Corporate Financial Management: Portfolio Analysis and M&A Assessment

VerifiedAdded on 2020/07/23

|19

|2973

|56

Report

AI Summary

This report provides an in-depth analysis of corporate financial management, focusing on portfolio analysis and a case study on Bayer's acquisition of Monsanto. Part A of the report calculates and compares monthly logarithmic returns of two portfolios: one constructed randomly and the other using technical analysis. Statistical methods, including independent sample t-tests, are employed to assess the significance of the return differences. The findings suggest that portfolios created through technical analysis generally outperform random portfolios. Furthermore, the report critically evaluates the findings in the context of the Weak Form of Market Efficiency (WFME) and random walk theory. Part B assesses the financial implications of Bayer's support for the Monsanto acquisition, considering capital structure, cost of capital, and shareholder wealth maximization. The analysis examines the impact of debt financing on Bayer's financial position and provides recommendations based on financial literature and debt-equity ratios. The report concludes with a discussion on the importance of strategic financial decisions in corporate finance.

Corporate Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

a. Calculating monthly logarithmic returns of the portfolio that include equally weighted 5

random companies.......................................................................................................................3

b. Creating an equally weighted portfolio by doing technical analysis and assessing monthly

returns..........................................................................................................................................5

c. Hypothesis framing..................................................................................................................6

d. Testing monthly logarithmic returns of both the portfolios by taking into account

independent sample t- test.........................................................................................................13

e. Discussion of findings derived through statistical evaluation...............................................14

f. Critically evaluating findings in the empirical study on WFME and random walk theory. . .14

PART B.........................................................................................................................................14

Assessing whether Bayer’s should support the deal pertaining to Monsanto’s acquisition......14

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

a. Calculating monthly logarithmic returns of the portfolio that include equally weighted 5

random companies.......................................................................................................................3

b. Creating an equally weighted portfolio by doing technical analysis and assessing monthly

returns..........................................................................................................................................5

c. Hypothesis framing..................................................................................................................6

d. Testing monthly logarithmic returns of both the portfolios by taking into account

independent sample t- test.........................................................................................................13

e. Discussion of findings derived through statistical evaluation...............................................14

f. Critically evaluating findings in the empirical study on WFME and random walk theory. . .14

PART B.........................................................................................................................................14

Assessing whether Bayer’s should support the deal pertaining to Monsanto’s acquisition......14

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

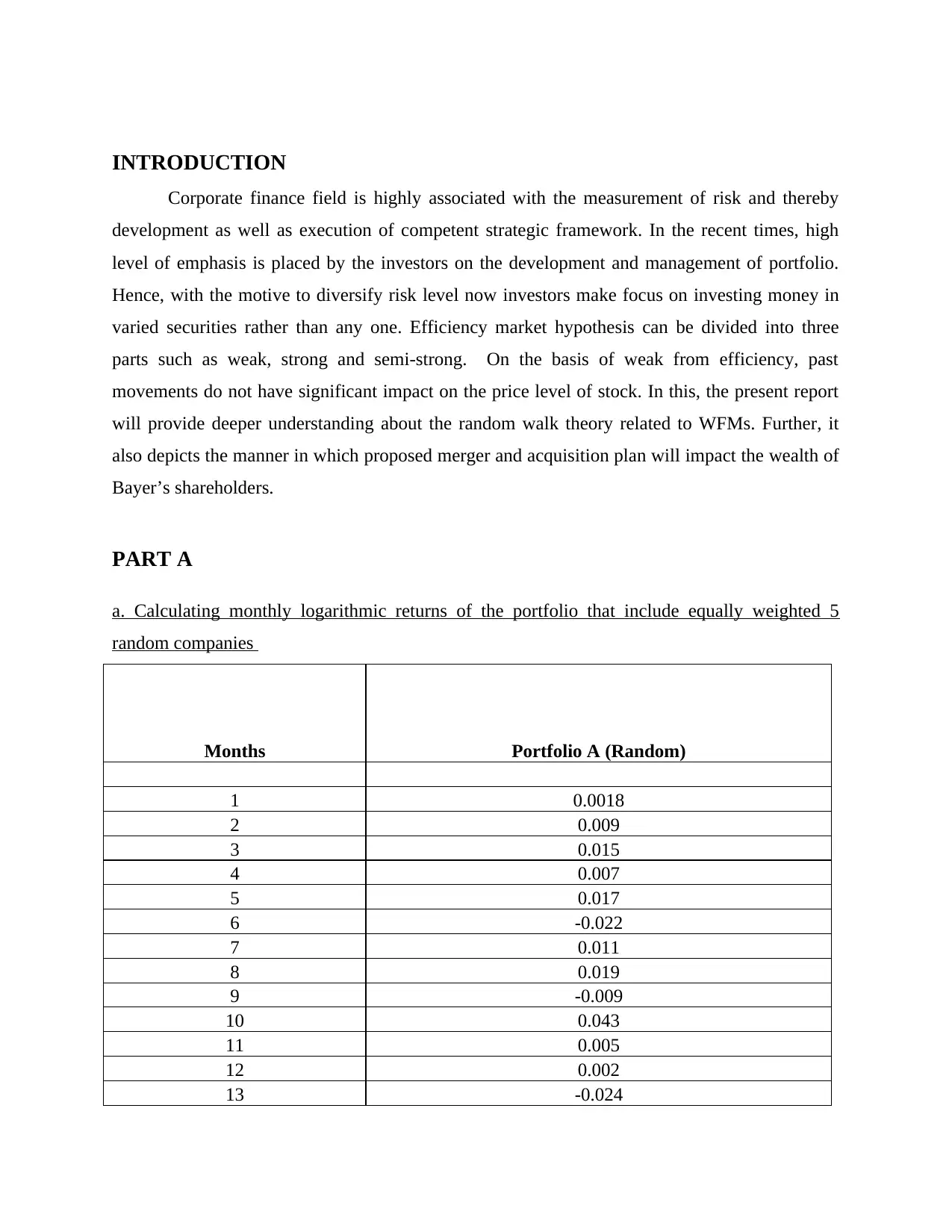

INTRODUCTION

Corporate finance field is highly associated with the measurement of risk and thereby

development as well as execution of competent strategic framework. In the recent times, high

level of emphasis is placed by the investors on the development and management of portfolio.

Hence, with the motive to diversify risk level now investors make focus on investing money in

varied securities rather than any one. Efficiency market hypothesis can be divided into three

parts such as weak, strong and semi-strong. On the basis of weak from efficiency, past

movements do not have significant impact on the price level of stock. In this, the present report

will provide deeper understanding about the random walk theory related to WFMs. Further, it

also depicts the manner in which proposed merger and acquisition plan will impact the wealth of

Bayer’s shareholders.

PART A

a. Calculating monthly logarithmic returns of the portfolio that include equally weighted 5

random companies

Months Portfolio A (Random)

1 0.0018

2 0.009

3 0.015

4 0.007

5 0.017

6 -0.022

7 0.011

8 0.019

9 -0.009

10 0.043

11 0.005

12 0.002

13 -0.024

Corporate finance field is highly associated with the measurement of risk and thereby

development as well as execution of competent strategic framework. In the recent times, high

level of emphasis is placed by the investors on the development and management of portfolio.

