Corporate Financial Management Part A and Part B

VerifiedAdded on 2023/06/17

|15

|4328

|209

AI Summary

This report discusses the pros and cons of incorporating debt in existing portfolio of equity and debt, reduction of risk by diversifying investment through pension scheme, and valuation of Sporty PLC using different methods. It also justifies the value of Sporty PLC and motive behind acquisition. The report is divided into two parts: Part A is included in Power point presentation and Part B includes tasks related to diversification, valuation and acquisition. The company chosen in this report is Rebecca and Roy Race (RR) Ltd, a fashion company dealing in seasonal brands and providing different products for middle income women and younger ones.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Corporate Financial

Management Part A

and Part B

Management Part A

and Part B

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION ..........................................................................................................................3

PART A...........................................................................................................................................3

PART B............................................................................................................................................3

Task 1: Reason behind diversification leading to reduction in risk in relation to return.......3

Task 2: Calculate the following and justify the value of Sporty PLC....................................5

Task 3: Calculate NPV...........................................................................................................9

Calculate Standard Deviation...............................................................................................10

Make the curve showing the probability of the NPV which is less than zero, assuming a

normal distribution of return................................................................................................10

Critically evaluate how the traditional NPV is as effective as NPV methods with real option

perspectives and incorporating probabilities........................................................................11

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION ..........................................................................................................................3

PART A...........................................................................................................................................3

PART B............................................................................................................................................3

Task 1: Reason behind diversification leading to reduction in risk in relation to return.......3

Task 2: Calculate the following and justify the value of Sporty PLC....................................5

Task 3: Calculate NPV...........................................................................................................9

Calculate Standard Deviation...............................................................................................10

Make the curve showing the probability of the NPV which is less than zero, assuming a

normal distribution of return................................................................................................10

Critically evaluate how the traditional NPV is as effective as NPV methods with real option

perspectives and incorporating probabilities........................................................................11

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Corporate finance deals with the arrangement of funds, capital formation and its

management in order to increase the reputation and value of firm among the stakeholders and

market. It focuses on maximising the price of shares by making different long and short term

plans. The concept helps the owners of the business to take various investment related decisions

so that they can grab best opportunities prevailing in the market (Agyei-Mensah, 2018). The

company chosen in this report is Rebecca and Roy Race (RR) Ltd. It is a fashion company

dealing in seasonal brands and providing different products for middle income women and

younger ones. The report is divided into two parts. The first sections deals in pros and cons of

incorporating debt in existing portfolio of equity and debt. The second part discusses about the

reduction of risk by diversifying investment through pension scheme. It further calculates the

value of company for taking investment decision. It also determines the present values of money

invested in a proposal and whether it is beneficial or not.

PART A

This part is included in Power point presentation.

PART B

Task 1: Reason behind diversification leading to reduction in risk in relation to return.

Diversification is tool of managing risks by distributing the investment among various

businesses, investment opportunities or industries. The main aim behind choosing this format is

to maximising the return from various sources so that failure in one scheme would not result in

loss from complete investment. Their is a well known phrase that never put all your eggs in one

basket only. Looking from the financial point of view, own should opt for multiple opportunities

rather than contributing in single plan only. For example, a person can invest its cash in stock as

well as debentures. When there is any sort of depression in the economy, the value of debentures

will be secured even when the prices of shares have been reduced. In this way, even when its

profits are not increasing, the risk of investment could be reduced (Brigham and Houston, 2021).

Whenever a person invests in any financial instrument, it brings risks along with returns

which must be taken into account while taking any investing decision. Risk can be defined as a

rate of chance with which the actual results can differ from the expected ones. Their are

generally two types of risk whose management depends on the calibre of the investor. Systematic

Corporate finance deals with the arrangement of funds, capital formation and its

management in order to increase the reputation and value of firm among the stakeholders and

market. It focuses on maximising the price of shares by making different long and short term

plans. The concept helps the owners of the business to take various investment related decisions

so that they can grab best opportunities prevailing in the market (Agyei-Mensah, 2018). The

company chosen in this report is Rebecca and Roy Race (RR) Ltd. It is a fashion company

dealing in seasonal brands and providing different products for middle income women and

younger ones. The report is divided into two parts. The first sections deals in pros and cons of

incorporating debt in existing portfolio of equity and debt. The second part discusses about the

reduction of risk by diversifying investment through pension scheme. It further calculates the

value of company for taking investment decision. It also determines the present values of money

invested in a proposal and whether it is beneficial or not.

PART A

This part is included in Power point presentation.

PART B

Task 1: Reason behind diversification leading to reduction in risk in relation to return.

Diversification is tool of managing risks by distributing the investment among various

businesses, investment opportunities or industries. The main aim behind choosing this format is

to maximising the return from various sources so that failure in one scheme would not result in

loss from complete investment. Their is a well known phrase that never put all your eggs in one

basket only. Looking from the financial point of view, own should opt for multiple opportunities

rather than contributing in single plan only. For example, a person can invest its cash in stock as

well as debentures. When there is any sort of depression in the economy, the value of debentures

will be secured even when the prices of shares have been reduced. In this way, even when its

profits are not increasing, the risk of investment could be reduced (Brigham and Houston, 2021).

Whenever a person invests in any financial instrument, it brings risks along with returns

which must be taken into account while taking any investing decision. Risk can be defined as a

rate of chance with which the actual results can differ from the expected ones. Their are

generally two types of risk whose management depends on the calibre of the investor. Systematic

risks are uncontrollable and holds the power to show effect on macro level. It can impact the

whole investment plan or the complete asset. Some common examples under this can be

inflation, interest rate or any law or policy passed by government related to investments. These

all can have major affect on the asset value. On the other hand, unsystematic risk are very small

and effects only at small level. It can be some specific industry or part of asset. For instance, fire

in factory can slightly make impact on the shares prices of that firm (Dalal and Thaker, 2019) .

These risks can be evaluated by applying various methods, out of this the two methods

which can be used in case of investing in assets are as follows:

Covariance is a technique that helps in valuing two assets in relation to one another. It

helps in reducing the chances of volatility by providing scope of diversification. Negative

result in its analysis shows that the two investing opportunities are following an opposite

trend. While the positive interprets that both of them are following the same path. This

positive result is very important for reducing the risk of investment. Normally, historical

price is used in it for ascertaining whether a particular scheme should be included in

portfolio or not. But there is some limitation which makes the use of tool slightly

ineffective. It do not calculate the strength of the relation among the prices of different

assets. But still this method is very much popular among the analysts for constructing

their portfolio (Giosi and Caiffa, 2020).

Capital Asset Pricing Model interprets the relation among the risks and returns which is

expected by the investor. Under this method, the investor tries to compensate its risk

along with the impact of time value of money on the scheme. It simply shows that

anticipated profits on security is same as the risk premium in addition to risk free return.

The objective of using this tool is for ascertaining the prices of securities and generating

information that whether the assets can bring expected returns in prevailing risk and cost

of capital.

Investors invest their money in order to yield some profits out of it. For this, it is

important for them to check how much return a particular investment can bring and the extent of

risk associated with it. The above mentioned methods can be used for solving this purpose.

Points to be kept in mind at the time of diversification:

whole investment plan or the complete asset. Some common examples under this can be

inflation, interest rate or any law or policy passed by government related to investments. These

all can have major affect on the asset value. On the other hand, unsystematic risk are very small

and effects only at small level. It can be some specific industry or part of asset. For instance, fire

in factory can slightly make impact on the shares prices of that firm (Dalal and Thaker, 2019) .

