MOD003462 - Financial Management Report: Cost, Valuation, Structure

VerifiedAdded on 2023/05/30

|9

|2886

|201

Report

AI Summary

This report provides an in-depth analysis of cost of capital estimation methods, including cost of debt, preference capital, equity capital (using CAPM, bond yield plus risk premium, dividend growth model, and earnings-price ratio), weighted average cost of capital, retained earnings, quasi capital, and marginal cost of capital. It further explores business valuation methods such as fund from operations (FFO), adjusted funds from operations (AFFO), and net asset value (NAV), applying NAV to value Segro PLC. The report also examines capital structure theories relevant to REITs, including trade-off theory, pecking order theory, and market timing theory, discussing changes in Segro's capital structure in 2017 due to the acquisition of APP and the subsequent equity share issuance through Right Issue.

Table of Contents

Cost of Equity and Other methods........................................................................................................2

Valuation methods of the business.......................................................................................................5

Theories of capital structure..................................................................................................................6

References.............................................................................................................................................8

Cost of Equity and Other methods........................................................................................................2

Valuation methods of the business.......................................................................................................5

Theories of capital structure..................................................................................................................6

References.............................................................................................................................................8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

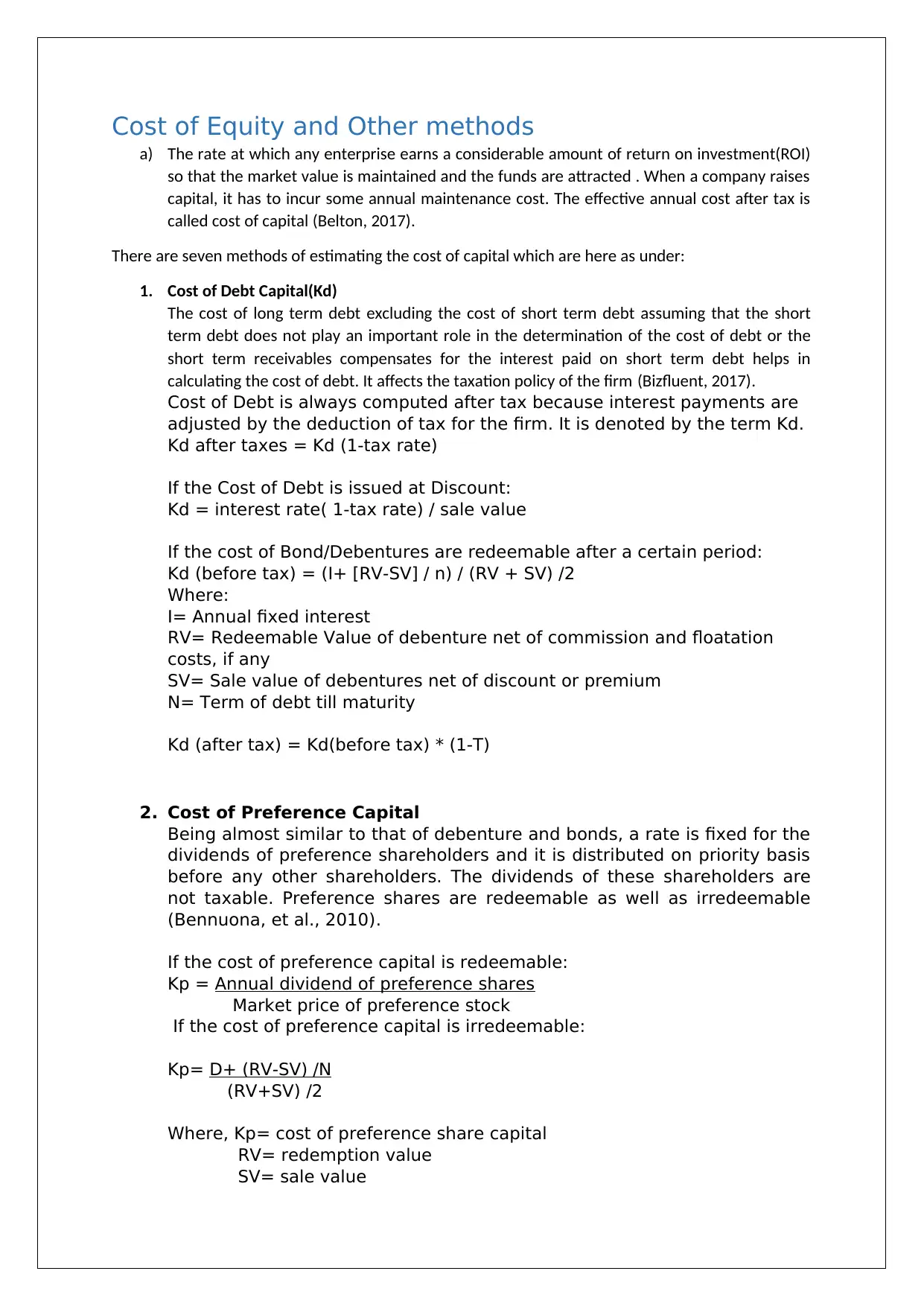

Cost of Equity and Other methods

a) The rate at which any enterprise earns a considerable amount of return on investment(ROI)

so that the market value is maintained and the funds are attracted . When a company raises

capital, it has to incur some annual maintenance cost. The effective annual cost after tax is

called cost of capital (Belton, 2017).

