Corporate Financial Accounting - PDF

VerifiedAdded on 2021/06/14

|14

|2844

|14

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

RUNNING HEAD: Corporate Financial Accounting

0

JB HI FI COMPANY

Corporate Accounting

JB Hi-FI Company

Name of the Author- Sagar Pokhrel

Student id- EMV 22235

0

JB HI FI COMPANY

Corporate Accounting

JB Hi-FI Company

Name of the Author- Sagar Pokhrel

Student id- EMV 22235

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Financial Accounting

1

Table of Contents

Introduction...........................................................................................................................................2

Answer to question-1.............................................................................................................................2

Answer to question-2.............................................................................................................................3

Comparative analysis of the all three main flow of activities............................................................3

Answer to question no-3.......................................................................................................................3

Answer to question no-4.......................................................................................................................4

Answer to question no-5.......................................................................................................................4

Answer to question no-6.......................................................................................................................5

Answer to question no-7........................................................................................................................5

Explain, why this is with reason.............................................................................................................5

Answer to question no-8........................................................................................................................6

Answer to question no-9........................................................................................................................8

Income tax payment differ from the income tax payable..................................................................8

Answer to question no-10......................................................................................................................9

Answer to question no-11......................................................................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

.

1

Table of Contents

Introduction...........................................................................................................................................2

Answer to question-1.............................................................................................................................2

Answer to question-2.............................................................................................................................3

Comparative analysis of the all three main flow of activities............................................................3

Answer to question no-3.......................................................................................................................3

Answer to question no-4.......................................................................................................................4

Answer to question no-5.......................................................................................................................4

Answer to question no-6.......................................................................................................................5

Answer to question no-7........................................................................................................................5

Explain, why this is with reason.............................................................................................................5

Answer to question no-8........................................................................................................................6

Answer to question no-9........................................................................................................................8

Income tax payment differ from the income tax payable..................................................................8

Answer to question no-10......................................................................................................................9

Answer to question no-11......................................................................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

.

Corporate Financial Accounting

2

Introduction

This report emphasises upon the financial statement analysis, deferred tax payment

and the recording of the tax provisions of the JB Hi- Fi Company. With the ramified

economic changes, government has been changing the taxation rules and regulation

throughout the time to make the tax implication better and effective on the corporations. In

this report, JB Hi- Fi Company has been taken to prepare this report. This company has been

running its business on international level for selling electronic goods and services (JB HI-FI,

2017).

Answer to question-1

Analysis of the Cash flow statement

Cash flow statement is accompanied with the flow of cash in the business irrespective of the

fact whether it belongs to present year or not. The cash flow statement represents the flow of

cash in its three main activities named investing, financial, operating activities.

The non-cash items are being added in the operating activities which have increased to AUD

$ 191 million in 2017 which is AUD $ 34 million as compared to last five year data. It is

reflected that company has increased the depreciation amount and increased operating

expenses (JB HI-FI, 2017).

The cash outflow shown by company in its investing activities is AUD $ 886 million which

arise due to its cash payment to buy new machineries and assets (JB HI-FI, 2017).

2

Introduction

This report emphasises upon the financial statement analysis, deferred tax payment

and the recording of the tax provisions of the JB Hi- Fi Company. With the ramified

economic changes, government has been changing the taxation rules and regulation

throughout the time to make the tax implication better and effective on the corporations. In

this report, JB Hi- Fi Company has been taken to prepare this report. This company has been

running its business on international level for selling electronic goods and services (JB HI-FI,

2017).

Answer to question-1

Analysis of the Cash flow statement

Cash flow statement is accompanied with the flow of cash in the business irrespective of the

fact whether it belongs to present year or not. The cash flow statement represents the flow of

cash in its three main activities named investing, financial, operating activities.

The non-cash items are being added in the operating activities which have increased to AUD

$ 191 million in 2017 which is AUD $ 34 million as compared to last five year data. It is

reflected that company has increased the depreciation amount and increased operating

expenses (JB HI-FI, 2017).