These risks can be evaluated by applying various methods, out of this the two methods

which can be used in case of investing in assets are as follows:

Covariance is a technique that helps in valuing two assets in relation to one another. It

helps in reducing the chances of volatility by providing scope of diversification. Negative

result in its analysis shows that the two investing opportunities are following an opposite

trend. While the positive interprets that both of them are following the same path. This

positive result is very important for reducing the risk of investment. Normally, historical

price is used in it for ascertaining whether a particular scheme should be included in

portfolio or not. But there is some limitation which makes the use of tool slightly

ineffective. It do not calculate the strength of the relation among the prices of different

assets. But still this method is very much popular among the analysts for constructing

their portfolio (Giosi and Caiffa, 2020).

Capital Asset Pricing Model interprets the relation among the risks and returns which is

expected by the investor. Under this method, the investor tries to compensate its risk

along with the impact of time value of money on the scheme. It simply shows that

anticipated profits on security is same as the risk premium in addition to risk free return.

The objective of using this tool is for ascertaining the prices of securities and generating

information that whether the assets can bring expected returns in prevailing risk and cost

of capital.

Investors invest their money in order to yield some profits out of it. For this, it is

important for them to check how much return a particular investment can bring and the extent of

risk associated with it. The above mentioned methods can be used for solving this purpose.

Points to be kept in mind at the time of diversification:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Risk tolerant- While investing in multiple options, one must consider that the amount of

risk it can tolerate. If its appetite is big, then it can opt of more riskier portfolio.

Otherwise, it should choose a mix of investing options with high and low-risk.

Time-frame- Another thing needed to be considered is the duration for which the money

is to deposited with that company. All the investments should be of different time period

otherwise the risk of liquidity may increase in future (Golden, 2021).

Amount of capital- It is also important to keep in mind that over diversification can also

lead to loss of profits. The decision of amount to be invested should be taken wisely.

Investing too less amount will amount for less income from it in future and too much

money can increase the risk of loss. So, an adequate amount of cash should be invested

after analysing the risk and return linked to it.

RR Ltd is opting to launch a private pension scheme for the benefit of its employees. It is

the set ups brought up by companies for enabling their staff members a hold on some money

after retirement. They are the money paid by workers along with the performance shown by the

scheme in which that particular amount has been invested in. Apart from giving benefits in

future, these plans also provides multiple advantages to the beholder. The amount paid for it can

be claimed as deduction under tax. Also, these plans are secure from the point of view of

liquidity in old age. One would not have to rely on other sources like bank loans.

Pension scheme launched by RR will help the employees in arranging separate funds

other than the formats they are currently investing in. It will lead them to the path of

diversification where they can mitigate their risk of losses. It will create an opportunity for them

to invest in another and secure portfolio (Gras and Krause, 2020).

Task 2: Calculate the following and justify the value of Sporty PLC.

1) Calculate the value of Sporty by the following valuation methods.

a) Price / Earning Ratio- It is used to ascertain the value of firm by measuring its current price

with that of to its earnings per share. It helps in determining whether the company is over or

under valued.

Formula = Share price / Earnings per share

RR Ltd. (£) Sporty PLC. (£)

Share price 6 2

risk it can tolerate. If its appetite is big, then it can opt of more riskier portfolio.

Otherwise, it should choose a mix of investing options with high and low-risk.

Time-frame- Another thing needed to be considered is the duration for which the money

is to deposited with that company. All the investments should be of different time period

otherwise the risk of liquidity may increase in future (Golden, 2021).

Amount of capital- It is also important to keep in mind that over diversification can also

lead to loss of profits. The decision of amount to be invested should be taken wisely.

Investing too less amount will amount for less income from it in future and too much

money can increase the risk of loss. So, an adequate amount of cash should be invested

after analysing the risk and return linked to it.

RR Ltd is opting to launch a private pension scheme for the benefit of its employees. It is

the set ups brought up by companies for enabling their staff members a hold on some money

after retirement. They are the money paid by workers along with the performance shown by the

scheme in which that particular amount has been invested in. Apart from giving benefits in

future, these plans also provides multiple advantages to the beholder. The amount paid for it can

be claimed as deduction under tax. Also, these plans are secure from the point of view of

liquidity in old age. One would not have to rely on other sources like bank loans.

Pension scheme launched by RR will help the employees in arranging separate funds

other than the formats they are currently investing in. It will lead them to the path of

diversification where they can mitigate their risk of losses. It will create an opportunity for them

to invest in another and secure portfolio (Gras and Krause, 2020).

Task 2: Calculate the following and justify the value of Sporty PLC.

1) Calculate the value of Sporty by the following valuation methods.

a) Price / Earning Ratio- It is used to ascertain the value of firm by measuring its current price

with that of to its earnings per share. It helps in determining whether the company is over or

under valued.

Formula = Share price / Earnings per share

RR Ltd. (£) Sporty PLC. (£)

