Corporate Financial Management Project: NPV, CAPM, APT, and Mergers

VerifiedAdded on 2020/05/28

|10

|2161

|33

Project

AI Summary

This project provides a detailed analysis of corporate financial management, encompassing the calculation of Net Present Value (NPV) for a capital investment project, comparing the Capital Asset Pricing Model (CAPM) and Arbitrage Pricing Model (APT), and examining mergers and acquisition...

CORPORATE FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Solution 1:.............................................................................................................................................3

Solution 2:.............................................................................................................................................5

References...........................................................................................................................................10

Solution 1:.............................................................................................................................................3

Solution 2:.............................................................................................................................................5

References...........................................................................................................................................10

Solution 1:

Part a.

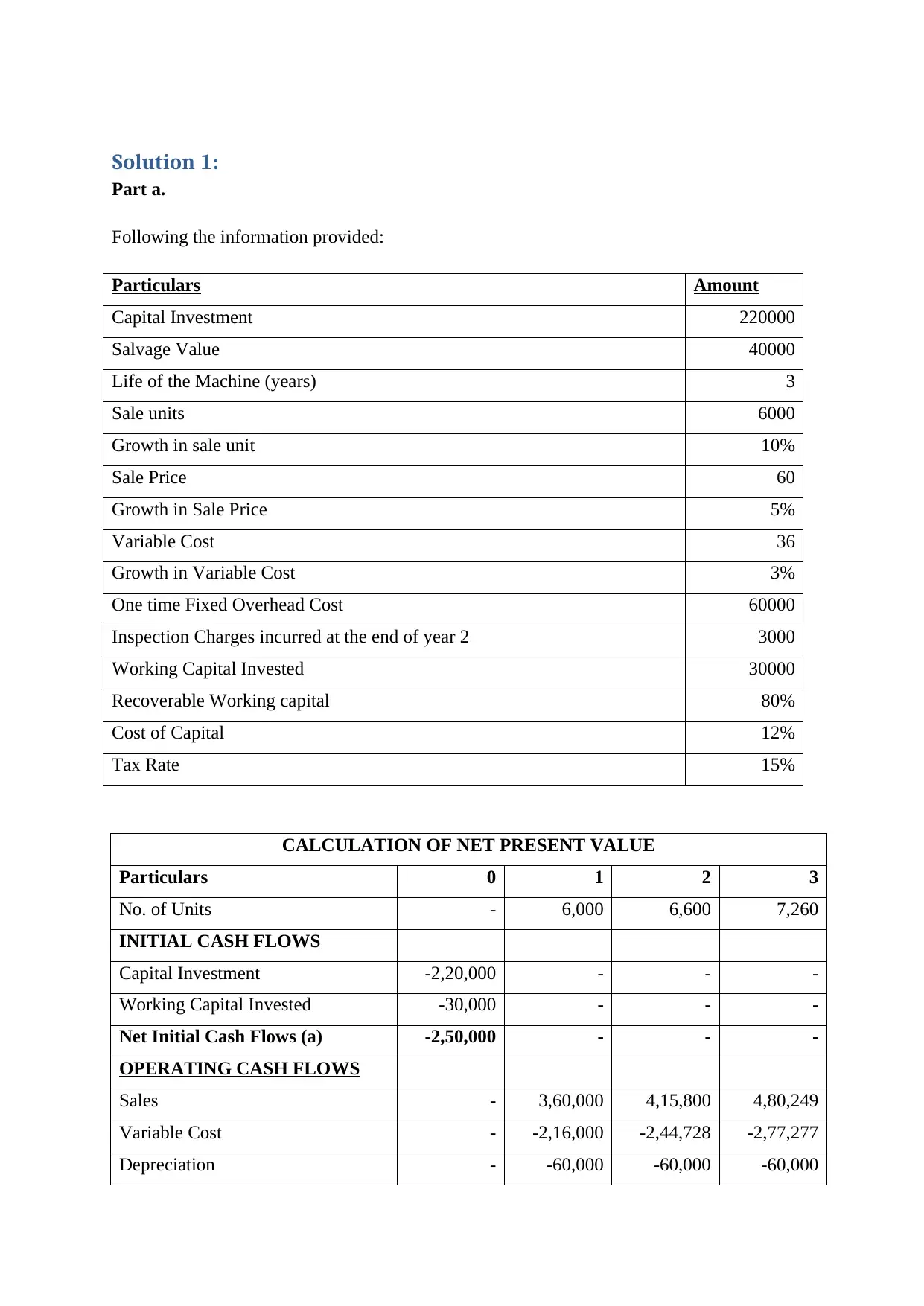

Following the information provided:

