Sales, Expense & Performance Budgeting

VerifiedAdded on 2020/05/08

|16

|3380

|54

AI Summary

The assignment delves into different budgeting methodologies used by businesses. It examines forecast budgeting, encompassing sales and expense budgets, and highlights the significance of performance budgeting for monitoring an entity's financial health and operational efficiency. The analysis emphasizes the role of cost control and planning strategies in achieving desired outcomes.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MPA

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Company background................................................................................................................1

Cost Information analysis..........................................................................................................2

Cost reduction and value added.................................................................................................4

Forecasts and budgets................................................................................................................4

Monitor Performance.................................................................................................................7

CONCLUSION..........................................................................................................................8

REFERENCES...........................................................................................................................9

Company background................................................................................................................1

Cost Information analysis..........................................................................................................2

Cost reduction and value added.................................................................................................4

Forecasts and budgets................................................................................................................4

Monitor Performance.................................................................................................................7

CONCLUSION..........................................................................................................................8

REFERENCES...........................................................................................................................9

COMPANY BACKGROUND

Woolworth is large scale supermarket based in Australia operated in a retail sector by

offering variety of goods to seal the attention of its most of the users. This grocery chain has

founded by Woolworth Limited in 1924 in Bella Vista New South Wales. The grocery stores

have 992 stores located all across the world to capture the whole world. Various products

available in the grocery stores Woolworth Ltd include Vegetables, fruits, poultry products

and packaged products (Woolworth, 2017). Customers like to visit this place as the current

saves the time of the client by purchasing all the stuff available under same roof. Other than

grocery items other stuff available at this store includes entertainment items, magazines,

health and wellness products, household products, pet and baby products and stationery

items. Due to the variety of ranges of products available in the store of an entity helps in

targeting different age group people such as infant, teenager, adult and old age people. A

person can purchase the products from this store by visiting the retail store as well as

purchasing from the online store (Durojaiye, Bell Gorrod, Andrews, Ntziora, and Cartwright,

2017). Through E- commerce website of the firm a customer can purchase the goods from

anywhere and anytime according to its availability.

Initial name of this store in 1924 was Wall worth bazaar Ltd which further changed to

Woolworth Ltd Supermarket that includes all the goods available in this market to meet the

desired needs of all the users (Winkler, 2017). Fresh and food people campaign has organised

by the firm o deliver quality oriented services to its variety of users by emphasizes on the

freshness of the products as health of the customers gets affected by eating fresh or stale

food. Slogan of the supermarket was Australian fresh food people that catch the attention of

most of the users towards this store as everyone wants to visits the store to explore different

varieties of stuff available in the same roof.

1

Woolworth is large scale supermarket based in Australia operated in a retail sector by

offering variety of goods to seal the attention of its most of the users. This grocery chain has

founded by Woolworth Limited in 1924 in Bella Vista New South Wales. The grocery stores

have 992 stores located all across the world to capture the whole world. Various products

available in the grocery stores Woolworth Ltd include Vegetables, fruits, poultry products

and packaged products (Woolworth, 2017). Customers like to visit this place as the current

saves the time of the client by purchasing all the stuff available under same roof. Other than

grocery items other stuff available at this store includes entertainment items, magazines,

health and wellness products, household products, pet and baby products and stationery

items. Due to the variety of ranges of products available in the store of an entity helps in

targeting different age group people such as infant, teenager, adult and old age people. A

person can purchase the products from this store by visiting the retail store as well as

purchasing from the online store (Durojaiye, Bell Gorrod, Andrews, Ntziora, and Cartwright,

2017). Through E- commerce website of the firm a customer can purchase the goods from

anywhere and anytime according to its availability.

Initial name of this store in 1924 was Wall worth bazaar Ltd which further changed to

Woolworth Ltd Supermarket that includes all the goods available in this market to meet the

desired needs of all the users (Winkler, 2017). Fresh and food people campaign has organised

by the firm o deliver quality oriented services to its variety of users by emphasizes on the

freshness of the products as health of the customers gets affected by eating fresh or stale

food. Slogan of the supermarket was Australian fresh food people that catch the attention of

most of the users towards this store as everyone wants to visits the store to explore different

varieties of stuff available in the same roof.

1

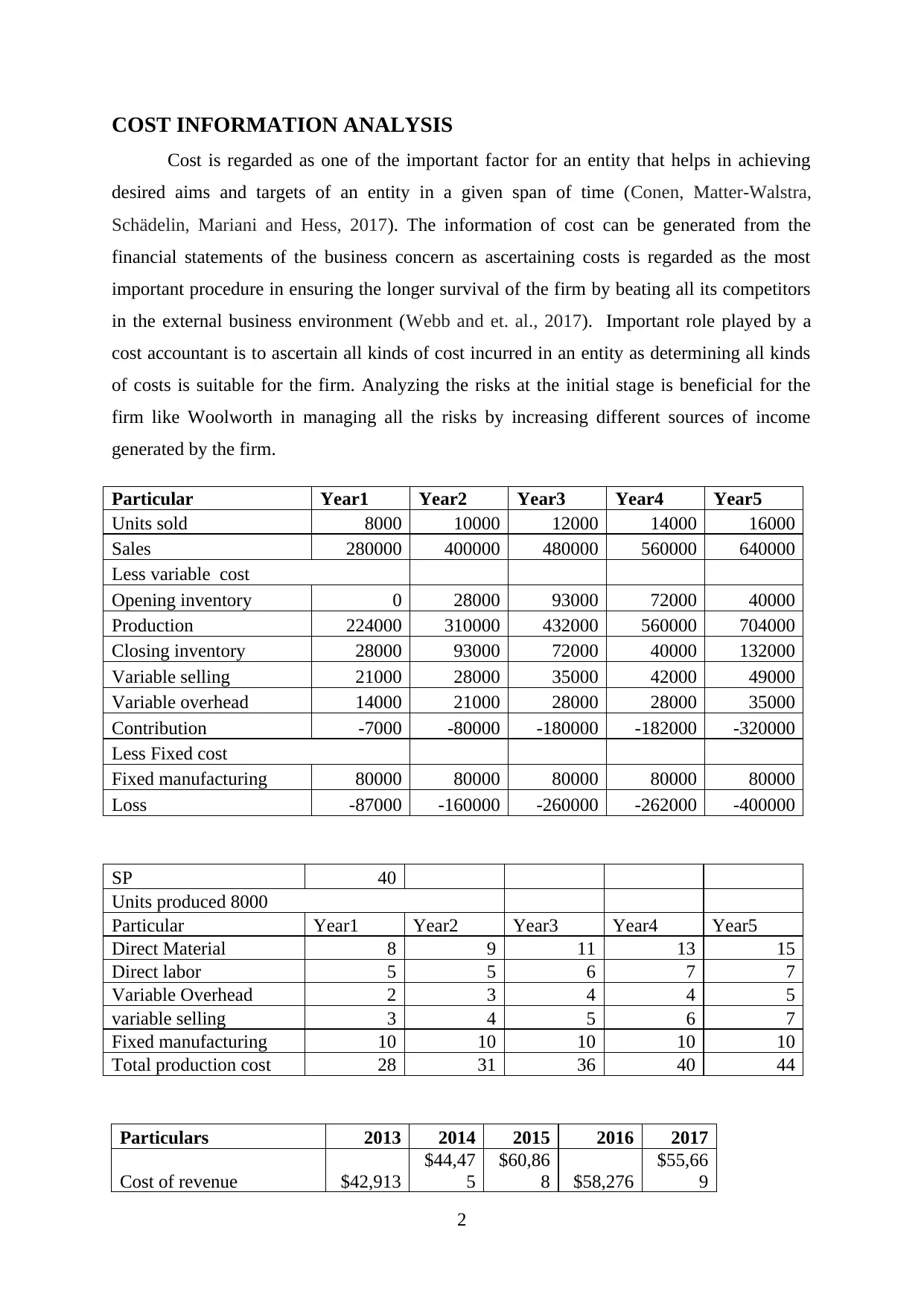

COST INFORMATION ANALYSIS

Cost is regarded as one of the important factor for an entity that helps in achieving

desired aims and targets of an entity in a given span of time (Conen, Matter-Walstra,

Schädelin, Mariani and Hess, 2017). The information of cost can be generated from the

financial statements of the business concern as ascertaining costs is regarded as the most

important procedure in ensuring the longer survival of the firm by beating all its competitors

in the external business environment (Webb and et. al., 2017). Important role played by a

cost accountant is to ascertain all kinds of cost incurred in an entity as determining all kinds

of costs is suitable for the firm. Analyzing the risks at the initial stage is beneficial for the

firm like Woolworth in managing all the risks by increasing different sources of income

generated by the firm.

