Corporate Takeover Decision Making and the Effects on Consolidation Accounting

VerifiedAdded on 2023/04/03

|16

|3196

|219

AI Summary

This report assesses the effects of corporate takeover decision making on consolidation accounting. It discusses equity accounting, intragroup transactions, and NCI disclosure. The report also highlights the importance of accurate financial statements and the relevance of accounting standards.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE TAKEOVER DECISION MAKING AND THE

EFFECTS ON CONSOLIDATION ACCOUNTING

Corporate Takeover Decision Making and the Effects on Consolidation Accounting

Name of the Student:

Name of the University:

Author’s Note:

EFFECTS ON CONSOLIDATION ACCOUNTING

Corporate Takeover Decision Making and the Effects on Consolidation Accounting

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

3

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Table of Contents

Introduction...................................................................................................................2

PART A Response........................................................................................................2

PART B.........................................................................................................................5

PART C.........................................................................................................................8

Conclusion..................................................................................................................11

Reference List.............................................................................................................12

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Table of Contents

Introduction...................................................................................................................2

PART A Response........................................................................................................2

PART B.........................................................................................................................5

PART C.........................................................................................................................8

Conclusion..................................................................................................................11

Reference List.............................................................................................................12

4

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Introduction

This report has assessed three segments where in the initial stage, the

segment which is being considered is the equity accounting and the consolidated

accounting. In this part, this has regarded the AASB 10 and AASB 128. In the

second segment, the part which is being considered is the intragroup transaction of

the JKY limited. The accounting standard of the AASB 10 & AASB 127 is analysed in

a detailed way. The third segment that is being considered is the NCI disclosure

considering the demand of the AASB 101 (Trichterborn, Zu Knyphausen‐Aufseß and

Schweizer, 2016). The task has summarised the entire section.

PART A Response

The profit of the company can be increased with some choices. The AASB

128 is made responsible for issuing the ventures as well as the guidelines of the

choices. The company is required to be abide by these guidelines. The FAB limited

can be attained with the two possible options. The first option is the acquisition and

the purchase method where the implication is performed over the direct purchase of

the company (Shroff, 2017). The second option is the acquisition involvement

through which the shares of the company can be attained. The company can

achieve a huge quantity of profit over the options of the acquisitions. The ASX listed

company named FAB Ltd. would be acquired by JKY Ltd. Hence it can be expected

that this organization has a lump sum amount of money or rather profit in its cash