Particulars Amount

Capital Investment 220000

Salvage Value 40000

Life of the Machine (years) 3

Sale units 6000

Growth in sale unit 10%

Sale Price 60

Growth in Sale Price 5%

Variable Cost 36

Growth in Variable Cost 3%

One time Fixed Overhead Cost 60000

Inspection Charges incurred at the end of year 2 3000

Working Capital Invested 30000

Recoverable Working capital 80%

Cost of Capital 12%

Tax Rate 15%

CALCULATION OF NET PRESENT VALUE

Particulars 0 1 2 3

No. of Units - 6,000 6,600 7,260

INITIAL CASH FLOWS

Capital Investment -2,20,000 - - -

Working Capital Invested -30,000 - - -

Net Initial Cash Flows (a) -2,50,000 - - -

OPERATING CASH FLOWS

Sales - 3,60,000 4,15,800 4,80,249

Variable Cost - -2,16,000 -2,44,728 -2,77,277

Depreciation - -60,000 -60,000 -60,000

Part a.

Following the information provided:

Particulars Amount

Capital Investment 220000

Salvage Value 40000

Life of the Machine (years) 3

Sale units 6000

Growth in sale unit 10%

Sale Price 60

Growth in Sale Price 5%

Variable Cost 36

Growth in Variable Cost 3%

One time Fixed Overhead Cost 60000

Inspection Charges incurred at the end of year 2 3000

Working Capital Invested 30000

Recoverable Working capital 80%

Cost of Capital 12%

Tax Rate 15%

CALCULATION OF NET PRESENT VALUE

Particulars 0 1 2 3

No. of Units - 6,000 6,600 7,260

INITIAL CASH FLOWS

Capital Investment -2,20,000 - - -

Working Capital Invested -30,000 - - -

Net Initial Cash Flows (a) -2,50,000 - - -

OPERATING CASH FLOWS

Sales - 3,60,000 4,15,800 4,80,249

Variable Cost - -2,16,000 -2,44,728 -2,77,277

Depreciation - -60,000 -60,000 -60,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

