Contemporary Corporate Reporting and Evaluation of Lucky Lanka Milk Processing Company

VerifiedAdded on 2023/06/03

|21

|3976

|365

AI Summary

This article discusses contemporary corporate reporting, accounting standards, and evaluates the financial and non-financial information of Lucky Lanka Milk Processing Company. It also includes a critical analysis of the company's performance and a comparison of financial ratios with Lanka Milk Food.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CONTEMPORARY CORPORATE REPORTING 1

Contemporary Corporate Reporting

Your Name

Name of Institution

Contemporary Corporate Reporting

Your Name

Name of Institution

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY CORPORATE REPORTING 2

Contemporary Corporate Reporting.

Part A

Corporate Reporting

Corporate reporting meaning differs according or depending to the intended audience of

the financial statements, (Lee & Maxfield, 2015). Corporate reporting can be defined as the

disclosure and presentation features of reporting which are different from accounting and its

measurements. Corporate reporting includes narrative reporting, financial reporting, corporate

governance reporting, integrated reporting, executive remuneration reporting and corporate

responsibility reporting. Corporate reporting comprises of voluntary disclosures which help to

add value to financial statements and make it useful to stakeholders of the company and other

external users of financial statements like the investors. Corporate reporting provides

stakeholders with insights into the activities of a company and therefore ends up to affect the

share price, (Corporate reporting,2014). Companies implement audit committees which help

them in ensuring corporate reporting and this act requires companies to be accountable and

transparent. The corporation act 2001 requires companies to safeguard integrity by corporate

reporting.

Importance of Corporate Reporting

Corporate reporting is used by companies because it is relevant in that it helps in

prioritizing social, economic and environmental issues which are useful for strategic planning

purposes. It is relevant in that it helps companies to illustrate and identify highly material issues

which help in the long-term success of companies, (Everingham, Kana & Wadee, 2012).

Corporate reporting enables companies to build good connection with their stakeholders and

Contemporary Corporate Reporting.

Part A

Corporate Reporting

Corporate reporting meaning differs according or depending to the intended audience of

the financial statements, (Lee & Maxfield, 2015). Corporate reporting can be defined as the

disclosure and presentation features of reporting which are different from accounting and its

measurements. Corporate reporting includes narrative reporting, financial reporting, corporate

governance reporting, integrated reporting, executive remuneration reporting and corporate

responsibility reporting. Corporate reporting comprises of voluntary disclosures which help to

add value to financial statements and make it useful to stakeholders of the company and other

external users of financial statements like the investors. Corporate reporting provides

stakeholders with insights into the activities of a company and therefore ends up to affect the

share price, (Corporate reporting,2014). Companies implement audit committees which help

them in ensuring corporate reporting and this act requires companies to be accountable and

transparent. The corporation act 2001 requires companies to safeguard integrity by corporate

reporting.

Importance of Corporate Reporting

Corporate reporting is used by companies because it is relevant in that it helps in

prioritizing social, economic and environmental issues which are useful for strategic planning

purposes. It is relevant in that it helps companies to illustrate and identify highly material issues

which help in the long-term success of companies, (Everingham, Kana & Wadee, 2012).

Corporate reporting enables companies to build good connection with their stakeholders and

CONTEMPORARY CORPORATE REPORTING 3

investors. Companies produce corporate reports so as to give enough information to specific

users of financial statements. Corporate reporting also enables companies to provide information

about how they raise funds and how those funds are utilized in the course of business. Corporate

reporting also helps companies to access debt, equity and other trade finances. Companies

produce corporate reports in order to avail their information concerning the financial position

and financial performance and this makes it useful to a wide range of financial statement users in

evaluating the stewardship of management and be able to make useful economic decisions.

Accounting Standards

Accounting standards can be described as authoritative standards that are used in

financial reporting, (Sapovadia, 2008). Accounting standards are the basic source of the

generally accepted accounting principles, (GAAP). These standards provide specifications of

how transactions and other accounting events should be measured, recognized, presented and

disclosed in companies’ financial statements, (Rayman 2013). Accounting standards are policies

that are imperative to all the accounting activities and they help business to run their activities

smoothly. All companies are required to adhere to the accounting standards set by FASB and

IASB, failure to comply with this standards will lead companies spending on legal action

initiated against it by their governments.

Importance of Accounting Standards in Reporting

Accounting standards enable companies to provide external users such as lenders and

investor, with information which is useful in decision making, (Sugara & Boland, 2011).

Accounting standards help companies to assess their business performance and be able to

compare it with the performance of competitors through the use of financial statements.

investors. Companies produce corporate reports so as to give enough information to specific

users of financial statements. Corporate reporting also enables companies to provide information

about how they raise funds and how those funds are utilized in the course of business. Corporate

reporting also helps companies to access debt, equity and other trade finances. Companies

produce corporate reports in order to avail their information concerning the financial position

and financial performance and this makes it useful to a wide range of financial statement users in

evaluating the stewardship of management and be able to make useful economic decisions.

Accounting Standards

Accounting standards can be described as authoritative standards that are used in

financial reporting, (Sapovadia, 2008). Accounting standards are the basic source of the

generally accepted accounting principles, (GAAP). These standards provide specifications of

how transactions and other accounting events should be measured, recognized, presented and

disclosed in companies’ financial statements, (Rayman 2013). Accounting standards are policies

that are imperative to all the accounting activities and they help business to run their activities

smoothly. All companies are required to adhere to the accounting standards set by FASB and

IASB, failure to comply with this standards will lead companies spending on legal action

initiated against it by their governments.

Importance of Accounting Standards in Reporting

Accounting standards enable companies to provide external users such as lenders and

investor, with information which is useful in decision making, (Sugara & Boland, 2011).

Accounting standards help companies to assess their business performance and be able to

compare it with the performance of competitors through the use of financial statements.

CONTEMPORARY CORPORATE REPORTING 4

Accounting standards enable companies to be transparent and by so doing they are able to

perform efficiently in the industry of operation, ( Al Frijat, 2016).