Hence, with the motive to diversify risk level now investors make focus on investing money in

varied securities rather than any one. Efficiency market hypothesis can be divided into three

parts such as weak, strong and semi-strong. On the basis of weak from efficiency, past

movements do not have significant impact on the price level of stock. In this, the present report

will provide deeper understanding about the random walk theory related to WFMs. Further, it

also depicts the manner in which proposed merger and acquisition plan will impact the wealth of

Bayer’s shareholders.

PART A

a. Calculating monthly logarithmic returns of the portfolio that include equally weighted 5

random companies

Months Portfolio A (Random)

1 0.0018

2 0.009

3 0.015

4 0.007

5 0.017

6 -0.022

7 0.011

8 0.019

9 -0.009

10 0.043

11 0.005

12 0.002

13 -0.024

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

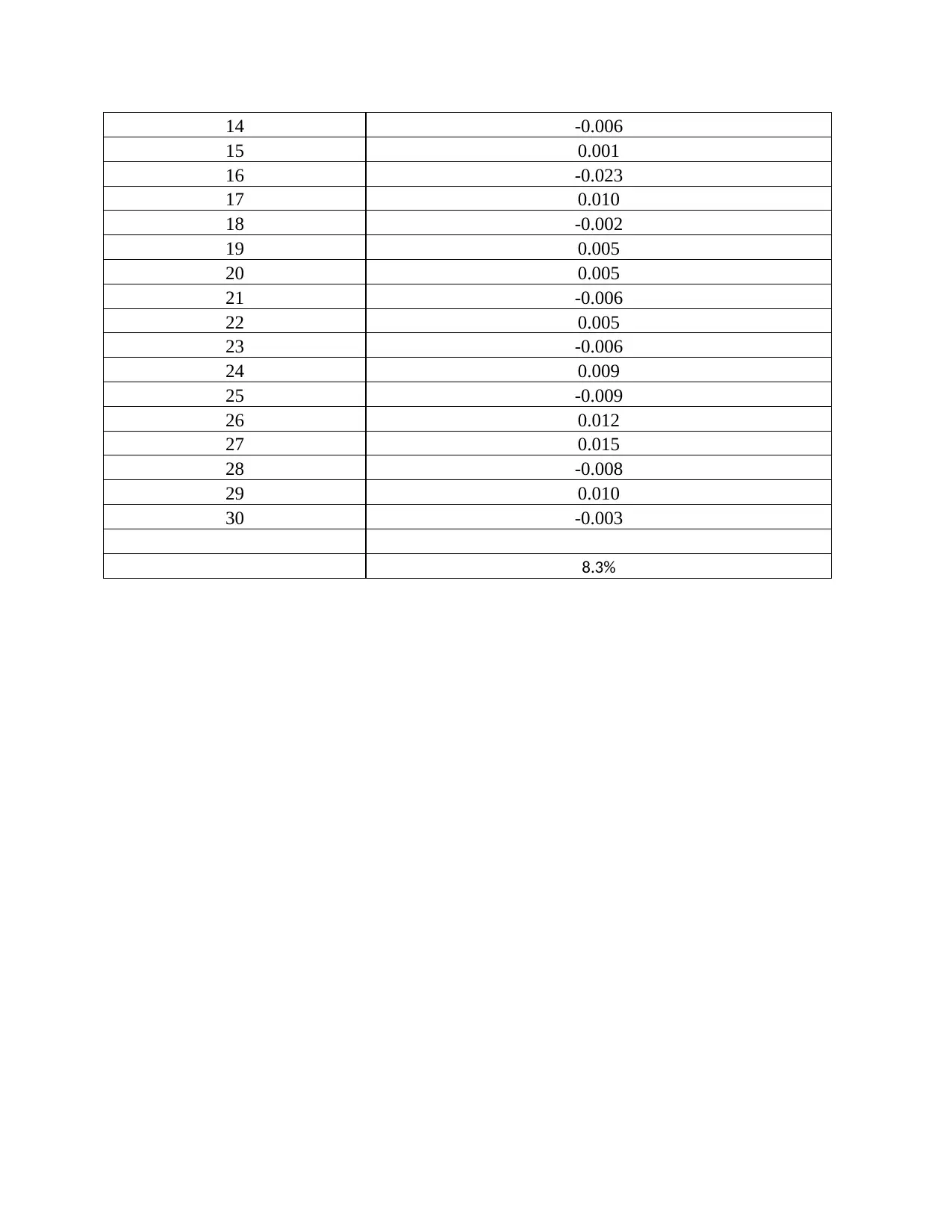

14 -0.006

15 0.001

16 -0.023

17 0.010

18 -0.002

19 0.005

20 0.005

21 -0.006

22 0.005

23 -0.006

24 0.009

25 -0.009

26 0.012

27 0.015

28 -0.008

29 0.010

30 -0.003

8.3%

15 0.001

16 -0.023

17 0.010

18 -0.002

19 0.005

20 0.005

21 -0.006

22 0.005

23 -0.006

24 0.009

25 -0.009

26 0.012

27 0.015

28 -0.008

29 0.010

30 -0.003

8.3%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

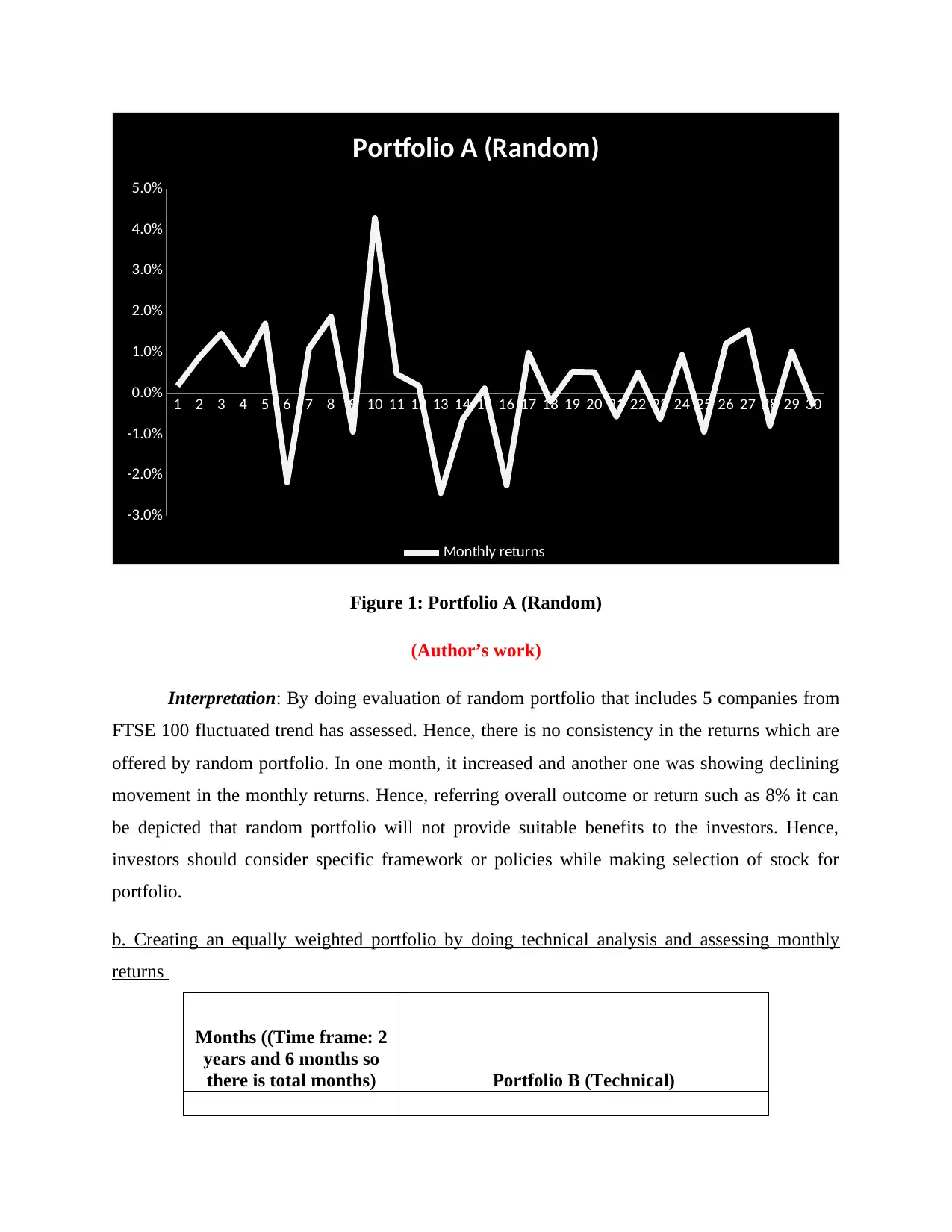

Portfolio A (Random)

Monthly returns

Figure 1: Portfolio A (Random)

(Author’s work)

Interpretation: By doing evaluation of random portfolio that includes 5 companies from

FTSE 100 fluctuated trend has assessed. Hence, there is no consistency in the returns which are

offered by random portfolio. In one month, it increased and another one was showing declining

movement in the monthly returns. Hence, referring overall outcome or return such as 8% it can

be depicted that random portfolio will not provide suitable benefits to the investors. Hence,

investors should consider specific framework or policies while making selection of stock for

portfolio.

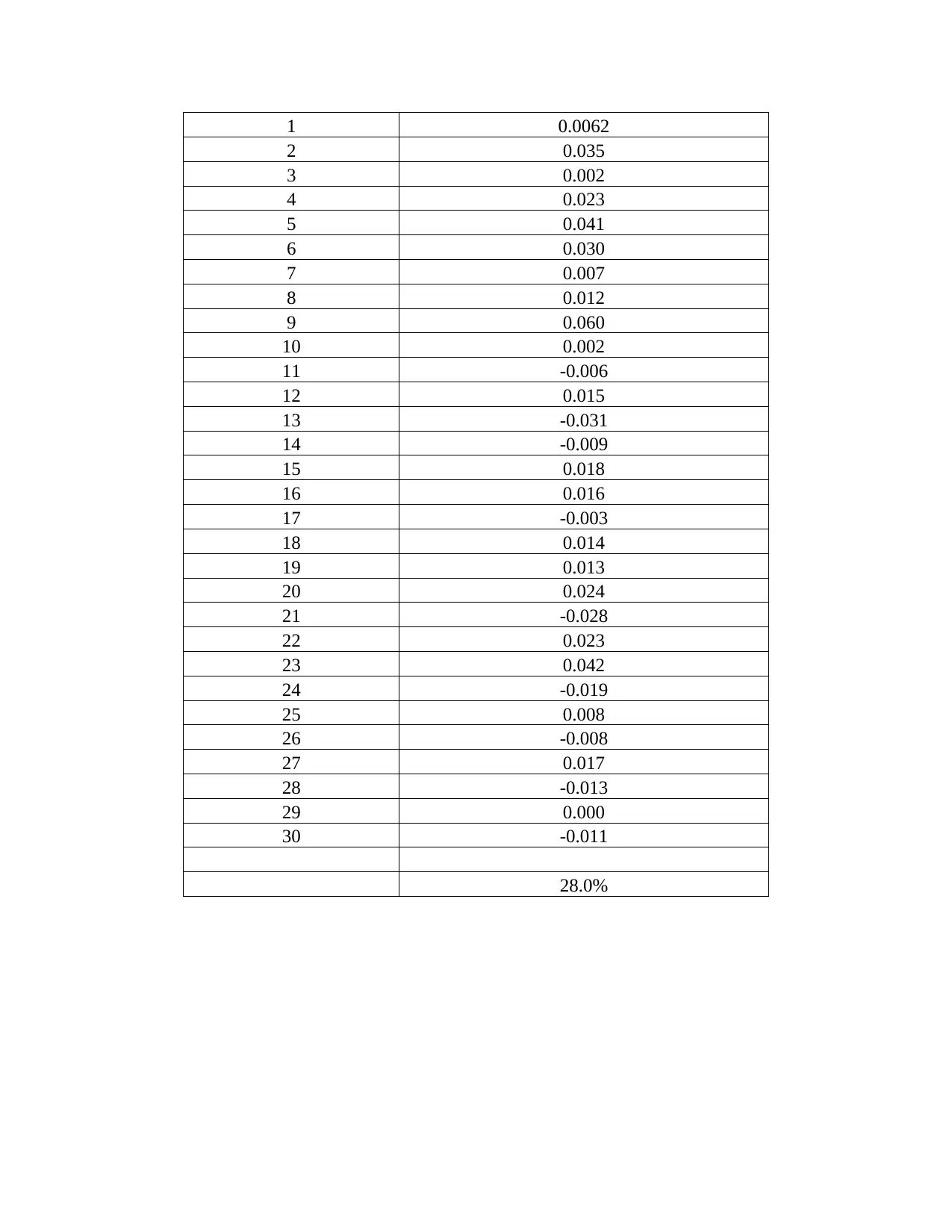

b. Creating an equally weighted portfolio by doing technical analysis and assessing monthly

returns

Months ((Time frame: 2

years and 6 months so

there is total months) Portfolio B (Technical)

