contributed share capital. There may be different types of reserves such as

revenue reserves, realized reserves, capital reserves etc. For example – In year 2016, total

amount of reserves in Woolworths is $ 93.9 million.

Issued capital -

Total number of shares that can be issued by the firm is limited up to the total number of

authorized shares. Issued shares can be described as the total outstanding shares that are held by

shareholders. It forms the equity share capital of the organisation. Example – Total amount of

issued share capital of Wesfarmers in year 2017 is $ 22268 million.

Retained earnings

It can be defined as the amount of net income accumulated in different areas and has kept

in the firm. It is the amount which is left over after making payment of dividend to the owners of

shares. Generally, firm re-invest the amount of accumulated net profit for the growth of firm.

2

Financial accounting is related with reporting of historical nature information. It can be

described as the field of accounting related with analysis and reporting of financial transactions.

The Report is based on two companies. Woolworths Group was founded in year 1924. It is

Headquartered in New South Wales, Australia. It offers products through chain of supermarkets

etc. Wesfarmers belongs to conglomerate industry. It was founded in year 1914. Headquarter is

located in Western Australia. It operates department stores etc. The Report will outline items that

are recorded under equity and liability section. Movement in items of equity and liability section,

sources of funds used by companies. It will also explain small, large proprietary firm and

reporting entity with difference among these.

PART A

1)Items recorded under owner's equity section.

Owner' equity

It refers to the part of the value of all the assets that owner can claim in case of sole

proprietorship or partnership firm or by the shareholders in case of company. The items that are

recorded in owner's equity section of Wools Worth and Wesfarmers are as follows -

Reserves -

In financial accounting, reserves are the item that is recorded under owners’ equity

section and contains a credit balance. It can be component of any part of equity of shareholders

except basic or contributed share capital. There may be different types of reserves such as

revenue reserves, realized reserves, capital reserves etc. For example – In year 2016, total

amount of reserves in Woolworths is $ 93.9 million.

Issued capital -

Total number of shares that can be issued by the firm is limited up to the total number of

authorized shares. Issued shares can be described as the total outstanding shares that are held by

shareholders. It forms the equity share capital of the organisation. Example – Total amount of

issued share capital of Wesfarmers in year 2017 is $ 22268 million.

Retained earnings

It can be defined as the amount of net income accumulated in different areas and has kept

in the firm. It is the amount which is left over after making payment of dividend to the owners of

shares. Generally, firm re-invest the amount of accumulated net profit for the growth of firm.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Profit helps to increase the amount of retained earnings while losses and payment of dividend

(Unerman, J., Bebbington and O’dwyer, 2018).