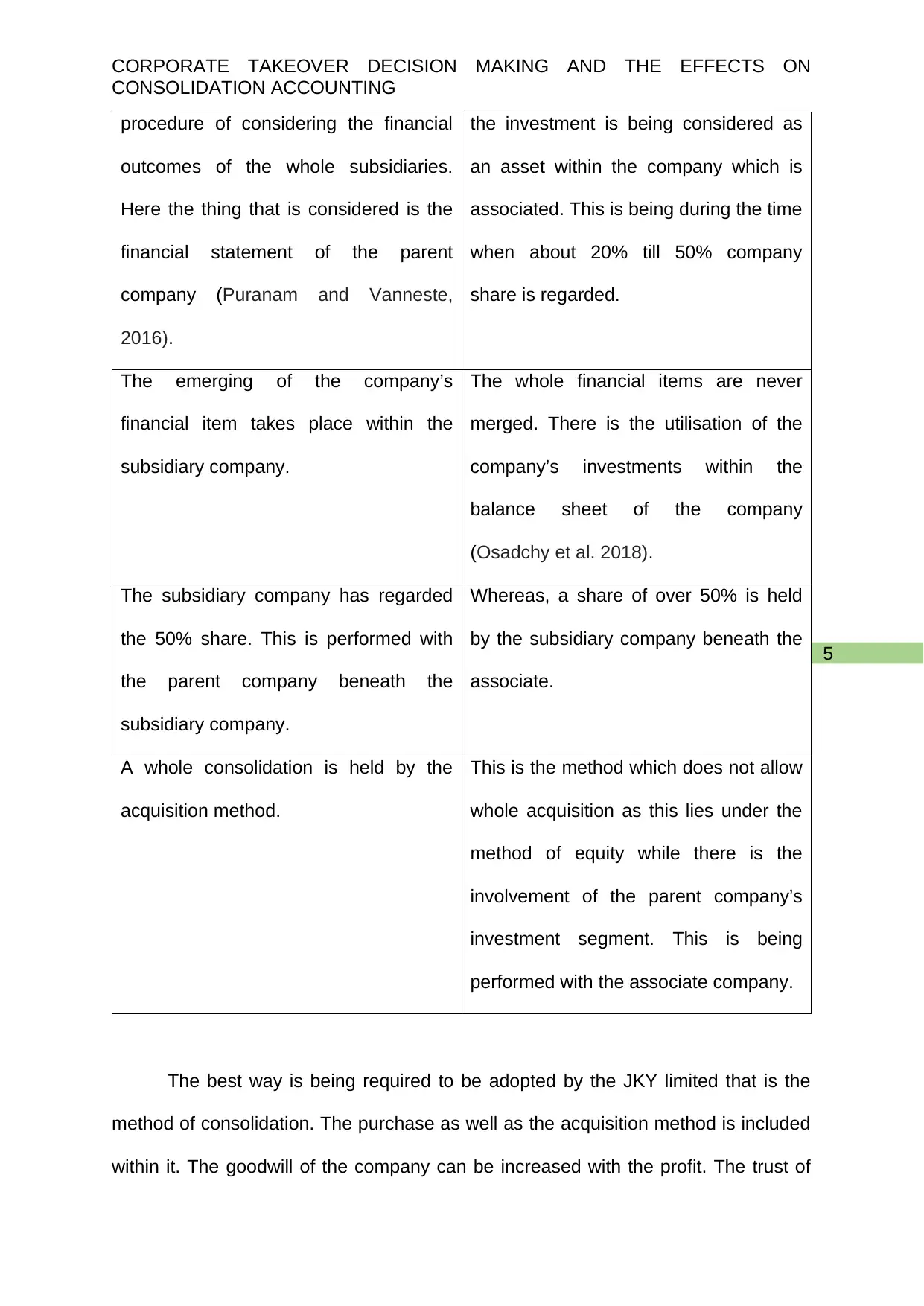

treasure. A chart is being presented where a special case of the equity accounting

and consolidation is being discussed:

Consolidation Accounting Equity Accounting

The consolidation accounting is the This is the process of accounting where

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Introduction

This report has assessed three segments where in the initial stage, the

segment which is being considered is the equity accounting and the consolidated

accounting. In this part, this has regarded the AASB 10 and AASB 128. In the

second segment, the part which is being considered is the intragroup transaction of

the JKY limited. The accounting standard of the AASB 10 & AASB 127 is analysed in

a detailed way. The third segment that is being considered is the NCI disclosure

considering the demand of the AASB 101 (Trichterborn, Zu Knyphausen‐Aufseß and

Schweizer, 2016). The task has summarised the entire section.

PART A Response

The profit of the company can be increased with some choices. The AASB

128 is made responsible for issuing the ventures as well as the guidelines of the

choices. The company is required to be abide by these guidelines. The FAB limited

can be attained with the two possible options. The first option is the acquisition and

the purchase method where the implication is performed over the direct purchase of

the company (Shroff, 2017). The second option is the acquisition involvement

through which the shares of the company can be attained. The company can

achieve a huge quantity of profit over the options of the acquisitions. The ASX listed

company named FAB Ltd. would be acquired by JKY Ltd. Hence it can be expected

that this organization has a lump sum amount of money or rather profit in its cash

treasure. A chart is being presented where a special case of the equity accounting

and consolidation is being discussed:

Consolidation Accounting Equity Accounting

The consolidation accounting is the This is the process of accounting where

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

procedure of considering the financial

outcomes of the whole subsidiaries.

Here the thing that is considered is the

financial statement of the parent

company (Puranam and Vanneste,

2016).

the investment is being considered as

an asset within the company which is

associated. This is being during the time

when about 20% till 50% company

share is regarded.

The emerging of the company’s

financial item takes place within the

subsidiary company.

The whole financial items are never

merged. There is the utilisation of the

company’s investments within the

balance sheet of the company

(Osadchy et al. 2018).

The subsidiary company has regarded

the 50% share. This is performed with

the parent company beneath the

subsidiary company.

Whereas, a share of over 50% is held

by the subsidiary company beneath the

associate.

A whole consolidation is held by the

acquisition method.

This is the method which does not allow

whole acquisition as this lies under the

method of equity while there is the

involvement of the parent company’s

investment segment. This is being

performed with the associate company.

The best way is being required to be adopted by the JKY limited that is the

method of consolidation. The purchase as well as the acquisition method is included

within it. The goodwill of the company can be increased with the profit. The trust of

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

procedure of considering the financial

outcomes of the whole subsidiaries.

Here the thing that is considered is the

financial statement of the parent

company (Puranam and Vanneste,

2016).

the investment is being considered as

an asset within the company which is

associated. This is being during the time

when about 20% till 50% company

share is regarded.

The emerging of the company’s

financial item takes place within the

subsidiary company.

The whole financial items are never

merged. There is the utilisation of the

company’s investments within the

balance sheet of the company

(Osadchy et al. 2018).

The subsidiary company has regarded

the 50% share. This is performed with

the parent company beneath the

subsidiary company.

Whereas, a share of over 50% is held

by the subsidiary company beneath the

associate.

A whole consolidation is held by the

acquisition method.

This is the method which does not allow

whole acquisition as this lies under the

method of equity while there is the

involvement of the parent company’s

investment segment. This is being

performed with the associate company.