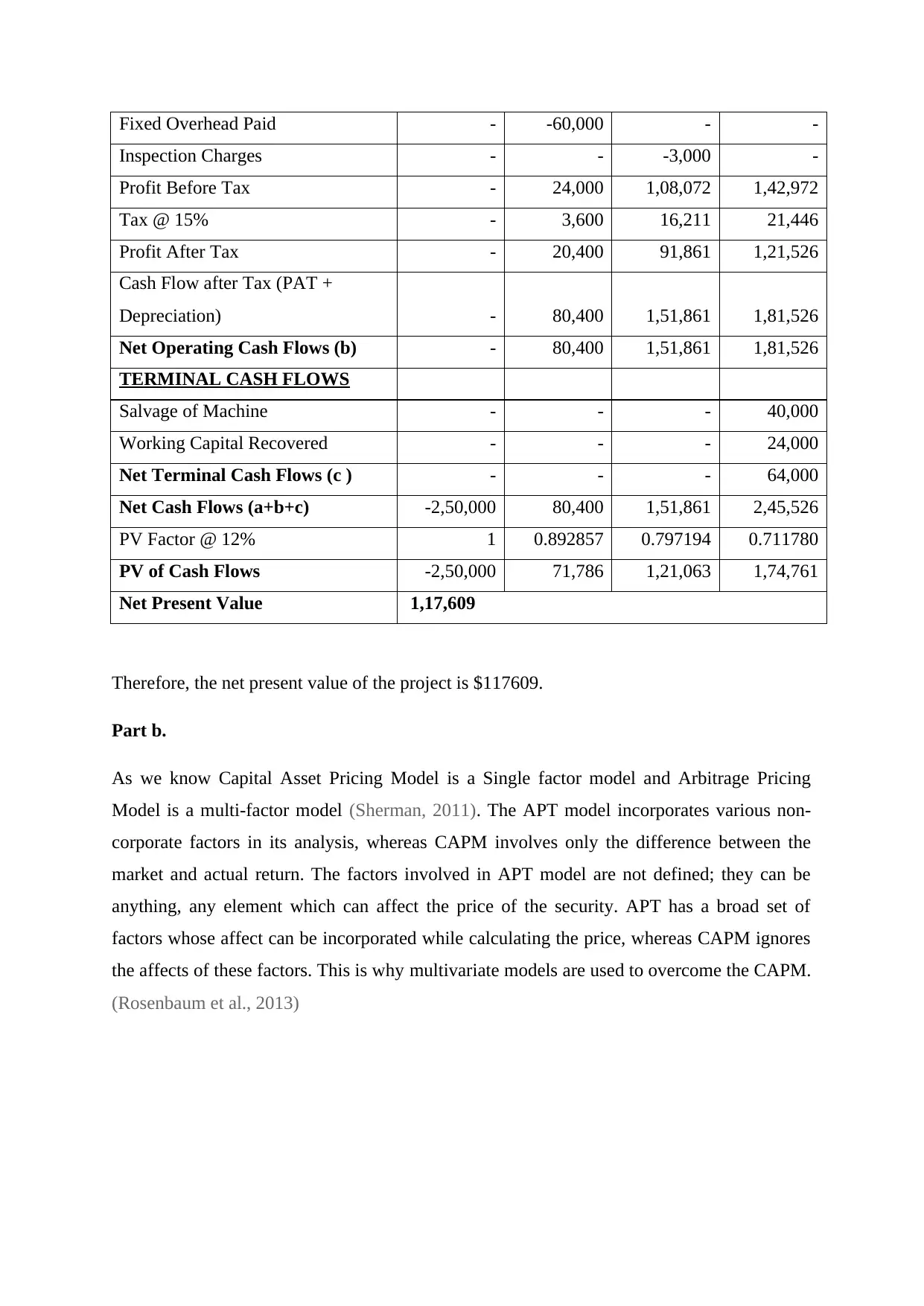

Fixed Overhead Paid - -60,000 - -

Inspection Charges - - -3,000 -

Profit Before Tax - 24,000 1,08,072 1,42,972

Tax @ 15% - 3,600 16,211 21,446

Profit After Tax - 20,400 91,861 1,21,526

Cash Flow after Tax (PAT +

Depreciation) - 80,400 1,51,861 1,81,526

Net Operating Cash Flows (b) - 80,400 1,51,861 1,81,526

TERMINAL CASH FLOWS

Salvage of Machine - - - 40,000

Working Capital Recovered - - - 24,000

Net Terminal Cash Flows (c ) - - - 64,000

Net Cash Flows (a+b+c) -2,50,000 80,400 1,51,861 2,45,526

PV Factor @ 12% 1 0.892857 0.797194 0.711780

PV of Cash Flows -2,50,000 71,786 1,21,063 1,74,761

Net Present Value 1,17,609

Therefore, the net present value of the project is $117609.

Part b.

As we know Capital Asset Pricing Model is a Single factor model and Arbitrage Pricing

Model is a multi-factor model (Sherman, 2011). The APT model incorporates various non-

corporate factors in its analysis, whereas CAPM involves only the difference between the

market and actual return. The factors involved in APT model are not defined; they can be

anything, any element which can affect the price of the security. APT has a broad set of

factors whose affect can be incorporated while calculating the price, whereas CAPM ignores

the affects of these factors. This is why multivariate models are used to overcome the CAPM.

(Rosenbaum et al., 2013)

Inspection Charges - - -3,000 -

Profit Before Tax - 24,000 1,08,072 1,42,972

Tax @ 15% - 3,600 16,211 21,446

Profit After Tax - 20,400 91,861 1,21,526

Cash Flow after Tax (PAT +

Depreciation) - 80,400 1,51,861 1,81,526

Net Operating Cash Flows (b) - 80,400 1,51,861 1,81,526

TERMINAL CASH FLOWS

Salvage of Machine - - - 40,000

Working Capital Recovered - - - 24,000

Net Terminal Cash Flows (c ) - - - 64,000

Net Cash Flows (a+b+c) -2,50,000 80,400 1,51,861 2,45,526

PV Factor @ 12% 1 0.892857 0.797194 0.711780

PV of Cash Flows -2,50,000 71,786 1,21,063 1,74,761

Net Present Value 1,17,609

Therefore, the net present value of the project is $117609.

Part b.

As we know Capital Asset Pricing Model is a Single factor model and Arbitrage Pricing

Model is a multi-factor model (Sherman, 2011). The APT model incorporates various non-

corporate factors in its analysis, whereas CAPM involves only the difference between the

market and actual return. The factors involved in APT model are not defined; they can be

anything, any element which can affect the price of the security. APT has a broad set of

factors whose affect can be incorporated while calculating the price, whereas CAPM ignores

the affects of these factors. This is why multivariate models are used to overcome the CAPM.

(Rosenbaum et al., 2013)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Solution 2:

Part a:

Mergers and acquisition is an organic growth strategy which is opted by the corporate. The

organic growth strategies such as internal expansion are a tad complicated procedure, but

merger takes less time (Snow, 2011). Though the process of merger is less time consuming, it

is expensive, as the acquirer firm is required to pay a premium to the acquired firm. The

management of the acquired firm is responsible to justify and explain the need for premium.