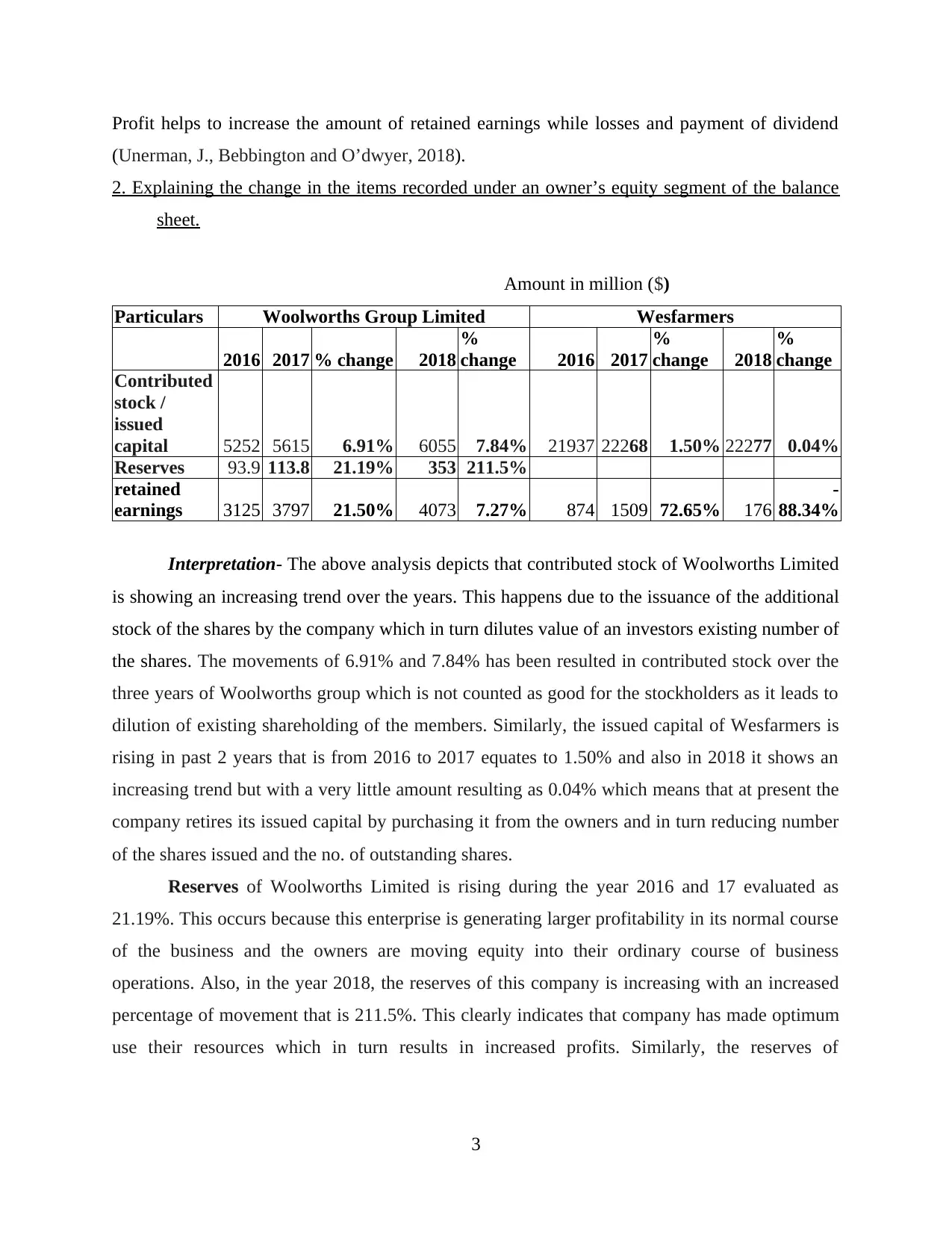

2. Explaining the change in the items recorded under an owner’s equity segment of the balance

sheet.

Amount in million ($)

Particulars Woolworths Group Limited Wesfarmers

2016 2017 % change 2018

%

change 2016 2017

%

change 2018

%

change

Contributed

stock /

issued

capital 5252 5615 6.91% 6055 7.84% 21937 22268 1.50% 22277 0.04%

Reserves 93.9 113.8 21.19% 353 211.5%

retained

earnings 3125 3797 21.50% 4073 7.27% 874 1509 72.65% 176

-

88.34%

Interpretation- The above analysis depicts that contributed stock of Woolworths Limited

is showing an increasing trend over the years. This happens due to the issuance of the additional

stock of the shares by the company which in turn dilutes value of an investors existing number of

the shares. The movements of 6.91% and 7.84% has been resulted in contributed stock over the

three years of Woolworths group which is not counted as good for the stockholders as it leads to

dilution of existing shareholding of the members. Similarly, the issued capital of Wesfarmers is

rising in past 2 years that is from 2016 to 2017 equates to 1.50% and also in 2018 it shows an

increasing trend but with a very little amount resulting as 0.04% which means that at present the

company retires its issued capital by purchasing it from the owners and in turn reducing number

of the shares issued and the no. of outstanding shares.

Reserves of Woolworths Limited is rising during the year 2016 and 17 evaluated as

21.19%. This occurs because this enterprise is generating larger profitability in its normal course

of the business and the owners are moving equity into their ordinary course of business

operations. Also, in the year 2018, the reserves of this company is increasing with an increased

percentage of movement that is 211.5%. This clearly indicates that company has made optimum

use their resources which in turn results in increased profits. Similarly, the reserves of

3

(Unerman, J., Bebbington and O’dwyer, 2018).

2. Explaining the change in the items recorded under an owner’s equity segment of the balance

sheet.

