Corporate Financial Strategy: Analysis and Concepts

VerifiedAdded on 2023/06/18

|11

|1793

|217

AI Summary

This module covers the concepts and strategies of corporate financial management, including dividend valuation, bond pricing, merger analysis, efficient market hypothesis, and more. It includes a detailed analysis of various financial strategies and their implications for corporate decision-making. The module is relevant for students pursuing courses in finance, accounting, and business management.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Module title: Corporate

Financial Strategy

Financial Strategy

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

SECTION A.....................................................................................................................................3

Question 1...................................................................................................................................3

Question 2...................................................................................................................................3

Question 3...................................................................................................................................3

Question 4...................................................................................................................................4

Question 5...................................................................................................................................4

Question 6...................................................................................................................................4

SECTION B.....................................................................................................................................5

Question: 8..................................................................................................................................5

SECTION C....................................................................................................................................9

Question 10.................................................................................................................................9

REFERENCES..............................................................................................................................11

SECTION A.....................................................................................................................................3

Question 1...................................................................................................................................3

Question 2...................................................................................................................................3

Question 3...................................................................................................................................3

Question 4...................................................................................................................................4

Question 5...................................................................................................................................4

Question 6...................................................................................................................................4

SECTION B.....................................................................................................................................5

Question: 8..................................................................................................................................5

SECTION C....................................................................................................................................9

Question 10.................................................................................................................................9

REFERENCES..............................................................................................................................11

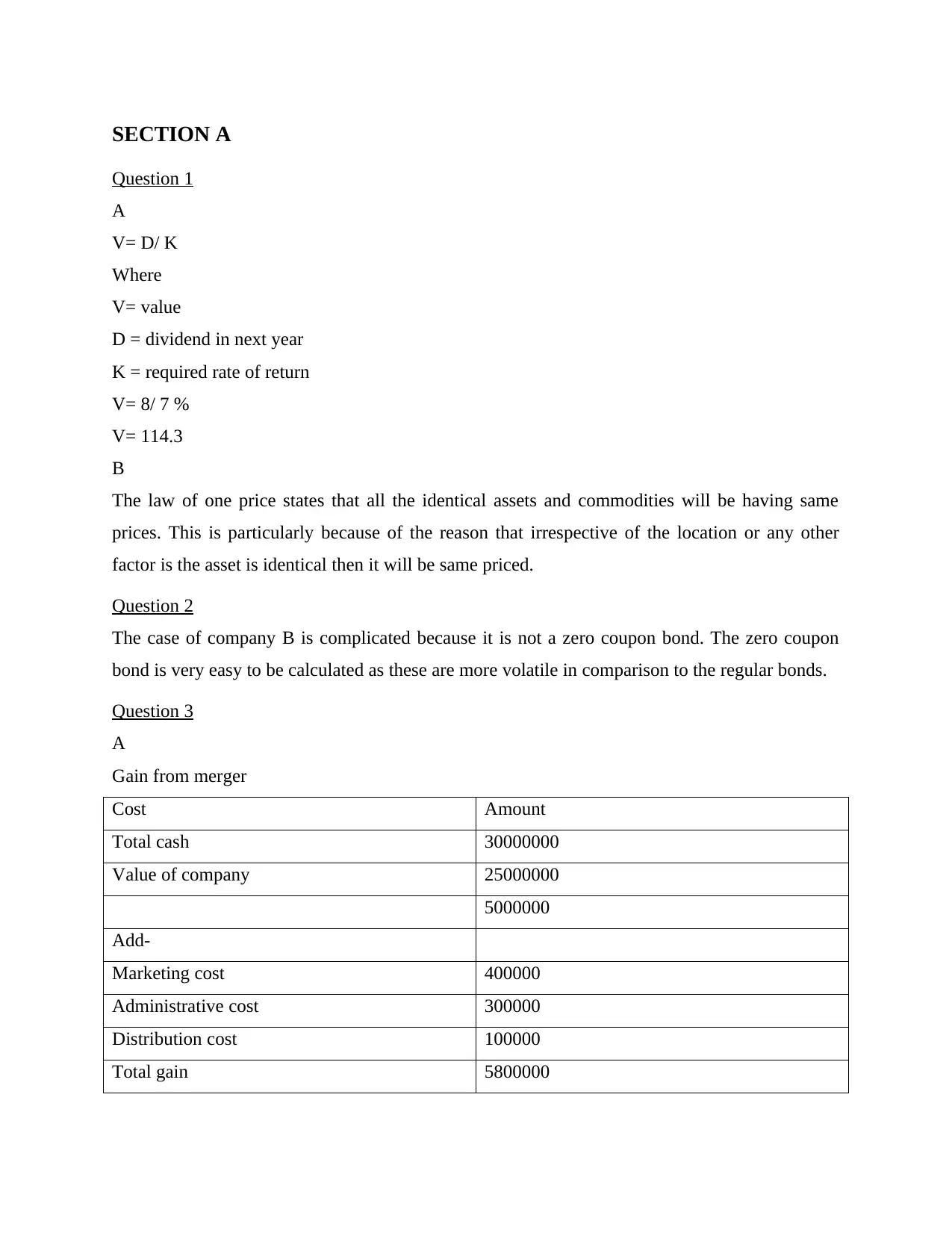

SECTION A

Question 1

A

V= D/ K

Where

V= value

D = dividend in next year

K = required rate of return

V= 8/ 7 %

V= 114.3

B

The law of one price states that all the identical assets and commodities will be having same

prices. This is particularly because of the reason that irrespective of the location or any other

factor is the asset is identical then it will be same priced.

Question 2

The case of company B is complicated because it is not a zero coupon bond. The zero coupon

bond is very easy to be calculated as these are more volatile in comparison to the regular bonds.