The cash outflow shown by company in its investing activities is AUD $ 886 million which

arise due to its cash payment to buy new machineries and assets (JB HI-FI, 2017).

Corporate Financial Accounting

3

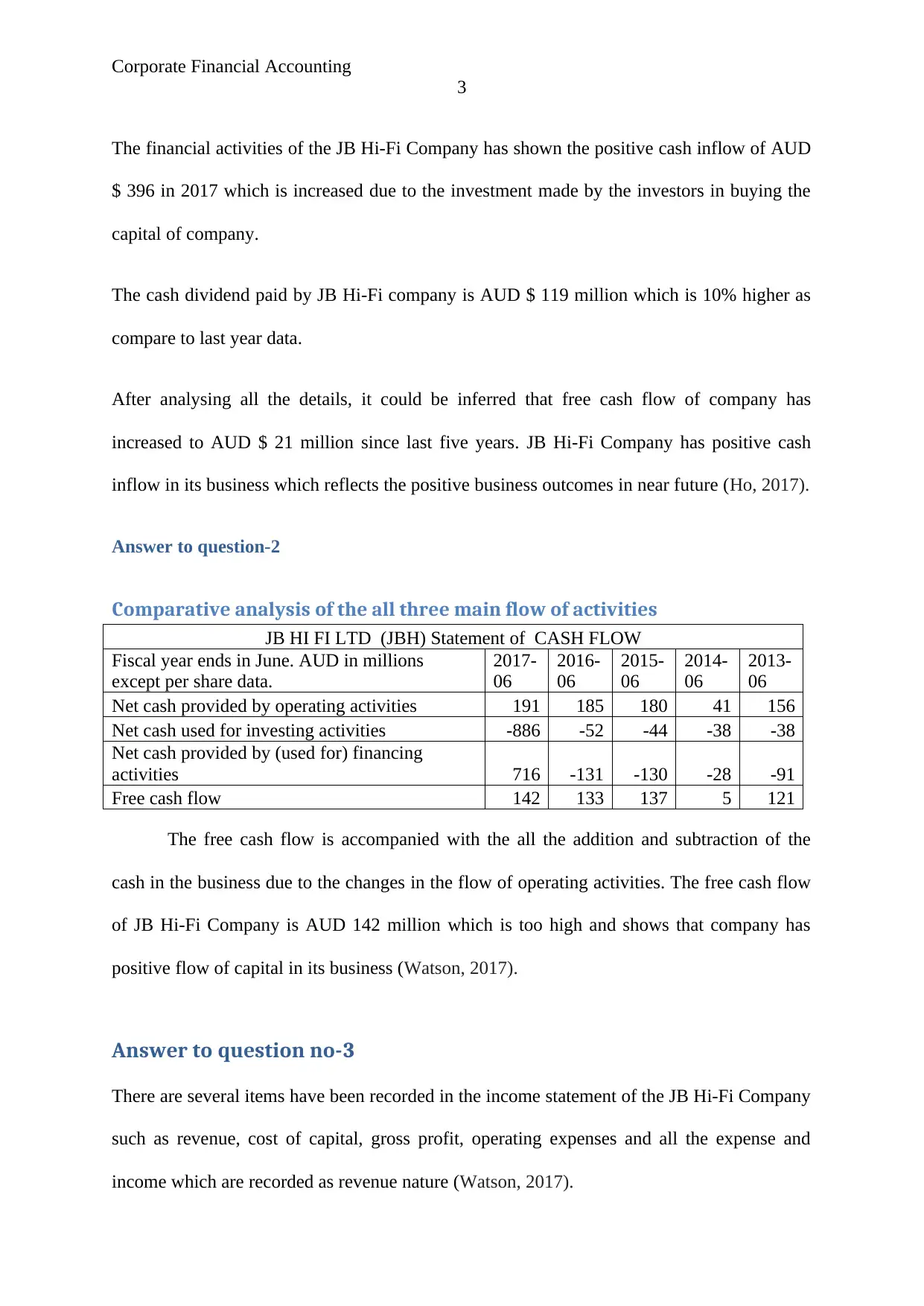

The financial activities of the JB Hi-Fi Company has shown the positive cash inflow of AUD

$ 396 in 2017 which is increased due to the investment made by the investors in buying the

capital of company.