Particular Year1 Year2 Year3 Year4 Year5

Units sold 8000 10000 12000 14000 16000

Sales 280000 400000 480000 560000 640000

Less variable cost

Opening inventory 0 28000 93000 72000 40000

Production 224000 310000 432000 560000 704000

Closing inventory 28000 93000 72000 40000 132000

Variable selling 21000 28000 35000 42000 49000

Variable overhead 14000 21000 28000 28000 35000

Contribution -7000 -80000 -180000 -182000 -320000

Less Fixed cost

Fixed manufacturing 80000 80000 80000 80000 80000

Loss -87000 -160000 -260000 -262000 -400000

SP 40

Units produced 8000

Particular Year1 Year2 Year3 Year4 Year5

Direct Material 8 9 11 13 15

Direct labor 5 5 6 7 7

Variable Overhead 2 3 4 4 5

variable selling 3 4 5 6 7

Fixed manufacturing 10 10 10 10 10

Total production cost 28 31 36 40 44

Particulars 2013 2014 2015 2016 2017

Cost of revenue $42,913

$44,47

5

$60,86

8 $58,276

$55,66

9

2

Cost is regarded as one of the important factor for an entity that helps in achieving

desired aims and targets of an entity in a given span of time (Conen, Matter-Walstra,

Schädelin, Mariani and Hess, 2017). The information of cost can be generated from the

financial statements of the business concern as ascertaining costs is regarded as the most

important procedure in ensuring the longer survival of the firm by beating all its competitors

in the external business environment (Webb and et. al., 2017). Important role played by a

cost accountant is to ascertain all kinds of cost incurred in an entity as determining all kinds

of costs is suitable for the firm. Analyzing the risks at the initial stage is beneficial for the

firm like Woolworth in managing all the risks by increasing different sources of income

generated by the firm.

Particular Year1 Year2 Year3 Year4 Year5

Units sold 8000 10000 12000 14000 16000

Sales 280000 400000 480000 560000 640000

Less variable cost

Opening inventory 0 28000 93000 72000 40000

Production 224000 310000 432000 560000 704000

Closing inventory 28000 93000 72000 40000 132000

Variable selling 21000 28000 35000 42000 49000

Variable overhead 14000 21000 28000 28000 35000

Contribution -7000 -80000 -180000 -182000 -320000

Less Fixed cost

Fixed manufacturing 80000 80000 80000 80000 80000

Loss -87000 -160000 -260000 -262000 -400000

SP 40

Units produced 8000

Particular Year1 Year2 Year3 Year4 Year5

Direct Material 8 9 11 13 15

Direct labor 5 5 6 7 7

Variable Overhead 2 3 4 4 5

variable selling 3 4 5 6 7

Fixed manufacturing 10 10 10 10 10

Total production cost 28 31 36 40 44

Particulars 2013 2014 2015 2016 2017

Cost of revenue $42,913

$44,47

5

$60,86

8 $58,276

$55,66

9

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

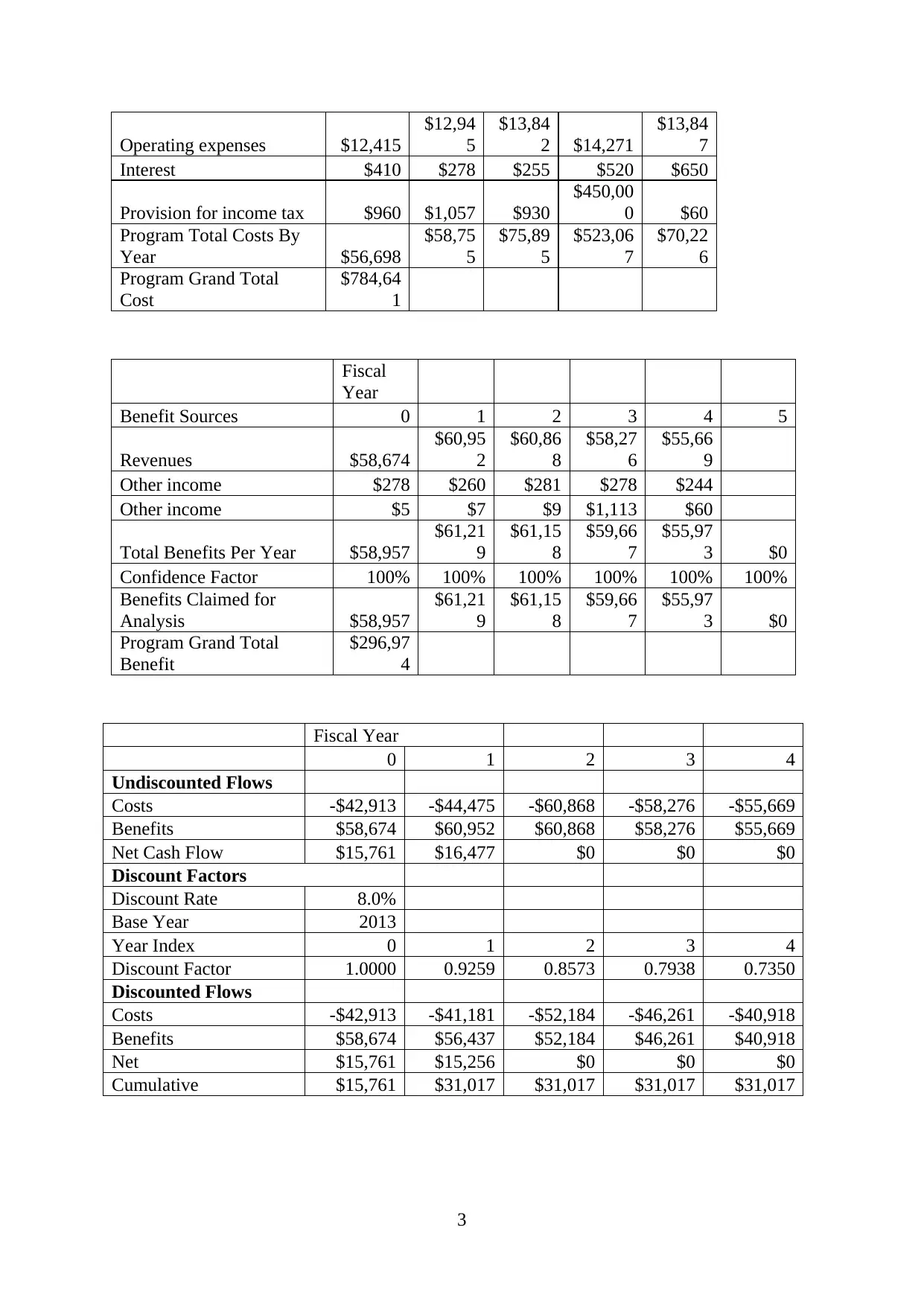

Operating expenses $12,415

$12,94

5

$13,84

2 $14,271

$13,84

7

Interest $410 $278 $255 $520 $650

Provision for income tax $960 $1,057 $930

$450,00

0 $60

Program Total Costs By

Year $56,698

$58,75

5

$75,89

5

$523,06

7

$70,22

6

Program Grand Total

Cost

$784,64

1

Fiscal

Year

Benefit Sources 0 1 2 3 4 5

Revenues $58,674

$60,95

2

$60,86

8

$58,27

6

$55,66

9

Other income $278 $260 $281 $278 $244

Other income $5 $7 $9 $1,113 $60

Total Benefits Per Year $58,957

$61,21

9

$61,15

8

$59,66

7

$55,97

3 $0

Confidence Factor 100% 100% 100% 100% 100% 100%

Benefits Claimed for

Analysis $58,957

$61,21

9

$61,15

8

$59,66

7

$55,97

3 $0

Program Grand Total

Benefit

$296,97

4

Fiscal Year

0 1 2 3 4

Undiscounted Flows

Costs -$42,913 -$44,475 -$60,868 -$58,276 -$55,669

Benefits $58,674 $60,952 $60,868 $58,276 $55,669

Net Cash Flow $15,761 $16,477 $0 $0 $0

Discount Factors

Discount Rate 8.0%

Base Year 2013

Year Index 0 1 2 3 4

Discount Factor 1.0000 0.9259 0.8573 0.7938 0.7350

Discounted Flows

Costs -$42,913 -$41,181 -$52,184 -$46,261 -$40,918

Benefits $58,674 $56,437 $52,184 $46,261 $40,918

Net $15,761 $15,256 $0 $0 $0

Cumulative $15,761 $31,017 $31,017 $31,017 $31,017

3

$12,94

5

$13,84

2 $14,271

$13,84

7

Interest $410 $278 $255 $520 $650

Provision for income tax $960 $1,057 $930

$450,00

0 $60

Program Total Costs By

Year $56,698

$58,75

5

$75,89

5

$523,06

7

$70,22

6

Program Grand Total

Cost

$784,64

1

Fiscal

Year

Benefit Sources 0 1 2 3 4 5

Revenues $58,674

$60,95

2

$60,86

8

$58,27

6

$55,66

9

Other income $278 $260 $281 $278 $244

Other income $5 $7 $9 $1,113 $60

Total Benefits Per Year $58,957

$61,21

9

$61,15

8

$59,66

7

$55,97

3 $0

Confidence Factor 100% 100% 100% 100% 100% 100%

Benefits Claimed for

Analysis $58,957

$61,21

9

$61,15

8

$59,66

7

$55,97

3 $0

Program Grand Total

Benefit

$296,97

4

Fiscal Year

0 1 2 3 4

Undiscounted Flows

Costs -$42,913 -$44,475 -$60,868 -$58,276 -$55,669

Benefits $58,674 $60,952 $60,868 $58,276 $55,669

Net Cash Flow $15,761 $16,477 $0 $0 $0

Discount Factors

Discount Rate 8.0%

Base Year 2013

Year Index 0 1 2 3 4

Discount Factor 1.0000 0.9259 0.8573 0.7938 0.7350

Discounted Flows

Costs -$42,913 -$41,181 -$52,184 -$46,261 -$40,918

Benefits $58,674 $56,437 $52,184 $46,261 $40,918

Net $15,761 $15,256 $0 $0 $0

Cumulative $15,761 $31,017 $31,017 $31,017 $31,017

3

Using different methods mentioned above, costs are ascertained by an entity by

evaluating the financial performance of an entity (Wong and et. al., 2017). Different kinds of

costs are evaluated by the Woolworth Ltd to ensure its survival in the external business

environment. Cost accountants will perform costs benefit analysis to determine the position f

the firm in the external environment as external market competition get eliminated by the

business by utilizing all its strengths and power.