Amount in million ($)

Particulars Woolworths Group Limited Wesfarmers

2016 2017 % change 2018

%

change 2016 2017

%

change 2018

%

change

Contributed

stock /

issued

capital 5252 5615 6.91% 6055 7.84% 21937 22268 1.50% 22277 0.04%

Reserves 93.9 113.8 21.19% 353 211.5%

retained

earnings 3125 3797 21.50% 4073 7.27% 874 1509 72.65% 176

-

88.34%

Interpretation- The above analysis depicts that contributed stock of Woolworths Limited

is showing an increasing trend over the years. This happens due to the issuance of the additional

stock of the shares by the company which in turn dilutes value of an investors existing number of

the shares. The movements of 6.91% and 7.84% has been resulted in contributed stock over the

three years of Woolworths group which is not counted as good for the stockholders as it leads to

dilution of existing shareholding of the members. Similarly, the issued capital of Wesfarmers is

rising in past 2 years that is from 2016 to 2017 equates to 1.50% and also in 2018 it shows an

increasing trend but with a very little amount resulting as 0.04% which means that at present the

company retires its issued capital by purchasing it from the owners and in turn reducing number

of the shares issued and the no. of outstanding shares.

Reserves of Woolworths Limited is rising during the year 2016 and 17 evaluated as

21.19%. This occurs because this enterprise is generating larger profitability in its normal course

of the business and the owners are moving equity into their ordinary course of business

operations. Also, in the year 2018, the reserves of this company is increasing with an increased

percentage of movement that is 211.5%. This clearly indicates that company has made optimum

use their resources which in turn results in increased profits. Similarly, the reserves of

3

Wesfarmers Ltd is showing a rising trend and in the year 2018 it is increasing with a greater

value percentage from 14.45% to 81.05%.

Retained earnings of Woolworths is increasing over the years due to increase in the

profits that resulted from increases in sales. However, over the previous 2 years the retained

earnings of Wesfarmers Limited increases with a percentage change of 72.65% but in the last

year it decreases and resulted to -88.34% which shows that it declined from a greater value. This

happens because of the decrease in the sales and profit of the company in the previous year.

3) Items recorded under liability section.

Liability section:

It can be described as the obligations or financial debts of the firm that arises during the

course of the business. Liability can be divided into two parts that are non current and current

liabilities. Items that are recorded under the section of liabilities in Woolworths and Wesfarmers

Ltd. are as follows -

Current liabilities:

It refers to the debt or obligation that are to be payable by the firm within a year or during

an operating cycle. Current liabilities of the firm appear in liabilities section such as short term

debt, creditors etc.

Current tax payable -

It is a part of current liabilities section that is shown in balance sheet. It describes the

amount of tax payable by the company to the government. Example – Tax payable by

Woolsworth in year 2016 is $ 39.5 million and income tax payable of Wesfarmers equated to $

29 million.

Borrowings -

It is a part of current liabilities that appears on liabilities side of the balance sheet of the

organisation. Firms are required to pay short term debt within one year. Example- In year 2017,

the total amount of borrowings in Woolworths company was $ 253 million and of Wesfarmers

evaluated as $ 1347 million.

Trade and trade payables -

It refers to the amount owed by the firm from creditors like suppliers etc. It appears under

liability section of the company. Example- Total amount of payables in year 2017 in

4

value percentage from 14.45% to 81.05%.

Retained earnings of Woolworths is increasing over the years due to increase in the

profits that resulted from increases in sales. However, over the previous 2 years the retained

earnings of Wesfarmers Limited increases with a percentage change of 72.65% but in the last

year it decreases and resulted to -88.34% which shows that it declined from a greater value. This

happens because of the decrease in the sales and profit of the company in the previous year.

3) Items recorded under liability section.

Liability section:

It can be described as the obligations or financial debts of the firm that arises during the

course of the business. Liability can be divided into two parts that are non current and current

liabilities. Items that are recorded under the section of liabilities in Woolworths and Wesfarmers

Ltd. are as follows -

Current liabilities:

It refers to the debt or obligation that are to be payable by the firm within a year or during

an operating cycle. Current liabilities of the firm appear in liabilities section such as short term

debt, creditors etc.

Current tax payable -

It is a part of current liabilities section that is shown in balance sheet. It describes the

amount of tax payable by the company to the government. Example – Tax payable by

Woolsworth in year 2016 is $ 39.5 million and income tax payable of Wesfarmers equated to $

29 million.

Borrowings -

It is a part of current liabilities that appears on liabilities side of the balance sheet of the

organisation. Firms are required to pay short term debt within one year. Example- In year 2017,

the total amount of borrowings in Woolworths company was $ 253 million and of Wesfarmers

evaluated as $ 1347 million.

