Corporate Reporting and Financial Analysis: Asset Impairment Report

VerifiedAdded on 2022/11/28

|13

|2628

|255

Report

AI Summary

This report provides a comprehensive analysis of asset impairment, focusing on the application of IAS 36. It begins by defining asset impairment and explaining how it is calculated, including the concepts of carrying value, recoverable amount, and impairment loss. The report then explores the reasons for asset impairment, such as changes in market value, interest rates, technology, and regulations. Using a case study involving an oil drilling platform, the report demonstrates how to apply IAS 36 to determine if an impairment has occurred, considering factors like the carrying amount, potential sale offers, and present value of cash flows. The report also examines the accounting treatment of dismantling costs and revaluation gains. Furthermore, it discusses the practical implementation of the impairment review process, highlighting both its advantages, such as improved stakeholder information, and its current criticisms, such as valuation challenges and a lack of detailed guidance. Finally, the report addresses the impact of acquisitions on financial statements, focusing on the UAE Company's acquisitions of Endomondo and MyFitnessPal. It analyzes the financial effects of these acquisitions, including changes in revenue, expenses, and goodwill, and discusses the potential benefits and impacts on financial statements.

Running head: ADVANCED COPRORATE REPORTING

Advanced Corporate Reporting

Name of the Student:

Name of the University:

Author’s Note:

Advanced Corporate Reporting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE REPORTING

Table of Contents

Question 1........................................................................................................................................2

Question 2........................................................................................................................................7

References......................................................................................................................................10

Table of Contents

Question 1........................................................................................................................................2

Question 2........................................................................................................................................7

References......................................................................................................................................10

2CORPORATE REPORTING

Question 1

a) Impairment of Assets can be well done with the Accounting Standard “IAS 36”, that sets out

the requirement to accounting for reporting and impairment of various non-financial assets of the

company. The IAS 36 specifies the needs to undertake and perform the various impairment test,

recognition of any asset impairment test and the associated disclosures for the company.

Impairment of Assets can be well explained with the help of a sudden or an unexpected fall in

the asset service utility or property. Changes in the legal code, physical damage in the asset,

obsolescence due to technological innovation (ACCA Global 2019).

The impairment value is calculated with the help of the carrying value of the asset and the

fair value of the asset whereby any changes recorded in the value of asset is recorded as an

impairment expenses for the company and the associated amount is charged in the income

statement of the company (Ifrs.org 2019). Impairment losses is the total amount by, which the

total carrying amount exceeds the cash-generation unit or the recoverable amount. The concept

of impairment of assets applies to all the assets except from the assets that arise from the

construction contracts, inventories, deferred tax assets and various other financial assets

(Readyratios.com 2013).

The key reason for the impairment of assets as stated in the IFRS Guidelines and in

accordance with the “IAS 36” is as follows:

i) When the market value for the property declines

ii) Increase in the market rate or prevailing rate of interest

iii) Changes in the technology, economy structure, laws rules and regulations.

Question 1

a) Impairment of Assets can be well done with the Accounting Standard “IAS 36”, that sets out

the requirement to accounting for reporting and impairment of various non-financial assets of the

company. The IAS 36 specifies the needs to undertake and perform the various impairment test,

recognition of any asset impairment test and the associated disclosures for the company.

Impairment of Assets can be well explained with the help of a sudden or an unexpected fall in

the asset service utility or property. Changes in the legal code, physical damage in the asset,

obsolescence due to technological innovation (ACCA Global 2019).

The impairment value is calculated with the help of the carrying value of the asset and the

fair value of the asset whereby any changes recorded in the value of asset is recorded as an

impairment expenses for the company and the associated amount is charged in the income

statement of the company (Ifrs.org 2019). Impairment losses is the total amount by, which the

total carrying amount exceeds the cash-generation unit or the recoverable amount. The concept

of impairment of assets applies to all the assets except from the assets that arise from the

construction contracts, inventories, deferred tax assets and various other financial assets

(Readyratios.com 2013).