Share price 6 2

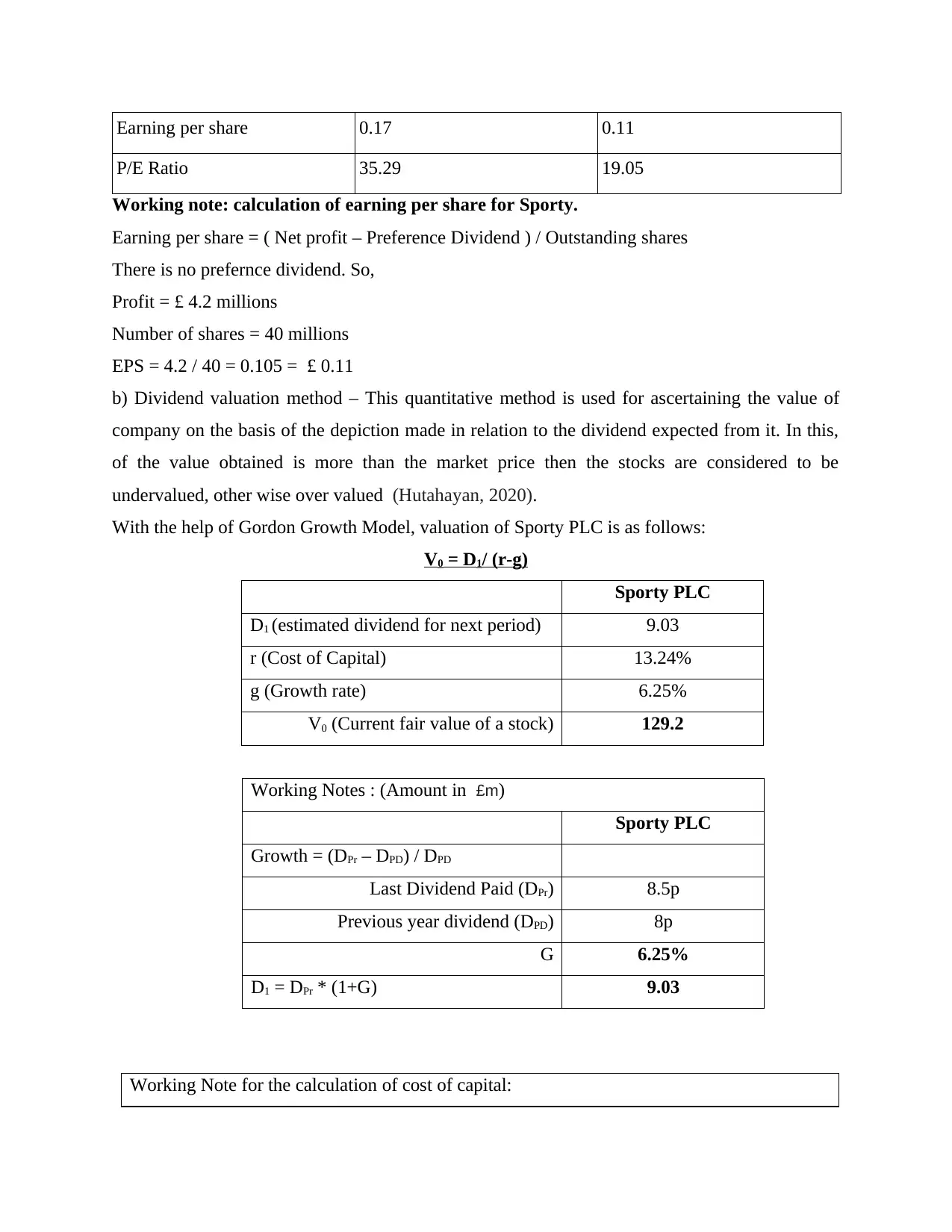

Earning per share 0.17 0.11

P/E Ratio 35.29 19.05

Working note: calculation of earning per share for Sporty.

Earning per share = ( Net profit – Preference Dividend ) / Outstanding shares

There is no prefernce dividend. So,

Profit = £ 4.2 millions

Number of shares = 40 millions

EPS = 4.2 / 40 = 0.105 = £ 0.11

b) Dividend valuation method – This quantitative method is used for ascertaining the value of

company on the basis of the depiction made in relation to the dividend expected from it. In this,

of the value obtained is more than the market price then the stocks are considered to be

undervalued, other wise over valued (Hutahayan, 2020).

With the help of Gordon Growth Model, valuation of Sporty PLC is as follows:

V0 = D1/ (r-g)

Sporty PLC

D1 (estimated dividend for next period) 9.03

r (Cost of Capital) 13.24%

g (Growth rate) 6.25%

V0 (Current fair value of a stock) 129.2

Working Notes : (Amount in £m)

Sporty PLC

Growth = (DPr – DPD) / DPD

Last Dividend Paid (DPr) 8.5p

Previous year dividend (DPD) 8p

G 6.25%

D1 = DPr * (1+G) 9.03

Working Note for the calculation of cost of capital:

P/E Ratio 35.29 19.05

Working note: calculation of earning per share for Sporty.

Earning per share = ( Net profit – Preference Dividend ) / Outstanding shares

There is no prefernce dividend. So,

Profit = £ 4.2 millions

Number of shares = 40 millions

EPS = 4.2 / 40 = 0.105 = £ 0.11

b) Dividend valuation method – This quantitative method is used for ascertaining the value of

company on the basis of the depiction made in relation to the dividend expected from it. In this,

of the value obtained is more than the market price then the stocks are considered to be

undervalued, other wise over valued (Hutahayan, 2020).

With the help of Gordon Growth Model, valuation of Sporty PLC is as follows:

V0 = D1/ (r-g)

Sporty PLC

D1 (estimated dividend for next period) 9.03

r (Cost of Capital) 13.24%

g (Growth rate) 6.25%

V0 (Current fair value of a stock) 129.2

Working Notes : (Amount in £m)

Sporty PLC

Growth = (DPr – DPD) / DPD

Last Dividend Paid (DPr) 8.5p

Previous year dividend (DPD) 8p

G 6.25%

D1 = DPr * (1+G) 9.03

Working Note for the calculation of cost of capital:

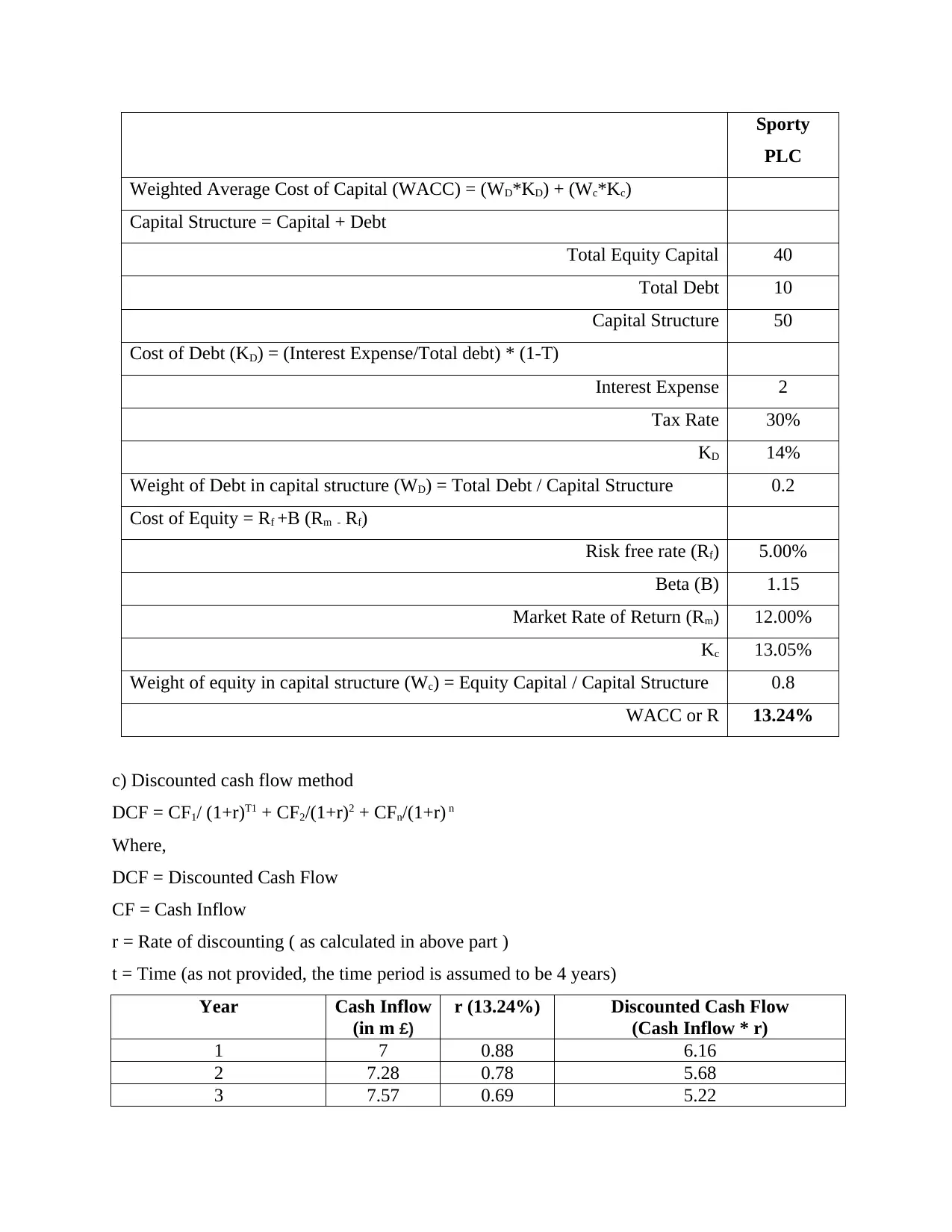

Sporty

PLC

Weighted Average Cost of Capital (WACC) = (WD*KD) + (Wc*Kc)

