Corporate Financial Statement: SML, CML, MVP and CAPM

VerifiedAdded on 2023/06/07

|12

|2867

|289

AI Summary

This report focuses on the various tools of corporate financial management such as security market line (SML), capital market line (CML), capital asset pricing method (CAPM), required rate of return, minimum portfolio variances etc.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Corporate Financial Statement

1

Project Report: Corporate Financial Statement

1

Project Report: Corporate Financial Statement

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Financial Statement

2

Contents

Introduction.......................................................................................................................3

Difference of security market line from capital market line.............................................3

Minimum variance portfolio.............................................................................................5

CAPM...............................................................................................................................7

Conclusion......................................................................................................................10

References.......................................................................................................................11

2

Contents

Introduction.......................................................................................................................3

Difference of security market line from capital market line.............................................3

Minimum variance portfolio.............................................................................................5

CAPM...............................................................................................................................7

Conclusion......................................................................................................................10

References.......................................................................................................................11

Corporate Financial Statement

3

Introduction:

Corporate financial management is a management process which deals with the

different sources to fund the business and improve the capital structure level of the business.

In this management process, the business takes various decisions to improve the value of the

business among the shareholders of the business (Tian & Jiang, 2015). The main objectives

of the corporate financial management are to offer the base to improve the value of the

business in front of the shareholders.

The report focuses on the various tools of corporate financial management such as

security market line (SML), capital market line (CML), capital asset pricing method

(CAPM), required rate of return, minimum portfolio variances etc. All of these tools, their

importance and relevance have been measured in an organization.

Difference of security market line from capital market line:

Security market line (SML) is a graphical representation which is used to represent

the capital asset pricing model (CAPM) such as the risk and return. It describe about the

expected rate of return from the stock of a business along with the systematic risk of the

business. The SML represents about the opportunity cost of an investment. Consequently, the

CML is a line which is used to show about the rate of return along with the risk of a specific

portfolio. The major difference among the SML and CML is how the factors of risk are

measured. In case of CML, the measurement of risk is standard deviation and beta co-

efficient is used in the security market line to measure the risk (Seitzinger et al, 2010). The

capital market line graph depict about the efficient portfolios while the graphs of security

market line brief efficient portfolios and the non efficient portfolios both.

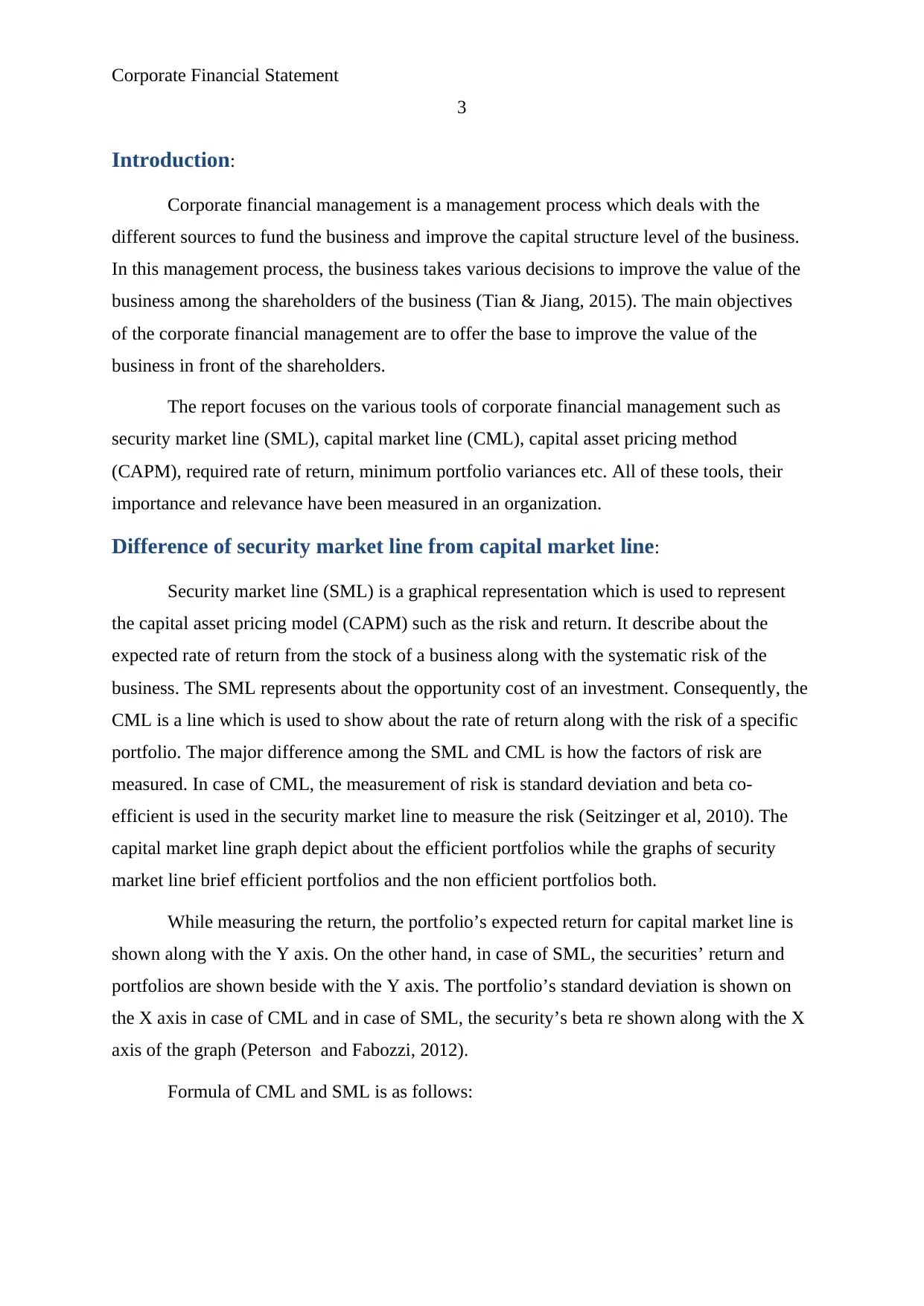

While measuring the return, the portfolio’s expected return for capital market line is

