Cost and Reveanes InTROUCTION 4 TASK 14

Added on 2020-10-22

21 Pages4172 Words171 Views

COST AND REVENUES

Table of ContentsINTRODUCTION................................................................................................................................4TASK 1.................................................................................................................................................41.1 purpose of internal reporting and providing accurate information to management..............41.2 Relationship between various costing system in the organisation........................................51.3 Identifying the responsibility centres ,cost centres , profit centres and investment centres in organisation.................................................................................................................................51.4 Characteristics of different types of cost classification and their use in costing .................61.5 Difference between marginal and absorption costing ..........................................................6TASK 2.................................................................................................................................................72.1 Cost information for material, labour and expenses in relation to organisation costing procedures...................................................................................................................................72.2 Analyse the cost information for material, labour and expense............................................72.4 Valuation of inventory ..........................................................................................................8Last in First out ( LIFO).......................................................................................................................92.5 Behaviour of the cost..........................................................................................................122.6 Record cost information using the costing system .............................................................12Job costing .........................................................................................................................................12TASK 3...............................................................................................................................................143.1 Attribution of overhead cost of production and service cost centres in accordance with agreedbases of allocation and apportionment......................................................................................143.2 Calculation of Overhead absorption rate.............................................................................143.3 Adjustment for over or under recorded absorption cost .....................................................15

3.4 Methods of allocation, apportionment and absorption ......................................................153.5 Communicate with staff to resolve queries in overhead cost data......................................16TASK 4......................................................................................................................................164.1 Cost budget to identify variances........................................................................................164.2 Analysing the variance........................................................................................................164.3 Information for budget holders of any significant variances .............................................164.4 Management report in appropriate format.........................................................................17TASK 5...............................................................................................................................................185.1 Estimates of future income and cost for decision – making ..............................................185.2 Effect of changing activity level in unit cost......................................................................185.3 Calculation of Effecting of changing level of activity .......................................................195.4 factors affecting short term and long term decision making ..............................................19CONCLUSION..................................................................................................................................19REFERENCES...................................................................................................................................20

INTRODUCTIONCosting refers to the process in which the organisation use the costing system to estimate thecost of the product. This system assist in allocating the cost to the business operation on the basis ofwhich the selling price is determined. This study will include the nature and the role of costing system within an organisation. Moreover, It will contain the information relating to recording of the cost information. Furthermore, this study will provide understanding of apportion of the cost according to the organisational requirement. Also, This will provide analysis of deviation from budget and the use of information gathered form costing system to assist in decision- making.TASK 11.1 purpose of internal reporting and providing accurate information to managementInternal reporting system are the reports which are prepared by management for improvingthe performance of the company by analysing the information recorded in the reports. The internalreporting support the organisation in providing the accurate information which assist managementin making effective decision for the organisation profitability (Bai, Chen and Xu, 2017). Thisreporting provides the management with the information relating to the expenses, sales, employeeturnover etc. Management by using this information is able to improve its effectiveness whichsupport the firm in increasing its effectiveness. Moreover, It provides the management with insightrelating to the various issues which the firm is going through support in making decision which willresolve the problems (Ghiyasi, 2017). Management requires the internal reporting for analysingthe trend and identifying the profitability. Internal reporting provide the management in identifyingthe areas which require development and need to be improve for increasing the performance offirm.1.2 Relationship between various costing system in the organisationThere are different costing system that includes job order costing, process costing , contractcosting etc. Job costing system is used in organisation to identity the cost attributable to each job. Itdetermines the cost incurred for completing the particular job (Jacobson And et.al., 2015). Processcosting is relating to identify the cost of product in it's each process. In this system the output of oneprocess is the input of the other. Under contract costing the cost of each contract but the period ofthe contract is more than one year. There is a close relationship between these costing system as thisassist in determining the cost of the product by using different methods. For example, job costing isrelated to the contract costing as they both identify the cost relating to the completion of the job orcontract (Jayarani and Prakash, 2018). The costing system are interdependent as the process costing