Question 3

A

Gain from merger

Cost Amount

Total cash 30000000

Value of company 25000000

5000000

Add-

Marketing cost 400000

Administrative cost 300000

Distribution cost 100000

Total gain 5800000

Question 1

A

V= D/ K

Where

V= value

D = dividend in next year

K = required rate of return

V= 8/ 7 %

V= 114.3

B

The law of one price states that all the identical assets and commodities will be having same

prices. This is particularly because of the reason that irrespective of the location or any other

factor is the asset is identical then it will be same priced.

Question 2

The case of company B is complicated because it is not a zero coupon bond. The zero coupon

bond is very easy to be calculated as these are more volatile in comparison to the regular bonds.

Question 3

A

Gain from merger

Cost Amount

Total cash 30000000

Value of company 25000000

5000000

Add-

Marketing cost 400000

Administrative cost 300000

Distribution cost 100000

Total gain 5800000

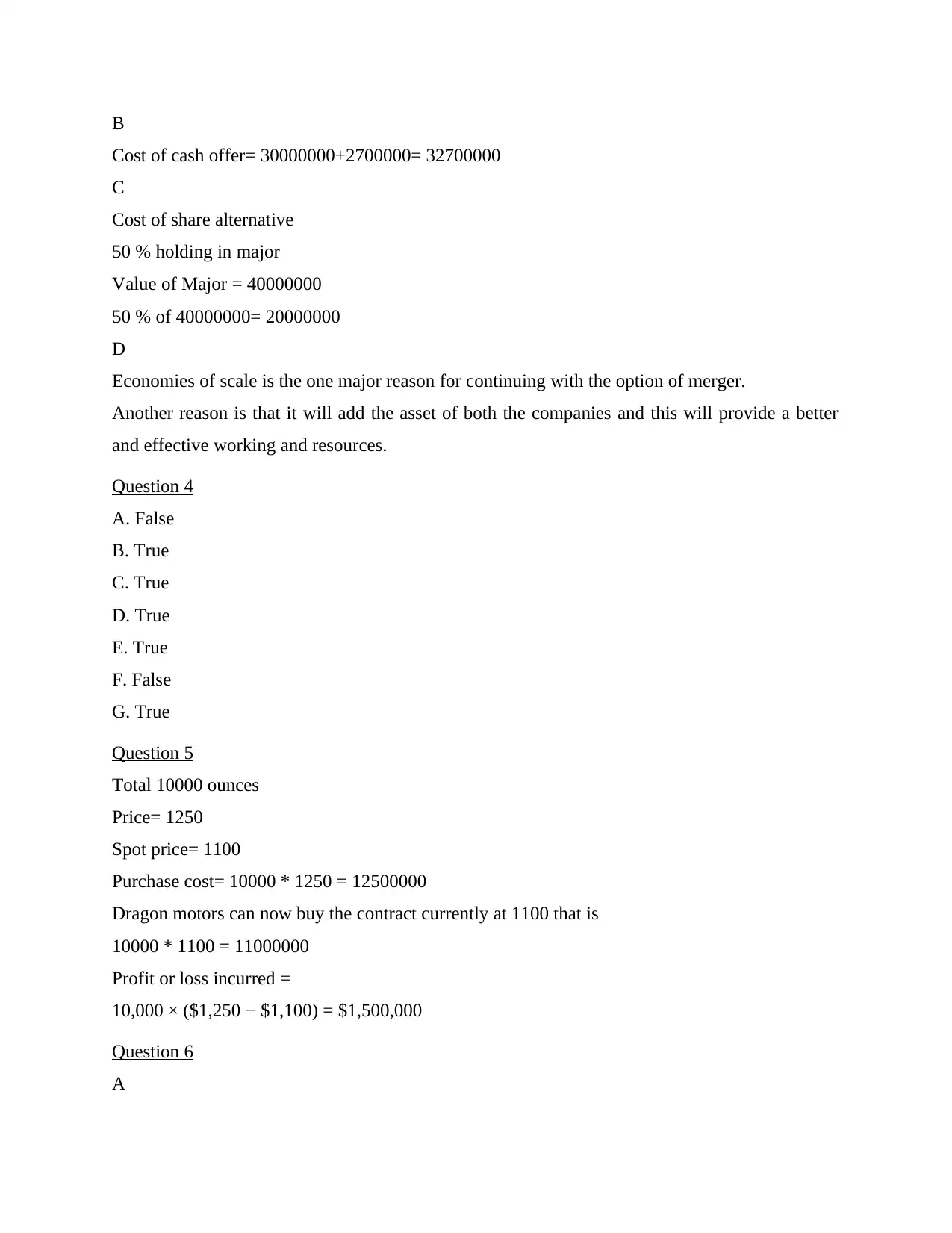

B

Cost of cash offer= 30000000+2700000= 32700000

C

Cost of share alternative

50 % holding in major

Value of Major = 40000000

50 % of 40000000= 20000000

D

Economies of scale is the one major reason for continuing with the option of merger.

Another reason is that it will add the asset of both the companies and this will provide a better

and effective working and resources.

Question 4

A. False

B. True

C. True

D. True

E. True

F. False

G. True

Question 5

Total 10000 ounces

Price= 1250

Spot price= 1100

Purchase cost= 10000 * 1250 = 12500000

Dragon motors can now buy the contract currently at 1100 that is

10000 * 1100 = 11000000

Profit or loss incurred =

10,000 × ($1,250 − $1,100) = $1,500,000

Question 6

A

Cost of cash offer= 30000000+2700000= 32700000

C

Cost of share alternative

50 % holding in major

Value of Major = 40000000

50 % of 40000000= 20000000

D

Economies of scale is the one major reason for continuing with the option of merger.