The cash dividend paid by JB Hi-Fi company is AUD $ 119 million which is 10% higher as

compare to last year data.

After analysing all the details, it could be inferred that free cash flow of company has

increased to AUD $ 21 million since last five years. JB Hi-Fi Company has positive cash

inflow in its business which reflects the positive business outcomes in near future (Ho, 2017).

Answer to question-2

Comparative analysis of the all three main flow of activities

JB HI FI LTD (JBH) Statement of CASH FLOW

Fiscal year ends in June. AUD in millions

except per share data.

2017-

06

2016-

06

2015-

06

2014-

06

2013-

06

Net cash provided by operating activities 191 185 180 41 156

Net cash used for investing activities -886 -52 -44 -38 -38

Net cash provided by (used for) financing

activities 716 -131 -130 -28 -91

Free cash flow 142 133 137 5 121

The free cash flow is accompanied with the all the addition and subtraction of the

cash in the business due to the changes in the flow of operating activities. The free cash flow

of JB Hi-Fi Company is AUD 142 million which is too high and shows that company has

positive flow of capital in its business (Watson, 2017).

Answer to question no-3

There are several items have been recorded in the income statement of the JB Hi-Fi Company

such as revenue, cost of capital, gross profit, operating expenses and all the expense and

income which are recorded as revenue nature (Watson, 2017).

3

The financial activities of the JB Hi-Fi Company has shown the positive cash inflow of AUD

$ 396 in 2017 which is increased due to the investment made by the investors in buying the

capital of company.

The cash dividend paid by JB Hi-Fi company is AUD $ 119 million which is 10% higher as

compare to last year data.

After analysing all the details, it could be inferred that free cash flow of company has

increased to AUD $ 21 million since last five years. JB Hi-Fi Company has positive cash

inflow in its business which reflects the positive business outcomes in near future (Ho, 2017).

Answer to question-2

Comparative analysis of the all three main flow of activities

JB HI FI LTD (JBH) Statement of CASH FLOW

Fiscal year ends in June. AUD in millions

except per share data.

2017-

06

2016-

06

2015-

06

2014-

06

2013-

06

Net cash provided by operating activities 191 185 180 41 156

Net cash used for investing activities -886 -52 -44 -38 -38

Net cash provided by (used for) financing

activities 716 -131 -130 -28 -91

Free cash flow 142 133 137 5 121

The free cash flow is accompanied with the all the addition and subtraction of the

cash in the business due to the changes in the flow of operating activities. The free cash flow

of JB Hi-Fi Company is AUD 142 million which is too high and shows that company has

positive flow of capital in its business (Watson, 2017).

Answer to question no-3

There are several items have been recorded in the income statement of the JB Hi-Fi Company

such as revenue, cost of capital, gross profit, operating expenses and all the expense and

income which are recorded as revenue nature (Watson, 2017).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Financial Accounting

4

JB HI FI LTD (JBH) Cash Flow Flag INCOME STATEMENT

Fiscal year ends in June. AUD in millions except per

share data.

2017

-06

2016

-06

2015

-06

2014

-06

2013

-06

Revenue 5628 3954 3652 3484 3308

Cost of revenue 4398 3089 2854 2745 2610

Gross profit 1230 865 798 739 699

Operating expenses

Sales, General and administrative 1434 1006 931 884 839

Other operating expenses -472 -361 -334 -336 -318

Total operating expenses 963 644 597 548 521

Operating income 268 221 201 191 178

Interest Expense 11 4 6 9 10

Other income (expense) 2 1 1 0 1

Income before income taxes 259 218 196 183 168

Provision for income taxes 87 66 59 54 51

The provision for the doubtful debts, provision for the tax and all the other items which

cannot be recorded in the cash are not shown the cash flow statement but adjusted in the

income statement of company (JB HI-FI, 2017).