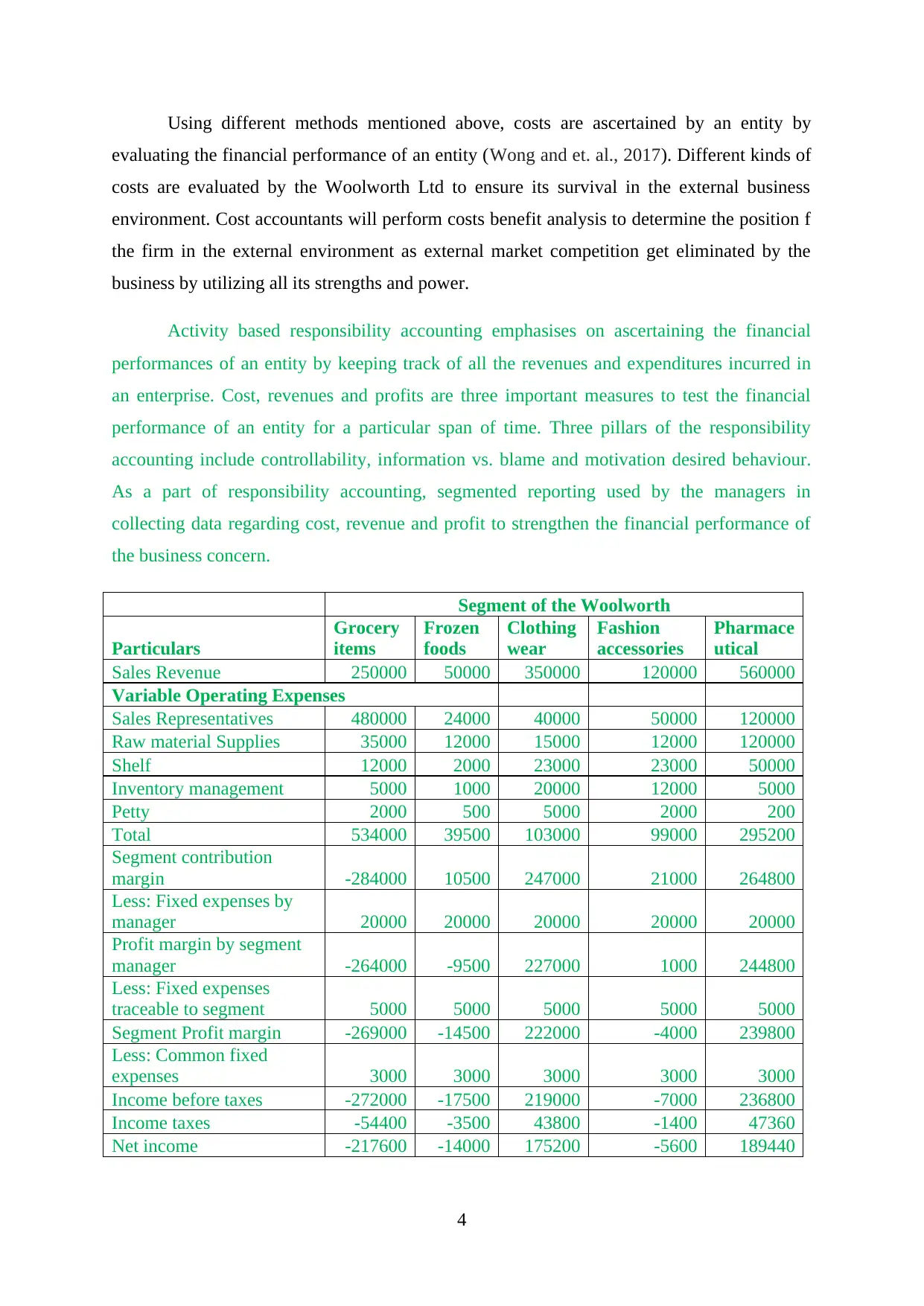

Activity based responsibility accounting emphasises on ascertaining the financial

performances of an entity by keeping track of all the revenues and expenditures incurred in

an enterprise. Cost, revenues and profits are three important measures to test the financial

performance of an entity for a particular span of time. Three pillars of the responsibility

accounting include controllability, information vs. blame and motivation desired behaviour.

As a part of responsibility accounting, segmented reporting used by the managers in

collecting data regarding cost, revenue and profit to strengthen the financial performance of

the business concern.

Segment of the Woolworth

Particulars

Grocery

items

Frozen

foods

Clothing

wear

Fashion

accessories

Pharmace

utical

Sales Revenue 250000 50000 350000 120000 560000

Variable Operating Expenses

Sales Representatives 480000 24000 40000 50000 120000

Raw material Supplies 35000 12000 15000 12000 120000

Shelf 12000 2000 23000 23000 50000

Inventory management 5000 1000 20000 12000 5000

Petty 2000 500 5000 2000 200

Total 534000 39500 103000 99000 295200

Segment contribution

margin -284000 10500 247000 21000 264800

Less: Fixed expenses by

manager 20000 20000 20000 20000 20000

Profit margin by segment

manager -264000 -9500 227000 1000 244800

Less: Fixed expenses

traceable to segment 5000 5000 5000 5000 5000

Segment Profit margin -269000 -14500 222000 -4000 239800

Less: Common fixed

expenses 3000 3000 3000 3000 3000

Income before taxes -272000 -17500 219000 -7000 236800

Income taxes -54400 -3500 43800 -1400 47360

Net income -217600 -14000 175200 -5600 189440

4

evaluating the financial performance of an entity (Wong and et. al., 2017). Different kinds of

costs are evaluated by the Woolworth Ltd to ensure its survival in the external business

environment. Cost accountants will perform costs benefit analysis to determine the position f

the firm in the external environment as external market competition get eliminated by the

business by utilizing all its strengths and power.

Activity based responsibility accounting emphasises on ascertaining the financial

performances of an entity by keeping track of all the revenues and expenditures incurred in

an enterprise. Cost, revenues and profits are three important measures to test the financial

performance of an entity for a particular span of time. Three pillars of the responsibility

accounting include controllability, information vs. blame and motivation desired behaviour.

As a part of responsibility accounting, segmented reporting used by the managers in

collecting data regarding cost, revenue and profit to strengthen the financial performance of

the business concern.

Segment of the Woolworth

Particulars

Grocery

items

Frozen

foods

Clothing

wear

Fashion

accessories

Pharmace

utical

Sales Revenue 250000 50000 350000 120000 560000

Variable Operating Expenses

Sales Representatives 480000 24000 40000 50000 120000

Raw material Supplies 35000 12000 15000 12000 120000

Shelf 12000 2000 23000 23000 50000

Inventory management 5000 1000 20000 12000 5000

Petty 2000 500 5000 2000 200

Total 534000 39500 103000 99000 295200

Segment contribution

margin -284000 10500 247000 21000 264800

Less: Fixed expenses by

manager 20000 20000 20000 20000 20000

Profit margin by segment

manager -264000 -9500 227000 1000 244800

Less: Fixed expenses

traceable to segment 5000 5000 5000 5000 5000

Segment Profit margin -269000 -14500 222000 -4000 239800

Less: Common fixed

expenses 3000 3000 3000 3000 3000

Income before taxes -272000 -17500 219000 -7000 236800

Income taxes -54400 -3500 43800 -1400 47360

Net income -217600 -14000 175200 -5600 189440

4

Balance score card is an important tool used by an enterprise in evaluating the

performance of the firm by stressing on various aspects. This approach helps in analyzing the

performance of the business overall particular span of time as providing quality oriented

services to the customers is important for the business. It helps in analyzing financial as well

as non-financial performance of the firm in the external business environment. Financial

measures used by the firm to compare the current performance with the past results generated

by the firm in an enterprise. This technique focuses on identifying errors in financial as well

as non-monetary areas as these areas play an integral role in the success of the business

within a particular span of time. An entity uses balance scorecard to identify all the unique

traits and skills of the business concern to ensure longer survival of the enterprise. Future of

the firm depends on the accomplishment of various goals and the objectives within a shorter

span of time. Two important indicators used in this approach helps in achieving the desired

market aims and targets within a shorter span of time. Cost minimised by the fir to enhance

the quality of the services delivered by the entity in lesser time. Cost, quality and time are the

three pillars used as weapon against the competitors of the business in capturing higher

market share in the external entity.