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Portfolio A (Random)

Monthly returns

Figure 1: Portfolio A (Random)

(Author’s work)

Interpretation: By doing evaluation of random portfolio that includes 5 companies from

FTSE 100 fluctuated trend has assessed. Hence, there is no consistency in the returns which are

offered by random portfolio. In one month, it increased and another one was showing declining

movement in the monthly returns. Hence, referring overall outcome or return such as 8% it can

be depicted that random portfolio will not provide suitable benefits to the investors. Hence,

investors should consider specific framework or policies while making selection of stock for

portfolio.

b. Creating an equally weighted portfolio by doing technical analysis and assessing monthly

returns

Months ((Time frame: 2

years and 6 months so

there is total months) Portfolio B (Technical)

1 0.0062

2 0.035

3 0.002

4 0.023

5 0.041

6 0.030

7 0.007

8 0.012

9 0.060

10 0.002

11 -0.006

12 0.015

13 -0.031

14 -0.009

15 0.018

16 0.016

17 -0.003

18 0.014

19 0.013

20 0.024

21 -0.028

22 0.023

23 0.042

24 -0.019

25 0.008

26 -0.008

27 0.017

28 -0.013

29 0.000

30 -0.011

28.0%

2 0.035

3 0.002

4 0.023

5 0.041

6 0.030

7 0.007

8 0.012

9 0.060

10 0.002

11 -0.006

12 0.015

13 -0.031

14 -0.009

15 0.018

16 0.016

17 -0.003

18 0.014

19 0.013

20 0.024

21 -0.028

22 0.023

23 0.042

24 -0.019

25 0.008

26 -0.008

27 0.017

28 -0.013

29 0.000

30 -0.011

28.0%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1

3

5

7

9

11

13

15

17

19

21

23

25

27

29

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Portfolio B (Technical)

Monthly returns

period in months

2 years and 6 months time frame

in %

Figure 2: Portfolio B (Technical)

(Author’s work)

Interpretation: The above depicted line chart shows increasing returns pertaining to the

securities included in portfolio. Hence, such portfolio is created considering technical analysis

which in turn clearly reflects the companies which will offer high return. Considering the

increasing trend of return most of the times, out of 30 months, it can be said that portfolio created

through the means of technical analysis considered as highly viable over others.

