HA2032 Corporate & Financial Accounting: Takeover Consolidation

VerifiedAdded on 2023/03/21

|10

|3322

|61

Report

AI Summary

This report evaluates AASB accounting standards relevant to corporate takeovers, focusing on business combinations, intra-company transactions, and non-controlling interest (NCI) guidelines. It uses scholarly articles and consolidation principles to understand these concepts, applying this knowledge to JKY Ltd. to guide its takeover strategies. The report covers equity and consolidation methods, highlighting when each is appropriate based on ownership percentages and influence. It explains how intra-company transactions must be eliminated during consolidation to avoid misstating profits and details the proper disclosure of NCI to provide stakeholders with accurate financial information. The report also provides journal entries to illustrate the accounting treatment of intra-group transactions, dividends, and borrowings. Ultimately, it emphasizes the importance of transparency and accurate financial reporting in corporate takeovers.

Running head: CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON CONSOLIDATION

ACCOUNTING

Name of the Student

Name of the University

Author Note

CONSOLIDATION ACCOUNTING

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON CONSOLIDATION

ACCOUNTING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Executive Summary

The main reason for preparing this report is to evaluate the accounting standards issued by

AASB, which are relevant to the process of taking over another company. Concepts like

combinations in business, intra-company transactions and NCI guidelines form a major part of

the report. These concepts are understood with the help of various scholarly articles and by

following the guidelines involved in the consolidation of financial statements. The knowledge

acquired from these standards is applied in the case of JKY Ltd. to provide guidance to the

company about the best possible measures that it should follow to successfully takeover the

other company. The report concludes by understanding the process of NCI disclosures in the

consolidated statements of accounts.

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Executive Summary

The main reason for preparing this report is to evaluate the accounting standards issued by

AASB, which are relevant to the process of taking over another company. Concepts like

combinations in business, intra-company transactions and NCI guidelines form a major part of

the report. These concepts are understood with the help of various scholarly articles and by

following the guidelines involved in the consolidation of financial statements. The knowledge

acquired from these standards is applied in the case of JKY Ltd. to provide guidance to the

company about the best possible measures that it should follow to successfully takeover the

other company. The report concludes by understanding the process of NCI disclosures in the

consolidated statements of accounts.

2

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Table of Contents

Introduction...........................................................................................................................................3

Response to Part A.............................................................................................................................3

Response to Part B.............................................................................................................................4

Response to part 3..............................................................................................................................6

Issues from Consolidation Process..................................................................................................7

Conclusion............................................................................................................................................8

References...........................................................................................................................................9

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Table of Contents

Introduction...........................................................................................................................................3

Response to Part A.............................................................................................................................3

Response to Part B.............................................................................................................................4

Response to part 3..............................................................................................................................6

Issues from Consolidation Process..................................................................................................7

Conclusion............................................................................................................................................8

References...........................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Introduction

Equity form of accounting is a method that is used to measure the amount that a

holding company has invested in the subsidiary company by measuring the important aspect

called the net value of assets (assets reduced by liabilities) of the subsidiary company. On

the other hand, consolidated method id used when a parent company owns at least 50.1%

share of its subsidiary. About consolidating financial statements, intra-company transactions

refer to transactions that occur between different companies, which are a part of the same

group. These should not be included in the financial statements at the time of consolidation.

Non-controlling interests’ disclosure guidelines suggest that these items should be presented

separately to avoid manipulating the stakeholders of an entity.

Response to Part A

As per the recommendations of AASB 3, the need to improve the transparency,

efficiency, inter-comparability and clarity of the information provided by an organization in its

consolidated financial statements is more than ever before (AASB and CAS 2014).

Accounting methods like consolidation method and equity accounting method are very

popular in preparing the consolidated financial statements (Milojevic, Vukoje and Mihajlovic

2013). However, to be able to obtain a reasonable level of understanding of the functioning of

both these methods, an understanding of the terms that are to be satisfied to apply these

methods, is necessary.

The usage of equity accounting happens when an investor is said to have a key

influence in his investee’s decision-making procedures (Grossi et al. 2013). According to the

5th paragraph in AASB 128, a holding company or otherwise is understood to have a

significant influence in another company if they have a share of at least 20% of the voting

power in the company by stock holding or any other manner. The significant influence can

end at any point of time due to reasons like modifications in capital structure, intervention of

the government or sale of the rights to another party. Using this method, recognition of the

investment first takes place at cost and the difference in balance is modified to present the

profit or loss of the investor in the investment. These modifications take place due to factors

like revaluating the assets; amount paid by investee to investor or because of fluctuations in

foreign currency rates.