Capital Structure = Capital + Debt

Total Equity Capital 40

Total Debt 10

Capital Structure 50

Cost of Debt (KD) = (Interest Expense/Total debt) * (1-T)

Interest Expense 2

Tax Rate 30%

KD 14%

Weight of Debt in capital structure (WD) = Total Debt / Capital Structure 0.2

Cost of Equity = Rf +B (Rm - Rf)

Risk free rate (Rf) 5.00%

Beta (B) 1.15

Market Rate of Return (Rm) 12.00%

Kc 13.05%

Weight of equity in capital structure (Wc) = Equity Capital / Capital Structure 0.8

WACC or R 13.24%

c) Discounted cash flow method

DCF = CF1/ (1+r)T1 + CF2/(1+r)2 + CFn/(1+r) n

Where,

DCF = Discounted Cash Flow

CF = Cash Inflow

r = Rate of discounting ( as calculated in above part )

t = Time (as not provided, the time period is assumed to be 4 years)

Year Cash Inflow

(in m £)

r (13.24%) Discounted Cash Flow

(Cash Inflow * r)

1 7 0.88 6.16

2 7.28 0.78 5.68

3 7.57 0.69 5.22

PLC

Weighted Average Cost of Capital (WACC) = (WD*KD) + (Wc*Kc)

Capital Structure = Capital + Debt

Total Equity Capital 40

Total Debt 10

Capital Structure 50

Cost of Debt (KD) = (Interest Expense/Total debt) * (1-T)

Interest Expense 2

Tax Rate 30%

KD 14%

Weight of Debt in capital structure (WD) = Total Debt / Capital Structure 0.2

Cost of Equity = Rf +B (Rm - Rf)

Risk free rate (Rf) 5.00%

Beta (B) 1.15

Market Rate of Return (Rm) 12.00%

Kc 13.05%

Weight of equity in capital structure (Wc) = Equity Capital / Capital Structure 0.8

WACC or R 13.24%

c) Discounted cash flow method

DCF = CF1/ (1+r)T1 + CF2/(1+r)2 + CFn/(1+r) n

Where,

DCF = Discounted Cash Flow

CF = Cash Inflow

r = Rate of discounting ( as calculated in above part )

t = Time (as not provided, the time period is assumed to be 4 years)

Year Cash Inflow

(in m £)

r (13.24%) Discounted Cash Flow

(Cash Inflow * r)

1 7 0.88 6.16

2 7.28 0.78 5.68

3 7.57 0.69 5.22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4 7.87 0.61 4.8

Total discounted cash inflow 21.86

Less: Equivalent initial outlay 40

Net Present value -18.14

Apart from this inflows, their will also be an initial inflow of around 20 million from the

sale of duplicate machinery. After this, the Net present value of acquiring firm after 4 years

would be

= 20 + 21.86 -40

= £ 1.86

2) Justify the value of Sporty PLC and motive behind Acquisition.

Based on the calculations made above, it can be interpreted that the decision of acquiring

Sporty Plc by RR Ltd is a good option. Though, price earning ratio of the former is far less than

the later one. But still, it is earning profits. Their is a huge possibility that the value of company

and shares may increase after the acquisition by RR. Value of shares is also good at present

which can be improved by the acquiring firm with the help improving the methods the former

previously works. On competition of four years, the expected value of investment is expected to

be £ 1.86. This value is good when looking at future. After fourth year the inflows arising from it

would be prpfits as the investement made would be convered in initital four years only.

According to the scenerio, the judgement made by RR Ltd can be considered opt be

optimistic. It itself is a profitable firm with good knowledge of women fashion and expert

desdigners. As per RR, its designers holds good ionformation and taste of the men's fashion and

their choices. And they are confident that they can improve the situatuion , market proce and

profiatbility of Sporty by their understandings. So, it can be the case that the these resources pf

RR helps Sporty to improve itself. Moreover the decision that the company would be handled by

the Sporty itself, even after acquisition is a good decision. They are already well known to the

structure of the management and the staff and knew the manner to deal with the employees of the

organisation. This will help RR in managing and guiding the employess of Sporty.

On the other hand, their is a huge risk of involving female fashion desigh experts in men's

apparels as their thought of having compete knowledge can prove to be false. It may happen that

their knowledge turns out to be bane for Sporty rather than becoming a boom. RR should keep a

great focus on this aspect as failure on the part of designers would cosuld very heavily to the RR.

Total discounted cash inflow 21.86

Less: Equivalent initial outlay 40

Net Present value -18.14

Apart from this inflows, their will also be an initial inflow of around 20 million from the

sale of duplicate machinery. After this, the Net present value of acquiring firm after 4 years

would be

= 20 + 21.86 -40

= £ 1.86

2) Justify the value of Sporty PLC and motive behind Acquisition.

Based on the calculations made above, it can be interpreted that the decision of acquiring

Sporty Plc by RR Ltd is a good option. Though, price earning ratio of the former is far less than

the later one. But still, it is earning profits. Their is a huge possibility that the value of company

and shares may increase after the acquisition by RR. Value of shares is also good at present

which can be improved by the acquiring firm with the help improving the methods the former

previously works. On competition of four years, the expected value of investment is expected to

be £ 1.86. This value is good when looking at future. After fourth year the inflows arising from it

would be prpfits as the investement made would be convered in initital four years only.

According to the scenerio, the judgement made by RR Ltd can be considered opt be

optimistic. It itself is a profitable firm with good knowledge of women fashion and expert

desdigners. As per RR, its designers holds good ionformation and taste of the men's fashion and

their choices. And they are confident that they can improve the situatuion , market proce and

profiatbility of Sporty by their understandings. So, it can be the case that the these resources pf

RR helps Sporty to improve itself. Moreover the decision that the company would be handled by

the Sporty itself, even after acquisition is a good decision. They are already well known to the

structure of the management and the staff and knew the manner to deal with the employees of the

organisation. This will help RR in managing and guiding the employess of Sporty.

On the other hand, their is a huge risk of involving female fashion desigh experts in men's

apparels as their thought of having compete knowledge can prove to be false. It may happen that

their knowledge turns out to be bane for Sporty rather than becoming a boom. RR should keep a

great focus on this aspect as failure on the part of designers would cosuld very heavily to the RR.