Trade and trade payables -

It refers to the amount owed by the firm from creditors like suppliers etc. It appears under

liability section of the company. Example- Total amount of payables in year 2017 in

4

Woolsworth was $ 6812 million and the trade payables of Wesfarmers resulted as $ 6615

million.

Non-current liabilities:

It refers to the obligations of the firm that are payable after one year. Examples of non-

current liabilities are long term debt, creditors etc.

Provisions - It refers to the amount set aside by the organisation for uncertain

obligations towards entity or individual. It helps firm to cover future liability. Example – In year

2016 total amount of provisions in Woolsworth is $ 1382.4 million and wesfarmers attained

provisions of $ 1554 million.

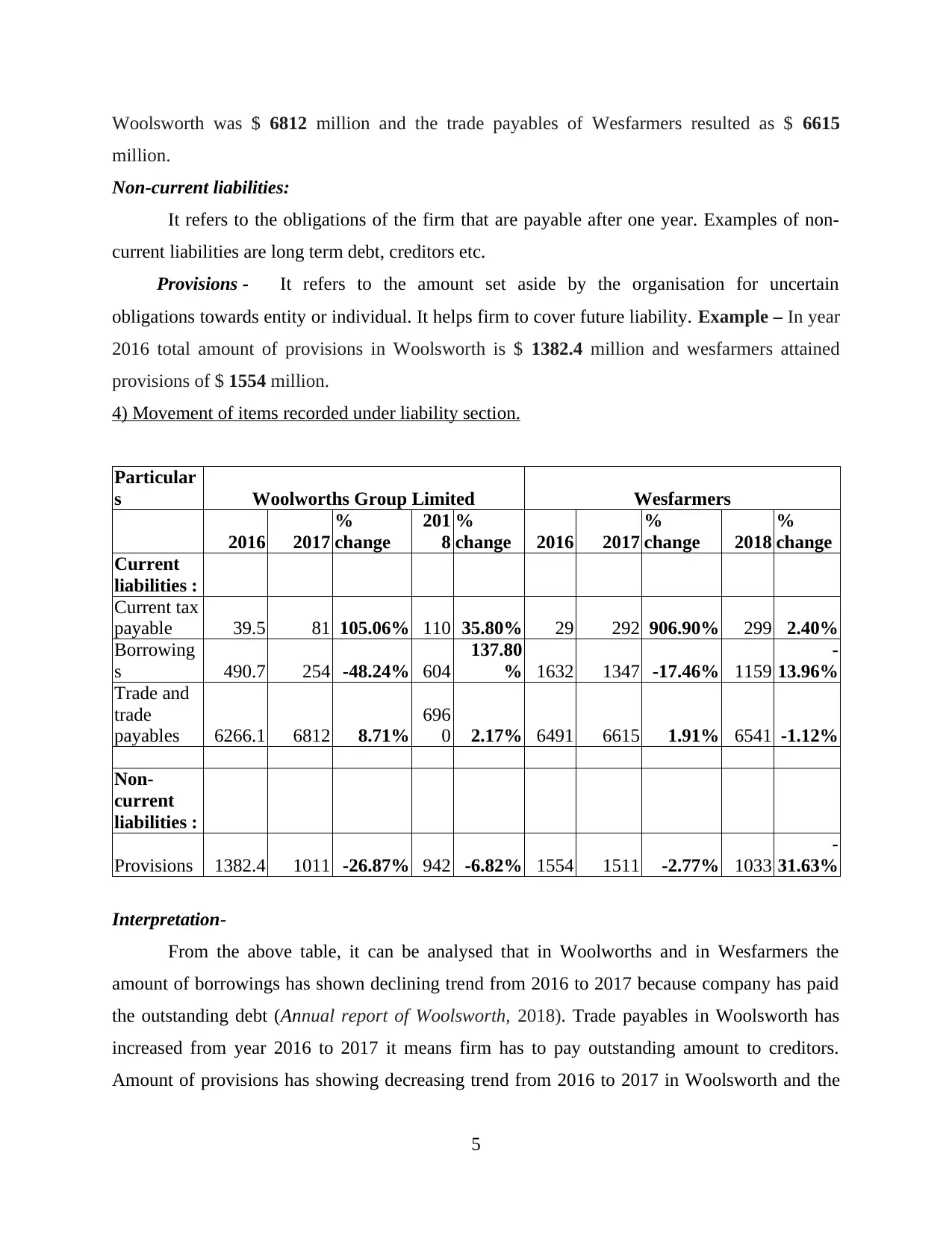

4) Movement of items recorded under liability section.