Mostly, the premium involved in mergers is due to synergies created.

As discussed the process of merger is expensive, but still people go for it because it has many

advantages. The process of merger brings together the strengths of entities promoting higher

growth. It also helps to create monopoly, which results in decreased competition and better

bargaining position. There are a lot of rules and regulations which in some cases can be

fulfilled by collaborations only, therefore mergers helps to satisfy these also. In the process of

merger one non-branded partner may get recognition by merging with a branded entity,

creating recognition of the former entity. Last but not the least the process of merger helps to

create synergy. Synergy is the extra value which is created by merging of two or more

entities. Merger helps to strengthen the entity by utilising the positive attributes and reducing

the negative. This results in better operating and financial environment for the entity to work

in and hence results in synergy creation.

Synergy is the potential or additional value that is expected to be generated as a result of the

merger. It is the most used rationale for the purpose of analysing a merger plan. But lack of

information and improper application of synergy calculations may lead to wrong conclusions.

(Bainbridge, 2012)

Few of the major reasons why synergy is generated are listed below:

- Economies of Scale: Due to large scale production as a result of merger, the cost per unit

declines, resulting in economies of scale.

- Better Pricing Power: Since the merged entity now has more resources and more

market share, it will be in a better position to enjoy the pricing power in the market.

Part a:

Mergers and acquisition is an organic growth strategy which is opted by the corporate. The

organic growth strategies such as internal expansion are a tad complicated procedure, but

merger takes less time (Snow, 2011). Though the process of merger is less time consuming, it

is expensive, as the acquirer firm is required to pay a premium to the acquired firm. The

management of the acquired firm is responsible to justify and explain the need for premium.

Mostly, the premium involved in mergers is due to synergies created.

As discussed the process of merger is expensive, but still people go for it because it has many

advantages. The process of merger brings together the strengths of entities promoting higher

growth. It also helps to create monopoly, which results in decreased competition and better

bargaining position. There are a lot of rules and regulations which in some cases can be

fulfilled by collaborations only, therefore mergers helps to satisfy these also. In the process of

merger one non-branded partner may get recognition by merging with a branded entity,

creating recognition of the former entity. Last but not the least the process of merger helps to

create synergy. Synergy is the extra value which is created by merging of two or more

entities. Merger helps to strengthen the entity by utilising the positive attributes and reducing

the negative. This results in better operating and financial environment for the entity to work

in and hence results in synergy creation.

Synergy is the potential or additional value that is expected to be generated as a result of the

merger. It is the most used rationale for the purpose of analysing a merger plan. But lack of

information and improper application of synergy calculations may lead to wrong conclusions.

(Bainbridge, 2012)

Few of the major reasons why synergy is generated are listed below:

- Economies of Scale: Due to large scale production as a result of merger, the cost per unit

declines, resulting in economies of scale.

- Better Pricing Power: Since the merged entity now has more resources and more

market share, it will be in a better position to enjoy the pricing power in the market.

- Complimentary Resources: where a big innovative firm with ample of resources

merges with a small firm with very limited resources, then the small firm enjoys the

resources which was not yet available to them.

- Utilisation of surplus funds: the funds which are idle and not being used can be used to

complete the buy-out in a merger, providing greater returns,

- Tax Benefits: whereby in the process of merger a profit making company acquires a loss

making company in order to generate tax shield, then the tax benefits can be availed by

the merger entity.

- Managerial Efficiency: there is a probability that the acquired firm would have been

mismanaged, after the completion of merger, better expertise and managerial efficiency

of the acquiring company, helps to manage the acquired company. (Filippell, 2011)

Mergers are also of various types. They have been discussed as below:

- Horizontal Merger: These types of merger take between the companies which belonh to

same industry and are at the same stage.

- Vertical Merger: this type of merger takes place between the companies which belong

to same industry but different stages. For example, an oil refilling company merging with

a company involved in the business of oil marketing.

- Concentric Merger: this type of merger takes place between companies belonging to

related industries. For example, a banking company merging with a insurance company.

- Conglomerate Merger: this type of merger takes place between companies of totally

different industries.

Synergy can be of various types too. In a merger, benefit generated in any area will be

termed as synergy. Synergies can be of following types:

- Cost savings synergy: we have already discussed above how economies of scale can be

achieved form the process of merger. Due to economies of scale the cost per unit

declines. Decrease in the cost results in higher revenue and profits which then results in

higher market value of the company. Hence generating synergy for the newly formed

entity.

- Revenue Synergies: revenue synergies are increase in revenue for the merged entities.

The revenue generated by the merged entity is more than the revenue individually

generated the participating entities. In our discussion below we will see a practical

example of how two merged entities have resulted in revenue synergies. The merged

merges with a small firm with very limited resources, then the small firm enjoys the

resources which was not yet available to them.