The best way is being required to be adopted by the JKY limited that is the

method of consolidation. The purchase as well as the acquisition method is included

within it. The goodwill of the company can be increased with the profit. The trust of

6

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

the people is gained by this. There is some assistance of the true and fair reporting

during the long run to the company. The firm has taken some of the benefits of the

acquisition method that is being regarded as a best practise for aiding within the

suitable financial reporting (Mohamad et al. 2017). Under this thing comes the best

practise of the firm. The JTY limited company has considered the acquisition benefits

and the process of post-acquisition. This is the company which is being assisted for

the structuring of the best from the price which is selected. Therefore, lies some

successful purchase acquisition method regarding the business (García‐Sánchez

and Noguera‐Gámez, 2017).

The whole revelation about the financial statement considering the parent

company is handled below the consolidating accounting laterally with the subsidiary

company.

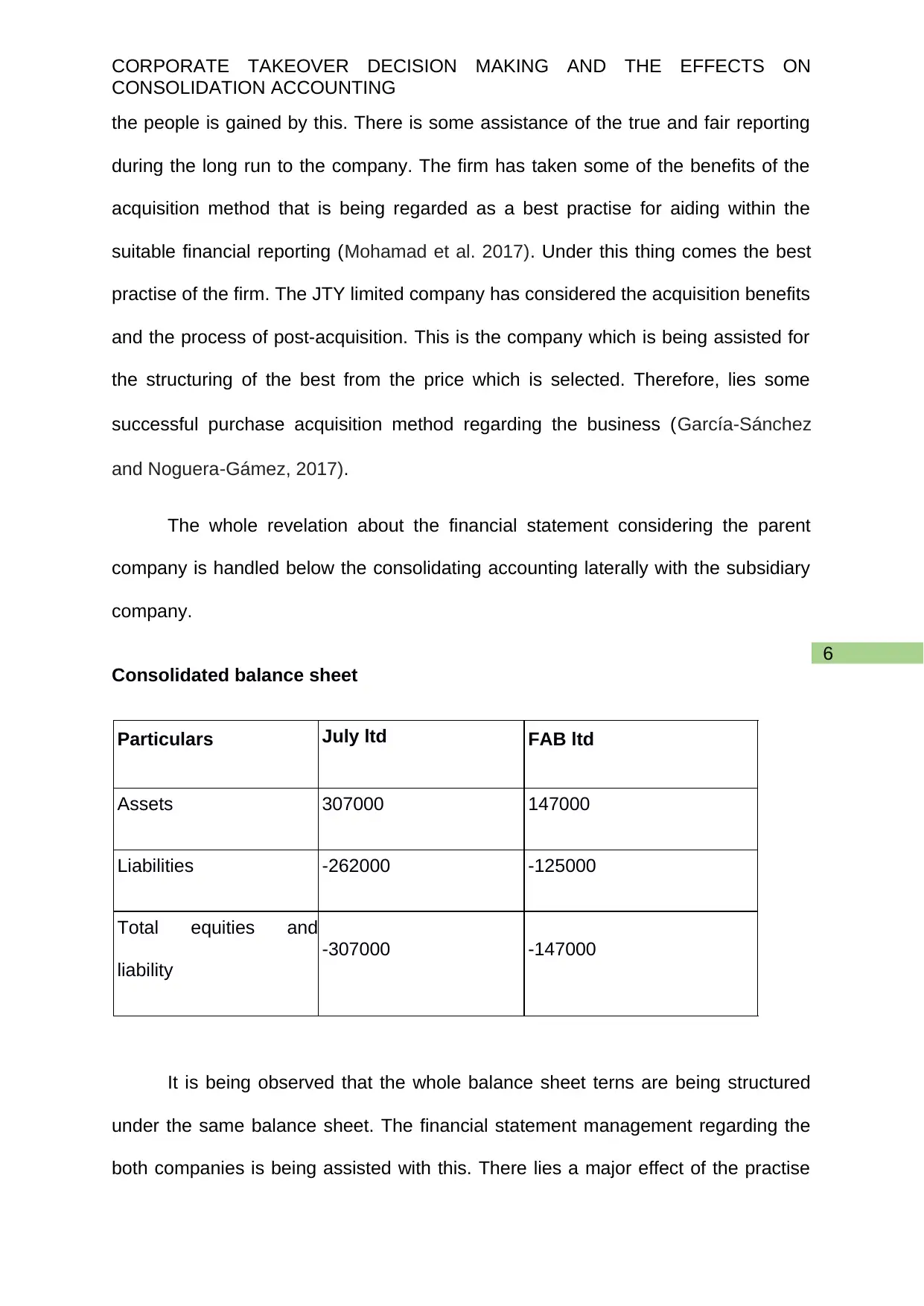

Consolidated balance sheet

Particulars July ltd FAB ltd

Assets 307000 147000

Liabilities -262000 -125000

Total equities and

liability

-307000 -147000

It is being observed that the whole balance sheet terns are being structured

under the same balance sheet. The financial statement management regarding the

both companies is being assisted with this. There lies a major effect of the practise

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

the people is gained by this. There is some assistance of the true and fair reporting

during the long run to the company. The firm has taken some of the benefits of the

acquisition method that is being regarded as a best practise for aiding within the

suitable financial reporting (Mohamad et al. 2017). Under this thing comes the best

practise of the firm. The JTY limited company has considered the acquisition benefits

and the process of post-acquisition. This is the company which is being assisted for

the structuring of the best from the price which is selected. Therefore, lies some

successful purchase acquisition method regarding the business (García‐Sánchez

and Noguera‐Gámez, 2017).