Lead and lag indicators used as important tool in creating the balance scorecard by

considering all positive and negative aspects in increasing the productivity of the firm against

all its rivals operated in the similar industry.

5

performance of the firm by stressing on various aspects. This approach helps in analyzing the

performance of the business overall particular span of time as providing quality oriented

services to the customers is important for the business. It helps in analyzing financial as well

as non-financial performance of the firm in the external business environment. Financial

measures used by the firm to compare the current performance with the past results generated

by the firm in an enterprise. This technique focuses on identifying errors in financial as well

as non-monetary areas as these areas play an integral role in the success of the business

within a particular span of time. An entity uses balance scorecard to identify all the unique

traits and skills of the business concern to ensure longer survival of the enterprise. Future of

the firm depends on the accomplishment of various goals and the objectives within a shorter

span of time. Two important indicators used in this approach helps in achieving the desired

market aims and targets within a shorter span of time. Cost minimised by the fir to enhance

the quality of the services delivered by the entity in lesser time. Cost, quality and time are the

three pillars used as weapon against the competitors of the business in capturing higher

market share in the external entity.

Lead and lag indicators used as important tool in creating the balance scorecard by

considering all positive and negative aspects in increasing the productivity of the firm against

all its rivals operated in the similar industry.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

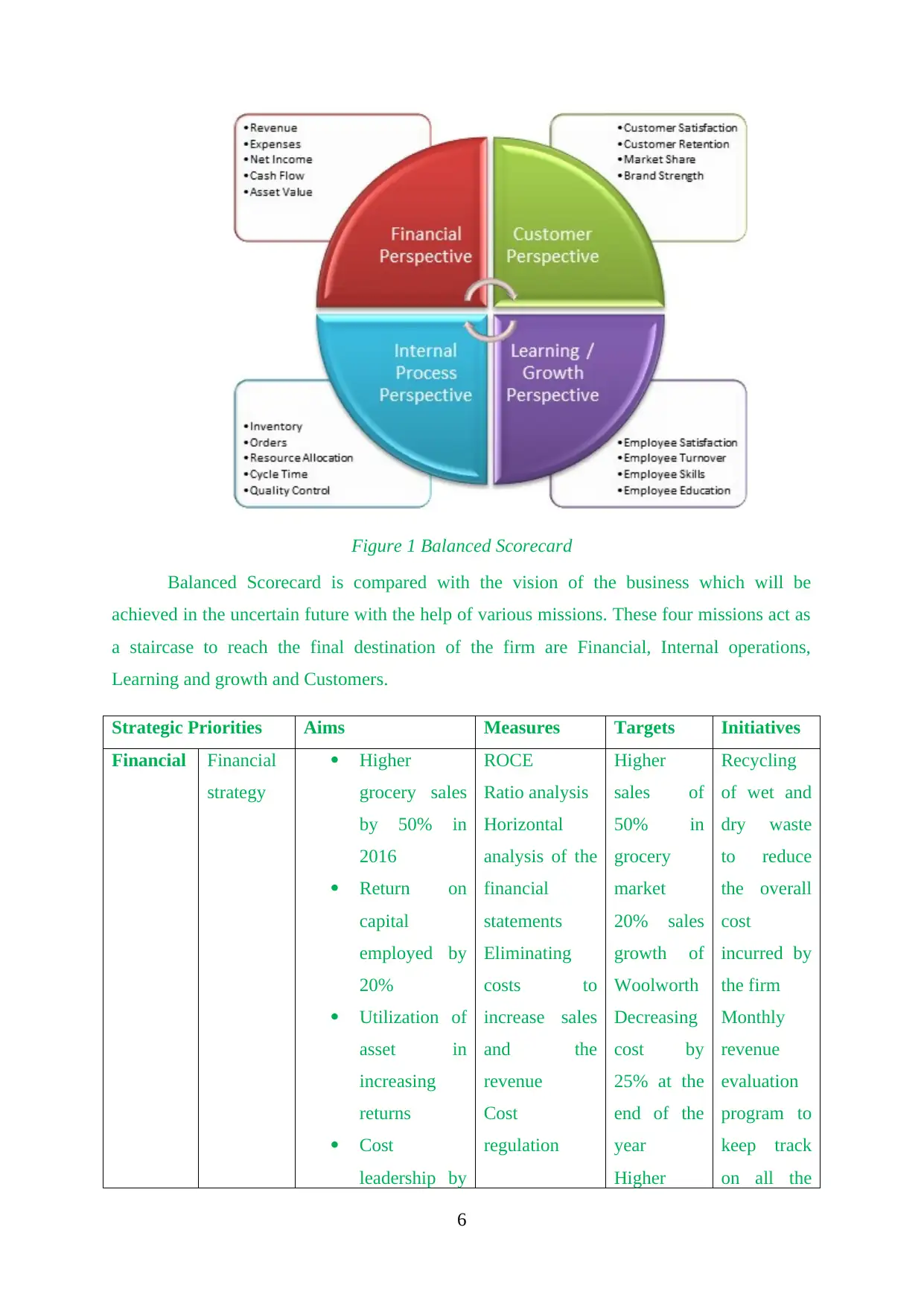

Figure 1 Balanced Scorecard

Balanced Scorecard is compared with the vision of the business which will be

achieved in the uncertain future with the help of various missions. These four missions act as

a staircase to reach the final destination of the firm are Financial, Internal operations,

Learning and growth and Customers.

Strategic Priorities Aims Measures Targets Initiatives

Financial Financial

strategy

Higher

grocery sales

by 50% in

2016

Return on

capital

employed by

20%

Utilization of

asset in

increasing

returns

Cost

leadership by

ROCE

Ratio analysis

Horizontal

analysis of the

financial

statements

Eliminating

costs to

increase sales

and the

revenue

Cost

regulation

Higher

sales of

50% in

grocery

market

20% sales

growth of

Woolworth

Decreasing

cost by

25% at the

end of the

year

Higher

Recycling

of wet and

dry waste

to reduce

the overall

cost

incurred by

the firm

Monthly

revenue

evaluation

program to

keep track

on all the

6

Balanced Scorecard is compared with the vision of the business which will be

achieved in the uncertain future with the help of various missions. These four missions act as

a staircase to reach the final destination of the firm are Financial, Internal operations,

Learning and growth and Customers.

Strategic Priorities Aims Measures Targets Initiatives

Financial Financial

strategy

Higher

grocery sales

by 50% in

2016

Return on

capital

employed by

20%

Utilization of

asset in

increasing

returns

Cost

leadership by

ROCE

Ratio analysis

Horizontal

analysis of the

financial

statements

Eliminating

costs to

increase sales

and the

revenue

Cost

regulation

Higher

sales of

50% in

grocery

market

20% sales

growth of

Woolworth

Decreasing

cost by

25% at the

end of the

year

Higher

Recycling

of wet and

dry waste

to reduce

the overall

cost

incurred by

the firm

Monthly

revenue

evaluation

program to

keep track

on all the

6

offering

products and

services in

lower prices

as compared

to all the

competitors.

Higher

Profitability

measures

Increasing

cash flow

Net profit

evaluation

Preparation of

costs

statements

Absorption

costing

statements

Segmental

reporting

current

ratio

earnings of

the business

Customer Customer

loyalty

Catching

the

attention

of the

customers

Extend the target

market of the firm

Using marketing

techniques to attract

large number of

customers

Questionnaires

distributed

among the

customers to

seek their

consent

Hoardings and

personal

selling used by

the firm

Attract 300

people by

the end of

quarter

Incur lesser

marketing

costs

Customer

loyalty club

Online

blogs

organised

by the firm

Learning

and

growth

Training

to

employees

Train all the regular

employees to fill the

potential vacancies

On the job

training

Internally

recruit

large

number of

employees

to higher

position

Promotion,

motivation,

awards and

recognition

program

Internal

operation

Logistics To provide free home

delivery all across the

world

Support of

voluntary

workers all

To deliver

500 people

all across

Giving

franchisee

to air lines

7

products and

services in

lower prices

as compared

to all the

competitors.