is finished then only the job costing is undertaken.1.3 Identifying the responsibility centres ,cost centres , profit centres and investment centres inorganisation.Responsibility centres are the part of the organisation for which the management hold theresponsibility. The most common responsibility centres are the departments of the company. Whenthe manager of the responsibility centre can only control the cost then it is known as cost centre.The different responsibility centres in the organisation consist of cost centres, revenue centres,profit centre, investment centre (Malfertheiner and et.al., 2017). If the manager can control bothcost and profit and then the responsibility centre is known as profit centre. Manager of investmentcentre is having more authority and responsibility that the cost and profit centres. The organisational chart shows the sub- task which will be performed by differentdepartments of the organisation. The cost centres the managers is held responsible for the costincurred in that segment and not for revenues. The organisation have production and servicedepartments which are classified as the cost centres. Also, marketing department, sales departmentare the cost centres (Nguyen, 2018). Profit centre is responsible for both cost and revenues. Theprofit centre of the organisation includes the marketing manager of product and individual salesrepresentative. The profit centre include the accounting, auditing etc. there are separate division inthe organisation which are made as profit centre and they focus on earning profit. Investment centreincludes department that is responsible for earning return of investment.1.4 Characteristics of different types of cost classification and their use in costing There are various types of cost which are used in costing for determine the cost of theproduct in the organisation. There are different cost used in costing which includes the following :Fixed cost : It includes the cost which does not change with the change in the output. Thiscost is fixed and the organisation have to incur this cost whether it produces output or not. Itincludes rent, interest payment, property tax, wages to the labour.Variable cost : It changes with the change in output of the product. It includes cost ofmaterial , labour etc.Total cost : It is defined as the sum total of the fixed and variable cost (Preuß, Andreff, andWeitzmann, 2018).Direct and indirect cost : Direct cost includes the major components of the production of theproduct such as direct labour, direct material. This cost is also refereed to as prime cost.

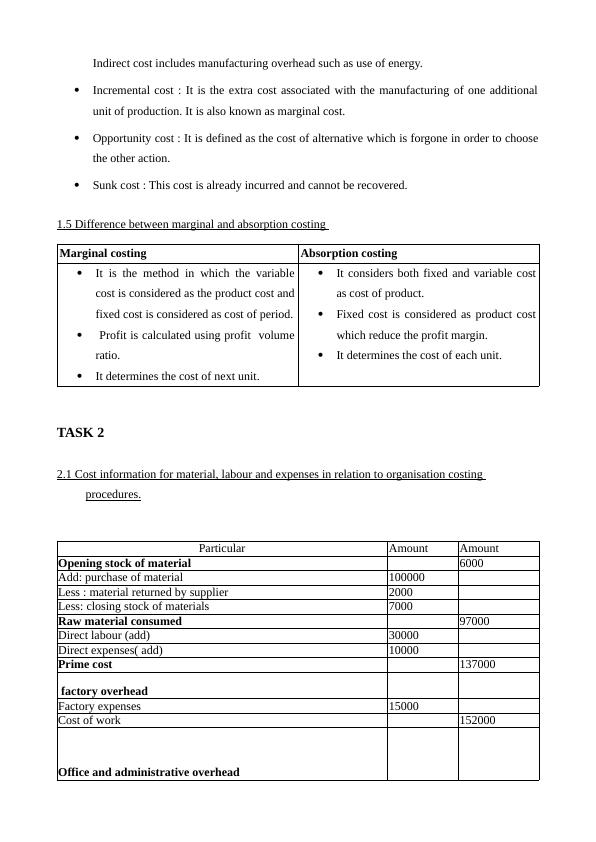

Indirect cost includes manufacturing overhead such as use of energy.Incremental cost : It is the extra cost associated with the manufacturing of one additionalunit of production. It is also known as marginal cost.Opportunity cost : It is defined as the cost of alternative which is forgone in order to choosethe other action.Sunk cost : This cost is already incurred and cannot be recovered.1.5 Difference between marginal and absorption costing Marginal costing Absorption costing It is the method in which the variablecost is considered as the product cost andfixed cost is considered as cost of period.Profit is calculated using profit volumeratio. It determines the cost of next unit.It considers both fixed and variable costas cost of product.Fixed cost is considered as product costwhich reduce the profit margin.It determines the cost of each unit.TASK 22.1 Cost information for material, labour and expenses in relation to organisation costing procedures.Particular Amount AmountOpening stock of material6000Add: purchase of material100000Less : material returned by supplier2000Less: closing stock of materials7000Raw material consumed97000Direct labour (add)30000Direct expenses( add)10000Prime cost 137000factory overheadFactory expenses15000Cost of work 152000Office and administrative overhead

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Costs and Revenues - Assignmentlg...

|23

|4695

|486

Cost and Revenue - Assignment Solutionlg...

|19

|3782

|497

Costs and Revenues Assignmentlg...

|18

|4722

|421

Cost and Revenue: Recording, Analysis, and Attribution of Costs in Business Entitieslg...

|17

|4216

|138

Cost and Revenue Assignment - Solvedlg...

|17

|4216

|126

Cost and Revenues - Assignmentlg...

|19

|4300

|341