The whole revelation about the financial statement considering the parent

company is handled below the consolidating accounting laterally with the subsidiary

company.

Consolidated balance sheet

Particulars July ltd FAB ltd

Assets 307000 147000

Liabilities -262000 -125000

Total equities and

liability

-307000 -147000

It is being observed that the whole balance sheet terns are being structured

under the same balance sheet. The financial statement management regarding the

both companies is being assisted with this. There lies a major effect of the practise

7

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

that is being helped within the true and the fair reporting regarding the financial

statements after acquisition (Ikeda, Inoue and Watanabe, 2018).

PART B

The consolidated transactions are known as the intragroup transactions. Here

the subsidiary company is responsible for making the investments considering this

company and the selling of the goods are done for making profit within a given

period. Profit can be earned by the parent company. The subsidiary company has

vended some asset which is being considered as the sales that lies within the

account of the subsidiary company (Chua, Cheong and Gould 2012). A major effect

is lying under the NCI, where the practise is being considered. This segment is

hugely important during the treatment of the company’s profit and loss. Numerous

rules are being provided by the intragroup transactions that is being incorporated at

the time of final reconciliation (Greve and Man Zhang, 2017). Things are being

performed within the context of several requirements:

The cut-off discrepancies: Discrepancies are lying within the dates of the

cut-offs. Therefore, there is the requirement of the process employment at the

time of the reconciliation method. At the time of mitigation of the

discrepancies, the companies are helped with the methods of the accounting

considering the commonalities.

Modification of the closed dates: There lies some of the modifications

within the closed dates within the parent and subsidiary company. Therefore,

it is essential for activating the process of reconciliation. The closed dates

have been made responsible to the big accounting discrepancies. While,

when the account book is getting closed, by the parent company over 31st

December of each year, simultaneously, the subsidiary company is also

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

that is being helped within the true and the fair reporting regarding the financial

statements after acquisition (Ikeda, Inoue and Watanabe, 2018).

PART B

The consolidated transactions are known as the intragroup transactions. Here

the subsidiary company is responsible for making the investments considering this

company and the selling of the goods are done for making profit within a given

period. Profit can be earned by the parent company. The subsidiary company has

vended some asset which is being considered as the sales that lies within the

account of the subsidiary company (Chua, Cheong and Gould 2012). A major effect

is lying under the NCI, where the practise is being considered. This segment is

hugely important during the treatment of the company’s profit and loss. Numerous

rules are being provided by the intragroup transactions that is being incorporated at

the time of final reconciliation (Greve and Man Zhang, 2017). Things are being

performed within the context of several requirements:

The cut-off discrepancies: Discrepancies are lying within the dates of the

cut-offs. Therefore, there is the requirement of the process employment at the

time of the reconciliation method. At the time of mitigation of the

discrepancies, the companies are helped with the methods of the accounting

considering the commonalities.

Modification of the closed dates: There lies some of the modifications

within the closed dates within the parent and subsidiary company. Therefore,

it is essential for activating the process of reconciliation. The closed dates

have been made responsible to the big accounting discrepancies. While,

when the account book is getting closed, by the parent company over 31st

December of each year, simultaneously, the subsidiary company is also

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

involved in closing the accounts book in half-yearly basis (Graham et al.

2017). The fire fights have focused over the several aspects for considering

the disclosure date.

The dominance of the foreign companies: The transactions are being

dominated by the foreign recurrence which the companies has processed

among each other. Therefore, the numerous aspects considering the foreign

market is regarded that is important for the company. Both the companies are

considered within this that is processing within same industries (Picker et al.,

2016). A continuous effect is being bored by these practises and the long run

continues. Therefore, during the time of the management process, to assist

the company has regarded to be important with suitable rules and regulation

formulation.

The further cause of assessment:

non-controlling interest

parent company $ subsidiary company $

revenues 812000 250000

expenses 354000 188000

Excess fair value

amortization

()50 32000

net income 458000 30000

ownership stake 85% 15%

controlling interest 25500

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

involved in closing the accounts book in half-yearly basis (Graham et al.

2017). The fire fights have focused over the several aspects for considering

the disclosure date.

The dominance of the foreign companies: The transactions are being

dominated by the foreign recurrence which the companies has processed

among each other. Therefore, the numerous aspects considering the foreign

market is regarded that is important for the company. Both the companies are

considered within this that is processing within same industries (Picker et al.,

2016). A continuous effect is being bored by these practises and the long run

continues. Therefore, during the time of the management process, to assist

the company has regarded to be important with suitable rules and regulation

formulation.