The key reason for the impairment of assets as stated in the IFRS Guidelines and in

accordance with the “IAS 36” is as follows:

i) When the market value for the property declines

ii) Increase in the market rate or prevailing rate of interest

iii) Changes in the technology, economy structure, laws rules and regulations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE REPORTING

iv) Asset as a part of restructure that is held for the purpose of disposal

v) Physical Damages or Obsolescence that would be resulting in the changes in the value of the

assets (Ey.com 2019).

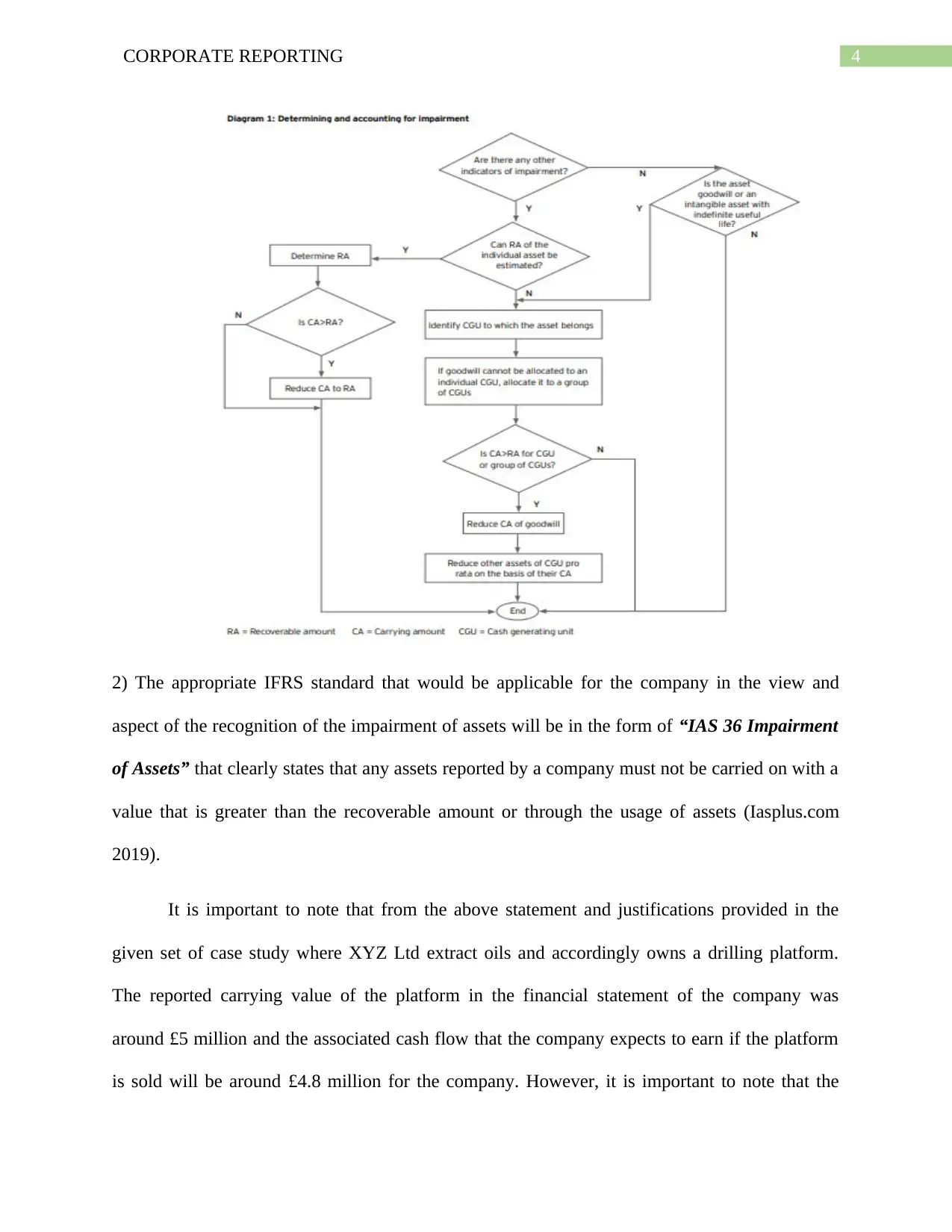

The key requirements of the IAS 38 can be well illustrated in the Diagram presented below:

If there is any slight indication for the asset can be well impaired, the amount

recoverable that would be well compared with the help of the carrying value of the

assets.

The recoverable amount for the company can be well compared with the help of the

carrying value and accordingly the company can take its decision accordingly.

It is important as stated in the Applicable IFRS and IAS 36 that any impairment charges

made by the company should be well accompanied with notes justifying the changes in

the values of assets and the reasons behind the changes in the assets of the company

(Ifrs.org 2019).

iv) Asset as a part of restructure that is held for the purpose of disposal

v) Physical Damages or Obsolescence that would be resulting in the changes in the value of the

assets (Ey.com 2019).

The key requirements of the IAS 38 can be well illustrated in the Diagram presented below:

If there is any slight indication for the asset can be well impaired, the amount

recoverable that would be well compared with the help of the carrying value of the

assets.

The recoverable amount for the company can be well compared with the help of the

carrying value and accordingly the company can take its decision accordingly.

It is important as stated in the Applicable IFRS and IAS 36 that any impairment charges

made by the company should be well accompanied with notes justifying the changes in

the values of assets and the reasons behind the changes in the assets of the company

(Ifrs.org 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE REPORTING

2) The appropriate IFRS standard that would be applicable for the company in the view and

aspect of the recognition of the impairment of assets will be in the form of “IAS 36 Impairment

of Assets” that clearly states that any assets reported by a company must not be carried on with a

value that is greater than the recoverable amount or through the usage of assets (Iasplus.com

2019).

It is important to note that from the above statement and justifications provided in the

given set of case study where XYZ Ltd extract oils and accordingly owns a drilling platform.

The reported carrying value of the platform in the financial statement of the company was

around £5 million and the associated cash flow that the company expects to earn if the platform

is sold will be around £4.8 million for the company. However, it is important to note that the

2) The appropriate IFRS standard that would be applicable for the company in the view and

aspect of the recognition of the impairment of assets will be in the form of “IAS 36 Impairment

of Assets” that clearly states that any assets reported by a company must not be carried on with a

value that is greater than the recoverable amount or through the usage of assets (Iasplus.com

2019).

It is important to note that from the above statement and justifications provided in the

given set of case study where XYZ Ltd extract oils and accordingly owns a drilling platform.

The reported carrying value of the platform in the financial statement of the company was

around £5 million and the associated cash flow that the company expects to earn if the platform

is sold will be around £4.8 million for the company. However, it is important to note that the

5CORPORATE REPORTING

recoverable amount of the value that would be generated by the company with the help of

present value model for the analysis will be around £5.4 million. At the same time it is important

to note that from the above definition stated in the IFRS and IAS 36 can be well linked with the

company’s current situation where company can revalue the asset at £5.4 million and no

impairment loss will be reflected in the books of account for the company.

Thus, at every assessment date of the financials of the company when the assets of the

company are compared or reviewed, which is required by the applicable IFRS and IAS 36, then

in that case the platform would be revalued at £5.4 million and the associated gain which is

around £ 0.6 million (£5.4 million - £4.8 million) would be recognized in the Other

Comprehensive Income which is well applicable with the IAS 16, Property Plant and

Equipment standard”. The standard clearly states that any revaluation associated with

equipment’s or plants should be recognized in the OCI and the associated value would be

associating in the equity balance of the company.