Another reason is that it will add the asset of both the companies and this will provide a better

and effective working and resources.

Question 4

A. False

B. True

C. True

D. True

E. True

F. False

G. True

Question 5

Total 10000 ounces

Price= 1250

Spot price= 1100

Purchase cost= 10000 * 1250 = 12500000

Dragon motors can now buy the contract currently at 1100 that is

10000 * 1100 = 11000000

Profit or loss incurred =

10,000 × ($1,250 − $1,100) = $1,500,000

Question 6

A

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

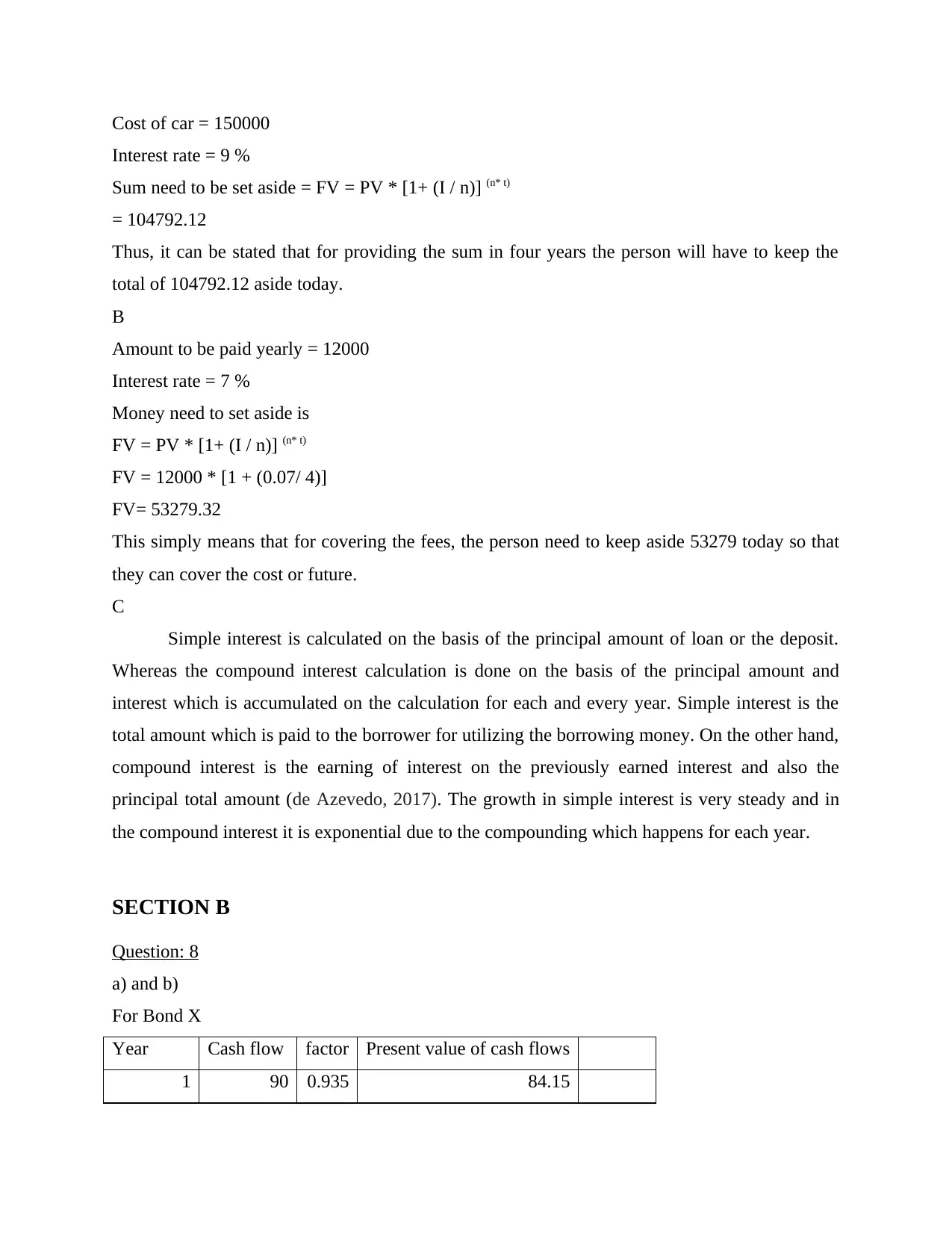

Cost of car = 150000

Interest rate = 9 %

Sum need to be set aside = FV = PV * [1+ (I / n)] (n* t)

= 104792.12

Thus, it can be stated that for providing the sum in four years the person will have to keep the

total of 104792.12 aside today.

B

Amount to be paid yearly = 12000

Interest rate = 7 %

Money need to set aside is

FV = PV * [1+ (I / n)] (n* t)

FV = 12000 * [1 + (0.07/ 4)]

FV= 53279.32

This simply means that for covering the fees, the person need to keep aside 53279 today so that

they can cover the cost or future.

C

Simple interest is calculated on the basis of the principal amount of loan or the deposit.

Whereas the compound interest calculation is done on the basis of the principal amount and

interest which is accumulated on the calculation for each and every year. Simple interest is the

total amount which is paid to the borrower for utilizing the borrowing money. On the other hand,

compound interest is the earning of interest on the previously earned interest and also the

principal total amount (de Azevedo, 2017). The growth in simple interest is very steady and in

the compound interest it is exponential due to the compounding which happens for each year.

