Comparison of Corporate Governance Codes: Norway vs UAE

VerifiedAdded on 2023/05/29

|6

|1166

|84

AI Summary

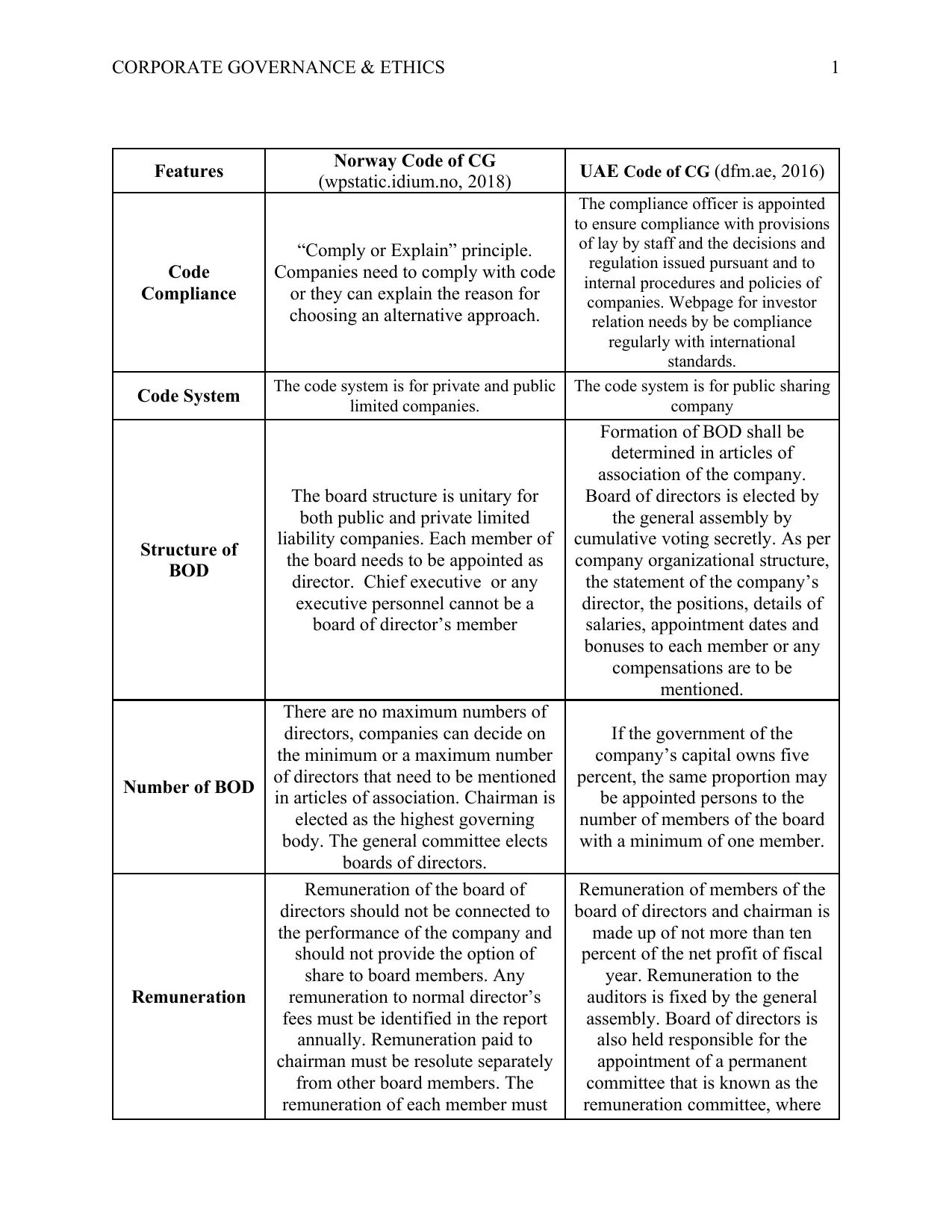

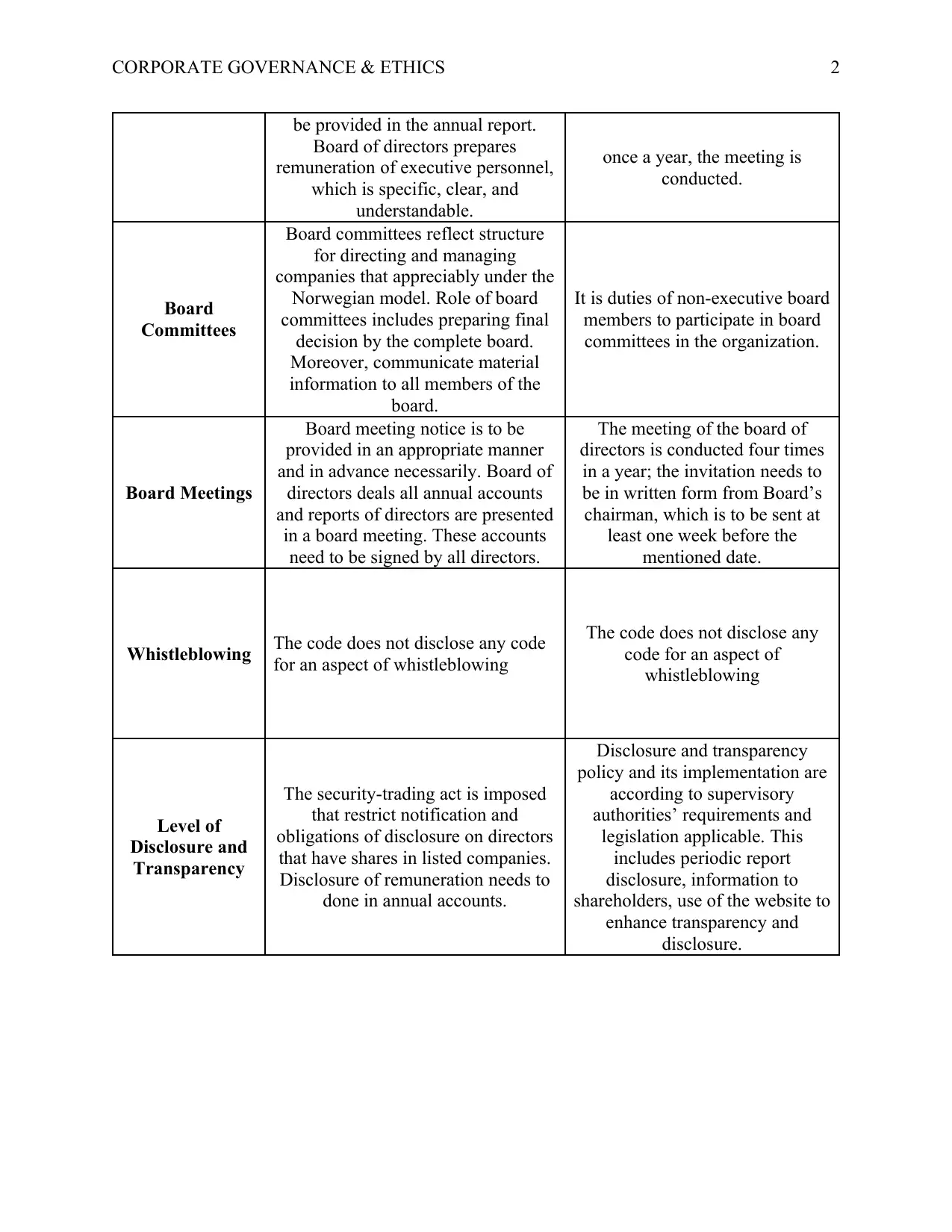