It should be noted, that since the company, did not had any fall in the value of the assets

for the undertaken time period no impairment losses will be shown by the company for the trend

period analyzed. On the other hand, provision for dismantling and extraction would be treated as

a capital expenditure by the company which will be well depreciated over the useful life of the

assets.

3) The review of the impairment of asset is done by the company based on the asset value and

characteristics that are eligible for the purpose of impairment. During the impairment review

process it is important that both the external and internal source of indications taken into account

such as:

recoverable amount of the value that would be generated by the company with the help of

present value model for the analysis will be around £5.4 million. At the same time it is important

to note that from the above definition stated in the IFRS and IAS 36 can be well linked with the

company’s current situation where company can revalue the asset at £5.4 million and no

impairment loss will be reflected in the books of account for the company.

Thus, at every assessment date of the financials of the company when the assets of the

company are compared or reviewed, which is required by the applicable IFRS and IAS 36, then

in that case the platform would be revalued at £5.4 million and the associated gain which is

around £ 0.6 million (£5.4 million - £4.8 million) would be recognized in the Other

Comprehensive Income which is well applicable with the IAS 16, Property Plant and

Equipment standard”. The standard clearly states that any revaluation associated with

equipment’s or plants should be recognized in the OCI and the associated value would be

associating in the equity balance of the company.

It should be noted, that since the company, did not had any fall in the value of the assets

for the undertaken time period no impairment losses will be shown by the company for the trend

period analyzed. On the other hand, provision for dismantling and extraction would be treated as

a capital expenditure by the company which will be well depreciated over the useful life of the

assets.

3) The review of the impairment of asset is done by the company based on the asset value and

characteristics that are eligible for the purpose of impairment. During the impairment review

process it is important that both the external and internal source of indications taken into account

such as:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE REPORTING

External Indication Sources

Decline in the overall value of the market

Changes in the interest rate prevailing in the market

If the associated stock price of a company is comparatively less than the book value of

company.

Changes in technological up gradation, economy, rules & regulations.

Internal Indication Sources

Asset as a key part of restructuring that is held for the purpose of disposal

If there is any reported damage or obsolescence seen in the asset affecting the cash

generating ability of the company.

Poor Economic Performance than the estimated once.

Advantages of Practical Implementation of the Impairment Review Process

Stakeholders especially the shareholders, analysts and investors of the company will be

better informed about the fair value of the assets and the associated information in

association with the assets reported. Any impairment charges that is applicable in

association with the company can be well applied by the company.

Impairment charges reported by the company on a particular asset also shows the extent

of nature that is applied by the company for the purpose of valuation and classification

of the assets of the company.

Current Criticism of Practical Implementation of the Impairment Review Process

External Indication Sources

Decline in the overall value of the market

Changes in the interest rate prevailing in the market

If the associated stock price of a company is comparatively less than the book value of

company.

Changes in technological up gradation, economy, rules & regulations.

Internal Indication Sources

Asset as a key part of restructuring that is held for the purpose of disposal

If there is any reported damage or obsolescence seen in the asset affecting the cash

generating ability of the company.

Poor Economic Performance than the estimated once.

Advantages of Practical Implementation of the Impairment Review Process

Stakeholders especially the shareholders, analysts and investors of the company will be

better informed about the fair value of the assets and the associated information in

association with the assets reported. Any impairment charges that is applicable in

association with the company can be well applied by the company.

Impairment charges reported by the company on a particular asset also shows the extent

of nature that is applied by the company for the purpose of valuation and classification

of the assets of the company.

Current Criticism of Practical Implementation of the Impairment Review Process

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE REPORTING

Measurement of assets can be at time difficult for the companies for the purpose of

measuring and valuing the assets of the company while following the procedure for

impairment process. The common valuation techniques that is applied by the

management of the company for the purpose of valuation of the asset is the current

market value, current cost or the net realisable value approach.