Accounting standards help in protecting the investors interests this is because if

companies adhere to the accounting standards they are able to provide the investors with genuine

and accurate reports which in return increases the investors’ confidence while making economic

decisions because they will have insights of how their money will be spend. Accounting

standards also help to prevent fraud both to the owners of businesses and customers. Accounting

standards also promote accountability and in the end making businesses to be efficient in

business transactions. Companies that adhere well to accounting standards are able to produce

financial statements that enable them to access investor capital. Accounting standards also help

in facilitation of reasonable assessment of business presentation and ensures good record keeping

by companies.

Part B

Introduction to Lucky Lanka Milk Processing Company.

Lucky Lanka milk processing company is situated in Sri Lanka and is majorly focused in

the field of milk processing in its aim to build a healthy nation. The company has a lot of

opportunities to supply its products over Sri Lanka. Its highly skilled and experienced staff uses

vast technology and fresh milk in production. Despite the fact that the company has this unique

features it has managed to acquire only 18% market share. The company currently manufactures

yoghurt and pasteurized milk. The products are of different flavors in yoghurt for example

vanilla, chocolate among others.

Accounting standards enable companies to be transparent and by so doing they are able to

perform efficiently in the industry of operation, ( Al Frijat, 2016).

Accounting standards help in protecting the investors interests this is because if

companies adhere to the accounting standards they are able to provide the investors with genuine

and accurate reports which in return increases the investors’ confidence while making economic

decisions because they will have insights of how their money will be spend. Accounting

standards also help to prevent fraud both to the owners of businesses and customers. Accounting

standards also promote accountability and in the end making businesses to be efficient in

business transactions. Companies that adhere well to accounting standards are able to produce

financial statements that enable them to access investor capital. Accounting standards also help

in facilitation of reasonable assessment of business presentation and ensures good record keeping

by companies.

Part B

Introduction to Lucky Lanka Milk Processing Company.

Lucky Lanka milk processing company is situated in Sri Lanka and is majorly focused in

the field of milk processing in its aim to build a healthy nation. The company has a lot of

opportunities to supply its products over Sri Lanka. Its highly skilled and experienced staff uses

vast technology and fresh milk in production. Despite the fact that the company has this unique

features it has managed to acquire only 18% market share. The company currently manufactures

yoghurt and pasteurized milk. The products are of different flavors in yoghurt for example

vanilla, chocolate among others.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY CORPORATE REPORTING 5

Lucky Lanka operates in a very promising business environment because the country has

enhanced political stability which encourages local manufacturers to continue with productivity.

Due to this factors, the company has potential of investing in different places and succeed. The

economic condition shows that there is a possibility of future economic growth as there is also

enough supply of labor, (Proctor, 2007). The company is also affected by inflation, interest rates

and disposable income.

The target market expectations are very high due to increased consumer knowledge in

consumption of nutritious food. The company majorly deals with the production of nutritious

foods and this is an advantage to them due to fulfilling the social needs of customers. Lucky

Lanka faces stiff competition from top competitors such as New dale, Highland, Lanka milk food

and Kethmale. The customers have high bargaining power because they are aware of other

quality milk products. Threats of few quality milk products in the market and there are no

barriers of new entrance of milk products in the market. Milk products are purchased from a few

selected suppliers which raise the bargaining power of suppliers.

Evaluation of Financial Statements for The Recent Five Years.

The financial statements of the company for the last five years (2017 -2013) have been

prepared using the same accounting standards and same methods of computations which comply

with LKAS 34 interim financial reporting. There have not been any material events which have

been taking place after the balance sheet date which require some adjustments and disclosures in

the financial statements. There have been some little changes in the current classification of

items and where appropriate changes were done for example in the year 2016 and 2017. The

balance sheets produced by the company represent the true economic position of the company.

Lucky Lanka operates in a very promising business environment because the country has

enhanced political stability which encourages local manufacturers to continue with productivity.

Due to this factors, the company has potential of investing in different places and succeed. The

economic condition shows that there is a possibility of future economic growth as there is also

enough supply of labor, (Proctor, 2007). The company is also affected by inflation, interest rates

and disposable income.

The target market expectations are very high due to increased consumer knowledge in

consumption of nutritious food. The company majorly deals with the production of nutritious

foods and this is an advantage to them due to fulfilling the social needs of customers. Lucky

Lanka faces stiff competition from top competitors such as New dale, Highland, Lanka milk food

and Kethmale. The customers have high bargaining power because they are aware of other

quality milk products. Threats of few quality milk products in the market and there are no

barriers of new entrance of milk products in the market. Milk products are purchased from a few

selected suppliers which raise the bargaining power of suppliers.

Evaluation of Financial Statements for The Recent Five Years.

The financial statements of the company for the last five years (2017 -2013) have been

prepared using the same accounting standards and same methods of computations which comply

with LKAS 34 interim financial reporting. There have not been any material events which have

been taking place after the balance sheet date which require some adjustments and disclosures in

the financial statements. There have been some little changes in the current classification of

items and where appropriate changes were done for example in the year 2016 and 2017. The

balance sheets produced by the company represent the true economic position of the company.

CONTEMPORARY CORPORATE REPORTING 6

Property plant and equipment is measured using the revaluation method. The company

reviews the residual values, methods of assets depreciation in each year of reporting. The

company derecognizes assets and financial liabilities. The company applies the carrying value

while measuring the associates and subsidiaries. The company tests the impairment of goodwill

in every financial year. The company prepares financial statements in accordance with Sri Lanka

accounting standards. Depreciation is calculated using straight-line method. Revenues, expenses

and assets are recognized using the net amount of tax. Property plant and equipment are

measured using the fair value. Revenue is measured using the fair value. The company engages

valuation specialists in determining the fair value of assets. Assets are valued over their useful

lives.

Evaluation of Non -Financial Information

Non-financial information deals with social and environmental aspects, (Maj 2018).

Lucky Lanka milk processing company reports on non-financial information. It reports on

corporate governance whereby it describes its decision making systems and how the stakeholders

directly or indirectly control the company activities. The board of directors are committed to

provide and ensuring business integrity and professionalism in all the activities of the business.

The board of directors is comprised of six members whereby two are executive members and

four are the non-executive members. The board members list the rules that are laid down by

Colombo stock exchange and submit the annual dependence declarations. The board members

work on an informed basis, due diligence, good faith and in the best interest of the company.

