Management Accounting: Cost Accounting Concepts Assignment Solution

VerifiedAdded on 2023/05/31

|12

|1150

|456

Homework Assignment

AI Summary

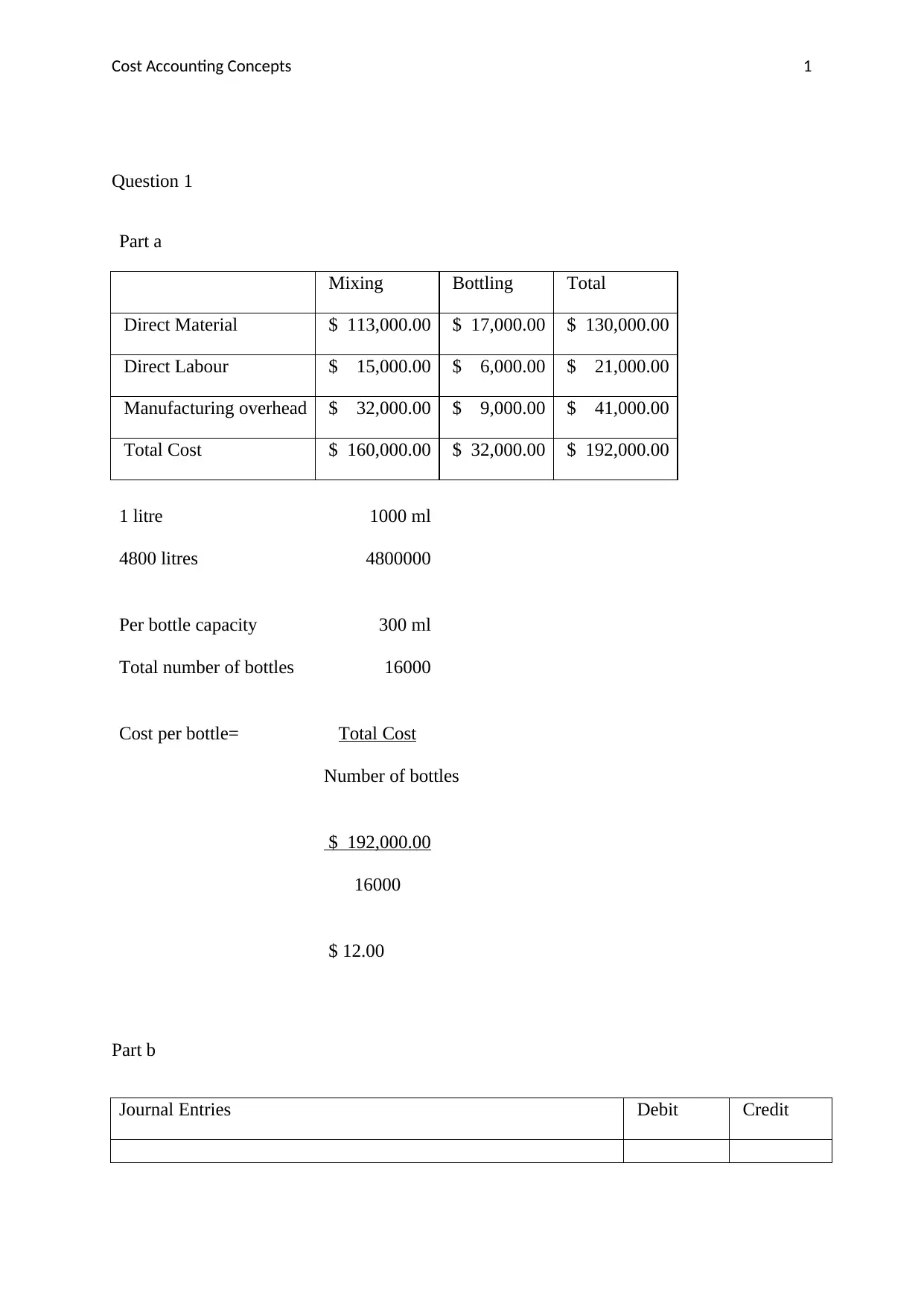