Answer to question no-4

As per the perception of me, I have understood that only those items which are related to the

present year are recorded in the income statement of company. It is observed that cash flow

statement covers all the items recording irrespective of the fact whether it belongs to present

year or not. On the other hand, income statement shows the income and expenses related to

the present year with a view to identity the true and fair net profit of company (JB HI-FI,

2017).

Answer to question no-5

Income statement is prepared with a view to identify the actual profit of the company in the

particuarl year. It is acomapenid with the details such as as revenue, cost of capital, gross

profit, operating expenses and all the expense and income which are recorded as revenue

4

JB HI FI LTD (JBH) Cash Flow Flag INCOME STATEMENT

Fiscal year ends in June. AUD in millions except per

share data.

2017

-06

2016

-06

2015

-06

2014

-06

2013

-06

Revenue 5628 3954 3652 3484 3308

Cost of revenue 4398 3089 2854 2745 2610

Gross profit 1230 865 798 739 699

Operating expenses

Sales, General and administrative 1434 1006 931 884 839

Other operating expenses -472 -361 -334 -336 -318

Total operating expenses 963 644 597 548 521

Operating income 268 221 201 191 178

Interest Expense 11 4 6 9 10

Other income (expense) 2 1 1 0 1

Income before income taxes 259 218 196 183 168

Provision for income taxes 87 66 59 54 51

The provision for the doubtful debts, provision for the tax and all the other items which

cannot be recorded in the cash are not shown the cash flow statement but adjusted in the

income statement of company (JB HI-FI, 2017).

Answer to question no-4

As per the perception of me, I have understood that only those items which are related to the

present year are recorded in the income statement of company. It is observed that cash flow

statement covers all the items recording irrespective of the fact whether it belongs to present

year or not. On the other hand, income statement shows the income and expenses related to

the present year with a view to identity the true and fair net profit of company (JB HI-FI,

2017).

Answer to question no-5

Income statement is prepared with a view to identify the actual profit of the company in the

particuarl year. It is acomapenid with the details such as as revenue, cost of capital, gross

profit, operating expenses and all the expense and income which are recorded as revenue

Corporate Financial Accounting

5

nature. All the advance payment and outstanding payment made in the current year will be

subtracted from its heading shown in the income statement of company.

Answer to question no-6

Each and every company needs to pay tax to government. It is the amount of liabilities or tax

payment which company needs to pay as their moral responsibilities to government on their

earning. The amount of tax payment by JB Hi-Fi Company is AUD $ 86.8 million in 2016

which decreased to AUD $ 65.65 million in 2017 (JB HI-FI, 2017).

Particular(AUD $ in million) 2016 2017

Income tax expenses 86.8 65.6

However, with the increasing tax expenses, company has increased its interest expenses

which will eventually reduce the tax implication on company (JB HI-FI, 2017).

Answer to question no-7

After analysing all the details shown in the annual report of company and AASB 112 taxation

rules and regulation for the tax implication on companies, it could be inferred that the tax

payment made by company is not equal to the computed tax rate times on the accounting

profit of company.

5

nature. All the advance payment and outstanding payment made in the current year will be

subtracted from its heading shown in the income statement of company.

Answer to question no-6

Each and every company needs to pay tax to government. It is the amount of liabilities or tax

payment which company needs to pay as their moral responsibilities to government on their

earning. The amount of tax payment by JB Hi-Fi Company is AUD $ 86.8 million in 2016

which decreased to AUD $ 65.65 million in 2017 (JB HI-FI, 2017).

Particular(AUD $ in million) 2016 2017

Income tax expenses 86.8 65.6

However, with the increasing tax expenses, company has increased its interest expenses

which will eventually reduce the tax implication on company (JB HI-FI, 2017).