The company reports on the remuneration of the executive members and it has executive

committee which recommends the remuneration that is payable to the executive members. The

committee sets guidelines for the remuneration of other senior management of the company. The

Property plant and equipment is measured using the revaluation method. The company

reviews the residual values, methods of assets depreciation in each year of reporting. The

company derecognizes assets and financial liabilities. The company applies the carrying value

while measuring the associates and subsidiaries. The company tests the impairment of goodwill

in every financial year. The company prepares financial statements in accordance with Sri Lanka

accounting standards. Depreciation is calculated using straight-line method. Revenues, expenses

and assets are recognized using the net amount of tax. Property plant and equipment are

measured using the fair value. Revenue is measured using the fair value. The company engages

valuation specialists in determining the fair value of assets. Assets are valued over their useful

lives.

Evaluation of Non -Financial Information

Non-financial information deals with social and environmental aspects, (Maj 2018).

Lucky Lanka milk processing company reports on non-financial information. It reports on

corporate governance whereby it describes its decision making systems and how the stakeholders

directly or indirectly control the company activities. The board of directors are committed to

provide and ensuring business integrity and professionalism in all the activities of the business.

The board of directors is comprised of six members whereby two are executive members and

four are the non-executive members. The board members list the rules that are laid down by

Colombo stock exchange and submit the annual dependence declarations. The board members

work on an informed basis, due diligence, good faith and in the best interest of the company.

The company reports on the remuneration of the executive members and it has executive

committee which recommends the remuneration that is payable to the executive members. The

committee sets guidelines for the remuneration of other senior management of the company. The

CONTEMPORARY CORPORATE REPORTING 7

main motive behind this activity is to attract and retain required skilled human resources which

makes the company to be successful and sustain its performance and operations.

The company reports on corporate social responsibility whereby it complies with the

rules, regulations, prescribed practices, procedures, internal policies and ethical standards. The

company has implemented strong risk control and management mechanisms in order to monitor

and make sure that the company complies with rules and laws which are applicable to it. It

conducts internal audits to mitigate possible risks of not complying with the accounting

standards. The company also ensures that it maintains environmental well-being by using

sustainable processing methods.

Critical Analysis of the Company’s Performance

2017 Financial Ratios

Gross profit ratio=Gross profit/revenue *100

435,077,000/1185,145000* 100 =36.71%

Efficiency ratio

Trade receivable days= trade receivables/revenue*365

210,411,000/1185145000*365= 64.80 which is 65days

Liquidity ratio

Current ratio= current assets/current liabilities

448,296,000/453,709,000= 0.988

Gearing ratio= debt/debt + equity

main motive behind this activity is to attract and retain required skilled human resources which

makes the company to be successful and sustain its performance and operations.

The company reports on corporate social responsibility whereby it complies with the

rules, regulations, prescribed practices, procedures, internal policies and ethical standards. The

company has implemented strong risk control and management mechanisms in order to monitor

and make sure that the company complies with rules and laws which are applicable to it. It

conducts internal audits to mitigate possible risks of not complying with the accounting

standards. The company also ensures that it maintains environmental well-being by using

sustainable processing methods.

Critical Analysis of the Company’s Performance

2017 Financial Ratios

Gross profit ratio=Gross profit/revenue *100

435,077,000/1185,145000* 100 =36.71%

Efficiency ratio

Trade receivable days= trade receivables/revenue*365

210,411,000/1185145000*365= 64.80 which is 65days

Liquidity ratio

Current ratio= current assets/current liabilities

448,296,000/453,709,000= 0.988

Gearing ratio= debt/debt + equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY CORPORATE REPORTING 8

306148,000/1280483,000= 0.239

Investor ratio

Return on shareholders= profit available to equity shareholders * 100%

2.69* 100% = 27%%(www.imfgruop.ik,2017)

2016 Financial Ratios

Gross profit ratio=Gross profit/revenue *100

373,124,457/995,245,984* 100 = 37.49%

Efficiency ratio

Trade receivable days= trade receivables/revenue*365

184,657,355/995,245,984* 365 =67.7 which is 68 days

Liquidity ratio

Current ratio= current assets/current liabilities

404,661,953/372,137,858 =1.087

Gearing ratio= debt/debt + equity

227,516840/1142567,000 = 0.1991

Investor ratio

Return on shareholders= profit available to equity shareholders * 100%

2.90 * 100% = 29%%(www.imfgruop.ik,2016)

306148,000/1280483,000= 0.239

Investor ratio

Return on shareholders= profit available to equity shareholders * 100%

2.69* 100% = 27%%(www.imfgruop.ik,2017)

2016 Financial Ratios

Gross profit ratio=Gross profit/revenue *100

373,124,457/995,245,984* 100 = 37.49%

Efficiency ratio

Trade receivable days= trade receivables/revenue*365

184,657,355/995,245,984* 365 =67.7 which is 68 days

Liquidity ratio

Current ratio= current assets/current liabilities

404,661,953/372,137,858 =1.087

Gearing ratio= debt/debt + equity

227,516840/1142567,000 = 0.1991

Investor ratio

Return on shareholders= profit available to equity shareholders * 100%

2.90 * 100% = 29%%(www.imfgruop.ik,2016)

CONTEMPORARY CORPORATE REPORTING 9

2015 Financial Ratios

Gross profit ratio=Gross profit/revenue *100

368,249,352/962,911,905*100 =38.24%

Efficiency ratio

Trade receivable days= trade receivables/revenue*365

182,635,602/962,911,905* 365 = 6.9 which is 7 days

Liquidity ratio

Current ratio= current assets/current liabilities

307,311,982/273,717,660 =1.1227

Gearing ratio= debt/debt + equity

150,332,568/1,002,290,395= 0.15

Investor ratio

Return on shareholders= profit available to equity shareholders * 100%

2.6 * 100 = 26%(www.imfgruop.ik,2015)

2014 Financial Ratios

Gross profit ratio=Gross profit/revenue *100

2015 Financial Ratios

Gross profit ratio=Gross profit/revenue *100

368,249,352/962,911,905*100 =38.24%

Efficiency ratio

Trade receivable days= trade receivables/revenue*365

182,635,602/962,911,905* 365 = 6.9 which is 7 days

Liquidity ratio

Current ratio= current assets/current liabilities

307,311,982/273,717,660 =1.1227

Gearing ratio= debt/debt + equity

150,332,568/1,002,290,395= 0.15

Investor ratio

Return on shareholders= profit available to equity shareholders * 100%

2.6 * 100 = 26%(www.imfgruop.ik,2015)