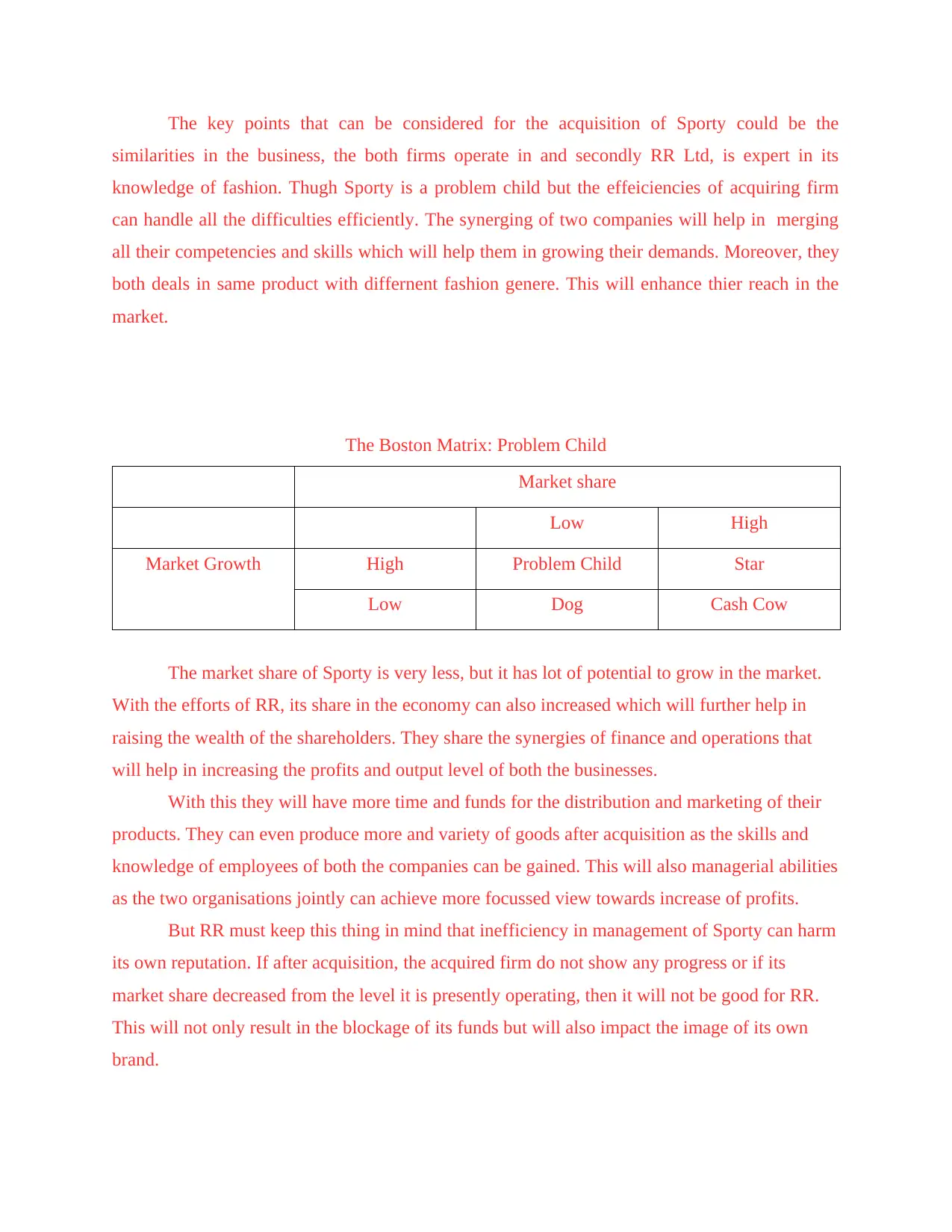

The key points that can be considered for the acquisition of Sporty could be the

similarities in the business, the both firms operate in and secondly RR Ltd, is expert in its

knowledge of fashion. Thugh Sporty is a problem child but the effeiciencies of acquiring firm

can handle all the difficulties efficiently. The synerging of two companies will help in merging

all their competencies and skills which will help them in growing their demands. Moreover, they

both deals in same product with differnent fashion genere. This will enhance thier reach in the

market.

The Boston Matrix: Problem Child

Market share

Low High

Market Growth High Problem Child Star

Low Dog Cash Cow

The market share of Sporty is very less, but it has lot of potential to grow in the market.

With the efforts of RR, its share in the economy can also increased which will further help in

raising the wealth of the shareholders. They share the synergies of finance and operations that

will help in increasing the profits and output level of both the businesses.

With this they will have more time and funds for the distribution and marketing of their

products. They can even produce more and variety of goods after acquisition as the skills and

knowledge of employees of both the companies can be gained. This will also managerial abilities

as the two organisations jointly can achieve more focussed view towards increase of profits.

But RR must keep this thing in mind that inefficiency in management of Sporty can harm

its own reputation. If after acquisition, the acquired firm do not show any progress or if its

market share decreased from the level it is presently operating, then it will not be good for RR.

This will not only result in the blockage of its funds but will also impact the image of its own

brand.

similarities in the business, the both firms operate in and secondly RR Ltd, is expert in its

knowledge of fashion. Thugh Sporty is a problem child but the effeiciencies of acquiring firm

can handle all the difficulties efficiently. The synerging of two companies will help in merging

all their competencies and skills which will help them in growing their demands. Moreover, they

both deals in same product with differnent fashion genere. This will enhance thier reach in the

market.

The Boston Matrix: Problem Child

Market share

Low High

Market Growth High Problem Child Star

Low Dog Cash Cow

The market share of Sporty is very less, but it has lot of potential to grow in the market.

With the efforts of RR, its share in the economy can also increased which will further help in

raising the wealth of the shareholders. They share the synergies of finance and operations that

will help in increasing the profits and output level of both the businesses.

With this they will have more time and funds for the distribution and marketing of their

products. They can even produce more and variety of goods after acquisition as the skills and

knowledge of employees of both the companies can be gained. This will also managerial abilities

as the two organisations jointly can achieve more focussed view towards increase of profits.

But RR must keep this thing in mind that inefficiency in management of Sporty can harm

its own reputation. If after acquisition, the acquired firm do not show any progress or if its

market share decreased from the level it is presently operating, then it will not be good for RR.

This will not only result in the blockage of its funds but will also impact the image of its own

brand.

So, on the whole the decision taken by RR and its motive behind acquisition both are

correct and can be considered for investment.