Detailed guidance on the accounting for impairment of various reported assets is quite

scarce, in regard to the process that should be followed or approached for the impairment

process and the applicable disclosures that a company should make in the same context.

Question 2

a) The acquisitions that were made by the UAE Company was Endomondo and MyFitnessPal

platforms that was primarily made in the first quarter of 2015, whereby the company did the

same for the purpose of creating the Connected Fit business (UA Newsroom 2019).

The UAE Company has almost bought 100% stake in the Endomondo Company on 5th

January 2015, which is a Denmark based Company that is in the digital connected fitness

company that would be expanding the various courses of operations under the Connected Fitness

Community. The proposed and the purchase price that was paid up by the UAE Company was

around $85 million. An all total of $1.4 million was treated as acquisition cost which were

treated as a selling, general and various other administrative expenses in the books of accounts of

the company (Beck et al., 2017). The expenses were recognized during the three month time

frame respectively in March 2015 and December 2014.

The UAE Company on 17th March, 2015 acquired MyFitness Pal Company via 100%

acquisition of the outstanding equity, which is a digital nutrition and fitness company. The value

Measurement of assets can be at time difficult for the companies for the purpose of

measuring and valuing the assets of the company while following the procedure for

impairment process. The common valuation techniques that is applied by the

management of the company for the purpose of valuation of the asset is the current

market value, current cost or the net realisable value approach.

Detailed guidance on the accounting for impairment of various reported assets is quite

scarce, in regard to the process that should be followed or approached for the impairment

process and the applicable disclosures that a company should make in the same context.

Question 2

a) The acquisitions that were made by the UAE Company was Endomondo and MyFitnessPal

platforms that was primarily made in the first quarter of 2015, whereby the company did the

same for the purpose of creating the Connected Fit business (UA Newsroom 2019).

The UAE Company has almost bought 100% stake in the Endomondo Company on 5th

January 2015, which is a Denmark based Company that is in the digital connected fitness

company that would be expanding the various courses of operations under the Connected Fitness

Community. The proposed and the purchase price that was paid up by the UAE Company was

around $85 million. An all total of $1.4 million was treated as acquisition cost which were

treated as a selling, general and various other administrative expenses in the books of accounts of

the company (Beck et al., 2017). The expenses were recognized during the three month time

frame respectively in March 2015 and December 2014.

The UAE Company on 17th March, 2015 acquired MyFitness Pal Company via 100%

acquisition of the outstanding equity, which is a digital nutrition and fitness company. The value

8CORPORATE REPORTING

of the total consideration amount for acquisition purpose was around $474.0 million. The

acquisition done by the company, was followed by the increase in the long-term borrowings of

the company and a usage of the revolving credit facility that the company was having (Lee

2015).

b) Potential Advantages

Acquisitions followed by the companies are generally an inorganic growth strategy that is

followed by the company in the due course of their investment and expansion purpose that is

carried on by the company. The revenue for the Connected Fitness Company increased $34.2

million, or 177.8%, to $53.4 million in the stated year2015, from the reported value of $19.2

million in 2014. The increase in the revenue base for the company can be well attributed to the

subsequent acquisitions that was observed in the financial year 2015 by the company. The

acquisitions done by the company helped the company increase the products and services

distributions it has under the current set of business capacity (Prather-Kinsey, Boyar and Hood

2018).

c) Impact of Acquisitions on Group Financial Statements was found as follows:

It is crucial to note that on September 2015, the FASB also has issued an accounting

standard that requires the acquiring company in the process of business combination for

recognizing the adjustments in relation to provisional amount that are being identified in the due

course of the undertaken measurement period. The applicable accounting standard as stated by

the company is not going to materially affect the financial statements of the company (Picker et

al., 2019). However, it is important to note that due to the acquisitions followed by the company

in the financial year impacted various accounts of the company which are as follows:

of the total consideration amount for acquisition purpose was around $474.0 million. The

acquisition done by the company, was followed by the increase in the long-term borrowings of

the company and a usage of the revolving credit facility that the company was having (Lee