There are seven methods of estimating the cost of capital which are here as under:

1. Cost of Debt Capital(Kd)

The cost of long term debt excluding the cost of short term debt assuming that the short

term debt does not play an important role in the determination of the cost of debt or the

short term receivables compensates for the interest paid on short term debt helps in

calculating the cost of debt. It affects the taxation policy of the firm (Bizfluent, 2017).

Cost of Debt is always computed after tax because interest payments are

adjusted by the deduction of tax for the firm. It is denoted by the term Kd.

Kd after taxes = Kd (1-tax rate)

If the Cost of Debt is issued at Discount:

Kd = interest rate( 1-tax rate) / sale value

If the cost of Bond/Debentures are redeemable after a certain period:

Kd (before tax) = (I+ [RV-SV] / n) / (RV + SV) /2

Where:

I= Annual fixed interest

RV= Redeemable Value of debenture net of commission and floatation

costs, if any

SV= Sale value of debentures net of discount or premium

N= Term of debt till maturity

Kd (after tax) = Kd(before tax) * (1-T)

2. Cost of Preference Capital

Being almost similar to that of debenture and bonds, a rate is fixed for the

dividends of preference shareholders and it is distributed on priority basis

before any other shareholders. The dividends of these shareholders are

not taxable. Preference shares are redeemable as well as irredeemable

(Bennuona, et al., 2010).

If the cost of preference capital is redeemable:

Kp = Annual dividend of preference shares

Market price of preference stock

If the cost of preference capital is irredeemable:

Kp= D+ (RV-SV) /N

(RV+SV) /2

Where, Kp= cost of preference share capital

RV= redemption value

SV= sale value

a) The rate at which any enterprise earns a considerable amount of return on investment(ROI)

so that the market value is maintained and the funds are attracted . When a company raises

capital, it has to incur some annual maintenance cost. The effective annual cost after tax is

called cost of capital (Belton, 2017).

There are seven methods of estimating the cost of capital which are here as under:

1. Cost of Debt Capital(Kd)

The cost of long term debt excluding the cost of short term debt assuming that the short

term debt does not play an important role in the determination of the cost of debt or the

short term receivables compensates for the interest paid on short term debt helps in

calculating the cost of debt. It affects the taxation policy of the firm (Bizfluent, 2017).

Cost of Debt is always computed after tax because interest payments are

adjusted by the deduction of tax for the firm. It is denoted by the term Kd.

Kd after taxes = Kd (1-tax rate)

If the Cost of Debt is issued at Discount:

Kd = interest rate( 1-tax rate) / sale value

If the cost of Bond/Debentures are redeemable after a certain period:

Kd (before tax) = (I+ [RV-SV] / n) / (RV + SV) /2

Where:

I= Annual fixed interest

RV= Redeemable Value of debenture net of commission and floatation

costs, if any

SV= Sale value of debentures net of discount or premium

N= Term of debt till maturity

Kd (after tax) = Kd(before tax) * (1-T)

2. Cost of Preference Capital

Being almost similar to that of debenture and bonds, a rate is fixed for the

dividends of preference shareholders and it is distributed on priority basis

before any other shareholders. The dividends of these shareholders are

not taxable. Preference shares are redeemable as well as irredeemable

(Bennuona, et al., 2010).

If the cost of preference capital is redeemable:

Kp = Annual dividend of preference shares

Market price of preference stock

If the cost of preference capital is irredeemable:

Kp= D+ (RV-SV) /N

(RV+SV) /2

Where, Kp= cost of preference share capital

RV= redemption value

SV= sale value

N= no. of years to maturity

D= Annual Dividend

3. Cost of Equity Capital

The money which is invested by the investors also the promoters of the firm determines the

cost of Equity (Choy, 2018). The return on investments earned in terms of dividends. The

various ways to calculate the cost of equity are:

CAPM model

The first is the most oldest way to calculate the cost of equity. The return rate

at which the cost of equity capital is determined.

Ke = Krf + Beta (Km-Krf)

Where,

Ke= cost of equity

Krf = Risk-free rate

Km = Equity market required return (expected return on the market portfolio)

beta =Systematic Risk Coefficient.