The further cause of assessment:

non-controlling interest

parent company $ subsidiary company $

revenues 812000 250000

expenses 354000 188000

Excess fair value

amortization

()50 32000

net income 458000 30000

ownership stake 85% 15%

controlling interest 25500

9

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Non-controlling interest 4500

There is the focusing of the ownership interest of the company that has

assisted the whole company. At the time of the analysis, this has assisted the

company while the specific effect has given rise to the transaction within the financial

statement. The table has specified about the calculation of the non-controlling

interest that is being mentioned previously. The non-controlling interest is being

estimated to be 4500. During the assessment of this, the thing that is made

responsible is the ownership stake that is 3000. The calculated interest is 15% which

is being seen within the non-controlling interest segment. The processing of the profit

assessment is performed where the company is being considered (Schührer 2018.).

Over the assets there is some simple classification, where the incomes of the

companies are being considered. There is the inclusion of both the companies which

are the subsidiary and parent company. There lies some special effect over the

translation of the financial statement of the company (Gatta. and Marcucci, 2016).

There is the measurement of the accurate intercede which is uncontrollable. The

classification as provided in the assets and incomes of the organization is very much

easier to calculate. The organization includes two of the kinds of the organizational

bodies those include both of the subsidiary as well as the parent organization. A

special effect on the translation of the statement of the finance is included in the

organization assisting in interceding of the accuracy that is non-controlling.

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Non-controlling interest 4500

There is the focusing of the ownership interest of the company that has

assisted the whole company. At the time of the analysis, this has assisted the

company while the specific effect has given rise to the transaction within the financial

statement. The table has specified about the calculation of the non-controlling

interest that is being mentioned previously. The non-controlling interest is being

estimated to be 4500. During the assessment of this, the thing that is made

responsible is the ownership stake that is 3000. The calculated interest is 15% which

is being seen within the non-controlling interest segment. The processing of the profit

assessment is performed where the company is being considered (Schührer 2018.).

Over the assets there is some simple classification, where the incomes of the

companies are being considered. There is the inclusion of both the companies which

are the subsidiary and parent company. There lies some special effect over the

translation of the financial statement of the company (Gatta. and Marcucci, 2016).

There is the measurement of the accurate intercede which is uncontrollable. The

classification as provided in the assets and incomes of the organization is very much

easier to calculate. The organization includes two of the kinds of the organizational

bodies those include both of the subsidiary as well as the parent organization. A

special effect on the translation of the statement of the finance is included in the

organization assisting in interceding of the accuracy that is non-controlling.

10

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

PART C

Some information is being provided over the financial statement of the

company that is confined with the suitable allocation of the resources of the

company. It is being observed about the investment of the company’s retained

earnings that lies within the suitable plans of business. These are the plans which

are comprised of investments that is free of resources. A less dependency is of the

company regarding the dependency over the debt fund. The basic need is the

reflection of the images that are true and fair across the financial statement. The

thing which is also being regarded is the introduction of the assets of fair value of the

company within the company’s balance sheet. There lies the allocation of the

resources over the availabilities of the subsidiaries. Here the company is being

regarded. The report is comprised of the disclosure of this matter according to the

statement of the independent auditor. The whole information about the company is

being regarded within the statutory compliance (Walton, Haller and Raffournier

2003).

The investors should take some proper decisions which is being relied over

the relevance and the reliability of the financial statements. The positive attitude of

the investors lies within this framework. This is being regarded by the investors or

the securities.as the company has constructed some important decision over the

revelation. The security market is being aided with the evidence for rating the

taxation jeopardy that is being deliberated within the financial account of the

company regarding the captivation of suitable choices over the rapports of

speculation. A discount is being observed within the profit later the tax as the

company is being allowable for reimbursing more tax. A droplet in the remaining

revenue of the company is also observed. Therefore, the stockholders have also

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

PART C

Some information is being provided over the financial statement of the

company that is confined with the suitable allocation of the resources of the

company. It is being observed about the investment of the company’s retained

earnings that lies within the suitable plans of business. These are the plans which

are comprised of investments that is free of resources. A less dependency is of the

company regarding the dependency over the debt fund. The basic need is the

reflection of the images that are true and fair across the financial statement. The

thing which is also being regarded is the introduction of the assets of fair value of the

company within the company’s balance sheet. There lies the allocation of the

resources over the availabilities of the subsidiaries. Here the company is being

regarded. The report is comprised of the disclosure of this matter according to the

statement of the independent auditor. The whole information about the company is

being regarded within the statutory compliance (Walton, Haller and Raffournier

2003).

The investors should take some proper decisions which is being relied over

the relevance and the reliability of the financial statements. The positive attitude of

the investors lies within this framework. This is being regarded by the investors or

the securities.as the company has constructed some important decision over the

revelation. The security market is being aided with the evidence for rating the

taxation jeopardy that is being deliberated within the financial account of the

company regarding the captivation of suitable choices over the rapports of

speculation. A discount is being observed within the profit later the tax as the

company is being allowable for reimbursing more tax. A droplet in the remaining

revenue of the company is also observed. Therefore, the stockholders have also

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

responded. Consequently, the users are essential to examine the financial

declarations. The accounting standard AASB 10 has recommended this (Benson et

al., 2015) . The AASB has completed this required where IFRS is being distributed

by this over the world. Business should accept the accounting standard for

bestowing the financial declaration in an appropriate method. AASB is being

exploited within this accounting determination concerning the executing of the rules

seeing the presentation, the construction as well as the financial statement gratified

that the company has organised (Frydman and Camerer, 2016). Hence, the

organization is going to cease its operation of the business as there are huge

chances of the organization to lose the grip of the market. Hence, it is relevant to

analyse the statements of finance by the users. This is thereby suggested on the

basis of the standard of accounting that is, AS 10 (Barth et al., 2008). Therefore, it

had been made compulsory by the Australian Accounting Standard Board that

provides IFRS all across the globe.