Higher

Profitability

measures

Increasing

cash flow

Net profit

evaluation

Preparation of

costs

statements

Absorption

costing

statements

Segmental

reporting

current

ratio

earnings of

the business

Customer Customer

loyalty

Catching

the

attention

of the

customers

Extend the target

market of the firm

Using marketing

techniques to attract

large number of

customers

Questionnaires

distributed

among the

customers to

seek their

consent

Hoardings and

personal

selling used by

the firm

Attract 300

people by

the end of

quarter

Incur lesser

marketing

costs

Customer

loyalty club

Online

blogs

organised

by the firm

Learning

and

growth

Training

to

employees

Train all the regular

employees to fill the

potential vacancies

On the job

training

Internally

recruit

large

number of

employees

to higher

position

Promotion,

motivation,

awards and

recognition

program

Internal

operation

Logistics To provide free home

delivery all across the

world

Support of

voluntary

workers all

To deliver

500 people

all across

Giving

franchisee

to air lines

7

across the

world

the globe

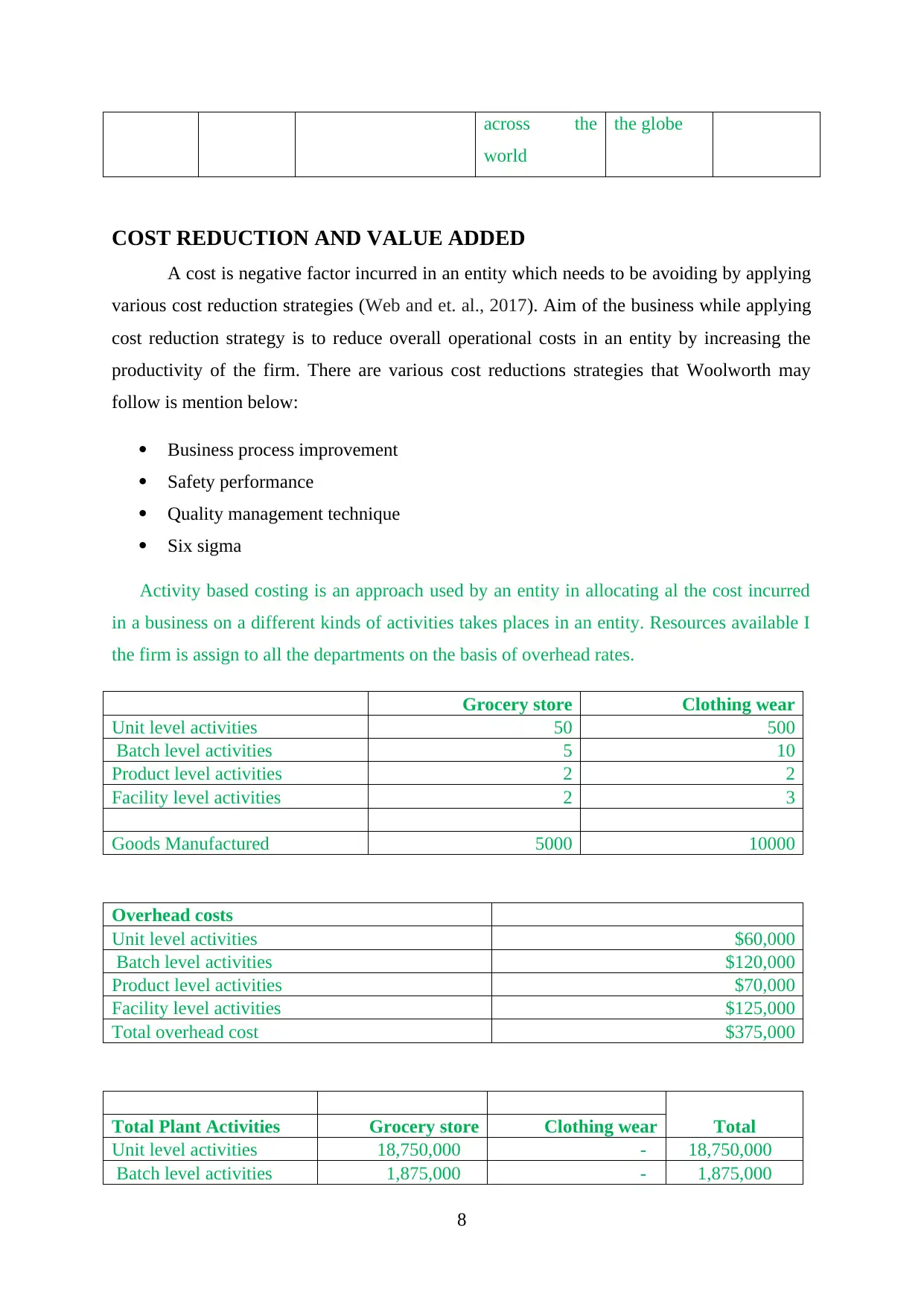

COST REDUCTION AND VALUE ADDED

A cost is negative factor incurred in an entity which needs to be avoiding by applying

various cost reduction strategies (Web and et. al., 2017). Aim of the business while applying

cost reduction strategy is to reduce overall operational costs in an entity by increasing the

productivity of the firm. There are various cost reductions strategies that Woolworth may

follow is mention below:

Business process improvement

Safety performance

Quality management technique

Six sigma

Activity based costing is an approach used by an entity in allocating al the cost incurred

in a business on a different kinds of activities takes places in an entity. Resources available I

the firm is assign to all the departments on the basis of overhead rates.

Grocery store Clothing wear

Unit level activities 50 500

Batch level activities 5 10

Product level activities 2 2

Facility level activities 2 3

Goods Manufactured 5000 10000

Overhead costs

Unit level activities $60,000

Batch level activities $120,000

Product level activities $70,000

Facility level activities $125,000

Total overhead cost $375,000

TotalTotal Plant Activities Grocery store Clothing wear

Unit level activities 18,750,000 - 18,750,000

Batch level activities 1,875,000 - 1,875,000

8

world

the globe

COST REDUCTION AND VALUE ADDED

A cost is negative factor incurred in an entity which needs to be avoiding by applying

various cost reduction strategies (Web and et. al., 2017). Aim of the business while applying

cost reduction strategy is to reduce overall operational costs in an entity by increasing the

productivity of the firm. There are various cost reductions strategies that Woolworth may

follow is mention below:

Business process improvement

Safety performance

Quality management technique

Six sigma

Activity based costing is an approach used by an entity in allocating al the cost incurred

in a business on a different kinds of activities takes places in an entity. Resources available I

the firm is assign to all the departments on the basis of overhead rates.

Grocery store Clothing wear

Unit level activities 50 500

Batch level activities 5 10

Product level activities 2 2

Facility level activities 2 3

Goods Manufactured 5000 10000

Overhead costs

Unit level activities $60,000

Batch level activities $120,000

Product level activities $70,000

Facility level activities $125,000

Total overhead cost $375,000

TotalTotal Plant Activities Grocery store Clothing wear

Unit level activities 18,750,000 - 18,750,000

Batch level activities 1,875,000 - 1,875,000

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Product level activities 750,000 - 750,000