2015).

b) Potential Advantages

Acquisitions followed by the companies are generally an inorganic growth strategy that is

followed by the company in the due course of their investment and expansion purpose that is

carried on by the company. The revenue for the Connected Fitness Company increased $34.2

million, or 177.8%, to $53.4 million in the stated year2015, from the reported value of $19.2

million in 2014. The increase in the revenue base for the company can be well attributed to the

subsequent acquisitions that was observed in the financial year 2015 by the company. The

acquisitions done by the company helped the company increase the products and services

distributions it has under the current set of business capacity (Prather-Kinsey, Boyar and Hood

2018).

c) Impact of Acquisitions on Group Financial Statements was found as follows:

It is crucial to note that on September 2015, the FASB also has issued an accounting

standard that requires the acquiring company in the process of business combination for

recognizing the adjustments in relation to provisional amount that are being identified in the due

course of the undertaken measurement period. The applicable accounting standard as stated by

the company is not going to materially affect the financial statements of the company (Picker et

al., 2019). However, it is important to note that due to the acquisitions followed by the company

in the financial year impacted various accounts of the company which are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE REPORTING

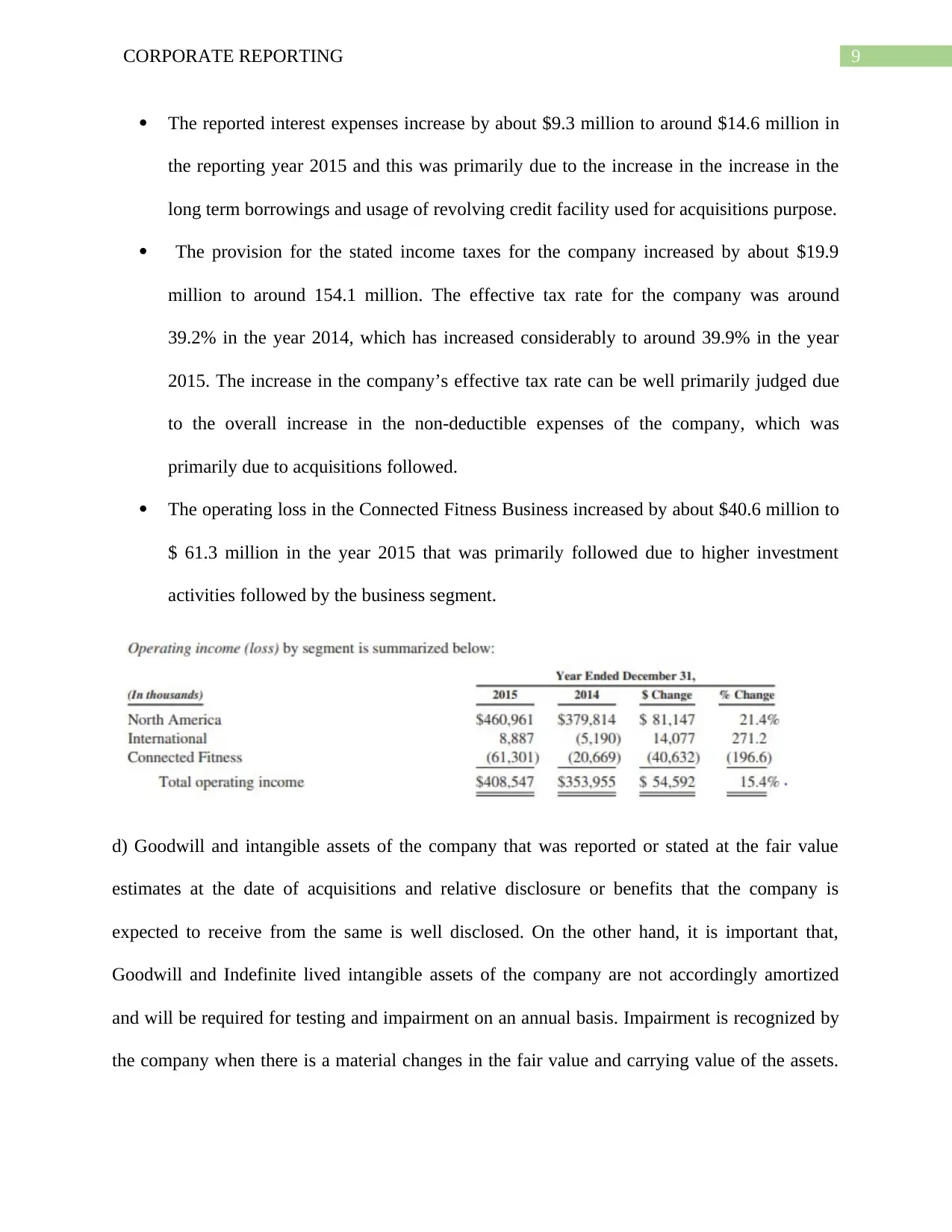

The reported interest expenses increase by about $9.3 million to around $14.6 million in

the reporting year 2015 and this was primarily due to the increase in the increase in the

long term borrowings and usage of revolving credit facility used for acquisitions purpose.

The provision for the stated income taxes for the company increased by about $19.9

million to around 154.1 million. The effective tax rate for the company was around

39.2% in the year 2014, which has increased considerably to around 39.9% in the year

2015. The increase in the company’s effective tax rate can be well primarily judged due

to the overall increase in the non-deductible expenses of the company, which was

primarily due to acquisitions followed.

The operating loss in the Connected Fitness Business increased by about $40.6 million to

$ 61.3 million in the year 2015 that was primarily followed due to higher investment

activities followed by the business segment.

d) Goodwill and intangible assets of the company that was reported or stated at the fair value

estimates at the date of acquisitions and relative disclosure or benefits that the company is