shown along with the Y axis. On the other hand, in case of SML, the securities’ return and

portfolios are shown beside with the Y axis. The portfolio’s standard deviation is shown on

the X axis in case of CML and in case of SML, the security’s beta re shown along with the X

axis of the graph (Peterson and Fabozzi, 2012).

Formula of CML and SML is as follows:

3

Introduction:

Corporate financial management is a management process which deals with the

different sources to fund the business and improve the capital structure level of the business.

In this management process, the business takes various decisions to improve the value of the

business among the shareholders of the business (Tian & Jiang, 2015). The main objectives

of the corporate financial management are to offer the base to improve the value of the

business in front of the shareholders.

The report focuses on the various tools of corporate financial management such as

security market line (SML), capital market line (CML), capital asset pricing method

(CAPM), required rate of return, minimum portfolio variances etc. All of these tools, their

importance and relevance have been measured in an organization.

Difference of security market line from capital market line:

Security market line (SML) is a graphical representation which is used to represent

the capital asset pricing model (CAPM) such as the risk and return. It describe about the

expected rate of return from the stock of a business along with the systematic risk of the

business. The SML represents about the opportunity cost of an investment. Consequently, the

CML is a line which is used to show about the rate of return along with the risk of a specific

portfolio. The major difference among the SML and CML is how the factors of risk are

measured. In case of CML, the measurement of risk is standard deviation and beta co-

efficient is used in the security market line to measure the risk (Seitzinger et al, 2010). The

capital market line graph depict about the efficient portfolios while the graphs of security

market line brief efficient portfolios and the non efficient portfolios both.

While measuring the return, the portfolio’s expected return for capital market line is

shown along with the Y axis. On the other hand, in case of SML, the securities’ return and

portfolios are shown beside with the Y axis. The portfolio’s standard deviation is shown on

the X axis in case of CML and in case of SML, the security’s beta re shown along with the X

axis of the graph (Peterson and Fabozzi, 2012).

Formula of CML and SML is as follows:

Corporate Financial Statement

4

Figure 1: Formula of CML

Required Return (security market line) = Risk Free Rate of Return + Beta (Market Return –

Risk Free Rate of Return)

(Peterson and Fabozzi, 2012)