- Utilisation of surplus funds: the funds which are idle and not being used can be used to

complete the buy-out in a merger, providing greater returns,

- Tax Benefits: whereby in the process of merger a profit making company acquires a loss

making company in order to generate tax shield, then the tax benefits can be availed by

the merger entity.

- Managerial Efficiency: there is a probability that the acquired firm would have been

mismanaged, after the completion of merger, better expertise and managerial efficiency

of the acquiring company, helps to manage the acquired company. (Filippell, 2011)

Mergers are also of various types. They have been discussed as below:

- Horizontal Merger: These types of merger take between the companies which belonh to

same industry and are at the same stage.

- Vertical Merger: this type of merger takes place between the companies which belong

to same industry but different stages. For example, an oil refilling company merging with

a company involved in the business of oil marketing.

- Concentric Merger: this type of merger takes place between companies belonging to

related industries. For example, a banking company merging with a insurance company.

- Conglomerate Merger: this type of merger takes place between companies of totally

different industries.

Synergy can be of various types too. In a merger, benefit generated in any area will be

termed as synergy. Synergies can be of following types:

- Cost savings synergy: we have already discussed above how economies of scale can be

achieved form the process of merger. Due to economies of scale the cost per unit

declines. Decrease in the cost results in higher revenue and profits which then results in

higher market value of the company. Hence generating synergy for the newly formed

entity.

- Revenue Synergies: revenue synergies are increase in revenue for the merged entities.

The revenue generated by the merged entity is more than the revenue individually

generated the participating entities. In our discussion below we will see a practical

example of how two merged entities have resulted in revenue synergies. The merged

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

entities have more resources which are put to use more efficiently which results in these

types of synergies. (Harrison, n.d.)

- Market value synergies: this is due to boot strap effect. Under this type of synergies the

market capitalization of merged entities is much more than the market cap of individual

participating entities. Difference between these figures is the amount of synergy created

form merger.