SECTION B

Question: 8

a) and b)

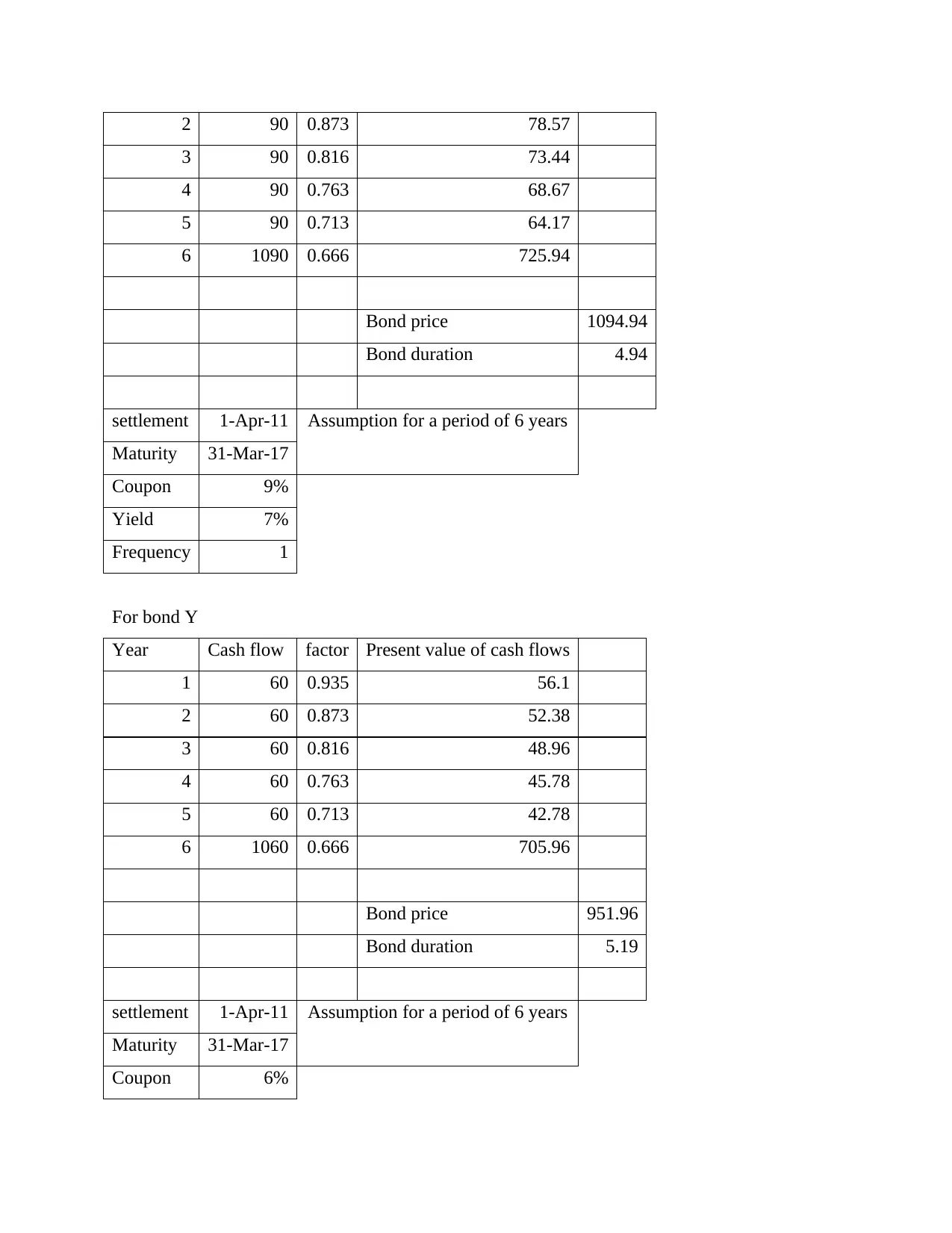

For Bond X

Year Cash flow factor Present value of cash flows

1 90 0.935 84.15

Interest rate = 9 %

Sum need to be set aside = FV = PV * [1+ (I / n)] (n* t)

= 104792.12

Thus, it can be stated that for providing the sum in four years the person will have to keep the

total of 104792.12 aside today.

B

Amount to be paid yearly = 12000

Interest rate = 7 %

Money need to set aside is

FV = PV * [1+ (I / n)] (n* t)

FV = 12000 * [1 + (0.07/ 4)]

FV= 53279.32

This simply means that for covering the fees, the person need to keep aside 53279 today so that

they can cover the cost or future.

C

Simple interest is calculated on the basis of the principal amount of loan or the deposit.

Whereas the compound interest calculation is done on the basis of the principal amount and

interest which is accumulated on the calculation for each and every year. Simple interest is the

total amount which is paid to the borrower for utilizing the borrowing money. On the other hand,

compound interest is the earning of interest on the previously earned interest and also the

principal total amount (de Azevedo, 2017). The growth in simple interest is very steady and in

the compound interest it is exponential due to the compounding which happens for each year.