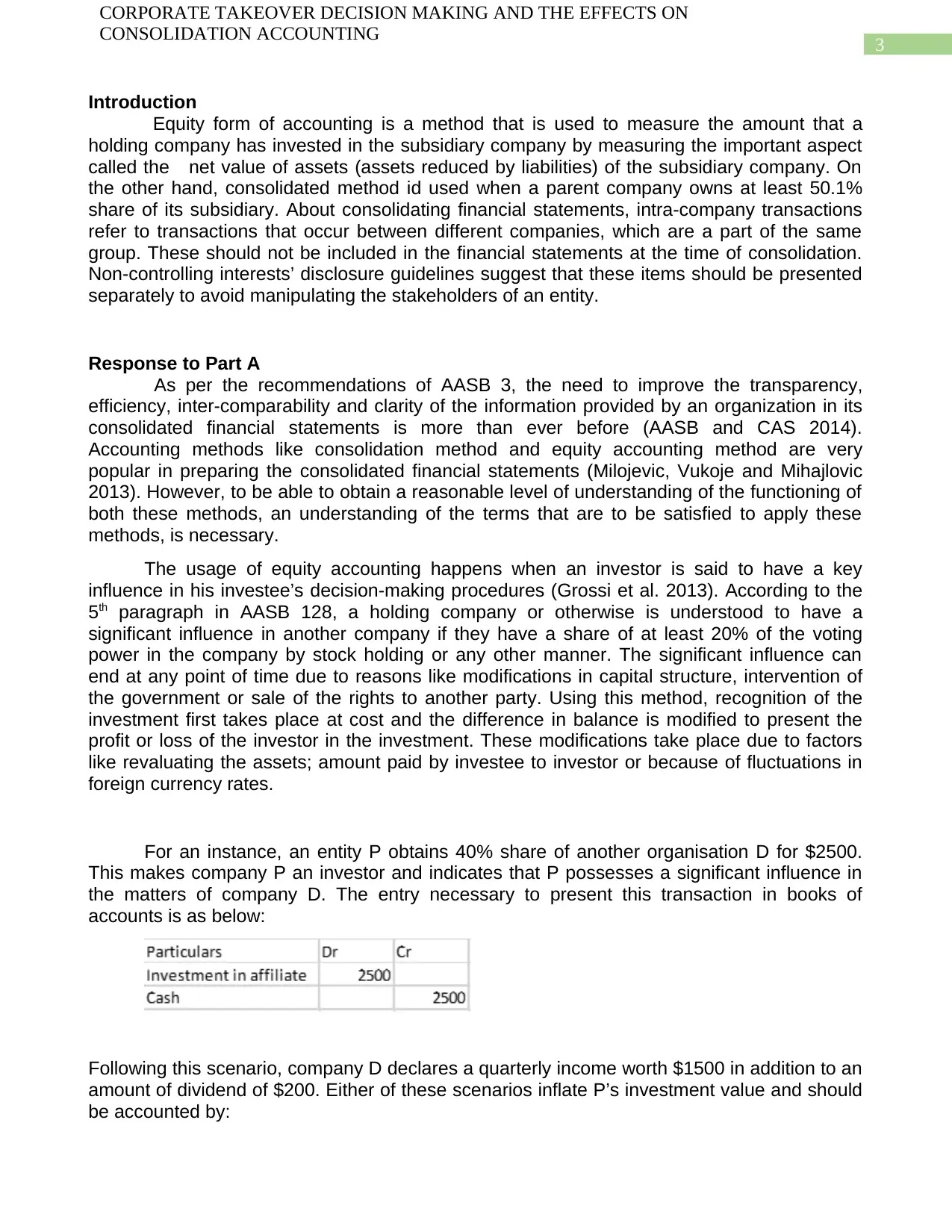

For an instance, an entity P obtains 40% share of another organisation D for $2500.

This makes company P an investor and indicates that P possesses a significant influence in

the matters of company D. The entry necessary to present this transaction in books of

accounts is as below:

Following this scenario, company D declares a quarterly income worth $1500 in addition to an

amount of dividend of $200. Either of these scenarios inflate P’s investment value and should

be accounted by:

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Introduction

Equity form of accounting is a method that is used to measure the amount that a

holding company has invested in the subsidiary company by measuring the important aspect

called the net value of assets (assets reduced by liabilities) of the subsidiary company. On

the other hand, consolidated method id used when a parent company owns at least 50.1%

share of its subsidiary. About consolidating financial statements, intra-company transactions

refer to transactions that occur between different companies, which are a part of the same

group. These should not be included in the financial statements at the time of consolidation.

Non-controlling interests’ disclosure guidelines suggest that these items should be presented

separately to avoid manipulating the stakeholders of an entity.

Response to Part A

As per the recommendations of AASB 3, the need to improve the transparency,

efficiency, inter-comparability and clarity of the information provided by an organization in its

consolidated financial statements is more than ever before (AASB and CAS 2014).

Accounting methods like consolidation method and equity accounting method are very

popular in preparing the consolidated financial statements (Milojevic, Vukoje and Mihajlovic

2013). However, to be able to obtain a reasonable level of understanding of the functioning of

both these methods, an understanding of the terms that are to be satisfied to apply these

methods, is necessary.

The usage of equity accounting happens when an investor is said to have a key

influence in his investee’s decision-making procedures (Grossi et al. 2013). According to the

5th paragraph in AASB 128, a holding company or otherwise is understood to have a

significant influence in another company if they have a share of at least 20% of the voting

power in the company by stock holding or any other manner. The significant influence can

end at any point of time due to reasons like modifications in capital structure, intervention of

the government or sale of the rights to another party. Using this method, recognition of the

investment first takes place at cost and the difference in balance is modified to present the

profit or loss of the investor in the investment. These modifications take place due to factors

like revaluating the assets; amount paid by investee to investor or because of fluctuations in

foreign currency rates.

For an instance, an entity P obtains 40% share of another organisation D for $2500.

This makes company P an investor and indicates that P possesses a significant influence in

the matters of company D. The entry necessary to present this transaction in books of

accounts is as below:

Following this scenario, company D declares a quarterly income worth $1500 in addition to an

amount of dividend of $200. Either of these scenarios inflate P’s investment value and should