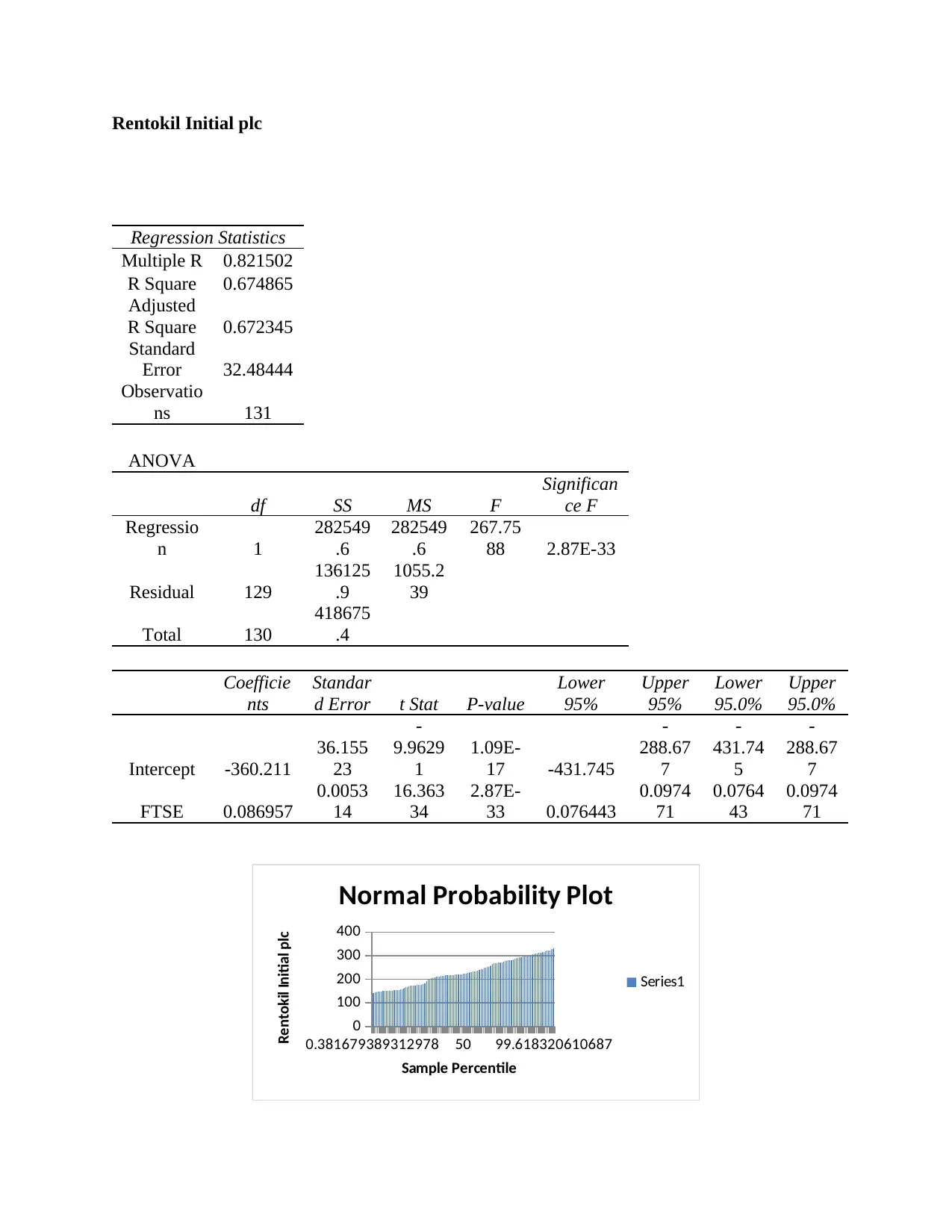

c. Hypothesis framing

Regression analysis

NMC Health Plc

Regression Statistics

Multiple R 0.82218

R Square 0.67598

Adjusted R

Square 0.673468

Standard

Error 478.0934

Observatio

ns 131

3

5

7

9

11

13

15

17

19

21

23

25

27

29

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Portfolio B (Technical)

Monthly returns

period in months

2 years and 6 months time frame

in %

Figure 2: Portfolio B (Technical)

(Author’s work)

Interpretation: The above depicted line chart shows increasing returns pertaining to the

securities included in portfolio. Hence, such portfolio is created considering technical analysis

which in turn clearly reflects the companies which will offer high return. Considering the

increasing trend of return most of the times, out of 30 months, it can be said that portfolio created

through the means of technical analysis considered as highly viable over others.

c. Hypothesis framing

Regression analysis

NMC Health Plc

Regression Statistics

Multiple R 0.82218

R Square 0.67598

Adjusted R

Square 0.673468

Standard

Error 478.0934

Observatio

ns 131

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ANOVA

df SS MS F

Significan

ce F

Regression 1

6151446

4

6151446

4

269.12

36 2.3E-33

Residual 129

2948595

4

228573.

3

Total 130

9100041

9

Coefficien

ts

Standar

d Error t Stat P-value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -6912.32

532.118

6

-

12.9902

3.44E-

25 -7965.13

-

5859.5073

18

-

7965.1

3

-

5859.5

1

FTSE 1.283058

0.07821

1

16.4049

9

2.3E-

33 1.128315

1.4378017

5

1.1283

15

1.4378

02

0.381679389312978 50 99.618320610687

0

1000

2000

3000

4000

Normal Probability Plot

Series1

Sample Percentile

NMC Health Plc

5500 6000 6500 7000 7500 8000

-1500

-1000

-500

0

500

1000

1500

FTSE Residual Plot

FTSE

Residuals

df SS MS F

Significan

ce F

Regression 1

6151446

4

6151446

4

269.12

36 2.3E-33

Residual 129

2948595

4

228573.