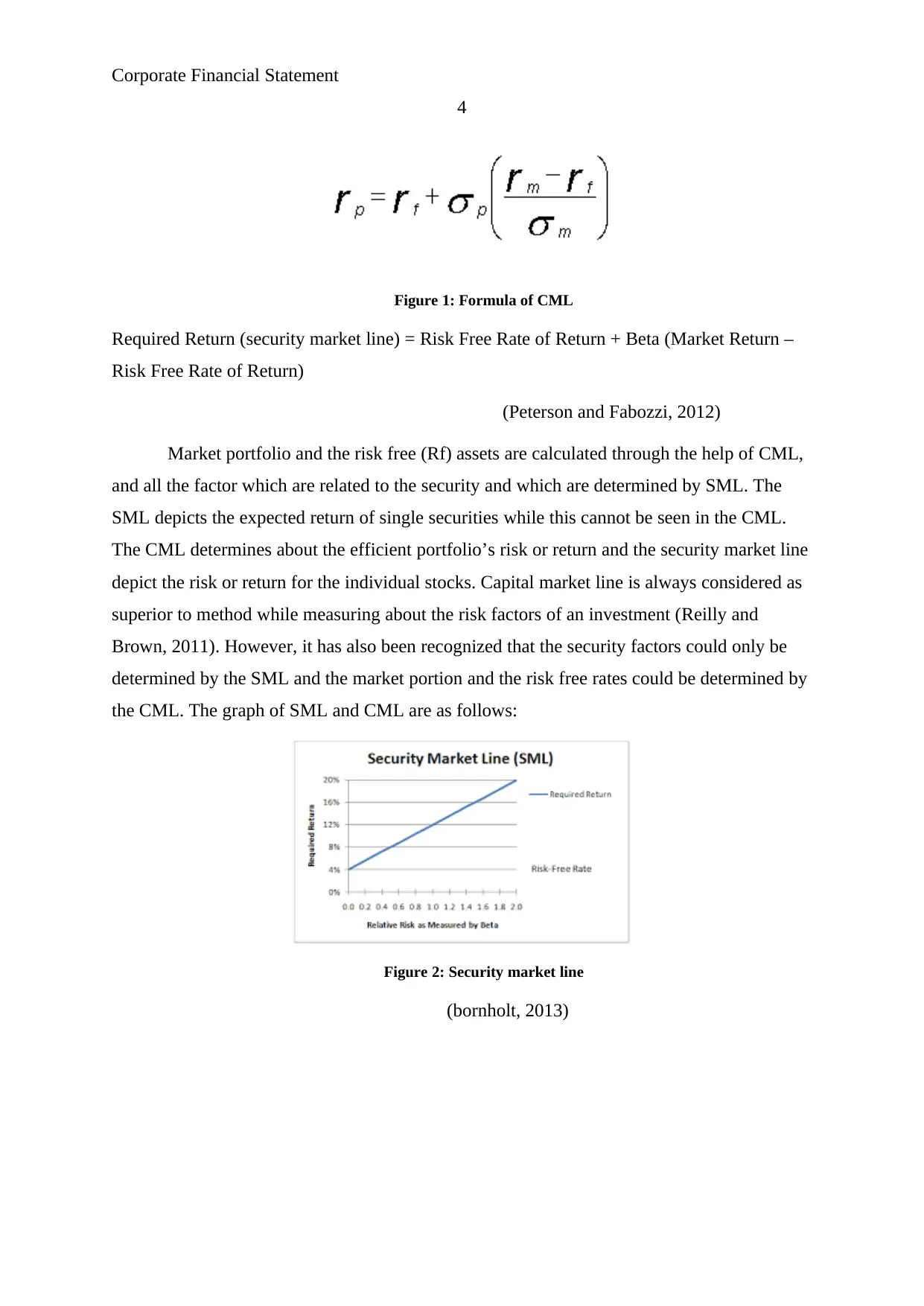

Market portfolio and the risk free (Rf) assets are calculated through the help of CML,

and all the factor which are related to the security and which are determined by SML. The

SML depicts the expected return of single securities while this cannot be seen in the CML.

The CML determines about the efficient portfolio’s risk or return and the security market line

depict the risk or return for the individual stocks. Capital market line is always considered as

superior to method while measuring about the risk factors of an investment (Reilly and

Brown, 2011). However, it has also been recognized that the security factors could only be

determined by the SML and the market portion and the risk free rates could be determined by

the CML. The graph of SML and CML are as follows:

Figure 2: Security market line

(bornholt, 2013)

4

Figure 1: Formula of CML

Required Return (security market line) = Risk Free Rate of Return + Beta (Market Return –

Risk Free Rate of Return)

(Peterson and Fabozzi, 2012)

Market portfolio and the risk free (Rf) assets are calculated through the help of CML,

and all the factor which are related to the security and which are determined by SML. The

SML depicts the expected return of single securities while this cannot be seen in the CML.

The CML determines about the efficient portfolio’s risk or return and the security market line

depict the risk or return for the individual stocks. Capital market line is always considered as

superior to method while measuring about the risk factors of an investment (Reilly and

Brown, 2011). However, it has also been recognized that the security factors could only be

determined by the SML and the market portion and the risk free rates could be determined by

the CML. The graph of SML and CML are as follows:

Figure 2: Security market line

(bornholt, 2013)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Financial Statement

5

Figure 3: Capital market line

(Reilly and Brown, 2011)

The Security market line and capital market line graph explains that there is huge

difference among both the lines. Both of these graphs are prepared and presented by the

financial manager and the financial analyst to evaluate and offer different information about

the investment into the individual security and the portfolio.