Bond Yield Plus Risk Premium Approach

This is a way which is precise enough to calculate the cost of equity. In this approach

a amount of premium related to risk is added to the return which is derived from the

long term bonds or debentures.

Cost of equity = Yield on long-term bonds + Risk Premium.

Dividend Growth Model Approach

The cost of the equity is dependent entirely on the dividends which are earned by

the shareholders.

r = D1/P0+ g

where: P0 = Current price of the stock

D1 = Expected dividend at the end of year 1

t = Year t

r = Equity shareholders' required rate of return

Earnings-Price Ratio Approach

This way shows the formula as :

Ke = E1 /P0

Where: E1 = Expected earnings per share for the next year

P0 = Current market price per share

E1 = (Current EPS) * (1 + growth rate of EPS)

4. Weighted Average cost of capital

WACC is calculated taking all the average of the weights using the book

value weights and the market value weights. It can use any of the values

as weights to determine the same (Sonu, et al., 2017).

Weighted Average Cost of Capital = (KE * E) + (KP * P) + (KD * D) + (KR*

R)

Where,

D= Annual Dividend

3. Cost of Equity Capital

The money which is invested by the investors also the promoters of the firm determines the

cost of Equity (Choy, 2018). The return on investments earned in terms of dividends. The

various ways to calculate the cost of equity are:

CAPM model

The first is the most oldest way to calculate the cost of equity. The return rate

at which the cost of equity capital is determined.

Ke = Krf + Beta (Km-Krf)

Where,

Ke= cost of equity

Krf = Risk-free rate

Km = Equity market required return (expected return on the market portfolio)

beta =Systematic Risk Coefficient.

Bond Yield Plus Risk Premium Approach

This is a way which is precise enough to calculate the cost of equity. In this approach

a amount of premium related to risk is added to the return which is derived from the

long term bonds or debentures.

Cost of equity = Yield on long-term bonds + Risk Premium.

Dividend Growth Model Approach

The cost of the equity is dependent entirely on the dividends which are earned by

the shareholders.

r = D1/P0+ g

where: P0 = Current price of the stock

D1 = Expected dividend at the end of year 1

t = Year t

r = Equity shareholders' required rate of return

Earnings-Price Ratio Approach

This way shows the formula as :

Ke = E1 /P0

Where: E1 = Expected earnings per share for the next year

P0 = Current market price per share

E1 = (Current EPS) * (1 + growth rate of EPS)

4. Weighted Average cost of capital

WACC is calculated taking all the average of the weights using the book

value weights and the market value weights. It can use any of the values

as weights to determine the same (Sonu, et al., 2017).

Weighted Average Cost of Capital = (KE * E) + (KP * P) + (KD * D) + (KR*

R)

Where,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

E = Proportion of equity capital in capital structure

P = Proportion of preference capital in capital structure

D = Proportion of debt capital in capital structure

KR = Cost of proportion of retained earnings in capital structure

R = Proportion of retained earnings in capital structure

5. Cost of Retained Earnings

A part of earnings set aside for the equity shareholders and for the equity

capital is known as retained earnings (Werner, 2017).

It can be said that Kr=Ke

Where:

Kr= cost of retained earnings

Ke= cost of equity share capital

6. Quasi Capital

7. Marginal Cost of Capital

It is the excess amount of cost to be raised, so when the additional

amount is required to be raised by debt then the cost of debt will be the

marginal cost of capital (Vieira, et al., 2017).

The marginal cost of capital will be calculated by taking the effects of

additional cost of capital on the profit of the company as a whole.

a (i) Cost of Equity:

The rate at which the return on an investment is predicted is by the CAPM

model.CAPM defines as Capital Assets Pricing Model .The formula for the CAPM

model is

The formula is:

Cost of Equity = Risk-Free Rate of Return + Beta of Asset X (Expected Return of the

Market - Risk-Free Rate of Return)

Using 10-Year Treasury Constant Maturity Rate as the risk-free rate. The current

risk-free rate is 1.50230000%.

Segro PLC's beta is 0.31.

market premium is 6%.

Cost of Equity of Segro Equity Providers = 1.50230000% + 0.31 * 6% = 3.3623%

(ii) Cost of Debt

Tenure of Bond 19 Years

Interest Rate 5.75%

Due date of Bond 2035

Book value of Debt £200.00

£11.50

Cost of Debt =

Interest

Expenses

Book

value of

P = Proportion of preference capital in capital structure

D = Proportion of debt capital in capital structure

KR = Cost of proportion of retained earnings in capital structure

R = Proportion of retained earnings in capital structure

5. Cost of Retained Earnings

A part of earnings set aside for the equity shareholders and for the equity

capital is known as retained earnings (Werner, 2017).