3

Total 130

9100041

9

Coefficien

ts

Standar

d Error t Stat P-value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -6912.32

532.118

6

-

12.9902

3.44E-

25 -7965.13

-

5859.5073

18

-

7965.1

3

-

5859.5

1

FTSE 1.283058

0.07821

1

16.4049

9

2.3E-

33 1.128315

1.4378017

5

1.1283

15

1.4378

02

0.381679389312978 50 99.618320610687

0

1000

2000

3000

4000

Normal Probability Plot

Series1

Sample Percentile

NMC Health Plc

5500 6000 6500 7000 7500 8000

-1500

-1000

-500

0

500

1000

1500

FTSE Residual Plot

FTSE

Residuals

Rentokil Initial plc

Regression Statistics

Multiple R 0.821502

R Square 0.674865

Adjusted

R Square 0.672345

Standard

Error 32.48444

Observatio

ns 131

ANOVA

df SS MS F

Significan

ce F

Regressio

n 1

282549

.6

282549

.6

267.75

88 2.87E-33

Residual 129

136125

.9

1055.2

39

Total 130

418675

.4

Coefficie

nts

Standar

d Error t Stat P-value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -360.211

36.155

23

-

9.9629

1

1.09E-

17 -431.745

-

288.67

7

-

431.74

5

-

288.67

7

FTSE 0.086957

0.0053

14

16.363

34

2.87E-

33 0.076443

0.0974

71

0.0764

43

0.0974

71

0.381679389312978 50 99.618320610687

0

100

200

300

400

Normal Probability Plot

Series1

Sample Percentile

Rentokil Initial plc

Regression Statistics

Multiple R 0.821502

R Square 0.674865

Adjusted

R Square 0.672345

Standard

Error 32.48444

Observatio

ns 131

ANOVA

df SS MS F

Significan

ce F

Regressio

n 1

282549

.6

282549

.6

267.75

88 2.87E-33

Residual 129

136125

.9

1055.2

39

Total 130

418675

.4

Coefficie

nts

Standar

d Error t Stat P-value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -360.211

36.155

23

-

9.9629

1

1.09E-

17 -431.745

-

288.67

7

-

431.74

5

-

288.67

7

FTSE 0.086957

0.0053

14

16.363

34

2.87E-

33 0.076443

0.0974

71

0.0764

43

0.0974

71

0.381679389312978 50 99.618320610687

0

100

200

300

400

Normal Probability Plot

Series1

Sample Percentile

Rentokil Initial plc

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5500 6000 6500 7000 7500 8000

-100

-50

0

50

100

FTSE Residual Plot

FTSE

Residuals

Intertek Group plc

Regression Statistics

Multiple R 0.789156

R Square 0.622767

Adjusted

R Square 0.619842

Standard

Error 552.5551

Observati

ons 131

ANOVA

df SS MS F

Significan

ce F

Regressio

n 1

650213

85

650213

85

212.96

34 4.35E-29

Residual 129

393859

10

305317.

1

Total 130

1.04E+

08

Coefficie

nts

Standar

d Error t Stat P-value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -5157.66 614.994

5

-

8.38651

7.52E-

14

-6374.44 -

3940.8

-

6374.4

-

3940.8

-100

-50

0

50

100

FTSE Residual Plot

FTSE

Residuals

Intertek Group plc

Regression Statistics

Multiple R 0.789156

R Square 0.622767

Adjusted

R Square 0.619842

Standard

Error 552.5551

Observati

ons 131

ANOVA

df SS MS F

Significan

ce F

Regressio

n 1

650213

85

650213

85

212.96

34 4.35E-29

Residual 129

393859

10

305317.

1

Total 130

1.04E+

08

Coefficie

nts

Standar

d Error t Stat P-value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -5157.66 614.994

5

-

8.38651

7.52E-

14

-6374.44 -

3940.8

-

6374.4

-

3940.8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8 4 8

FTSE 1.319125

0.09039

3

14.5932

7

4.35E-

29 1.140281

1.4979

69

1.1402

81

1.4979

69

0.381679389312978 50 99.618320610687

0

1000

2000

3000

4000

5000

6000

Normal Probability Plot

Series1

Sample Percentile

Intertek Group plc

5500 6000 6500 7000 7500 8000

-2000

-1500

-1000

-500

0

500

1000

1500

FTSE Residual Plot

FTSE

Residuals

DCC Plc

Regression Statistics

Multiple R

0.6171

37

R Square

0.3808

58

Adjusted R

Square

0.3760

58

Standard

Error

577.67

64

Observation

s 131

FTSE 1.319125

0.09039

3

14.5932

7

4.35E-

29 1.140281

1.4979

69

1.1402

81

1.4979

69

0.381679389312978 50 99.618320610687

0

1000

2000

3000

4000

5000

6000

Normal Probability Plot

Series1

Sample Percentile

Intertek Group plc

5500 6000 6500 7000 7500 8000

-2000

-1500

-1000

-500

0

500

1000

1500

FTSE Residual Plot

FTSE

Residuals

DCC Plc

Regression Statistics

Multiple R

0.6171

37

R Square

0.3808

58

Adjusted R

Square

0.3760

58

Standard

Error

577.67

64

Observation

s 131

ANOVA

df SS MS F

Significa

nce F

Regression 1 26480816

26480

816

79.35

277 4.18E-15

Residual 129 43048597

33371

0.1

Total 130 69529413

Coeffici

ents

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

743.19

45 642.9546

1.1559

05

0.249

856 -528.907

2015.2

96

-

528.907

2015.29

6

FTSE

0.8418

28 0.094502

8.9080

17

4.18E

-15 0.654853

1.0288

03

0.65485

3

1.02880

3

0

0.2

0.4

0.6

0.8

1

1.2

Normal Probability Plot

Series1

Sample Percentile

DCC

5500 6000 6500 7000 7500 8000

0

5

10

15

FTSE Residual Plot

FTSE

Residuals

Fresnillo Plc

df SS MS F

Significa

nce F

Regression 1 26480816

26480

816

79.35

277 4.18E-15

Residual 129 43048597

33371

0.1

Total 130 69529413

Coeffici

ents

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

743.19

45 642.9546

1.1559

05

0.249

856 -528.907

2015.2

96

-

528.907

2015.29

6

FTSE

0.8418

28 0.094502

8.9080

17

4.18E

-15 0.654853

1.0288

03

0.65485

3

1.02880

3

0

0.2

0.4

0.6

0.8

1

1.2

Normal Probability Plot

Series1

Sample Percentile

DCC

5500 6000 6500 7000 7500 8000

0

5

10

15

FTSE Residual Plot

FTSE

Residuals

Fresnillo Plc

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Regression Statistics

Multiple R 0.253018

R Square 0.064018

Adjusted

R Square 0.056762

Standard

Error 328.2137

Observatio

ns 131

ANOVA

df SS MS F

Significan

ce F

Regressio

n 1

950466.

3

950466

.3

8.8231

45 0.003548

Residual 129

138964

23

107724

.2

Total 130

148468

90

Coefficie

nts

Standar

d Error t Stat P-value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 208.5889

365.302

2

0.5710

04

0.5689

91 -514.17

931.34

83

-

514.17

931.34

83

FTSE 0.159487

0.05369

3

2.9703

78

0.0035

48 0.053255

0.2657

19

0.0532

55

0.2657

19

0

0.2

0.4

0.6

0.8

1

1.2

Normal Probability Plot

Series1

Sample Percentile

FRES

Multiple R 0.253018

R Square 0.064018

Adjusted

R Square 0.056762

Standard

Error 328.2137

Observatio

ns 131

ANOVA

df SS MS F

Significan

ce F

Regressio

n 1

950466.