be accounted by:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

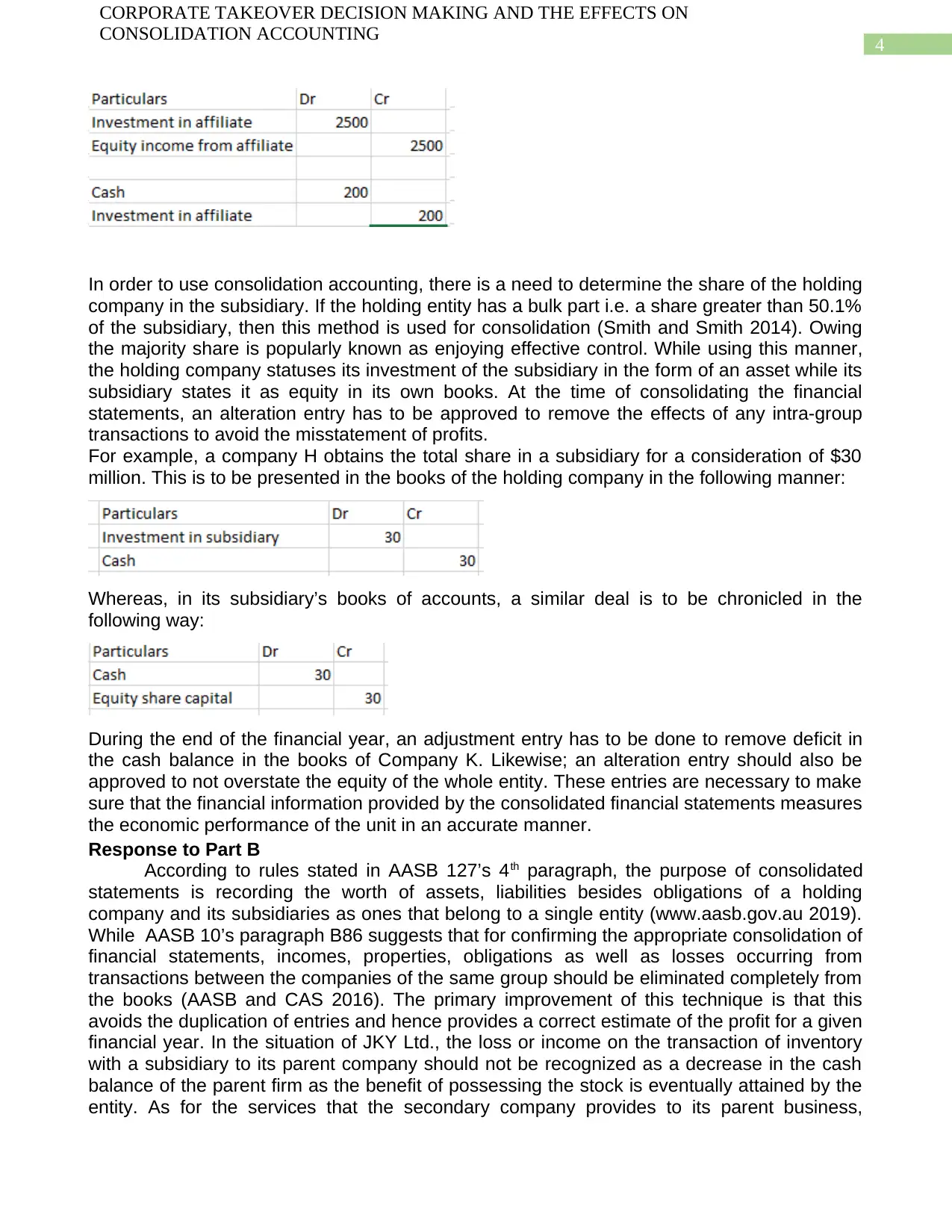

In order to use consolidation accounting, there is a need to determine the share of the holding

company in the subsidiary. If the holding entity has a bulk part i.e. a share greater than 50.1%

of the subsidiary, then this method is used for consolidation (Smith and Smith 2014). Owing

the majority share is popularly known as enjoying effective control. While using this manner,

the holding company statuses its investment of the subsidiary in the form of an asset while its

subsidiary states it as equity in its own books. At the time of consolidating the financial

statements, an alteration entry has to be approved to remove the effects of any intra-group

transactions to avoid the misstatement of profits.

For example, a company H obtains the total share in a subsidiary for a consideration of $30

million. This is to be presented in the books of the holding company in the following manner:

Whereas, in its subsidiary’s books of accounts, a similar deal is to be chronicled in the

following way:

During the end of the financial year, an adjustment entry has to be done to remove deficit in

the cash balance in the books of Company K. Likewise; an alteration entry should also be

approved to not overstate the equity of the whole entity. These entries are necessary to make

sure that the financial information provided by the consolidated financial statements measures

the economic performance of the unit in an accurate manner.

Response to Part B

According to rules stated in AASB 127’s 4th paragraph, the purpose of consolidated

statements is recording the worth of assets, liabilities besides obligations of a holding

company and its subsidiaries as ones that belong to a single entity (www.aasb.gov.au 2019).

While AASB 10’s paragraph B86 suggests that for confirming the appropriate consolidation of

financial statements, incomes, properties, obligations as well as losses occurring from

transactions between the companies of the same group should be eliminated completely from

the books (AASB and CAS 2016). The primary improvement of this technique is that this

avoids the duplication of entries and hence provides a correct estimate of the profit for a given

financial year. In the situation of JKY Ltd., the loss or income on the transaction of inventory

with a subsidiary to its parent company should not be recognized as a decrease in the cash

balance of the parent firm as the benefit of possessing the stock is eventually attained by the

entity. As for the services that the secondary company provides to its parent business,

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

In order to use consolidation accounting, there is a need to determine the share of the holding

company in the subsidiary. If the holding entity has a bulk part i.e. a share greater than 50.1%

of the subsidiary, then this method is used for consolidation (Smith and Smith 2014). Owing

the majority share is popularly known as enjoying effective control. While using this manner,

the holding company statuses its investment of the subsidiary in the form of an asset while its

subsidiary states it as equity in its own books. At the time of consolidating the financial

statements, an alteration entry has to be approved to remove the effects of any intra-group

transactions to avoid the misstatement of profits.

For example, a company H obtains the total share in a subsidiary for a consideration of $30

million. This is to be presented in the books of the holding company in the following manner:

Whereas, in its subsidiary’s books of accounts, a similar deal is to be chronicled in the

following way:

During the end of the financial year, an adjustment entry has to be done to remove deficit in

the cash balance in the books of Company K. Likewise; an alteration entry should also be

approved to not overstate the equity of the whole entity. These entries are necessary to make

sure that the financial information provided by the consolidated financial statements measures

the economic performance of the unit in an accurate manner.

Response to Part B

According to rules stated in AASB 127’s 4th paragraph, the purpose of consolidated

statements is recording the worth of assets, liabilities besides obligations of a holding

company and its subsidiaries as ones that belong to a single entity (www.aasb.gov.au 2019).