Particular

s Woolworths Group Limited Wesfarmers

2016 2017

%

change

201

8

%

change 2016 2017

%

change 2018

%

change

Current

liabilities :

Current tax

payable 39.5 81 105.06% 110 35.80% 29 292 906.90% 299 2.40%

Borrowing

s 490.7 254 -48.24% 604

137.80

% 1632 1347 -17.46% 1159

-

13.96%

Trade and

trade

payables 6266.1 6812 8.71%

696

0 2.17% 6491 6615 1.91% 6541 -1.12%

Non-

current

liabilities :

Provisions 1382.4 1011 -26.87% 942 -6.82% 1554 1511 -2.77% 1033

-

31.63%

Interpretation-

From the above table, it can be analysed that in Woolworths and in Wesfarmers the

amount of borrowings has shown declining trend from 2016 to 2017 because company has paid

the outstanding debt (Annual report of Woolsworth, 2018). Trade payables in Woolsworth has

increased from year 2016 to 2017 it means firm has to pay outstanding amount to creditors.

Amount of provisions has showing decreasing trend from 2016 to 2017 in Woolsworth and the

5

million.

Non-current liabilities:

It refers to the obligations of the firm that are payable after one year. Examples of non-

current liabilities are long term debt, creditors etc.

Provisions - It refers to the amount set aside by the organisation for uncertain

obligations towards entity or individual. It helps firm to cover future liability. Example – In year

2016 total amount of provisions in Woolsworth is $ 1382.4 million and wesfarmers attained

provisions of $ 1554 million.

4) Movement of items recorded under liability section.

Particular

s Woolworths Group Limited Wesfarmers

2016 2017

%

change

201

8

%

change 2016 2017

%

change 2018

%

change

Current

liabilities :

Current tax

payable 39.5 81 105.06% 110 35.80% 29 292 906.90% 299 2.40%

Borrowing

s 490.7 254 -48.24% 604

137.80

% 1632 1347 -17.46% 1159

-

13.96%

Trade and

trade

payables 6266.1 6812 8.71%

696

0 2.17% 6491 6615 1.91% 6541 -1.12%

Non-

current

liabilities :

Provisions 1382.4 1011 -26.87% 942 -6.82% 1554 1511 -2.77% 1033

-

31.63%

Interpretation-

From the above table, it can be analysed that in Woolworths and in Wesfarmers the

amount of borrowings has shown declining trend from 2016 to 2017 because company has paid

the outstanding debt (Annual report of Woolsworth, 2018). Trade payables in Woolsworth has

increased from year 2016 to 2017 it means firm has to pay outstanding amount to creditors.

Amount of provisions has showing decreasing trend from 2016 to 2017 in Woolsworth and the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

resultant amount remains unchanged in both the years that is 2017 and 2018 (Yiu, Wan and Xu,

2018).

5) Benefits and limitations of sources of funds.

There are various sources from which company can raise funds. Currently, Woolworths

and Wesfarmers are using following source of funds. Such as -

Equity-

Company can raise funds by issuing shares to shareholders. Benefit and limitations of

using equity finance for Woolworths and Wesfarmers are-

Advantage:

There is no obligation on the firm to pay fixed amount as in case of loan.

Equity shareholders does not expect immediate payment of return on investment.

Disadvantage:

By issuing additional equity shares, stake of owner get diluted (Schroeder, Clark, and

Cathey, 2019). Conflict may arise due to disagreement on management style.

Debt-

It refers to borrowing funds by the firm from another party to finance growth and

operations of the organisation.

Benefits:

Interest payable on debt is tax deductible.

Creditor does not have control on business.

Limitations:

Firm and lender should have good credit rating. Owner of the company may require to give personal guarantee.

Retained earnings-

It is considered as a major source of internal financing and it is a part of net profit set

aside by companies like Woolworths and Wesfarmers Ltd. It helps the firm in meeting out its

future contingency.

Advantage:

Firms does not have to incur any acquisition expenses.

It helps to improve financial position of firms.

6

2018).

5) Benefits and limitations of sources of funds.

There are various sources from which company can raise funds. Currently, Woolworths

and Wesfarmers are using following source of funds. Such as -

Equity-

Company can raise funds by issuing shares to shareholders. Benefit and limitations of

using equity finance for Woolworths and Wesfarmers are-

Advantage:

There is no obligation on the firm to pay fixed amount as in case of loan.