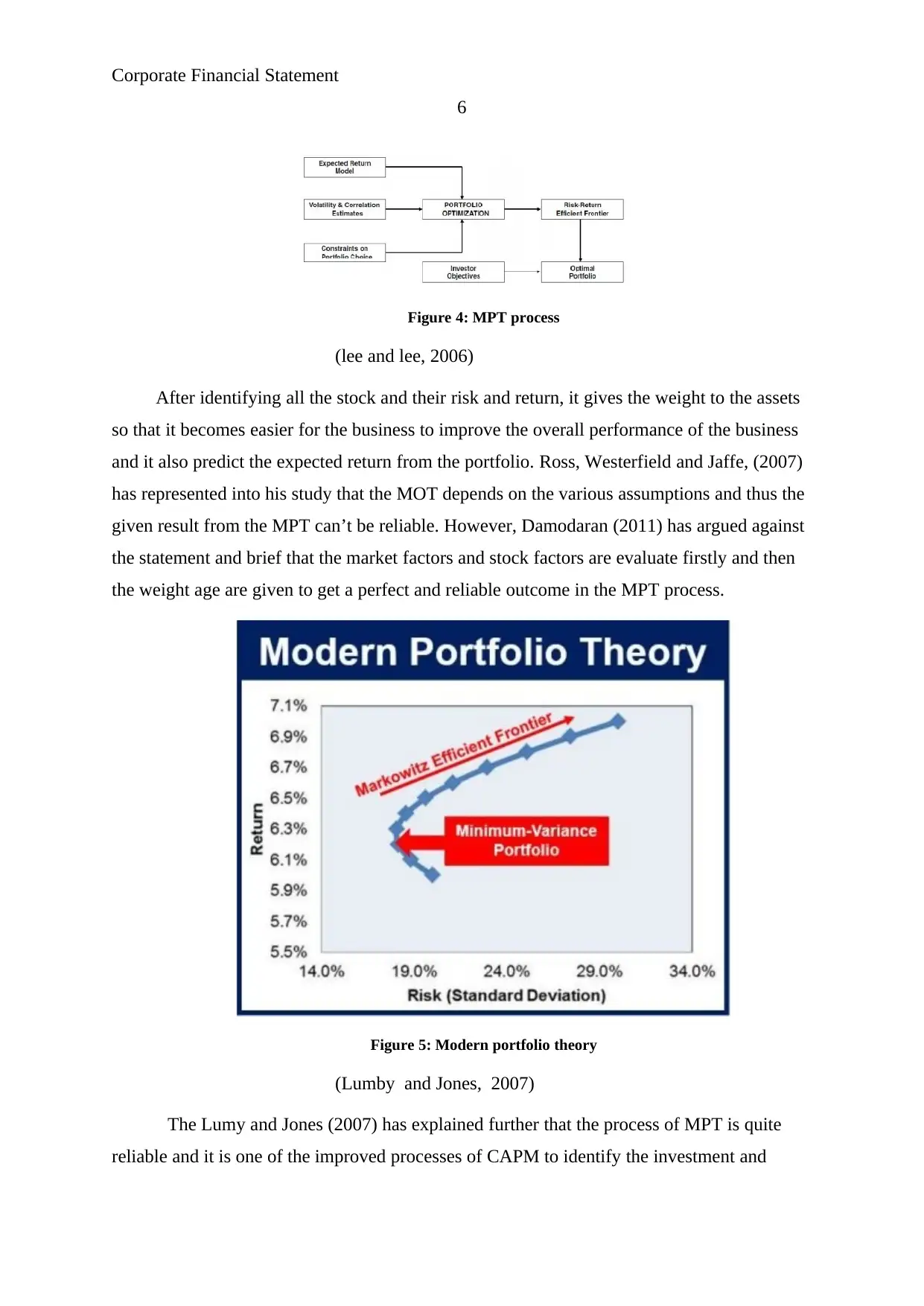

Minimum variance portfolio:

Minimum variance portfolio is the individual risky asset which are taken together in

order to get an outcome in the highest possible risk level against the expected rate return. The

investment into the minimum variance portfolio is individually riskier than the entire

portfolio. Minimum variance portfolio is actually a process which assigns the different

weight to the stocks in such a way that the portfolio risk of the investment could be

minimized. MVP has the lowest risk against the investment into the individual security and it

is independent from the expected return (Ross, Westerfield, Jaffe and Kakani, 2008). Because

of the impact of the diversification, MPT does not take the concern on single security along

with the lowers variance. It takes the concern on various securities which weighted average

variance is lowest. In the process, the first step is to determine the assets which are good

choice for the investment, in the next step, return, volatilities and correlations are calculated

and then the estimates are used to identify the individual security’s performance. The process

of MPT is as follows:

5

Figure 3: Capital market line

(Reilly and Brown, 2011)

The Security market line and capital market line graph explains that there is huge

difference among both the lines. Both of these graphs are prepared and presented by the

financial manager and the financial analyst to evaluate and offer different information about

the investment into the individual security and the portfolio.

Minimum variance portfolio:

Minimum variance portfolio is the individual risky asset which are taken together in

order to get an outcome in the highest possible risk level against the expected rate return. The

investment into the minimum variance portfolio is individually riskier than the entire

portfolio. Minimum variance portfolio is actually a process which assigns the different

weight to the stocks in such a way that the portfolio risk of the investment could be

minimized. MVP has the lowest risk against the investment into the individual security and it

is independent from the expected return (Ross, Westerfield, Jaffe and Kakani, 2008). Because

of the impact of the diversification, MPT does not take the concern on single security along

with the lowers variance. It takes the concern on various securities which weighted average

variance is lowest. In the process, the first step is to determine the assets which are good

choice for the investment, in the next step, return, volatilities and correlations are calculated

and then the estimates are used to identify the individual security’s performance. The process

of MPT is as follows:

Corporate Financial Statement

6

Figure 4: MPT process

(lee and lee, 2006)

After identifying all the stock and their risk and return, it gives the weight to the assets

so that it becomes easier for the business to improve the overall performance of the business

and it also predict the expected return from the portfolio. Ross, Westerfield and Jaffe, (2007)

has represented into his study that the MOT depends on the various assumptions and thus the

given result from the MPT can’t be reliable. However, Damodaran (2011) has argued against

the statement and brief that the market factors and stock factors are evaluate firstly and then

the weight age are given to get a perfect and reliable outcome in the MPT process.