3

950466

.3

8.8231

45 0.003548

Residual 129

138964

23

107724

.2

Total 130

148468

90

Coefficie

nts

Standar

d Error t Stat P-value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 208.5889

365.302

2

0.5710

04

0.5689

91 -514.17

931.34

83

-

514.17

931.34

83

FTSE 0.159487

0.05369

3

2.9703

78

0.0035

48 0.053255

0.2657

19

0.0532

55

0.2657

19

0

0.2

0.4

0.6

0.8

1

1.2

Normal Probability Plot

Series1

Sample Percentile

FRES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5500 6000 6500 7000 7500 8000

0

5

10

15

FTSE Residual Plot

FTSE

Residuals

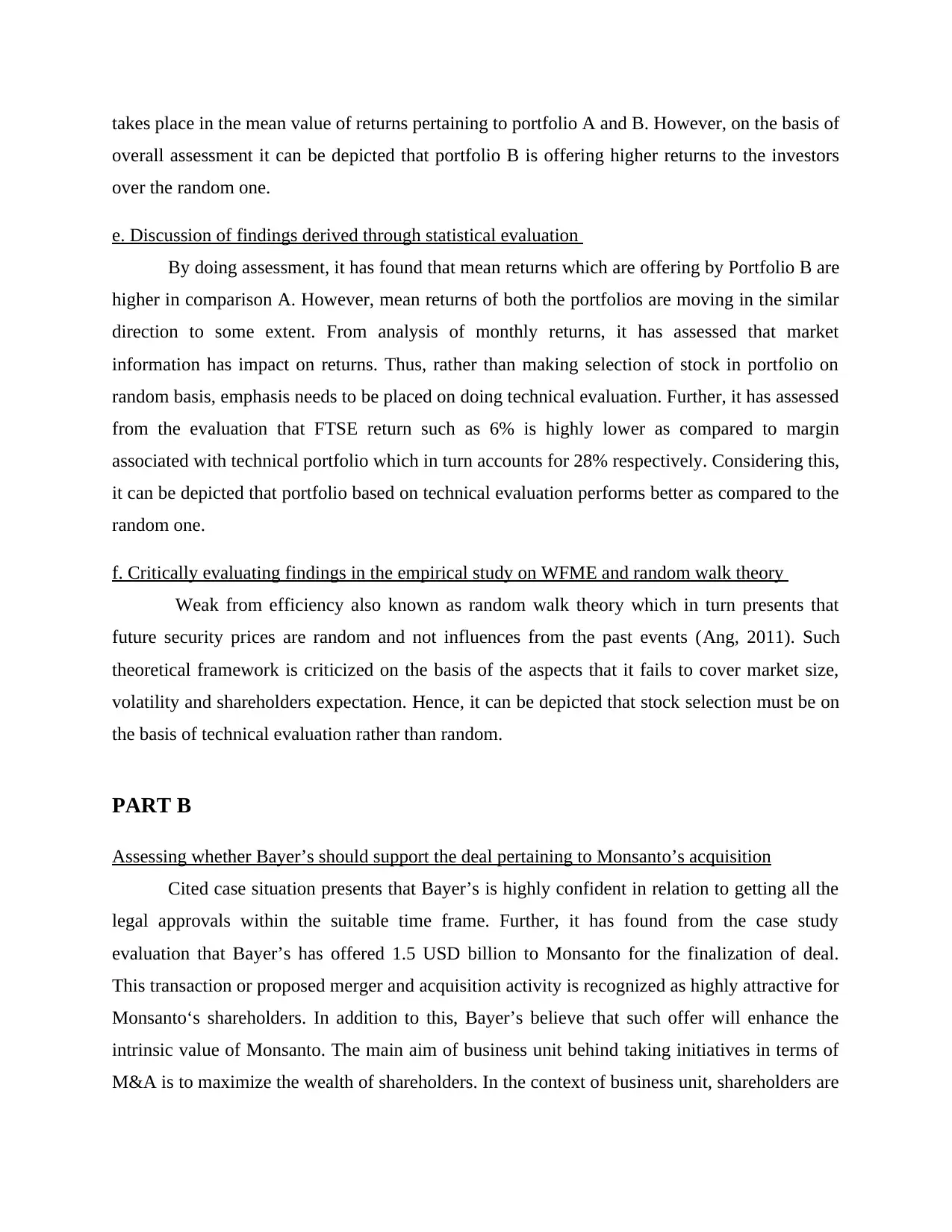

d. Testing monthly logarithmic returns of both the portfolios by taking into account independent

sample t- test

Hypothesis

H0 (Null hypothesis): There is no significant mean difference in the return generated by

portfolio A and portfolio B.

H1 (Alternative hypothesis): There is no significant mean difference in the return generated by

portfolio A and portfolio B.

Independent sample t test

Portfolio A

(Random)

Portfolio B

(Technical)

Mean 0.002772 0.009324

Variance 0.000188 0.000435

Observations 30 30

Pooled Variance 0.000311

Hypothesized Mean Difference 0

df 58

t Stat -1.43809

P(T<=t) one-tail 0.077892

t Critical one-tail 1.671553

P(T<=t) two-tail 0.155784

t Critical two-tail 2.001717

Outcome of t test evaluation shows that p>0.05 which shows that null hypothesis is true

and other one is rejected. Referring this, it can be stated that no statistical significant difference

0

5

10

15

FTSE Residual Plot

FTSE

Residuals

d. Testing monthly logarithmic returns of both the portfolios by taking into account independent

sample t- test

Hypothesis

H0 (Null hypothesis): There is no significant mean difference in the return generated by

portfolio A and portfolio B.

H1 (Alternative hypothesis): There is no significant mean difference in the return generated by

portfolio A and portfolio B.

Independent sample t test

Portfolio A

(Random)

Portfolio B

(Technical)

Mean 0.002772 0.009324

Variance 0.000188 0.000435

Observations 30 30

Pooled Variance 0.000311

Hypothesized Mean Difference 0

df 58

t Stat -1.43809

P(T<=t) one-tail 0.077892

t Critical one-tail 1.671553

P(T<=t) two-tail 0.155784

t Critical two-tail 2.001717

Outcome of t test evaluation shows that p>0.05 which shows that null hypothesis is true

and other one is rejected. Referring this, it can be stated that no statistical significant difference

takes place in the mean value of returns pertaining to portfolio A and B. However, on the basis of

overall assessment it can be depicted that portfolio B is offering higher returns to the investors

over the random one.

e. Discussion of findings derived through statistical evaluation

By doing assessment, it has found that mean returns which are offering by Portfolio B are

higher in comparison A. However, mean returns of both the portfolios are moving in the similar

direction to some extent. From analysis of monthly returns, it has assessed that market

information has impact on returns. Thus, rather than making selection of stock in portfolio on

random basis, emphasis needs to be placed on doing technical evaluation. Further, it has assessed

from the evaluation that FTSE return such as 6% is highly lower as compared to margin

associated with technical portfolio which in turn accounts for 28% respectively. Considering this,

it can be depicted that portfolio based on technical evaluation performs better as compared to the

random one.

f. Critically evaluating findings in the empirical study on WFME and random walk theory

Weak from efficiency also known as random walk theory which in turn presents that

future security prices are random and not influences from the past events (Ang, 2011). Such

theoretical framework is criticized on the basis of the aspects that it fails to cover market size,

volatility and shareholders expectation. Hence, it can be depicted that stock selection must be on

the basis of technical evaluation rather than random.