Answer to question no-7

After analysing all the details shown in the annual report of company and AASB 112 taxation

rules and regulation for the tax implication on companies, it could be inferred that the tax

payment made by company is not equal to the computed tax rate times on the accounting

profit of company.

Corporate Financial Accounting

6

Explain, why this is with reason

It is analysed that JB Hi-Fi Company has paid the income tax AUD $ 65.6 million in 2017

which includes all the tax payment such as deferred tax and current tax (Obinson, Stomberg,

and Towery, 2015).

The company’s tax rate times expenses would be Accounting income * 30% tax rates.

It would be around 259*30%.

The amount of tax should be 77.7 million.

The treatment of tax recording in the income statement varies as per the accounting

rules and regulation and AASB 112 income tax standards (Towery, 2017).

The tax payment shown in the profit and loss account is computed by using the proper

taxation rules and manual calculation is done on the basis of company’s tax rate

times’ expense and accounting rules.

There are main two reasons of the differences between the tax amount shown in the

profit and loss and manual calculation

1. Revenue and expense recorded by the accounting rules and regulations may not be

allowed as per the income tax rules and standard AASB 112.

2. The recording of the bad debts, interest charged, and deduction charged for the charity

may not be allowed by the income tax rules and standards (Brigham, and Ehrhardt,

2013).

6

Explain, why this is with reason

It is analysed that JB Hi-Fi Company has paid the income tax AUD $ 65.6 million in 2017

which includes all the tax payment such as deferred tax and current tax (Obinson, Stomberg,

and Towery, 2015).

The company’s tax rate times expenses would be Accounting income * 30% tax rates.

It would be around 259*30%.

The amount of tax should be 77.7 million.

The treatment of tax recording in the income statement varies as per the accounting

rules and regulation and AASB 112 income tax standards (Towery, 2017).

The tax payment shown in the profit and loss account is computed by using the proper

taxation rules and manual calculation is done on the basis of company’s tax rate

times’ expense and accounting rules.

There are main two reasons of the differences between the tax amount shown in the

profit and loss and manual calculation

1. Revenue and expense recorded by the accounting rules and regulations may not be

allowed as per the income tax rules and standard AASB 112.

2. The recording of the bad debts, interest charged, and deduction charged for the charity

may not be allowed by the income tax rules and standards (Brigham, and Ehrhardt,

2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Financial Accounting

7

Answer to question no-8

The deferred tax liabilities shown in the balance sheet is AUD $ 8.2 million. It is evaluated

that deferred tax liabilities is recognized and carried forward to the extent to which it could be

resonbly charged to the books of accounts of company (Watson, 2017).

The JB Hi-Fi Company has recorded the deferred tax liabilities in its balance sheet.

The treatment of the deferred tax assets and libiliteis recorded in the balance sheet of the

company (Bradley, 2017).

If company paid higher tax as per the AASB 112 in comparison with the tax computed as per

the accounting rules and standards then the same additional amount would be recorded as

deferred tax assets.

If company charges less tax as per the AASB 112 in comparison with the tax computed as per

the accounting rules and standards then the less amount would be recorded as deferred tax

liabilities (JB HI-FI, 2017).

JB Hi-Fi Company has recorded deferred tax liabilities. It shows that company has paid

higher tax to government (Ho, 2017).

Particular (AUD $ million) 2017 2016

Deferred tax liabilities 8.2 0

7

Answer to question no-8

The deferred tax liabilities shown in the balance sheet is AUD $ 8.2 million. It is evaluated

that deferred tax liabilities is recognized and carried forward to the extent to which it could be

resonbly charged to the books of accounts of company (Watson, 2017).

The JB Hi-Fi Company has recorded the deferred tax liabilities in its balance sheet.

The treatment of the deferred tax assets and libiliteis recorded in the balance sheet of the

company (Bradley, 2017).

If company paid higher tax as per the AASB 112 in comparison with the tax computed as per

the accounting rules and standards then the same additional amount would be recorded as

deferred tax assets.