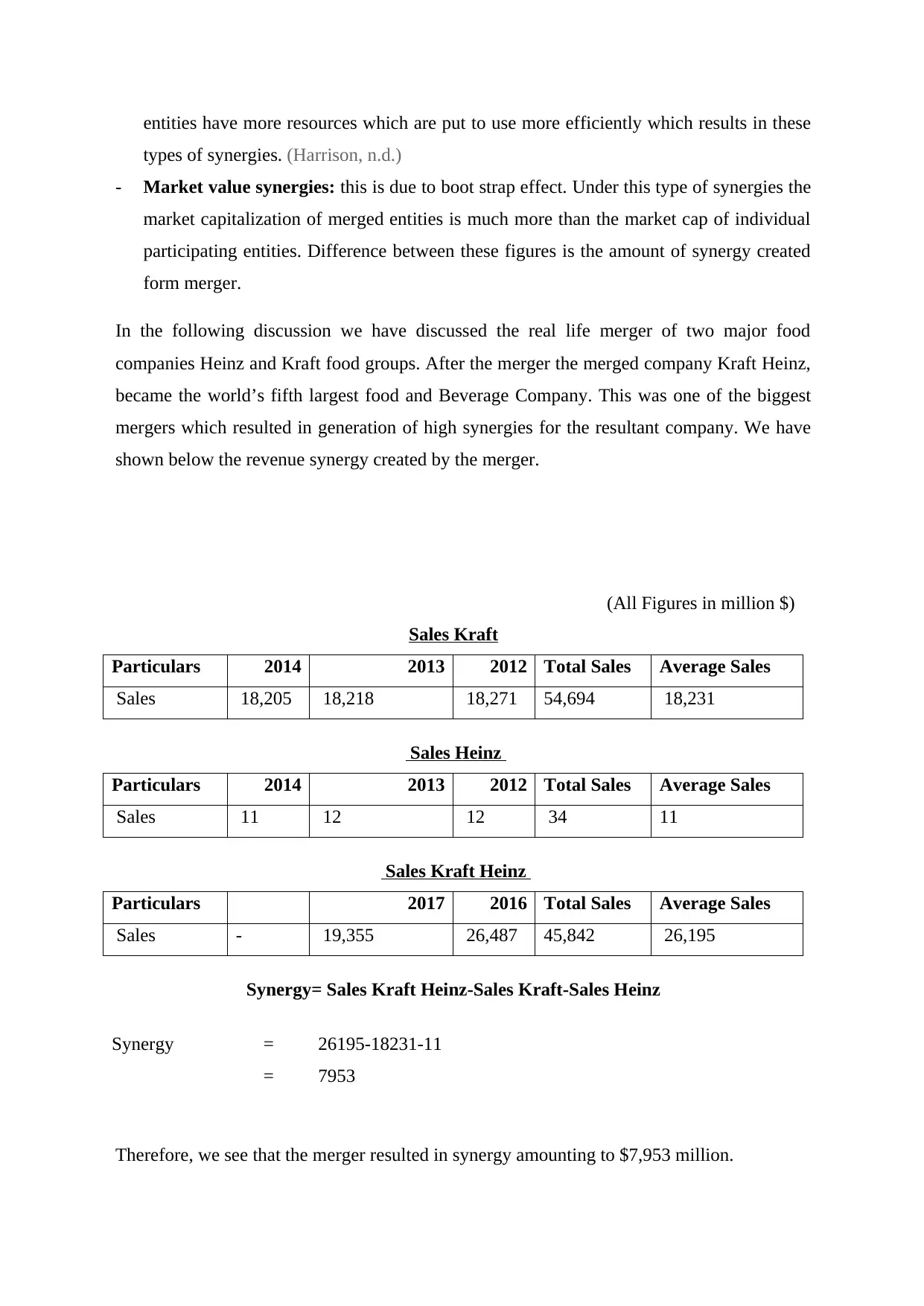

In the following discussion we have discussed the real life merger of two major food

companies Heinz and Kraft food groups. After the merger the merged company Kraft Heinz,

became the world’s fifth largest food and Beverage Company. This was one of the biggest

mergers which resulted in generation of high synergies for the resultant company. We have

shown below the revenue synergy created by the merger.

(All Figures in million $)

Sales Kraft

Particulars 2014 2013 2012 Total Sales Average Sales

Sales 18,205 18,218 18,271 54,694 18,231

Sales Heinz

Particulars 2014 2013 2012 Total Sales Average Sales

Sales 11 12 12 34 11

Sales Kraft Heinz

Particulars 2017 2016 Total Sales Average Sales

Sales - 19,355 26,487 45,842 26,195

Synergy= Sales Kraft Heinz-Sales Kraft-Sales Heinz

Synergy = 26195-18231-11

= 7953

Therefore, we see that the merger resulted in synergy amounting to $7,953 million.

types of synergies. (Harrison, n.d.)

- Market value synergies: this is due to boot strap effect. Under this type of synergies the

market capitalization of merged entities is much more than the market cap of individual

participating entities. Difference between these figures is the amount of synergy created

form merger.

In the following discussion we have discussed the real life merger of two major food

companies Heinz and Kraft food groups. After the merger the merged company Kraft Heinz,

became the world’s fifth largest food and Beverage Company. This was one of the biggest

mergers which resulted in generation of high synergies for the resultant company. We have

shown below the revenue synergy created by the merger.

(All Figures in million $)

Sales Kraft

Particulars 2014 2013 2012 Total Sales Average Sales

Sales 18,205 18,218 18,271 54,694 18,231

Sales Heinz

Particulars 2014 2013 2012 Total Sales Average Sales

Sales 11 12 12 34 11

Sales Kraft Heinz

Particulars 2017 2016 Total Sales Average Sales

Sales - 19,355 26,487 45,842 26,195

Synergy= Sales Kraft Heinz-Sales Kraft-Sales Heinz

Synergy = 26195-18231-11

= 7953

Therefore, we see that the merger resulted in synergy amounting to $7,953 million.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Before the merger, 605 of the revenue of Heinz was generated from sales from regions other

the North America, whereas 98% of Kraft revenue was generated from North America.

Therefore merger gave Kraft the scope for expansion in international markets (Galpin and

Herndon, 2014). Also, when the merger was about to take place it was estimated that it

would result in cost savings of $1.5 billion per year. The cost synergies were expected to

realise from economies of scale. The economies of scale would help them have better

bargaining power which will provide them higher operating margin. Also, other cost

reducing strategies were to be implemented in order to achieve cost synergies such as closing

down of inefficient units, reduction in headcount, etc. Therefore, we see that the expected

plan of the management of Kraft came through and helped them realise the revenue synergy

of $ 795 million.

Part b:

We have already discussed that the merger of these two companies resulted in generation of

high synergies for the resulting company. We will now show calculations which will support

the above statement. Also we will prove that the equation of PV (Acquirer) + PV (Target) <

PV (Combined Firm) is being satisfied by the said merger (Halibozek and Kovacich, n.d.).

Below are the figures stating the market price per share of the companies and the number of

shares of the companies before and after merger. The market capitalisations of the companies

are calculated in order to arrive at the present value of the companies before and after

acquisition. All the figures below are in million $ except for share price, which are per unit.