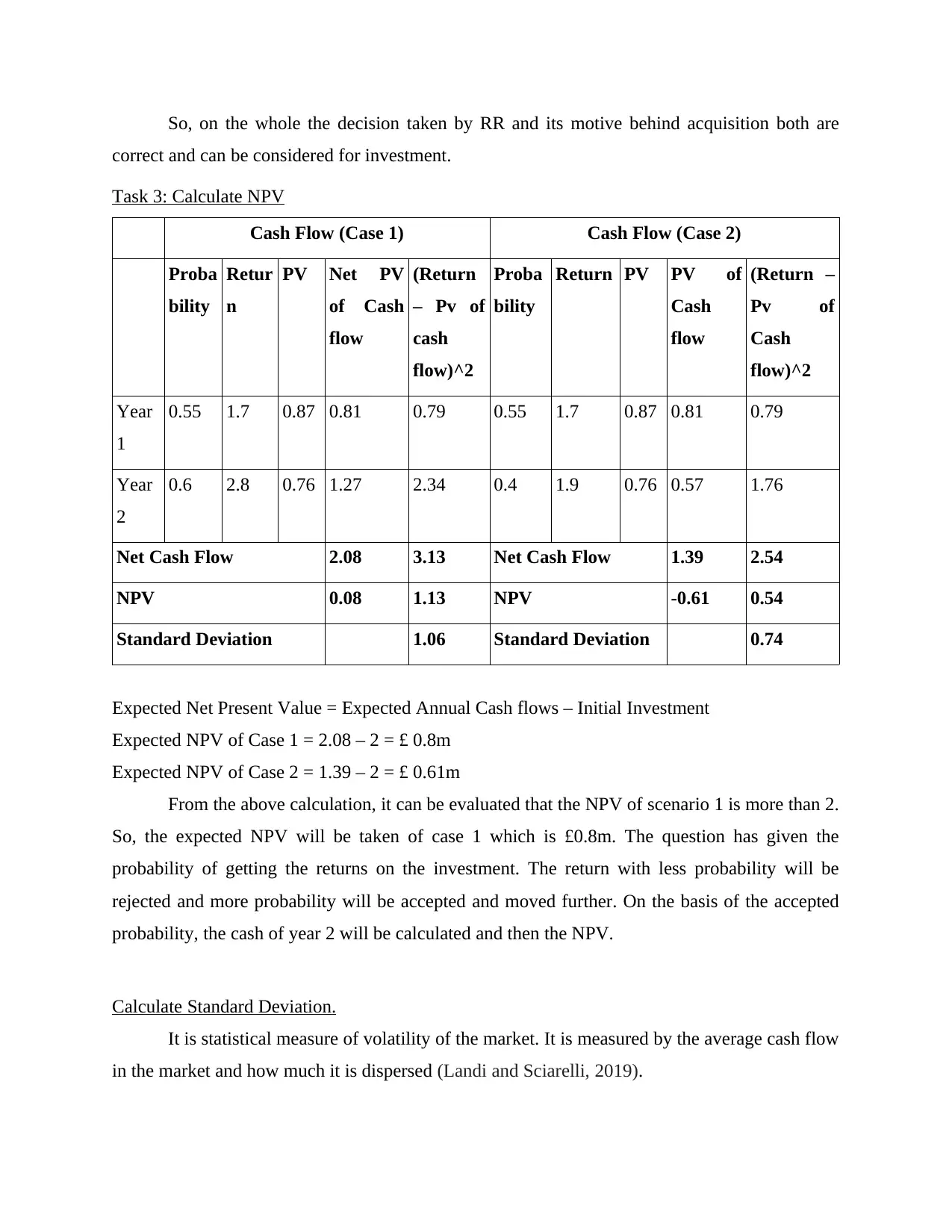

Task 3: Calculate NPV

Cash Flow (Case 1) Cash Flow (Case 2)

Proba

bility

Retur

n

PV Net PV

of Cash

flow

(Return

– Pv of

cash

flow)^2

Proba

bility

Return PV PV of

Cash

flow

(Return –

Pv of

Cash

flow)^2

Year

1

0.55 1.7 0.87 0.81 0.79 0.55 1.7 0.87 0.81 0.79

Year

2

0.6 2.8 0.76 1.27 2.34 0.4 1.9 0.76 0.57 1.76

Net Cash Flow 2.08 3.13 Net Cash Flow 1.39 2.54

NPV 0.08 1.13 NPV -0.61 0.54

Standard Deviation 1.06 Standard Deviation 0.74

Expected Net Present Value = Expected Annual Cash flows – Initial Investment

Expected NPV of Case 1 = 2.08 – 2 = £ 0.8m

Expected NPV of Case 2 = 1.39 – 2 = £ 0.61m

From the above calculation, it can be evaluated that the NPV of scenario 1 is more than 2.

So, the expected NPV will be taken of case 1 which is £0.8m. The question has given the

probability of getting the returns on the investment. The return with less probability will be

rejected and more probability will be accepted and moved further. On the basis of the accepted

probability, the cash of year 2 will be calculated and then the NPV.

Calculate Standard Deviation.

It is statistical measure of volatility of the market. It is measured by the average cash flow

in the market and how much it is dispersed (Landi and Sciarelli, 2019).

correct and can be considered for investment.

Task 3: Calculate NPV

Cash Flow (Case 1) Cash Flow (Case 2)

Proba

bility

Retur

n

PV Net PV

of Cash

flow

(Return

– Pv of

cash

flow)^2

Proba

bility

Return PV PV of

Cash

flow

(Return –

Pv of

Cash

flow)^2

Year

1

0.55 1.7 0.87 0.81 0.79 0.55 1.7 0.87 0.81 0.79

Year

2

0.6 2.8 0.76 1.27 2.34 0.4 1.9 0.76 0.57 1.76

Net Cash Flow 2.08 3.13 Net Cash Flow 1.39 2.54

NPV 0.08 1.13 NPV -0.61 0.54

Standard Deviation 1.06 Standard Deviation 0.74

Expected Net Present Value = Expected Annual Cash flows – Initial Investment

Expected NPV of Case 1 = 2.08 – 2 = £ 0.8m

Expected NPV of Case 2 = 1.39 – 2 = £ 0.61m

From the above calculation, it can be evaluated that the NPV of scenario 1 is more than 2.

So, the expected NPV will be taken of case 1 which is £0.8m. The question has given the

probability of getting the returns on the investment. The return with less probability will be

rejected and more probability will be accepted and moved further. On the basis of the accepted

probability, the cash of year 2 will be calculated and then the NPV.

Calculate Standard Deviation.

It is statistical measure of volatility of the market. It is measured by the average cash flow

in the market and how much it is dispersed (Landi and Sciarelli, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

From the above table, it can be analysed that the standard deviation calculated of case 1 is 1.06

and of case 2 it is 0.74. So, from this it can be interpreted that a low standard deviation measure

the low volatility and high measures the high volatility. It means the standard deviation of case 1

will be chosen, because it is more compared to case 2.

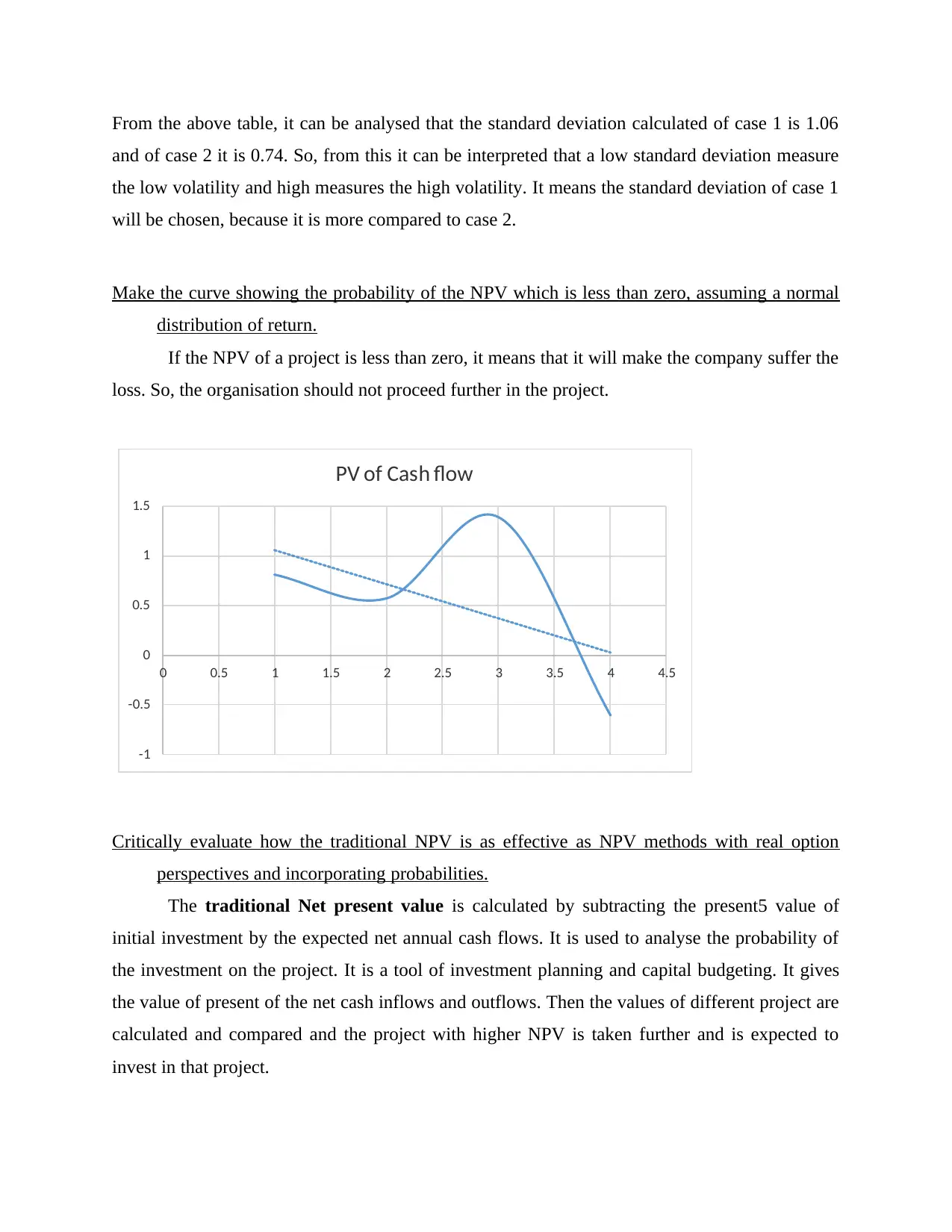

Make the curve showing the probability of the NPV which is less than zero, assuming a normal

distribution of return.