While AASB 10’s paragraph B86 suggests that for confirming the appropriate consolidation of

financial statements, incomes, properties, obligations as well as losses occurring from

transactions between the companies of the same group should be eliminated completely from

the books (AASB and CAS 2016). The primary improvement of this technique is that this

avoids the duplication of entries and hence provides a correct estimate of the profit for a given

financial year. In the situation of JKY Ltd., the loss or income on the transaction of inventory

with a subsidiary to its parent company should not be recognized as a decrease in the cash

balance of the parent firm as the benefit of possessing the stock is eventually attained by the

entity. As for the services that the secondary company provides to its parent business,

5

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

recording the same as an expense should be avoided as both the cost of the service and its

benefit belong to the whole entity (Beuselinck and Deloof 2014).

AASB 10’s rules suggest that non-controlling interest (NCI) is understood to be that

part of the segment of the subsidiary firm which does not belong to its parent concern neither

directly nor indirectly. In order to calculate the NCI of an establishment for a specified financial

year, all kinds of intra-company dealings have to be detached completely and there is no part

that the proportion of the holding or subsidiary business plays. Although, while distributing the

dividends, their distribution takes place in accordance with the portion of the parent company

in its subsidiary without using any other manner (Presentation of Financial Statements, 2016).

In case of JKY Ltd., NCI should be calculated by deducting the gains on the sale of stock and

the consideration for the facilities delivered by its subsidiary completely.

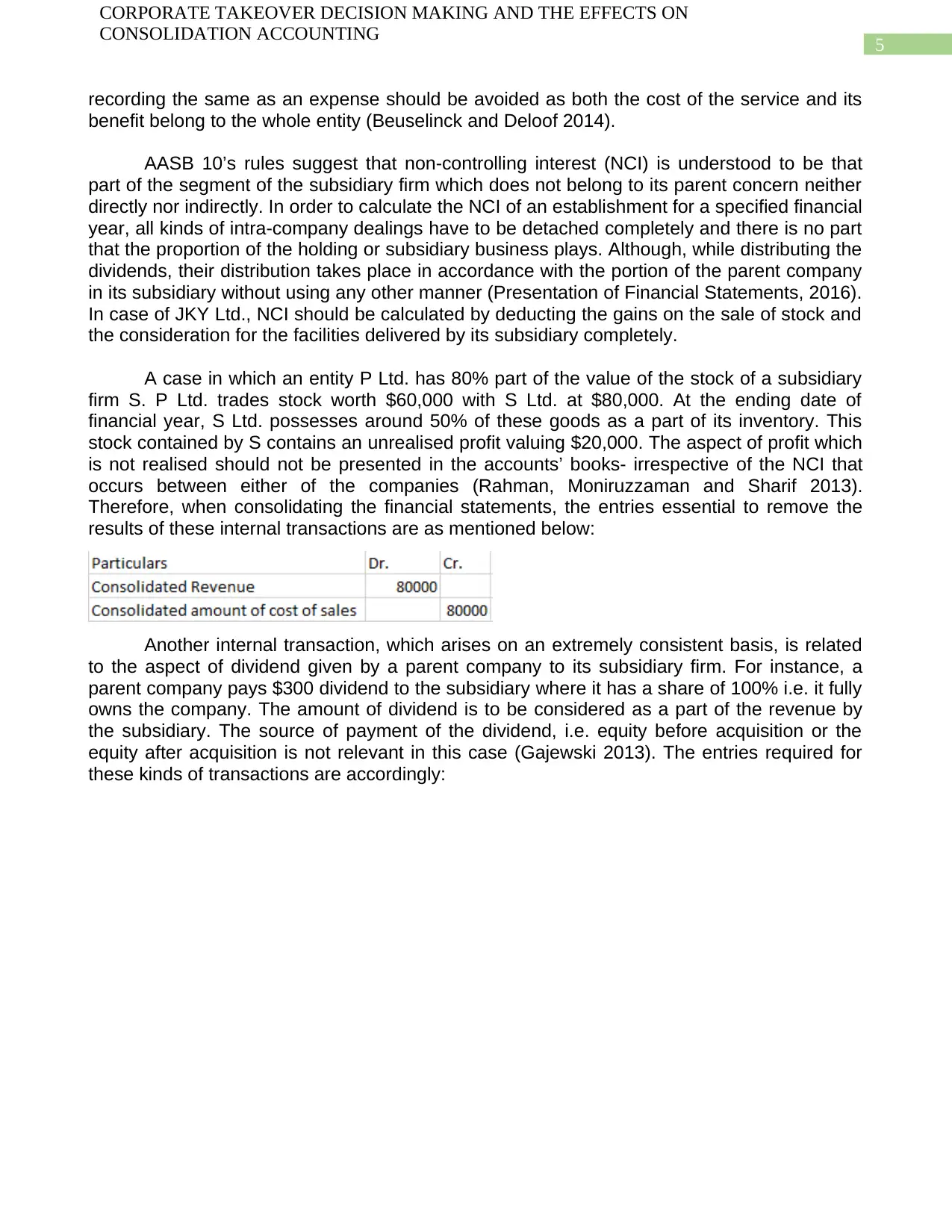

A case in which an entity P Ltd. has 80% part of the value of the stock of a subsidiary

firm S. P Ltd. trades stock worth $60,000 with S Ltd. at $80,000. At the ending date of

financial year, S Ltd. possesses around 50% of these goods as a part of its inventory. This

stock contained by S contains an unrealised profit valuing $20,000. The aspect of profit which

is not realised should not be presented in the accounts’ books- irrespective of the NCI that

occurs between either of the companies (Rahman, Moniruzzaman and Sharif 2013).