If company charges less tax as per the AASB 112 in comparison with the tax computed as per

the accounting rules and standards then the less amount would be recorded as deferred tax

liabilities (JB HI-FI, 2017).

JB Hi-Fi Company has recorded deferred tax liabilities. It shows that company has paid

higher tax to government (Ho, 2017).

Particular (AUD $ million) 2017 2016

Deferred tax liabilities 8.2 0

Corporate Financial Accounting

8

Answer to question no-9

Current tax payment and current tax payable by the JB Hi-Fi Company

The current tax payable recorded in the books of accounts of company is AUD $ 4.9 million

in 2016 which have reduced and resulted to AUD $ 9 million in 2017 (JB HI-FI, 2017).

The income tax payment shown in the income statement is the amount of tax implication

which was paid by JB Hi-Fi Company on its profit as per the income tax rules and AASB 112

(Gorry, et al., 2017).

Particular(AUD $ in

million)

2016 2017

Income tax payable 4.9 9

Income tax payment differ from the income tax payable

There are several reasons for the difference between the income tax payment amount show in

the income statement of company and income tax payable shown in the liabilities side of the

balance sheet (Ladas, Negkakis, and Samara, 2017).

Nature- Income tax payment amount show in the income statement of company is of revenue

in nature. On the other hand, income tax payable shown in the liabilities side of the balance

sheet.

8

Answer to question no-9

Current tax payment and current tax payable by the JB Hi-Fi Company

The current tax payable recorded in the books of accounts of company is AUD $ 4.9 million

in 2016 which have reduced and resulted to AUD $ 9 million in 2017 (JB HI-FI, 2017).

The income tax payment shown in the income statement is the amount of tax implication

which was paid by JB Hi-Fi Company on its profit as per the income tax rules and AASB 112

(Gorry, et al., 2017).

Particular(AUD $ in

million)

2016 2017

Income tax payable 4.9 9

Income tax payment differ from the income tax payable

There are several reasons for the difference between the income tax payment amount show in

the income statement of company and income tax payable shown in the liabilities side of the

balance sheet (Ladas, Negkakis, and Samara, 2017).

Nature- Income tax payment amount show in the income statement of company is of revenue

in nature. On the other hand, income tax payable shown in the liabilities side of the balance

sheet.

Corporate Financial Accounting

9

Payment- income tax payment covers the tax payment of Company related for the present

year. On the other hand, income tax payable is recorded as cumulative taxable libiliteis of

company (Landoni, and Zeldes, 2017).

Answer to question no-10

The cash flow statement covers all the inflow and outflow of cash in the present year

irrespective of the fact that whether it belongs to the current year or not.

The cash flow statement shown the income tax payment of $98.5 million which covers entire

tax payment in present year irrespective of the fact that whether it belongs to the current year

or not (Kim, 2017).

The recorded income tax in the income statement is related to the current year tax implication

which is charged against profit to identify the true and fair of the profit earned by JB Hi-Fi

Company (Ladas, Negkakis, and Samara2017).

Reason

The main reason of the difference between the amount shown in the cash flow statement for

the tax and the amount charged in the income statement is related to the current year tax

implication is based on the recording of the nature of transaction in the separate books of

accounts for which they are prepared.

Answer to question no-11

Treatment of the tax amount recorded in the books of account of JB HI Fi Company

9

Payment- income tax payment covers the tax payment of Company related for the present

year. On the other hand, income tax payable is recorded as cumulative taxable libiliteis of

company (Landoni, and Zeldes, 2017).

Answer to question no-10

The cash flow statement covers all the inflow and outflow of cash in the present year

irrespective of the fact that whether it belongs to the current year or not.

The cash flow statement shown the income tax payment of $98.5 million which covers entire

tax payment in present year irrespective of the fact that whether it belongs to the current year

or not (Kim, 2017).

The recorded income tax in the income statement is related to the current year tax implication

which is charged against profit to identify the true and fair of the profit earned by JB Hi-Fi

Company (Ladas, Negkakis, and Samara2017).