PART B

Assessing whether Bayer’s should support the deal pertaining to Monsanto’s acquisition

Cited case situation presents that Bayer’s is highly confident in relation to getting all the

legal approvals within the suitable time frame. Further, it has found from the case study

evaluation that Bayer’s has offered 1.5 USD billion to Monsanto for the finalization of deal.

This transaction or proposed merger and acquisition activity is recognized as highly attractive for

Monsanto‘s shareholders. In addition to this, Bayer’s believe that such offer will enhance the

intrinsic value of Monsanto. The main aim of business unit behind taking initiatives in terms of

M&A is to maximize the wealth of shareholders. In the context of business unit, shareholders are

overall assessment it can be depicted that portfolio B is offering higher returns to the investors

over the random one.

e. Discussion of findings derived through statistical evaluation

By doing assessment, it has found that mean returns which are offering by Portfolio B are

higher in comparison A. However, mean returns of both the portfolios are moving in the similar

direction to some extent. From analysis of monthly returns, it has assessed that market

information has impact on returns. Thus, rather than making selection of stock in portfolio on

random basis, emphasis needs to be placed on doing technical evaluation. Further, it has assessed

from the evaluation that FTSE return such as 6% is highly lower as compared to margin

associated with technical portfolio which in turn accounts for 28% respectively. Considering this,

it can be depicted that portfolio based on technical evaluation performs better as compared to the

random one.

f. Critically evaluating findings in the empirical study on WFME and random walk theory

Weak from efficiency also known as random walk theory which in turn presents that

future security prices are random and not influences from the past events (Ang, 2011). Such

theoretical framework is criticized on the basis of the aspects that it fails to cover market size,

volatility and shareholders expectation. Hence, it can be depicted that stock selection must be on

the basis of technical evaluation rather than random.

PART B

Assessing whether Bayer’s should support the deal pertaining to Monsanto’s acquisition

Cited case situation presents that Bayer’s is highly confident in relation to getting all the

legal approvals within the suitable time frame. Further, it has found from the case study

evaluation that Bayer’s has offered 1.5 USD billion to Monsanto for the finalization of deal.

This transaction or proposed merger and acquisition activity is recognized as highly attractive for

Monsanto‘s shareholders. In addition to this, Bayer’s believe that such offer will enhance the

intrinsic value of Monsanto. The main aim of business unit behind taking initiatives in terms of

M&A is to maximize the wealth of shareholders. In the context of business unit, shareholders are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

considered as real owner of firm. Hence, being a owner, shareholders expect that proposed

expansion plan will contribute in their wealth to the significant level.

Referring case, it can be depicted that with the motive to explore business operations and

functions Bayer’s has taken decision in relation to acquiring Monsanto. For the purpose of such

international M&A, Bayer bids by 1.5 USD million respectively (Bayer’s acquisition, 2018). In

this regard, the main issue is to assess the extent to which capital structure and cost of capital

affects shareholders wealth. Thus, it can be presented from the evaluation that sources of funding

that are undertaken for the purpose of financing acquisition has significant impact on cost of

capital structure.

Given case situation presents that Bayer’s will settle such deal by making cash payment

to the shareholders. In the context of such cash settlement, Bayer’s depicted that loan will be

taken from five banks namely BofA Merrill Lynch, Credit Suisse, Goldman Sachs, HSBC and JP

Morgan. Acquiring company presents that, on the basis of complementary product portfolio, loan

will be granted by such banks to it. From assessment, it has identified that strategy pertaining to

taking loan will significantly affect capital structure and thereby cost of capital.

According to Pratt and Grabowski (2008), high debt-equity ratio closely impacts

organizational profitability and thereby shareholders wealth or return. Moreover, in the case of

debt or loan business unit is obliged to make interest payment and installment when it become

due irrespective of the aspect that whether profit generated in the concerned year or not. On the

other side, in the case of shares, business unit provides shareholders with dividends when it earns

enough margins. Thus, debt imposes high level of financial burden as compared to equity source

of financing. However, on the critical note, Baker and Wurgler (2015) mentioned that, from the

perspective of shareholders, dividend decreases when firm issues large number of equities.

Moreover, as per dividend policy, profit is divided among all the shareholders. Thus, negative

relationship takes place between number of shareholders and dividend per share. Further,

considering trade-off theory Li (2015) depicted that at the time of raising funds business unit

should give priority to internal sources and thereby external. In relation to external sources,

priority should be given to debt over equity. Moreover, debt offers benefit to the company in tax

shield. Caskey, Hughes and Liu (2015) argued that optimal structure is when debt-equity ratio

accounts for .5:1 significantly. On the basis of such standard or ideal measure 2 equities need to

expansion plan will contribute in their wealth to the significant level.

Referring case, it can be depicted that with the motive to explore business operations and

functions Bayer’s has taken decision in relation to acquiring Monsanto. For the purpose of such

international M&A, Bayer bids by 1.5 USD million respectively (Bayer’s acquisition, 2018). In

this regard, the main issue is to assess the extent to which capital structure and cost of capital

affects shareholders wealth. Thus, it can be presented from the evaluation that sources of funding

that are undertaken for the purpose of financing acquisition has significant impact on cost of

capital structure.

Given case situation presents that Bayer’s will settle such deal by making cash payment

to the shareholders. In the context of such cash settlement, Bayer’s depicted that loan will be

taken from five banks namely BofA Merrill Lynch, Credit Suisse, Goldman Sachs, HSBC and JP

Morgan. Acquiring company presents that, on the basis of complementary product portfolio, loan

will be granted by such banks to it. From assessment, it has identified that strategy pertaining to

taking loan will significantly affect capital structure and thereby cost of capital.

According to Pratt and Grabowski (2008), high debt-equity ratio closely impacts

organizational profitability and thereby shareholders wealth or return. Moreover, in the case of

debt or loan business unit is obliged to make interest payment and installment when it become

due irrespective of the aspect that whether profit generated in the concerned year or not. On the

other side, in the case of shares, business unit provides shareholders with dividends when it earns

enough margins. Thus, debt imposes high level of financial burden as compared to equity source

of financing. However, on the critical note, Baker and Wurgler (2015) mentioned that, from the

perspective of shareholders, dividend decreases when firm issues large number of equities.

Moreover, as per dividend policy, profit is divided among all the shareholders. Thus, negative

relationship takes place between number of shareholders and dividend per share. Further,

considering trade-off theory Li (2015) depicted that at the time of raising funds business unit

should give priority to internal sources and thereby external. In relation to external sources,

priority should be given to debt over equity. Moreover, debt offers benefit to the company in tax

shield. Caskey, Hughes and Liu (2015) argued that optimal structure is when debt-equity ratio

accounts for .5:1 significantly. On the basis of such standard or ideal measure 2 equities need to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be issued over 1 debt. Hence, by following such ratio optimal capital structure can be created by

the firm. Thus, at the time of raising funding sources business unit should keep in mind such

ideal measure. Biørn (2017) entailed in their study that for the enhancement of shareholder’s

wealth appropriate use of financial leverage is highly required. Moreover, leverage has direct

impact on cost of capital and financial structure.