2014 Financial Ratios

Gross profit ratio=Gross profit/revenue *100

CONTEMPORARY CORPORATE REPORTING 10

365,290,290/893,123,959* 100= 40.9%

Efficiency ratio

Trade receivable days= trade receivables/revenue*365

131,487,736/893,123,959 * 365 =53.49 which is 54 days

Liquidity ratio

Current ratio= current assets/current liabilities

236,561,344/297,667,245 = 0.0008

Gearing ratio= debt/debt + equity

237,201,039/763,101,198 = 0.3108

Investor ratio

Return on shareholders= profit available to equity shareholders * 100%

2.8 * 100 = 28%%(www.imfgruop.ik,2014)

2013 Financial Ratios

Gross profit ratio=Gross profit/revenue *100

331,603,101/837,580,595* 100 =39.59%

Efficiency ratios

Trade receivable days= trade receivables/revenue*365

261,475,963/837,580,595* 365 = 113.94 which is 114 days

365,290,290/893,123,959* 100= 40.9%

Efficiency ratio

Trade receivable days= trade receivables/revenue*365

131,487,736/893,123,959 * 365 =53.49 which is 54 days

Liquidity ratio

Current ratio= current assets/current liabilities

236,561,344/297,667,245 = 0.0008

Gearing ratio= debt/debt + equity

237,201,039/763,101,198 = 0.3108

Investor ratio

Return on shareholders= profit available to equity shareholders * 100%

2.8 * 100 = 28%%(www.imfgruop.ik,2014)

2013 Financial Ratios

Gross profit ratio=Gross profit/revenue *100

331,603,101/837,580,595* 100 =39.59%

Efficiency ratios

Trade receivable days= trade receivables/revenue*365

261,475,963/837,580,595* 365 = 113.94 which is 114 days

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY CORPORATE REPORTING 11

Liquidity ratio

Current ratio= current assets/current liabilities

123,925,116/172,950,759 = 0.7165

Gearing ratio= debt/debt + equity

207,738,887/587,519,465 = 0.3535

Investor ratio

Return on shareholders= profit available to equity shareholders * 100%

2.7 * 100 = 27% (www.imfgruop.ik,2013)

Comparison of the Financial Ratios with Lanka Milk Food

2017 Financial Ratios

Gross profit ratio = 15.04%

Efficiency ratio = 117 days

Liquidity ratio = 1.60

Gearing ratio = 9.72

Investor ratio = 14%(www.imfgruop.ik,2017)

Liquidity ratio

Current ratio= current assets/current liabilities

123,925,116/172,950,759 = 0.7165

Gearing ratio= debt/debt + equity

207,738,887/587,519,465 = 0.3535

Investor ratio

Return on shareholders= profit available to equity shareholders * 100%

2.7 * 100 = 27% (www.imfgruop.ik,2013)

Comparison of the Financial Ratios with Lanka Milk Food

2017 Financial Ratios

Gross profit ratio = 15.04%

Efficiency ratio = 117 days

Liquidity ratio = 1.60

Gearing ratio = 9.72

Investor ratio = 14%(www.imfgruop.ik,2017)

CONTEMPORARY CORPORATE REPORTING 12

2016 Financial Ratios

Gross profit ratio =14.53%

Efficiency ratio= 114 days

Liquidity ratio = 1.02

Gearing ratio = 13.76

Investor ratio = 31% (www.imfgruop.ik,2016)

2015 Financial Ratios

Gross profit ratio = 10.34%

Efficiency ratio = 79 days

Liquidity ratio = 0.71

Gearing ratio = 3.96%

Investor ratio = 20%(www.imfgruop.ik,2015)

2014 Financial Ratios

Gross profit ratio = 10.34%

Efficiency ratio = 70 days

Liquidity ratio = 0.84

2016 Financial Ratios

Gross profit ratio =14.53%

Efficiency ratio= 114 days

Liquidity ratio = 1.02

Gearing ratio = 13.76

Investor ratio = 31% (www.imfgruop.ik,2016)

2015 Financial Ratios

Gross profit ratio = 10.34%

Efficiency ratio = 79 days

Liquidity ratio = 0.71

Gearing ratio = 3.96%

Investor ratio = 20%(www.imfgruop.ik,2015)