Therefore, when consolidating the financial statements, the entries essential to remove the

results of these internal transactions are as mentioned below:

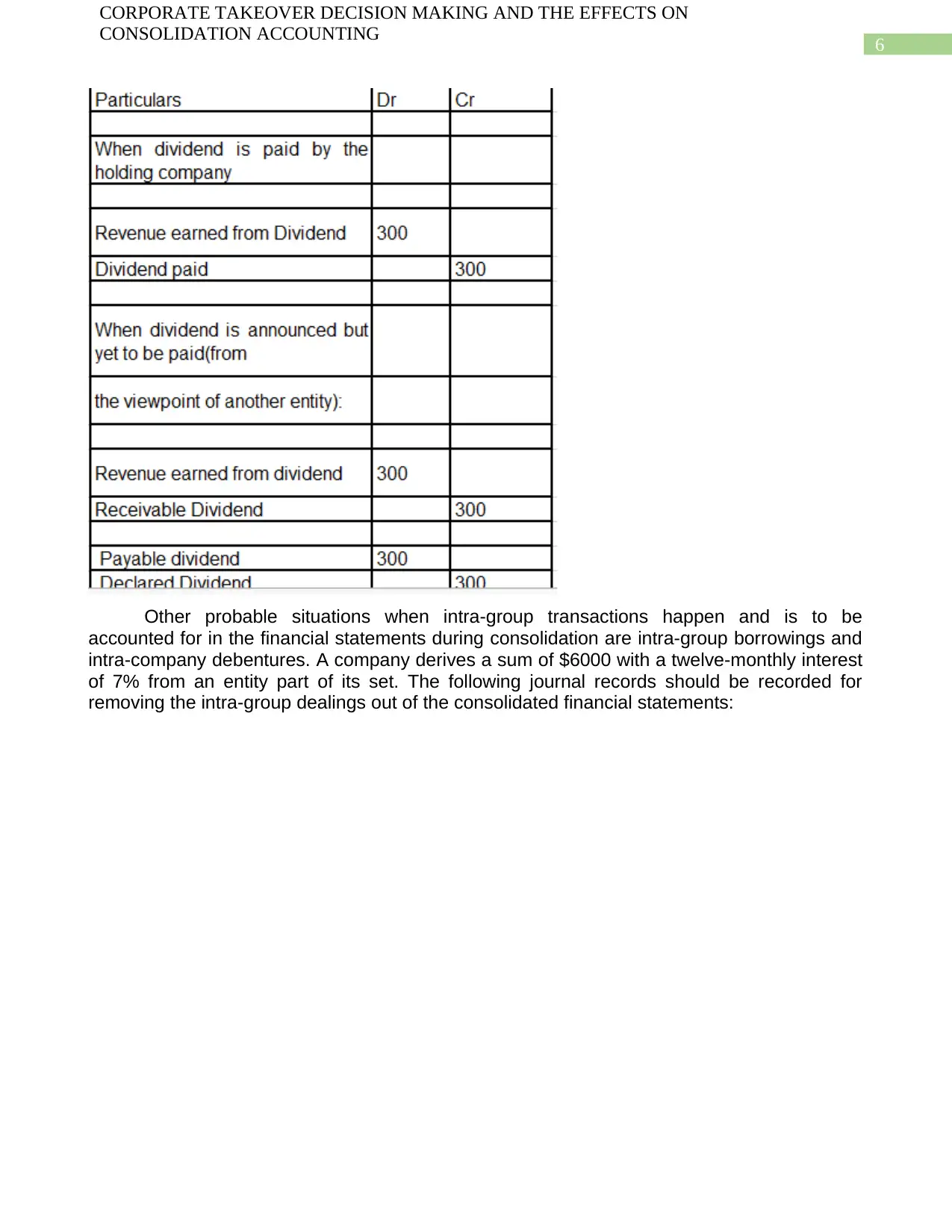

Another internal transaction, which arises on an extremely consistent basis, is related

to the aspect of dividend given by a parent company to its subsidiary firm. For instance, a

parent company pays $300 dividend to the subsidiary where it has a share of 100% i.e. it fully

owns the company. The amount of dividend is to be considered as a part of the revenue by

the subsidiary. The source of payment of the dividend, i.e. equity before acquisition or the

equity after acquisition is not relevant in this case (Gajewski 2013). The entries required for

these kinds of transactions are accordingly:

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

recording the same as an expense should be avoided as both the cost of the service and its

benefit belong to the whole entity (Beuselinck and Deloof 2014).

AASB 10’s rules suggest that non-controlling interest (NCI) is understood to be that

part of the segment of the subsidiary firm which does not belong to its parent concern neither

directly nor indirectly. In order to calculate the NCI of an establishment for a specified financial

year, all kinds of intra-company dealings have to be detached completely and there is no part

that the proportion of the holding or subsidiary business plays. Although, while distributing the

dividends, their distribution takes place in accordance with the portion of the parent company

in its subsidiary without using any other manner (Presentation of Financial Statements, 2016).

In case of JKY Ltd., NCI should be calculated by deducting the gains on the sale of stock and

the consideration for the facilities delivered by its subsidiary completely.

A case in which an entity P Ltd. has 80% part of the value of the stock of a subsidiary

firm S. P Ltd. trades stock worth $60,000 with S Ltd. at $80,000. At the ending date of

financial year, S Ltd. possesses around 50% of these goods as a part of its inventory. This

stock contained by S contains an unrealised profit valuing $20,000. The aspect of profit which

is not realised should not be presented in the accounts’ books- irrespective of the NCI that

occurs between either of the companies (Rahman, Moniruzzaman and Sharif 2013).

Therefore, when consolidating the financial statements, the entries essential to remove the

results of these internal transactions are as mentioned below:

Another internal transaction, which arises on an extremely consistent basis, is related

to the aspect of dividend given by a parent company to its subsidiary firm. For instance, a

parent company pays $300 dividend to the subsidiary where it has a share of 100% i.e. it fully

owns the company. The amount of dividend is to be considered as a part of the revenue by

the subsidiary. The source of payment of the dividend, i.e. equity before acquisition or the

equity after acquisition is not relevant in this case (Gajewski 2013). The entries required for

these kinds of transactions are accordingly:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