It can be said that Kr=Ke

Where:

Kr= cost of retained earnings

Ke= cost of equity share capital

6. Quasi Capital

7. Marginal Cost of Capital

It is the excess amount of cost to be raised, so when the additional

amount is required to be raised by debt then the cost of debt will be the

marginal cost of capital (Vieira, et al., 2017).

The marginal cost of capital will be calculated by taking the effects of

additional cost of capital on the profit of the company as a whole.

a (i) Cost of Equity:

The rate at which the return on an investment is predicted is by the CAPM

model.CAPM defines as Capital Assets Pricing Model .The formula for the CAPM

model is

The formula is:

Cost of Equity = Risk-Free Rate of Return + Beta of Asset X (Expected Return of the

Market - Risk-Free Rate of Return)

Using 10-Year Treasury Constant Maturity Rate as the risk-free rate. The current

risk-free rate is 1.50230000%.

Segro PLC's beta is 0.31.

market premium is 6%.

Cost of Equity of Segro Equity Providers = 1.50230000% + 0.31 * 6% = 3.3623%

(ii) Cost of Debt

Tenure of Bond 19 Years

Interest Rate 5.75%

Due date of Bond 2035

Book value of Debt £200.00

£11.50

Cost of Debt =

Interest

Expenses

Book

value of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

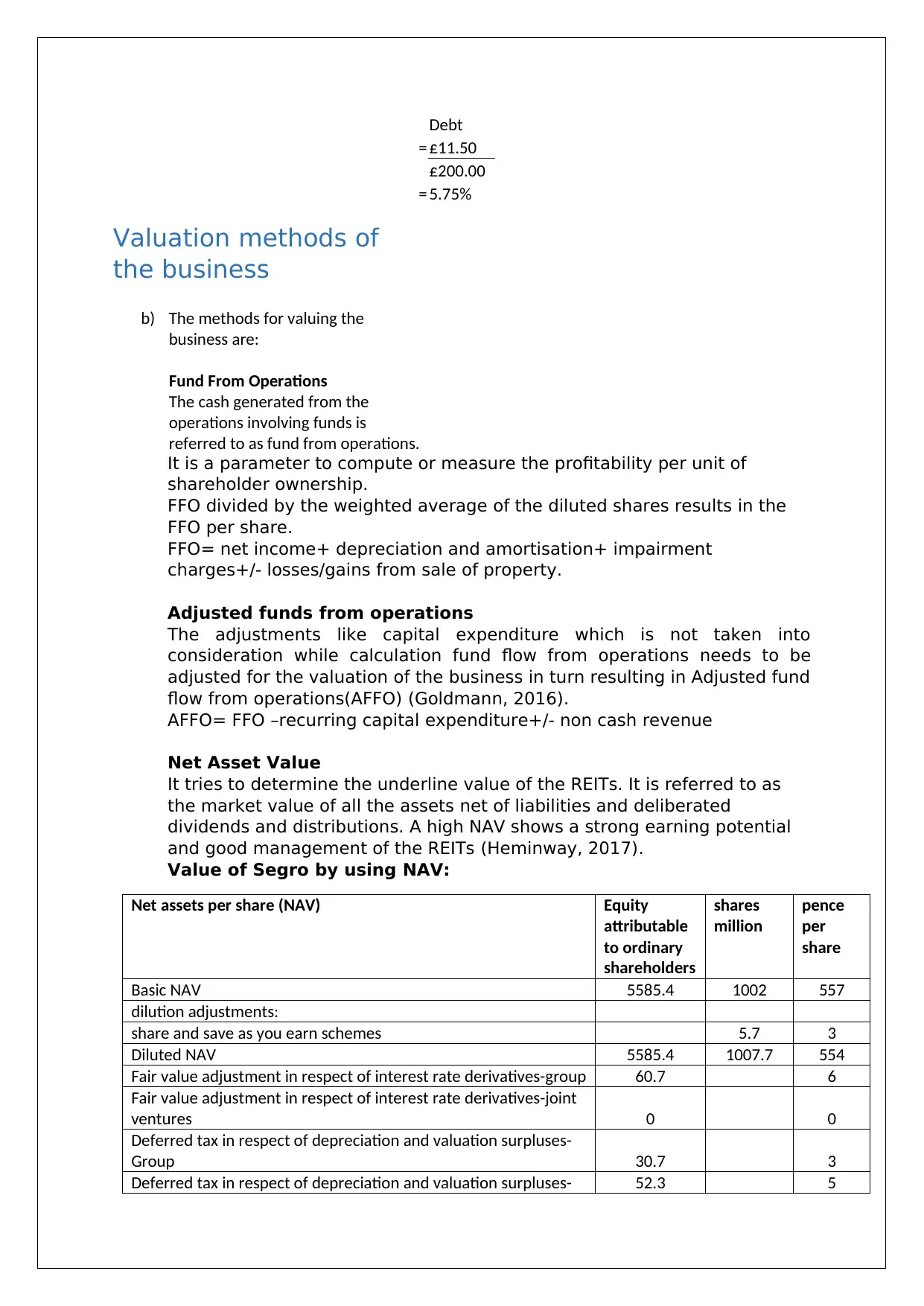

Debt

= £11.50

£200.00

= 5.75%

Valuation methods of

the business

b) The methods for valuing the

business are:

Fund From Operations

The cash generated from the

operations involving funds is

referred to as fund from operations.

It is a parameter to compute or measure the profitability per unit of

shareholder ownership.

FFO divided by the weighted average of the diluted shares results in the

FFO per share.

FFO= net income+ depreciation and amortisation+ impairment

charges+/- losses/gains from sale of property.

Adjusted funds from operations

The adjustments like capital expenditure which is not taken into

consideration while calculation fund flow from operations needs to be

adjusted for the valuation of the business in turn resulting in Adjusted fund

flow from operations(AFFO) (Goldmann, 2016).

AFFO= FFO –recurring capital expenditure+/- non cash revenue

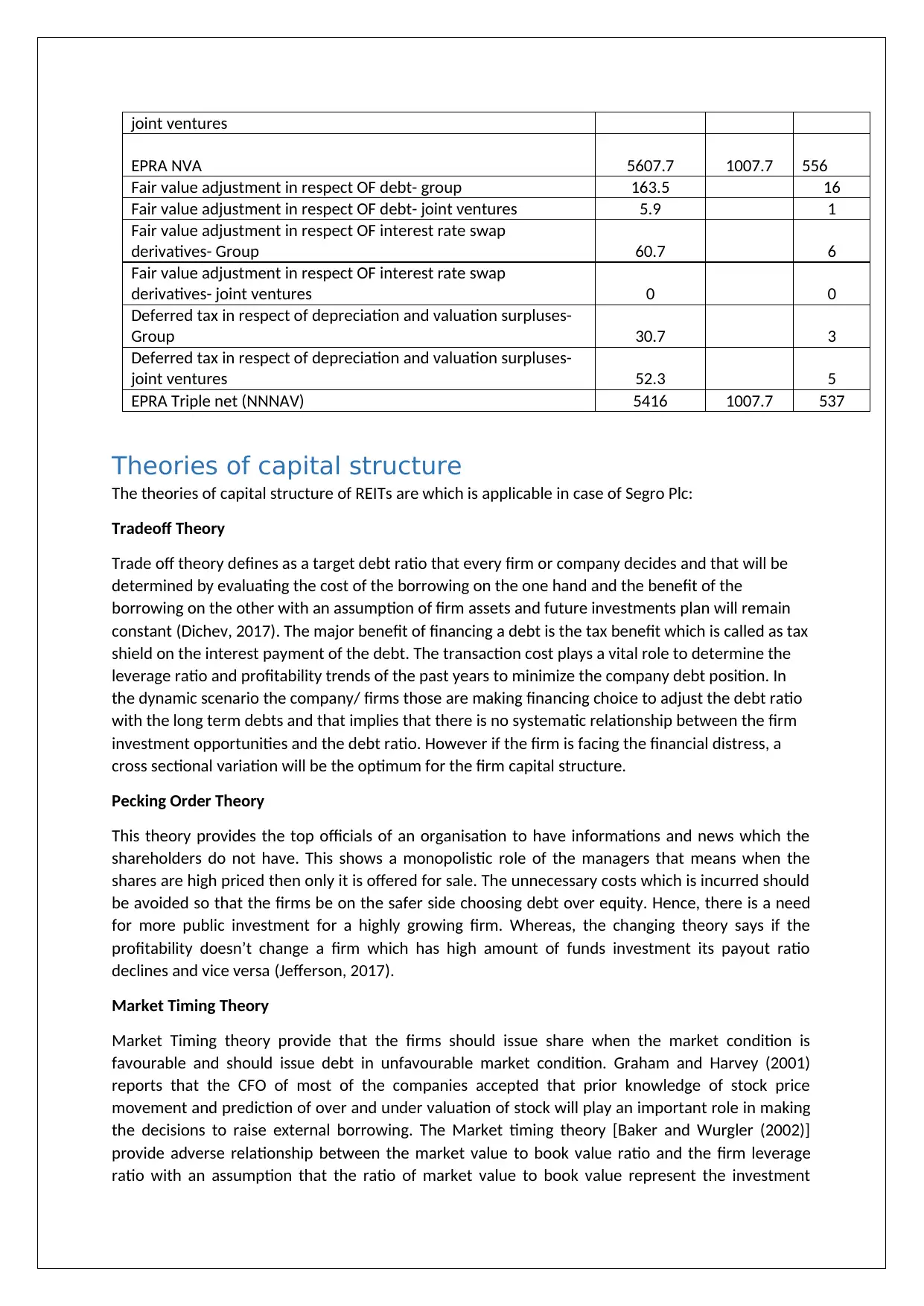

Net Asset Value

It tries to determine the underline value of the REITs. It is referred to as

the market value of all the assets net of liabilities and deliberated

dividends and distributions. A high NAV shows a strong earning potential

and good management of the REITs (Heminway, 2017).

Value of Segro by using NAV:

Net assets per share (NAV) Equity

attributable

to ordinary

shareholders

shares

million

pence

per

share

Basic NAV 5585.4 1002 557

dilution adjustments:

share and save as you earn schemes 5.7 3

Diluted NAV 5585.4 1007.7 554

Fair value adjustment in respect of interest rate derivatives-group 60.7 6

Fair value adjustment in respect of interest rate derivatives-joint

ventures 0 0

Deferred tax in respect of depreciation and valuation surpluses-

Group 30.7 3

Deferred tax in respect of depreciation and valuation surpluses- 52.3 5

= £11.50

£200.00

= 5.75%

Valuation methods of

the business

b) The methods for valuing the

business are:

Fund From Operations

The cash generated from the

operations involving funds is

referred to as fund from operations.

It is a parameter to compute or measure the profitability per unit of

shareholder ownership.

FFO divided by the weighted average of the diluted shares results in the

FFO per share.

FFO= net income+ depreciation and amortisation+ impairment

charges+/- losses/gains from sale of property.

Adjusted funds from operations

The adjustments like capital expenditure which is not taken into

consideration while calculation fund flow from operations needs to be

adjusted for the valuation of the business in turn resulting in Adjusted fund

flow from operations(AFFO) (Goldmann, 2016).

AFFO= FFO –recurring capital expenditure+/- non cash revenue

Net Asset Value

It tries to determine the underline value of the REITs. It is referred to as

the market value of all the assets net of liabilities and deliberated

dividends and distributions. A high NAV shows a strong earning potential

and good management of the REITs (Heminway, 2017).

Value of Segro by using NAV:

Net assets per share (NAV) Equity

attributable

to ordinary

shareholders

shares

million

pence

per

share

Basic NAV 5585.4 1002 557

dilution adjustments:

share and save as you earn schemes 5.7 3

Diluted NAV 5585.4 1007.7 554

Fair value adjustment in respect of interest rate derivatives-group 60.7 6

Fair value adjustment in respect of interest rate derivatives-joint

ventures 0 0

Deferred tax in respect of depreciation and valuation surpluses-

Group 30.7 3

Deferred tax in respect of depreciation and valuation surpluses- 52.3 5

joint ventures

EPRA NVA 5607.7 1007.7 556

Fair value adjustment in respect OF debt- group 163.5 16

Fair value adjustment in respect OF debt- joint ventures 5.9 1

Fair value adjustment in respect OF interest rate swap

derivatives- Group 60.7 6

Fair value adjustment in respect OF interest rate swap

derivatives- joint ventures 0 0

Deferred tax in respect of depreciation and valuation surpluses-

Group 30.7 3

Deferred tax in respect of depreciation and valuation surpluses-

joint ventures 52.3 5

EPRA Triple net (NNNAV) 5416 1007.7 537

Theories of capital structure

The theories of capital structure of REITs are which is applicable in case of Segro Plc:

Tradeoff Theory

Trade off theory defines as a target debt ratio that every firm or company decides and that will be

determined by evaluating the cost of the borrowing on the one hand and the benefit of the

borrowing on the other with an assumption of firm assets and future investments plan will remain

constant (Dichev, 2017). The major benefit of financing a debt is the tax benefit which is called as tax

shield on the interest payment of the debt. The transaction cost plays a vital role to determine the

leverage ratio and profitability trends of the past years to minimize the company debt position. In

the dynamic scenario the company/ firms those are making financing choice to adjust the debt ratio

with the long term debts and that implies that there is no systematic relationship between the firm

investment opportunities and the debt ratio. However if the firm is facing the financial distress, a

cross sectional variation will be the optimum for the firm capital structure.

Pecking Order Theory

This theory provides the top officials of an organisation to have informations and news which the

shareholders do not have. This shows a monopolistic role of the managers that means when the

shares are high priced then only it is offered for sale. The unnecessary costs which is incurred should

be avoided so that the firms be on the safer side choosing debt over equity. Hence, there is a need

for more public investment for a highly growing firm. Whereas, the changing theory says if the

profitability doesn’t change a firm which has high amount of funds investment its payout ratio

declines and vice versa (Jefferson, 2017).