Share price of Kraft

Year Share Price No. of Share

2012 44.15 592.76

2013 53.91 596.23

2014 62.66 587.33

Average Share Price 53.57

Average Number of Shares 592.11

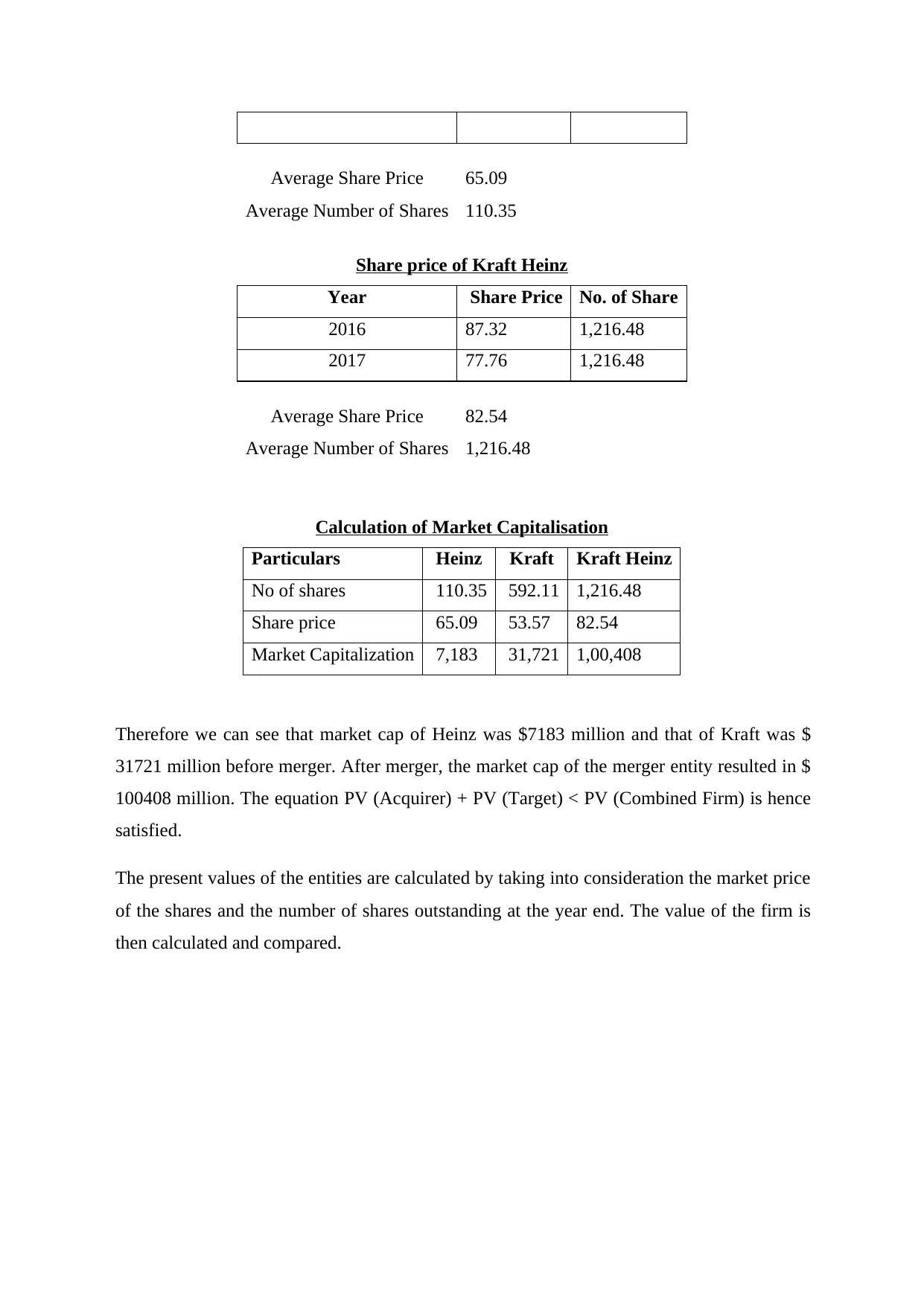

Share price of Heinz

Year Share Price No. of Share

2012 57.68 110.87

2013 72.50 109.83

the North America, whereas 98% of Kraft revenue was generated from North America.

Therefore merger gave Kraft the scope for expansion in international markets (Galpin and

Herndon, 2014). Also, when the merger was about to take place it was estimated that it

would result in cost savings of $1.5 billion per year. The cost synergies were expected to

realise from economies of scale. The economies of scale would help them have better

bargaining power which will provide them higher operating margin. Also, other cost

reducing strategies were to be implemented in order to achieve cost synergies such as closing

down of inefficient units, reduction in headcount, etc. Therefore, we see that the expected

plan of the management of Kraft came through and helped them realise the revenue synergy

of $ 795 million.