Some details are there which is processed regarding the reveals significant which

are:

There is the view of the true worth of the assets.

There is the assistance of the dividend payment for increasing the value of

the assets, then more are the investors are being attracted. Probabilities are

lying for receiving more from the bonuses from company.

A true return rate is being viewed considering the capital employment

Within the financial asset of the company lies the fair as well as the true value.

The company is being aided with it through the taking of loans from the banks

which stipulates regarding the increased price of the assets for possession of

appropriate mortgage with the ban. Probabilities are lying where the

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

responded. Consequently, the users are essential to examine the financial

declarations. The accounting standard AASB 10 has recommended this (Benson et

al., 2015) . The AASB has completed this required where IFRS is being distributed

by this over the world. Business should accept the accounting standard for

bestowing the financial declaration in an appropriate method. AASB is being

exploited within this accounting determination concerning the executing of the rules

seeing the presentation, the construction as well as the financial statement gratified

that the company has organised (Frydman and Camerer, 2016). Hence, the

organization is going to cease its operation of the business as there are huge

chances of the organization to lose the grip of the market. Hence, it is relevant to

analyse the statements of finance by the users. This is thereby suggested on the

basis of the standard of accounting that is, AS 10 (Barth et al., 2008). Therefore, it

had been made compulsory by the Australian Accounting Standard Board that

provides IFRS all across the globe.

Some details are there which is processed regarding the reveals significant which

are:

There is the view of the true worth of the assets.

There is the assistance of the dividend payment for increasing the value of

the assets, then more are the investors are being attracted. Probabilities are

lying for receiving more from the bonuses from company.

A true return rate is being viewed considering the capital employment

Within the financial asset of the company lies the fair as well as the true value.

The company is being aided with it through the taking of loans from the banks

which stipulates regarding the increased price of the assets for possession of

appropriate mortgage with the ban. Probabilities are lying where the

12

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

anticipated return rate can be received by the companies (Barth, Landsman

and Lang 2008).

The true quantity of the assets can be received after the asset revaluation.

The assets’ true and fair image is being visible after the assets’ revaluation.

Some SAC2 statement is being required by the accounting system considering

the concept of accounting supporting the general purpose. During the dealing of

the objectives, this is being required by the stakeholder of the company as well

as the investors of the company considering the revelation. This is being utilised

by the directors of the company as well regarding the structuring of the suitable

plans of business along with the business policies (Avetisyan and Hockerts,

2017). There is the proper allocation of the resources of the company considering

this. There lies the presence of the certain qualitative characteristics where the

business can depend on. This is the thing which is being regarded as the base of

the financial statement.

There is the add-on of the profits as well within the financial statements. This

is being regarded to be comprehensive. The company is required to add the

profits within each funds of the owners as the huge percentage for holding the

subsidiary company. Whereas, NCI is not to be viewed when a minimum of 50%

is the share that the shareholder has owned. There is also no presence of the

ownership rights resulting in the negative voting rights of the shareholders.

During the time, when less than 50% of the shares are being held by the entity,

then, the NCI is not to be observed of reporting as the fund for the equity of the

owner (Appelbaum et al. 2017). There lies the consolidated account regarding

the companies where the financial statement is being reported by the NCI that is

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

anticipated return rate can be received by the companies (Barth, Landsman

and Lang 2008).

The true quantity of the assets can be received after the asset revaluation.

The assets’ true and fair image is being visible after the assets’ revaluation.

Some SAC2 statement is being required by the accounting system considering

the concept of accounting supporting the general purpose. During the dealing of

the objectives, this is being required by the stakeholder of the company as well

as the investors of the company considering the revelation. This is being utilised

by the directors of the company as well regarding the structuring of the suitable

plans of business along with the business policies (Avetisyan and Hockerts,

2017). There is the proper allocation of the resources of the company considering

this. There lies the presence of the certain qualitative characteristics where the

business can depend on. This is the thing which is being regarded as the base of

the financial statement.

There is the add-on of the profits as well within the financial statements. This

is being regarded to be comprehensive. The company is required to add the

profits within each funds of the owners as the huge percentage for holding the

subsidiary company. Whereas, NCI is not to be viewed when a minimum of 50%

is the share that the shareholder has owned. There is also no presence of the

ownership rights resulting in the negative voting rights of the shareholders.