Facility level activities 750,000 - 750,000

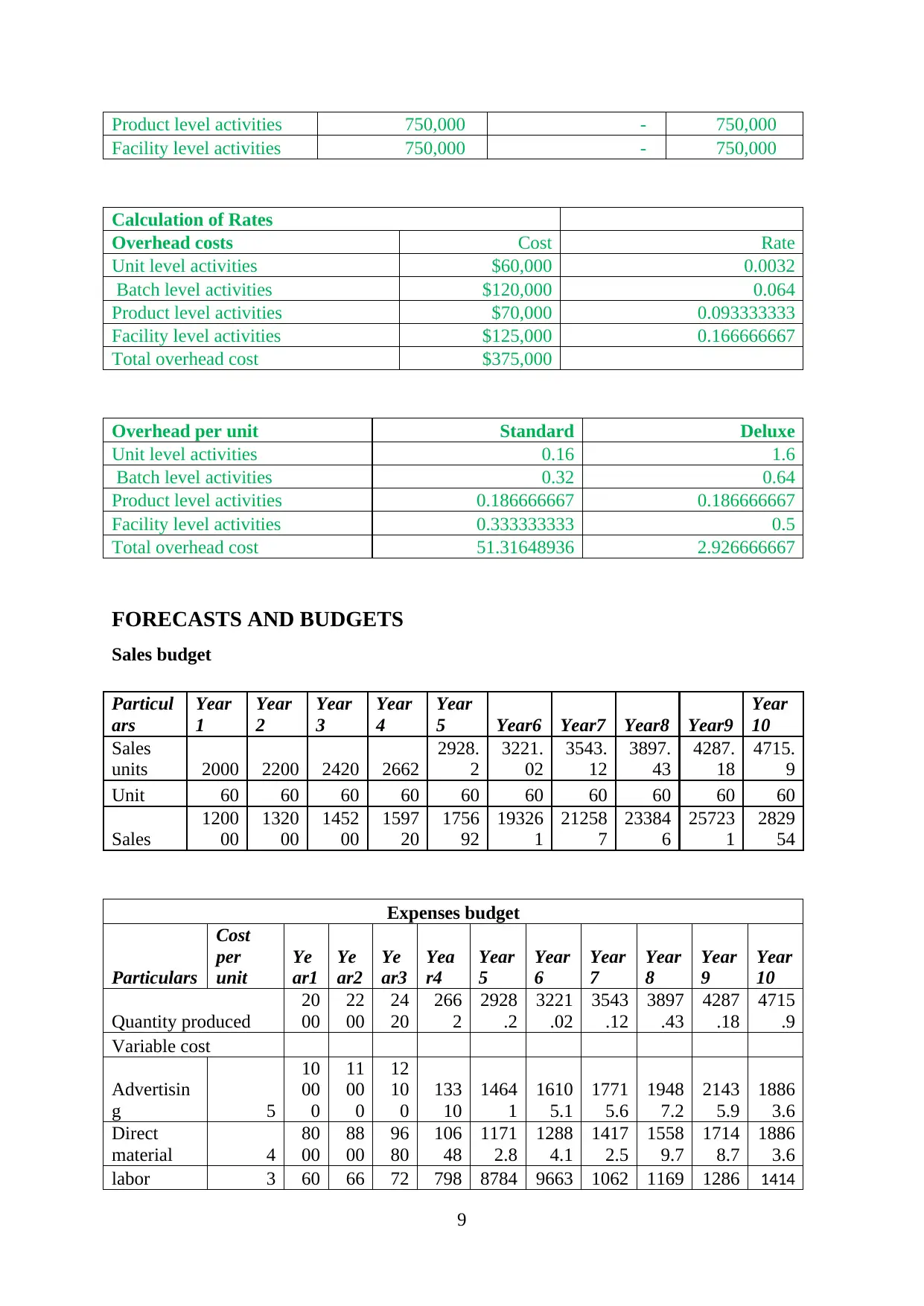

Calculation of Rates

Overhead costs Cost Rate

Unit level activities $60,000 0.0032

Batch level activities $120,000 0.064

Product level activities $70,000 0.093333333

Facility level activities $125,000 0.166666667

Total overhead cost $375,000

Overhead per unit Standard Deluxe

Unit level activities 0.16 1.6

Batch level activities 0.32 0.64

Product level activities 0.186666667 0.186666667

Facility level activities 0.333333333 0.5

Total overhead cost 51.31648936 2.926666667

FORECASTS AND BUDGETS

Sales budget

Particul

ars

Year

1

Year

2

Year

3

Year

4

Year

5 Year6 Year7 Year8 Year9

Year

10

Sales

units 2000 2200 2420 2662

2928.

2

3221.

02

3543.

12

3897.

43

4287.

18

4715.

9

Unit 60 60 60 60 60 60 60 60 60 60

Sales

1200

00

1320

00

1452

00

1597

20

1756

92

19326

1

21258

7

23384

6

25723

1

2829

54

Expenses budget

Particulars

Cost

per

unit

Ye

ar1

Ye

ar2

Ye

ar3

Yea

r4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Quantity produced

20

00

22

00

24

20

266

2

2928

.2

3221

.02

3543

.12

3897

.43

4287

.18

4715

.9

Variable cost

Advertisin

g 5

10

00

0

11

00

0

12

10

0

133

10

1464

1

1610

5.1

1771

5.6

1948

7.2

2143

5.9

1886

3.6

Direct

material 4

80

00

88

00

96

80

106

48

1171

2.8

1288

4.1

1417

2.5

1558

9.7

1714

8.7

1886

3.6

labor 3 60 66 72 798 8784 9663 1062 1169 1286 1414

9

Facility level activities 750,000 - 750,000

Calculation of Rates

Overhead costs Cost Rate

Unit level activities $60,000 0.0032

Batch level activities $120,000 0.064

Product level activities $70,000 0.093333333

Facility level activities $125,000 0.166666667

Total overhead cost $375,000

Overhead per unit Standard Deluxe

Unit level activities 0.16 1.6

Batch level activities 0.32 0.64

Product level activities 0.186666667 0.186666667

Facility level activities 0.333333333 0.5

Total overhead cost 51.31648936 2.926666667

FORECASTS AND BUDGETS

Sales budget

Particul

ars

Year

1

Year

2

Year

3

Year

4

Year

5 Year6 Year7 Year8 Year9

Year

10

Sales

units 2000 2200 2420 2662

2928.

2

3221.

02

3543.

12

3897.

43

4287.

18

4715.