If the NPV of a project is less than zero, it means that it will make the company suffer the

loss. So, the organisation should not proceed further in the project.

-1

-0.5

0

0.5

1

1.5

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

PV of Cash flow

Critically evaluate how the traditional NPV is as effective as NPV methods with real option

perspectives and incorporating probabilities.

The traditional Net present value is calculated by subtracting the present5 value of

initial investment by the expected net annual cash flows. It is used to analyse the probability of

the investment on the project. It is a tool of investment planning and capital budgeting. It gives

the value of present of the net cash inflows and outflows. Then the values of different project are

calculated and compared and the project with higher NPV is taken further and is expected to

invest in that project.

and of case 2 it is 0.74. So, from this it can be interpreted that a low standard deviation measure

the low volatility and high measures the high volatility. It means the standard deviation of case 1

will be chosen, because it is more compared to case 2.

Make the curve showing the probability of the NPV which is less than zero, assuming a normal

distribution of return.

If the NPV of a project is less than zero, it means that it will make the company suffer the

loss. So, the organisation should not proceed further in the project.

-1

-0.5

0

0.5

1

1.5

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

PV of Cash flow

Critically evaluate how the traditional NPV is as effective as NPV methods with real option

perspectives and incorporating probabilities.

The traditional Net present value is calculated by subtracting the present5 value of

initial investment by the expected net annual cash flows. It is used to analyse the probability of

the investment on the project. It is a tool of investment planning and capital budgeting. It gives

the value of present of the net cash inflows and outflows. Then the values of different project are

calculated and compared and the project with higher NPV is taken further and is expected to

invest in that project.

1. It gives the flexibility to the management to react on the changing conditions of the

business and project.

2. In this approach, different NPV's can be added of multiple projects and can calculate the

aggregate value of the investable projects.

3. IT recognizes the time value of the money and gives an analysis for the long – term.

4. It is more easy to calculate than the real option approach (Lizares and Bautista, 2021) .

Real option Approach given an analysis of the capital investment project by accepting and

rejecting the projects on the basis of its probabilities and expected returns. It gives the flexibility

to the management and gives a strategic value of entry and exit of the project. It is effective as

the traditional method. It gives the real strategic approach of the project. It is a complex method

to understand but then it is easy to evaluate. Because the projects which have the less chances of

generating the return will be rejected and more will be accepted. So, the time of calculating the

NPV of useless project will be saved. In this technique also the NPV is calculated on the basis of

discounting factor.

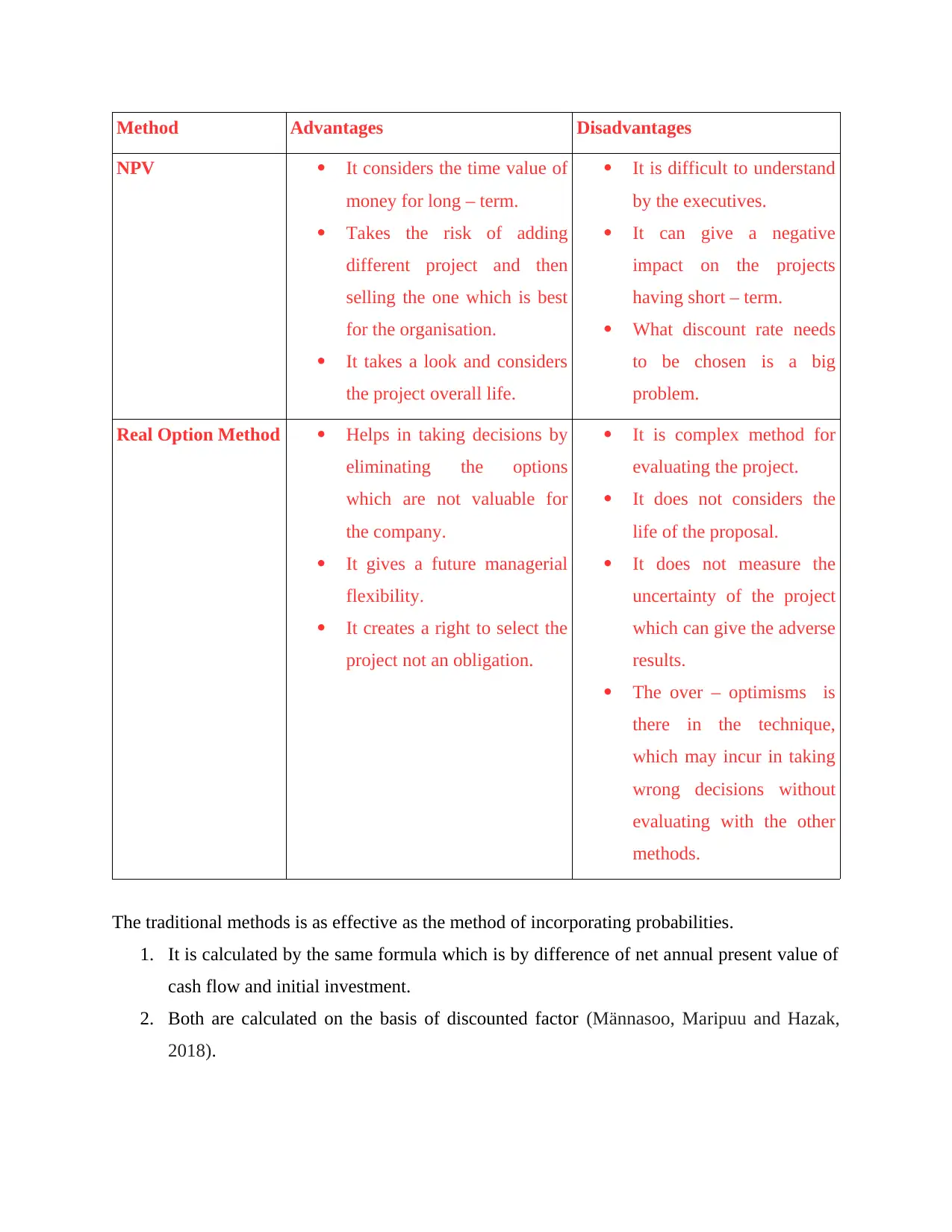

Pros and Cons of Traditional NPV

business and project.

2. In this approach, different NPV's can be added of multiple projects and can calculate the

aggregate value of the investable projects.