Equity shareholders does not expect immediate payment of return on investment.

Disadvantage:

By issuing additional equity shares, stake of owner get diluted (Schroeder, Clark, and

Cathey, 2019). Conflict may arise due to disagreement on management style.

Debt-

It refers to borrowing funds by the firm from another party to finance growth and

operations of the organisation.

Benefits:

Interest payable on debt is tax deductible.

Creditor does not have control on business.

Limitations:

Firm and lender should have good credit rating. Owner of the company may require to give personal guarantee.

Retained earnings-

It is considered as a major source of internal financing and it is a part of net profit set

aside by companies like Woolworths and Wesfarmers Ltd. It helps the firm in meeting out its

future contingency.

Advantage:

Firms does not have to incur any acquisition expenses.

It helps to improve financial position of firms.

6

Disadvantage:

In case of huge accumulated amount of retained earnings there may arise situation of over

capitalization (Malik and Kanwal, 2018).

PART B

Concept of small company, large company and reporting entity.

Small proprietary company:

It refers to a type of privately held firm that is operated by a single individual. It is

defined under section 45A (1) Corporations Act, 2001. Proprietary company is classified under

the category of small proprietary firm only when it fulfils conditions. These thresholds are

redefined under Corporations Amendment Regulations 2018. Further, these conditions are

applicable form 1st July, 2019. Such as -

Total assets are not more than $ 25 million at the time when financial year ends.

It should not have more than 100 workers at the end of financial year. Further, total gross operating revenue is not more than $ 25 million at the end of financial

year (Small Proprietary business, 2019)

Large proprietary company :

It is also defined under section 45A of Corporations Act, 2001. The section has

distinguished large companies with small companies. They differ on various basis of number of

employees, raising funds, disclosure requirements etc. Further, small and large companies are

also differentiated on the basis of operating revenue, total assets etc. A company is classified as

large proprietary firm only when it fulfils some conditions. These are as follows -

Total revenue should be at least $ 50 million at the end of financial year.

Total assets should be at least $ 25 million at the time when financial year ends.

Total number of employees should be minimum 100 (Epstein, 2018).

Reporting company :

Accounting Standards of Australia has defined the term Reporting entity as the firm in

which it is general to expect that the stakeholders are dependent on financial reports to obtain

information that will help them in taking decisions regarding proper utilisation of resources.

Whereas, International Financial Reporting Standards (IFRS) has provided the revised definition

of Reporting entity as the firm that chooses to prepare financial statements. Further, AASB does

not consider that it has the power to determine who should prepare financial statements.

7

In case of huge accumulated amount of retained earnings there may arise situation of over

capitalization (Malik and Kanwal, 2018).

PART B

Concept of small company, large company and reporting entity.

Small proprietary company:

It refers to a type of privately held firm that is operated by a single individual. It is

defined under section 45A (1) Corporations Act, 2001. Proprietary company is classified under

the category of small proprietary firm only when it fulfils conditions. These thresholds are

redefined under Corporations Amendment Regulations 2018. Further, these conditions are

applicable form 1st July, 2019. Such as -

Total assets are not more than $ 25 million at the time when financial year ends.

It should not have more than 100 workers at the end of financial year. Further, total gross operating revenue is not more than $ 25 million at the end of financial

year (Small Proprietary business, 2019)

Large proprietary company :

It is also defined under section 45A of Corporations Act, 2001. The section has

distinguished large companies with small companies. They differ on various basis of number of

employees, raising funds, disclosure requirements etc. Further, small and large companies are

also differentiated on the basis of operating revenue, total assets etc. A company is classified as

large proprietary firm only when it fulfils some conditions. These are as follows -

Total revenue should be at least $ 50 million at the end of financial year.

Total assets should be at least $ 25 million at the time when financial year ends.

Total number of employees should be minimum 100 (Epstein, 2018).

Reporting company :

Accounting Standards of Australia has defined the term Reporting entity as the firm in

which it is general to expect that the stakeholders are dependent on financial reports to obtain

information that will help them in taking decisions regarding proper utilisation of resources.

Whereas, International Financial Reporting Standards (IFRS) has provided the revised definition

of Reporting entity as the firm that chooses to prepare financial statements. Further, AASB does

not consider that it has the power to determine who should prepare financial statements.