9

Unit 60 60 60 60 60 60 60 60 60 60

Sales

1200

00

1320

00

1452

00

1597

20

1756

92

19326

1

21258

7

23384

6

25723

1

2829

54

Expenses budget

Particulars

Cost

per

unit

Ye

ar1

Ye

ar2

Ye

ar3

Yea

r4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Quantity produced

20

00

22

00

24

20

266

2

2928

.2

3221

.02

3543

.12

3897

.43

4287

.18

4715

.9

Variable cost

Advertisin

g 5

10

00

0

11

00

0

12

10

0

133

10

1464

1

1610

5.1

1771

5.6

1948

7.2

2143

5.9

1886

3.6

Direct

material 4

80

00

88

00

96

80

106

48

1171

2.8

1288

4.1

1417

2.5

1558

9.7

1714

8.7

1886

3.6

labor 3 60 66 72 798 8784 9663 1062 1169 1286 1414

9

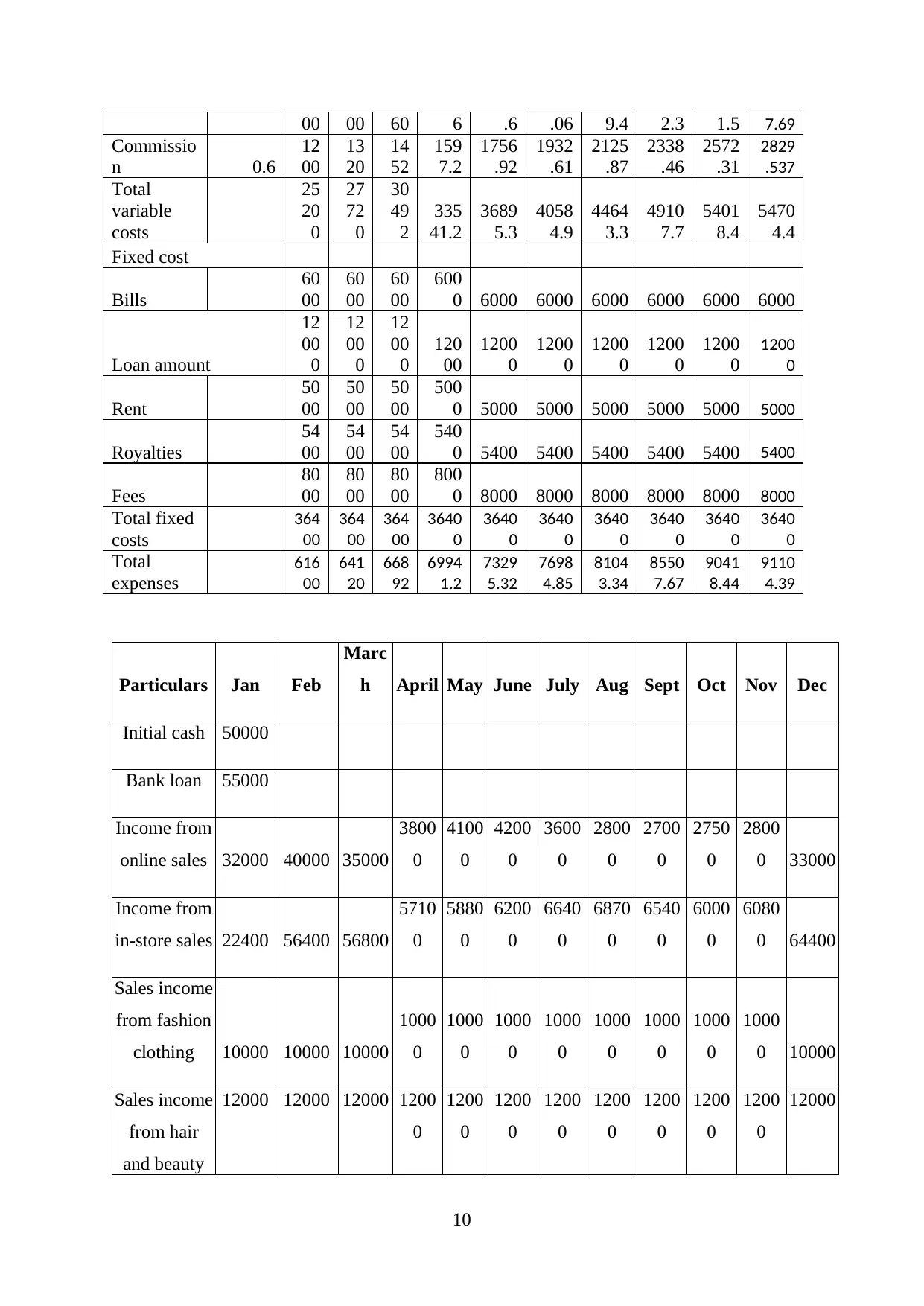

00 00 60 6 .6 .06 9.4 2.3 1.5 7.69

Commissio

n 0.6

12

00

13

20

14

52

159

7.2

1756

.92

1932

.61

2125

.87

2338

.46

2572

.31

2829

.537

Total

variable

costs

25

20

0

27

72

0

30

49

2

335

41.2

3689

5.3

4058

4.9

4464

3.3

4910

7.7

5401

8.4

5470

4.4

Fixed cost

Bills

60

00

60

00

60

00

600

0 6000 6000 6000 6000 6000 6000

Loan amount

12

00

0

12

00

0

12

00

0

120

00

1200

0

1200

0

1200

0

1200

0

1200

0

1200

0

Rent

50

00

50

00

50

00

500

0 5000 5000 5000 5000 5000 5000

Royalties

54

00

54

00

54

00

540

0 5400 5400 5400 5400 5400 5400

Fees

80

00

80

00

80

00

800

0 8000 8000 8000 8000 8000 8000

Total fixed

costs

364

00

364

00

364

00

3640

0

3640

0

3640

0

3640

0

3640

0

3640

0

3640

0

Total

expenses

616

00

641

20

668

92

6994

1.2

7329

5.32

7698

4.85

8104

3.34

8550

7.67

9041

8.44

9110

4.39

Particulars Jan Feb

Marc

h April May June July Aug Sept Oct Nov Dec

Initial cash 50000

Bank loan 55000

Income from

online sales 32000 40000 35000

3800

0

4100

0

4200

0

3600

0

2800

0

2700

0

2750

0

2800

0 33000

Income from

in-store sales 22400 56400 56800

5710

0

5880

0

6200

0

6640

0

6870

0

6540

0

6000

0

6080

0 64400

Sales income

from fashion

clothing 10000 10000 10000

1000

0

1000

0

1000

0

1000

0

1000

0

1000

0

1000

0

1000

0 10000

Sales income

from hair

and beauty

12000 12000 12000 1200

0

1200

0

1200

0

1200

0

1200

0

1200

0

1200

0

1200

0

12000

10

Commissio

n 0.6

12

00

13

20

14

52

159

7.2

1756

.92

1932

.61

2125

.87

2338

.46

2572

.31

2829

.537

Total

variable

costs

25

20

0

27

72

0

30

49

2

335

41.2

3689

5.3

4058

4.9

4464

3.3

4910

7.7

5401

8.4

5470

4.4

Fixed cost

Bills

60

00

60

00

60

00

600

0 6000 6000 6000 6000 6000 6000

Loan amount

12

00

0

12

00

0

12

00

0

120

00

1200

0

1200

0

1200

0

1200

0

1200

0

1200

0

Rent

50

00

50

00

50

00

500

0 5000 5000 5000 5000 5000 5000

Royalties

54

00

54

00

54

00

540

0 5400 5400 5400 5400 5400 5400

Fees

80

00

80

00

80

00

800

0 8000 8000 8000 8000 8000 8000

Total fixed

costs

364

00

364

00

364

00

3640

0

3640

0

3640

0

3640

0

3640

0

3640

0

3640

0

Total

expenses

616

00

641

20

668

92

6994

1.2

7329

5.32

7698

4.85

8104

3.34

8550

7.67

9041

8.44

9110

4.39

Particulars Jan Feb

Marc

h April May June July Aug Sept Oct Nov Dec

Initial cash 50000

Bank loan 55000

Income from

online sales 32000 40000 35000

3800

0

4100

0

4200

0

3600

0

2800

0

2700

0

2750

0

2800

0 33000

Income from

in-store sales 22400 56400 56800

5710

0

5880

0

6200

0

6640

0

6870

0

6540

0

6000

0

6080

0 64400

Sales income

from fashion

clothing 10000 10000 10000

1000

0

1000

0

1000

0

1000

0

1000

0

1000

0

1000

0

1000

0 10000

Sales income

from hair

and beauty

12000 12000 12000 1200

0

1200

0

1200

0

1200

0

1200

0

1200

0

1200

0

1200

0

12000

10

products

Receipts

from

disposal of

old store

building

3000

00

Total interest

receivables

3000

0 30000

Total cash

income

18140

0 118400

11380

0

1171

00

1218

00

4560

00

1244

00

1187

00

1144

00

1095

00

1108

00

14940

0

Cash

disbursement

Store and

warehouse

building

lease rental

14400

0

Purchase of

office and

fire

Equipment 80000

Purchase of

delivery van

and cars

15000

0

Shelves and

store

furniture 50000

Purchase of

fork lift for

70000

11

Receipts

from

disposal of

old store

building

3000

00

Total interest

receivables

3000

0 30000

Total cash

income

18140

0 118400

11380

0

1171

00

1218

00

4560

00

1244

00

1187

00

1144

00

1095

00

1108

00

14940

0

Cash

disbursement

Store and

warehouse

building

lease rental

14400

0

Purchase of

office and

fire

Equipment 80000

Purchase of

delivery van

and cars

15000

0

Shelves and

store

furniture 50000

Purchase of

fork lift for

70000

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

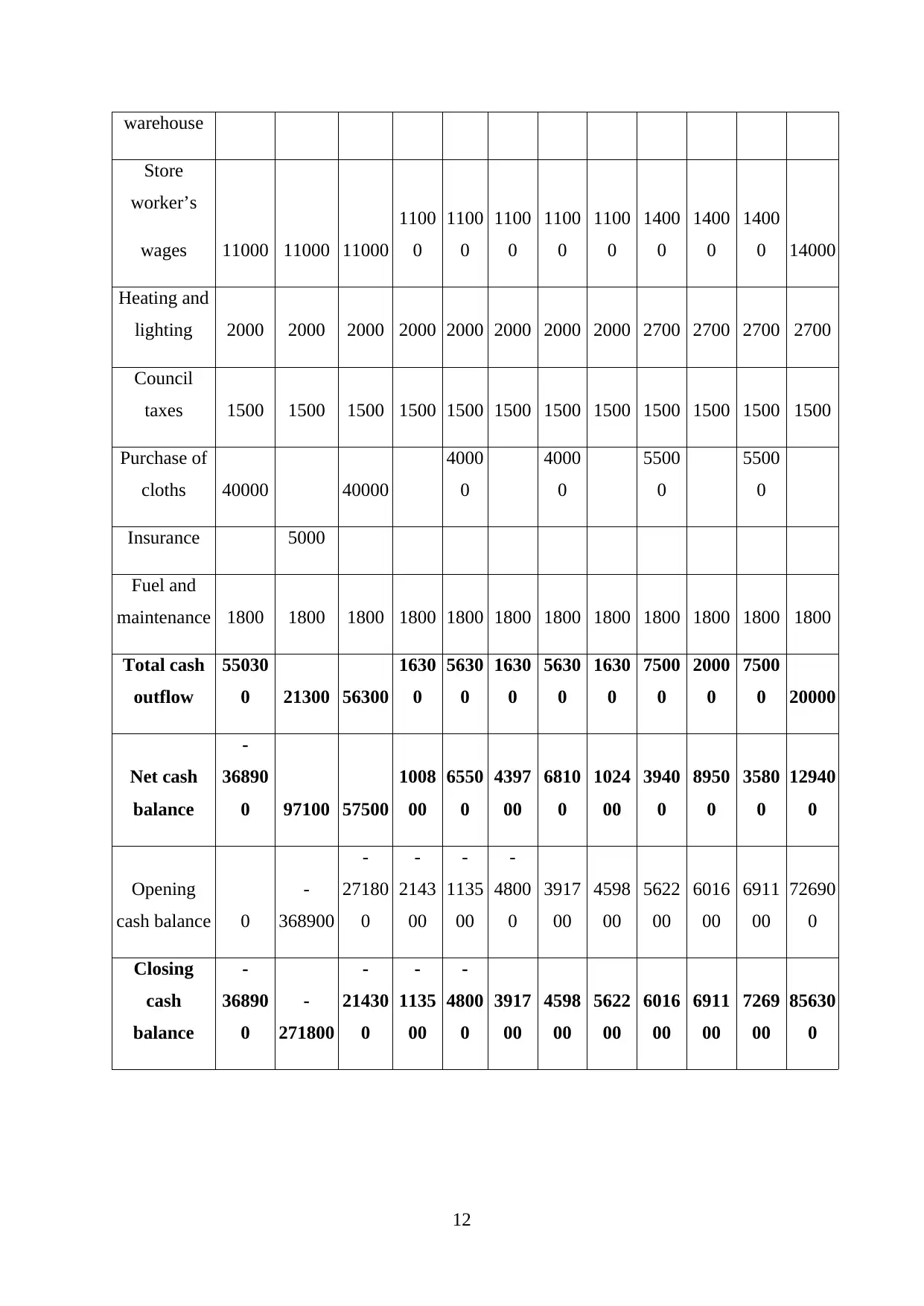

warehouse

Store

worker’s

wages 11000 11000 11000

1100

0

1100

0

1100

0

1100

0

1100

0

1400

0

1400

0

1400

0 14000

Heating and

lighting 2000 2000 2000 2000 2000 2000 2000 2000 2700 2700 2700 2700

Council

taxes 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500

Purchase of

cloths 40000 40000

4000

0

4000

0

5500

0

5500

0

Insurance 5000

Fuel and

maintenance 1800 1800 1800 1800 1800 1800 1800 1800 1800 1800 1800 1800

Total cash

outflow

55030

0 21300 56300

1630

0

5630

0

1630

0

5630

0

1630

0

7500

0

2000

0

7500

0 20000

Net cash

balance

-

36890

0 97100 57500

1008

00

6550

0

4397

00

6810

0

1024

00

3940

0

8950

0

3580

0

12940

0

Opening

cash balance 0

-

368900

-

27180

0

-

2143

00

-

1135

00

-

4800

0

3917

00

4598

00

5622

00

6016

00

6911

00

72690

0

Closing

cash

balance

-

36890

0

-

271800

-

21430

0

-

1135

00

-

4800

0

3917

00

4598

00

5622

00

6016

00

6911

00

7269

00

85630

0

12

Store

worker’s

wages 11000 11000 11000

1100

0

1100

0

1100

0

1100

0

1100

0

1400

0

1400

0

1400

0 14000

Heating and

lighting 2000 2000 2000 2000 2000 2000 2000 2000 2700 2700 2700 2700

Council

taxes 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500 1500

Purchase of

cloths 40000 40000

4000

0

4000

0

5500

0

5500

0

Insurance 5000

Fuel and

maintenance 1800 1800 1800 1800 1800 1800 1800 1800 1800 1800 1800 1800

Total cash

outflow

55030

0 21300 56300

1630

0

5630

0

1630

0

5630

0

1630

0

7500

0

2000

0

7500

0 20000

Net cash

balance

-

36890

0 97100 57500

1008

00

6550

0

4397

00

6810

0

1024

00

3940

0

8950

0

3580

0

12940

0

Opening

cash balance 0

-

368900

-

27180

0

-

2143

00

-

1135

00

-

4800

0

3917

00

4598

00

5622

00

6016

00

6911

00

72690

0

Closing

cash

balance

-

36890

0

-

271800

-

21430

0

-

1135

00

-

4800

0

3917

00

4598

00

5622

00

6016

00

6911

00

7269

00

85630

0

12

MONITOR PERFORMANCE

Wool worth Ltd can use performance budgeting in keeping record of all the

transactions takes places in an entity. This budget helps an entity in forecasting future

performance of the business by utilizing current facts and figures. Motive of this budgeting is

