ACCT6004 Management Accounting: Costing Concepts and Scenario Analysis

VerifiedAdded on 2023/06/09

|11

|1333

|423

Report

AI Summary

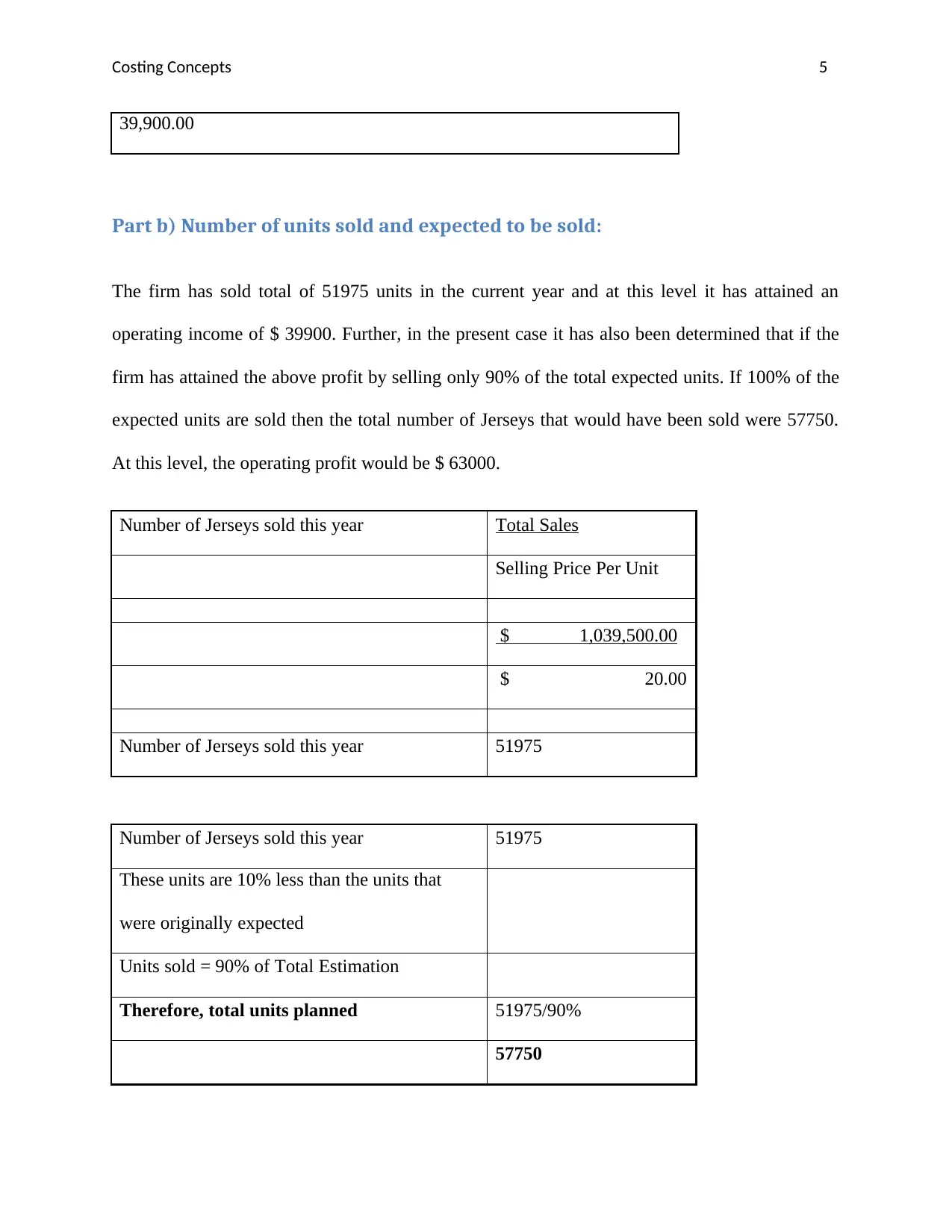

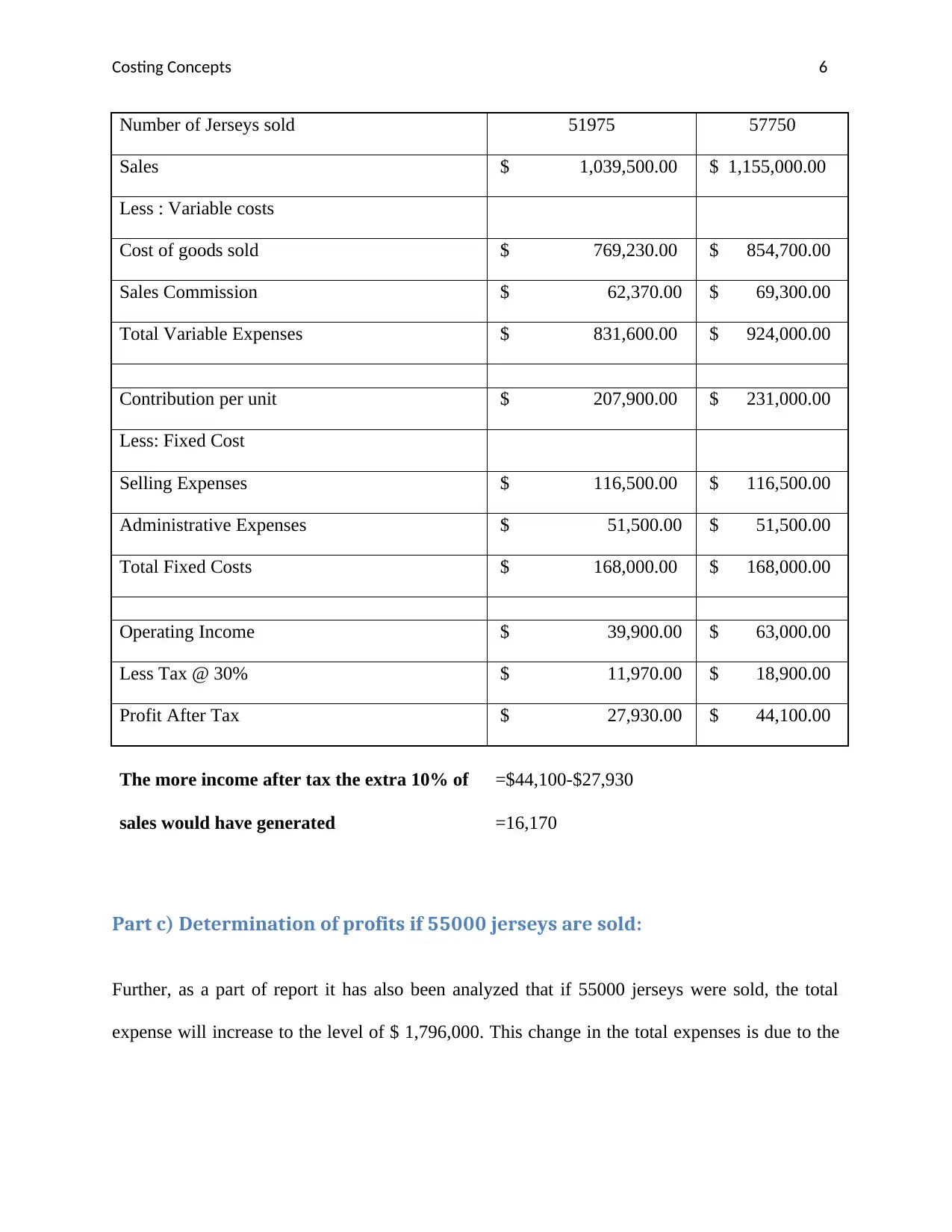

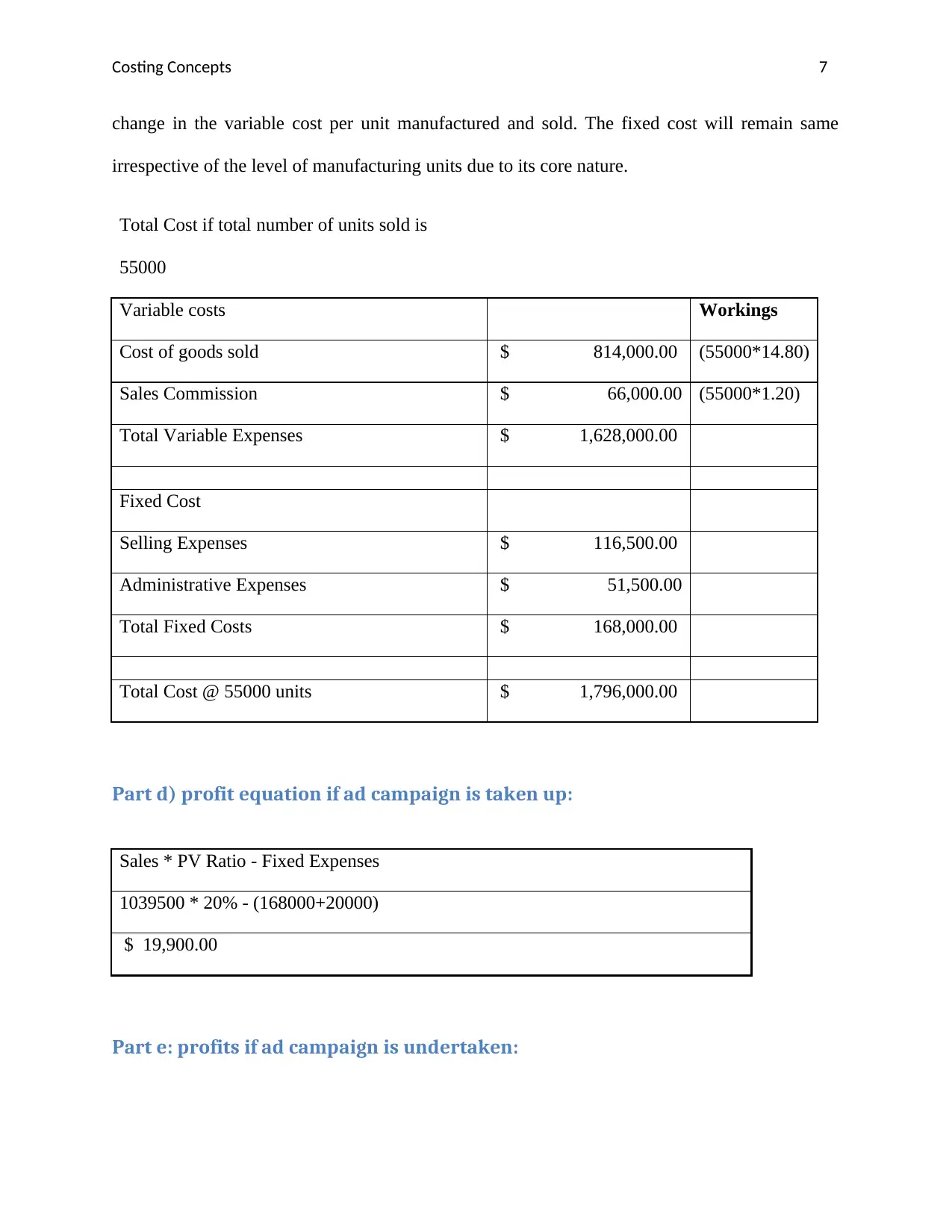

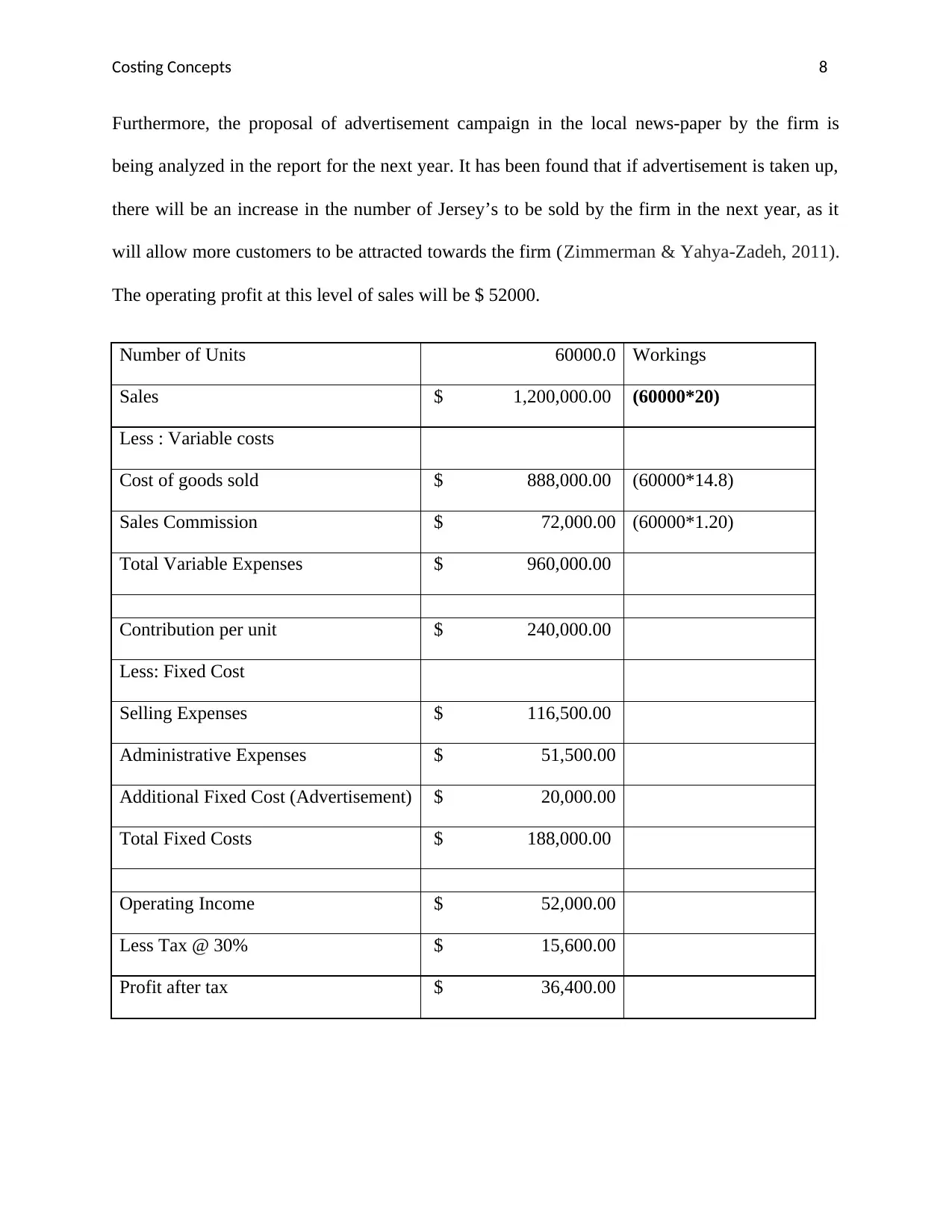

This report analyzes the costing concepts applied to the case of J&B Sports, a sports uniform manufacturer. It begins with an executive summary and introduction, then delves into the categorization of different costs, including variable, fixed, step, and mixed costs, within the business. The report then presents a scenario analysis, calculating operating profit, determining the number of units sold, and projecting profits under different scenarios, such as varying sales volumes and the implementation of an advertising campaign. The analysis includes detailed calculations and recommendations for the firm's financial strategies, concluding with a recommendation to undertake the advertising campaign. The report uses references from various accounting texts and journals to support its findings.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.