By doing analysis of current financial position, it has assessed that debt-equity ratio of

Bayer was .51 and .33 in the accounting year 2016 & 2017. Hence, referring the literature it can

be depicted that solvency position of Bayer is currently good and in line with the ideal ratio such

as .5:1. Hence, in the context of financing such proposed acquisition it can be stated that option

pertaining to taking loan is highly suitable (Levi and Welch, 2017). However, company should

avoid taking only one financing source such as bank loan for funding proposed global merger

and acquisition plan. Moreover, if company takes resort of debt then capital structure of Bayer

will be affected negatively. Along with this, inclusion of high debt will also impose burden in

front of firm under monetary terms. In the case of high interest obligation Bayer would not

become able to offer suitable returns to the shareholders.

Along with this, it has assessed that current ratio of Bayer was 1.64 and 2.21 respectively

in the financial year 2016 & 2017. Hence, as compared to ideal ratio, company had maintained

high liquidity or working capital. From evaluation, it has assessed that acquisition deal can be

financed through undertaking different sources such as cash, stock, equity and loan. Hence, by

undertaking combination of sources such as cash available within the firm, equity and debt such

global merger and acquisition deal can be executed. This in turn directly contributes in both

development of optimal capital structure and maximization of shareholders wealth. Further, in

accordance with the theoretical framework, emphasis needs to be placed on lowering down the

cost of capital while making selection of funding source. The reason behind this, high cost of

capital has negative impact on shareholders wealth. Thus, debt should be preferred over equity

only when it has lower cost of capital as compared to equity. Hence, Bayer should undertake

financial source by taking into account and comparing the cost of each financial source.

Referring overall evaluation, it is suggested to Bayer that undertakes both equity and debt loan

source for funding proposed acquisition. This in turn helps in developing optimal capital

structure, reducing cost of capital and maximizing shareholders’ wealth.

the firm. Thus, at the time of raising funding sources business unit should keep in mind such

ideal measure. Biørn (2017) entailed in their study that for the enhancement of shareholder’s

wealth appropriate use of financial leverage is highly required. Moreover, leverage has direct

impact on cost of capital and financial structure.

By doing analysis of current financial position, it has assessed that debt-equity ratio of

Bayer was .51 and .33 in the accounting year 2016 & 2017. Hence, referring the literature it can

be depicted that solvency position of Bayer is currently good and in line with the ideal ratio such

as .5:1. Hence, in the context of financing such proposed acquisition it can be stated that option

pertaining to taking loan is highly suitable (Levi and Welch, 2017). However, company should

avoid taking only one financing source such as bank loan for funding proposed global merger

and acquisition plan. Moreover, if company takes resort of debt then capital structure of Bayer

will be affected negatively. Along with this, inclusion of high debt will also impose burden in

front of firm under monetary terms. In the case of high interest obligation Bayer would not

become able to offer suitable returns to the shareholders.

Along with this, it has assessed that current ratio of Bayer was 1.64 and 2.21 respectively

in the financial year 2016 & 2017. Hence, as compared to ideal ratio, company had maintained

high liquidity or working capital. From evaluation, it has assessed that acquisition deal can be

financed through undertaking different sources such as cash, stock, equity and loan. Hence, by

undertaking combination of sources such as cash available within the firm, equity and debt such

global merger and acquisition deal can be executed. This in turn directly contributes in both

development of optimal capital structure and maximization of shareholders wealth. Further, in

accordance with the theoretical framework, emphasis needs to be placed on lowering down the

cost of capital while making selection of funding source. The reason behind this, high cost of

capital has negative impact on shareholders wealth. Thus, debt should be preferred over equity

only when it has lower cost of capital as compared to equity. Hence, Bayer should undertake

financial source by taking into account and comparing the cost of each financial source.

Referring overall evaluation, it is suggested to Bayer that undertakes both equity and debt loan

source for funding proposed acquisition. This in turn helps in developing optimal capital

structure, reducing cost of capital and maximizing shareholders’ wealth.

CONCLUSION

By summing up this report, it has been concluded that portfolios that developed on the

basis of technical evaluation are highly suitable. Moreover, highly structured portfolio offers

more return to the investors over the one in which stock selection made on random basis.

Further, it has been articulated that Bayer should focus on raising funds by taking into account

ideal debt-equity ratio. It can be seen in the report that shareholders’ wealth increases when

declining trend assessed in cost of capital. It can be summarized from the report that rather than

settling deal in cash through taking resort of loan Bayer should focus on other sources. Hence, by

using funding sources such as equity, cash equivalents and loan Bayer can build and maintain

suitable capital structure and thereby become able to enhance shareholders wealth.

By summing up this report, it has been concluded that portfolios that developed on the

basis of technical evaluation are highly suitable. Moreover, highly structured portfolio offers

more return to the investors over the one in which stock selection made on random basis.

Further, it has been articulated that Bayer should focus on raising funds by taking into account

ideal debt-equity ratio. It can be seen in the report that shareholders’ wealth increases when

declining trend assessed in cost of capital. It can be summarized from the report that rather than

settling deal in cash through taking resort of loan Bayer should focus on other sources. Hence, by

using funding sources such as equity, cash equivalents and loan Bayer can build and maintain

suitable capital structure and thereby become able to enhance shareholders wealth.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic Review. 105(5).

pp.315-20.

Biørn, E., 2017. Taxation, technology, and the user cost of capital. Elsevier.

Caskey, J., Hughes, J. and Liu, J., 2015. Strategic Informed Trades, Diversification, and Cost of

Capital. Accounting Review. 90(5). pp.1811-37.

Levi, Y. and Welch, I., 2017. Best practice for cost-of-capital estimates. Journal of Financial

and Quantitative Analysis. 52(2). pp.427-463.

Li, X., 2015. Accounting conservatism and the cost of capital: An international analysis. Journal

of Business Finance & Accounting. 42(5-6). pp.555-582.

Pratt, S. P. and Grabowski, R. J., 2008. Cost of capital. John Wiley & Sons.

Online

Ang, A., 2011. Review of the Efficient Market Theory and Evidence. [Online]. Available through:

<https://www0.gsb.columbia.edu/faculty/aang/papers/EMH.pdf>:

Bayer’s acquisition. 2018. [Online]. Available through:

<http://press.bayer.com/baynews/baynews.nsf/id/2016-0157-EN >:

Books and Journals

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic Review. 105(5).

pp.315-20.

Biørn, E., 2017. Taxation, technology, and the user cost of capital. Elsevier.

Caskey, J., Hughes, J. and Liu, J., 2015. Strategic Informed Trades, Diversification, and Cost of

Capital. Accounting Review. 90(5). pp.1811-37.

Levi, Y. and Welch, I., 2017. Best practice for cost-of-capital estimates. Journal of Financial

and Quantitative Analysis. 52(2). pp.427-463.

Li, X., 2015. Accounting conservatism and the cost of capital: An international analysis. Journal

of Business Finance & Accounting. 42(5-6). pp.555-582.

Pratt, S. P. and Grabowski, R. J., 2008. Cost of capital. John Wiley & Sons.

Online

Ang, A., 2011. Review of the Efficient Market Theory and Evidence. [Online]. Available through:

<https://www0.gsb.columbia.edu/faculty/aang/papers/EMH.pdf>:

Bayer’s acquisition. 2018. [Online]. Available through:

<http://press.bayer.com/baynews/baynews.nsf/id/2016-0157-EN >:

1 out of 19