to manage the financial resources held in an entity for long term purpose by considering all

the important criteria’s (Mullie, Schwartzman, Zwerling and N’Diaye, 2017). Performance

budgeting helps in building relationships between funding level and expected outcomes

generated by the business concern. Current budgeting approach has categorized into two

categories such as private entity and public entity. Performance budgeting is based on three

different elements such as final outcome, strategy and activity. Goals and the objectives

crafted by the firm used as various criteria’s in improving the performance of the firm in

achieving all the desired final outcomes within a given span of time (Azizoddin and et.al.,

2017). Performance budgeting is suitable for private entities as quality of the services

delivered by an entity depends on the overall performance of an entity. Positive as well as

negative performance of the firm. Performance budgeting is based on financial as well as

non-financial metric such as activity based costing in which various costs incurred in an

entity in segregating all the costs among various departments takes places in an entity.

Planning and controlling measures used by the firm to keep track on all the expenses incurred

in an entity.

CONCLUSION

It can be summarized from the above study that Sales budget and expense budget

comes under forecast budgeting in predicting the performance of the firm. Performance

budgeting is used by the business concern in monitoring the performance of an entity by

considering all the factors of an entity. Current report targets positive aspects of the business

concern by spotting all kinds of costs incurred in a firm to eliminate same by following

various tools and techniques.

13

Wool worth Ltd can use performance budgeting in keeping record of all the

transactions takes places in an entity. This budget helps an entity in forecasting future

performance of the business by utilizing current facts and figures. Motive of this budgeting is

to manage the financial resources held in an entity for long term purpose by considering all

the important criteria’s (Mullie, Schwartzman, Zwerling and N’Diaye, 2017). Performance

budgeting helps in building relationships between funding level and expected outcomes

generated by the business concern. Current budgeting approach has categorized into two

categories such as private entity and public entity. Performance budgeting is based on three

different elements such as final outcome, strategy and activity. Goals and the objectives

crafted by the firm used as various criteria’s in improving the performance of the firm in

achieving all the desired final outcomes within a given span of time (Azizoddin and et.al.,

2017). Performance budgeting is suitable for private entities as quality of the services

delivered by an entity depends on the overall performance of an entity. Positive as well as

negative performance of the firm. Performance budgeting is based on financial as well as

non-financial metric such as activity based costing in which various costs incurred in an

entity in segregating all the costs among various departments takes places in an entity.

Planning and controlling measures used by the firm to keep track on all the expenses incurred

in an entity.

CONCLUSION

It can be summarized from the above study that Sales budget and expense budget

comes under forecast budgeting in predicting the performance of the firm. Performance

budgeting is used by the business concern in monitoring the performance of an entity by

considering all the factors of an entity. Current report targets positive aspects of the business

concern by spotting all kinds of costs incurred in a firm to eliminate same by following

various tools and techniques.

13

REFERENCES

Azizoddin, D. R and et.al., 2017. A multi-group confirmatory factor analyses of the

LupusPRO between southern California and Filipino samples of patients with systemic

lupus erythematosus. Lupus, p.0961203316686706.

Conen, K.L., Matter-Walstra, K., Schädelin, S., Mariani, L. and Hess, V., 2017. Benefits and

costs of bevacizumab in recurrent glioblastoma: A quality adjusted survival and cost

analysis (EVALUATE).

Durojaiye, O. C., Bell Gorrod, H., Andrews, D., Ntziora, F. and Cartwright, K., 2017.

Clinical efficacy, cost-analysis and patient acceptability of outpatient parenteral antibiotic

therapy (OPAT): a decade of Sheffield (UK) OPAT service. International Journal of

Antimicrobial Agents.

Mullie, G. A., Schwartzman, K., Zwerling, A. and N’Diaye, D. S., 2017. Revisiting annual

screening for latent tuberculosis infection in healthcare workers: a cost-effectiveness

analysis. BMC medicine. 15(1). p.104.

Webb, M and et.al., 2017. Cost effectiveness of a government supported policy strategy to

decrease sodium intake: global analysis across 183 nations. Bmj. 356. p.i6699.

Winkler, J. K., 2017. Five and Ten: The Fabulous Life of FW Woolworth. Pickle Partners

Publishing.

Wong, C. K. H., and et.al., 2017. Traditional growing rod versus magnetically controlled

growing rod for treatment of early onset scoliosis: Cost analysis from implantation till

skeletal maturity.Journal of Orthopaedic Surgery. 25(2). p.2309499017705022.

Woolworth, D. S., 2017. Sound systems in reverberant spaces: Approaches in practice. The

Journal of the Acoustical Society of America. 141(5). pp.3996-3996.

14

Azizoddin, D. R and et.al., 2017. A multi-group confirmatory factor analyses of the

LupusPRO between southern California and Filipino samples of patients with systemic

lupus erythematosus. Lupus, p.0961203316686706.

Conen, K.L., Matter-Walstra, K., Schädelin, S., Mariani, L. and Hess, V., 2017. Benefits and

costs of bevacizumab in recurrent glioblastoma: A quality adjusted survival and cost

analysis (EVALUATE).

Durojaiye, O. C., Bell Gorrod, H., Andrews, D., Ntziora, F. and Cartwright, K., 2017.

Clinical efficacy, cost-analysis and patient acceptability of outpatient parenteral antibiotic

therapy (OPAT): a decade of Sheffield (UK) OPAT service. International Journal of

Antimicrobial Agents.

Mullie, G. A., Schwartzman, K., Zwerling, A. and N’Diaye, D. S., 2017. Revisiting annual

screening for latent tuberculosis infection in healthcare workers: a cost-effectiveness

analysis. BMC medicine. 15(1). p.104.

Webb, M and et.al., 2017. Cost effectiveness of a government supported policy strategy to

decrease sodium intake: global analysis across 183 nations. Bmj. 356. p.i6699.

Winkler, J. K., 2017. Five and Ten: The Fabulous Life of FW Woolworth. Pickle Partners

Publishing.

Wong, C. K. H., and et.al., 2017. Traditional growing rod versus magnetically controlled

growing rod for treatment of early onset scoliosis: Cost analysis from implantation till

skeletal maturity.Journal of Orthopaedic Surgery. 25(2). p.2309499017705022.

Woolworth, D. S., 2017. Sound systems in reverberant spaces: Approaches in practice. The

Journal of the Acoustical Society of America. 141(5). pp.3996-3996.

14

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.