expected to receive from the same is well disclosed. On the other hand, it is important that,

Goodwill and Indefinite lived intangible assets of the company are not accordingly amortized

and will be required for testing and impairment on an annual basis. Impairment is recognized by

the company when there is a material changes in the fair value and carrying value of the assets.

The reported interest expenses increase by about $9.3 million to around $14.6 million in

the reporting year 2015 and this was primarily due to the increase in the increase in the

long term borrowings and usage of revolving credit facility used for acquisitions purpose.

The provision for the stated income taxes for the company increased by about $19.9

million to around 154.1 million. The effective tax rate for the company was around

39.2% in the year 2014, which has increased considerably to around 39.9% in the year

2015. The increase in the company’s effective tax rate can be well primarily judged due

to the overall increase in the non-deductible expenses of the company, which was

primarily due to acquisitions followed.

The operating loss in the Connected Fitness Business increased by about $40.6 million to

$ 61.3 million in the year 2015 that was primarily followed due to higher investment

activities followed by the business segment.

d) Goodwill and intangible assets of the company that was reported or stated at the fair value

estimates at the date of acquisitions and relative disclosure or benefits that the company is

expected to receive from the same is well disclosed. On the other hand, it is important that,

Goodwill and Indefinite lived intangible assets of the company are not accordingly amortized

and will be required for testing and impairment on an annual basis. Impairment is recognized by

the company when there is a material changes in the fair value and carrying value of the assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE REPORTING

The company undertakes various qualitative factors are undertaken into consideration while

following the process of impairment.

It is important to note that as of 31st December 2015, the company has not reported any kind

of goodwill impairment and none of the reporting unit was found to be at a material risky

position.

e) Results of research can be well evaluated with the help of cash flow activities that was

observed for the company for the year 2015:

The cash used in investing activities increased by about $695.2 million to about $847.5 million

in the year 2015, which was around $152.3 million in the year 2014. On the other hand, the cash

used in investing activities of the company decreased by about $85.8 million to around $152.3

million in the year 2014 which was reported to be around $238.1 million in the year 2013.