7

Implications of different organizations-

small proprietary firm- Small proprietary companies do not require to prepare and file

financial statements, director's report etc. to ASIC unless they are controlled by foreign

company, shareholders more than 5% of total shareholders have vote to request the firm to

prepare financial report etc. (Dou, Wong and Xin, 2019). ASIC will provide relief to small

proprietary companies in respect of appointing an auditor, having financial report audited,

lodging the report of auditor etc. ASIC will consider various factors while providing relief such

as all the shareholders agrees that there is no requirement of audit, financial report is compiled

by an accountant etc. The relief is provided to small proprietary companies controlled by entity

situated in foreign country. It can avail tax benefits. Further it requires less number of

employees. Less than 100 workers are required (Crowther, 2018).

large proprietary firm- Large proprietary companies like Woolworths, Wesfarmers are

required to file director's report, financial report, and the audit report of the auditor to Australian

Securities and Investments Commission (ASIC) for every financial year. Firms like Woolworths

and Wesfarmers are required to loge audit report prepared by an auditor. Further, they have to

get audited the financial statements. Further, certain companies are exempted from this

requirement if, financial statements of large company are not audited for year ending 1993 or

financial year later than this from the requirements of the act. Large proprietary firms may

employ more than 100 employees. This will help in growth and sales of business.

Reporting entity- Reporting entities are required to prepare financial statements

according to Chapter 2M given under ASIC act. It should follow all the requirements regarding

accounting standards. Determination by the director's regarding status of entity as reporting or

non-reporting is an important factor that affects the disclosure of financial report. According to

AASB, the reporting entities are required to get audited their financial statements by an auditor.

Moreover, the auditor should provide information in the form of Report to the members of

reporting entity to get their written opinion on financial statements of the company. It has

obligation to comply all the accounting standards by preparing profit and loss statement, balance

sheet, cash flow statement etc. This helps to promote transparency in accounts. Accounting

standards are prescribed by Australian Accounting Standards Board (AASB).

8

small proprietary firm- Small proprietary companies do not require to prepare and file

financial statements, director's report etc. to ASIC unless they are controlled by foreign

company, shareholders more than 5% of total shareholders have vote to request the firm to

prepare financial report etc. (Dou, Wong and Xin, 2019). ASIC will provide relief to small

proprietary companies in respect of appointing an auditor, having financial report audited,

lodging the report of auditor etc. ASIC will consider various factors while providing relief such

as all the shareholders agrees that there is no requirement of audit, financial report is compiled

by an accountant etc. The relief is provided to small proprietary companies controlled by entity

situated in foreign country. It can avail tax benefits. Further it requires less number of

employees. Less than 100 workers are required (Crowther, 2018).

large proprietary firm- Large proprietary companies like Woolworths, Wesfarmers are

required to file director's report, financial report, and the audit report of the auditor to Australian

Securities and Investments Commission (ASIC) for every financial year. Firms like Woolworths

and Wesfarmers are required to loge audit report prepared by an auditor. Further, they have to

get audited the financial statements. Further, certain companies are exempted from this

requirement if, financial statements of large company are not audited for year ending 1993 or

financial year later than this from the requirements of the act. Large proprietary firms may

employ more than 100 employees. This will help in growth and sales of business.

Reporting entity- Reporting entities are required to prepare financial statements

according to Chapter 2M given under ASIC act. It should follow all the requirements regarding

accounting standards. Determination by the director's regarding status of entity as reporting or

non-reporting is an important factor that affects the disclosure of financial report. According to

AASB, the reporting entities are required to get audited their financial statements by an auditor.

Moreover, the auditor should provide information in the form of Report to the members of

reporting entity to get their written opinion on financial statements of the company. It has

obligation to comply all the accounting standards by preparing profit and loss statement, balance

sheet, cash flow statement etc. This helps to promote transparency in accounts. Accounting

standards are prescribed by Australian Accounting Standards Board (AASB).

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONCLUSION

The above report has explained that there are various items that come under equity

section like issued capital, reserves, retained earnings, etc. Further, it has analysed that firm have

to pay fixed interest on debt whereas there is no such requirement on equity financing. There are

various elements of liability section like borrowings, provisions etc. Moreover, it has been

concluded that total number of employees in small proprietary firm should be maximum 100

whereas, it can exceed in case of large proprietary firm. Trade payables in Woolsworth has

increased from year 2016 to 2017 it means firm has to pay outstanding amount to creditors in

near future.