SECTION B

Question: 8

a) and b)

For Bond X

Year Cash flow factor Present value of cash flows

1 90 0.935 84.15

2 90 0.873 78.57

3 90 0.816 73.44

4 90 0.763 68.67

5 90 0.713 64.17

6 1090 0.666 725.94

Bond price 1094.94

Bond duration 4.94

settlement 1-Apr-11 Assumption for a period of 6 years

Maturity 31-Mar-17

Coupon 9%

Yield 7%

Frequency 1

For bond Y

Year Cash flow factor Present value of cash flows

1 60 0.935 56.1

2 60 0.873 52.38

3 60 0.816 48.96

4 60 0.763 45.78

5 60 0.713 42.78

6 1060 0.666 705.96

Bond price 951.96

Bond duration 5.19

settlement 1-Apr-11 Assumption for a period of 6 years

Maturity 31-Mar-17

Coupon 6%

3 90 0.816 73.44

4 90 0.763 68.67

5 90 0.713 64.17

6 1090 0.666 725.94

Bond price 1094.94

Bond duration 4.94

settlement 1-Apr-11 Assumption for a period of 6 years

Maturity 31-Mar-17

Coupon 9%

Yield 7%

Frequency 1

For bond Y

Year Cash flow factor Present value of cash flows

1 60 0.935 56.1

2 60 0.873 52.38

3 60 0.816 48.96

4 60 0.763 45.78

5 60 0.713 42.78

6 1060 0.666 705.96

Bond price 951.96

Bond duration 5.19

settlement 1-Apr-11 Assumption for a period of 6 years

Maturity 31-Mar-17

Coupon 6%

Yield 7%

Frequency 1

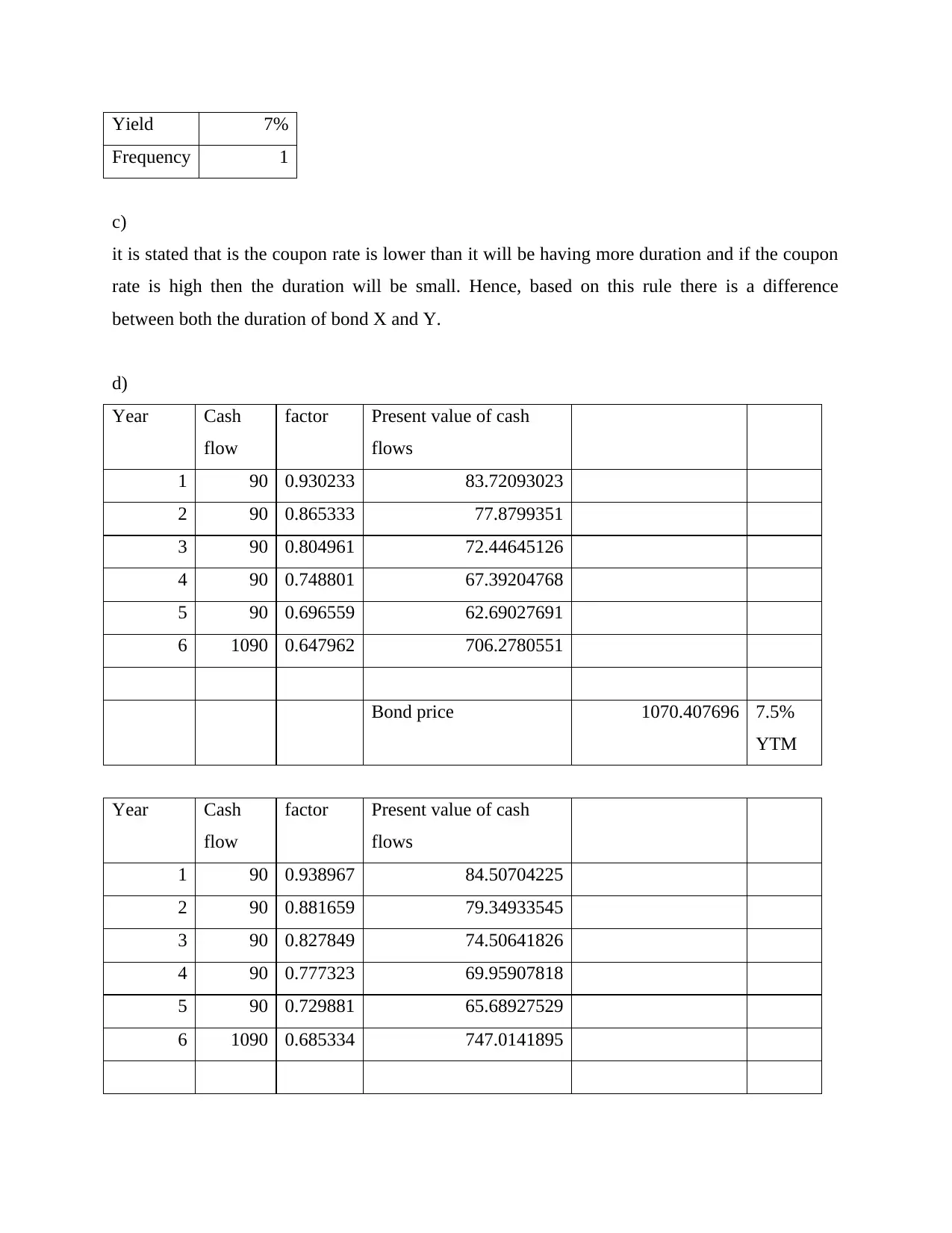

c)

it is stated that is the coupon rate is lower than it will be having more duration and if the coupon

rate is high then the duration will be small. Hence, based on this rule there is a difference

between both the duration of bond X and Y.

d)

Year Cash

flow

factor Present value of cash

flows

1 90 0.930233 83.72093023

2 90 0.865333 77.8799351

3 90 0.804961 72.44645126

4 90 0.748801 67.39204768

5 90 0.696559 62.69027691

6 1090 0.647962 706.2780551

Bond price 1070.407696 7.5%

YTM

Year Cash

flow

factor Present value of cash

flows

1 90 0.938967 84.50704225

2 90 0.881659 79.34933545

3 90 0.827849 74.50641826

4 90 0.777323 69.95907818

5 90 0.729881 65.68927529

6 1090 0.685334 747.0141895

Frequency 1

c)

it is stated that is the coupon rate is lower than it will be having more duration and if the coupon

rate is high then the duration will be small. Hence, based on this rule there is a difference

between both the duration of bond X and Y.