The company undertakes various qualitative factors are undertaken into consideration while

following the process of impairment.

It is important to note that as of 31st December 2015, the company has not reported any kind

of goodwill impairment and none of the reporting unit was found to be at a material risky

position.

e) Results of research can be well evaluated with the help of cash flow activities that was

observed for the company for the year 2015:

The cash used in investing activities increased by about $695.2 million to about $847.5 million

in the year 2015, which was around $152.3 million in the year 2014. On the other hand, the cash

used in investing activities of the company decreased by about $85.8 million to around $152.3

million in the year 2014 which was reported to be around $238.1 million in the year 2013.

11CORPORATE REPORTING

References

ACCA Global. 2019. https://www.accaglobal.com, A. 2019. Concepts of profit or loss and other

comprehensive income | ACCA Global. [online] Accaglobal.com. Available at:

https://www.accaglobal.com/lk/en/student/exam-support-resources/professional-exams-study-

resources/strategic-business-reporting/technical-articles/pl-concepts.html [Accessed 23 Sep.

2019].

Beck, A.K., Behn, B.K., Lionzo, A. and Rossignoli, F., 2017. Firm Equity Investment Decisions

and US GAAP and IFRS Consolidation Control Guidelines: An Empirical Analysis. Journal of

International Accounting Research, 16(1), pp.37-57.

Ey.com. 2019. [online] Available at:

https://www.ey.com/Publication/vwLUAssets/Impairment_accounting_the_basics_of_IAS_36_I

mpairment_of_Assets/$FILE/Impairment_accounting_IAS_36.pdf [Accessed 23 Sep. 2019].

Iasplus.com. 2019. IAS 36 — Impairment of Assets. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias36 [Accessed 23 Sep. 2019].

Ifrs.org. 2019. IFRS . [online] Available at: https://www.ifrs.org/issued-standards/list-of-

standards/ias-36-impairment-of-assets/ [Accessed 23 Sep. 2019].

Ifrs.org. 2019. IFRS . [online] Available at: https://www.ifrs.org/issued-standards/list-of-

standards/ias-36-impairment-of-assets/ [Accessed 23 Sep. 2019].

References

ACCA Global. 2019. https://www.accaglobal.com, A. 2019. Concepts of profit or loss and other

comprehensive income | ACCA Global. [online] Accaglobal.com. Available at:

https://www.accaglobal.com/lk/en/student/exam-support-resources/professional-exams-study-

resources/strategic-business-reporting/technical-articles/pl-concepts.html [Accessed 23 Sep.

2019].

Beck, A.K., Behn, B.K., Lionzo, A. and Rossignoli, F., 2017. Firm Equity Investment Decisions

and US GAAP and IFRS Consolidation Control Guidelines: An Empirical Analysis. Journal of

International Accounting Research, 16(1), pp.37-57.

Ey.com. 2019. [online] Available at:

https://www.ey.com/Publication/vwLUAssets/Impairment_accounting_the_basics_of_IAS_36_I

mpairment_of_Assets/$FILE/Impairment_accounting_IAS_36.pdf [Accessed 23 Sep. 2019].

Iasplus.com. 2019. IAS 36 — Impairment of Assets. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias36 [Accessed 23 Sep. 2019].

Ifrs.org. 2019. IFRS . [online] Available at: https://www.ifrs.org/issued-standards/list-of-

standards/ias-36-impairment-of-assets/ [Accessed 23 Sep. 2019].

Ifrs.org. 2019. IFRS . [online] Available at: https://www.ifrs.org/issued-standards/list-of-

standards/ias-36-impairment-of-assets/ [Accessed 23 Sep. 2019].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.