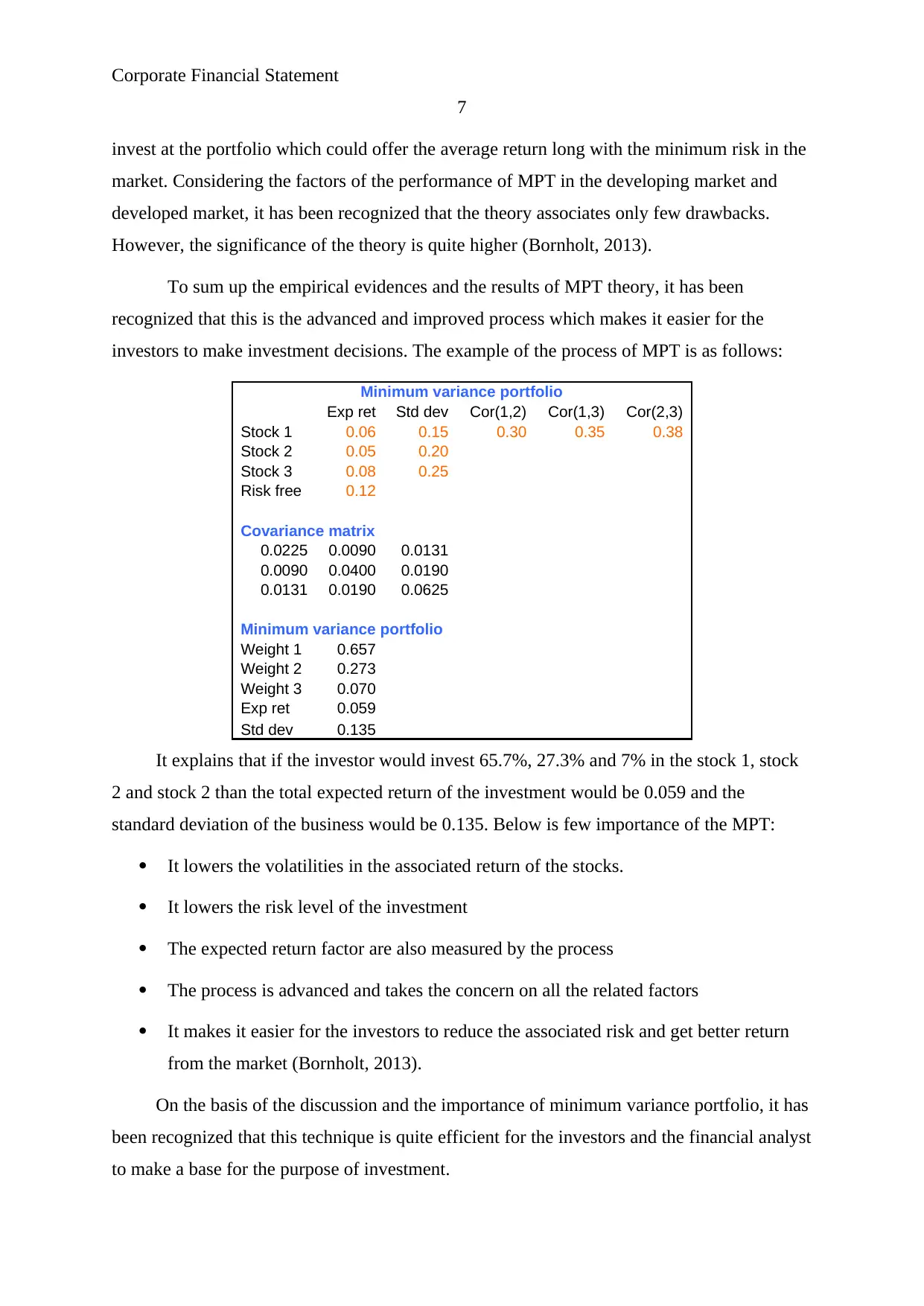

Figure 5: Modern portfolio theory

(Lumby and Jones, 2007)

The Lumy and Jones (2007) has explained further that the process of MPT is quite

reliable and it is one of the improved processes of CAPM to identify the investment and

6

Figure 4: MPT process

(lee and lee, 2006)

After identifying all the stock and their risk and return, it gives the weight to the assets

so that it becomes easier for the business to improve the overall performance of the business

and it also predict the expected return from the portfolio. Ross, Westerfield and Jaffe, (2007)

has represented into his study that the MOT depends on the various assumptions and thus the

given result from the MPT can’t be reliable. However, Damodaran (2011) has argued against

the statement and brief that the market factors and stock factors are evaluate firstly and then

the weight age are given to get a perfect and reliable outcome in the MPT process.

Figure 5: Modern portfolio theory

(Lumby and Jones, 2007)

The Lumy and Jones (2007) has explained further that the process of MPT is quite

reliable and it is one of the improved processes of CAPM to identify the investment and

Corporate Financial Statement

7

invest at the portfolio which could offer the average return long with the minimum risk in the

market. Considering the factors of the performance of MPT in the developing market and

developed market, it has been recognized that the theory associates only few drawbacks.

However, the significance of the theory is quite higher (Bornholt, 2013).

To sum up the empirical evidences and the results of MPT theory, it has been

recognized that this is the advanced and improved process which makes it easier for the

investors to make investment decisions. The example of the process of MPT is as follows:

Minimum variance portfolio

Exp ret Std dev Cor(1,2) Cor(1,3) Cor(2,3)

Stock 1 0.06 0.15 0.30 0.35 0.38

Stock 2 0.05 0.20

Stock 3 0.08 0.25

Risk free 0.12

Covariance matrix

0.0225 0.0090 0.0131

0.0090 0.0400 0.0190

0.0131 0.0190 0.0625

Minimum variance portfolio

Weight 1 0.657

Weight 2 0.273

Weight 3 0.070

Exp ret 0.059

Std dev 0.135

It explains that if the investor would invest 65.7%, 27.3% and 7% in the stock 1, stock

2 and stock 2 than the total expected return of the investment would be 0.059 and the

standard deviation of the business would be 0.135. Below is few importance of the MPT:

It lowers the volatilities in the associated return of the stocks.

It lowers the risk level of the investment

The expected return factor are also measured by the process

The process is advanced and takes the concern on all the related factors

It makes it easier for the investors to reduce the associated risk and get better return

from the market (Bornholt, 2013).

On the basis of the discussion and the importance of minimum variance portfolio, it has

been recognized that this technique is quite efficient for the investors and the financial analyst

to make a base for the purpose of investment.

7

invest at the portfolio which could offer the average return long with the minimum risk in the

market. Considering the factors of the performance of MPT in the developing market and

developed market, it has been recognized that the theory associates only few drawbacks.

However, the significance of the theory is quite higher (Bornholt, 2013).

To sum up the empirical evidences and the results of MPT theory, it has been

recognized that this is the advanced and improved process which makes it easier for the

investors to make investment decisions. The example of the process of MPT is as follows:

Minimum variance portfolio

Exp ret Std dev Cor(1,2) Cor(1,3) Cor(2,3)

Stock 1 0.06 0.15 0.30 0.35 0.38

Stock 2 0.05 0.20

Stock 3 0.08 0.25

Risk free 0.12

Covariance matrix

0.0225 0.0090 0.0131

0.0090 0.0400 0.0190

0.0131 0.0190 0.0625

Minimum variance portfolio

Weight 1 0.657

Weight 2 0.273

Weight 3 0.070

Exp ret 0.059

Std dev 0.135

It explains that if the investor would invest 65.7%, 27.3% and 7% in the stock 1, stock

2 and stock 2 than the total expected return of the investment would be 0.059 and the

standard deviation of the business would be 0.135. Below is few importance of the MPT:

It lowers the volatilities in the associated return of the stocks.