2014 Financial Ratios

Gross profit ratio = 10.34%

Efficiency ratio = 70 days

Liquidity ratio = 0.84

CONTEMPORARY CORPORATE REPORTING 13

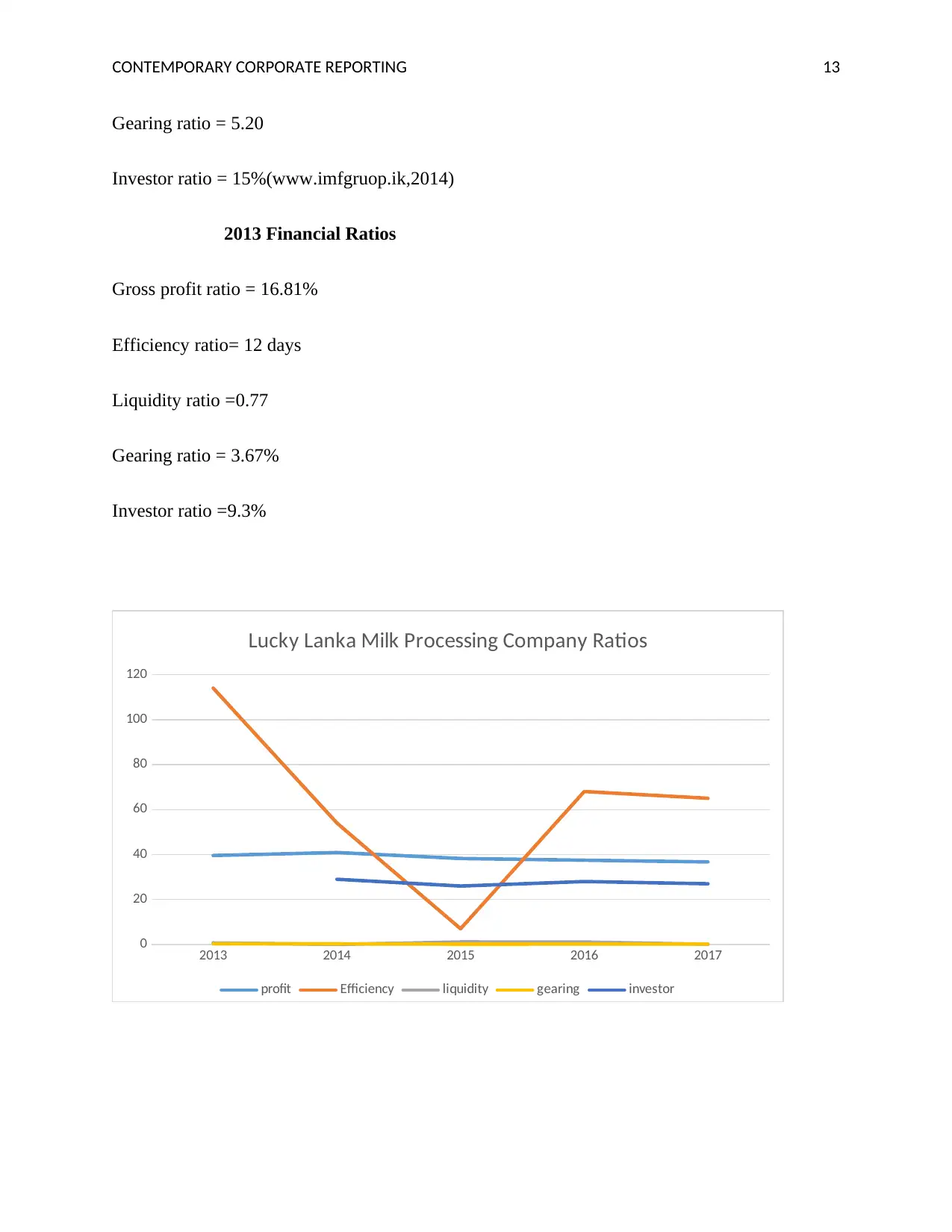

Gearing ratio = 5.20

Investor ratio = 15%(www.imfgruop.ik,2014)

2013 Financial Ratios

Gross profit ratio = 16.81%

Efficiency ratio= 12 days

Liquidity ratio =0.77

Gearing ratio = 3.67%

Investor ratio =9.3%

2013 2014 2015 2016 2017

0

20

40

60

80

100

120

Lucky Lanka Milk Processing Company Ratios

profit Efficiency liquidity gearing investor

Gearing ratio = 5.20

Investor ratio = 15%(www.imfgruop.ik,2014)