d)

Year Cash

flow

factor Present value of cash

flows

1 90 0.930233 83.72093023

2 90 0.865333 77.8799351

3 90 0.804961 72.44645126

4 90 0.748801 67.39204768

5 90 0.696559 62.69027691

6 1090 0.647962 706.2780551

Bond price 1070.407696 7.5%

YTM

Year Cash

flow

factor Present value of cash

flows

1 90 0.938967 84.50704225

2 90 0.881659 79.34933545

3 90 0.827849 74.50641826

4 90 0.777323 69.95907818

5 90 0.729881 65.68927529

6 1090 0.685334 747.0141895

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

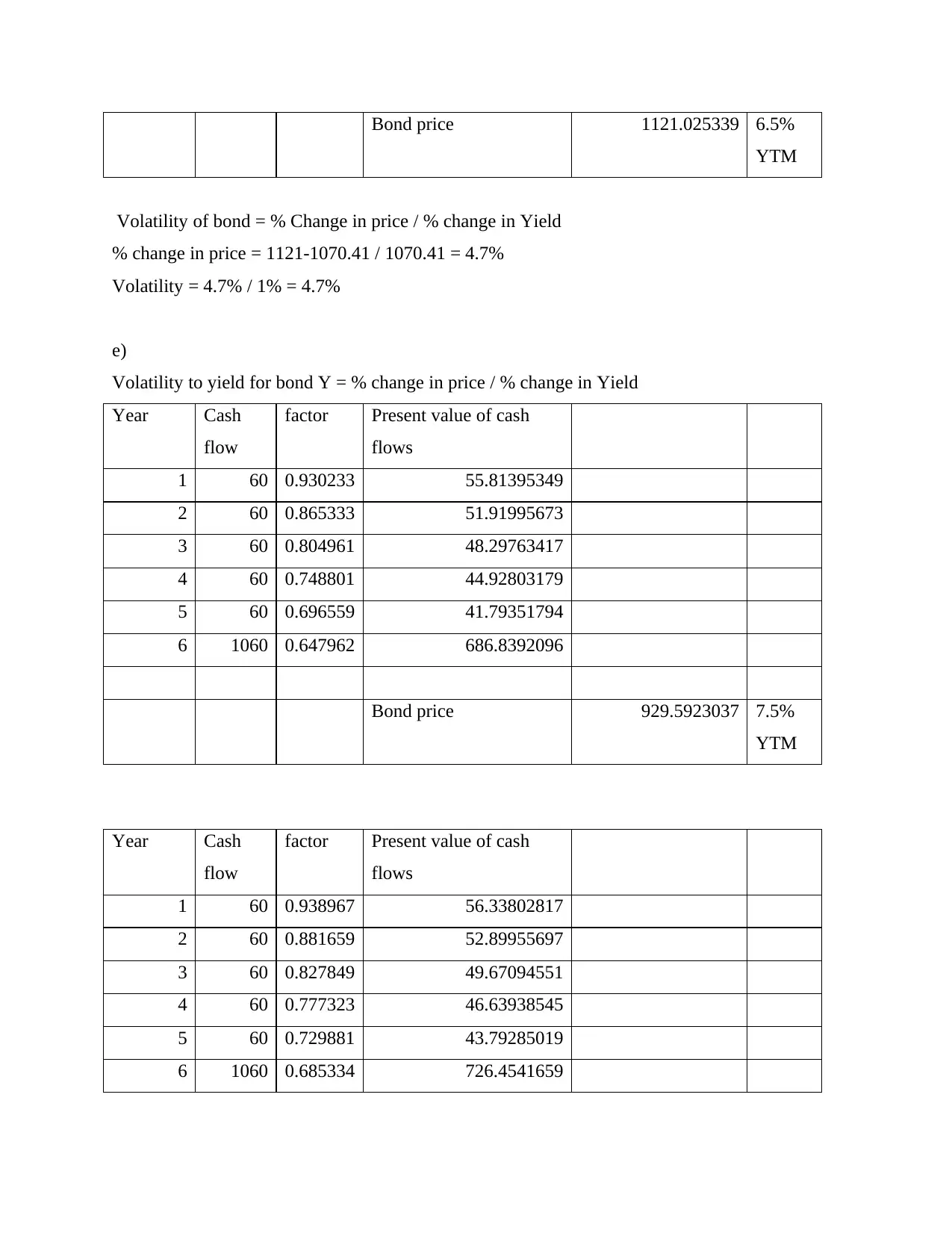

Bond price 1121.025339 6.5%

YTM

Volatility of bond = % Change in price / % change in Yield

% change in price = 1121-1070.41 / 1070.41 = 4.7%

Volatility = 4.7% / 1% = 4.7%

e)

Volatility to yield for bond Y = % change in price / % change in Yield

Year Cash

flow

factor Present value of cash

flows

1 60 0.930233 55.81395349

2 60 0.865333 51.91995673

3 60 0.804961 48.29763417

4 60 0.748801 44.92803179

5 60 0.696559 41.79351794

6 1060 0.647962 686.8392096

Bond price 929.5923037 7.5%

YTM

Year Cash

flow

factor Present value of cash

flows

1 60 0.938967 56.33802817

2 60 0.881659 52.89955697

3 60 0.827849 49.67094551

4 60 0.777323 46.63938545

5 60 0.729881 43.79285019

6 1060 0.685334 726.4541659

YTM

Volatility of bond = % Change in price / % change in Yield

% change in price = 1121-1070.41 / 1070.41 = 4.7%

Volatility = 4.7% / 1% = 4.7%

e)