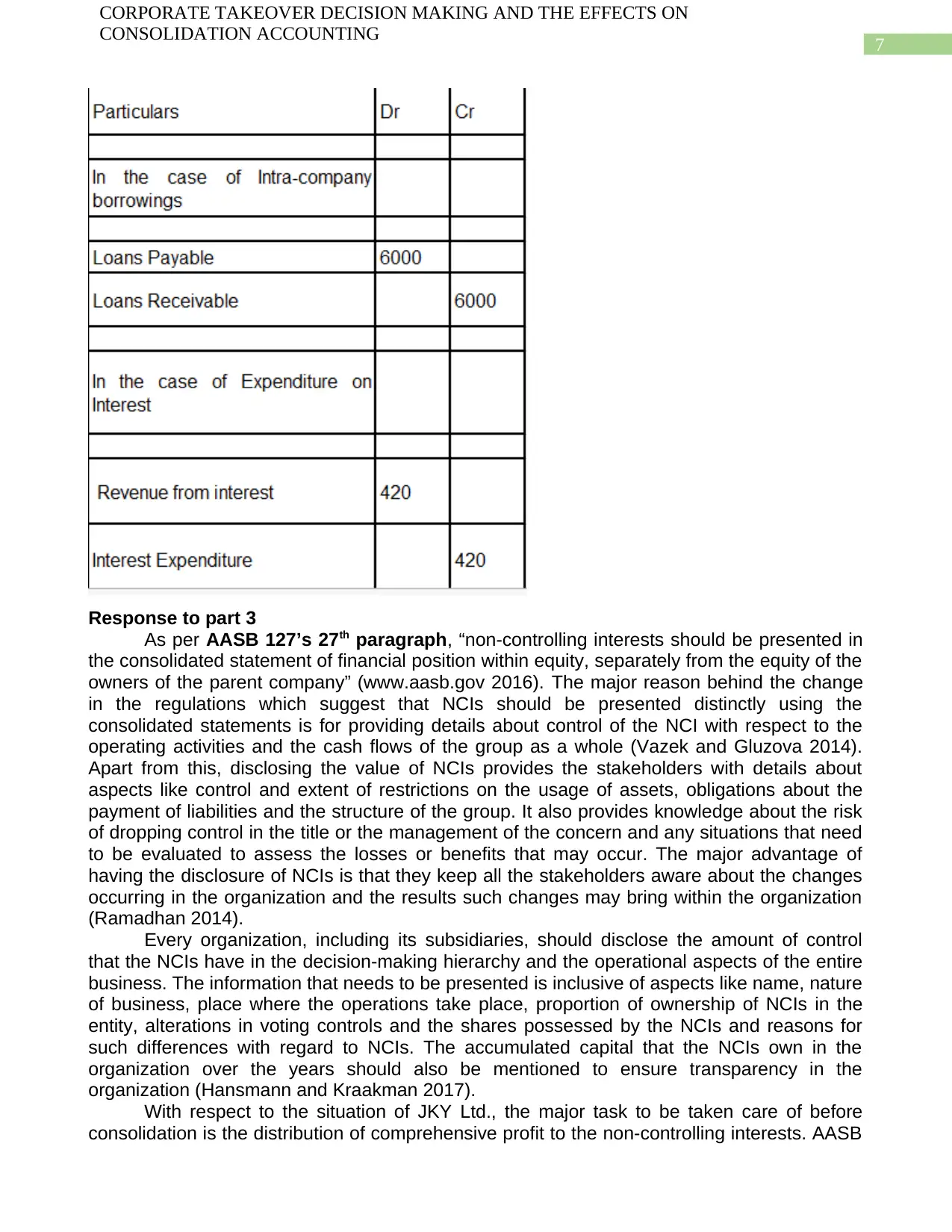

Other probable situations when intra-group transactions happen and is to be

accounted for in the financial statements during consolidation are intra-group borrowings and

intra-company debentures. A company derives a sum of $6000 with a twelve-monthly interest

of 7% from an entity part of its set. The following journal records should be recorded for

removing the intra-group dealings out of the consolidated financial statements:

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Other probable situations when intra-group transactions happen and is to be

accounted for in the financial statements during consolidation are intra-group borrowings and

intra-company debentures. A company derives a sum of $6000 with a twelve-monthly interest

of 7% from an entity part of its set. The following journal records should be recorded for

removing the intra-group dealings out of the consolidated financial statements:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Response to part 3

As per AASB 127’s 27th paragraph, “non-controlling interests should be presented in

the consolidated statement of financial position within equity, separately from the equity of the

owners of the parent company” (www.aasb.gov 2016). The major reason behind the change

in the regulations which suggest that NCIs should be presented distinctly using the

consolidated statements is for providing details about control of the NCI with respect to the

operating activities and the cash flows of the group as a whole (Vazek and Gluzova 2014).

Apart from this, disclosing the value of NCIs provides the stakeholders with details about

aspects like control and extent of restrictions on the usage of assets, obligations about the

payment of liabilities and the structure of the group. It also provides knowledge about the risk

of dropping control in the title or the management of the concern and any situations that need

to be evaluated to assess the losses or benefits that may occur. The major advantage of

having the disclosure of NCIs is that they keep all the stakeholders aware about the changes

occurring in the organization and the results such changes may bring within the organization

(Ramadhan 2014).

Every organization, including its subsidiaries, should disclose the amount of control

that the NCIs have in the decision-making hierarchy and the operational aspects of the entire

business. The information that needs to be presented is inclusive of aspects like name, nature

of business, place where the operations take place, proportion of ownership of NCIs in the

entity, alterations in voting controls and the shares possessed by the NCIs and reasons for

such differences with regard to NCIs. The accumulated capital that the NCIs own in the

organization over the years should also be mentioned to ensure transparency in the

organization (Hansmann and Kraakman 2017).

With respect to the situation of JKY Ltd., the major task to be taken care of before

consolidation is the distribution of comprehensive profit to the non-controlling interests. AASB

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Response to part 3

As per AASB 127’s 27th paragraph, “non-controlling interests should be presented in

the consolidated statement of financial position within equity, separately from the equity of the

owners of the parent company” (www.aasb.gov 2016). The major reason behind the change

in the regulations which suggest that NCIs should be presented distinctly using the

consolidated statements is for providing details about control of the NCI with respect to the

operating activities and the cash flows of the group as a whole (Vazek and Gluzova 2014).