During the time, when less than 50% of the shares are being held by the entity,

then, the NCI is not to be observed of reporting as the fund for the equity of the

owner (Appelbaum et al. 2017). There lies the consolidated account regarding

the companies where the financial statement is being reported by the NCI that is

13

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

regarded to be necessary for the company for focusing over the financial

statements.

There is the importance of the dependability of the financial statement. The

quality of the financial statements has been referred by the interpreting of

information where the financial statement is being considered. This has been

impacted due to the errors and the biases (Alfredson et al., 2005). During the

serving of the faithful information considering the financial statement, this is

possible. The information is regarded as the base for the reader. The events are

being read by the stakeholders as well as about the transactions that is being

presented by the company. they are required to take some decision over the

served information which is sometimes not to be understandable. The entire thing

has specified about something, that is, the economic terms are not to be

understood by the stakeholders that is not essential. Therefore, the information is

required to be served in simple terms.

Conclusion

An important disclosure is necessary within the financial statement. There is

the focusing of the several aspects of the financial reporting, for benefitting the

company. The security market is being attracted by the financial statement of the

company along with the investors as well as the other businesses. The financial

statement is being affected by the NCI. The company has specified the equity of

the owners where a minimum of 50% share is being held considering the

subsidiary company.

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

regarded to be necessary for the company for focusing over the financial

statements.

There is the importance of the dependability of the financial statement. The

quality of the financial statements has been referred by the interpreting of

information where the financial statement is being considered. This has been

impacted due to the errors and the biases (Alfredson et al., 2005). During the

serving of the faithful information considering the financial statement, this is

possible. The information is regarded as the base for the reader. The events are

being read by the stakeholders as well as about the transactions that is being

presented by the company. they are required to take some decision over the

served information which is sometimes not to be understandable. The entire thing

has specified about something, that is, the economic terms are not to be

understood by the stakeholders that is not essential. Therefore, the information is

required to be served in simple terms.

Conclusion

An important disclosure is necessary within the financial statement. There is

the focusing of the several aspects of the financial reporting, for benefitting the

company. The security market is being attracted by the financial statement of the

company along with the investors as well as the other businesses. The financial

statement is being affected by the NCI. The company has specified the equity of

the owners where a minimum of 50% share is being held considering the

subsidiary company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Reference List

Alfredson, K., Leo, K., Picker, R., Pacter, P., Radford, J. and Wise, V.,

2005. Applying international accounting standards. John Wiley & Sons.

Appelbaum, D., Kogan, A., Vasarhelyi, M. and Yan, Z., 2017. Impact of business

analytics and enterprise systems on managerial accounting. International Journal of

Accounting Information Systems, 25, pp.29-44.

Avetisyan, E. and Hockerts, K., 2017. The consolidation of the ESG rating industry

as an enactment of institutional retrogression. Business Strategy and the

Environment, 26(3), pp.316-330.

Barth, M.E., Landsman, W.R. and Lang, M.H., 2008. International accounting

standards and accounting quality. Journal of accounting research, 46(3), pp.467-

498.

Benson, K., Clarkson, P.M., Smith, T., and Tutticci, I., 2015. A review of accounting

research in the Asia Pacific region. Australian Journal of Management, 40(1), pp.36-

88.

Chua, Y.L., Cheong, C.S. and Gould, G., 2012. The impact of mandatory IFRS

adoption on accounting quality: Evidence from Australia. Journal of International

accounting research, 11(1), pp.119-146.

Frydman, C. and Camerer, C.F., 2016. The psychology and neuroscience of

financial decision making. Trends in cognitive sciences, 20(9), pp.661-675.

García‐Sánchez, I.M. and Noguera‐Gámez, L., 2017. Integrated reporting and

stakeholder engagement: The effect on information asymmetry. Corporate Social

Responsibility and Environmental Management, 24(5), pp.395-413.

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Reference List

Alfredson, K., Leo, K., Picker, R., Pacter, P., Radford, J. and Wise, V.,

2005. Applying international accounting standards. John Wiley & Sons.

Appelbaum, D., Kogan, A., Vasarhelyi, M. and Yan, Z., 2017. Impact of business

analytics and enterprise systems on managerial accounting. International Journal of

Accounting Information Systems, 25, pp.29-44.

Avetisyan, E. and Hockerts, K., 2017. The consolidation of the ESG rating industry

as an enactment of institutional retrogression. Business Strategy and the

Environment, 26(3), pp.316-330.

Barth, M.E., Landsman, W.R. and Lang, M.H., 2008. International accounting

standards and accounting quality. Journal of accounting research, 46(3), pp.467-

498.

Benson, K., Clarkson, P.M., Smith, T., and Tutticci, I., 2015. A review of accounting

research in the Asia Pacific region. Australian Journal of Management, 40(1), pp.36-

88.

Chua, Y.L., Cheong, C.S. and Gould, G., 2012. The impact of mandatory IFRS

adoption on accounting quality: Evidence from Australia. Journal of International

accounting research, 11(1), pp.119-146.

Frydman, C. and Camerer, C.F., 2016. The psychology and neuroscience of

financial decision making. Trends in cognitive sciences, 20(9), pp.661-675.