2013 Financial Ratios

Gross profit ratio = 16.81%

Efficiency ratio= 12 days

Liquidity ratio =0.77

Gearing ratio = 3.67%

Investor ratio =9.3%

2013 2014 2015 2016 2017

0

20

40

60

80

100

120

Lucky Lanka Milk Processing Company Ratios

profit Efficiency liquidity gearing investor

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY CORPORATE REPORTING 14

2013 2014 2015 2016 2017

0

20

40

60

80

100

120

140

Lanka Milk Food Company ratios

profit efficiency liquidity gearing investor

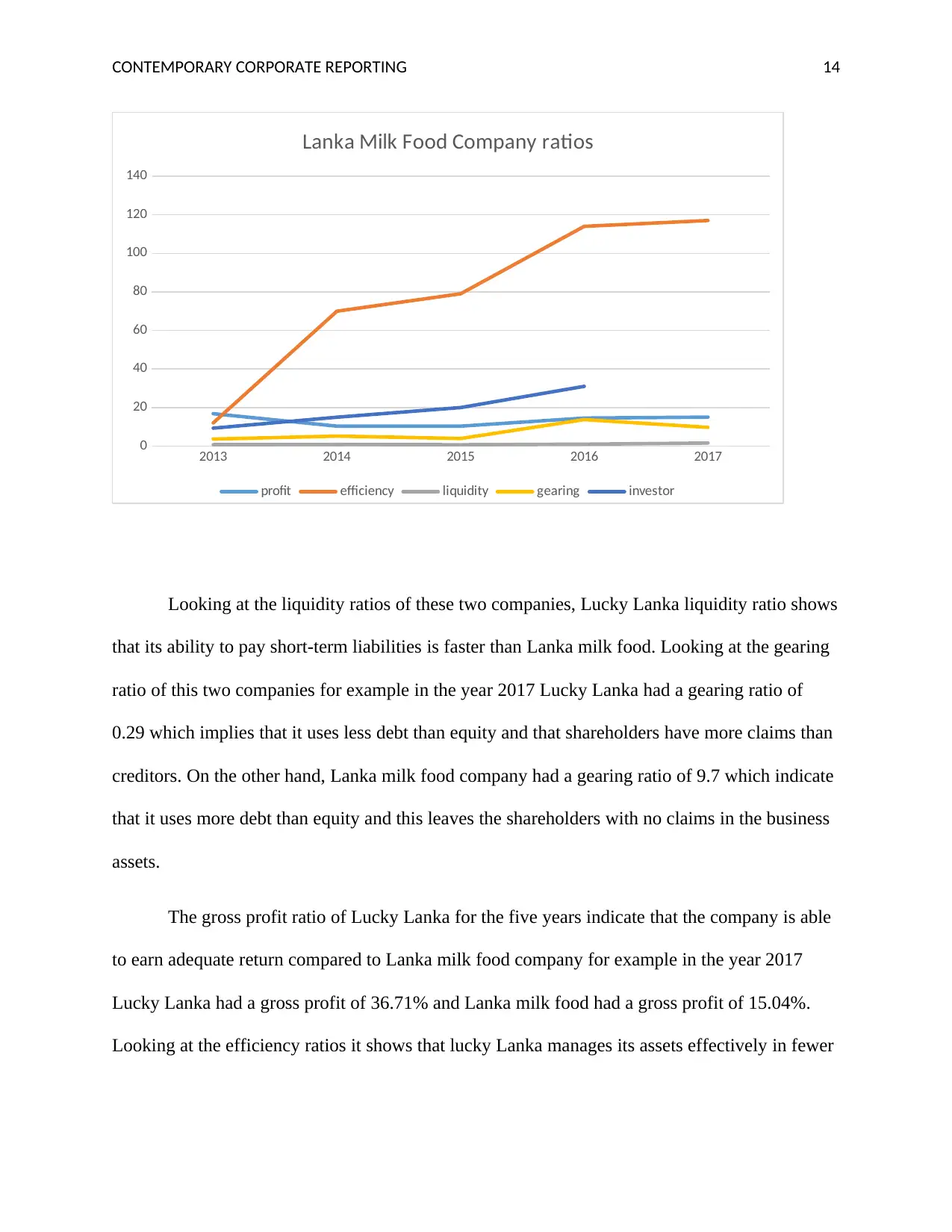

Looking at the liquidity ratios of these two companies, Lucky Lanka liquidity ratio shows

that its ability to pay short-term liabilities is faster than Lanka milk food. Looking at the gearing

ratio of this two companies for example in the year 2017 Lucky Lanka had a gearing ratio of

0.29 which implies that it uses less debt than equity and that shareholders have more claims than

creditors. On the other hand, Lanka milk food company had a gearing ratio of 9.7 which indicate

that it uses more debt than equity and this leaves the shareholders with no claims in the business

assets.

The gross profit ratio of Lucky Lanka for the five years indicate that the company is able

to earn adequate return compared to Lanka milk food company for example in the year 2017

Lucky Lanka had a gross profit of 36.71% and Lanka milk food had a gross profit of 15.04%.

Looking at the efficiency ratios it shows that lucky Lanka manages its assets effectively in fewer

2013 2014 2015 2016 2017

0

20

40

60

80

100

120

140

Lanka Milk Food Company ratios

profit efficiency liquidity gearing investor

Looking at the liquidity ratios of these two companies, Lucky Lanka liquidity ratio shows

that its ability to pay short-term liabilities is faster than Lanka milk food. Looking at the gearing

ratio of this two companies for example in the year 2017 Lucky Lanka had a gearing ratio of

0.29 which implies that it uses less debt than equity and that shareholders have more claims than

creditors. On the other hand, Lanka milk food company had a gearing ratio of 9.7 which indicate

that it uses more debt than equity and this leaves the shareholders with no claims in the business

assets.

The gross profit ratio of Lucky Lanka for the five years indicate that the company is able

to earn adequate return compared to Lanka milk food company for example in the year 2017

Lucky Lanka had a gross profit of 36.71% and Lanka milk food had a gross profit of 15.04%.

Looking at the efficiency ratios it shows that lucky Lanka manages its assets effectively in fewer

CONTEMPORARY CORPORATE REPORTING 15

days (65) compared to Lanka milk food (117 days). The investor ratios show that Lucky Lanka is

able to pay its shareholders more dividends compared to Lanka milk food.

Impression Management.

This deals with how the company ventures in influencing customers’ perception about it,

(Busenbark, Lange & Certo 2017). The company puts strategies to achieve customer loyalty by

offering diversified products and services. It focuses on ensuring healthy life of the nation by

offering products which are of nutritional value to their customers. Lucky Lanka provides its

employees with a better working place and utilizes their capabilities well. It also provides

security for its shareholders.

Lucky Lanka tries to impress the stakeholders by continuously improving their products,

processes, ideas and be able to come up with a more efficient way that enables them to give more

satisfaction to their stakeholders. The company is passionate about customer care in that it is

dedicated to serving customers better than its competitors. The company tries to impress the

employees by establishing teamwork so as to achieve its strategic objective. The company

manages to meet deadlines in terms of work accomplished and this is impressive to stakeholders.

Lucky Lanka upholds democracy from senior management to minor workers as they

adhere to the same rules and regulations. This attracts more highly skilled employees and makes

the company sustain its good performance. It is result driven and this is impressive to the

investors and stakeholders. Good corporate governance and effective internal control helps the

financial statements to be faithful and show the performance of the business in the market.

Lucky Lanka milk processing company manages the image it creates to its customers by

being a market leader in terms of technology, development of products and enhancing its

days (65) compared to Lanka milk food (117 days). The investor ratios show that Lucky Lanka is

able to pay its shareholders more dividends compared to Lanka milk food.

Impression Management.

This deals with how the company ventures in influencing customers’ perception about it,

(Busenbark, Lange & Certo 2017). The company puts strategies to achieve customer loyalty by

offering diversified products and services. It focuses on ensuring healthy life of the nation by

offering products which are of nutritional value to their customers. Lucky Lanka provides its

employees with a better working place and utilizes their capabilities well. It also provides

security for its shareholders.

Lucky Lanka tries to impress the stakeholders by continuously improving their products,

processes, ideas and be able to come up with a more efficient way that enables them to give more

satisfaction to their stakeholders. The company is passionate about customer care in that it is

dedicated to serving customers better than its competitors. The company tries to impress the

employees by establishing teamwork so as to achieve its strategic objective. The company

manages to meet deadlines in terms of work accomplished and this is impressive to stakeholders.

Lucky Lanka upholds democracy from senior management to minor workers as they

adhere to the same rules and regulations. This attracts more highly skilled employees and makes

the company sustain its good performance. It is result driven and this is impressive to the

investors and stakeholders. Good corporate governance and effective internal control helps the

financial statements to be faithful and show the performance of the business in the market.

Lucky Lanka milk processing company manages the image it creates to its customers by

being a market leader in terms of technology, development of products and enhancing its

CONTEMPORARY CORPORATE REPORTING 16

reputation by producing healthy foods. It creates a good perception in the maximization of

shareholders’ wealth through increased profits. Reporting on non-financial information enables it

to create good perception by the users of financial statements and its customers. The activities of

the company portray a true and fair image to its customers.

Recommendations to the Client.

The client should invest in this company. This is because of the company reports of

sustainability and financial information which has shown the true picture of the company

performance. The client can use this information in making an important decision about the

company. There are strong and effective internal controls which ensures that the company works

hard to maximize the shareholders’ wealth.