Reason

The main reason of the difference between the amount shown in the cash flow statement for

the tax and the amount charged in the income statement is related to the current year tax

implication is based on the recording of the nature of transaction in the separate books of

accounts for which they are prepared.

Answer to question no-11

Treatment of the tax amount recorded in the books of account of JB HI Fi Company

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Financial Accounting

10

Interesting thing

The tax payment shown in the income statement may be changed with the changes in the

taxation rules and standards (Morris, 2017).

It may be hard for the organization to determine the right amount of cash flow for the income

tax which company need to make in the assessment year.

Surprising thing

The surprising thing about the recording of the tax in the books of accounts is related to its

booking entries. JB Hi-Fi Company cannot have deferred tax assets and deferred tax

liabilities in the books of accounts at the same time. It may result to conflict as per the

accounting rules if recorded (Larson, Lewis, and Spilker, 2017).

Difficulty in recorded the entire tax amount

The main difficulty in the recording of the entire tax arise when company has high amount of

tax payment and at the same time company needs to set off its deferred tax liabilities in its

books of accounts (Eberhartinger, Genest, and Lee, 2017).

Conclusion

After analysing all the details and deferred tax recording of the JB Hi-Fi Company, it

could be inferred that company has complied with the all the domestic and international rules

for the tax payment. It is inferred that if in case accounting rules and standards conflict with

the rules and regulation of the AASB 112 then in that case the computation of the tax

implication will be made as per the income tax rules and regulation.

10

Interesting thing

The tax payment shown in the income statement may be changed with the changes in the

taxation rules and standards (Morris, 2017).

It may be hard for the organization to determine the right amount of cash flow for the income

tax which company need to make in the assessment year.

Surprising thing

The surprising thing about the recording of the tax in the books of accounts is related to its

booking entries. JB Hi-Fi Company cannot have deferred tax assets and deferred tax

liabilities in the books of accounts at the same time. It may result to conflict as per the

accounting rules if recorded (Larson, Lewis, and Spilker, 2017).

Difficulty in recorded the entire tax amount

The main difficulty in the recording of the entire tax arise when company has high amount of

tax payment and at the same time company needs to set off its deferred tax liabilities in its

books of accounts (Eberhartinger, Genest, and Lee, 2017).

Conclusion

After analysing all the details and deferred tax recording of the JB Hi-Fi Company, it

could be inferred that company has complied with the all the domestic and international rules

for the tax payment. It is inferred that if in case accounting rules and standards conflict with

the rules and regulation of the AASB 112 then in that case the computation of the tax

implication will be made as per the income tax rules and regulation.

Corporate Financial Accounting

11

11

Corporate Financial Accounting

12

References

Bradley, S., 2017. Inattention to Deferred Increases in Tax Bases: How Michigan Home

Buyers Are Paying for Assessment Limits. Review of Economics and Statistics, 99(1),

pp.53-66.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Eberhartinger, E., Genest, N. and Lee, S., 2017. Practitioners’ Judgment and Deferred

Tax Disclosure: A Case for Materiality.

Gorry, A., Hassett, K.A., Hubbard, R.G. and Mathur, A., 2017. The response of deferred

executive compensation to changes in tax rates. Journal of Public Economics, 151, pp.28-

40.

Ho, A.T., 2017. Tax-deferred saving accounts: Heterogeneity and policy

reforms. European Economic Review, 97, pp.26-41.

JB HI-FI, 2017., Annual report., [Online]., Available from

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_JBH_2016.pdf

[Accessed 14th May, 2018].

Kim, J.H., 2017. What Really Determines the Information Content of Tax Expense and

Deferred Tax?. 회회회회회, 42(2), pp.1-44.

Ladas, A.C., Negkakis, C.I. and Samara, A.D., 2017. Accounting quality deferred tax and

risk in the banking industry. International Journal of Banking, Accounting and

Finance, 8(1), pp.1-19.