It lowers the risk level of the investment

The expected return factor are also measured by the process

The process is advanced and takes the concern on all the related factors

It makes it easier for the investors to reduce the associated risk and get better return

from the market (Bornholt, 2013).

On the basis of the discussion and the importance of minimum variance portfolio, it has

been recognized that this technique is quite efficient for the investors and the financial analyst

to make a base for the purpose of investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Financial Statement

8

CAPM:

CAPM stands for the capital asset pricing model which measures the required rate of

return form an individual security or the portfolio. It is an equilibrium based model which

represented the slop of the SML which mainly takes place because of the risk (beta). This

model takes the concern over the actual and relevant figures to identify the expected rate of

return form an individual security or the portfolio (Batra & Verma, 2014). It is also used by

the investors and the financial analyst to identify the stock price in the market.

It is a fundamental analyst tool which is used to estimate about the stock’s intrinsic

value and it is required for the analyst to measure the beta risk of an organization through

either identifying the historical risk and return or forecast the risk and return of the securities.

These estimates and the figures allow the analyst and the investors to measure the required

return which must be expected from the rational investors by the company (Damodaran,

2011).

The CAPM model is one of various available tools to identify the expected return.

The other models are dividend discount model, dividend growth model etc. The empirical

evidence briefs the CAMP model and the equation of CAPM model are better than other

models to identify the expected return. As CAPM model is the one which takes the concern

on market risk, risk free rate of the business and the volatility in the stock prices. The

equation of the CAPM model is as follows:

r = kRF + b(kM - kRF)

It is basically the equation of a line, where:

r = required return

kRF = the risk-free rate

kM = the average market return

b = the beta coefficient of the security

(Batra and Verma, 2014)

The equation briefs all the items in the equation could affect the return from a security

or the portfolio at any time and thus it is mandatory for the financial analyst to focus on these

items.

8

CAPM:

CAPM stands for the capital asset pricing model which measures the required rate of

return form an individual security or the portfolio. It is an equilibrium based model which

represented the slop of the SML which mainly takes place because of the risk (beta). This

model takes the concern over the actual and relevant figures to identify the expected rate of

return form an individual security or the portfolio (Batra & Verma, 2014). It is also used by

the investors and the financial analyst to identify the stock price in the market.

It is a fundamental analyst tool which is used to estimate about the stock’s intrinsic

value and it is required for the analyst to measure the beta risk of an organization through

either identifying the historical risk and return or forecast the risk and return of the securities.

These estimates and the figures allow the analyst and the investors to measure the required

return which must be expected from the rational investors by the company (Damodaran,

2011).

The CAPM model is one of various available tools to identify the expected return.

The other models are dividend discount model, dividend growth model etc. The empirical

evidence briefs the CAMP model and the equation of CAPM model are better than other

models to identify the expected return. As CAPM model is the one which takes the concern

on market risk, risk free rate of the business and the volatility in the stock prices. The

equation of the CAPM model is as follows:

r = kRF + b(kM - kRF)

It is basically the equation of a line, where:

r = required return

kRF = the risk-free rate

kM = the average market return

b = the beta coefficient of the security

(Batra and Verma, 2014)

The equation briefs all the items in the equation could affect the return from a security

or the portfolio at any time and thus it is mandatory for the financial analyst to focus on these

items.

Corporate Financial Statement

9

Beta:

Each of the stock is different by nature and the associated risk of each stock is also

different. The beta coefficient describes about the associated risk of the stock. The rate of

return (r) of an asset explains about the risk which can’t be diversified away even in the case

of a portfolio. Beta coefficient mainly briefs the changes into the stock prices. The beta

values play a significant role in order to identify the exact return from the security or the

portfolio (Moles, Parrino and Kidwekk, 2011).

Risk free rate:

R (f) Risk free rate is estimated by the Australia’s government treasury bonds. It

explains that how long an investors wants to hold the investment and if for the same time, the

investment would be done in the fixed rate treasury bond of the country than how much

return could be got by the investors (Lee and lee, 2006). It is the minimum return which is

expected from the investors through investing into the security.

Market risk premium:

Market risk premium explains about the expected return of risky investment which is

in excess of the risk free rate of the country. This define that the changes into the market

stock price is so and thus the required rate of return from an individual security must be

accordingly (Zabarankin, Pavlikov and Uryasev, 2014).

Required return:

Required return is the total % of return which is expected from the company by

investors. That is the minimum return for which an investor makes the investment into the

company. The required return is calculated in CAPM model by measuring the beta, risk free

rate of the market and the average market return of the index (Lumby and Jones, 2007). It

offers the better outcome to the investors than the other model because of its wider

application and the focus.