Apart from this, disclosing the value of NCIs provides the stakeholders with details about

aspects like control and extent of restrictions on the usage of assets, obligations about the

payment of liabilities and the structure of the group. It also provides knowledge about the risk

of dropping control in the title or the management of the concern and any situations that need

to be evaluated to assess the losses or benefits that may occur. The major advantage of

having the disclosure of NCIs is that they keep all the stakeholders aware about the changes

occurring in the organization and the results such changes may bring within the organization

(Ramadhan 2014).

Every organization, including its subsidiaries, should disclose the amount of control

that the NCIs have in the decision-making hierarchy and the operational aspects of the entire

business. The information that needs to be presented is inclusive of aspects like name, nature

of business, place where the operations take place, proportion of ownership of NCIs in the

entity, alterations in voting controls and the shares possessed by the NCIs and reasons for

such differences with regard to NCIs. The accumulated capital that the NCIs own in the

organization over the years should also be mentioned to ensure transparency in the

organization (Hansmann and Kraakman 2017).

With respect to the situation of JKY Ltd., the major task to be taken care of before

consolidation is the distribution of comprehensive profit to the non-controlling interests. AASB

8

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

101 also suggests that irrespective of the possibility that NCI could deal with undesirable

balances in their accounts’ books, comprehensive profit has to be appropriately apportioned

between the parent company’s owners as well as the NCIs of the entity. Since it is mentioned

that the subsidiary registers its assets using the method of historic costing, depreciation or the

amount of amortization should be deducted correctly before arriving at the amount of

comprehensive profit earned in a given financial year. Comprehensive income is slightly

different from comprehensive profit in the sense that it is allocated to both the subsidiary and

the owners of the parent in accordance with their shares in its subsidiary enterprise (Bratten,

Causholli and Khan 2016).

In case of any changes in a share held by the NCIs in a subsidiary company, the same

should be specified in the financial reports to reflect changes in capital structure of the

organization. This is to benefit the stakeholders with an understanding of the probable change

in benefits, which may occur. This is to be treated by computing the alteration between the

additional portion obtained by the NCI and the amount paid by them for obtaining such share.

The difference becomes the income of the holding company’s owners (Cordazzo 2013).

In cases where a parent company loses control of the subsidiary to the NCIs, it should

stop recognizing the assets and obligations of that entity on the date when control of such

kind ceases to exist, in addition to its interests in the previous subsidiaries (Ioannou and

Serafeim 2017). Any amount that it receives as a part of the compensation for losing the

control is to be recognized in its books of accounts by the subsidiary company. The remaining

amount of the investment in the subsidiary should also be clearly stated.

Issues from Consolidation Process

Although consolidation intends to increase the transparency with which a business is to

be conducted, its reliability becomes questionable in many practical situations. In the modern

day business scenario, every major corporation has a large number of subsidiaries operating

under it. Determining and mentioning the amount of NCI in every subsidiary’s case becomes

tedious and pointless after a certain time. This also leads to the wastage of time and

capabilities of the personnel. The lack of exact application of the procedures at the time of

consolidation makes the information provided by the consolidated financial statements

redundant (Allen, Gu and Kowalewski 2013). Bogus firms are a major cause of obtaining tax

benefits and manipulating profits for most of the major companies. Enron is the biggest

example of the disadvantages of having a large number of subsidiaries.

Conclusion

From the above discussion, it can be concluded that consolidated and equity

accounting have their own set of benefits and disadvantages. They should be applied

according to the limitations mentioned by the guidelines of AASB to get effective results at the

time of consolidation. Benefits or damages incurred from intra-group transactions have to be

exempted from being a part of the consolidated statements as they lead to the statement of

misleading profits and losses because of passing the same entries twice in the books. In

previous years, there was never enough emphasis on statement of NCIs. The change in this

scenario is expected to cause an improvement in the quality required in the presentation of

consolidated financial statements.

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

101 also suggests that irrespective of the possibility that NCI could deal with undesirable

balances in their accounts’ books, comprehensive profit has to be appropriately apportioned

between the parent company’s owners as well as the NCIs of the entity. Since it is mentioned

that the subsidiary registers its assets using the method of historic costing, depreciation or the

amount of amortization should be deducted correctly before arriving at the amount of

comprehensive profit earned in a given financial year. Comprehensive income is slightly

different from comprehensive profit in the sense that it is allocated to both the subsidiary and

the owners of the parent in accordance with their shares in its subsidiary enterprise (Bratten,

Causholli and Khan 2016).

In case of any changes in a share held by the NCIs in a subsidiary company, the same

should be specified in the financial reports to reflect changes in capital structure of the

organization. This is to benefit the stakeholders with an understanding of the probable change

in benefits, which may occur. This is to be treated by computing the alteration between the

additional portion obtained by the NCI and the amount paid by them for obtaining such share.

The difference becomes the income of the holding company’s owners (Cordazzo 2013).

In cases where a parent company loses control of the subsidiary to the NCIs, it should

stop recognizing the assets and obligations of that entity on the date when control of such

kind ceases to exist, in addition to its interests in the previous subsidiaries (Ioannou and

Serafeim 2017). Any amount that it receives as a part of the compensation for losing the

control is to be recognized in its books of accounts by the subsidiary company. The remaining

amount of the investment in the subsidiary should also be clearly stated.

Issues from Consolidation Process

Although consolidation intends to increase the transparency with which a business is to

be conducted, its reliability becomes questionable in many practical situations. In the modern

day business scenario, every major corporation has a large number of subsidiaries operating

under it. Determining and mentioning the amount of NCI in every subsidiary’s case becomes

tedious and pointless after a certain time. This also leads to the wastage of time and

capabilities of the personnel. The lack of exact application of the procedures at the time of

consolidation makes the information provided by the consolidated financial statements

redundant (Allen, Gu and Kowalewski 2013). Bogus firms are a major cause of obtaining tax

benefits and manipulating profits for most of the major companies. Enron is the biggest

example of the disadvantages of having a large number of subsidiaries.