Ladas, A.C., Negkakis, C.I. and Samara, A.D., 2017. Accounting quality deferred tax and

risk in the banking industry. International Journal of Banking, Accounting and

Finance, 8(1), pp.1-19.

Landoni, M. and Zeldes, S.P., 2017. Should the government be paying investment fees on

$3 trillion of tax-deferred retirement assets?

12

References

Bradley, S., 2017. Inattention to Deferred Increases in Tax Bases: How Michigan Home

Buyers Are Paying for Assessment Limits. Review of Economics and Statistics, 99(1),

pp.53-66.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Eberhartinger, E., Genest, N. and Lee, S., 2017. Practitioners’ Judgment and Deferred

Tax Disclosure: A Case for Materiality.

Gorry, A., Hassett, K.A., Hubbard, R.G. and Mathur, A., 2017. The response of deferred

executive compensation to changes in tax rates. Journal of Public Economics, 151, pp.28-

40.

Ho, A.T., 2017. Tax-deferred saving accounts: Heterogeneity and policy

reforms. European Economic Review, 97, pp.26-41.

JB HI-FI, 2017., Annual report., [Online]., Available from

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_JBH_2016.pdf

[Accessed 14th May, 2018].

Kim, J.H., 2017. What Really Determines the Information Content of Tax Expense and

Deferred Tax?. 회회회회회, 42(2), pp.1-44.

Ladas, A.C., Negkakis, C.I. and Samara, A.D., 2017. Accounting quality deferred tax and

risk in the banking industry. International Journal of Banking, Accounting and

Finance, 8(1), pp.1-19.

Ladas, A.C., Negkakis, C.I. and Samara, A.D., 2017. Accounting quality deferred tax and

risk in the banking industry. International Journal of Banking, Accounting and

Finance, 8(1), pp.1-19.

Landoni, M. and Zeldes, S.P., 2017. Should the government be paying investment fees on

$3 trillion of tax-deferred retirement assets?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Financial Accounting

13

Larson, M.P., Lewis, T.K. and Spilker, B.C., 2017. A Case Integrating Financial and Tax

Accounting Using the Balance Sheet Approach to Account for Income Taxes. Issues in

Accounting Education, 32(4), pp.41-49.

Morris, J.L., 2017. Classification of Deferred Tax Assets and Deferred Tax Liabilities:

An Evaluation of FASB's Attempt at Standards Simplication. Journal of Accounting and

Finance, 17(8), pp.198-208.

Robinson, L.A., Stomberg, B. and Towery, E.M., 2015. One size does not fit all: How the

uniform rules of FIN 48 affect the relevance of income tax accounting. The Accounting

Review, 91(4), pp.1195-1217.

Towery, E.M., 2017. Unintended consequences of linking tax return disclosures to

financial reporting for income taxes: Evidence from Schedule UTP. The Accounting

Review, 92(5), pp.201-226.

Watson, L. (2017). Discussion of'Does the Deferred Tax Asset Valuation Allowance

Signal Firm Creditworthiness?'.

13

Larson, M.P., Lewis, T.K. and Spilker, B.C., 2017. A Case Integrating Financial and Tax

Accounting Using the Balance Sheet Approach to Account for Income Taxes. Issues in

Accounting Education, 32(4), pp.41-49.

Morris, J.L., 2017. Classification of Deferred Tax Assets and Deferred Tax Liabilities:

An Evaluation of FASB's Attempt at Standards Simplication. Journal of Accounting and

Finance, 17(8), pp.198-208.

Robinson, L.A., Stomberg, B. and Towery, E.M., 2015. One size does not fit all: How the

uniform rules of FIN 48 affect the relevance of income tax accounting. The Accounting

Review, 91(4), pp.1195-1217.

Towery, E.M., 2017. Unintended consequences of linking tax return disclosures to

financial reporting for income taxes: Evidence from Schedule UTP. The Accounting

Review, 92(5), pp.201-226.

Watson, L. (2017). Discussion of'Does the Deferred Tax Asset Valuation Allowance

Signal Firm Creditworthiness?'.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.