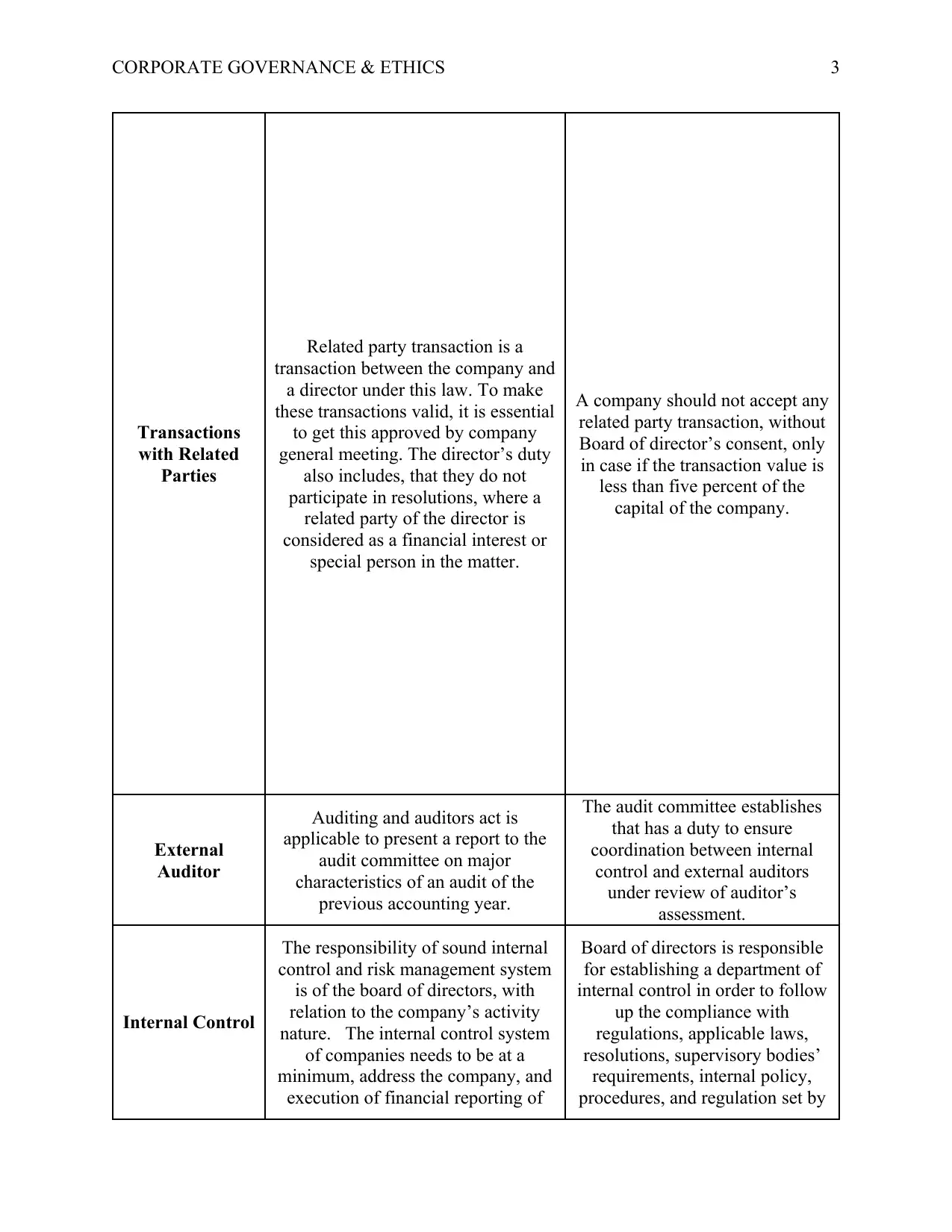

This article compares the corporate governance codes of Norway and UAE, focusing on their features, code compliance, board structure, remuneration, board committees, board meetings, whistleblowing, transactions with related parties, external auditor, internal control, and other aspects.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.