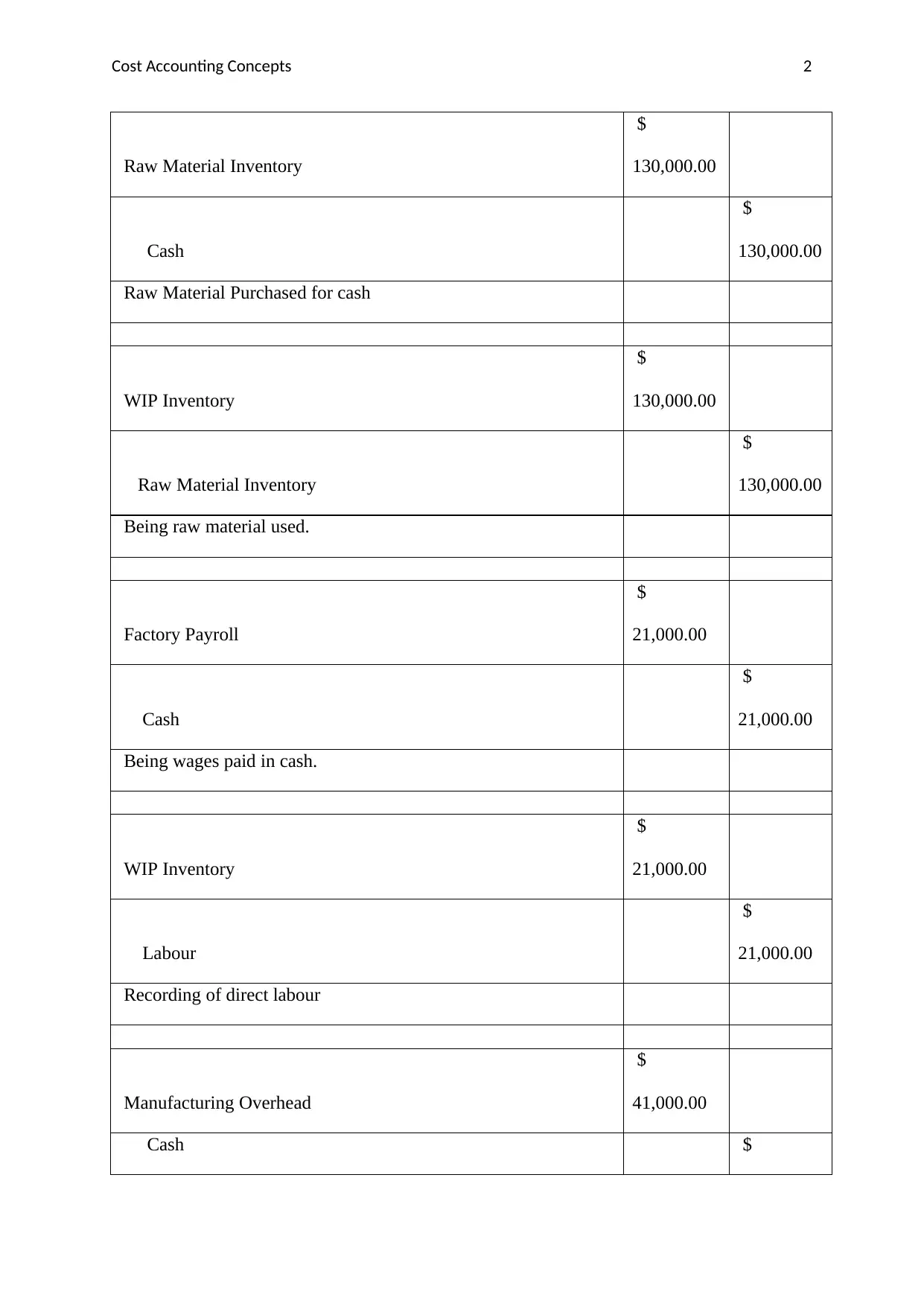

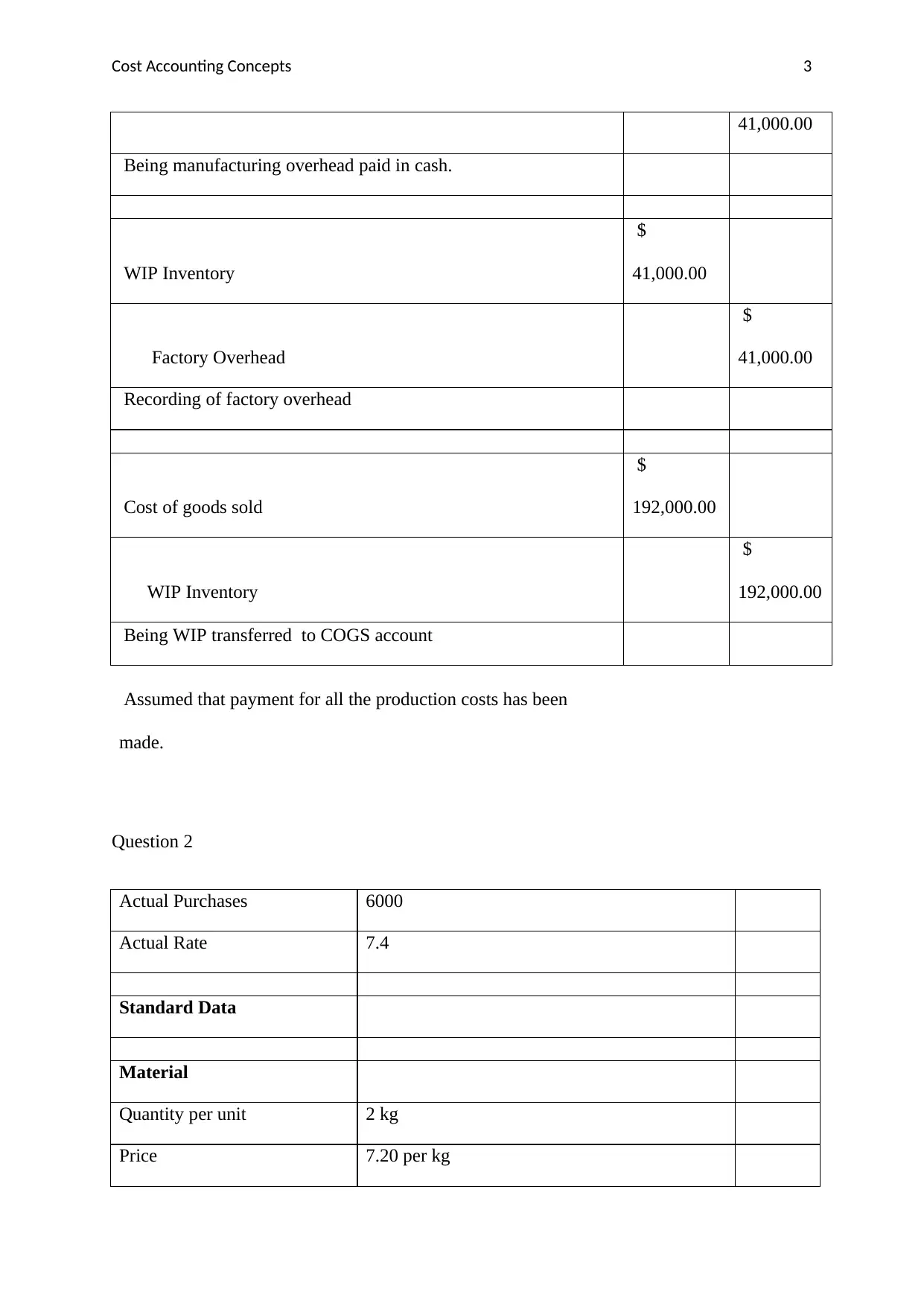

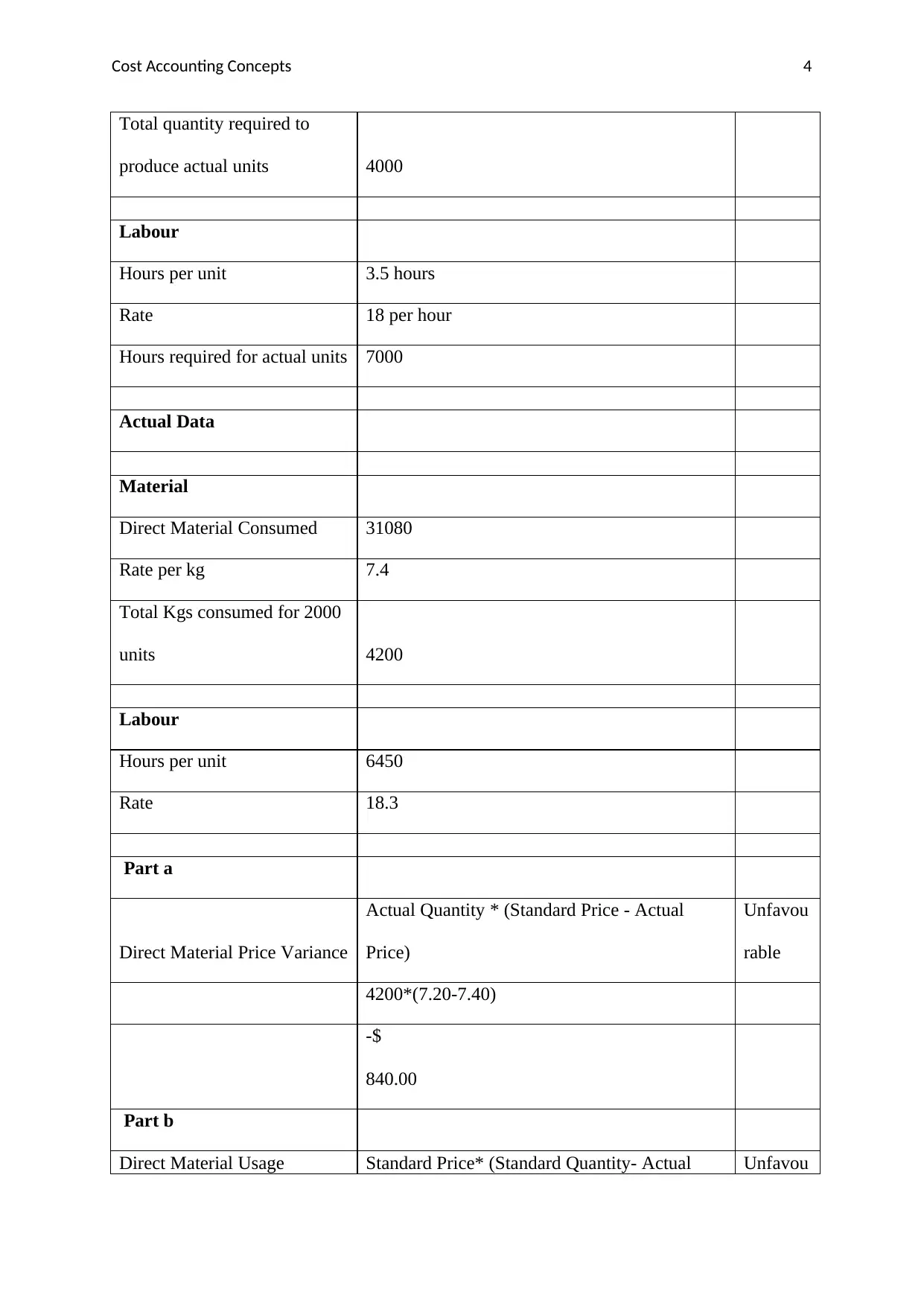

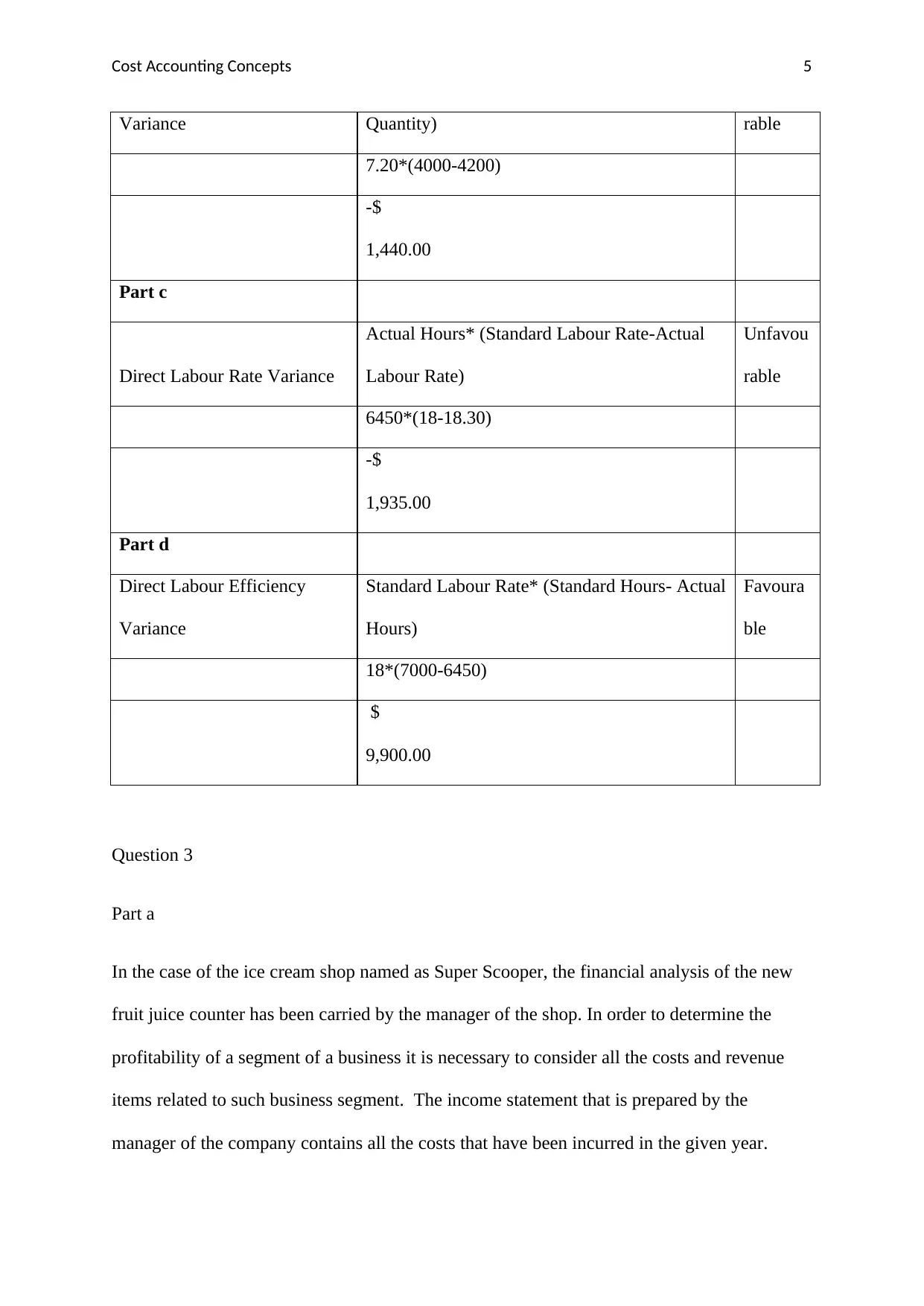

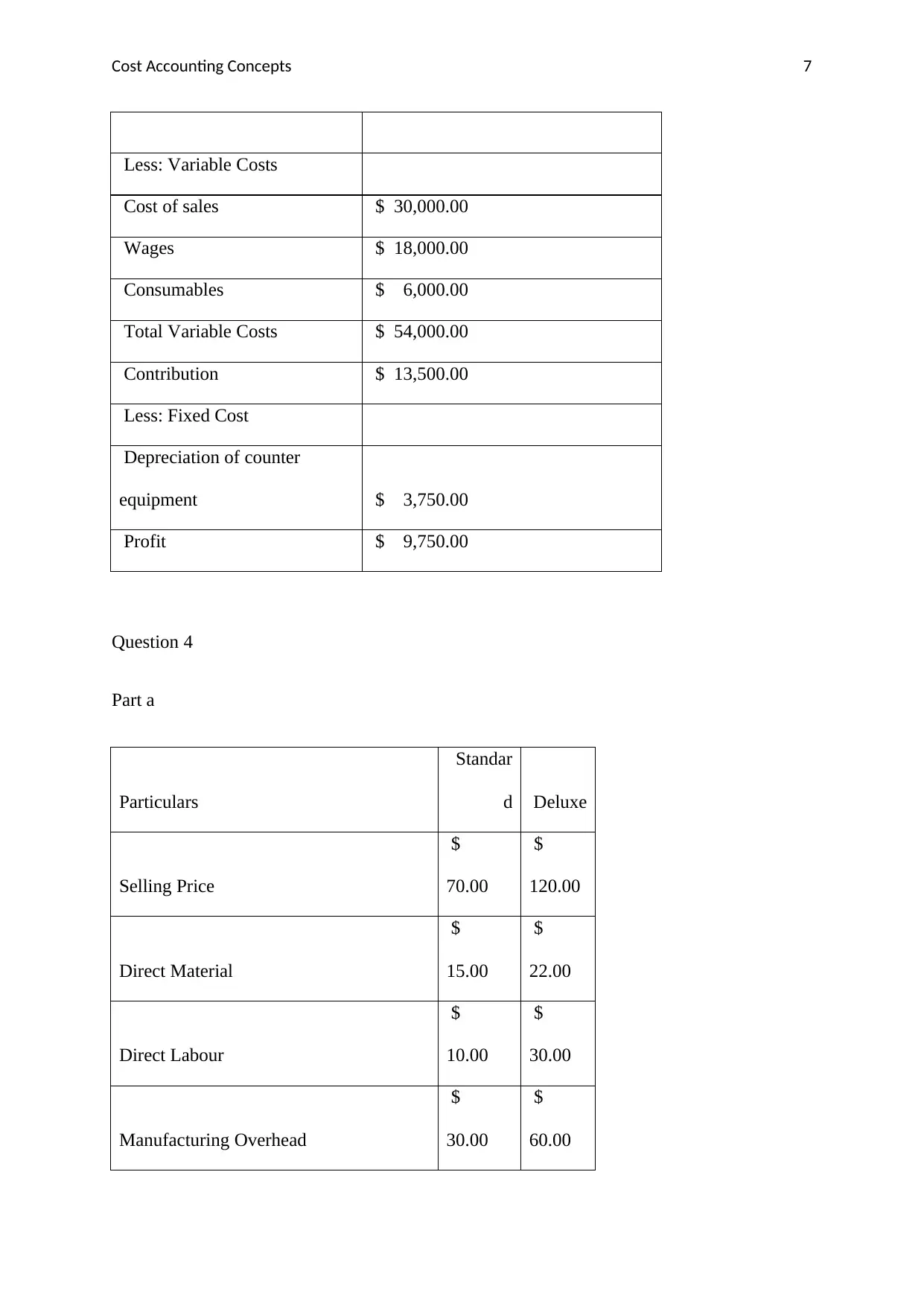

This document presents a comprehensive solution to a management accounting assignment focused on cost accounting concepts. The solution addresses several key areas, including calculating the cost per bottle for a brewing company, preparing journal entries to record production costs, and performing variance analysis for direct materials and labor. The assignment covers topics such as direct materials, direct labor, manufacturing overhead, and the calculation of variances. Additionally, the solution includes an analysis of a fruit juice counter's profitability, considering relevant and irrelevant costs, and a contribution margin analysis to determine optimal product mix. The document provides detailed calculations, explanations, and journal entries to illustrate the concepts effectively.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.