García‐Sánchez, I.M. and Noguera‐Gámez, L., 2017. Integrated reporting and

stakeholder engagement: The effect on information asymmetry. Corporate Social

Responsibility and Environmental Management, 24(5), pp.395-413.

15

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Gatta, V. and Marcucci, E., 2016. Stakeholder-specific data acquisition and urban

freight policy evaluation: evidence, implications and new suggestions. Transport

Reviews, 36(5), pp.585-609.

Graham, J.R., Hanlon, M., Shevlin, T. and Shroff, N., 2017. Tax rates and corporate

decision-making. The Review of Financial Studies, 30(9), pp.3128-3175.

Greve, H.R. and Man Zhang, C., 2017. Institutional logics and power sources:

Merger and acquisition decisions. Academy of Management Journal, 60(2), pp.671-

694.

Ikeda, N., Inoue, K. and Watanabe, S., 2018. Enjoying the quiet life: Corporate

decision-making by entrenched managers. Journal of the Japanese and

International Economies, 47, pp.55-69.

Mohamad, A., Zainuddin, Y., Alam, N. and Kendall, G., 2017. Does decentralized

decision making increase company performance through its Information Technology

infrastructure investment?. International Journal of Accounting Information

Systems, 27, pp.1-15.

Osadchy, E.A., Akhmetshin, E.M., Amirova, E.F., Bochkareva, T.N., Gazizyanova,

Y.Y. and Yumashev, A.V., 2018. Financial statements of a company as an

information base for decision-making in a transforming economy. European

Research Studies Journal, 21(2), pp.339-350.

Picker, R., Clark, K., Dunn, J., Kolitz, D., Levine, G., Loftus, J. and Van der Tas, L.,

2016. Applying IFRS standards. John Wiley & Sons.

Puranam, P. and Vanneste, B., 2016. Corporate strategy: Tools for analysis and

decision-making. Cambridge University Press.

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Gatta, V. and Marcucci, E., 2016. Stakeholder-specific data acquisition and urban

freight policy evaluation: evidence, implications and new suggestions. Transport

Reviews, 36(5), pp.585-609.

Graham, J.R., Hanlon, M., Shevlin, T. and Shroff, N., 2017. Tax rates and corporate

decision-making. The Review of Financial Studies, 30(9), pp.3128-3175.

Greve, H.R. and Man Zhang, C., 2017. Institutional logics and power sources:

Merger and acquisition decisions. Academy of Management Journal, 60(2), pp.671-

694.

Ikeda, N., Inoue, K. and Watanabe, S., 2018. Enjoying the quiet life: Corporate

decision-making by entrenched managers. Journal of the Japanese and

International Economies, 47, pp.55-69.

Mohamad, A., Zainuddin, Y., Alam, N. and Kendall, G., 2017. Does decentralized

decision making increase company performance through its Information Technology

infrastructure investment?. International Journal of Accounting Information

Systems, 27, pp.1-15.

Osadchy, E.A., Akhmetshin, E.M., Amirova, E.F., Bochkareva, T.N., Gazizyanova,

Y.Y. and Yumashev, A.V., 2018. Financial statements of a company as an

information base for decision-making in a transforming economy. European

Research Studies Journal, 21(2), pp.339-350.

Picker, R., Clark, K., Dunn, J., Kolitz, D., Levine, G., Loftus, J. and Van der Tas, L.,

2016. Applying IFRS standards. John Wiley & Sons.

Puranam, P. and Vanneste, B., 2016. Corporate strategy: Tools for analysis and

decision-making. Cambridge University Press.

16

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Schührer, S., 2018. Identifying policy entrepreneurs of public sector accounting

agenda setting in Australia. Accounting, Auditing & Accountability

Journal, 31(4), pp.1067-1097.

Shroff, N., 2017. Corporate investment and changes in GAAP. Review of Accounting

Studies, 22(1), pp.1-63.

Trichterborn, A., Zu Knyphausen‐Aufseß, D. and Schweizer, L., 2016. How to

improve acquisition performance: The role of a dedicated M&A function, M&A

learning process, and M&A capability. Strategic Management Journal, 37(4), pp.763-

773.

Walton, P., Haller, A. and Raffournier, B. eds., 2003. International accounting.

Cengage Learning EMEA.

CORPORATE TAKEOVER DECISION MAKING AND THE EFFECTS ON

CONSOLIDATION ACCOUNTING

Schührer, S., 2018. Identifying policy entrepreneurs of public sector accounting

agenda setting in Australia. Accounting, Auditing & Accountability

Journal, 31(4), pp.1067-1097.

Shroff, N., 2017. Corporate investment and changes in GAAP. Review of Accounting

Studies, 22(1), pp.1-63.

Trichterborn, A., Zu Knyphausen‐Aufseß, D. and Schweizer, L., 2016. How to

improve acquisition performance: The role of a dedicated M&A function, M&A

learning process, and M&A capability. Strategic Management Journal, 37(4), pp.763-

773.

Walton, P., Haller, A. and Raffournier, B. eds., 2003. International accounting.

Cengage Learning EMEA.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.