Market Timing Theory

Market Timing theory provide that the firms should issue share when the market condition is

favourable and should issue debt in unfavourable market condition. Graham and Harvey (2001)

reports that the CFO of most of the companies accepted that prior knowledge of stock price

movement and prediction of over and under valuation of stock will play an important role in making

the decisions to raise external borrowing. The Market timing theory [Baker and Wurgler (2002)]

provide adverse relationship between the market value to book value ratio and the firm leverage

ratio with an assumption that the ratio of market value to book value represent the investment

EPRA NVA 5607.7 1007.7 556

Fair value adjustment in respect OF debt- group 163.5 16

Fair value adjustment in respect OF debt- joint ventures 5.9 1

Fair value adjustment in respect OF interest rate swap

derivatives- Group 60.7 6

Fair value adjustment in respect OF interest rate swap

derivatives- joint ventures 0 0

Deferred tax in respect of depreciation and valuation surpluses-

Group 30.7 3

Deferred tax in respect of depreciation and valuation surpluses-

joint ventures 52.3 5

EPRA Triple net (NNNAV) 5416 1007.7 537

Theories of capital structure

The theories of capital structure of REITs are which is applicable in case of Segro Plc:

Tradeoff Theory

Trade off theory defines as a target debt ratio that every firm or company decides and that will be

determined by evaluating the cost of the borrowing on the one hand and the benefit of the

borrowing on the other with an assumption of firm assets and future investments plan will remain

constant (Dichev, 2017). The major benefit of financing a debt is the tax benefit which is called as tax

shield on the interest payment of the debt. The transaction cost plays a vital role to determine the

leverage ratio and profitability trends of the past years to minimize the company debt position. In

the dynamic scenario the company/ firms those are making financing choice to adjust the debt ratio

with the long term debts and that implies that there is no systematic relationship between the firm

investment opportunities and the debt ratio. However if the firm is facing the financial distress, a

cross sectional variation will be the optimum for the firm capital structure.

Pecking Order Theory

This theory provides the top officials of an organisation to have informations and news which the

shareholders do not have. This shows a monopolistic role of the managers that means when the

shares are high priced then only it is offered for sale. The unnecessary costs which is incurred should

be avoided so that the firms be on the safer side choosing debt over equity. Hence, there is a need

for more public investment for a highly growing firm. Whereas, the changing theory says if the

profitability doesn’t change a firm which has high amount of funds investment its payout ratio

declines and vice versa (Jefferson, 2017).

Market Timing Theory

Market Timing theory provide that the firms should issue share when the market condition is

favourable and should issue debt in unfavourable market condition. Graham and Harvey (2001)

reports that the CFO of most of the companies accepted that prior knowledge of stock price

movement and prediction of over and under valuation of stock will play an important role in making

the decisions to raise external borrowing. The Market timing theory [Baker and Wurgler (2002)]

provide adverse relationship between the market value to book value ratio and the firm leverage

ratio with an assumption that the ratio of market value to book value represent the investment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

opportunities (Kewell & Linsley, 2017). This theory is contradictory with the pecking order theory but

seems to be consistent and more dynamic form. The authors has rejected both the trade-off theory

pecking order model provide the solution with a supporting of all that current leverage ratio provide

a cumulative outcome of the firm past attempts to time the stock market. While all the three

theories has overlapping effects, and they also provide some forecasts that can be used to

determine which theories fit the best while making choices regarding capital structure.

Changes of Segro Capital Structure

In end of the financial year 2017, the company had assessed the impact on the financial statement of

investment in acquisition of the company APP and Board decided top issue equity share of the

company through Right Issue. (Linden & Freeman, 2017) The company has issued 166 million shares

at an issue price of 345 pence per share. The Company had made a right issue in the ratio of one

share for every five share held. Through right issue company had obtained to raise a handsome sum

of Pound 573 million after bearing the expenditure of Pound 16 million as issue expenses. The

proceeds received against the right issue were utilised to acquire the APP and the balance proceeds

were kept for funding the capital expenditure in forthcoming development of the company. The

company had made a right issue at discount rate and provide the privileged to all the shareholders

to participate in the right issue (Meroño-Cerdán, et al., 2017).