The company operates in a stable economy with a good possibility of growth in future,

investing in the company implies that an investor will be able to get good earnings per share. A

stable economy with favorable conditions show that the business may not become bankrupt

putting shareholders' wealth at stake. In a stable economy like Sri Lanka, the company has many

opportunities to expand and grow due to its diversified milk products and this is a good indicator

to the client that investing in this company will be useful.

Lucky Lanka milk processing company has a high gross profit ratio which is a good

indicator to an investor of getting high returns. Investing in a company with increased profits

means that the investors will be able to grow because as profits increase the dividends and

earnings per share increases.

The company has high profit compared to its competitors like Lanka Milk food. This

means that it is able to generate income faster than its competitors hence it would be appropriate

reputation by producing healthy foods. It creates a good perception in the maximization of

shareholders’ wealth through increased profits. Reporting on non-financial information enables it

to create good perception by the users of financial statements and its customers. The activities of

the company portray a true and fair image to its customers.

Recommendations to the Client.

The client should invest in this company. This is because of the company reports of

sustainability and financial information which has shown the true picture of the company

performance. The client can use this information in making an important decision about the

company. There are strong and effective internal controls which ensures that the company works

hard to maximize the shareholders’ wealth.

The company operates in a stable economy with a good possibility of growth in future,

investing in the company implies that an investor will be able to get good earnings per share. A

stable economy with favorable conditions show that the business may not become bankrupt

putting shareholders' wealth at stake. In a stable economy like Sri Lanka, the company has many

opportunities to expand and grow due to its diversified milk products and this is a good indicator

to the client that investing in this company will be useful.

Lucky Lanka milk processing company has a high gross profit ratio which is a good

indicator to an investor of getting high returns. Investing in a company with increased profits

means that the investors will be able to grow because as profits increase the dividends and

earnings per share increases.

The company has high profit compared to its competitors like Lanka Milk food. This

means that it is able to generate income faster than its competitors hence it would be appropriate

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY CORPORATE REPORTING 17

to invest in it. The liquidity of the company shows that it can easily convert assets to cash in

order to meet its short-term obligations and so the company may not become bankrupt. This

shows the client or an investor that the company operates efficiently.

Conclusion

To sum up we can say that corporate reporting by companies deals with sustainability

reporting on non- financial information, (Slehat, Alnimer & Abbadi,2013). Companies should

report conduct corporate reporting so as to add value to their financial statements. Companies

which implements corporate reporting make their financial statements to be relevant, authentic

and engaging.

Lucky Lanka Milk processing company deals with the provision of nutritious food to

people. It has a lot of opportunities to spread its market of operation throughout Sri Lanka due to

a stable economy, wide customer base, vast development in technology and due to good

economic policies of the country. Lucky Lanka operates as a market leader in the milk food

industry and this is achieved by timely introduction of new products, identifying competitors

such as Lanka Milk food and developing new diversified milk products.

Lucky Lanka is a company which has managed to impress its customers by providing

them with diversified nutritious foods (www.luckylanka.ik). It maximizes on shareholders’

wealth by meeting deadlines. The company is focused on innovation and builds teamwork so as

to retain their qualified staff to enhance its production. Looking at the gross profit ratio the

company has been able to utilize every shareholders’ rupees and generate income. The company

prepares its annual reports in accordance with the Sri Lanka accounting policies which indicates

that there are strong and effective internal controls.

to invest in it. The liquidity of the company shows that it can easily convert assets to cash in

order to meet its short-term obligations and so the company may not become bankrupt. This

shows the client or an investor that the company operates efficiently.

Conclusion

To sum up we can say that corporate reporting by companies deals with sustainability

reporting on non- financial information, (Slehat, Alnimer & Abbadi,2013). Companies should

report conduct corporate reporting so as to add value to their financial statements. Companies

which implements corporate reporting make their financial statements to be relevant, authentic

and engaging.

Lucky Lanka Milk processing company deals with the provision of nutritious food to

people. It has a lot of opportunities to spread its market of operation throughout Sri Lanka due to

a stable economy, wide customer base, vast development in technology and due to good

economic policies of the country. Lucky Lanka operates as a market leader in the milk food

industry and this is achieved by timely introduction of new products, identifying competitors

such as Lanka Milk food and developing new diversified milk products.

Lucky Lanka is a company which has managed to impress its customers by providing

them with diversified nutritious foods (www.luckylanka.ik). It maximizes on shareholders’

wealth by meeting deadlines. The company is focused on innovation and builds teamwork so as

to retain their qualified staff to enhance its production. Looking at the gross profit ratio the

company has been able to utilize every shareholders’ rupees and generate income. The company

prepares its annual reports in accordance with the Sri Lanka accounting policies which indicates

that there are strong and effective internal controls.

CONTEMPORARY CORPORATE REPORTING 18

References

AL Frijat, Y. (2016). The Dynamics Application of Accounting Standards, and Its Importance in

the Measurement with Fair Value & Disclosure. Asian Journal Of Finance & Accounting,

8(2), 46. doi: 10.5296/ajfa.v8i2.9354

Busenbark , J., Lange, D. and Certo, S. (2017). Foreshadowing as Impression Management:

Illuminating the path for security analysts. Strategic Management Journal, 38(12)

Everingham, G., Kana, S., & Wadee, Z. (2012). Corporate reporting. Cape Town: Juta.

Kaplan Pub. (2014). Corporate reporting. Wokingham, Berkshire.

Lanka milk food plc annual report. (2017). (Online) Retrieved from:

www.imfgroup.ik/downloads/annual20%report%202017

Lanka milk food plc annual report. (2016). (Online) Retrieved from:

www.imfgroup.ik/downloads/annual20%report%202016

Lanka milk food plc annual report. (2015). (Online) Retrieved from:

www.imfgroup.ik/downloads/annual20%report%202015

Lanka milk food plc annual report. (2014). (Online) Retrieved from:

www.imfgroup.ik/downloads/annual20%report%202014

Lanka milk food plc annual report. (2013). (Online) Retrieved from:

www.imfgroup.ik/downloads/annual20%report%202013

References

AL Frijat, Y. (2016). The Dynamics Application of Accounting Standards, and Its Importance in

the Measurement with Fair Value & Disclosure. Asian Journal Of Finance & Accounting,

8(2), 46. doi: 10.5296/ajfa.v8i2.9354

Busenbark , J., Lange, D. and Certo, S. (2017). Foreshadowing as Impression Management:

Illuminating the path for security analysts. Strategic Management Journal, 38(12)

Everingham, G., Kana, S., & Wadee, Z. (2012). Corporate reporting. Cape Town: Juta.