For instance, the risk free rate of Australia is 6%, market return is 16% and the beta

coefficient of the security is 1.7. Than the CAPM calculations of the case is as follows:

Cost of Equity: CAPM model

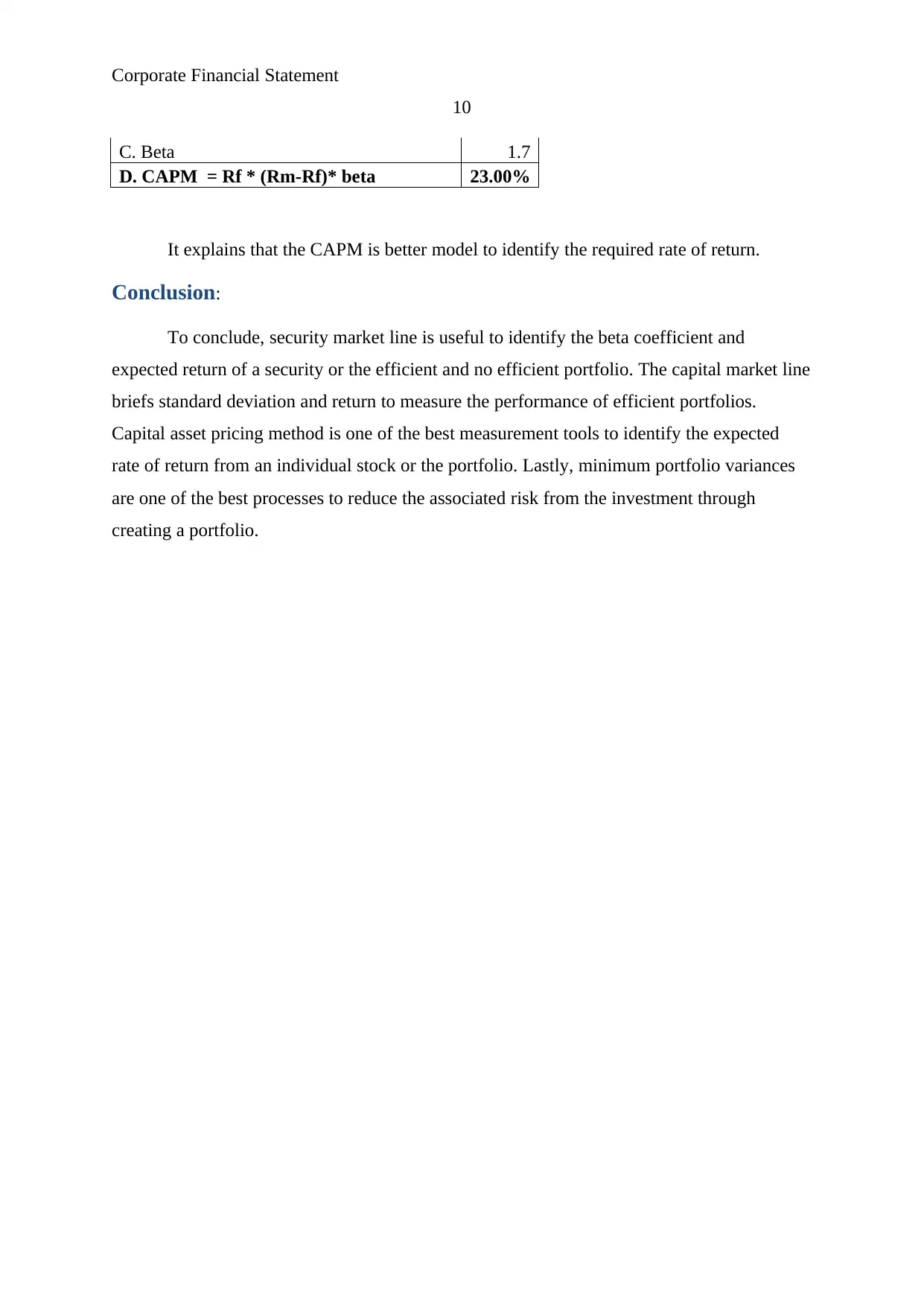

A. Risk free rate 6.00%

B. Market rate of return 16%

9

Beta:

Each of the stock is different by nature and the associated risk of each stock is also

different. The beta coefficient describes about the associated risk of the stock. The rate of

return (r) of an asset explains about the risk which can’t be diversified away even in the case

of a portfolio. Beta coefficient mainly briefs the changes into the stock prices. The beta

values play a significant role in order to identify the exact return from the security or the

portfolio (Moles, Parrino and Kidwekk, 2011).

Risk free rate:

R (f) Risk free rate is estimated by the Australia’s government treasury bonds. It

explains that how long an investors wants to hold the investment and if for the same time, the

investment would be done in the fixed rate treasury bond of the country than how much

return could be got by the investors (Lee and lee, 2006). It is the minimum return which is

expected from the investors through investing into the security.

Market risk premium:

Market risk premium explains about the expected return of risky investment which is

in excess of the risk free rate of the country. This define that the changes into the market

stock price is so and thus the required rate of return from an individual security must be

accordingly (Zabarankin, Pavlikov and Uryasev, 2014).

Required return:

Required return is the total % of return which is expected from the company by

investors. That is the minimum return for which an investor makes the investment into the

company. The required return is calculated in CAPM model by measuring the beta, risk free

rate of the market and the average market return of the index (Lumby and Jones, 2007). It

offers the better outcome to the investors than the other model because of its wider

application and the focus.

For instance, the risk free rate of Australia is 6%, market return is 16% and the beta

coefficient of the security is 1.7. Than the CAPM calculations of the case is as follows:

Cost of Equity: CAPM model

A. Risk free rate 6.00%

B. Market rate of return 16%

Corporate Financial Statement

10

C. Beta 1.7

D. CAPM = Rf * (Rm-Rf)* beta 23.00%

It explains that the CAPM is better model to identify the required rate of return.

Conclusion:

To conclude, security market line is useful to identify the beta coefficient and

expected return of a security or the efficient and no efficient portfolio. The capital market line

briefs standard deviation and return to measure the performance of efficient portfolios.