Conclusion

From the above discussion, it can be concluded that consolidated and equity

accounting have their own set of benefits and disadvantages. They should be applied

according to the limitations mentioned by the guidelines of AASB to get effective results at the

time of consolidation. Benefits or damages incurred from intra-group transactions have to be

exempted from being a part of the consolidated statements as they lead to the statement of

misleading profits and losses because of passing the same entries twice in the books. In

previous years, there was never enough emphasis on statement of NCIs. The change in this

scenario is expected to cause an improvement in the quality required in the presentation of

consolidated financial statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

References

AASB, C.A.S., 2014. Business Combinations. Disclosure, 66, p.77.

AASB, C.A.S., 2016. Consolidated Financial Statements

Aasb.gov.au. (2019). [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed 25 Jun.

2019].

Aasb.gov.au. (2019). [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 25 Jun.

2019].

Allen, F., Gu, X. and Kowalewski, O., 2013. Corporate governance and intra-group

transactions in European bank holding companies during the crisis. In Global Banking,

Financial Markets and Crises (pp. 365-431). Emerald Group Publishing Limited.

Beuselinck, C. and Deloof, M., 2014. Earnings management in business groups: Tax

incentives or expropriation concealment?. The International Journal of Accounting, 49(1),

pp.27-52.

Bratten, B., Causholli, M. and Khan, U., 2016. Usefulness of fair values for predicting banks’

future earnings: evidence from other comprehensive income and its components. Review of

Accounting Studies, 21(1), pp.280-315.

Cordazzo, M., 2013. The impact of IFRS on net income and equity: evidence from Italian

listed companies. Journal of Applied Accounting Research, 14(1), pp.54-73.

Gajewski, D., 2013. The Holding Company as an Instrument of Companies’ Tax-Financial

Policy Formation. Contemporary Economics, 7(1), pp.75-82.

Grossi, G., Bergmann, A., Rauskala, I. and Fuchs, S., 2013. „Applying the equity method as a

means of consolidation in the public sector: experiences in OECD countries”. Journal of

Commerce and Management, 16(2), pp.95-115.

Hansmann, H. and Kraakman, R., 2017. The end of history for corporate law. In Corporate

Governance (pp. 49-78). Gower.

Ioannou, I. and Serafeim, G., 2017. The consequences of mandatory corporate sustainability

reporting. Harvard Business School research working paper, (11-100).

Milojević, I., Vukoje, A. and Mihajlović, M., 2013. Accounting consolidation of the balance by

the acquisition method. Economics of Agriculture, 60(297-2016-3534), p.237.

Rahman, M. M., Moniruzzaman, M., & Sharif, M. J. (2013). Techniques, motives and controls

of earnings management. International Journal of Information Technology and Business

Management, 11(1), 22-34.

Ramadhan, S., 2014. Board composition, audit committees, ownership structure and

voluntary disclosure: Evidence from Bahrain. Research Journal of Finance and

Accounting, 5(7), pp.124-139.

Smith, S.R. and Smith, K.R., 2014. The journey from historical cost accounting to fair value

accounting: the case of acquisition costs. Journal of Business & Accounting, 7(1), pp.3-10.

Vašek, L. and Gluzová, T., 2014. Can a New Concept of Control under IFRS Have an Impact

on a CCCTB?. European Financial and Accounting Journal, 9(4), pp.110-127.

www.aasb.gov.au. (2019). [Ebook]. Retrieved from

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-11_COMPjan15_07-15.pdf

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

References

AASB, C.A.S., 2014. Business Combinations. Disclosure, 66, p.77.

AASB, C.A.S., 2016. Consolidated Financial Statements

Aasb.gov.au. (2019). [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed 25 Jun.

2019].

Aasb.gov.au. (2019). [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 25 Jun.

2019].

Allen, F., Gu, X. and Kowalewski, O., 2013. Corporate governance and intra-group

transactions in European bank holding companies during the crisis. In Global Banking,

Financial Markets and Crises (pp. 365-431). Emerald Group Publishing Limited.

Beuselinck, C. and Deloof, M., 2014. Earnings management in business groups: Tax

incentives or expropriation concealment?. The International Journal of Accounting, 49(1),

pp.27-52.

Bratten, B., Causholli, M. and Khan, U., 2016. Usefulness of fair values for predicting banks’

future earnings: evidence from other comprehensive income and its components. Review of

Accounting Studies, 21(1), pp.280-315.

Cordazzo, M., 2013. The impact of IFRS on net income and equity: evidence from Italian

listed companies. Journal of Applied Accounting Research, 14(1), pp.54-73.

Gajewski, D., 2013. The Holding Company as an Instrument of Companies’ Tax-Financial

Policy Formation. Contemporary Economics, 7(1), pp.75-82.

Grossi, G., Bergmann, A., Rauskala, I. and Fuchs, S., 2013. „Applying the equity method as a

means of consolidation in the public sector: experiences in OECD countries”. Journal of

Commerce and Management, 16(2), pp.95-115.

Hansmann, H. and Kraakman, R., 2017. The end of history for corporate law. In Corporate

Governance (pp. 49-78). Gower.

Ioannou, I. and Serafeim, G., 2017. The consequences of mandatory corporate sustainability

reporting. Harvard Business School research working paper, (11-100).

Milojević, I., Vukoje, A. and Mihajlović, M., 2013. Accounting consolidation of the balance by

the acquisition method. Economics of Agriculture, 60(297-2016-3534), p.237.

Rahman, M. M., Moniruzzaman, M., & Sharif, M. J. (2013). Techniques, motives and controls

of earnings management. International Journal of Information Technology and Business

Management, 11(1), 22-34.

Ramadhan, S., 2014. Board composition, audit committees, ownership structure and

voluntary disclosure: Evidence from Bahrain. Research Journal of Finance and

Accounting, 5(7), pp.124-139.

Smith, S.R. and Smith, K.R., 2014. The journey from historical cost accounting to fair value

accounting: the case of acquisition costs. Journal of Business & Accounting, 7(1), pp.3-10.

Vašek, L. and Gluzová, T., 2014. Can a New Concept of Control under IFRS Have an Impact

on a CCCTB?. European Financial and Accounting Journal, 9(4), pp.110-127.

www.aasb.gov.au. (2019). [Ebook]. Retrieved from

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-11_COMPjan15_07-15.pdf

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.