Analysis of Cost Reduction Techniques: Job and Activity-Based Costing

VerifiedAdded on 2021/02/19

|6

|950

|61

Homework Assignment

AI Summary

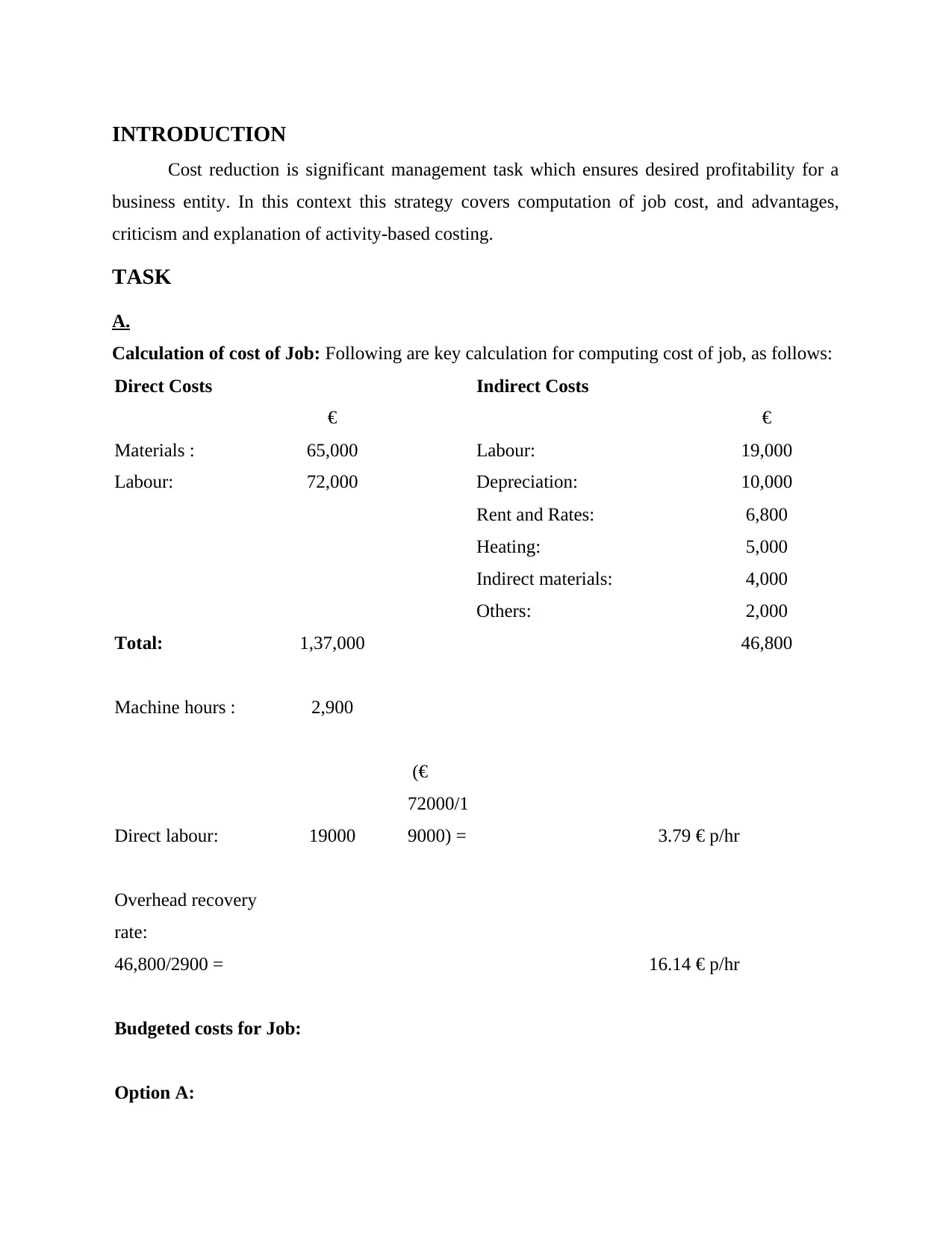

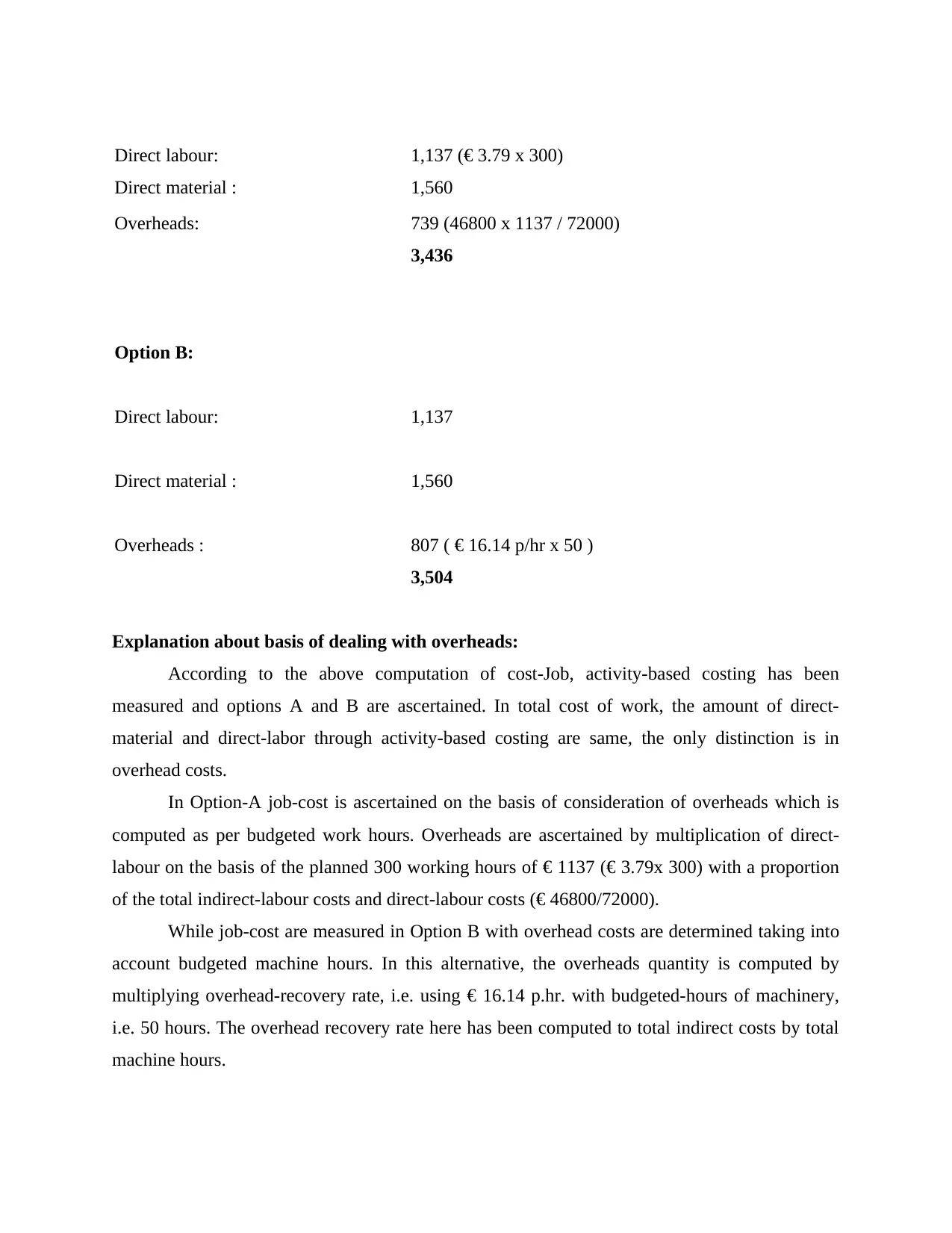

This assignment solution focuses on cost reduction strategies within a business context. It begins with the calculation of job costs, detailing direct and indirect costs, and presents two options for budgeting, considering direct labor and overheads. The solution then provides an in-depth explanation of activity-based costing (ABC), outlining its advantages, such as accurate costing and improved understanding of overheads, as well as its criticisms, including resource intensity and potential discrepancies with traditional costing methods. The document also includes calculations for job costing, showing the impact of different overhead allocation methods. Finally, the assignment concludes by emphasizing the importance of using various cost assessment methods, like job costing and ABC, to maintain operational accountability and achieve desired profitability within an enterprise.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.