Volatility to yield for bond Y = % change in price / % change in Yield

Year Cash

flow

factor Present value of cash

flows

1 60 0.930233 55.81395349

2 60 0.865333 51.91995673

3 60 0.804961 48.29763417

4 60 0.748801 44.92803179

5 60 0.696559 41.79351794

6 1060 0.647962 686.8392096

Bond price 929.5923037 7.5%

YTM

Year Cash

flow

factor Present value of cash

flows

1 60 0.938967 56.33802817

2 60 0.881659 52.89955697

3 60 0.827849 49.67094551

4 60 0.777323 46.63938545

5 60 0.729881 43.79285019

6 1060 0.685334 726.4541659

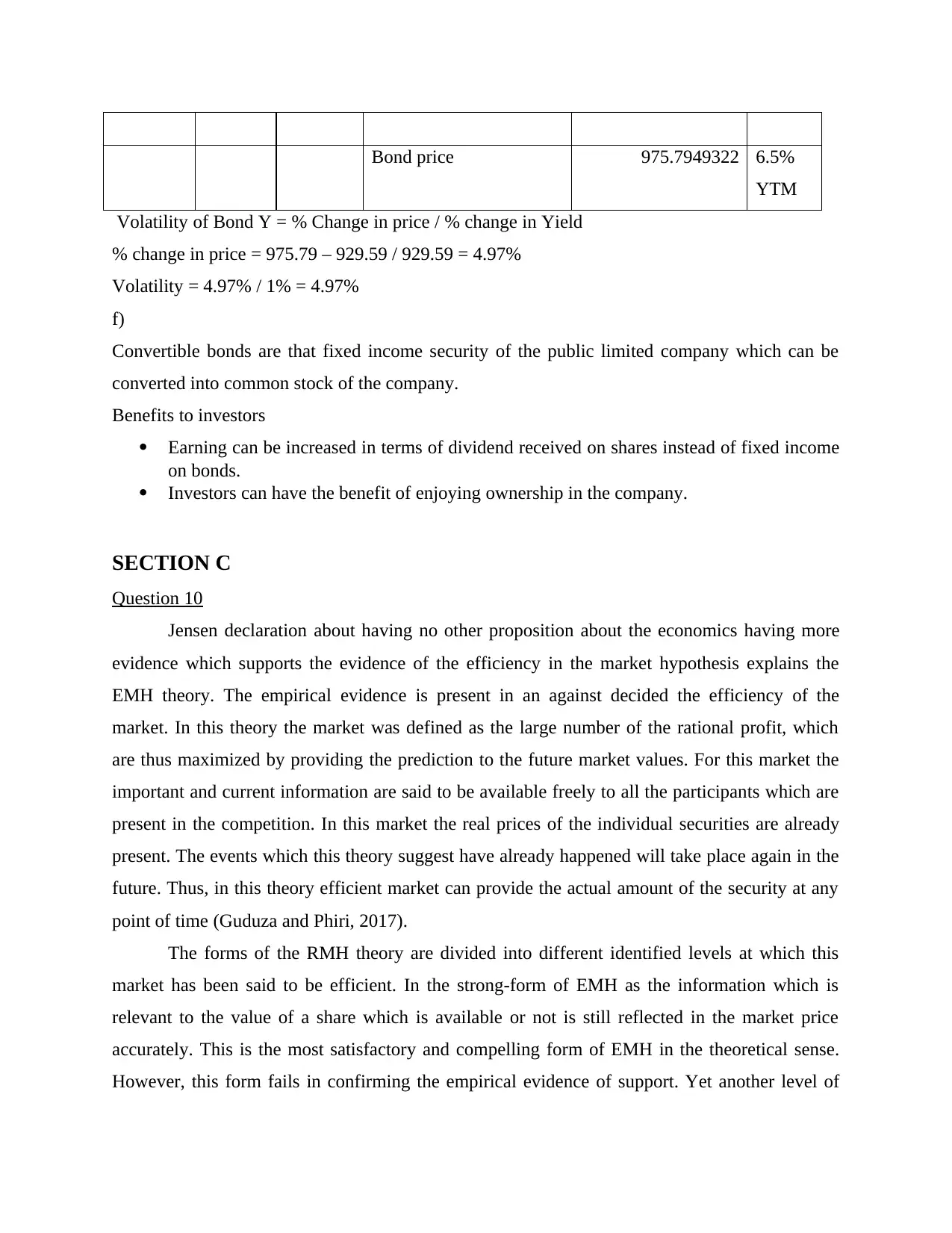

Bond price 975.7949322 6.5%

YTM

Volatility of Bond Y = % Change in price / % change in Yield

% change in price = 975.79 – 929.59 / 929.59 = 4.97%

Volatility = 4.97% / 1% = 4.97%

f)

Convertible bonds are that fixed income security of the public limited company which can be

converted into common stock of the company.

Benefits to investors

Earning can be increased in terms of dividend received on shares instead of fixed income

on bonds.

Investors can have the benefit of enjoying ownership in the company.

SECTION C

Question 10

Jensen declaration about having no other proposition about the economics having more

evidence which supports the evidence of the efficiency in the market hypothesis explains the

EMH theory. The empirical evidence is present in an against decided the efficiency of the

market. In this theory the market was defined as the large number of the rational profit, which

are thus maximized by providing the prediction to the future market values. For this market the

important and current information are said to be available freely to all the participants which are

present in the competition. In this market the real prices of the individual securities are already

present. The events which this theory suggest have already happened will take place again in the

future. Thus, in this theory efficient market can provide the actual amount of the security at any

point of time (Guduza and Phiri, 2017).