REFERENCES

Crowther, D., 2018. A Social Critique of Corporate Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting: A Semiotic Analysis of Corporate Financial and

Environmental Reporting. Routledge.

Dou, Y., Wong, M. F. and Xin, B., 2019. The effect of financial reporting quality on corporate

investment efficiency: Evidence from the adoption of SFAS No. 123R. Management

Science, 65(5). pp.2249-2266.

Epstein, M. J., 2018. Making sustainability work: Best practices in managing and measuring

corporate social, environmental and economic impacts. Routledge.

Malik, M. S. and Kanwal, L., 2018. Impact of corporate social responsibility disclosure on

financial performance: Case study of listed pharmaceutical firms of Pakistan. Journal of

Business Ethics, 150(1). pp.69-78.

Schroeder, R. G., Clark, M. W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Unerman, J., Bebbington, J. and O’dwyer, B., 2018. Corporate reporting and accounting for

externalities. Accounting and Business Research, 48(5). pp.497-522.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Yiu, D. W., Wan, W. P. and Xu, Y., 2018. Alternative governance and corporate financial fraud

in transition economies: Evidence from China. Journal of Management,

p.0149206318764296.

Online

Annual report of Wesfarmers. 2017. [Online] Available Through:

<https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-

annual-report.pdf?sfvrsn=0>

Annual report of Wesfarmers. 2018. [Online] Available Through:

<https://www.wesfarmers.com.au/docs/default-source/asx-announcements/2018-annual-

report.pdf?sfvrsn=0>

Annual report of Woolsworth, 2017 [Online] Available Through:

<https://wow2017ar.qreports.com.au/home/performance-highlights/2017-at-a-

glance.html>

9

The above report has explained that there are various items that come under equity

section like issued capital, reserves, retained earnings, etc. Further, it has analysed that firm have

to pay fixed interest on debt whereas there is no such requirement on equity financing. There are

various elements of liability section like borrowings, provisions etc. Moreover, it has been

concluded that total number of employees in small proprietary firm should be maximum 100

whereas, it can exceed in case of large proprietary firm. Trade payables in Woolsworth has

increased from year 2016 to 2017 it means firm has to pay outstanding amount to creditors in

near future.

REFERENCES

Crowther, D., 2018. A Social Critique of Corporate Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting: A Semiotic Analysis of Corporate Financial and

Environmental Reporting. Routledge.

Dou, Y., Wong, M. F. and Xin, B., 2019. The effect of financial reporting quality on corporate

investment efficiency: Evidence from the adoption of SFAS No. 123R. Management

Science, 65(5). pp.2249-2266.

Epstein, M. J., 2018. Making sustainability work: Best practices in managing and measuring

corporate social, environmental and economic impacts. Routledge.

Malik, M. S. and Kanwal, L., 2018. Impact of corporate social responsibility disclosure on

financial performance: Case study of listed pharmaceutical firms of Pakistan. Journal of

Business Ethics, 150(1). pp.69-78.

Schroeder, R. G., Clark, M. W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Unerman, J., Bebbington, J. and O’dwyer, B., 2018. Corporate reporting and accounting for

externalities. Accounting and Business Research, 48(5). pp.497-522.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Yiu, D. W., Wan, W. P. and Xu, Y., 2018. Alternative governance and corporate financial fraud

in transition economies: Evidence from China. Journal of Management,

p.0149206318764296.

Online

Annual report of Wesfarmers. 2017. [Online] Available Through:

<https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-

annual-report.pdf?sfvrsn=0>

Annual report of Wesfarmers. 2018. [Online] Available Through:

<https://www.wesfarmers.com.au/docs/default-source/asx-announcements/2018-annual-

report.pdf?sfvrsn=0>

Annual report of Woolsworth, 2017 [Online] Available Through:

<https://wow2017ar.qreports.com.au/home/performance-highlights/2017-at-a-

glance.html>

9

Annual report of Woolsworth. 2018 [Online] Available Through:

<https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf>

Small Proprietory firm. 2019 [Online] Available Through:

<https://home.kpmg/au/en/home/insights/2019/04/19ru-004-proprietary-company-

threshold-changes.html>

10

<https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf>

Small Proprietory firm. 2019 [Online] Available Through:

<https://home.kpmg/au/en/home/insights/2019/04/19ru-004-proprietary-company-

threshold-changes.html>

10

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.