During 2017, the company has got the opportunity to improve the efficiency in the company and

also increase the duration of borrowing in the Group. The company had issued a new Pound 1.77

billion of debt with a maturity of approx 13 years bearing interest rate of 2.1 percent, in addition

also raised the banking facilities by pound 388 million. In May 2017, the company had entered into a

euro transaction issuing Euro 650 million with a maturity of approx. 11.2 years bearing interest rate

of 1.9 percent (Oberoi, 2018). The proceeds were utilised in repaying the debt that were acquired

along with the APP acquisition. The debt were comprises of sterling bond of pound 200 million

bearing coupon rate of 5.5 percent having due date in June 2018. Thus, the year of 2017 were seems

to be the most favourable year for the company in respect of the financial position.

seems to be consistent and more dynamic form. The authors has rejected both the trade-off theory

pecking order model provide the solution with a supporting of all that current leverage ratio provide

a cumulative outcome of the firm past attempts to time the stock market. While all the three

theories has overlapping effects, and they also provide some forecasts that can be used to

determine which theories fit the best while making choices regarding capital structure.

Changes of Segro Capital Structure

In end of the financial year 2017, the company had assessed the impact on the financial statement of

investment in acquisition of the company APP and Board decided top issue equity share of the

company through Right Issue. (Linden & Freeman, 2017) The company has issued 166 million shares

at an issue price of 345 pence per share. The Company had made a right issue in the ratio of one

share for every five share held. Through right issue company had obtained to raise a handsome sum

of Pound 573 million after bearing the expenditure of Pound 16 million as issue expenses. The

proceeds received against the right issue were utilised to acquire the APP and the balance proceeds

were kept for funding the capital expenditure in forthcoming development of the company. The

company had made a right issue at discount rate and provide the privileged to all the shareholders

to participate in the right issue (Meroño-Cerdán, et al., 2017).

During 2017, the company has got the opportunity to improve the efficiency in the company and

also increase the duration of borrowing in the Group. The company had issued a new Pound 1.77

billion of debt with a maturity of approx 13 years bearing interest rate of 2.1 percent, in addition

also raised the banking facilities by pound 388 million. In May 2017, the company had entered into a

euro transaction issuing Euro 650 million with a maturity of approx. 11.2 years bearing interest rate

of 1.9 percent (Oberoi, 2018). The proceeds were utilised in repaying the debt that were acquired

along with the APP acquisition. The debt were comprises of sterling bond of pound 200 million

bearing coupon rate of 5.5 percent having due date in June 2018. Thus, the year of 2017 were seems

to be the most favourable year for the company in respect of the financial position.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London:

Macat International ltd.

Bennuona, K., Meredith, G. & Marchant, T., 2010. Improved capital budgeting decision making:

Evidence from Canada. Emerald Management Division, 48(2), pp. 225-247.

Bizfluent, 2017. Advantages & Disadvantages of Internal Control. [Online]

Available at: https://bizfluent.com/info-8064250-advantages-disadvantages-internal-control.html

[Accessed 13 September 2018].

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, p. 145.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, Volume 4, pp. 103-112.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Kewell, B. & Linsley, P., 2017. Risk tools and risk technologies.. The Routledge Companion to

Accounting and Risk, 15.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making.

Business Ethics Quarterly, 27(3), pp. 353-379.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

Oberoi, J., 2018. Interest rate risk management and the mix of fixed and floating rate debt. Journal

of Banking and Finance, Volume 86, pp. 70-86.

Sonu, C., Ahn, H. & Choi, A., 2017. Audit fee pressure and audit risk: evidence from the financial crisis

of 2008. Asia-Pacific Journal of Accounting & Economics , 24(1-2), pp. 127-144.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management

Systems. SAGE Journals, 30(1).

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London:

Macat International ltd.

Bennuona, K., Meredith, G. & Marchant, T., 2010. Improved capital budgeting decision making:

Evidence from Canada. Emerald Management Division, 48(2), pp. 225-247.

Bizfluent, 2017. Advantages & Disadvantages of Internal Control. [Online]

Available at: https://bizfluent.com/info-8064250-advantages-disadvantages-internal-control.html

[Accessed 13 September 2018].

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, p. 145.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, Volume 4, pp. 103-112.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Kewell, B. & Linsley, P., 2017. Risk tools and risk technologies.. The Routledge Companion to

Accounting and Risk, 15.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making.

Business Ethics Quarterly, 27(3), pp. 353-379.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

Oberoi, J., 2018. Interest rate risk management and the mix of fixed and floating rate debt. Journal

of Banking and Finance, Volume 86, pp. 70-86.

Sonu, C., Ahn, H. & Choi, A., 2017. Audit fee pressure and audit risk: evidence from the financial crisis

of 2008. Asia-Pacific Journal of Accounting & Economics , 24(1-2), pp. 127-144.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management

Systems. SAGE Journals, 30(1).

Werner, M., 2017. Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, Volume 25, pp. 57-80.

inference. International Journal of Accounting Information Systems, Volume 25, pp. 57-80.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9