3. IT recognizes the time value of the money and gives an analysis for the long – term.

4. It is more easy to calculate than the real option approach (Lizares and Bautista, 2021) .

Real option Approach given an analysis of the capital investment project by accepting and

rejecting the projects on the basis of its probabilities and expected returns. It gives the flexibility

to the management and gives a strategic value of entry and exit of the project. It is effective as

the traditional method. It gives the real strategic approach of the project. It is a complex method

to understand but then it is easy to evaluate. Because the projects which have the less chances of

generating the return will be rejected and more will be accepted. So, the time of calculating the

NPV of useless project will be saved. In this technique also the NPV is calculated on the basis of

discounting factor.

Pros and Cons of Traditional NPV

Method Advantages Disadvantages

NPV It considers the time value of

money for long – term.

Takes the risk of adding

different project and then

selling the one which is best

for the organisation.

It takes a look and considers

the project overall life.

It is difficult to understand

by the executives.

It can give a negative

impact on the projects

having short – term.

What discount rate needs

to be chosen is a big

problem.

Real Option Method Helps in taking decisions by

eliminating the options

which are not valuable for

the company.

It gives a future managerial

flexibility.

It creates a right to select the

project not an obligation.

It is complex method for

evaluating the project.

It does not considers the

life of the proposal.

It does not measure the

uncertainty of the project

which can give the adverse

results.

The over – optimisms is

there in the technique,

which may incur in taking

wrong decisions without

evaluating with the other

methods.

The traditional methods is as effective as the method of incorporating probabilities.

1. It is calculated by the same formula which is by difference of net annual present value of

cash flow and initial investment.

2. Both are calculated on the basis of discounted factor (Männasoo, Maripuu and Hazak,

2018).

NPV It considers the time value of

money for long – term.

Takes the risk of adding

different project and then

selling the one which is best

for the organisation.

It takes a look and considers

the project overall life.

It is difficult to understand

by the executives.

It can give a negative

impact on the projects

having short – term.

What discount rate needs

to be chosen is a big

problem.

Real Option Method Helps in taking decisions by

eliminating the options

which are not valuable for

the company.

It gives a future managerial

flexibility.

It creates a right to select the

project not an obligation.

It is complex method for

evaluating the project.

It does not considers the

life of the proposal.

It does not measure the

uncertainty of the project

which can give the adverse

results.

The over – optimisms is

there in the technique,

which may incur in taking

wrong decisions without

evaluating with the other

methods.

The traditional methods is as effective as the method of incorporating probabilities.

1. It is calculated by the same formula which is by difference of net annual present value of

cash flow and initial investment.

2. Both are calculated on the basis of discounted factor (Männasoo, Maripuu and Hazak,

2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above reasons, it can be evaluated that the above reasons, that the the traditional

method of NPV is as affective as the real option approach.

CONCLUSION

From the above analysis, it can be concluded that individuals must opt for adopting the

technique of differentiation while making any type of investment. This means that they should

never rely on single large investment or investing in same type of format always, but should opt

of multiple number of options for investing their amount. This will help in reducing the risk of

loss and market failure and will also safeguard the amount invested in different schemes. It can

be the bonds, shares or debentures. The private pension policy is also a good format available for

employees to make secure investment which can be used by them in future or old age.

Acquisition of companies is also one of its format through which the value of firm and its capital

structure can be improved. But these acquisitions must be made by checking out its net present

value, either by probability method or by probability. Both the manners are normally the same,

but with just a minor difference of elimination of profits from it.

method of NPV is as affective as the real option approach.

CONCLUSION

From the above analysis, it can be concluded that individuals must opt for adopting the

technique of differentiation while making any type of investment. This means that they should

never rely on single large investment or investing in same type of format always, but should opt

of multiple number of options for investing their amount. This will help in reducing the risk of

loss and market failure and will also safeguard the amount invested in different schemes. It can

be the bonds, shares or debentures. The private pension policy is also a good format available for

employees to make secure investment which can be used by them in future or old age.

Acquisition of companies is also one of its format through which the value of firm and its capital

structure can be improved. But these acquisitions must be made by checking out its net present

value, either by probability method or by probability. Both the manners are normally the same,

but with just a minor difference of elimination of profits from it.

REFERENCES

Books and Journals

Agyei-Mensah, B. K., 2018. Impact of corporate governance attributes and financial reporting

lag on corporate financial performance. African Journal of Economic and Management

Studies.

Brigham, E. F. and Houston, J. F., 2021. Fundamentals of financial management: Concise.

Cengage Learning.

Dalal, K. K. and Thaker, N., 2019. ESG and corporate financial performance: A panel study of

Indian companies. IUP Journal of Corporate Governance. 18(1). pp.44-59.

Giosi, A. and Caiffa, M., 2020. Political connections, media impact and state-owned enterprises:

an empirical analysis on corporate financial performance. Journal of Public Budgeting,

Accounting & Financial Management.

Golden, J., 2021. Local crime environment and corporate financial misconduct using Benford’s

law. Journal of Forensic Accounting Research.

Gras, D. and Krause, R., 2020. When does it pay to stand out as stand-up? Competitive

contingencies in the corporate social performance–corporate financial performance

relationship. Strategic Organization. 18(3). pp.448-471.

Hutahayan, B., 2020. The mediating role of human capital and management accounting

information system in the relationship between innovation strategy and internal process

performance and the impact on corporate financial performance. Benchmarking: An

International Journal.

Landi, G. and Sciarelli, M., 2019. Towards a more ethical market: the impact of ESG rating on

corporate financial performance. Social Responsibility Journal.

Lizares, R. M. and Bautista, C. C., 2021. Corporate financial distress: The case of publicly listed

firms in an emerging market economy. Journal of International Financial Management

& Accounting. 32(1). pp.5-20.

Männasoo, K., Maripuu, P. and Hazak, A., 2018. Investments, credit, and corporate financial

distress: Evidence from Central and Eastern Europe. Emerging Markets Finance and

Trade. 54(3). pp.677-689.

Books and Journals

Agyei-Mensah, B. K., 2018. Impact of corporate governance attributes and financial reporting

lag on corporate financial performance. African Journal of Economic and Management

Studies.

Brigham, E. F. and Houston, J. F., 2021. Fundamentals of financial management: Concise.

Cengage Learning.

Dalal, K. K. and Thaker, N., 2019. ESG and corporate financial performance: A panel study of

Indian companies. IUP Journal of Corporate Governance. 18(1). pp.44-59.

Giosi, A. and Caiffa, M., 2020. Political connections, media impact and state-owned enterprises:

an empirical analysis on corporate financial performance. Journal of Public Budgeting,

Accounting & Financial Management.

Golden, J., 2021. Local crime environment and corporate financial misconduct using Benford’s

law. Journal of Forensic Accounting Research.

Gras, D. and Krause, R., 2020. When does it pay to stand out as stand-up? Competitive

contingencies in the corporate social performance–corporate financial performance

relationship. Strategic Organization. 18(3). pp.448-471.

Hutahayan, B., 2020. The mediating role of human capital and management accounting

information system in the relationship between innovation strategy and internal process

performance and the impact on corporate financial performance. Benchmarking: An

International Journal.

Landi, G. and Sciarelli, M., 2019. Towards a more ethical market: the impact of ESG rating on

corporate financial performance. Social Responsibility Journal.

Lizares, R. M. and Bautista, C. C., 2021. Corporate financial distress: The case of publicly listed

firms in an emerging market economy. Journal of International Financial Management

& Accounting. 32(1). pp.5-20.

Männasoo, K., Maripuu, P. and Hazak, A., 2018. Investments, credit, and corporate financial

distress: Evidence from Central and Eastern Europe. Emerging Markets Finance and

Trade. 54(3). pp.677-689.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.