Capital asset pricing method is one of the best measurement tools to identify the expected

rate of return from an individual stock or the portfolio. Lastly, minimum portfolio variances

are one of the best processes to reduce the associated risk from the investment through

creating a portfolio.

10

C. Beta 1.7

D. CAPM = Rf * (Rm-Rf)* beta 23.00%

It explains that the CAPM is better model to identify the required rate of return.

Conclusion:

To conclude, security market line is useful to identify the beta coefficient and

expected return of a security or the efficient and no efficient portfolio. The capital market line

briefs standard deviation and return to measure the performance of efficient portfolios.

Capital asset pricing method is one of the best measurement tools to identify the expected

rate of return from an individual stock or the portfolio. Lastly, minimum portfolio variances

are one of the best processes to reduce the associated risk from the investment through

creating a portfolio.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate Financial Statement

11

References:

Barlow.J.F., 2006, Excel models for business and operations management, 2nd edition, John

Wiley & sons ltd, England.

Batra, R. and Verma, S. 2014, "An Empirical Insight into Different Stages of Capital

Budgeting", Global Business Review, 15 (2), pp. 339-362.

Bornholt, G. 2013, "The Failure of the Capital Asset Pricing Model (CAPM): An Update and

Discussion: The Capital Asset Pricing Model", Abacus, 49 (1), pp. 36-43.

Damodaran, A, 2011, Applied corporate finance. 3rd edition, John Wiley & sons, USA.

Lee.C.F and Lee, A, C,.2006. Encyclopedia of finance. Springer science, new York.

Lumby,S and Jones,C,.2007, Corporate finance theory & practice, 7th edition, Thomson,

London.

Moles, P. Parrino, R and Kidwekk, D,.2011. Corporate finance. European edition, John

Wiley &sons, United Kingdom.

Peterson, P,P and Fabozzi,F,J,. 2012. Capital budgeting: theory and practice. John Wiley &

sons, Canada.

Reilly.F.K and Brown.K.C,.2011. Investment analysis & portfolio management. 10th edition,

South western Cengage learning, India.

Ross, A,. Westerfield, R,W,. Jaffe,J,.and Kakani,R,K,.2008. Corporate Finance. 8th edition,

Tata McGraw hill education private limited, New Delhi, India

Ross, S, A,. Westerfield, R, W,. And Jaffe, J,.2007. Corporate Finance. the McGraw-hill,

India

Seitzinger, S.P., Mayorga, E., Bouwman, A.F., Kroeze, C., Beusen, A.H.W., Billen, G., cht,

v., G, Dumont, E.L., Fekete, B.M., Garnier, J. and Harrison, J. 2010, "Global River Nutrient

Export: A Scenario Analysis of Past and Future Trends", Global Biogeochemical Cycles, 24

(3) pp. GB0A08-GB0A08.

Tian, D. and Jiang, L. 2015, "Quasiconvex risk statistics with scenario

analysis", Mathematics and Financial Economics, 9(2), pp. 111-121.

11

References:

Barlow.J.F., 2006, Excel models for business and operations management, 2nd edition, John

Wiley & sons ltd, England.

Batra, R. and Verma, S. 2014, "An Empirical Insight into Different Stages of Capital

Budgeting", Global Business Review, 15 (2), pp. 339-362.

Bornholt, G. 2013, "The Failure of the Capital Asset Pricing Model (CAPM): An Update and

Discussion: The Capital Asset Pricing Model", Abacus, 49 (1), pp. 36-43.

Damodaran, A, 2011, Applied corporate finance. 3rd edition, John Wiley & sons, USA.

Lee.C.F and Lee, A, C,.2006. Encyclopedia of finance. Springer science, new York.

Lumby,S and Jones,C,.2007, Corporate finance theory & practice, 7th edition, Thomson,

London.

Moles, P. Parrino, R and Kidwekk, D,.2011. Corporate finance. European edition, John

Wiley &sons, United Kingdom.

Peterson, P,P and Fabozzi,F,J,. 2012. Capital budgeting: theory and practice. John Wiley &

sons, Canada.

Reilly.F.K and Brown.K.C,.2011. Investment analysis & portfolio management. 10th edition,

South western Cengage learning, India.

Ross, A,. Westerfield, R,W,. Jaffe,J,.and Kakani,R,K,.2008. Corporate Finance. 8th edition,

Tata McGraw hill education private limited, New Delhi, India

Ross, S, A,. Westerfield, R, W,. And Jaffe, J,.2007. Corporate Finance. the McGraw-hill,

India

Seitzinger, S.P., Mayorga, E., Bouwman, A.F., Kroeze, C., Beusen, A.H.W., Billen, G., cht,

v., G, Dumont, E.L., Fekete, B.M., Garnier, J. and Harrison, J. 2010, "Global River Nutrient

Export: A Scenario Analysis of Past and Future Trends", Global Biogeochemical Cycles, 24

(3) pp. GB0A08-GB0A08.

Tian, D. and Jiang, L. 2015, "Quasiconvex risk statistics with scenario

analysis", Mathematics and Financial Economics, 9(2), pp. 111-121.

Corporate Financial Statement

12

Zabarankin, M., Pavlikov, K. and Uryasev, S. 2014. "Capital Asset Pricing Model with

drawdown measure", European Journal of Operational Research, 234 (2), pp. 508.

12

Zabarankin, M., Pavlikov, K. and Uryasev, S. 2014. "Capital Asset Pricing Model with

drawdown measure", European Journal of Operational Research, 234 (2), pp. 508.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.