The forms of the RMH theory are divided into different identified levels at which this

market has been said to be efficient. In the strong-form of EMH as the information which is

relevant to the value of a share which is available or not is still reflected in the market price

accurately. This is the most satisfactory and compelling form of EMH in the theoretical sense.

However, this form fails in confirming the empirical evidence of support. Yet another level of

YTM

Volatility of Bond Y = % Change in price / % change in Yield

% change in price = 975.79 – 929.59 / 929.59 = 4.97%

Volatility = 4.97% / 1% = 4.97%

f)

Convertible bonds are that fixed income security of the public limited company which can be

converted into common stock of the company.

Benefits to investors

Earning can be increased in terms of dividend received on shares instead of fixed income

on bonds.

Investors can have the benefit of enjoying ownership in the company.

SECTION C

Question 10

Jensen declaration about having no other proposition about the economics having more

evidence which supports the evidence of the efficiency in the market hypothesis explains the

EMH theory. The empirical evidence is present in an against decided the efficiency of the

market. In this theory the market was defined as the large number of the rational profit, which

are thus maximized by providing the prediction to the future market values. For this market the

important and current information are said to be available freely to all the participants which are

present in the competition. In this market the real prices of the individual securities are already

present. The events which this theory suggest have already happened will take place again in the

future. Thus, in this theory efficient market can provide the actual amount of the security at any

point of time (Guduza and Phiri, 2017).

The forms of the RMH theory are divided into different identified levels at which this

market has been said to be efficient. In the strong-form of EMH as the information which is

relevant to the value of a share which is available or not is still reflected in the market price

accurately. This is the most satisfactory and compelling form of EMH in the theoretical sense.

However, this form fails in confirming the empirical evidence of support. Yet another level of

EMH is the Semi-strong form of EMH. This has a less rigorous form as the EMH considers the

market to be efficient. Thus, all the relevant information is publicly available quickly reflects in

the market price. This form of EMH appeals towards the common sense, this allows the investor

to have the price at the new equilibrium level, which reflects the changes in the demand and

supply which is caused by the emergence of that information. Due to the lack of intellectual

rigour the EMH in this level shows empirical strength as it is less difficult to be tested in the

strong form. The weak-form of EMH is the least rigorous form, it has just one subset of

information available to it. This is the level in which the no other proposition in economics has

more solid empirical evidence for. It is supported highly from the empirical evidence which

supports the efficiency of the market hypothesis (Kholesta, 2019).

The efficient market's hypothesis is said to be dominated with the academical and

business scene. Due to which the findings of Jensen is backed up. However, in the later studies it

was found that the increased value of the theoretical and empirical work is either considered to

be contradicted to the EMH or out right can show that the case is not yet proven. The use of this

assumption was later found to be herd instinct, having a tendency to churn the portfolios, it was

known to also overreact to the different news which affected the information and it also caused

asymmetrical judgements on the previous profits and losses. EMH finally suggests that investor

cannot make excess returns out of the stale information which is inaccurate due to the non

relevancy of the efficient market (Sardana and Gupta, 2018).

market to be efficient. Thus, all the relevant information is publicly available quickly reflects in

the market price. This form of EMH appeals towards the common sense, this allows the investor

to have the price at the new equilibrium level, which reflects the changes in the demand and

supply which is caused by the emergence of that information. Due to the lack of intellectual

rigour the EMH in this level shows empirical strength as it is less difficult to be tested in the

strong form. The weak-form of EMH is the least rigorous form, it has just one subset of

information available to it. This is the level in which the no other proposition in economics has

more solid empirical evidence for. It is supported highly from the empirical evidence which

supports the efficiency of the market hypothesis (Kholesta, 2019).

The efficient market's hypothesis is said to be dominated with the academical and

business scene. Due to which the findings of Jensen is backed up. However, in the later studies it

was found that the increased value of the theoretical and empirical work is either considered to

be contradicted to the EMH or out right can show that the case is not yet proven. The use of this

assumption was later found to be herd instinct, having a tendency to churn the portfolios, it was

known to also overreact to the different news which affected the information and it also caused

asymmetrical judgements on the previous profits and losses. EMH finally suggests that investor

cannot make excess returns out of the stale information which is inaccurate due to the non

relevancy of the efficient market (Sardana and Gupta, 2018).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Guduza, S. and Phiri, A., 2017. Efficient Market Hypothesis: Evidence from the JSE equity and

bond markets.

Kholesta, A.K., 2019. Weak Form Efficient Market Hypothesis and January Effect; Study Case

in LQ45 Index of Indonesia Stock Exchange Market Period 2016-2018. Jurnal

Manajemen Update, 8(4).

Sardana, S. and Gupta, P., 2018. A Study on Efficient Market Hypothesis in Hotels Sector in

Indian Stock Market. Apeejay Journal of Management & Technology, pp.47-54.

de Azevedo, R.M.M., 2017. Characterization of the Turbulent Structure in Compound Channel

Flows (Doctoral dissertation, Universidade NOVA de Lisboa (Portugal)).

Books and Journals

Guduza, S. and Phiri, A., 2017. Efficient Market Hypothesis: Evidence from the JSE equity and

bond markets.

Kholesta, A.K., 2019. Weak Form Efficient Market Hypothesis and January Effect; Study Case

in LQ45 Index of Indonesia Stock Exchange Market Period 2016-2018. Jurnal

Manajemen Update, 8(4).

Sardana, S. and Gupta, P., 2018. A Study on Efficient Market Hypothesis in Hotels Sector in

Indian Stock Market. Apeejay Journal of Management & Technology, pp.47-54.

de Azevedo, R.M.M., 2017. Characterization of the Turbulent Structure in Compound Channel

Flows (Doctoral dissertation, Universidade NOVA de Lisboa (Portugal)).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.