Kaplan Pub. (2014). Corporate reporting. Wokingham, Berkshire.

Lanka milk food plc annual report. (2017). (Online) Retrieved from:

www.imfgroup.ik/downloads/annual20%report%202017

Lanka milk food plc annual report. (2016). (Online) Retrieved from:

www.imfgroup.ik/downloads/annual20%report%202016

Lanka milk food plc annual report. (2015). (Online) Retrieved from:

www.imfgroup.ik/downloads/annual20%report%202015

Lanka milk food plc annual report. (2014). (Online) Retrieved from:

www.imfgroup.ik/downloads/annual20%report%202014

Lanka milk food plc annual report. (2013). (Online) Retrieved from:

www.imfgroup.ik/downloads/annual20%report%202013

CONTEMPORARY CORPORATE REPORTING 19

Lucky Lanka Annual report. (2017). (online). Lucky Lanka milk processing company.

Retrieved from: www.imfgroup.ik/download/annual%report 2017.

Lucky Lanka Annual report. (2016). (online). Lucky Lanka milk processing company.

Retrieved from: www.imfgroup.ik/download/annual%report 2016.

Lucky Lanka Annual report. (2015). (online). Lucky Lanka milk processing company.

Retrieved from: www.imfgroup.ik/download/annual%report 2015.

Lucky Lanka Annual report. (2014). (online). Lucky Lanka milk processing company.

Retrieved from: www.imfgroup.ik/download/annual%report 2014.

Lucky Lanka Annual report. (2013). (online). Lucky Lanka milk processing company.

Retrieved from: www.imfgroup.ik/download/annual%report 2013

Lucky Lanka company overview. (online.). Retrieved from:

www.luckylanka.ik/company-overview

Lee, J., & Maxfield, S. (2015). Doing Well by Reporting Good: Reporting Corporate

Responsibility and Corporate Performance. Business And Society Review, 120(4), 577-

606. doi: 10.1111/basr.12075

Maj, J. (2018). Embedding Diversity in Sustainability Reporting. Sustainability, 10(7), 2487. doi:

10.3390/su10072487

Lucky Lanka Annual report. (2017). (online). Lucky Lanka milk processing company.

Retrieved from: www.imfgroup.ik/download/annual%report 2017.

Lucky Lanka Annual report. (2016). (online). Lucky Lanka milk processing company.

Retrieved from: www.imfgroup.ik/download/annual%report 2016.

Lucky Lanka Annual report. (2015). (online). Lucky Lanka milk processing company.

Retrieved from: www.imfgroup.ik/download/annual%report 2015.

Lucky Lanka Annual report. (2014). (online). Lucky Lanka milk processing company.

Retrieved from: www.imfgroup.ik/download/annual%report 2014.

Lucky Lanka Annual report. (2013). (online). Lucky Lanka milk processing company.

Retrieved from: www.imfgroup.ik/download/annual%report 2013

Lucky Lanka company overview. (online.). Retrieved from:

www.luckylanka.ik/company-overview

Lee, J., & Maxfield, S. (2015). Doing Well by Reporting Good: Reporting Corporate

Responsibility and Corporate Performance. Business And Society Review, 120(4), 577-

606. doi: 10.1111/basr.12075

Maj, J. (2018). Embedding Diversity in Sustainability Reporting. Sustainability, 10(7), 2487. doi:

10.3390/su10072487

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY CORPORATE REPORTING 20

Proctor, T. (2007), Essentials of Marketing Research, Pitman

Rayman, R. (2013). Accounting Standards. Hoboken: Taylor and Francis.

Sapovadia, D. (2008). Relevance, Issues & Importance of Accounting Standards. SSRN

Electronic Journal. doi: 10.2139/ssrn.1245962

Sugahara, S., & Boland, G. (2011). Effects of exposure to the International Education Standards

on perceived importance of the global harmonization of accounting education among

Japanese accounting academics. Advances In Accounting, 27(2), 382-389. doi:

10.1016/j.adiac.2011.08.008

Slehat, N., Alnimer, M., & Abbadi, S. (2013). Incremental Information Content of Financial and

Non-Financial Performance Measures. Dirasat : Administrative Sciences, 40(1), 144-161.

doi:10.12816/0000639

Proctor, T. (2007), Essentials of Marketing Research, Pitman

Rayman, R. (2013). Accounting Standards. Hoboken: Taylor and Francis.

Sapovadia, D. (2008). Relevance, Issues & Importance of Accounting Standards. SSRN

Electronic Journal. doi: 10.2139/ssrn.1245962

Sugahara, S., & Boland, G. (2011). Effects of exposure to the International Education Standards

on perceived importance of the global harmonization of accounting education among

Japanese accounting academics. Advances In Accounting, 27(2), 382-389. doi:

10.1016/j.adiac.2011.08.008

Slehat, N., Alnimer, M., & Abbadi, S. (2013). Incremental Information Content of Financial and

Non-Financial Performance Measures. Dirasat : Administrative Sciences, 40(1), 144-161.

doi:10.12816/0000639

CONTEMPORARY CORPORATE REPORTING 21

Appendixes

Tables

Profit represent the gross profit ratio

Efficiency represent the efficiency ratio

Liquidity represent liquidity ratio

Gearing represent the gearing ratio

Investor represent the Investor ratio

LKAS 34 - Sri Lanka accounting standard 34 interim financial reporting

FASB- Financial accounting standards board

IASB- International accounting standards board

Appendixes

Tables

Profit represent the gross profit ratio

Efficiency represent the efficiency ratio

Liquidity represent liquidity ratio

Gearing represent the gearing ratio

Investor represent the Investor ratio

LKAS 34 - Sri Lanka accounting standard 34 interim financial reporting

FASB- Financial accounting standards board

IASB- International accounting standards board

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.