Part b:

We have already discussed that the merger of these two companies resulted in generation of

high synergies for the resulting company. We will now show calculations which will support

the above statement. Also we will prove that the equation of PV (Acquirer) + PV (Target) <

PV (Combined Firm) is being satisfied by the said merger (Halibozek and Kovacich, n.d.).

Below are the figures stating the market price per share of the companies and the number of

shares of the companies before and after merger. The market capitalisations of the companies

are calculated in order to arrive at the present value of the companies before and after

acquisition. All the figures below are in million $ except for share price, which are per unit.

Share price of Kraft

Year Share Price No. of Share

2012 44.15 592.76

2013 53.91 596.23

2014 62.66 587.33

Average Share Price 53.57

Average Number of Shares 592.11

Share price of Heinz

Year Share Price No. of Share

2012 57.68 110.87

2013 72.50 109.83

Average Share Price 65.09

Average Number of Shares 110.35

Share price of Kraft Heinz

Year Share Price No. of Share

2016 87.32 1,216.48

2017 77.76 1,216.48

Average Share Price 82.54

Average Number of Shares 1,216.48

Calculation of Market Capitalisation

Particulars Heinz Kraft Kraft Heinz

No of shares 110.35 592.11 1,216.48

Share price 65.09 53.57 82.54

Market Capitalization 7,183 31,721 1,00,408

Therefore we can see that market cap of Heinz was $7183 million and that of Kraft was $

31721 million before merger. After merger, the market cap of the merger entity resulted in $

100408 million. The equation PV (Acquirer) + PV (Target) < PV (Combined Firm) is hence

satisfied.

The present values of the entities are calculated by taking into consideration the market price

of the shares and the number of shares outstanding at the year end. The value of the firm is

then calculated and compared.

Average Number of Shares 110.35

Share price of Kraft Heinz

Year Share Price No. of Share

2016 87.32 1,216.48

2017 77.76 1,216.48

Average Share Price 82.54

Average Number of Shares 1,216.48

Calculation of Market Capitalisation

Particulars Heinz Kraft Kraft Heinz

No of shares 110.35 592.11 1,216.48

Share price 65.09 53.57 82.54

Market Capitalization 7,183 31,721 1,00,408

Therefore we can see that market cap of Heinz was $7183 million and that of Kraft was $

31721 million before merger. After merger, the market cap of the merger entity resulted in $

100408 million. The equation PV (Acquirer) + PV (Target) < PV (Combined Firm) is hence

satisfied.

The present values of the entities are calculated by taking into consideration the market price

of the shares and the number of shares outstanding at the year end. The value of the firm is

then calculated and compared.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Bainbridge, S. (2012). Mergers and acquisitions. New York: Foundation Press.

Filippell, M. (2011). Mergers and Acquisitions Playbook: Lessons from the Middle-Market

Trenches. John Wiley & Sons.

Galpin, T. and Herndon, M. (2014). The complete guide to mergers and acquisitions. San

Francisco, Calif.: Jossey-Bass.

Halibozek, E. and Kovacich, G. (n.d.). Mergers and Acquisitions Security. Burlington:

Elsevier.

Harrison, C. (n.d.). Make the deal.

Rosenbaum, J., Pearl, J., Perella, J. and Harri. (2013). Investment Banking: Valuation,

Leveraged Buyouts, and Mergers & Acquisition. John Wiley & Sons.

Sherman, A. (2011). Mergers & acquisitions from A to Z. New York: Amacom.

Snow, W. (2011). Mergers & Acquisitions For Dummies. John Wiley & Sons.

Bainbridge, S. (2012). Mergers and acquisitions. New York: Foundation Press.

Filippell, M. (2011). Mergers and Acquisitions Playbook: Lessons from the Middle-Market

Trenches. John Wiley & Sons.

Galpin, T. and Herndon, M. (2014). The complete guide to mergers and acquisitions. San

Francisco, Calif.: Jossey-Bass.

Halibozek, E. and Kovacich, G. (n.d.). Mergers and Acquisitions Security. Burlington:

Elsevier.

Harrison, C. (n.d.). Make the deal.

Rosenbaum, J., Pearl, J., Perella, J. and Harri. (2013). Investment Banking: Valuation,

Leveraged Buyouts, and Mergers & Acquisition. John Wiley & Sons.

Sherman, A. (2011). Mergers & acquisitions from A to Z. New York: Amacom.

Snow, W. (2011). Mergers & Acquisitions For Dummies. John Wiley & Sons.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.