Jackson Ltd.: Activity-Based Costing vs. Conventional Costing Report

VerifiedAdded on 2020/02/19

|9

|2275

|40

Report

AI Summary

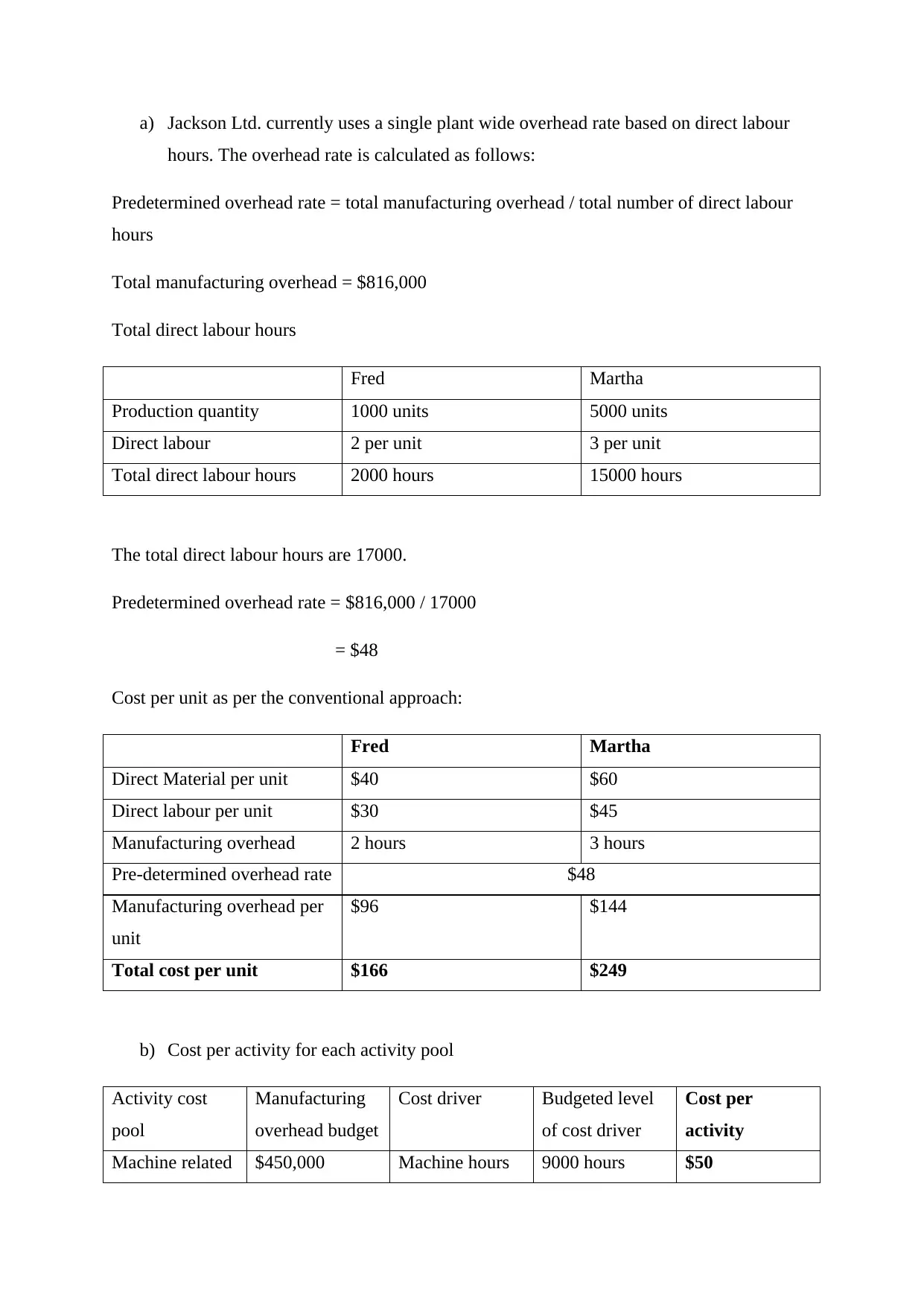

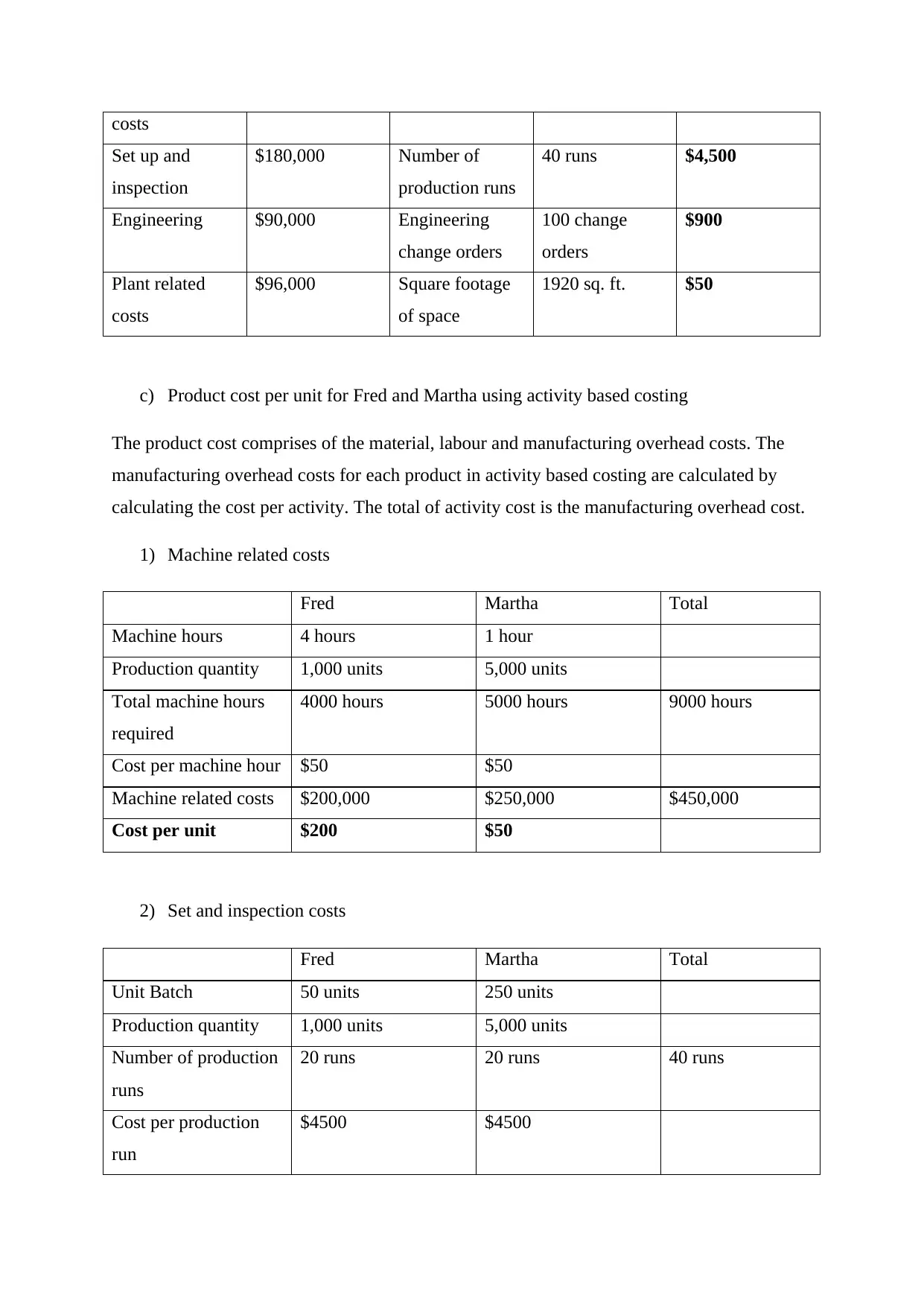

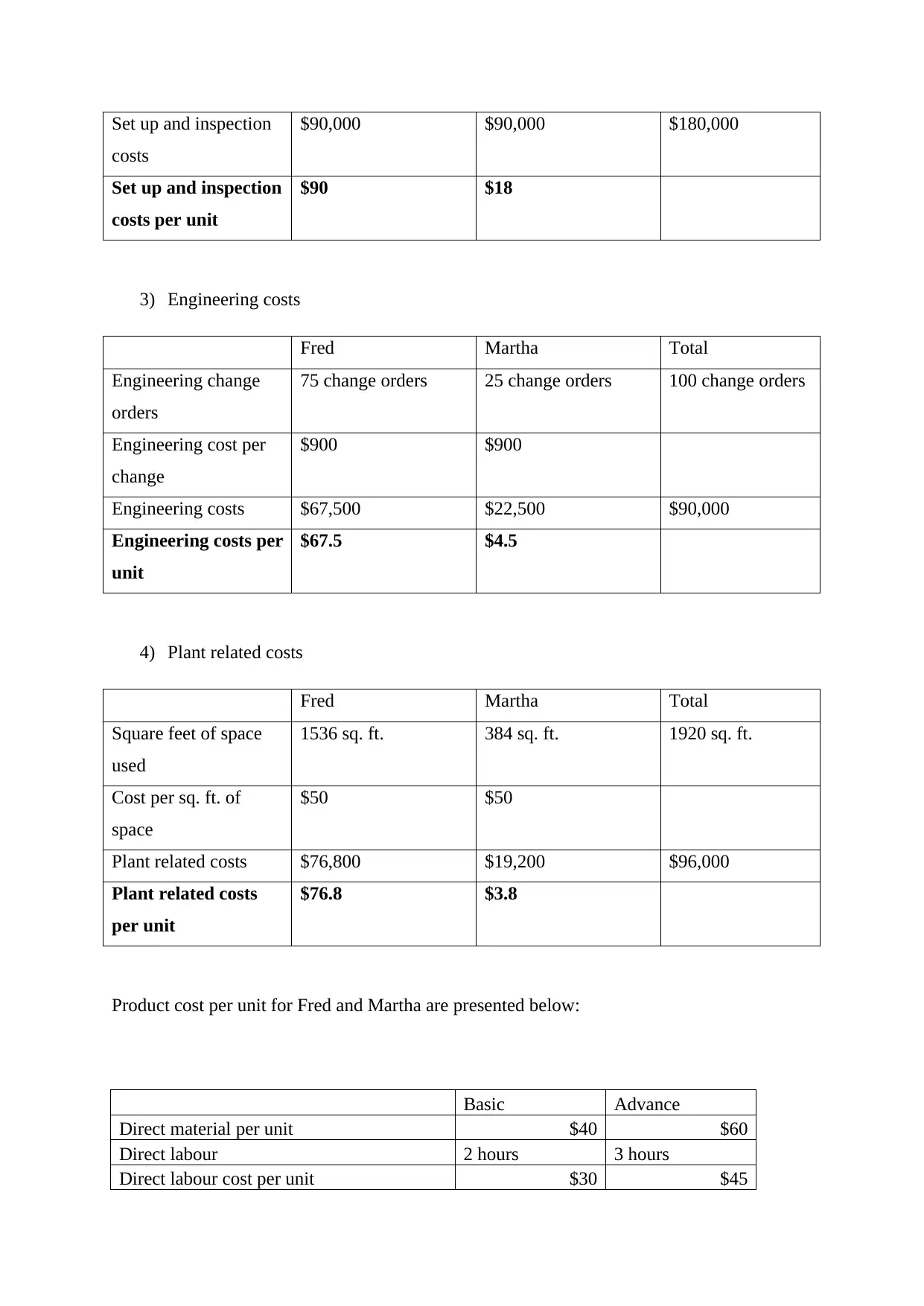

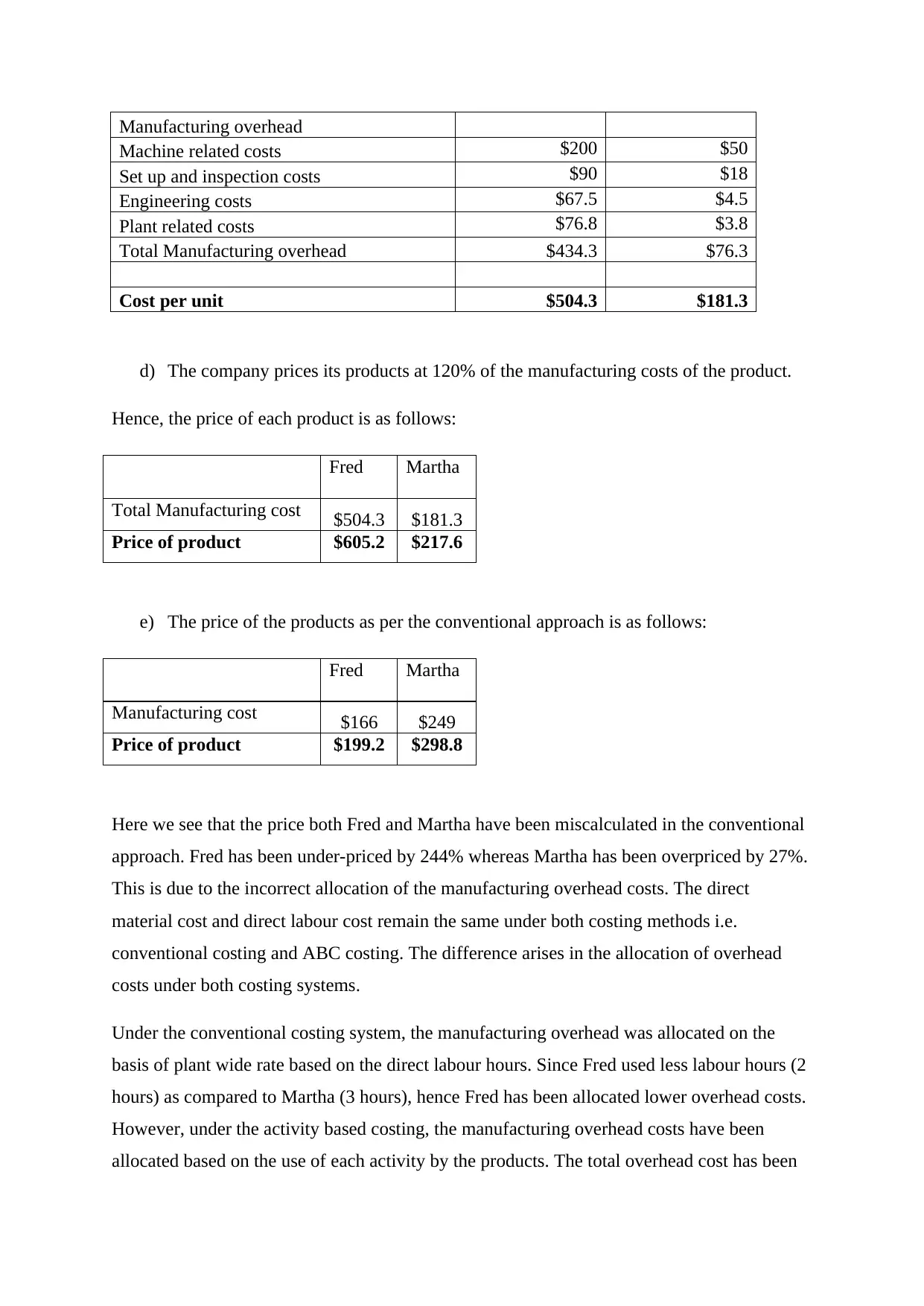

This report provides a comprehensive comparison between Activity-Based Costing (ABC) and conventional costing methods, using Jackson Ltd. as a case study. It begins by outlining the traditional approach, calculating overhead rates based on direct labor hours, and determining product costs for Fred and Martha. The analysis then transitions to ABC, detailing activity cost pools, cost drivers, and their impact on product costing. The report reveals how ABC provides a more accurate allocation of overhead costs, leading to more precise product pricing compared to the traditional method, where Fred was underpriced and Martha overpriced. It also discusses the advantages of ABC, such as improved product cost accuracy, better cost planning, and decision-making, while also acknowledging its limitations, including implementation challenges and the complexity of data gathering. The report concludes by emphasizing the benefits of ABC in today's competitive environment, advocating for its use to enhance efficiency and cost reduction, ultimately ensuring more accurate pricing decisions.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.